lehman brothers ceo energy/power conference september 6, 2007

DESCRIPTION

Lehman Brothers CEO Energy/Power Conference September 6, 2007. Energy / Growth / Leadership. Safe Harbor Provisions. - PowerPoint PPT PresentationTRANSCRIPT

Lehman Brothers

CEO Energy/Power ConferenceSeptember 6, 2007

Energy / Growth / Leadership

2

Safe Harbor Provisions

This presentation contains statements concerning NU’s expectations, plans, objectives, future financial performance and other statements that are not historical facts. These statements are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. In some cases, a listener can identify these forward-looking statements by words such as “estimate”, “expect”, “anticipate”, “intend”, “plan”, “believe”, “forecast”, “should”, “could”, and similar expressions. Forward-looking statements involve risks and uncertainties that may cause actual results or outcomes to differ materially from those included in the forward-looking statements. Factors that may cause actual results to differ materially from those included in the forward-looking statements include, but are not limited to, actions or inactions by local, state and federal regulatory bodies; competition and industry restructuring; changes in economic conditions; changes in weather patterns; changes in laws, regulations or regulatory policy; changes in levels or timing of capital expenditures; developments in legal or public policy doctrines; technological developments; changes in accounting standards and financial reporting regulations; fluctuations in the value of our remaining competitive electricity positions; actions of rating agencies; subsequent recognition, derecognition and measurement of tax positions; and other presently unknown or unforeseen factors. Other risk factors are detailed from time to time in our reports to the Securities and Exchange Commission. Any forward looking statement speaks only as of the date on which such statement is made, and we undertake no obligation to update the information contained in any forward-looking statements to reflect developments or circumstances occurring after the statement is made.

3

A Successful First 8 Months of 2007 In Meeting Our Short-Term And Long-Term Goals

Short Term

23% increase in Y-T-D regulated earnings, consistent with guidance

Rate settlements implemented at 3 of 4 utilities

LNG facility placed in service on budget, on schedule

Transmission projects on budget, on or ahead of schedule

CL&P rate case filed

Competitive business divestitures largely complete

Longer Term

Rate base growth expectations intact

Design of next generation of transmission projects advancing

Connecticut legislation offers new opportunities for customers, utilities

4

$62.7

$25.4

-$76.9

$12.1

$71.6

$37.0

$7.6 $7.4

$123.6

$0.9

($100.0)

($80.0)

($60.0)

($40.0)

($20.0)

$0.0

$20.0

$40.0

$60.0

$80.0

$100.0

$120.0

$140.0

1H 2006

1H 2007

2007 Results

Distribution and Regulated Generation

Transmission Parent/Other

In M

illio

ns

Competitive Total

14.2%

45.7%

5

$29.8

$15.4

$11.7

$27.6

$20.7

$9.4

$13.9

$5.8

$0.0

$5.0

$10.0

$15.0

$20.0

$25.0

$30.0

$35.0

1H 2006

1H 2007

Distribution/Regulated Generation Results

CL&P PSNH WMECO

In M

illio

ns

Yankee Gas

7.4%

34.4%

62.1%

18.8%

6

Transmission Earnings Tracking Rate Base Investment

$140.7

$167.5

$216.0

$141.8

$37.0

$59.8

$41.1

$28.2

$0.0

$50.0

$100.0

$150.0

$200.0

$250.0

2004 2005 2006 2007

$0.0

$10.0

$20.0

$30.0

$40.0

$50.0

$60.0

$70.0

Revenues Net Income

Rev

en

ues

in M

illio

ns N

et Inco

me

in M

illions

Six Months

7

EPS Guidance

2006 Actual Regulated/Parent $1.16

2007 Guidance $1.30 – $1.55

2006 – 201110% - 14% CAGR with higher growth in 2007 and 2008

Dist./Gen: $0.80-$0.90

Trans.: $0.50-$0.60

Competitive: modestly profitable

Parent: $0.00-$0.05

8

Rate Settlements in Place for 3 of 4 Distribution Companies

Company Rate Increase ROE Other

PSNH $46.6M on 7/1/07 in addition to $24.5M increase on 7/1/06

6.4% in 2006

9-10% projected in 2007, 2008

Transmission tracker accepted

Reliability funding

WMECO $1 M (D) – 1/1/07

$3 M (D) – 1/1/08

9.6% in 2006

9-10% projected in 2007, 2008

New trackers for pension, post- retirement benefits and certain uncollectibles and capital investment

