klöckner & co - q2 2011 results

TRANSCRIPT

Klöckner & Co SEKlöckner & Co SEA Leading Multi Metal Distributor

Q2 2011 resultsGisbert RühlCEO/CFO Analysts’ and Investors’ Conference CallCEO/CFO

August 10, 2011

Ein- bis zweizeiliger Folientitel00 Disclaimer

This presentation contains forward-looking statements which reflect the current views of the management of Klöckner & Co SE with respect to future events. They generally are designated by the words “expect”, “assume”, “presume”, “intend”, “estimate”, “strive for”, “aim for”, “plan”, “will”, “strive”, “outlook” and comparable expressions and generally contain information that relates to expectations or goals for economic conditions, sales proceeds or other yardsticks for the success of the enterprise. Forward-looking statements are based on currently valid plans, estimates and expectations. You therefore should view them with caution. Such statements are subject to risks and factors of uncertainty, most of which are difficult to assess and which generally are outside of the control of Klöckner & Co SE. The relevant factors include the effects of significant strategic and operational initiatives, including the acquisition or disposition of companies. If these or other risks and factors of uncertainty occur or if the assumptions on which the statements are based turn out to be incorrect, the actual results of Klöckner & Co SE can deviate significantly from those that are expressed or implied in these statements. Klöckner & Co SE cannot give any guarantee that the expectations or goals will be attained. Klöckner & Co SE – notwithstanding existing obligations under laws pertaining to capital markets – rejects any responsibility for updating the forward-looking statements through taking into consideration new information or future events or other things.

In addition to the key data prepared in accordance with International Financial Reporting Standards, Klöckner & Co SE is presenting non-GAAP key data such as EBITDA, EBIT, Net Working Capital and net financial liabilities that are not a component of the accounting regulations. These key data are to be viewed as supplementary to, but not as a substitute for data prepared in accordance with International Financial Reporting Standards Non-GAAP key datasubstitute for data prepared in accordance with International Financial Reporting Standards. Non-GAAP key data are not subject to IFRS or any other generally applicable accounting regulations. Other companies may base these concepts upon other definitions.

2

Agenda

01 Recent developments, financials and performance Q2 2011

02 Market environment

03 Outlook

04 Appendix04 Appendix

3

01 Highlights Q2

• Challenging quarter due to unexpectedly strong price pressure in all markets leading to an

EBITDA f €62 (3 3% i ) ti l i t d b ff f €10 (3 8% dj t dEBITDA of €62m (3.3% margin), negatively impacted by one offs of €10m (3.8% adjusted

margin)

• Sales volumes increased organically less than typical seasonally due to prebuying effect in• Sales volumes increased organically less than typical seasonally due to prebuying effect in

Q1 rolling over and a cautious stance of customers in Q2

• Consolidation of Macsteel and Frefer completed• Consolidation of Macsteel and Frefer completed

• Integration of Macsteel and Namasco in the US progressing, synergies higher than initially

expectedexpected

• Principle agreement to terminate the earn-out for Macsteel will lead to reduced purchase

price by USD60m and earlier realization of synergy effectsprice by USD60m and earlier realization of synergy effects

• Capital increase with net proceeds of €517m provides strong backing for

Klöckner & Co 2020

4

01 Steel imports caused pressure in all markets

• Orders to the US were placed during Q1 when the spread

US imports of steel products (in kto/ month)US3,500

Orders to the US were placed during Q1 when the spread between domestic and import prices justified it and domestic prices were still rising

• Imports rose by 26% in Q2 to an average of 2.4m 1,500

2,000

2,500

3,000

to/month compared to 1.9m to/ month in Q1

• HRC price dropped by USD220 per st since peak

• Fewer imports in the coming months expected due to 0

500

1,000

Jul Nov Mar July Nov Mar Jul Nov Mar Jul Nov Mar Jul

lower domestic prices and uncertain economic environment EU imports of steel products (in kto/ month)

Europe

07 07 08 08 08 09 09 09 10 10 10 11 11

3,500

• Flat steel import licenses increased by 67% in H1 vs. last year to an average of 1.8m to/ month reaching the peak in May 2,000

2,500

3,000

g p y

• HRC dropped by €75 per ton since peak

• Eurometal expects imports into EU to grow by 26% in 2011 500

1,000

1,500

5

Source: US Census bureau, Eurostat/ Eurometal 0

Jul07

Nov07

Mar08

July08

Nov08

Mar09

Jul09

Nov09

Mar10

Jul10

Nov10

Mar11

Jul11

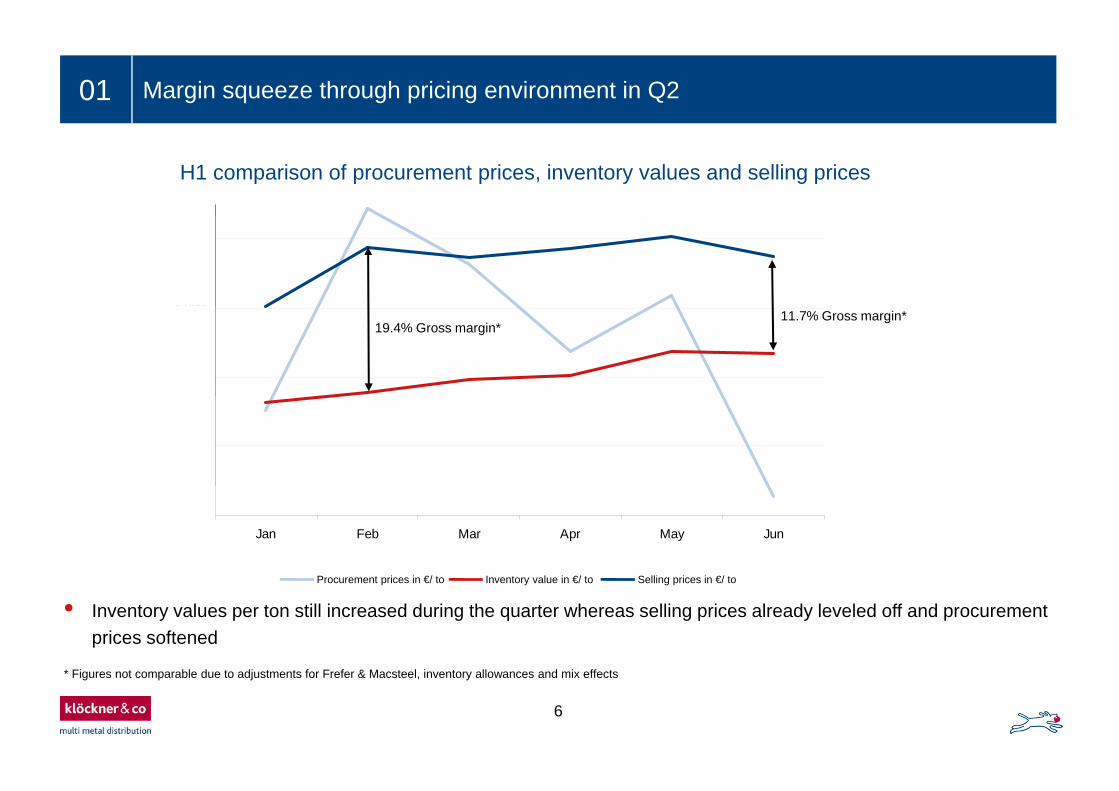

01 Margin squeeze through pricing environment in Q2

H1 comparison of procurement prices, inventory values and selling prices

1 000

1,100

900

1,00019.4% Gross margin*

11.7% Gross margin*

800

700Jan Feb Mar Apr May Jun

Procurement prices in €/ to Inventory value in €/ to Selling prices in €/ to

• Inventory values per ton still increased during the quarter whereas selling prices already leveled off and procurement prices softened

6

* Figures not comparable due to adjustments for Frefer & Macsteel, inventory allowances and mix effects

