portuguese competitiveness - harvard business … files/caon portugal 04-10-02 ck2...portuguese...

TRANSCRIPT

1

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter1

Portuguese Competitiveness

Professor Michael E. PorterInstitute for Strategy and Competitiveness

Harvard Business School

Novos Desafiois da CompetitividadeLisbon, PortugalApril 17th, 2002

This presentation draws on ideas from Professor Porter’s articles and books, in particular, The Competitive Advantage of Nations (The Free Press, 1990), “The Microeconomic Foundations of Economic Development,” in The Global Competitiveness Report 2001/02, (World Economic Forum, 1998), “Clusters and the New Competitive Agenda for Companies and Governments” in On Competition (Harvard Business School Press, 1998), ongoing statistical study of clusters, and “What is Strategy?” (Harvard Business Review, Nov/Dec 1996). For further information please check the Institute’s web site at www.isc.hbs.edu. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means - electronic, mechanical, photocopying, recording, or otherwise - without the permission of Michael E. Porter.

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter2

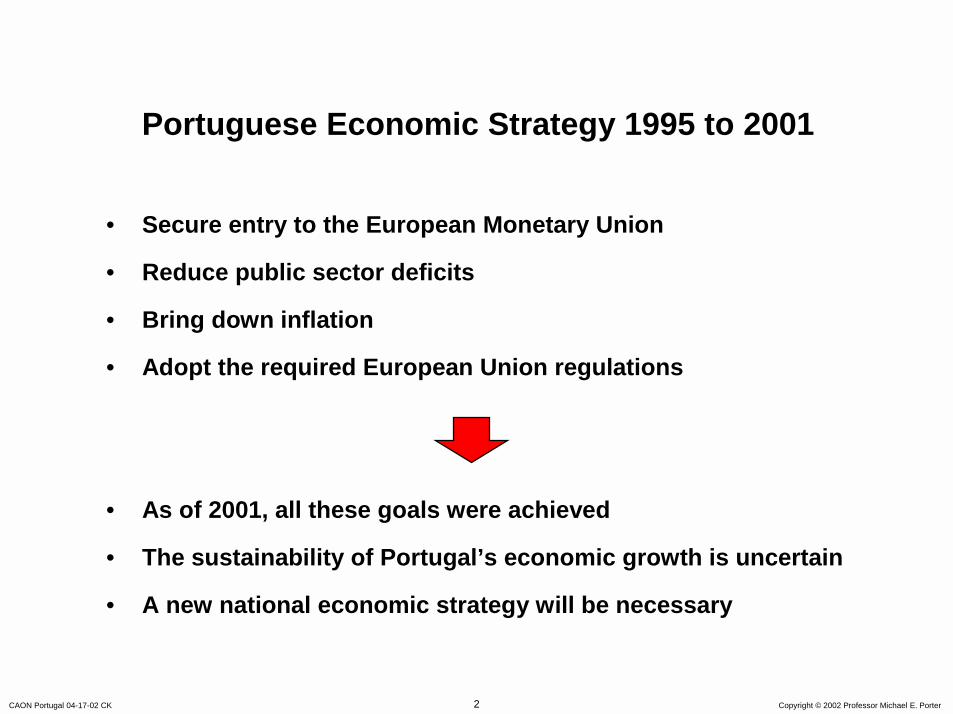

Portuguese Economic Strategy 1995 to 2001

• Secure entry to the European Monetary Union

• Reduce public sector deficits