Yankee Gas $22.1M net on 7/1/07 after $30M+ of commodity savings

5.9% in 2006

9-10% projected for 7/1/07 – 6/30/08

$108M LNG facility in Waterbury, CT, complete and reflected in rates

9

CL&P Distribution Rate Case

10/1-10/4/07

10/9-11/9/07

12/27/07

Case Filed

ConsumerCounsel

TestimonyDue

PublicHearings

EvidentiaryHearings

DecisionScheduled

Case Timeline Two annual increases requested

$189 million 1/1/08

$22 million 1/1/09

11% requested ROE

Expected 2007 ROE 7% – 7.5%

Projected average common equity in 2008 CL&P distribution company = $1 billion

Capitalization 45% equity/55% debt (rating agency methodology)

7/30/07 9/21/07

10

Reliability And Increased Costs Key Topic in CL&P Case

Need to address aging infrastructure as equipment costs have risen

$290 million in distribution cap ex annually

Pole top transformer costs are up 62% since 2003

Overhead wire cost up 80% Underground cable costs up

53% Substation transformers up

105% Tree trimming costs up 80%

11

Four Major Southwest Connecticut Projects – A $1.65 Billion Investment

More Than Half Complete

50% of CT Load

Bethel-Norwalk 345-kV underground& overhead$350 Million

21 miles 345-kV (56% underground)

10 miles 115-kV (100% underground)

Completed October 2006 at a cost of $340 million Middletown-Norwalk 345-kV

underground & overhead$1,047 Million (NU share)Glenbrook Cables

115-kV underground$183 Million

9 miles 115-kV underground

Projected in-service date: 2008

Under contract – construction under way, 36% complete at 6/30/07

Long Island Cable138-kV cross-sound$72 Million (NU share)

11 miles 138-kV submarine cable

Joint project with LIPA

Projected in-service date: 2008

41% complete at 6/30/07

69 miles 345-kV (35% underground)

57 miles 115-kV (1% underground)

Joint project with United Illuminating

Projected in-service date: 2009

38% complete at 6/30/07

COMPLETE

COMPLETE

12

Bethel-Norwalk Line Expected To Help Reduce Connecticut

Congestion Costs By $100 Million in 2007

Norwalk-Stamford Area Representative Avg Peak Hours Congestion Comparison

2006 vs 2007

0102030405060708090

100110120130140150160170180190200210220230240250

06/18/07

06/20/07

06/22/07

06/26/07

06/28/07

07/02/07

07/06/07

07/10/07

07/12/07

07/16/07

07/18/07

07/20/07

07/24/07

07/26/07

07/30/07

08/01/07

08/03/07

08/07/07

08/09/07

08/13/07

08/15/07

08/17/07

Avg

$/M

Wh

Co

ng

esti

on

(N

orw

alk

Hrb

r 1

no

de

- M

ass

Hu

b)

2006 Average 2007 Average

2007 Avg. = $11/MWh

2006 Avg. = $103/MWh

13

2007-2011 Projected Capital Expenditures

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

Distribution Capex

Transmission Capex

2006 Actual 2007 2010 20112008 2009

$908*

$779*$874*

$1,265*

$1,126*

$880*

*Excludes approximately $18 million per year at corporate service companies

In M

illio

ns

14

The Next Five Years: Transmission Capital Expenditures

$0

$100

$200

$300

$400

$500

$600

$700

$800

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Other

NEEWS

Major Southwest CT

Historic Forecast

In M

illio

ns

Up To $2.5 Billion $1,062 Million

$1.1 Billion of major SW CT projects in

2007-2011 forecast period; $1.65 billion

in total

NEEWS, Springfield projects estimated at $710 million during the

2007-2011 forecast period

15

Chicopee

LudlowHolyoke

WestSpringfield

Springfield

Agawam

9090

9191

9090

9191

Major Substation Upgrade

Overhead Line(Rebuild/Reconductor)

Underground(New/Reconductor)

Substation

Springfield 115-kV Projects

16

Springfield-115 Projects

SPRINGFIELD

HARTFORD

345-kV Substation

Generation Station

345-kV ROW

115-kV ROW

Greater SpringfieldReliability Project

Central ConnecticutReliability Project

InterstateReliability Project

The NEEWS Family of Projects Contains Four Main Elements

17

Projected Transmission Year-End Rate Base

$840

$2,117 $2,218$2,461

$140

$175

$276

$282$335

$325

$75

$80

$132

$173$208

$239

$1,512$1,173

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

2006 2007 2008 2009 2010 2011

CL&P PSNH WMECO

Transmission Rate Base2006-2011

CAGR of 23%

In M

illio

ns

*Reflects FERC approved 50% CWIP for southwest CT projects

* **

$1.1B

$1.4B

$1.9B

$2.6B$2.8B

$3.0B

18

Connecticut Legislation

2007: “An Act Concerning Electricity and Energy Efficiency” was signed by Governor Rell June 4 Generation provisions