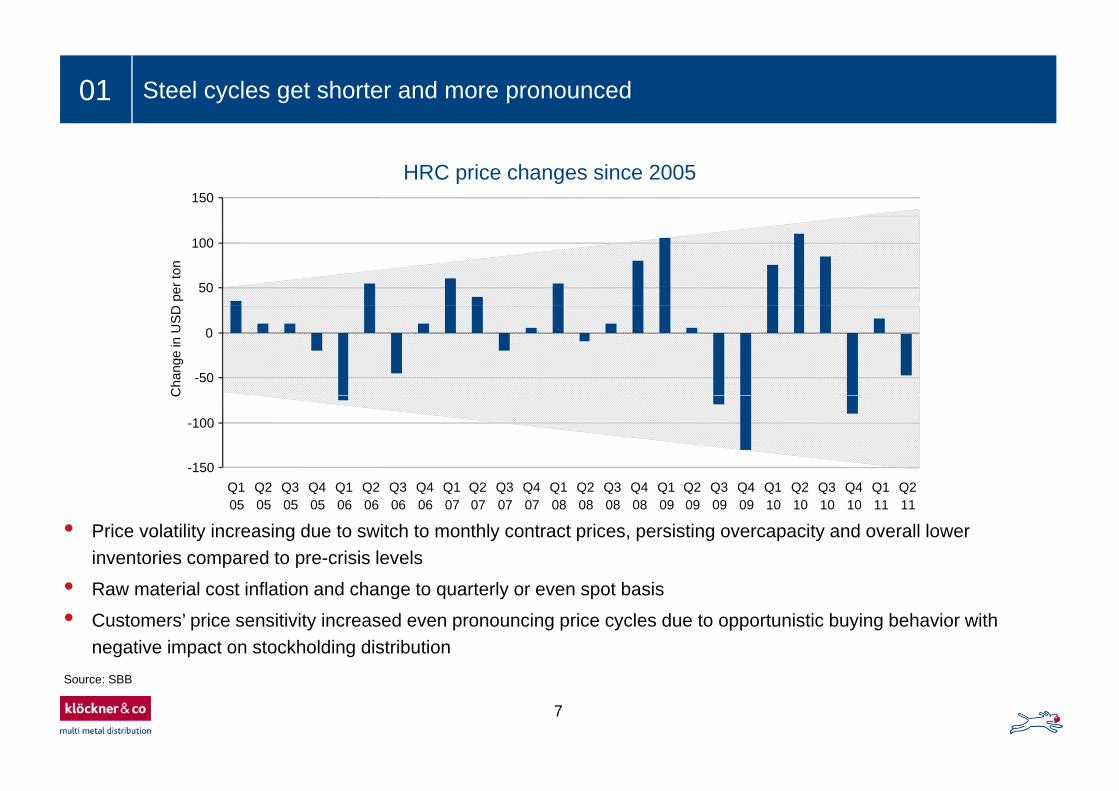

01 Steel cycles get shorter and more pronounced

HRC price development150

HRC price changes since 2005

50

100

per

ton

-50

0

Cha

nge

in U

SD

-150

-100

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

C

Q105

Q205

Q305

Q405

Q106

Q206

Q306

Q406

Q107

Q207

Q307

Q407

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Q310

Q410

Q111

Q211

• Price volatility increasing due to switch to monthly contract prices, persisting overcapacity and overall lower inventories compared to pre-crisis levels

• Raw material cost inflation and change to quarterly or even spot basis

• Customers’ price sensitivity increased even pronouncing price cycles due to opportunistic buying behavior with negative impact on stockholding distribution

7

Source: SBB

01 Klöckner & Co´s exposure to steel prices still too high

• Strategy to further reduce steel price related earnings volatility proves to be right but takes some time

• Acquisition of BSS, Macsteel and Frefer being important steps towards more balanced and less commoditized q g p pbusiness

• Negative impact could not yet be absorbed by value added services with strong margins also during Q2

C it l M k t D

700

800

€/to €m

400,0

500,0

400

Capital Market Day 2010

400

500

600

100,0

200,0

300,0300

200

100

100

200

300

-200,0

-100,0

0,00

-100

-200100Q105

Q205

Q305

Q405

Q106

Q206

Q306

Q406

Q107

Q207

Q307

Q407

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Q310

Q410

Q111

Q211

200,0

Flat Products / HRC / N.Europe domestic €/ to Scrap / Shredded / Rotterdam export FOB €/ to EBITDA €m

Comment: EBITDA normalized for one-offs from asset disposals, VAOs, stock provisions and cartel fine France

8

Source: SBB, Company figures

01 Key financials Q2 2011

SalesSales volumes

€1,885m+33.1%

1 448 Tt

+21.8%1,763 Tto

€1,416m

Q2 2011Q2 2010

1,448 Tto

Q2 2010 Q2 2011

EBITDAGross profit

-38.3%+1.8%

€100m€62m

Q2 2011Q2 2010€331m €337m

Q2 2011Q2 2010

9

01 Sales volumes and sales

Sales (€m)Sales volumes (Tto) ( )( )

1,885

1 0331,180

1,448 1,368 1,3181,498

1,763

934 8731,049

1,416 1,401 1,332

1,587

1,033 966 873

+21.8% +33.1%

+17.7% +18.8%

Q3 2009 Q4 2009 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2009 Q4 2009 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011

10

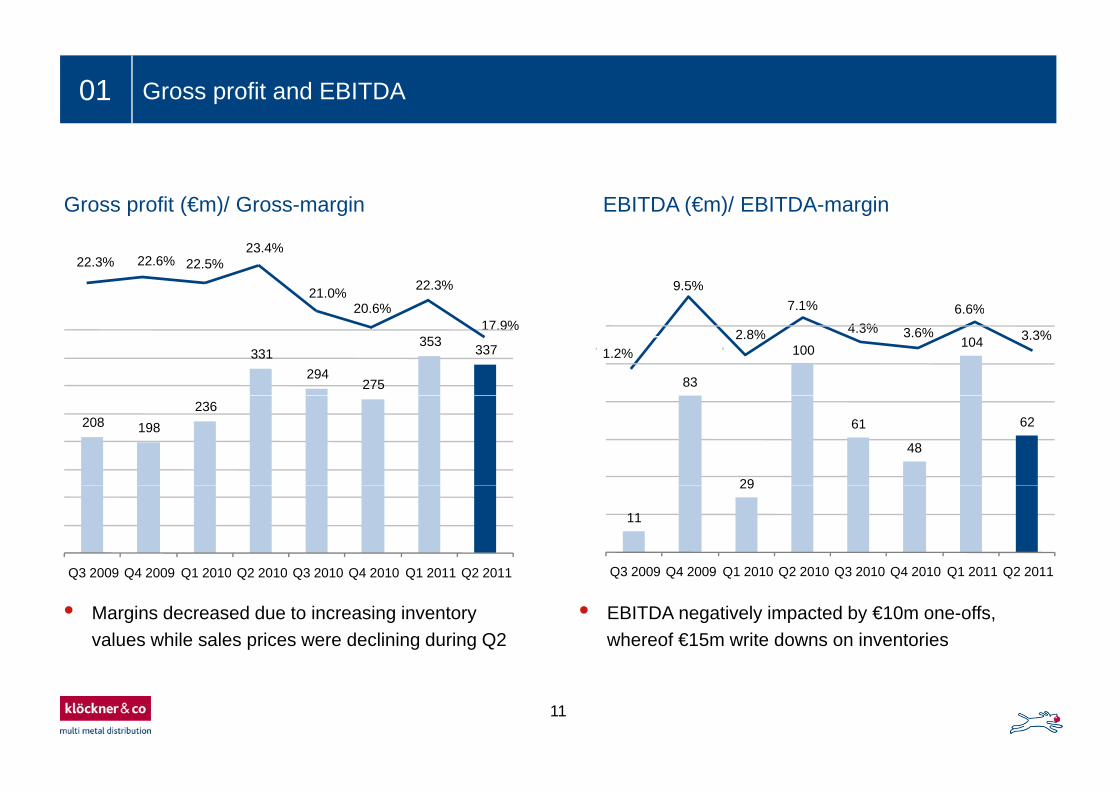

Ein- bis zweizeiliger Folientitel01 Gross profit and EBITDA

Gross profit (€m)/ Gross-margin EBITDA (€m)/ EBITDA-margin( ) g

0

2

4

6

8

10

12

( ) g

22.3% 22.6% 22.5%23.4%

21.0%20 6%

22.3% 9.5%7 1%

6.6% Reihe1

6 6%020.6%17.9%

1.2%2.8%

7.1%

4.3% 3.6% 3.3%1 3

6.6%

83

100 104331

294275

353 337

29

61

48

62208 198236

11

29

Q3 2009 Q4 2009 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011Q3 2009 Q4 2009 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011

• Margins decreased due to increasing inventory values while sales prices were declining during Q2

• EBITDA negatively impacted by €10m one-offs, whereof €15m write downs on inventories

Q3 2009 Q4 2009 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011Q3 2009 Q4 2009 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011

