kenya’s competitiveness in business

DESCRIPTION

KENYA’S COMPETITIVENESS IN BUSINESS. BY JULIUS KIPNGETICH MANAGING DIRECTOR INVESTMENT PROMOTION CENTRE. AFRICA AT A GLANCE. The continent’s size is to equivalent to USA China India Argentina Western Europe New Zealand Has a population of 740 million - PowerPoint PPT PresentationTRANSCRIPT

KENYA’S COMPETITIVENESS IN BUSINESS

BYJULIUS KIPNGETICHMANAGING DIRECTORINVESTMENT PROMOTION CENTRE

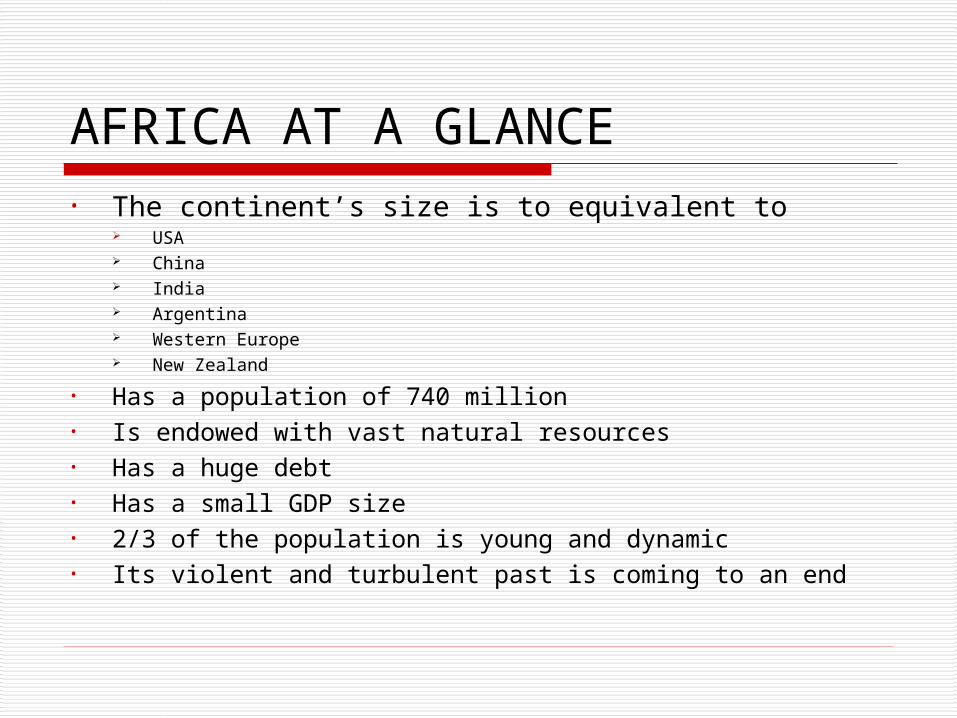

AFRICA AT A GLANCE• The continent’s size is to equivalent to

USA China India Argentina Western Europe New Zealand

• Has a population of 740 million• Is endowed with vast natural resources• Has a huge debt • Has a small GDP size• 2/3 of the population is young and dynamic• Its violent and turbulent past is coming to an end

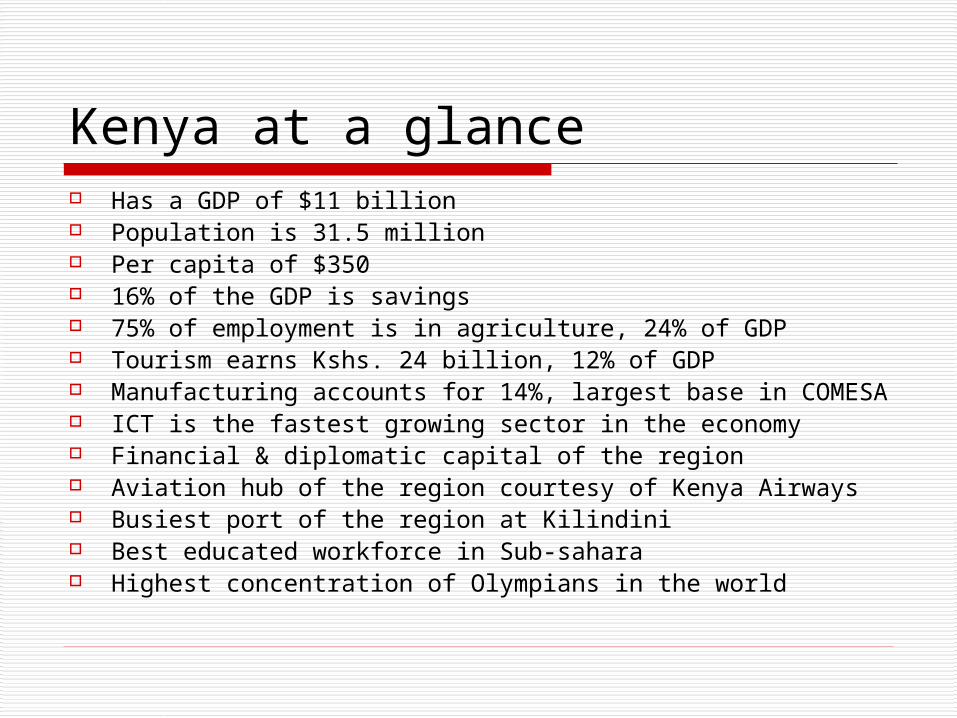

Kenya at a glance Has a GDP of $11 billion Population is 31.5 million Per capita of $350 16% of the GDP is savings 75% of employment is in agriculture, 24% of GDP Tourism earns Kshs. 24 billion, 12% of GDP Manufacturing accounts for 14%, largest base in COMESA ICT is the fastest growing sector in the economy Financial & diplomatic capital of the region Aviation hub of the region courtesy of Kenya Airways Busiest port of the region at Kilindini Best educated workforce in Sub-sahara Highest concentration of Olympians in the world

