lecture 1 introduction-to_audit_and_assurance

TRANSCRIPT

Lecture 1-Part I

Introduction to Auditing and Assurance Services

1

Learning Outcomes

• Describe auditing• Distinguish between auditing and

accounting• Describe different types of audit.• Explain why there is a need for auditing

and assurance services• Explain the framework of auditing• Describe the requirements for becoming a

Chartered Accountant2

Auditing

• Auditing is a systematic process of objectively obtaining and evaluating evidence regarding assertions on economic actions and events, to ascertain the degree of correspondence between those assertions, and established criteria and communicating the results to interested users.

3

Audit of Financial Statement

Auditing of financial statement is a type of assurance engagement.

The objective of an audit of Financial Statements is “ to enable the auditor to express an opinion whether the financial statements are prepared in all material respects,in accordance with identified financial reporting framework”(ISA 200)

4

Opinion and Reasonable Assurance

• Reasonable assurance as opposed to Absolute assurance (Guarantee)

4 reasons:

1)Use of testing

2)Inherent Limitation of Internal Control

3)Audit Evidence is Persuasive and Not Conclusive

4)Use Of Judgement5

Benefits of Financial statements audit

• Obtain access to capital markets. Without an audit, companies may be denied access to capital markets by the SC and Bursa Malaysia

• Have a lower cost of capital. Given the reduced risk resulting from audited financial reports, potential creditors may offer low interest rates and potential investors may be willing to accept a lower rate of return on their investment.

• Be a deterrent to inefficiency and fraud. Knowledge that an independent audit is to be performed is likely to result in fewer errors in the accounting process and reduce the likelihood of employee misappropriation of assets.

• Control and operational improvements. Based on observations made during the financial report audit, the independent auditor can suggest how controls could be improved and how greater operating efficiencies within the entity’s organisation may be achieved.

6

Distinguish BetweenAuditing and Accounting

• Accounting is the recording, classifying,and summarizing of economic eventsfor the purpose of providing financialinformation used in decision making.• Auditing is determining whetherrecorded information properlyreflects the economic events thatoccurred during the accounting period

7

Limitation of external auditThe main limitations are as follows.• Time lapse – by the time the audit report is released the information

is relatively ‘old’.• Audit testing on selective samples, which has limitations due to

sampling risk.• The assessment of materiality, with both quantitative and qualitative

considerations, requires a high degree of professional judgement. There are, however, some guidelines, although by their nature are necessarily arbitrary.

• Forming professional judgements in highly specialised areas Can often result in disagreements between auditors and clients

• Report format limitations and the consequent “expectation gap” often arises with users of financial statements.

8

9

• Early audits focused on finding errors in balance sheet accounts, due to concerns about management fraud

• Auditors now face an increasing demand for more accountability and more perceived benefits for users of financial information

• An audit enhances credibility, integrity and usefulness of financial information

Development of nature and scope of auditing and assurance services

9

10

The principal–agent relationship

• Shareholders (principals) employ directors and managers (agents) to conduct the business, in the interest of the owners

• This often results in information asymmetry

• The managers assume a stewardship function and are expected to manage the business in the best interest of the principals

(Refer to page 4 of Margaret Boh 3rd ed)10

11

Auditing — a shifting paradigm

• From 2000, a series of corporate failures, most of which related to accounting misstatements, internal control problems and the apparent failure of the auditors, caused a major credibility crisis in the accounting and auditing profession

• A spate of radical reforms undertaken by the profession and regulators has since followed

11

12

Accounting crises and corporate collapses

• The major corporate collapses of Enron and HIH Insurance have reshaped the auditing profession

• Enron, an energy giant in the United States, collapsed in October 2001

• HIH Insurance, the leading Australian general insurance group, was placed into liquidation in March 2001 12

Relationships Among Auditors, Client, and External Users

AuditorAuditor

Client ExternalExternalUsersUsers

Client or auditcommittee hires

auditor

Auditor issuesreport relied

upon by users to reduce information risk

Provides capital

Client provides financial statements to users

13

Certified Public Accounting Firms

• The four largest CPA firms in the United States are called the “Big Four” international CPA firms.

• These four firms have offices in most major cities in the United States and in many cities throughout the world.

