latest market review - sep 2016 pdf

TRANSCRIPT

The Office

Singapore September 2016

Overview

The Singapore office leasing market has remained challenging, but by no means inactive despite fickle demand. There has been a flurry of activity involving larger space users committing on space in the new schemes but the net absorption has been minimal. The leasing market continues to be fragile with many landlords managing to convince their tenants to stay by lowering renewal rates still further. Some of the big moves came as no surprise with Bank of Tokyo Mitsubishi (150,000 sq ft Marina One), Mitsui and Co. (80,000 sq ft Asia Square) and PwC (180,000 sq ft Marina One East Tower) all having been in their current buildings (Republic Plaza, 80 Robinson Road and PWC Building respectively) for over 15 years. The time is ripe for many other large space users to upgrade/right size and there are quite a few players in this category who will be aware that opportunities to move into new schemes after 2018 will be more limited.

Rentals Rates continue to soften but at a slower rate than witnessed in Q4 2015/ Q1 2016 and are already 20% off their peak in March 2015. However the full impact of the major voids that will appear next year, as a result of relocations, has not filtered through yet and we expect more severe triage come 2017.The most expensive office buildings are now commanding effective rates between $10.50- $11.00 per sq ft for the smaller units but larger space users, focusing on the new schemes are targeting average effective rents between $8.00 and $9.00 per sq ft. The Tanjong Pagar area still offers the best value for money, with many quality options available between $6.25 and $7.50 per sq ft.

Market Forecast Rates are expected to soften for at least another 2 years and may begin to bottom out at the end of 2017 / early 2018. Within the next two years there will still be more high quality schemes coming stream including Frasers Tower (approx. 690,000 sq ft) and Robinson Tower (approx. 200,000 sq ft) within the Financial District as well as Paya Lebar Quarter (approx. 1,000,000 sq ft) outside the CBD. This will ensure Singapore office market will remain very competitive compared to other financial hubs in the region, as well as continuing to attract new enterprises and expansion of regional offices here.

Over the next 12 months we expect rates to fall by around 10% but the rate of decline could begin to slow by the end of next year.

REFER AND EARN

Do you know someone looking for office space?$$ Big cash rewards for successful leads 15% of our commission Total confidentiality assured

Please contact us for full details.

Marina One

Singapore | Hong Kong

Market Forecast Rates are expected to continue to soften for at least another 2 years

Corporate Locations (S) Pte Ltd License No. L3010044A

T +65 6320 8355 / [email protected] / www.corporatelocations.com.sg

A review of the Singapore office market

Supply Continues to be very healthy for tenants with ample choice in all locations

The supply situation continues to be very healthy for tenants with ample choice in all locations, covering a wide variety of buildings, so there should be something for everyone. Most of the shadow space has either been leased out or the leases for fallen in/expired, so no longer sublease space. All the new schemes have been active and they still have a wide choice of units to pick from. However, Marina One is more suited to the larger space users over 9,000 sq ft, whereas Guoco Tower can be more flexible and cater for sizes from 3,000 sq ft upwards. Duo Tower on Beach Road has been slow in the market

but the rental rates have been adjusted recently to be more competitive and should attract renewed interest soon.

Rental rates in Duo Tower have been adjusted recently to be more competitive

In Raffles Place the buildings with the widest choice of units include One Raffles Place Towers 1 & 2, Bank of Singapore Centre, 20 Collyer Quay and One George Street. Next year, significant space will be coming available in Republic Plaza. In the New Downtown area, MBFC Towers 1 & 2 are

full and there is only limited space in Tower 3. One Raffles Quay North Tower is nearly full but South Tower still has the ex- Royal Bank of Scotland space available. There is plenty of space available in Asia Square and of course Marina One will soon be ready to take in tenants. In Shenton Way / Robinson Road, OUE Downtown 2, and Robinson 77 have the most space available and next year 80 Robinson Road will have a large void to fill after Mitsui & Co move out and 5 Shenton Way will be coming on stream in Q1 2017.