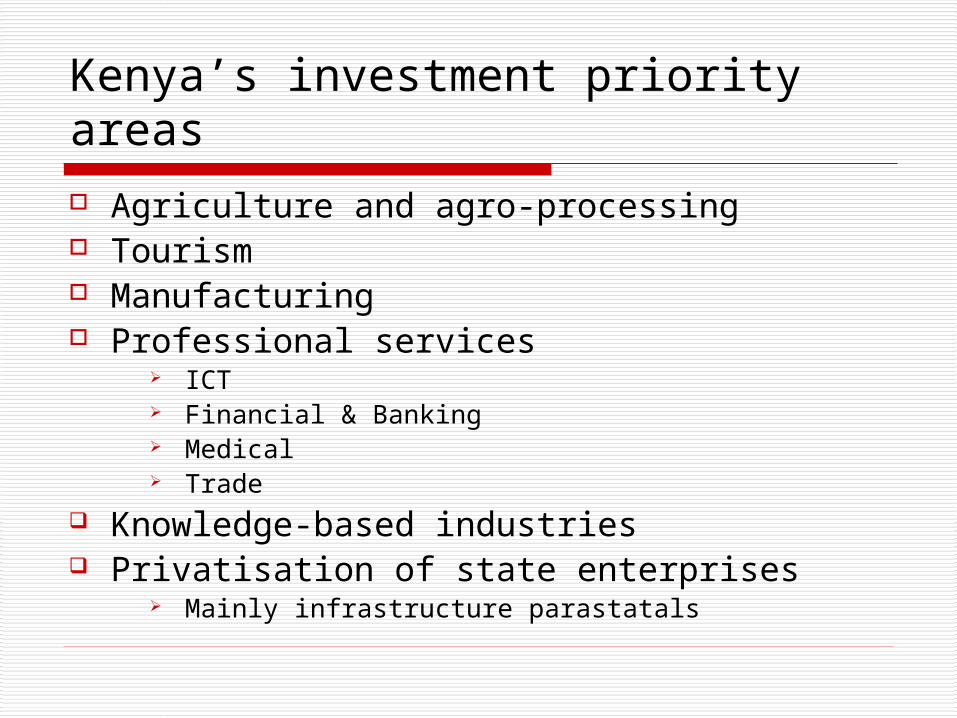

Kenya’s investment priority areas Agriculture and agro-processing Tourism Manufacturing Professional services

ICT Financial & Banking Medical Trade

Knowledge-based industries Privatisation of state enterprises

Mainly infrastructure parastatals

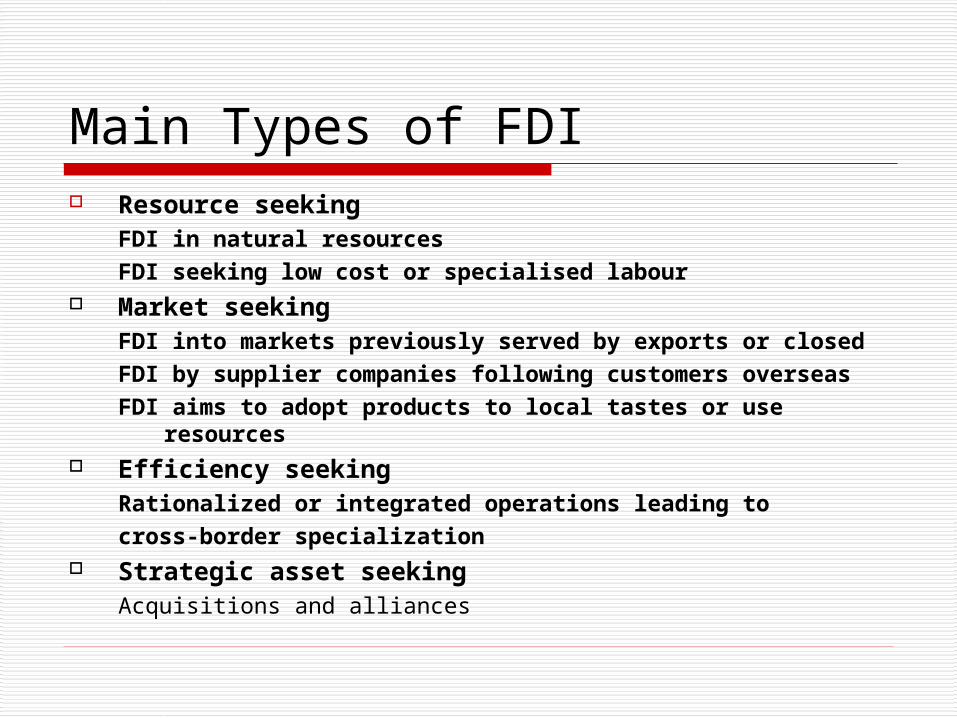

Main Types of FDI Resource seeking

FDI in natural resourcesFDI seeking low cost or specialised labour

Market seekingFDI into markets previously served by exports or closedFDI by supplier companies following customers overseasFDI aims to adopt products to local tastes or use resources

Efficiency seekingRationalized or integrated operations leading to cross-border specialization

Strategic asset seekingAcquisitions and alliances

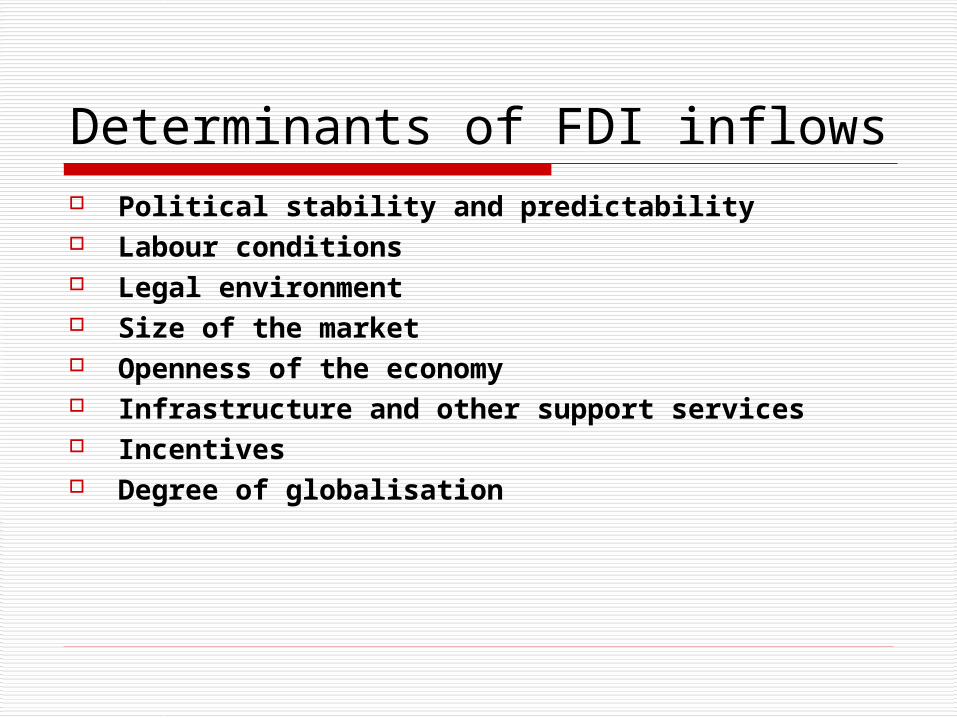

Determinants of FDI inflows Political stability and predictability Labour conditions Legal environment Size of the market Openness of the economy Infrastructure and other support services Incentives Degree of globalisation