• Bring down inflation

• Adopt the required European Union regulations

• As of 2001, all these goals were achieved

• The sustainability of Portugal’s economic growth is uncertain

• A new national economic strategy will be necessary

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter3

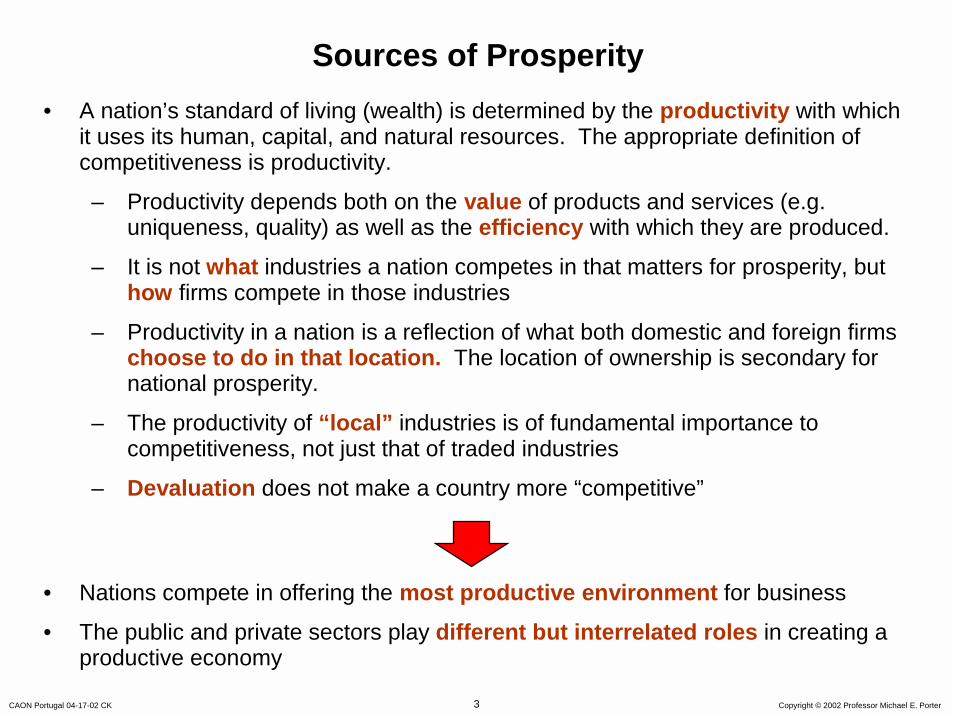

Sources of Prosperity• A nation’s standard of living (wealth) is determined by the productivity with which

it uses its human, capital, and natural resources. The appropriate definition of competitiveness is productivity.

– Productivity depends both on the value of products and services (e.g. uniqueness, quality) as well as the efficiency with which they are produced.

– It is not what industries a nation competes in that matters for prosperity, buthow firms compete in those industries

– Productivity in a nation is a reflection of what both domestic and foreign firms choose to do in that location. The location of ownership is secondary for national prosperity.

– The productivity of “local” industries is of fundamental importance to competitiveness, not just that of traded industries

– Devaluation does not make a country more “competitive”

• Nations compete in offering the most productive environment for business

• The public and private sectors play different but interrelated roles in creating a productive economy