In Tanjong Pagar, AXA Tower still has a

substantial amount of space available. Elsewhere, Fuji Xerox Tower has a large variety of small units available but it is Keppel Towers and Tower Fifteen that have the most space on offer, although their long term future remains uncertain. In Beach Road / Marina Bay / City area, Suntec City is enjoying a relatively high occupancy rate and Millennia Tower is nearly full. However there is significant space in Centennial Tower and on Beach Road there are a variety of buildings with good space available including Beach Centre, The Concourse and The Gateway East, all of whom will be competing with Duo Tower in this district.

Raffles Place / Marina Bay

6 Battery Road $14.0020 Collyer Quay $10.00 - $12.0055 Market Street FullAsia Square Tower 1 $12.00 - $13.00Asia Square Tower 2 $12.00 - $13.00Bank of China Building FullBharat Building $6.50Bank of Singapore Centre $9.50CapitaGreen $13.00Chevron House $9.00Clifford Centre $8.50Income@Raffles $9.00Maybank Tower $11.00MBFC Tower 1, 2 & 3 $13.00OCBC Centre $9.60OCBC Centre East $8.50Ocean Financial Centre $11.50One Finlayson Green $8.50One George Street $10.50One Raffles Place Tower 1 $8.00 - $9.90One Raffles Place Tower 2 $9.50 - $9.90One Raffles Quay North Tower $11.00 - $12.00OUE Bayfront $11.00 - $13.00RB Capital Building $8.50Republic Plaza 1 $10.00 - $11.00Republic Plaza 2 $8.80Royal Group Building $9.50Royal One Phillip $8.50Singapore Land Tower $11.00Straits Trading Building FullThe Arcade $7.30UOB Plaza 1 $10.50UOB Plaza 2 $10.50 Robinson Road / Shenton Way

4 Robinson Road $6.906 Raffles Quay $7.80+71 Robinson Road Full80 Robinson Road $8.50 120 Robinson Road $7.00135 Cecil Street $7.00137 Telok Ayer Street $7.00146 Robinson Road $5.50+150 Cecil Street $6.30

158 Cecil Street $8.20AIA Tower FullASO Building FullBangkok Bank Building FullBEA Building $7.15Capital Square $TBCCapital Tower $9.50Cecil Court $6.50China Square Central $8.50City House $8.00Far East Finance Building $5.50+Far Eastern Bank Building $6.50Finexis Building $7.00GB Building $6.00+Grace Global Raffles $8.50Great Eastern Centre $9.50Hong Leong Building $9.00Keck Seng Tower $5.50+ PIL Building FullPWC Building $9.50Prudential Tower $9.50Robinson 77 $8.00Robinson 112 $6.50Robinson Centre $8.50Robinson Point $8.50Samsung Hub $9.50+SGX Centre 1 & 2 $8.50SIF Building $8.50Shenton House $5.50The Globe $6.60The Octagon $6.50Tokio Marine Centre $7.00Tong Eng Building $5.50+ Tanjong Pagar

78 Shenton Way $7.8079 Anson Road $7.00+ABI Plaza $6.50Amara Corporate Tower $7.00+Anson Centre $5.30Anson House $7.00+AXA Tower $8.50Fuji Xerox Towers $7.50Guoco Tower $11.00Hub Synergy Point $5.00International Plaza $6.50Jit Poh Building $6.50Keppel Towers $7.00Mapletree Anson $8.50MAS Building FullSt. Andrew’s Centre FullSouthpoint $7.00Tower Fifteen $7.00Twenty Anson $9.00

RENTAL GUIDESummary of Asking Rates

* Business Park / B1 space

City Hall / Marina Centre / Beach Road

11 Beach Road $6.2030 Hill Street $8.50Bugis Junction Towers $8.20Centennial Tower $12.50Beach Centre $7.80Duo Tower $9.00Millenia Tower $12.50Odeon Tower $8.50OG Albert Complex $5.50Parkview Square $8.00Peninsula Plaza $5.80Raffles City Tower $11.00Shaw Tower $6.00South Beach Tower $10.00Stamford Court $7.50Suntec Towers 1-5 $9.00The Adelphi $7.00The Concourse $7.50The Gateway East and West $8.00 Orchard Road / Dhoby Ghaut