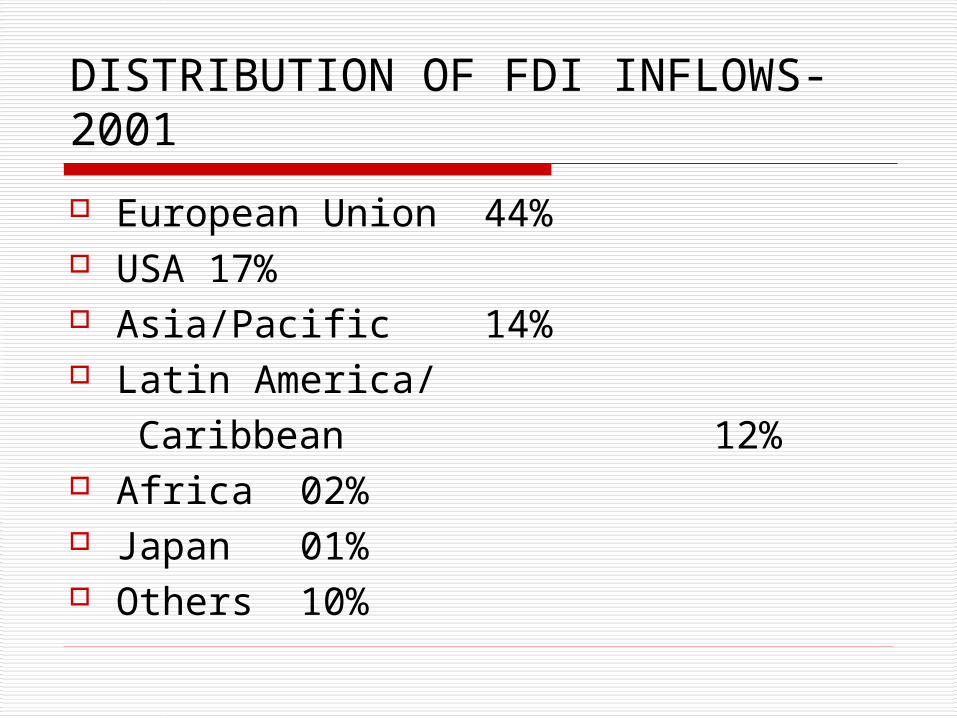

DISTRIBUTION OF FDI INFLOWS- 2001 European Union 44% USA 17% Asia/Pacific 14% Latin America/ Caribbean 12% Africa 02% Japan 01% Others 10%

Africa’s top 10 FDI destinations ($ billions) - 2001

South Africa 7 Morocco 3 Algeria 1.2 Angola 1.1 Nigeria 1.1 Sudan 0.6 Egypt 0.6 Tunisia 0.6 Ivory Coast 0.25 Mozambique 0.25

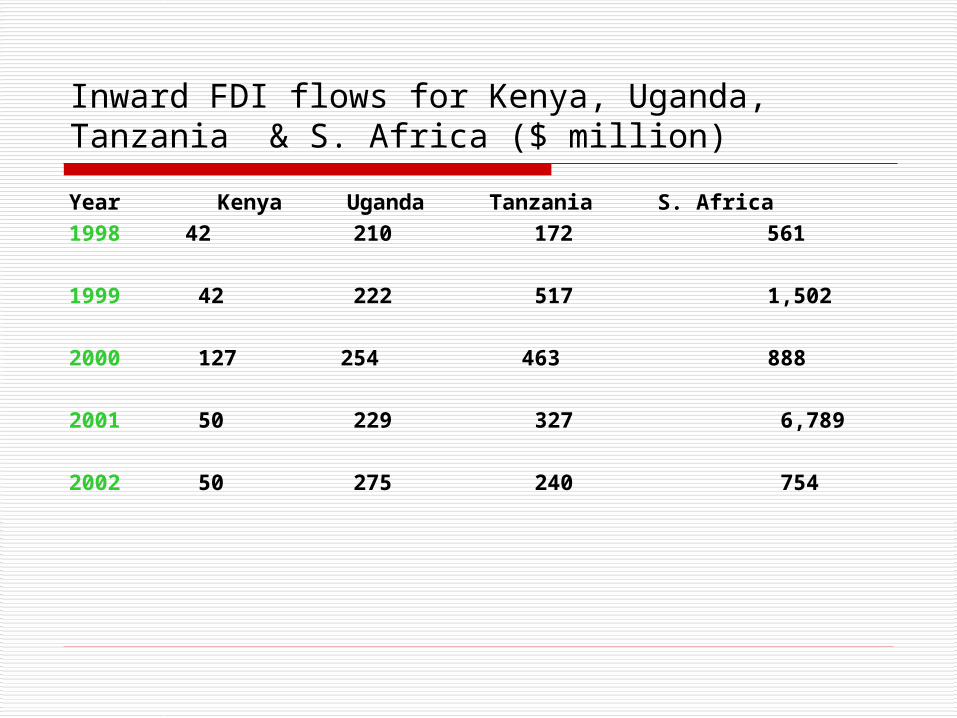

Inward FDI flows for Kenya, Uganda, Tanzania & S. Africa ($ million)Year Kenya Uganda Tanzania S. Africa1998 42 210 172 561