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter4

Microeconomic Foundations of DevelopmentMicroeconomic Foundations of Development

Quality of the Microeconomic

BusinessEnvironment

Quality of the Microeconomic

BusinessEnvironment

Sophisticationof Company

Operations andStrategy

Sophisticationof Company

Operations andStrategy

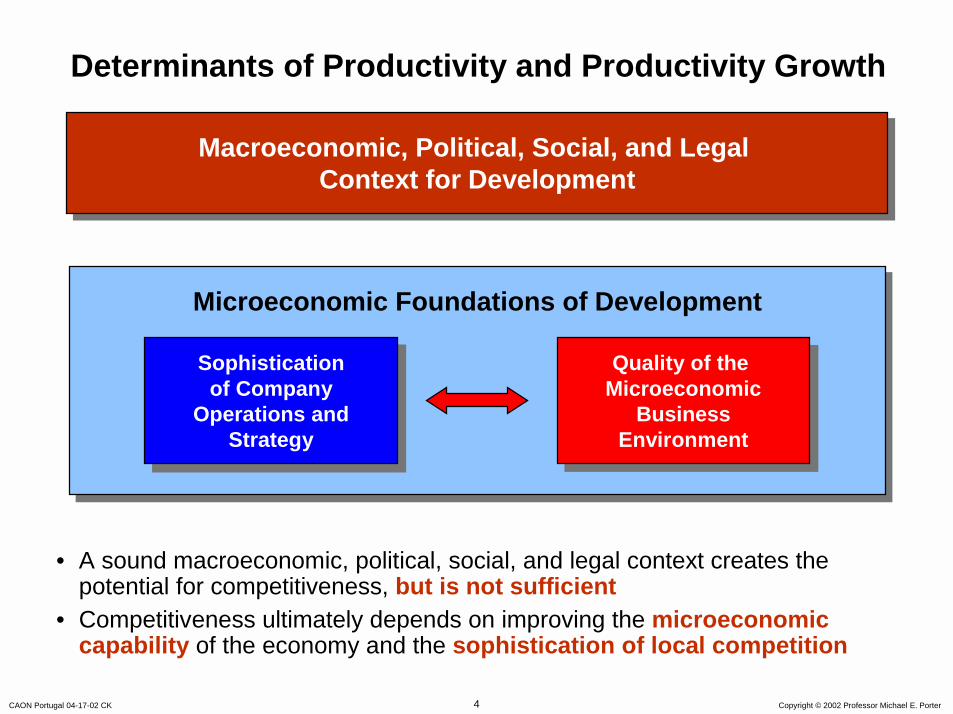

Determinants of Productivity and Productivity Growth

Macroeconomic, Political, Social, and Legal Context for Development

Macroeconomic, Political, Social, and Legal Context for Development

• A sound macroeconomic, political, social, and legal context creates the potential for competitiveness, but is not sufficient

• Competitiveness ultimately depends on improving the microeconomic capability of the economy and the sophistication of local competition

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter5

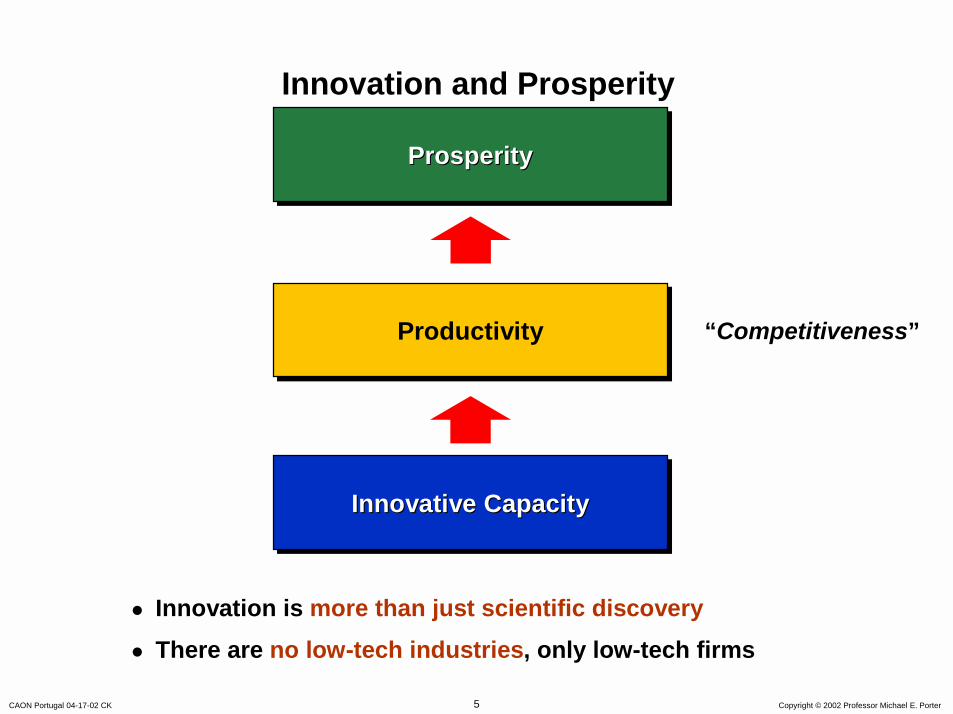

Innovation and Prosperity

ProductivityProductivity

Innovative CapacityInnovative CapacityInnovative Capacity

ProsperityProsperityProsperity

! Innovation is more than just scientific discovery! There are no low-tech industries, only low-tech firms

“Competitiveness”