50 Scotts Road Full51 Cuppage Road $7.50182 Clemenceau Ave TBCBurlington Square $6.00Faber House $8.00Fortune Centre $5.20Forum $8.00Goldbell Towers $8.50Haw Par Centre $7.00Haw Par Glass Tower $4.80International Building $8.50Liat Towers $8.50Manulife Centre $8.00Ngee Ann City $10.50Orchard Building $8.50Orchard Gateway $9.00Orchard Towers $4.00Palais Renaissance $8.90Regency House $7.20Shaw Centre $8.00Shaw House $9.00Singapore Pools Building FullSunshine Plaza $6.00Tanglin Shopping Centre $6.20The Bencoolen $6.50The Heeren $11.00Thong Teck Building FullTong Building FullTripleOne Somerset $9.00VisionCrest Commercial $9.00Wheelock Place $12.00Wilkie Edge $7.00Winsland House 1 $10.50Winsland House 2 $10.50Wisma Atria $10.50

Chinatown / River Valley Road

CES Centre $5.50Central Mall $7.00Chinatown Point TBCGreat World City $7.00King’s Centre $6.50The Central $8.00UE Square $7.50Valley Point $7.00 Edge of CBD

Alfa Centre FullAperia* $6.80Boon Siew Building FullCentral Plaza $7.50Goldhill Plaza $6.00Newton 200 $9.00Novena Square $8.50Rex House FullSLF Building $5.00+United Square $7.50 West / Others

Alexandra Point $7.00Alexandra Techno Park* $4.30Fragrance Empire Building $6.00Harbourfront Centre $6.90Harbourfront Tower 1 $7.50Harbourfront Tower 2 $6.90International Business Park (Jurong)* $4.00JEM @ Jurong Gateway $5.90Keppel Bay Tower $7.50Mapletree Business City* $6.50 Pacific Tech Centre* $3.55PSA Building $7.20PSA Vista $4.50Singapore Science Parks* $4.50+The JTC Summit $4.65Westgate $6.50 East

Abacus Plaza FullAIA Tampines FullChangi Business Park* $4.50CPF Tampines Building $4.90NTUC Tampines Junction $5.50NTUC Tampines Point $5.50Parkway Parade $6.00Singapore Post Centre $6.50Tampines Concourse $5.20Tampines Grande $5.50Tampines Plaza $5.50Viva Business Park $3.00 - 3.50

All rents quoted are asking rental rates and subject to change without prior notice

Development Location Estimated Size Completion Date

Beach Centre Beach Rod 90,000 sq ft June 2016SBF Centre Robinson Road 250,000 sq ft July 2016Guoco Tower Tanjong Pagar 900,000 sq ft August 2016Crown@Robinson Robinson Road 68,000 sq ft September 2016Duo Tower Beach Road 568,000 sq ft October 2016GSH Plaza Cecil Street 250,000 sq ft December 2016Marina One New Downtown 1,800,000 sq ft December 2016Vision Exchange Jurong East 475,000 sq ft January 20175 Shenton Way / UIC Shenton Way 276,000 sq ft March 2017Oxley Tower Robinson Road 130,000 sq ft June 2017Frasers Tower Cecil Street 690,000 sq ft December 2017Robinson Tower Robinson Road 195,000 sq ft March 2018Paya Lebar Quarter Paya Lebar 1,000,000 sq ft June 2018Woodlands Square Woodlands 630,000 sq ft TBC