1999 42 222 517 1,502

2000 127 254 463 888

2001 50 229 327 6,789

2002 50 275 240 754

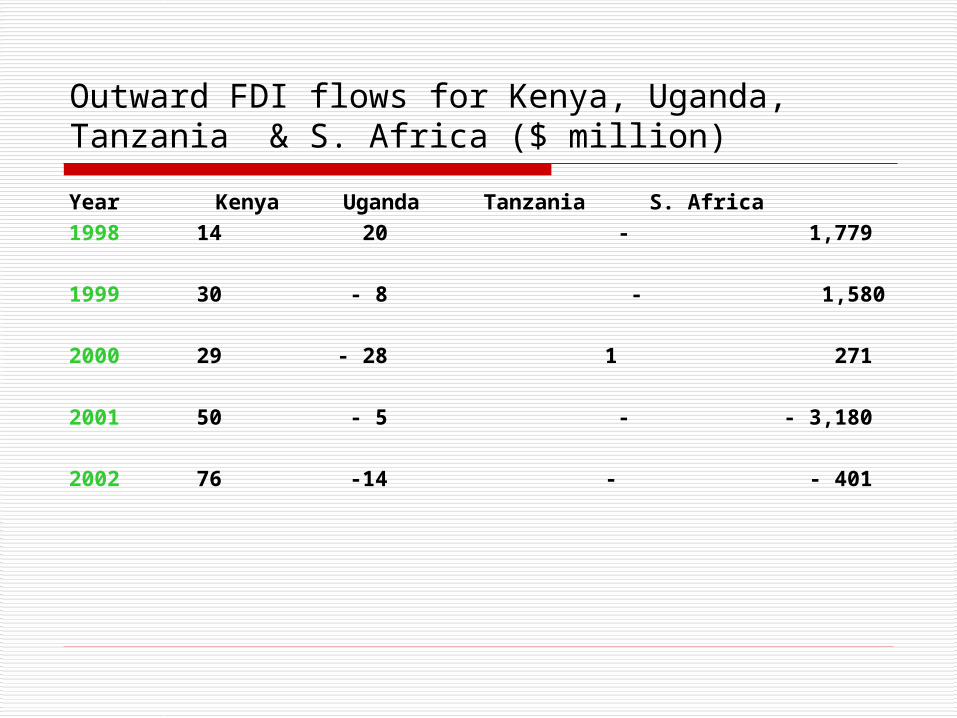

Outward FDI flows for Kenya, Uganda, Tanzania & S. Africa ($ million)Year Kenya Uganda Tanzania S. Africa1998 14 20 - 1,779

1999 30 - 8 - 1,580

2000 29 - 28 1 271

2001 50 - 5 - - 3,180

2002 76 -14 - - 401

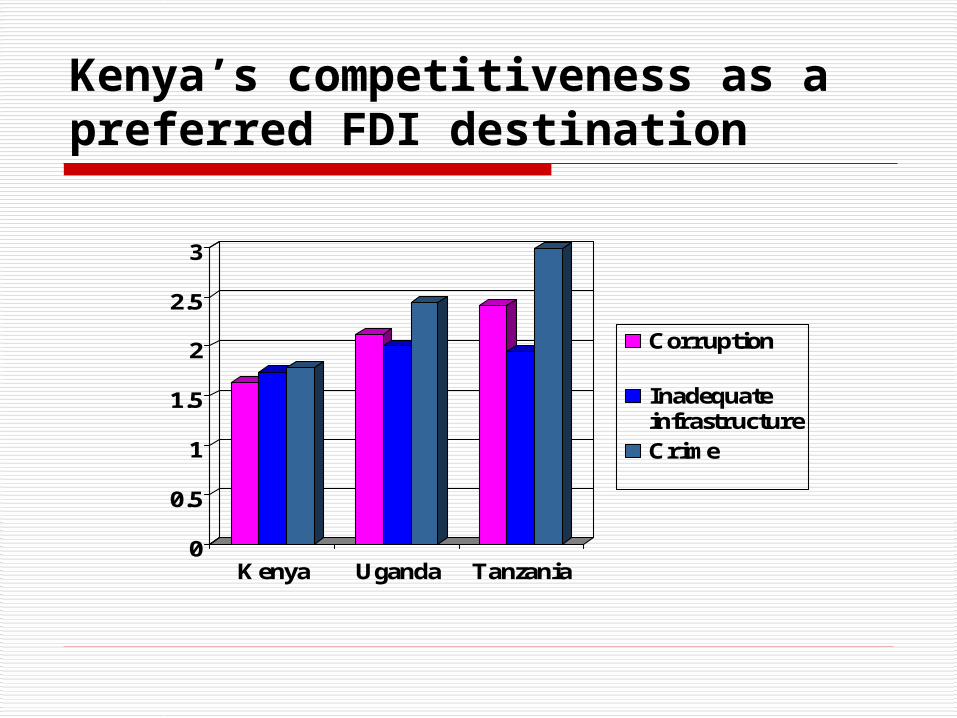

KENYA’S COMPETITIVENESS AS A PREFERRED FDI DESTINATION

( 1 ) denotes negative perception and( 4 ) denotes no impact on deciding investment destination