11

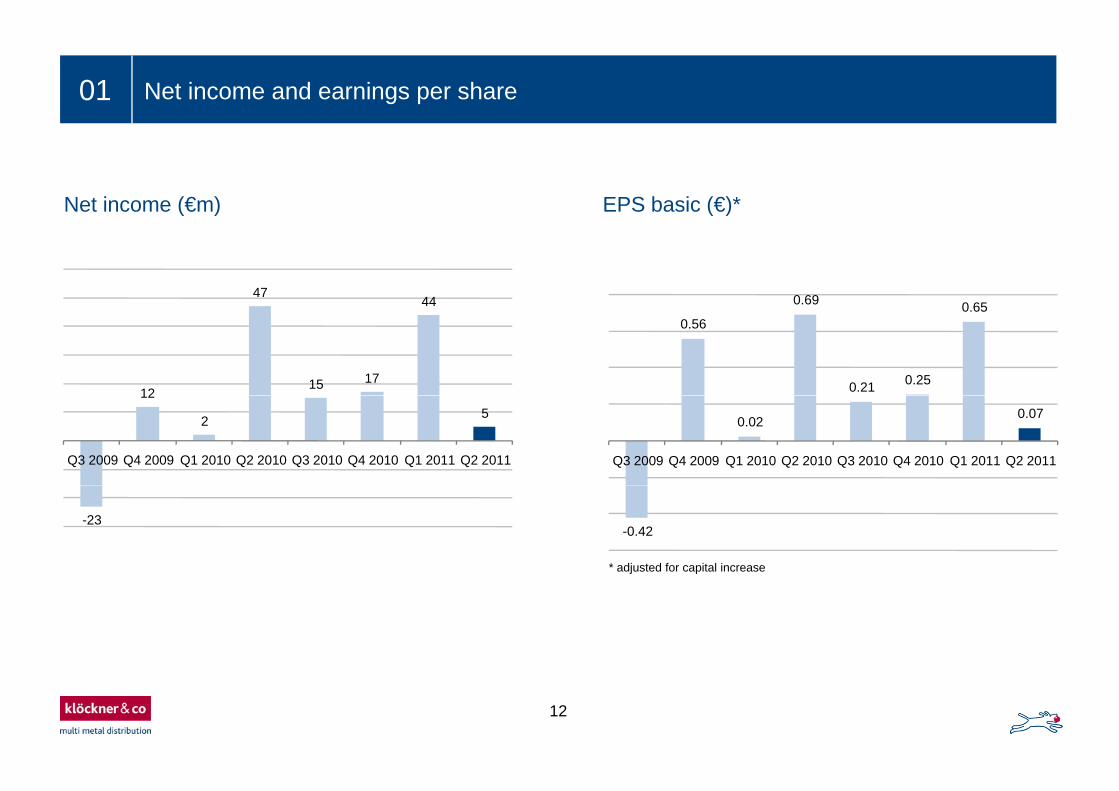

Ein- bis zweizeiliger Folientitel01 Net income and earnings per share

EPS basic (€)*Net income (€m) ( )( )

4744 0.69 0 65

1215 17

44

0.56

0.21 0.25

0.65

12

2 5

Q3 2009 Q4 2009 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011

0.02 0.07

Q3 2009 Q4 2009 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011

* adjusted for capital increase

-23-0.42

12

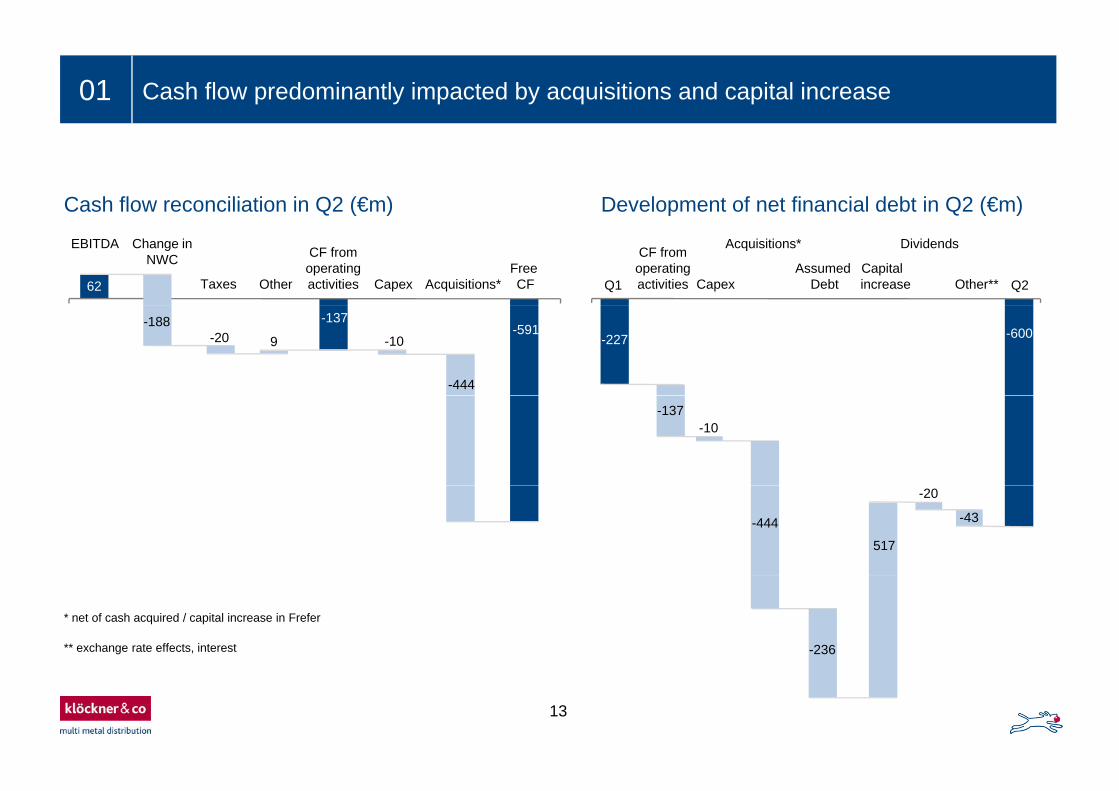

Ein- bis zweizeiliger Folientitel01 Cash flow predominantly impacted by acquisitions and capital increase

Development of net financial debt in Q2 (€m)Cash flow reconciliation in Q2 (€m)

Capex Other**

( )( )

Q1 Q262

EBITDA Change inNWC

Taxes Other

CF fromoperatingactivities Capex

Free CFAcquisitions*

Capital increase

Acquisitions*

Assumed Debt

CF fromoperatingactivities

Dividends

-227 -600-137

-591-20

-444

-10-188

9

-137-10

517

-43-444

-20

** exchange rate effects, interest -236

* net of cash acquired / capital increase in Frefer

13

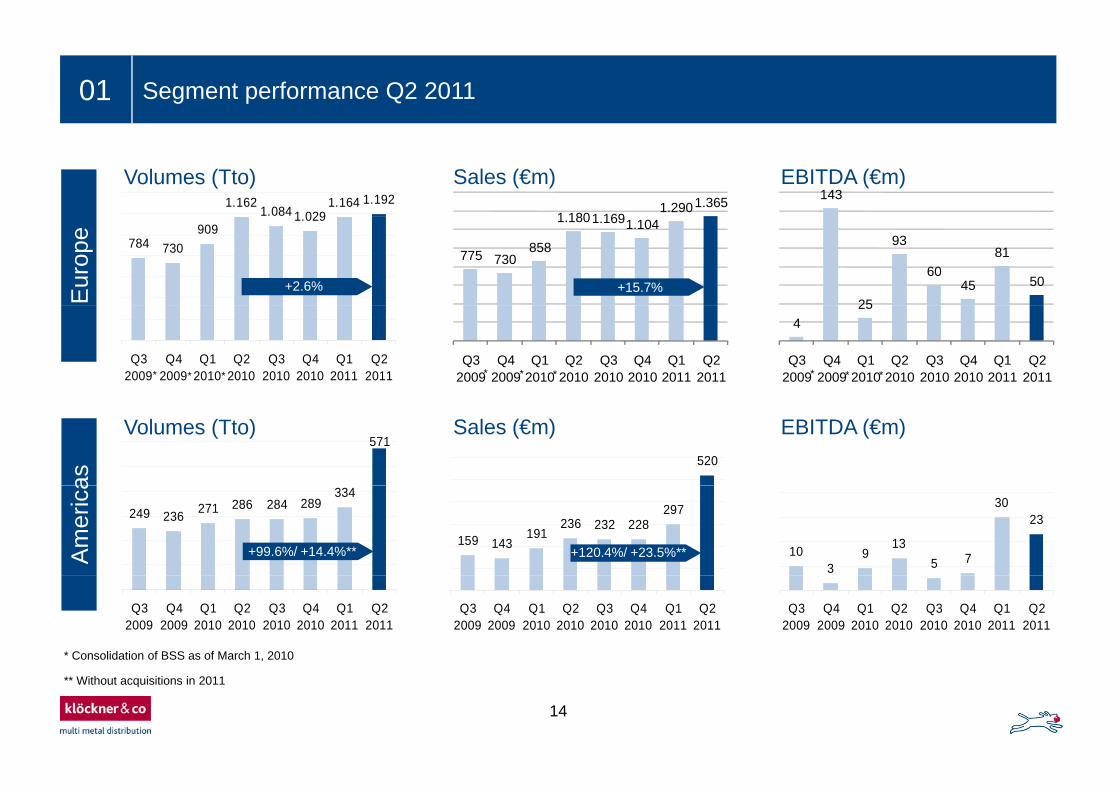

Ein- bis zweizeiliger Folientitel01 Segment performance Q2 2011

1.1621.084 1 029

1.164 1.192Volumes (Tto) Sales (€m) EBITDA (€m)