Future Office Developments 2016 - 2018

GSH Plaza Robinson Tower

Summary of New Schemes 03

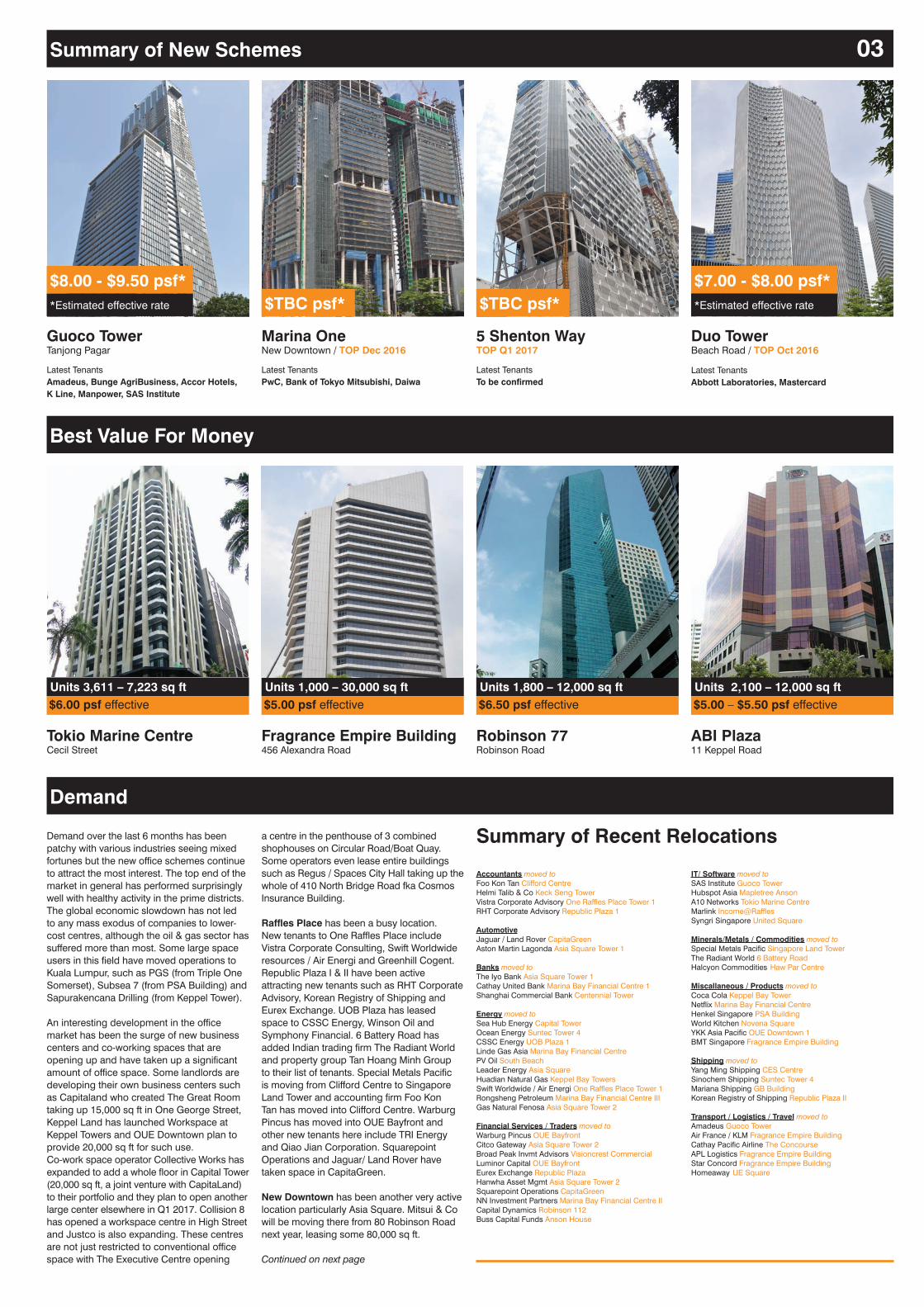

Units 3,611 – 7,223 sq ft $6.00 psf effective Tokio Marine Centre Cecil Street

Units 1,000 – 30,000 sq ft $5.00 psf effective Fragrance Empire Building 456 Alexandra Road

Units 1,800 – 12,000 sq ft $10.00 – $6.50 psf effective Robinson 77 Robinson Road