Kenya’s competitiveness as a preferred FDI destination

0

0.5

1

1.5

2

2.5

3

Kenya Uganda Tanzania

Corruption

InadequateinfrastructureCrime

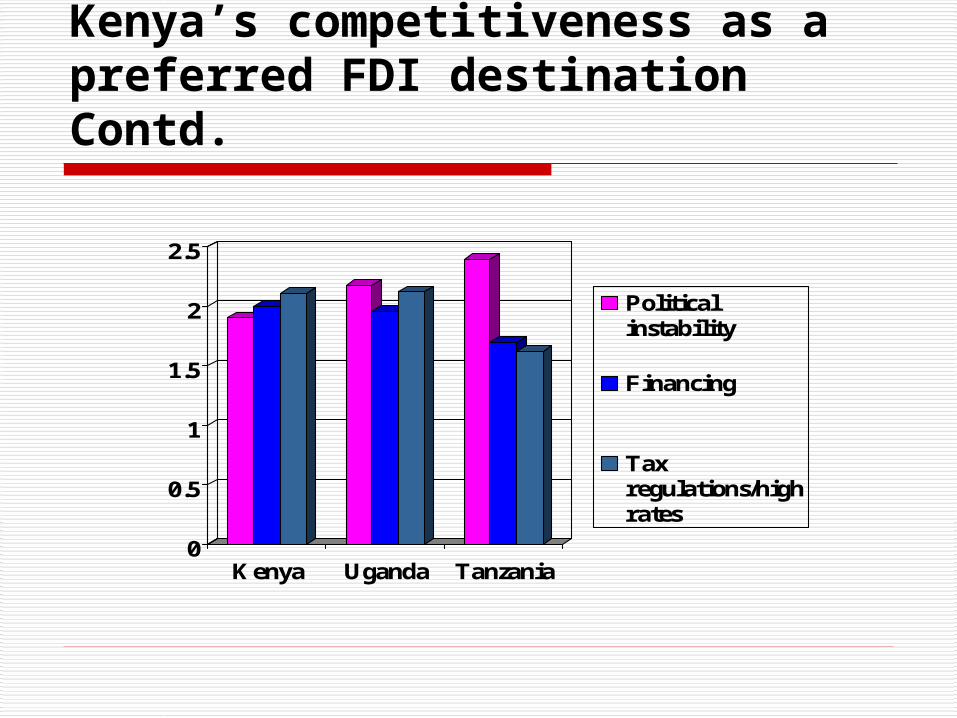

Kenya’s competitiveness as a preferred FDI destination Contd.

0

0.5

1

1.5

2

2.5

Kenya Uganda Tanzania

Politicalinstability

Financing

Taxregulations/highrates

Kenya’s competitiveness as a preferred FDI destination Contd.

0

0.5

1

1.5

2

2.5

3

Kenya Uganda Tanzania

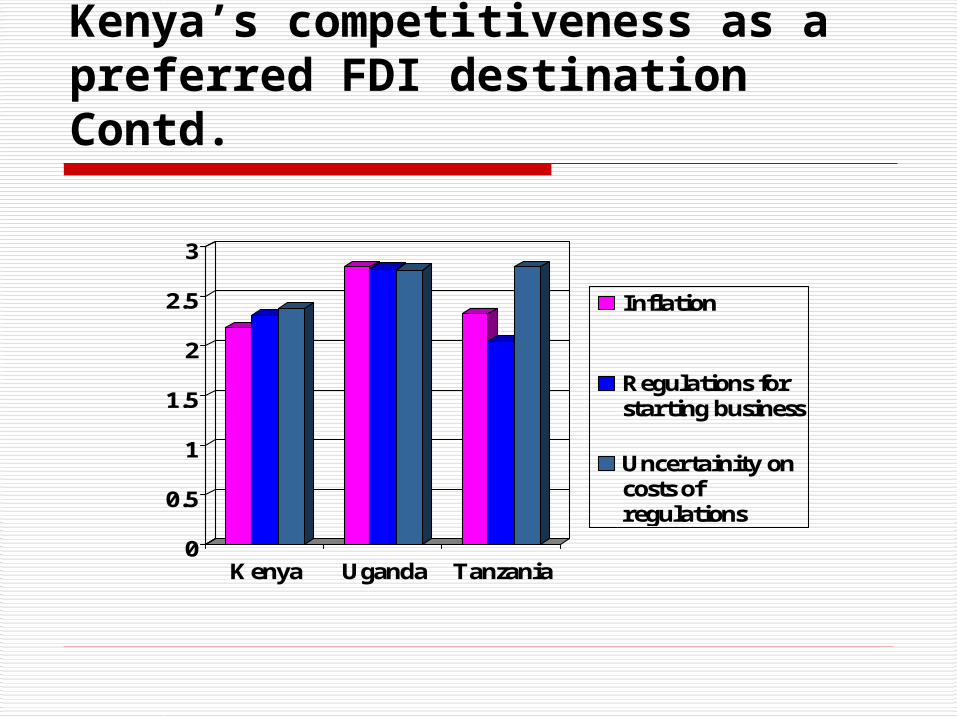

Inflation

Regulations forstarting business

Uncertainity oncosts ofregulations

Kenya’s competitiveness as a preferred FDI destination Contd.

0

0.5

1

1.5

2

2.5

3

3.5

4

Kenya Uganda Tanzania

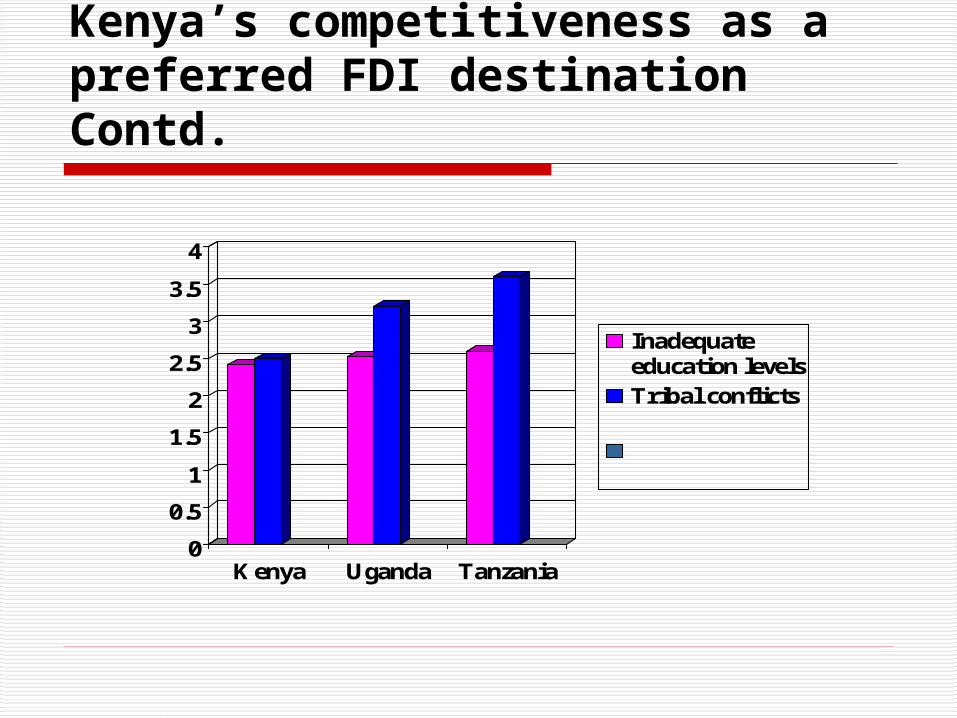

Inadequateeducation levelsTribal conflicts

Kenya’s competitiveness as a preferred FDI destination Contd.