1 1801 1691.2901.365 143

784 730909

1.029

Eur

ope

775 730858

1.1801.1691.104

25

93

6045

81

50+2.6% +15.7%

Q32009

Q42009

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011** * * * * ** *

Q32009

Q42009

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

425

Q32009

Q42009

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Volumes (Tto) Sales (€m) EBITDA (€m)

as

571520

Am

eric

a

249 236 271 286 284 289334

159 143191

236 232 228297

103

913

5 7

3023

+99.6%/ +14.4%** +120.4%/ +23.5%**

Q32009

Q42009

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Q32009

Q42009

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Q32009

Q42009

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

* Consolidation of BSS as of March 1, 2010

14

** Without acquisitions in 2011

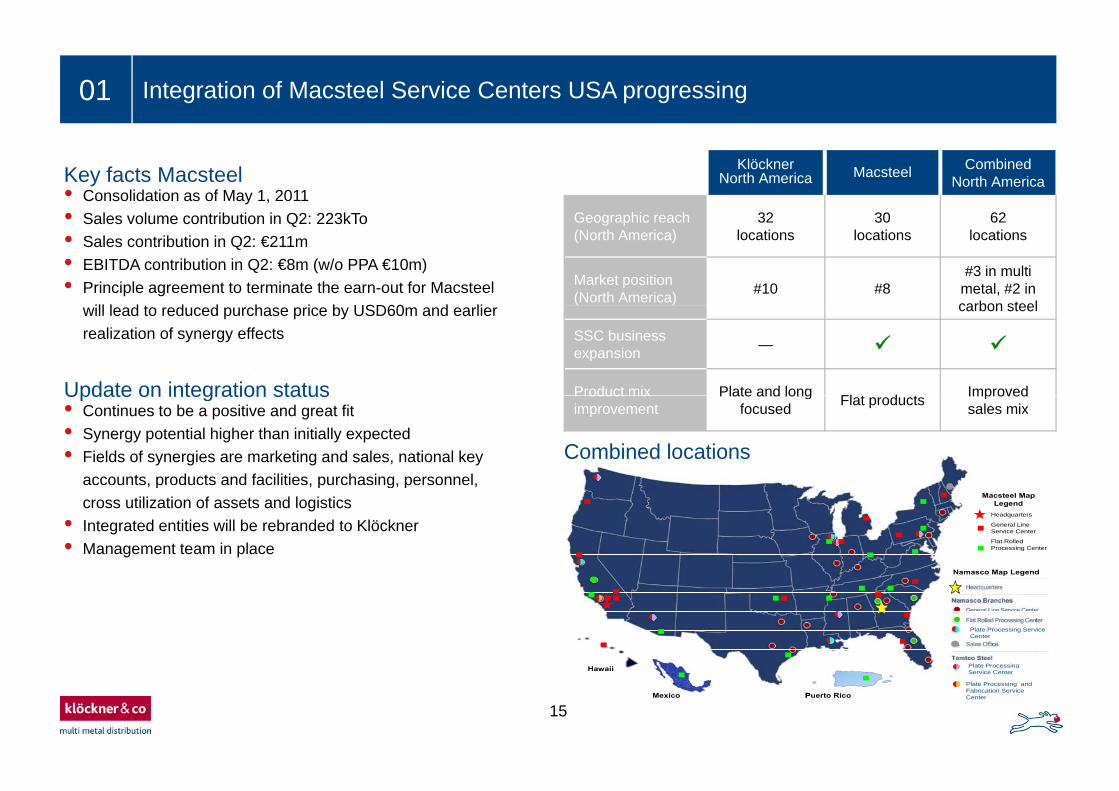

01 Integration of Macsteel Service Centers USA progressing

Key facts Macsteel• Consolidation as of May 1, 2011• Sales volume contribution in Q2: 223kTo

KlöcknerNorth America Macsteel Combined

North America

Geographic reach 32 30 62• Sales volume contribution in Q2: 223kTo• Sales contribution in Q2: €211m• EBITDA contribution in Q2: €8m (w/o PPA €10m)• Principle agreement to terminate the earn-out for Macsteel

ill l d t d d h i b USD60 d li

Geographic reach(North America)

32locations

30locations

62locations

Market position(North America) #10 #8

#3 in multi metal, #2 in carbon steelwill lead to reduced purchase price by USD60m and earlier

realization of synergy effects

carbon steel

SSC business expansion —

Product mix Plate and long Fl t d t ImprovedUpdate on integration status• Continues to be a positive and great fit• Synergy potential higher than initially expected• Fields of synergies are marketing and sales, national key

accounts, products and facilities, purchasing, personnel,

Product mix improvement

Plate and long focused Flat products Improved

sales mix

Combined locations

Update on integration status

, p , p g, p ,cross utilization of assets and logistics

• Integrated entities will be rebranded to Klöckner• Management team in place

Macsteel Map Legend

Headquarters

General Line Service Center

Flat Rolled Processing Center

Namasco Map Legend

Macsteel Map Legend

Headquarters

General Line Service Center

Flat Rolled Processing Center

Namasco Map Legend

Plate Processing

Plate Processing Service Center

p g

Plate Processing

Plate Processing Service Center

p g

15

Plate Processing Service Center

Plate Processing and Fabrication Service Center

Hawaii

Puerto RicoMexico

Plate Processing Service Center

Plate Processing and Fabrication Service Center

Hawaii

Puerto RicoMexico

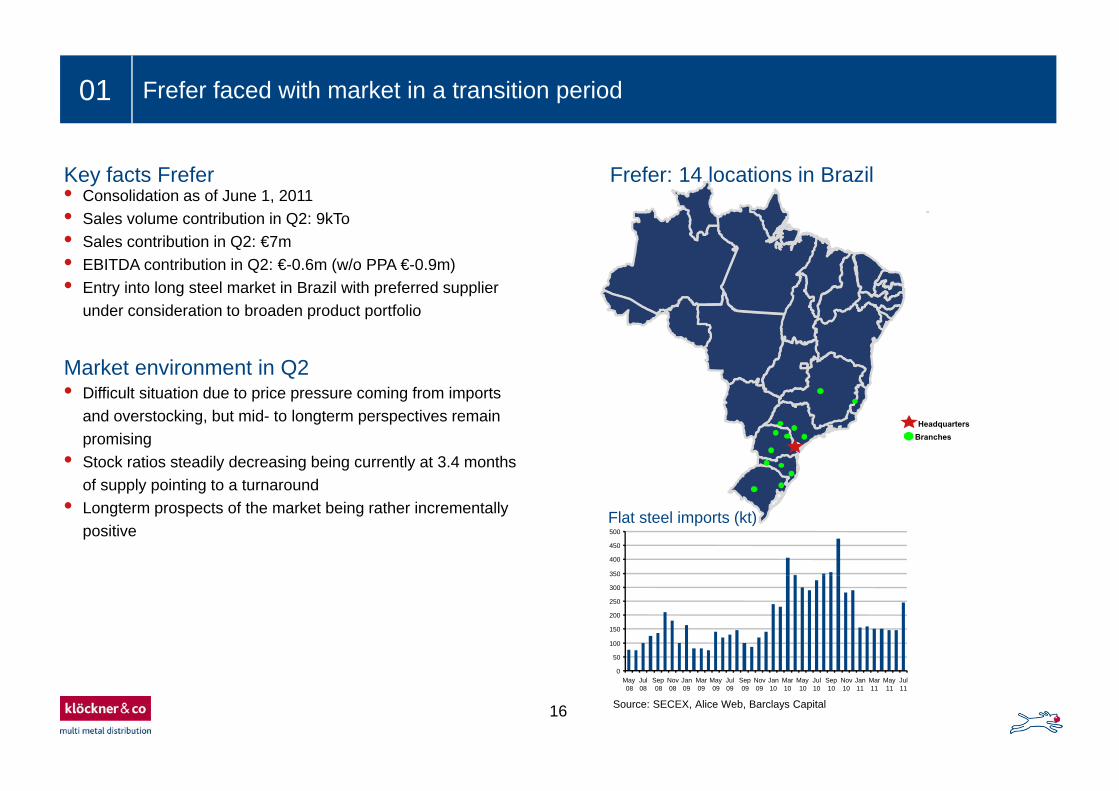

01 Frefer faced with market in a transition period

Key facts Frefer • Consolidation as of June 1, 2011• Sales volume contribution in Q2: 9kTo