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter6

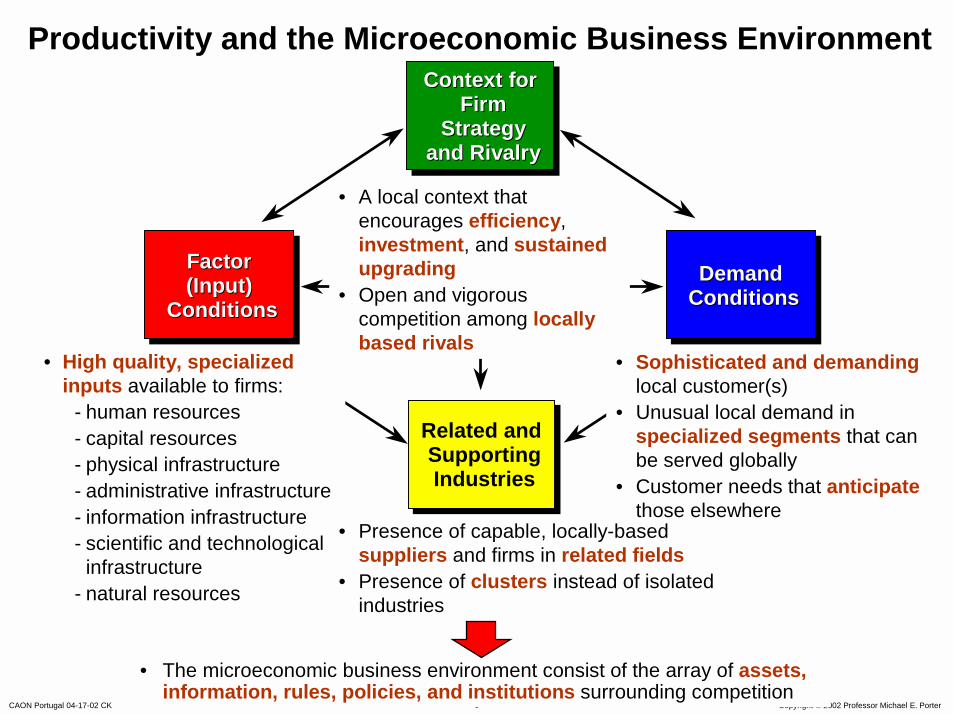

Context for Firm

Strategy and Rivalry

Context for Context for Firm Firm

Strategy Strategy and Rivalryand Rivalry

Related and Supporting Industries

Related and Supporting Industries

Factor(Input)

Conditions

FactorFactor(Input) (Input)

ConditionsConditions

• A local context that encourages efficiency,investment, and sustained upgrading

• Open and vigorous competition among locally based rivals

Demand ConditionsDemand Demand

ConditionsConditions

Productivity and the Microeconomic Business Environment

• The microeconomic business environment consist of the array of assets, information, rules, policies, and institutions surrounding competition

• Sophisticated and demandinglocal customer(s)

• Unusual local demand in specialized segments that can be served globally

• Customer needs that anticipatethose elsewhere

• High quality, specialized inputs available to firms:

- human resources- capital resources- physical infrastructure- administrative infrastructure- information infrastructure- scientific and technological