Units 2,100 – 12,000 sq ft $5.00 – $5.50 psf effective ABI Plaza 11 Keppel Road

Demand

Demand over the last 6 months has been patchy with various industries seeing mixed fortunes but the new office schemes continue to attract the most interest. The top end of the market in general has performed surprisingly well with healthy activity in the prime districts. The global economic slowdown has not led to any mass exodus of companies to lower-cost centres, although the oil & gas sector has suffered more than most. Some large space users in this field have moved operations to Kuala Lumpur, such as PGS (from Triple One Somerset), Subsea 7 (from PSA Building) and Sapurakencana Drilling (from Keppel Tower).

An interesting development in the office market has been the surge of new business centers and co-working spaces that are opening up and have taken up a significant amount of office space. Some landlords are developing their own business centers such as Capitaland who created The Great Room taking up 15,000 sq ft in One George Street, Keppel Land has launched Workspace at Keppel Towers and OUE Downtown plan to provide 20,000 sq ft for such use. Co-work space operator Collective Works has expanded to add a whole floor in Capital Tower (20,000 sq ft, a joint venture with CapitaLand) to their portfolio and they plan to open another large center elsewhere in Q1 2017. Collision 8 has opened a workspace centre in High Street and Justco is also expanding. These centres are not just restricted to conventional office space with The Executive Centre opening

a centre in the penthouse of 3 combined shophouses on Circular Road/Boat Quay. Some operators even lease entire buildings such as Regus / Spaces City Hall taking up the whole of 410 North Bridge Road fka Cosmos Insurance Building.

Raffles Place has been a busy location. New tenants to One Raffles Place include Vistra Corporate Consulting, Swift Worldwide resources / Air Energi and Greenhill Cogent. Republic Plaza I & II have been active attracting new tenants such as RHT Corporate Advisory, Korean Registry of Shipping and Eurex Exchange. UOB Plaza has leased space to CSSC Energy, Winson Oil and Symphony Financial. 6 Battery Road has added Indian trading firm The Radiant World and property group Tan Hoang Minh Group to their list of tenants. Special Metals Pacific is moving from Clifford Centre to Singapore Land Tower and accounting firm Foo Kon Tan has moved into Clifford Centre. Warburg Pincus has moved into OUE Bayfront and other new tenants here include TRI Energy and Qiao Jian Corporation. Squarepoint Operations and Jaguar/ Land Rover have taken space in CapitaGreen.

New Downtown has been another very active location particularly Asia Square. Mitsui & Co will be moving there from 80 Robinson Road next year, leasing some 80,000 sq ft. Continued on next page

Marina One New Downtown / TOP Dec 2016

5 Shenton Way TOP Q1 2017

Duo Tower Beach Road / TOP Oct 2016

Guoco Tower Tanjong Pagar

Latest Tenants Amadeus, Bunge AgriBusiness, Accor Hotels, K Line, Manpower, SAS Institute

Latest Tenants PwC, Bank of Tokyo Mitsubishi, Daiwa

Latest Tenants To be confirmed

Latest Tenants Abbott Laboratories, Mastercard

*Estimated effective rate

$8.00 - $9.50 psf*$TBC psf* $TBC psf*

Summary of Recent Relocations

Accountants moved toFoo Kon Tan Clifford CentreHelmi Talib & Co Keck Seng TowerVistra Corporate Advisory One Raffles Place Tower 1RHT Corporate Advisory Republic Plaza 1

AutomotiveJaguar / Land Rover CapitaGreenAston Martin Lagonda Asia Square Tower 1

Banks moved toThe Iyo Bank Asia Square Tower 1Cathay United Bank Marina Bay Financial Centre 1Shanghai Commercial Bank Centennial Tower

Energy moved toSea Hub Energy Capital Tower Ocean Energy Suntec Tower 4CSSC Energy UOB Plaza 1Linde Gas Asia Marina Bay Financial CentrePV Oil South BeachLeader Energy Asia SquareHuadian Natural Gas Keppel Bay TowersSwift Worldwide / Air Energi One Raffles Place Tower 1Rongsheng Petroleum Marina Bay Financial Centre IIIGas Natural Fenosa Asia Square Tower 2