Frefer: 14 locations in Brazil

• Sales volume contribution in Q2: 9kTo• Sales contribution in Q2: €7m• EBITDA contribution in Q2: €-0.6m (w/o PPA €-0.9m)• Entry into long steel market in Brazil with preferred supplier

d id ti t b d d t tf li

Market environment in Q2

under consideration to broaden product portfolio

• Difficult situation due to price pressure coming from importsDifficult situation due to price pressure coming from imports and overstocking, but mid- to longterm perspectives remain promising

• Stock ratios steadily decreasing being currently at 3.4 months of supply pointing to a turnaround

HeadquartersBranches

of supply pointing to a turnaround• Longterm prospects of the market being rather incrementally

positiveFlat steel imports (kt)

350

400

450

500

50

100

150

200

250

300

350

16 Source: SECEX, Alice Web, Barclays Capital

0May08

Jul08

Sep08

Nov08

Jan09

Mar09

May09

Jul09

Sep09

Nov09

Jan10

Mar10

May10

Jul10

Sep10

Nov10

Jan11

Mar11

May11

Jul11

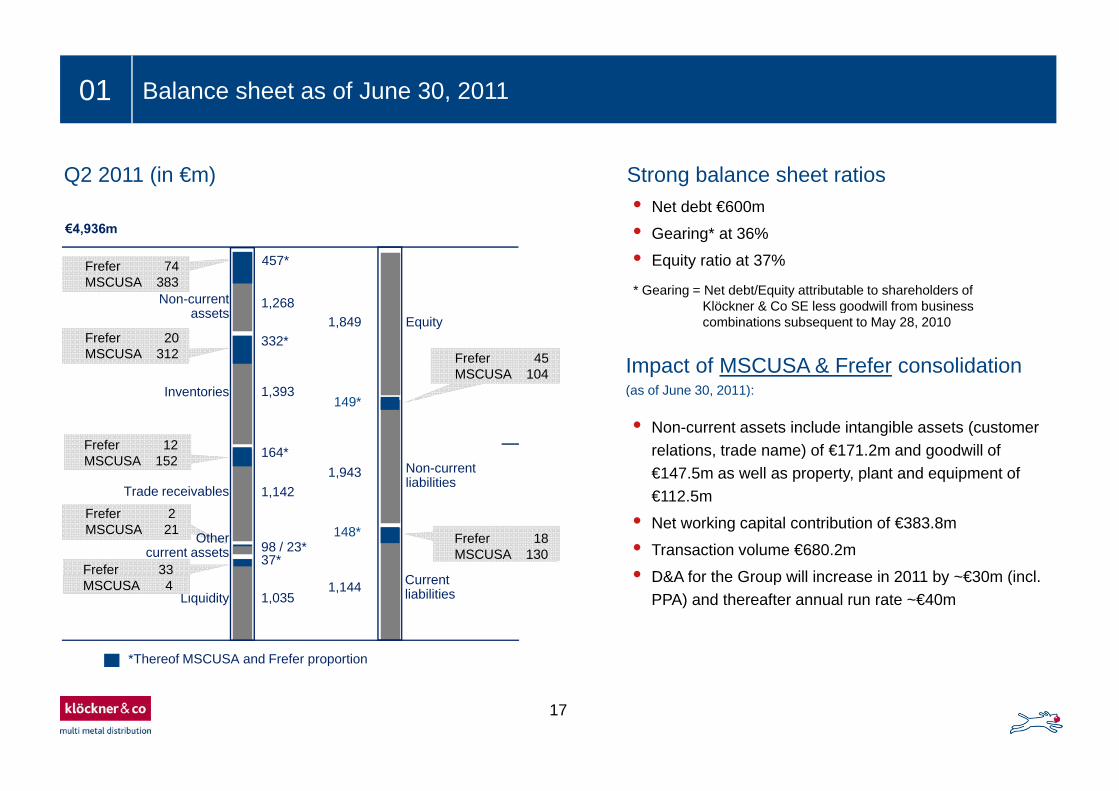

01 Balance sheet as of June 30, 2011

Q2 2011 (in €m) Strong balance sheet ratios• Net debt €600m

• Gearing* at 36%

• Equity ratio at 37%

* Gearing = Net debt/Equity attributable to shareholders of Klöckner & Co SE less goodwill from business1 268

€4,936m

Non-current

457*Frefer 74MSCUSA 383

Klöckner & Co SE less goodwill from business combinations subsequent to May 28, 2010

1,268

1,393

1,849assets

Inventories

Equity332*

Impact of MSCUSA & Frefer consolidation (as of June 30, 2011):

Frefer 45 MSCUSA 104

Frefer 20MSCUSA 312

1,393

1,943

Inventories

Non-currentliabilities

149*

164*

( , )

• Non-current assets include intangible assets (customer relations, trade name) of €171.2m and goodwill of €147.5m as well as property, plant and equipment of

Frefer 12MSCUSA 152

1,142

98 / 23*

Trade receivables

Othercurrent assets

liabilities

C t

148*

37*

Frefer 2MSCUSA 21 Frefer 18

MSCUSA 130

€112.5m

• Net working capital contribution of €383.8m

• Transaction volume €680.2m

• D&A for the Group will increase in 2011 by ~€30m (inclFrefer 33

1,0351,144

LiquidityCurrent liabilities

*Thereof MSCUSA and Frefer proportion

• D&A for the Group will increase in 2011 by ~€30m (incl. PPA) and thereafter annual run rate ~€40m

MSCUSA 4

17

p p

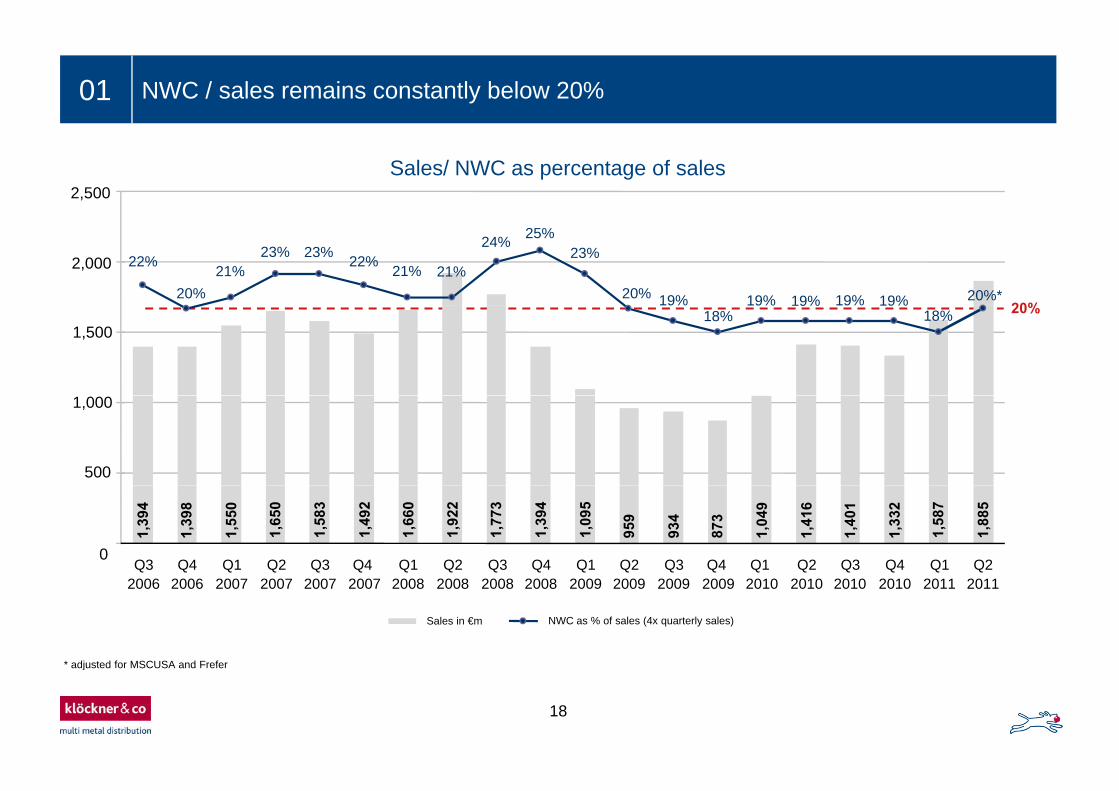

01 NWC / sales remains constantly below 20%

Sales/ NWC as percentage of sales30%30%

2,500 30%

25%25%

20%

2,000 22%

20%21%

23% 23% 22% 21% 21%

24% 25%23%

20% 19% 19% 19% 19% 19%

25%

20%*

15%15%

20%1,500

18%9% %

15%

18%

10%10%

1,000

5005%

10%

500

0%

5%

0%

5%

0

1,39

4

1,39

8

1,55

0

1,65

0

1,58

3

1,49

2

1,66

0

1,92

2

1,77

3

1,39

4

1,09

5

959

934

873

1,04

9

1,41

6

1,40

1

1,33

2

1,58

7

1,88

5

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q20%

5%

0%

* adjusted for MSCUSA and Frefer

2006 2006 2007 2007 2007 2007 2008 2008 2008 2008 2009 2009 2009 2009 2010 2010 2010 2010 2011 2011