14

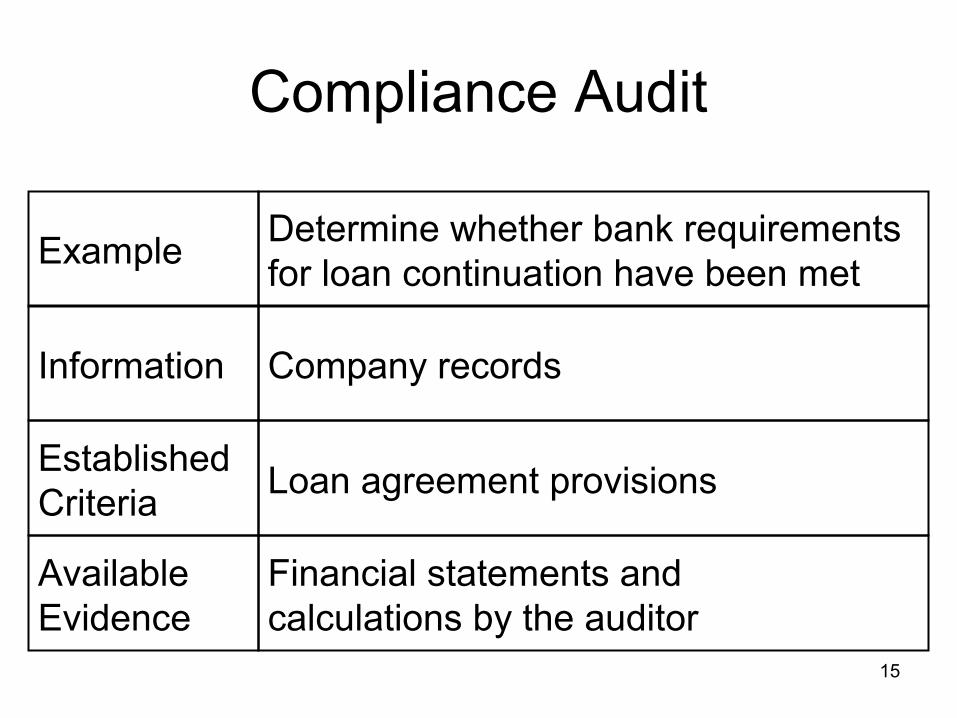

Compliance Audit

ExampleDetermine whether bank requirementsfor loan continuation have been met

Information Company records

EstablishedCriteria

Loan agreement provisions

AvailableEvidence

Financial statements andcalculations by the auditor

15

Audit of Historical Financial Statements

ExampleAnnual audit of Boeing’s financialstatements

Information Boeing's financial statements

EstablishedCriteria

Generally accepted accountingprinciples

AvailableEvidence

Documents, records, and outsidesources of evidence

16

The need for company auditor

• The appointment of an auditor is also required by sec 172 of the CA, which states that every company incorporated under the CA must appoint an auditor and have the company's accounts audited before presenting the accounts to the shareholders at the Annual General Meeting.