Financial Services / Traders moved toWarburg Pincus OUE BayfrontCitco Gateway Asia Square Tower 2Broad Peak Invmt Advisors Visioncrest CommercialLuminor Capital OUE BayfrontEurex Exchange Republic PlazaHanwha Asset Mgmt Asia Square Tower 2Squarepoint Operations CapitaGreenNN Investment Partners Marina Bay Financial Centre IICapital Dynamics Robinson 112Buss Capital Funds Anson House

IT/ Software moved toSAS Institute Guoco TowerHubspot Asia Mapletree AnsonA10 Networks Tokio Marine CentreMarlink Income@RafflesSyngri Singapore United Square

Minerals/Metals / Commodities moved toSpecial Metals Pacific Singapore Land TowerThe Radiant World 6 Battery RoadHalcyon Commodities Haw Par Centre

Miscallaneous / Products moved toCoca Cola Keppel Bay TowerNetflix Marina Bay Financial CentreHenkel Singapore PSA BuildingWorld Kitchen Novena SquareYKK Asia Pacific OUE Downtown 1 BMT Singapore Fragrance Empire Building

Shipping moved toYang Ming Shipping CES CentreSinochem Shipping Suntec Tower 4 Mariana Shipping GB BuildingKorean Registry of Shipping Republic Plaza II Transport / Logistics / Travel moved toAmadeus Guoco Tower Air France / KLM Fragrance Empire BuildingCathay Pacific Airline The ConcourseAPL Logistics Fragrance Empire BuildingStar Concord Fragrance Empire BuildingHomeaway UE Square

*Estimated effective rate

$7.00 - $8.00 psf*

Best Value For Money

T +65 6320 8355www.corporatelocations.com.sg

Request a ListingGet bottom line effective rates on all buildings

Disclaimer The information in this publication should be regarded as a general guide only. Whilst every care is taken in it preparation, no representation is made or responsibility accepted for its accuracy or completeness. The rentals mentioned are neither asking rentals nor rentals agreed by property owners, but only represent the writers views on estimated rentals and is intended as reference only.

Demand cont.

Douglas Dunkerley Director CEA Reg No. R030779G

T +65 6391 5200 [email protected]

Edmund Goh Director CEA Reg No. R030777J

T +65 6391 5201 [email protected]

Darren Ng Associate Director CEA Reg No. R022103E

T +65 6391 5209 [email protected]

John Lee Commercial Agency Manager CEA Reg No. R016701D

T +65 6391 5211 [email protected]

Air France / KLM Cargo Fragrance Empire BuildingBechtel Shaw TowerCity Gas PSA BuildingKorean Registry of Shipping Republic Plaza IIM.P. Silva Asia SquareNMG Financial Services 30 Hill StreetPropex Singapore SGX CentreOHL - Obrascon Huate Lain The ConcourseSea Hub Energy Capital TowerSky Premium One Raffles PlaceSoftbank Telecom 78 Shenton WaySymphony Financial UOB Plaza IITeekay Shipping PSA BuildingWorld Kitchen Novena SquareYang Ming Shipping CES Centre

Reinstatement Costs Tenants should note that reinstatement costs (to strip out everything a tenant puts in), depends upon the quality of the building and building management requirements, as well as the extent of works the tenant undertook at the beginning.