Sales in €m NWC as % of sales (4x quarterly sales)

18

adjusted for MSCUSA and Frefer

01 Further diversification and improvement of financial position in Q2

€m Drawn amount

Facility Committed Q2 2011* FY 2010* €mQ2

2011

Bilateral Facilities1) 580 250 73

Other Bonds 40 41 0

ABS 560 221 88

Equity 1,849

Net debt 600

Gearing4) 36%

Syndicated Loan 500 226 226

Promissory Note2) 343 345 147

Total Senior Debt 2,023 1,083 534

C tibl 20073) 325 314 306

Maturity profile of committed facilities and drawn amounts (€m)Convertible 20073) 325 314 306

Convertible 20093) 98 81 81

Convertible 20103) 186 157 151

Total Debt 2 632 1 635 1 072

amounts (€m)

517

676753

682

Total Debt 2,632 1,635 1,072

Cash 1,035 935

Net Debt 600 137 244

442517

51

378

179

398

*Including interest1) Including finance lease; volume increased in connection with the acquisition of Macsteel2) New promissory notes issued in Q2 2011 (€198m)3) Drawn amount excludes equity component4) Net debt/Equity attributable to shareholders of Klöckner & Co SE less goodwill from business combinations subsequent to May 28 2010

Credit limits

Drawn amounts

51

2011 2012 2013 2014 Thereafter

goodwill from business combinations subsequent to May 28, 2010 Drawn amounts

19

Agenda

01 Recent developments, financials and performance Q2 2011

02 Market environment

03 Outlook

04 Appendix04 Appendix

20

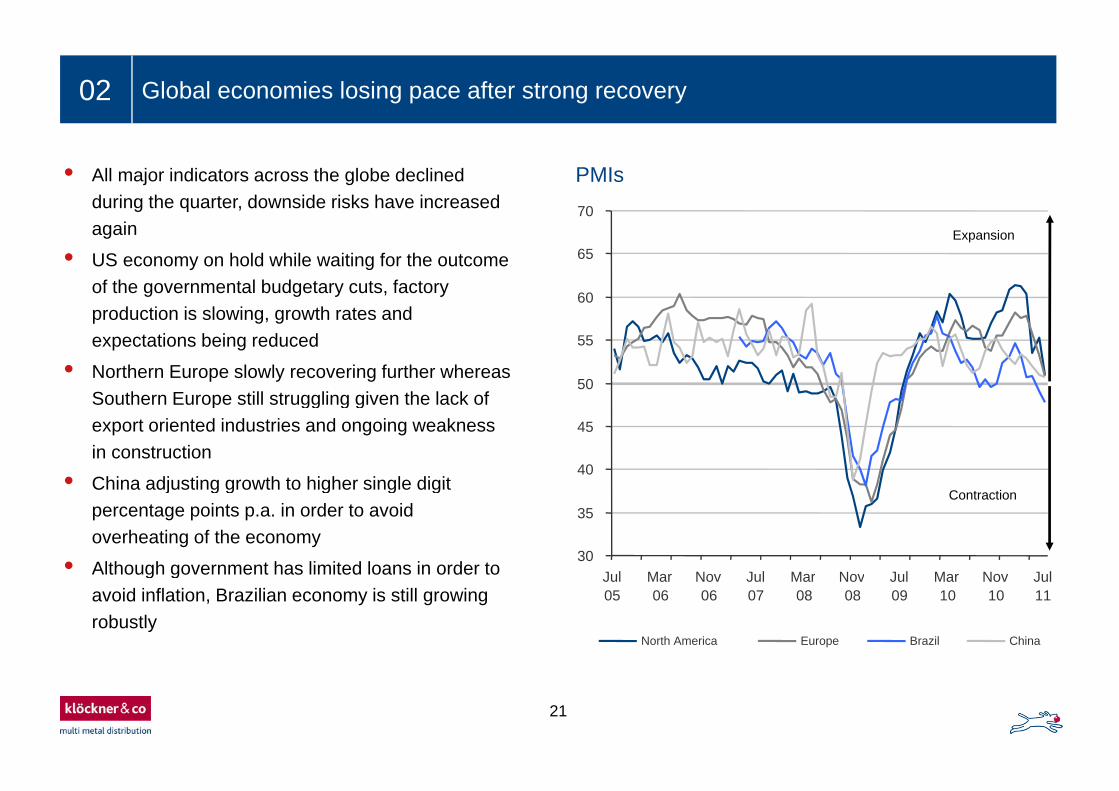

02 Global economies losing pace after strong recovery

• All major indicators across the globe declined during the quarter, downside risks have increased

PMIs 70

again

• US economy on hold while waiting for the outcome of the governmental budgetary cuts, factory

Expansion

60

65

70

production is slowing, growth rates and expectations being reduced

• Northern Europe slowly recovering further whereas Southern Europe still struggling given the lack of

50

55

Southern Europe still struggling given the lack of export oriented industries and ongoing weakness in construction

• China adjusting growth to higher single digit40

45

China adjusting growth to higher single digit percentage points p.a. in order to avoid overheating of the economy

• Although government has limited loans in order to

Contraction

30

35

Jul Mar Nov Jul Mar Nov Jul Mar Nov Julg gavoid inflation, Brazilian economy is still growing robustly

Jul05

Mar06

Nov06

Jul07

Mar08

Nov08

Jul09

Mar10

Nov10

Jul11

North America Europe Brazil China

21

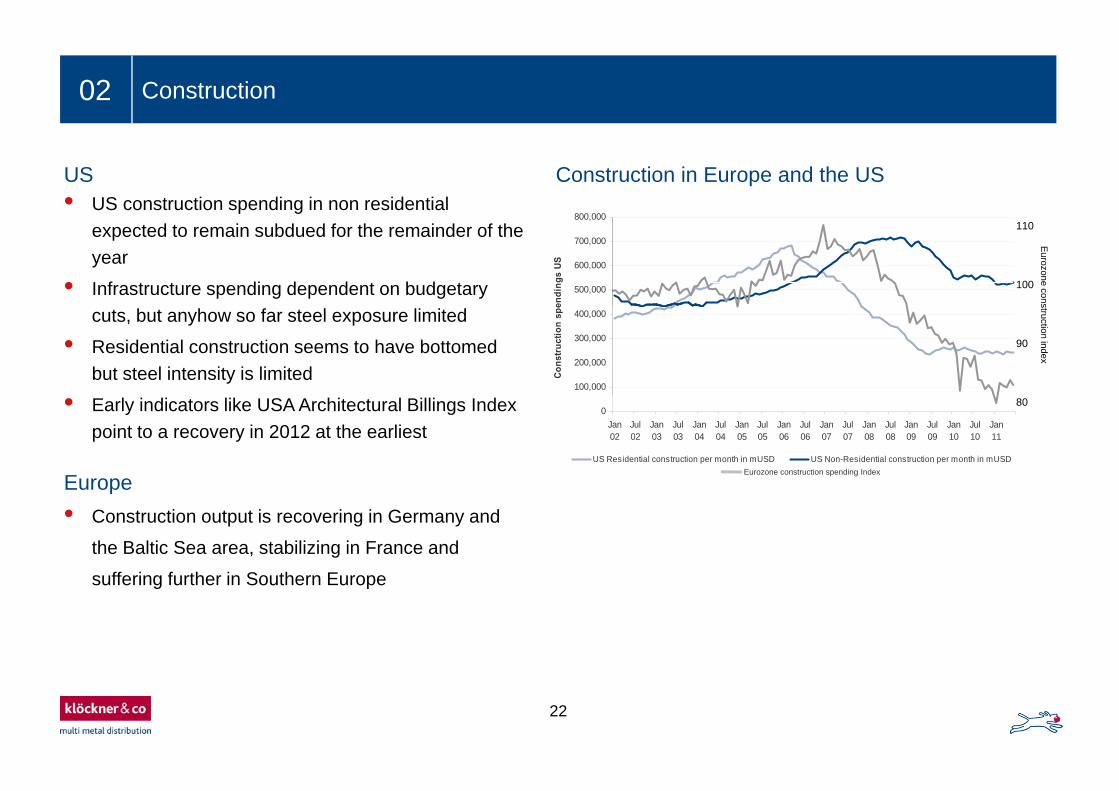

02 Construction

• US construction spending in non residential US

800 000

Construction in Europe and the US

expected to remain subdued for the remainder of the year

• Infrastructure spending dependent on budgetary

Eurozone cons

500,000

600,000

700,000

800,000

endi

ngs

US

100

110

cuts, but anyhow so far steel exposure limited

• Residential construction seems to have bottomed but steel intensity is limited

struction index

100,000

200,000

300,000

400,000

Cons

truc

tion

spe

90

• Early indicators like USA Architectural Billings Index point to a recovery in 2012 at the earliest