0

0.5

1

1.5

2

2.5

3

3.5

Kenya Uganda Tanzania

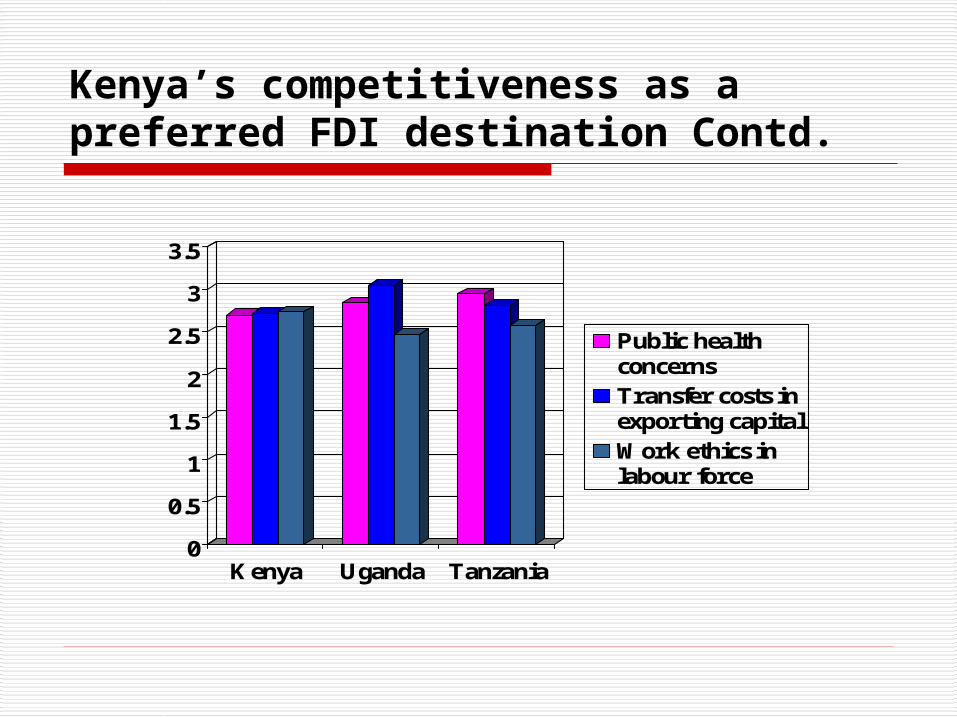

Public healthconcernsTransfer costs inexporting capitalWork ethics inlabour force

Kenya’s competitiveness as a preferred FDI destination Contd.

0

0.5

1

1.5

2

2.5

3

3.5

Kenya Uganda Tanzania

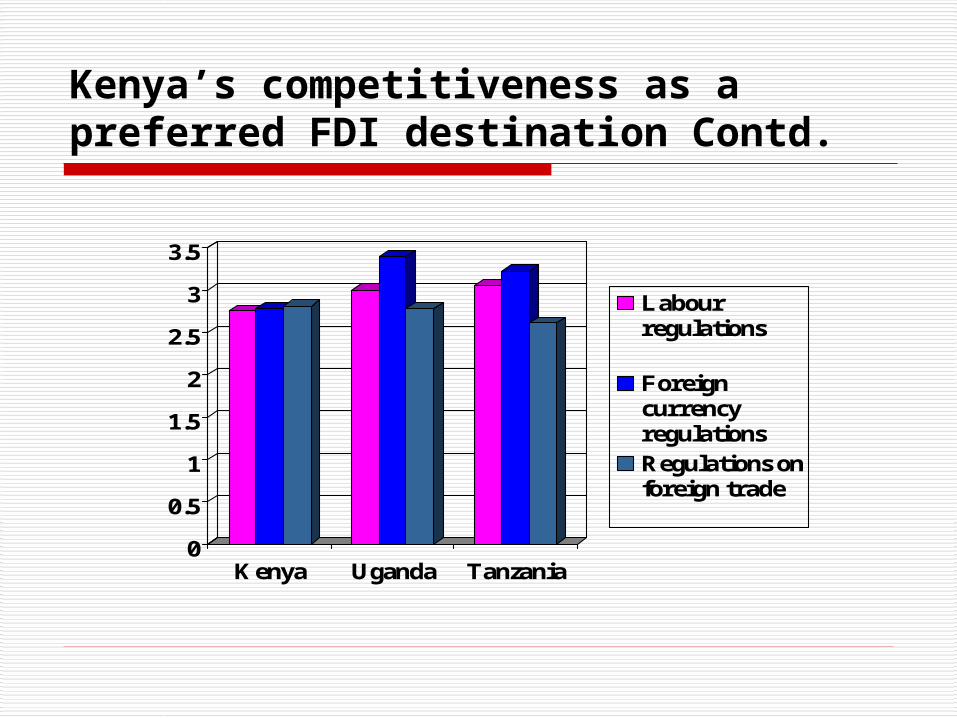

Labourregulations

ForeigncurrencyregulationsRegulations onforeign trade

Kenya’s competitiveness as a preferred FDI destination Contd.