Fitting Out Costs

Guide To Basic Fitting Out Costs Economy Mid-Range Premium

Lease Capital Expenditure Per sq ft Per sq ft Per sq ftFixtures & Fittings and Finishes $19 $24 $33Carpets / Floor finishes $3 $4 $7Wall finishes $2 $3 $6Ceiling finishes $3 $4 $5Partitions (glass or gypsum board) $7 $8 $9Doors, Frames & Ironmongery $4 $5 $6

Furniture $13 $24 $36Custom and system furnitureF & F including filing and storage cabinetsConference table and presentation cabinetPantry and equipment cabinets

M & E Services $13 $16 $19Electrical Works & NetworkingFire Protection SystemAir-conditioning Works

Miscellaneous $5 $6 $7SignagePlumbing WorksGraphics / Blinds / Features (plants, artwork etc)

General Services $5 $5 $5Insurance & PreliminariesConsultancy Fees: Architect / M & E / Structural

GRAND TOTAL $55 $75 $100

As a general rule of thumb, most businesses allow between 125 sq ft and 200 sq ft (net) per person, depending upon the overall headcount, culture of the company (open plan or many enclosed offices), and the need for amenities eg. break out rooms, pantry, library and storage.

Breakdown By Function

Description Size (sq ft) ReceptionReceptionist plus waiting area – for 2 to 4 people 125-200Receptionist plus waiting area – for 6 to 8 people 200-300

Chairman’s office 250-400Managing director/ vice president 175-200Executive’s office 100-150Open plan workstation – manager 100-120Open plan workstation – clerical 70-100

Conference room - theatre style 15 sq ft per personConference room - conference seating 25-30 sq ft per person

Clerical pool areas 80-100 sq ft per person Lunch room/break out area 15 sq ft per personCorridor space 20%-30% of totalWater cooler 1 unit per 75 staff

The figures on this page are a general guide only and we recommend all tenants contact any designer in our list of useful contacts and most will provide free advice on space planning to meet your specific needs.

Business Category

sq ft net per employee Size (sq ft)

Corporate headquarters 200+Banking, financial 150-180Business services, general commercial 110-140Trading, manufacturing, sales, insurance 80-120

Morgan McKinley – One Raffles Place Helm – The Concourse

Citco Gateway, Aston Martin Lagonda, Leader Energy, CFLD Investment and Gas Natural Fenosa are all new tenants to this scheme. A wide variety of smaller units here that were given up by Lloyds of London were quickly snapped up by companies such as PAG Investment Advisors, Zedra Trust Company, Trilliant Holdings Inc, Milken Institute Asia and The Iyo Bank. Marina Bay Financial Centre has also been busy, with Cathay United Bank, Netflix, NN Investment, Linde Gas Asia and Rongsheng Petrochemical all moving in. The leasing of Marina One is now in full swing and already over 500,000 sq ft in this scheme has been committed with Daiwa Singapore, PwC

and Bank of Toyko Mitsubishi being the first major tenants.

Tanjong Pagar / Shenton Way remains one of the most competitive locations and Guoco Tower offers the best combination of quality and value for money. New tenants to secure space in this scheme include Amadeus – 36,000 sq ft (from Parkview Square), SAS Institute (moving from Twenty Anson) and Prudential Assurance is rumoured to be lined up to secure 90,000 sq ft in this developement. Hubspot and Taiyo International have taken space in Mapletree Anson and Twenty Anson respectively.

Mariana Shipping has taken a floor into GB Building, A10 Networks lease space in Tokio Marine Centre and YKK Asia Pacific has leased a floor in OUE Downtown 1.

Orchard Road has been relatively quiet because of lack of supply. Halycon Agri Commodities has moved into Haw Par Centre from Raffles City Tower and Broad Peak Investment Advisors moved into Visioncrest Commercial. Beach Road / Marina Bay has also been relatively subdued. Edelman Public Relations has leased space in Beach Centre. PV Oil has moved from Winsland House to South Beach Tower. New tenants to Suntec

City include Sinochem Shipping, Ocean Energy and Third Rock Issea Advisers and many of Suntec’s tenants have expanded within the scheme.

Outside the CBD the Harbourfront / Alexandra Road area has been the most active. Coca Cola has leased 13,000 sq ft in Keppel Bay Tower and Huadian Natural Gas has also leased space here. Fragrance Empire Building has proved popular with logistic companies and new tenants here include Air France / KLM Cargo, APL Logistics, Star Concord and well as engineering design firm BMT Asia.

Space Planning Guide

04

Recent Clients in 2016