Europe

0Jan02

Jul02

Jan03

Jul03

Jan04

Jul04

Jan05

Jul05

Jan06

Jul06

Jan07

Jul07

Jan08

Jul08

Jan09

Jul09

Jan10

Jul10

Jan11

US Residential construction per month in mUSD US Non-Residential construction per month in mUSD

80

Eurozone construction spending Index

• Construction output is recovering in Germany and

the Baltic Sea area, stabilizing in France and

ff i f th i S th E

Europe

suffering further in Southern Europe

22

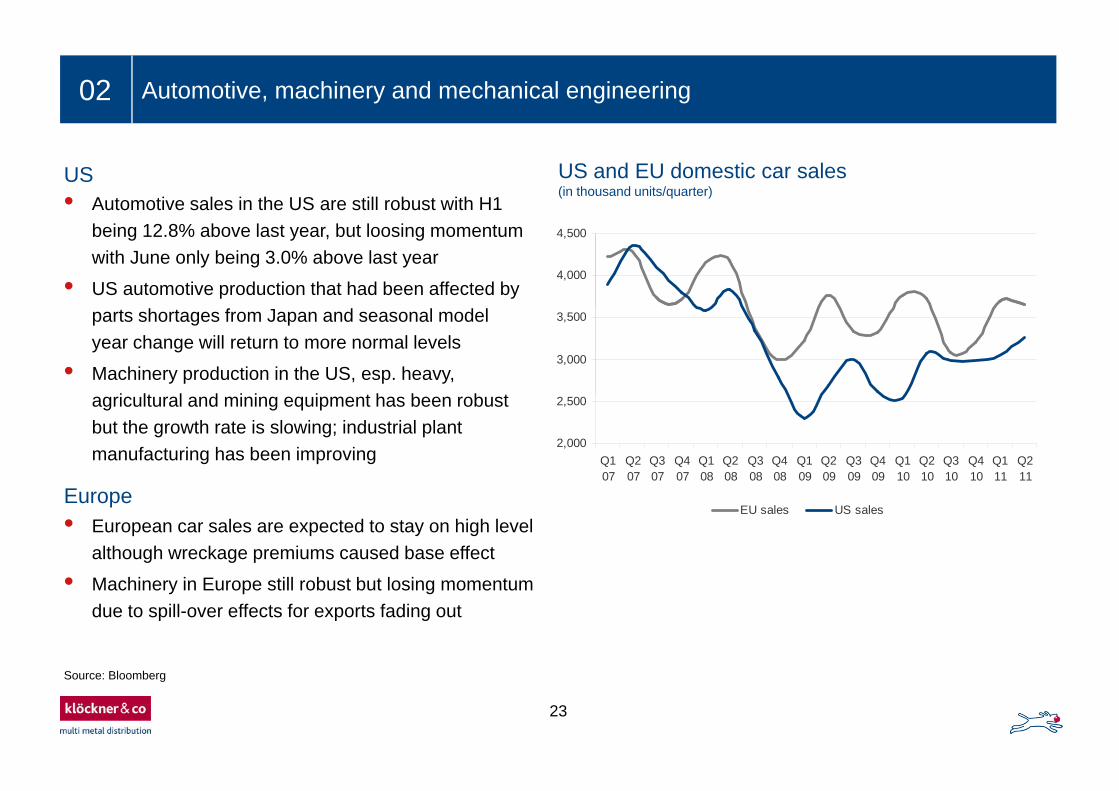

02 Automotive, machinery and mechanical engineering

• Automotive sales in the US are still robust with H1

US and EU domestic car sales (in thousand units/quarter)

US

being 12.8% above last year, but loosing momentum with June only being 3.0% above last year

• US automotive production that had been affected by 4,000

4,500

parts shortages from Japan and seasonal model year change will return to more normal levels

• Machinery production in the US, esp. heavy, i lt l d i i i t h b b t

3,000

3,500

agricultural and mining equipment has been robust but the growth rate is slowing; industrial plant manufacturing has been improving

2,000

2,500

Q107

Q207

Q307

Q407

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Q310

Q410

Q111

Q211

Europe • European car sales are expected to stay on high level

although wreckage premiums caused base effect

EU sales US sales

• Machinery in Europe still robust but losing momentum due to spill-over effects for exports fading out

23

Source: Bloomberg

Agenda

01 Recent developments, financials and performance Q2 2011

02 Market environment

03 Outlook

04 Appendix04 Appendix

24

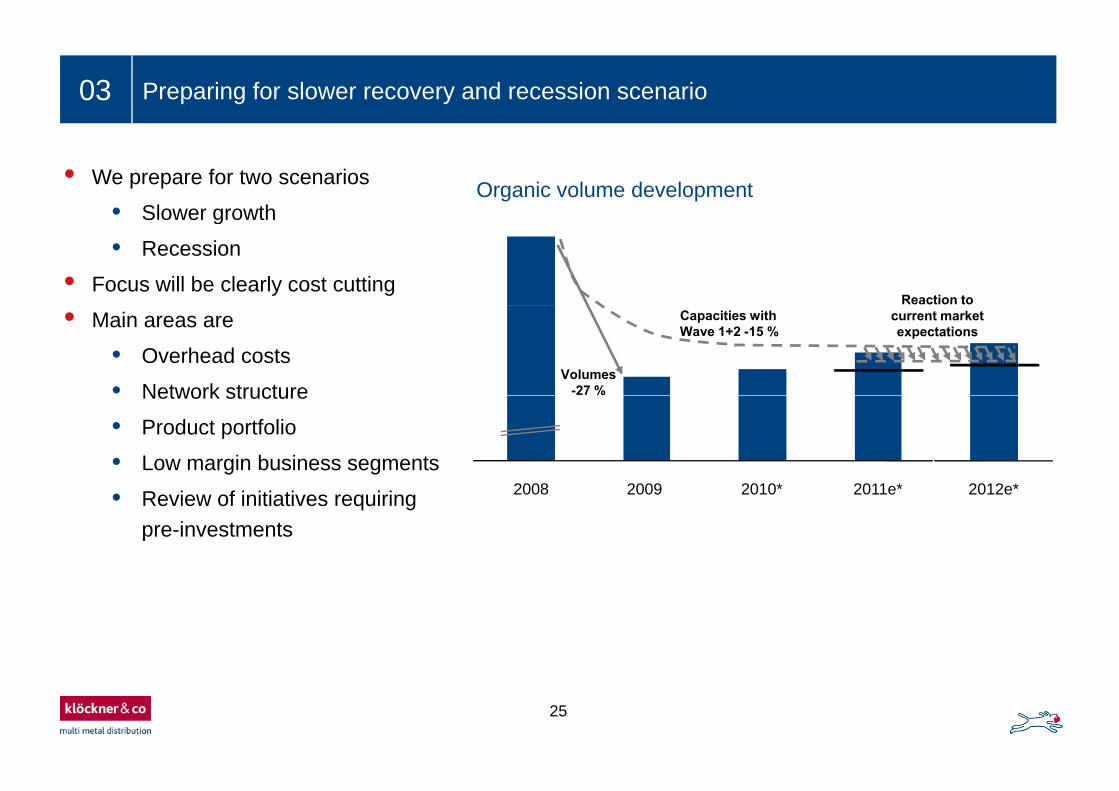

03 Preparing for slower recovery and recession scenario

• We prepare for two scenarios

• Slower growthOrganic volume development

Reaction to

Slower growth

• Recession

• Focus will be clearly cost cutting

Volumes -27 %

Capacities with Wave 1+2 -15 %

current market expectations• Main areas are

• Overhead costs

• Network structure

2008 2009 2010* 2011 * 2012 *

Network structure

• Product portfolio

• Low margin business segments2008 2009 2010* 2011e* 2012e*• Review of initiatives requiring

pre-investments

25

03 Outlook

• Q3 2011• Volumes to be seasonally lighter on organic basis• Volumes to be seasonally lighter on organic basis