infrastructure- natural resources

• Presence of capable, locally-based suppliers and firms in related fields

• Presence of clusters instead of isolated industries

7

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter7

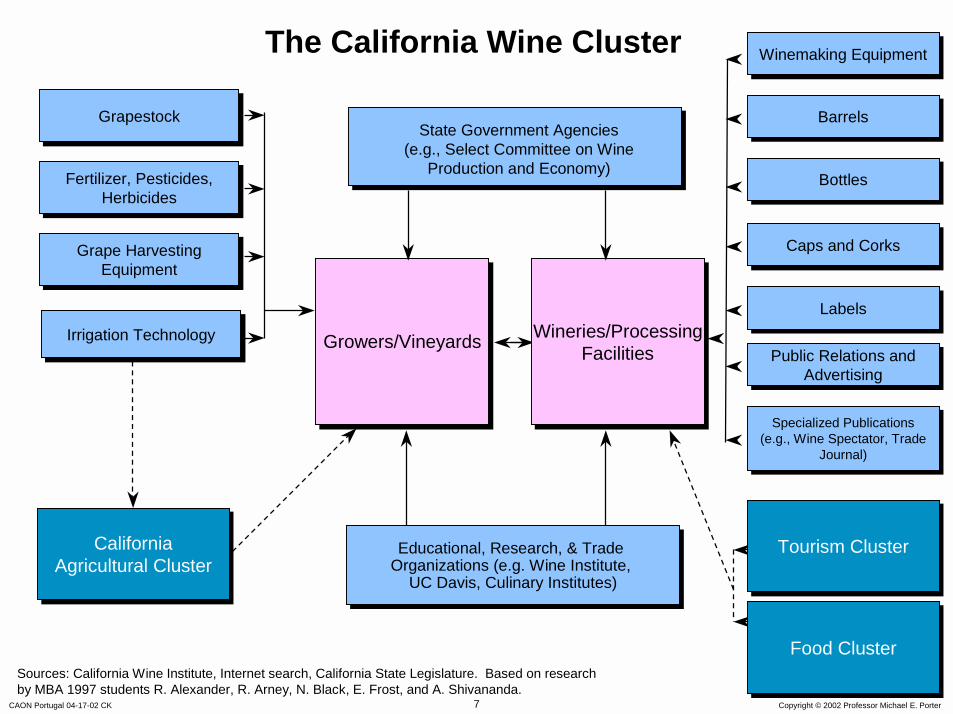

The California Wine Cluster

Educational, Research, & Trade Organizations (e.g. Wine Institute,

UC Davis, Culinary Institutes)

Educational, Research, & Trade Organizations (e.g. Wine Institute,

UC Davis, Culinary Institutes)

Growers/VineyardsGrowers/Vineyards

Sources: California Wine Institute, Internet search, California State Legislature. Based on research by MBA 1997 students R. Alexander, R. Arney, N. Black, E. Frost, and A. Shivananda.

Wineries/ProcessingFacilities

Wineries/ProcessingFacilities

GrapestockGrapestock

Fertilizer, Pesticides, Herbicides

Fertilizer, Pesticides, Herbicides

Grape Harvesting Equipment

Grape Harvesting Equipment

Irrigation TechnologyIrrigation Technology

Winemaking EquipmentWinemaking Equipment

BarrelsBarrels

LabelsLabels

BottlesBottles

Caps and CorksCaps and Corks

Public Relations and Advertising

Public Relations and Advertising

Specialized Publications (e.g., Wine Spectator, Trade

Journal)

Specialized Publications (e.g., Wine Spectator, Trade

Journal)

Food ClusterFood Cluster

Tourism ClusterTourism ClusterCalifornia Agricultural Cluster

California Agricultural Cluster

State Government Agencies(e.g., Select Committee on Wine

Production and Economy)