Requires distribution companies to file plans in January 2008 to build cost of service peaking generation

Requires DPUC to allow distribution companies to buy generation put up for sale, if in the public interest

For future identified generation needs, distribution companies can submit proposals to compete with IPP developers and will serve as builders of last resort

Ratemaking Requires DPUC to decouple electric and natural gas distribution revenues from

sales volumes

Planning and incentives Institutes long-term integrated energy planning for state through utility filings with

Energy Advisory Board and DPUC Maintains one-time utility incentives created in 2005 “Energy Independence Act”

• $200/kw to host utility for customer-side generation

• $25/kw to utilities for traditional generation

19

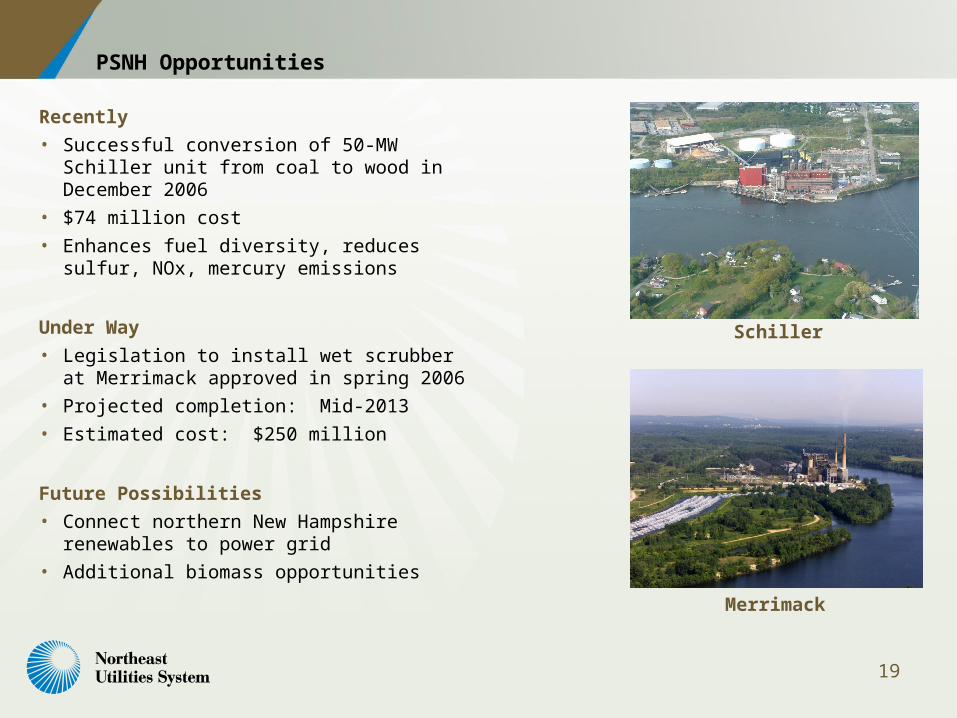

PSNH Opportunities

Recently

• Successful conversion of 50-MW Schiller unit from coal to wood in December 2006

• $74 million cost

• Enhances fuel diversity, reduces sulfur, NOx, mercury emissions

Under Way

• Legislation to install wet scrubber at Merrimack approved in spring 2006

• Projected completion: Mid-2013

• Estimated cost: $250 million

Future Possibilities

• Connect northern New Hampshire renewables to power grid

• Additional biomass opportunities

Schiller

Merrimack

20

Ability To Finance Growth

$3,307

$116

$2,823

Total Debt Preferred Stock Common Equity

6/30/07

Strong balance sheet

Strong cash and liquidity position

Strong access to capital

Approximately $400 million of NU parent cash

Nearly $1 billion unused bank, accounts receivable lines

Solid credit ratings at parent, subsidiaries

Successful debt financings

Minimal equity requirements

21

NU’s Transformation Producing Solid Results, Prospects

Financial performance consistent with projections Transmission business is growing rapidly to meet customer

needs Distribution results improving as reasonable rate case outcomes

are implemented Additional infrastructure needs being identified Financial flexibility to finance the growth Attractive total shareholder return profile