2.32.42.52.62.72.82.9

33.13.2

Kenya Uganda Tanzania

Safety orenvironmentalregulationsPrice controls

Geographicallocation of thefirm

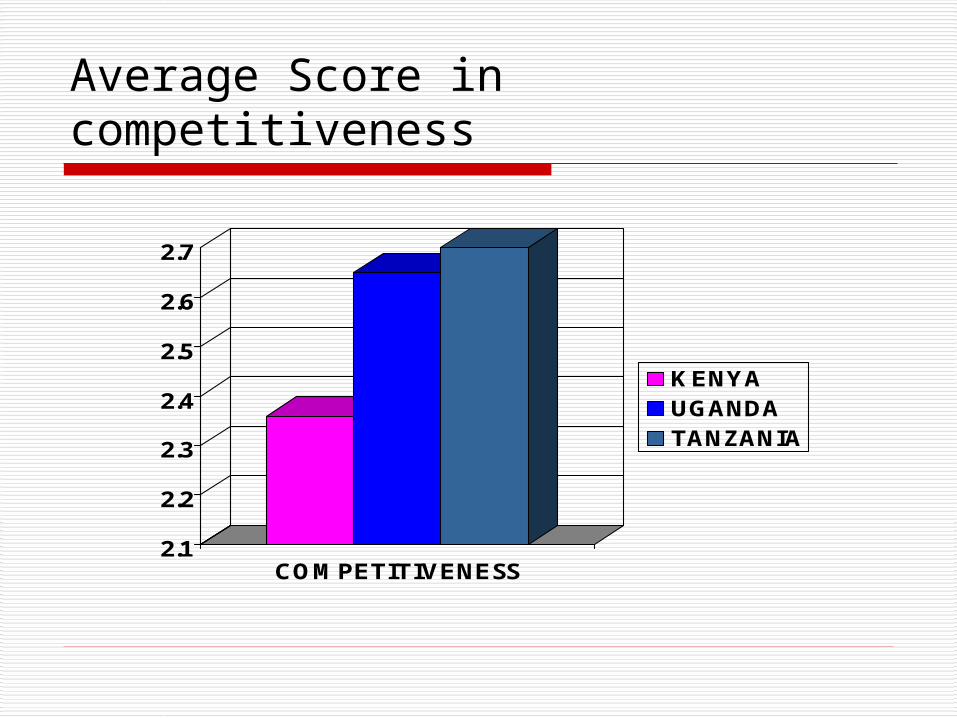

Average Score in competitiveness

2.1

2.2

2.3

2.4

2.5

2.6

2.7

COMPETITIVENESS

KENYAUGANDATANZANIA

CORPORATE TAX RATES (%) Kenya 30 China 30 Indonesia 30 Malaysia 28 Philippines 32 Thailand 30 Vietnam 25

TELECOMMUNICATIONSKENYA SELECTED COUNTRIES

US$/minute to US

Private landphone (Local calls 0-60 km)US$ 0.02 per minute

Trunk calls US$ 0.08 – 0.25 per minute International calls - USUS$ 1.25 per minute

Indonesia 1.00 Malaysia 0.24 Philippines

0.30 Thailand 0.56 China 0.25 Vietnam 1.30

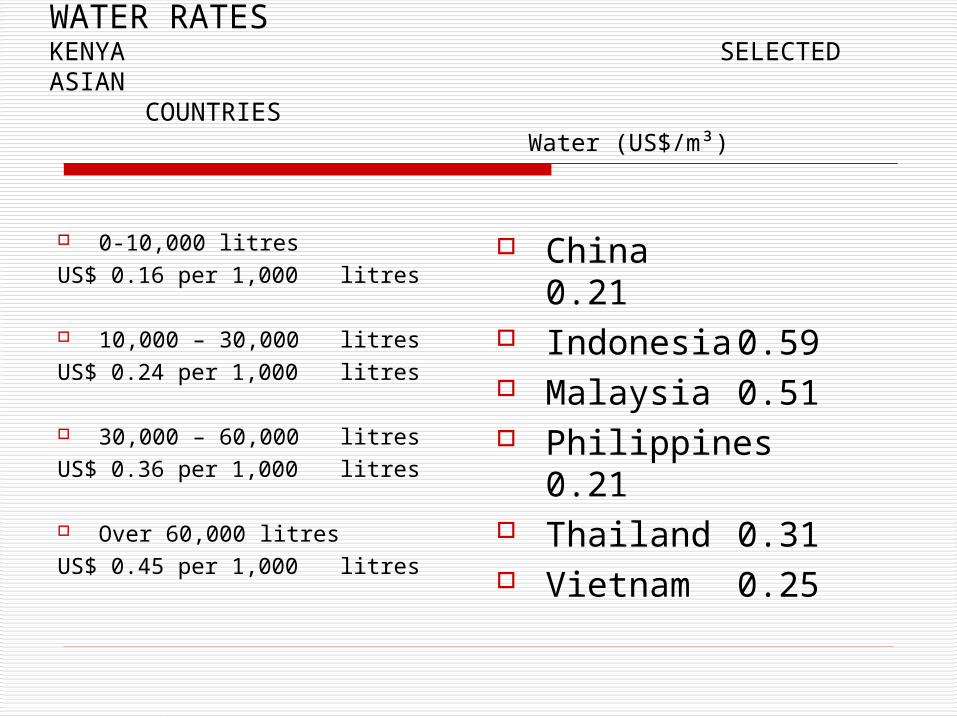

WATER RATESKENYA SELECTED ASIAN

COUNTRIESWater (US$/m³)