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter8

Agenda

• Portugal’s economic performance

• Portugal’s competitiveness

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter9

0

5,000

10,000

15,000

20,000

25,000

0%

2%

4%

6%

8%

10%

12%

14%

Hungary Slovenia Greece S Korea Portugal Spain NewZealand

Israel Taiwan

1990-19951995-2000

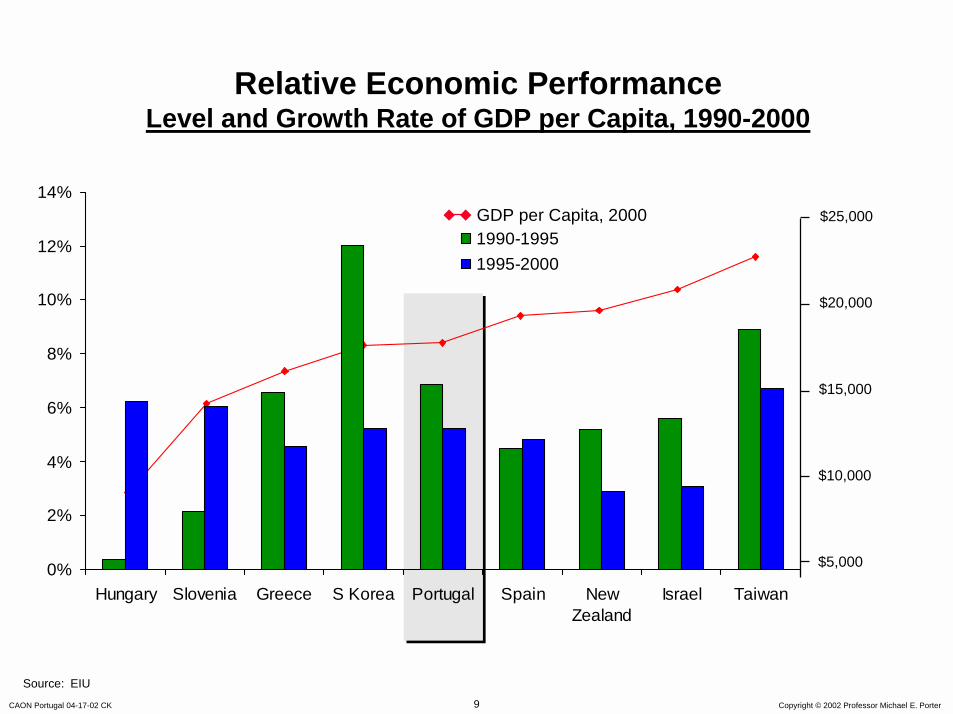

Relative Economic PerformanceLevel and Growth Rate of GDP per Capita, 1990-2000

$25,000

$20,000

$15,000

$10,000

$5,000

GDP per Capita, 2000

Source: EIU

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter10

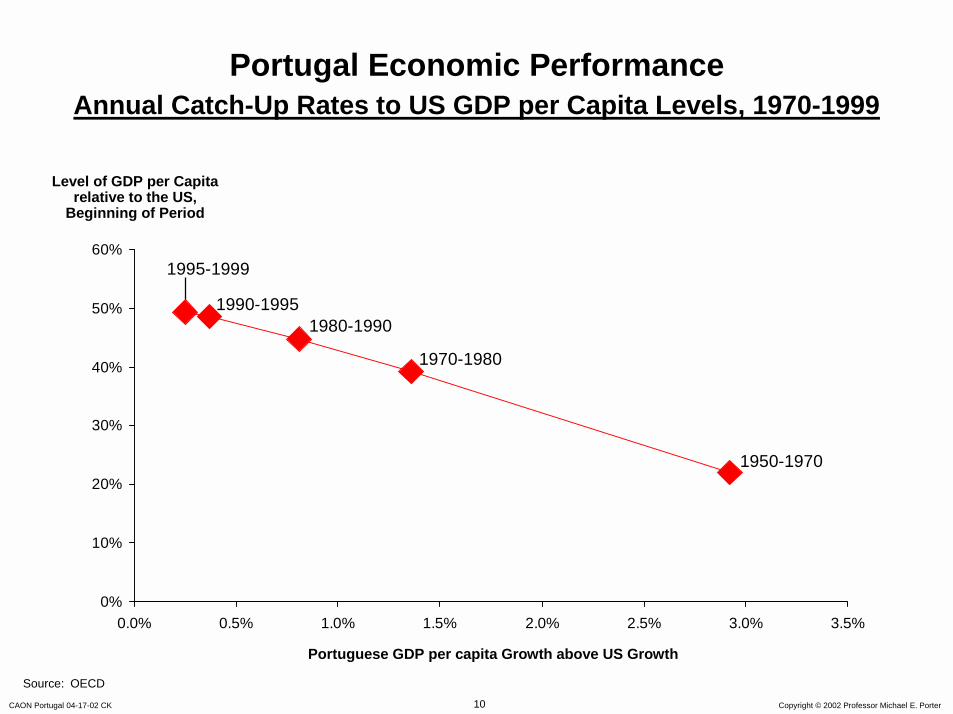

Portugal Economic PerformanceAnnual Catch-Up Rates to US GDP per Capita Levels, 1970-1999