17

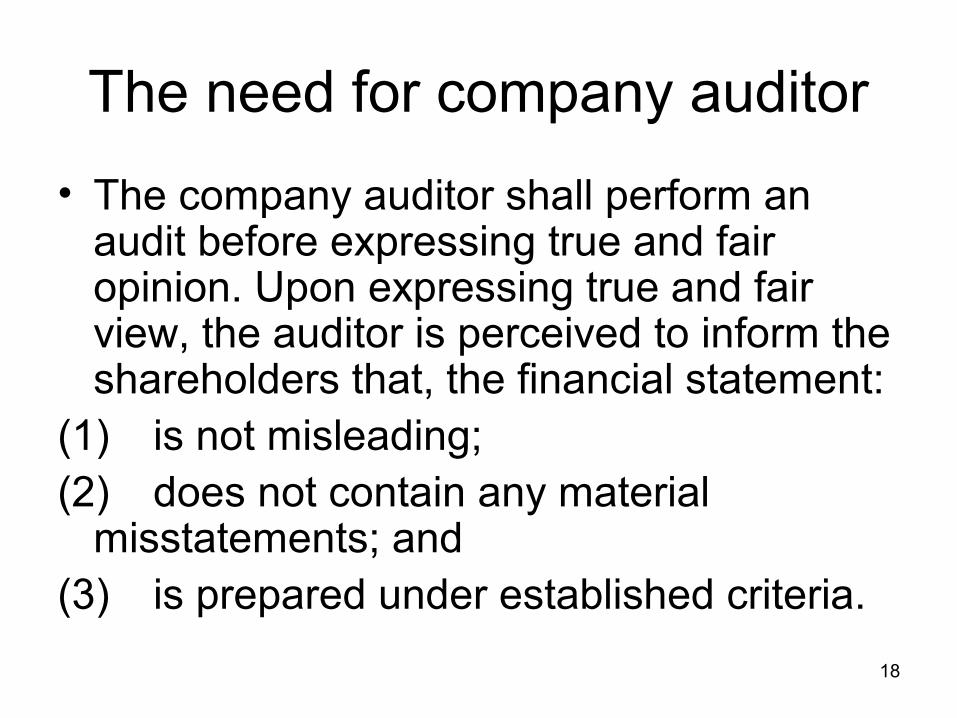

The need for company auditor

• The company auditor shall perform an audit before expressing true and fair opinion. Upon expressing true and fair view, the auditor is perceived to inform the shareholders that, the financial statement:

(1) is not misleading;(2) does not contain any material

misstatements; and(3) is prepared under established criteria.

18

Audited items

(1) Balance sheet;(2) Income statement;(3) Cash flow statement;(4) Statement of changes of equity;(5) Notes to the financial statement;(6) Accounting system;(7) Internal control system; and(8) Relevant documentations.

19

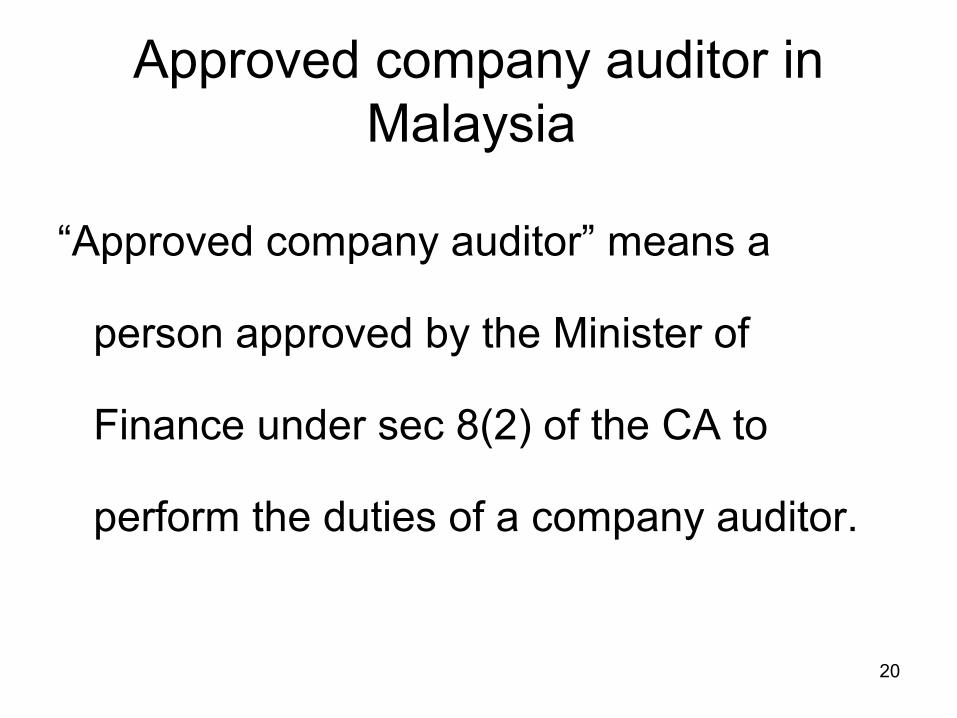

Approved company auditor in Malaysia

“Approved company auditor” means a

person approved by the Minister of

Finance under sec 8(2) of the CA to

perform the duties of a company auditor.

20

Post Enron and Worldcom

The work of 2 senators in US

Paul Sarbanes and Michael Oxley

In 2002, Sarbanes Oxley Act 2002 was passed. (SOX)

21

End of Lecture