0-10,000 litres US$ 0.16 per 1,000 litres

10,000 – 30,000 litresUS$ 0.24 per 1,000 litres

30,000 – 60,000 litresUS$ 0.36 per 1,000 litres

Over 60,000 litresUS$ 0.45 per 1,000 litres

China 0.21

Indonesia 0.59 Malaysia 0.51 Philippines

0.21 Thailand 0.31 Vietnam 0.25

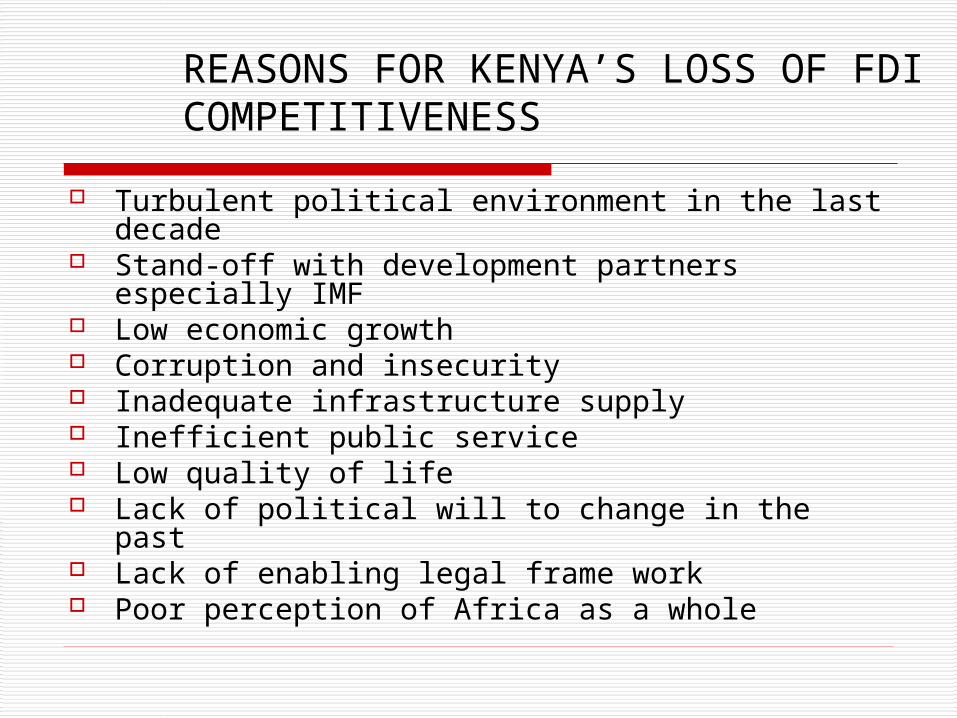

REASONS FOR KENYA’S LOSS OF FDI COMPETITIVENESS

Turbulent political environment in the last decade

Stand-off with development partners especially IMF

Low economic growth Corruption and insecurity Inadequate infrastructure supply Inefficient public service Low quality of life Lack of political will to change in the past Lack of enabling legal frame work Poor perception of Africa as a whole

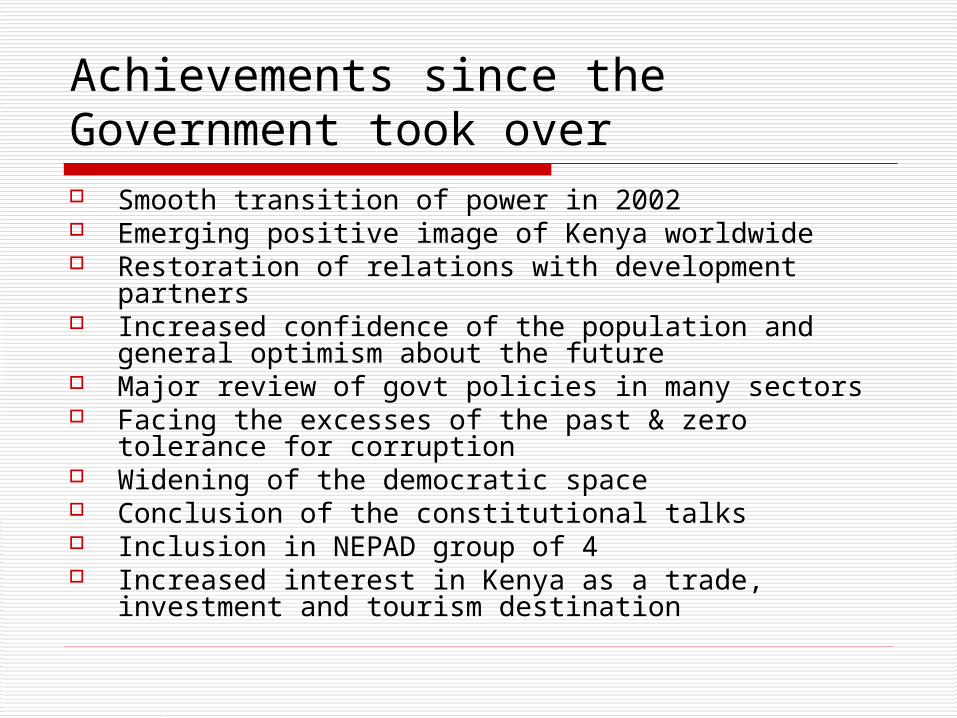

Achievements since the Government took over Smooth transition of power in 2002 Emerging positive image of Kenya worldwide Restoration of relations with development partners Increased confidence of the population and general

optimism about the future Major review of govt policies in many sectors Facing the excesses of the past & zero tolerance for

corruption Widening of the democratic space Conclusion of the constitutional talks Inclusion in NEPAD group of 4 Increased interest in Kenya as a trade, investment

and tourism destination

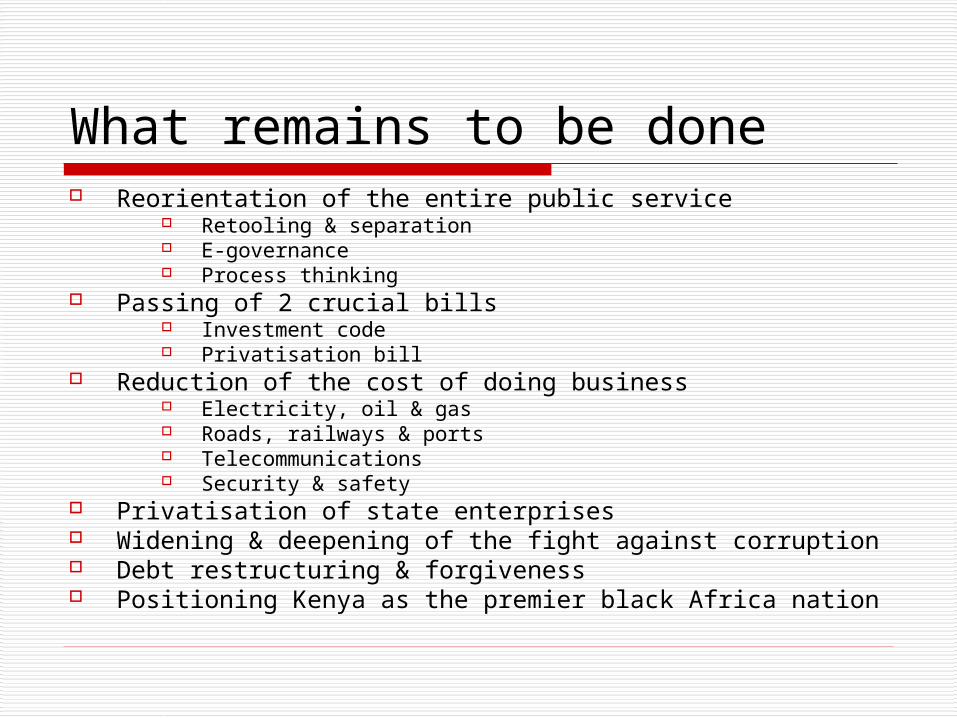

What remains to be done Reorientation of the entire public service

Retooling & separation E-governance Process thinking

Passing of 2 crucial bills Investment code Privatisation bill

Reduction of the cost of doing business Electricity, oil & gas Roads, railways & ports Telecommunications Security & safety

Privatisation of state enterprises Widening & deepening of the fight against corruption Debt restructuring & forgiveness Positioning Kenya as the premier black Africa nation