• EBITDA expected seasonally below Q2 level

• Prices to stabilize during Q3 with upside potential after summer depending on supply balance and further macro economic trends

• Full year 2011 guidance• >25% volume and sales growth resulting from acquisitions expected with precondition that world• >25% volume and sales growth resulting from acquisitions expected with precondition that world

economies not entering into a recession

• Midterm EBITDA margin target of 6% not realistic to be achieved already in 2011

26

Agenda

01 Recent developments, financials and performance Q2 201101 Recent developments, financials and performance Q2 2011

Outlook0202 Market environment

03 Outlook

04 Appendix04 Appendix

27

04 Appendix

Financial calendar 2011/2012

November 9, 2011 Q3 interim report 2011

March 7, 2012 Annual Financial Statements 2011

May 9, 2012 Q1 interim report 2012

May 25, 2012 Annual General Meeting 2012

August 8, 2012 Q2 interim report 2012

November 7 2012 Q3 interim report 2012

Contact details Investor Relations

November 7, 2012 Q3 interim report 2012

Contact details Investor Relations

Dr. Thilo Theilen, Head of Investor Relations & Corporate Communications

Phone: +49 203 307 2050

Fax: +49 203 307 5025

E-mail: [email protected]

Internet: www.kloeckner.de

28

04 Quarterly results and FY results 2006-2011

(€m)Q2

2011Q1

2011Q4

2010Q3

2010Q2

2010Q1

2010Q4

2009Q3

2009Q2

2009Q1

2009FY

2010FY

2009FY

2008FY

2007FY

2006

Volumes (Tto) 1,763 1,498 1,318 1,368 1,448 1,180 966 1,033 1,053 1,068 5,314 4,119 5,974 6,478 6,127

Sales 1,885 1,587 1,332 1,401 1,416 1,049 873 934 959 1,095 5,198 3,860 6,750 6,274 5,532

Gross profit 337 353 275 294 331 236 198 208 161 78 1,136 645 1,366 1,221 1,208Gross profit 337 353 275 294 331 236 198 208 161 78 1,136 645 1,366 1,221 1,208

% margin 17.9 22.3 20.6 21.0 23.4 22.5 22.6 22.3 16.8 7.1 21.9 16.7 20.2 19.5 21.8

EBITDA 62 104 48 61 100 29 83 11 -31 -132 238 -68 601 371 395

% margin 3.3 6.6 3.6 4.3 7.1 2.8 9.5 1.2 -3.2 -12.0 4.6 -1.8 8.9 5.9 7.1g

EBIT 36 86 24 39 78 11 26 -7 -48 -149 152 -178 533 307 337

Financial result -21 -19 -19 -16 -17 -15 -16 -14 -15 -16 -67 -62 -70 -97 -64

Income before taxes 15 66 5 22 61 -4 9 -21 -63 -165 84 -240 463 210 273

Income taxes -9 -22 12 -7 -14 6 3 -2 16 38 -4 54 -79 -54 -39

Net income 5 44 17 15 47 2 12 -23 -47 -127 80 -186 384 156 235

Minority interests 0 1 1 1 1 1 3 0 1 -2 3 3 -14 23 28

Net income KlöCo 5 43 16 14 46 1 9 -23 -48 -126 77 -188 398 133 206

EPS basic (€) 0.07 0.65 0.25 0.21 0.69 0.02 0.56 -0.42 -1.04 -2.70 1.17 -3.61 8.56 2.87 4.44

EPS diluted (€) 0.07 0.60 0.25 0.21 0.69 0.02 0.56 -0.42 -0.85 -2.43 1.17 -3.61 8.11 2.87 4.44

29

* Pro-forma consolidated figures for FY 2005, without release of negative goodwill of €139 million and without transaction costs of €39 million, without restructuring expenses of €17 million (incurred Q4) and without activity disposal of €1.9 million (incurred Q4).

04 Strong Growth: 24 acquisitions since the IPO, 2 in 2011

Acquisitions1) Acquired sales1),2)Country Acquired 1) Company Sales (FY)2)

€1.15bnBrazil May 2011 Frefer €150m

USA April 2011 Macsteel €1bn

€712mGER Mar 2010 Becker Stahl-Service €600m

CH Jan 2010 Bläsi €32m

USA Dec 2010 Lake Steel €50m

USA Sep 2010 Angeles Welding €30m

2011 2 acquisitions so far €1,150m

€567m

2010 4 acquisitions €712m

US Mar 2008 Temtco €226m

UK Jan 2008 Multitubes €5m

2008 2 acquisitions €231m

CH S 2007 L h & T i €9CH Sep 2007 Lehner & Tonossi €9m

UK Sep 2007 Interpipe €14m

US Sep 2007 ScanSteel €7m

BG Aug 2007 Metalsnab €36m

UK Jun 2007 Westok €26m

€141m

12 €231m

US May 2007 Premier Steel €23m

GER Apr 2007 Zweygart €11m

GER Apr 2007 Max Carl €15m

GER Apr 2007 Edelstahlservice €17m

US Apr 2007 Primary Steel €360m€108m

2

4

24

US Apr 2007 Primary Steel €360m

NL Apr 2007 Teuling €14m

F Jan 2007 Tournier €35m

2007 12 acquisitions €567m

2006 4 acquisitions €108m

2

30

¹ Date of announcement 2 Sales in the year prior to acquisitions 2005 2006 2007 2008 2009 2010 2011

04 Balance sheet as of June 30, 2011

(€m) June 30, 2011

Dec. 31, 2010

Comments

Non-current assets 1,268 856

Inventories 1,393 899

Shareholders’ equity:• Stable at 37% despite NWC

increase benefitting from capitalTrade receivables 1,142 703

Cash & Cash equivalents 1,035 935

Other assets 98 98

increase, benefitting from capital increase

Financial debt:

Total assets 4,936 3,491

Equity 1,849 1,290

Total non-current liabilities 1,943 1,361

• Gearing at 36%

• Net debt position due to acquisitions increased business

thereof financial liabilities 1,519 1,021

Total current liabilities 1,144 840

thereof trade payables 102 585

NWC:• Swing mainly driven by acquisitions

and also due to increased businessp y

Total equity and liabilities 4,936 3,491

Net working capital 1,713 1,017

Net financial debt 600 137

31

Net financial debt 600 137

04 Statement of cash flow Q2

Comments(€m) Q2 2011 Q2 2010

• NWC changes due to increased business and acquisitions

Operating CF 64 99

Changes in net working capital -188 -170

Others -13 14 acquisitions

• €444m were cash outflows for MSCUSA and Frefer

Others -13 14

Cash flow from operating activities -137 -57

Inflow from disposals of fixed assets/others 0 1

Outflow for acquisitions -444 0Outflow for acquisitions 444 0

Outflow for investments in fixed assets/others -10 -6

Cash flow from investing activities -454 -5

Capital increase 517 0p

Changes in financial liabilities 430 196

Dividends -20 0

Net interest payments -21 -16p y

Repayments of financial liabilities in connection with business combinations -196 0

Cash flow from financing activities 710 180

32

Total cash flow 118 118

04 Segment performance Q2 2011

(€m) Europe Americas*HQ/

Consol. TotalComments

Volume (Ttons)

Q2 2011 1,192 571 - 1,763

Q2 2010 1,162 286 - 1,448• Excl. MSCUSA, Frefer and Lake

Steel volume increase in Americas

Δ % 2.6 99.6 21.8

Sales

Q2 2011 1 365 520 - 1 885

was 14.4% and sales increase was 23.5% yoy

• Without acquisitions total volume increased by 4.9% and total sales Q2 2011 1,365 520 1,885

Q2 2010 1,180 236 - 1,416

Δ % 15.7 120.4 33.1

EBITDA

yby 17.0% yoy

EBITDA

Q2 2011 50 23 -11 62

% margin 3.6 4.4 3.3

Q2 2010 93 13 -6 100

% margin 7.9 5.4 7.1

Δ % EBITDA -46.6 81.7 -38.3

33* in 2010 North America

04 Current shareholder structure

Geographical breakdown of identified institutional investors

Comments• Identified institutional investors account for 50%

• German investors incl. retail dominate

• Top 10 shareholdings represent around 26%

• Retail shareholders represent 20%

34

04 Our Symbol

the earsattentive to customer needs

the eyeslooking forward to new developmentsattentive to customer needs looking forward to new developments

the nosesniffing out opportunitiessniffing out opportunitiesto improve performance

the ballsymbolic of our role to fetchand carry for our customers

the legsthe legsalways moving fast to keep up withthe demands of the customers

35