0%

10%

20%

30%

40%

50%

60%

0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5%

Source: OECD

Portuguese GDP per capita Growth above US Growth

Level of GDP per Capita relative to the US,

Beginning of Period

1950-1970

1970-1980

1980-19901990-1995

1995-1999

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter11

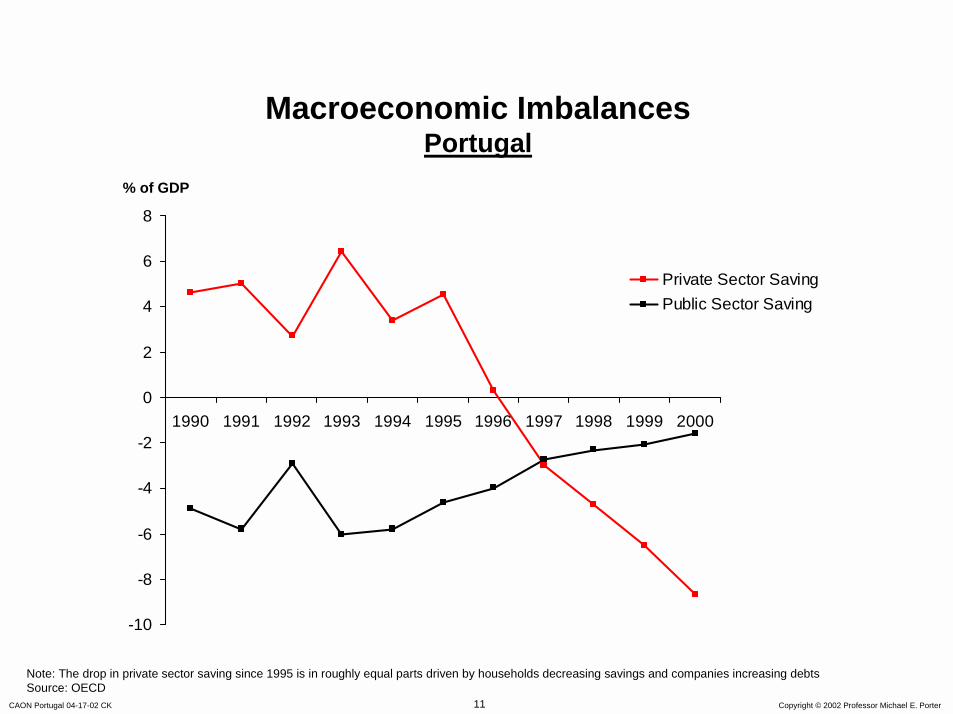

Macroeconomic ImbalancesPortugal

-10

-8

-6

-4

-2

0

2

4

6

8

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000

Private Sector SavingPublic Sector Saving

% of GDP

Note: The drop in private sector saving since 1995 is in roughly equal parts driven by households decreasing savings and companies increasing debtsSource: OECD

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter12

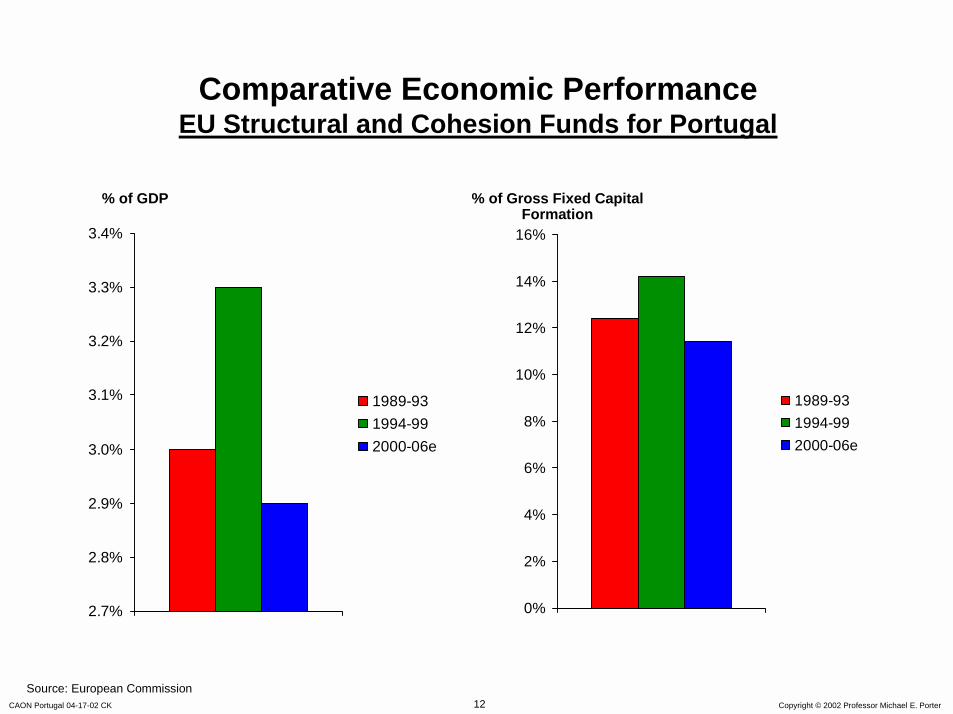

Comparative Economic PerformanceEU Structural and Cohesion Funds for Portugal

2.7%

2.8%

2.9%

3.0%

3.1%

3.2%

3.3%

3.4%

1989-931994-992000-06e

% of GDP

Source: European Commission

0%

2%

4%

6%

8%

10%

12%

14%

16%

1989-931994-992000-06e

% of Gross Fixed Capital Formation

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter13

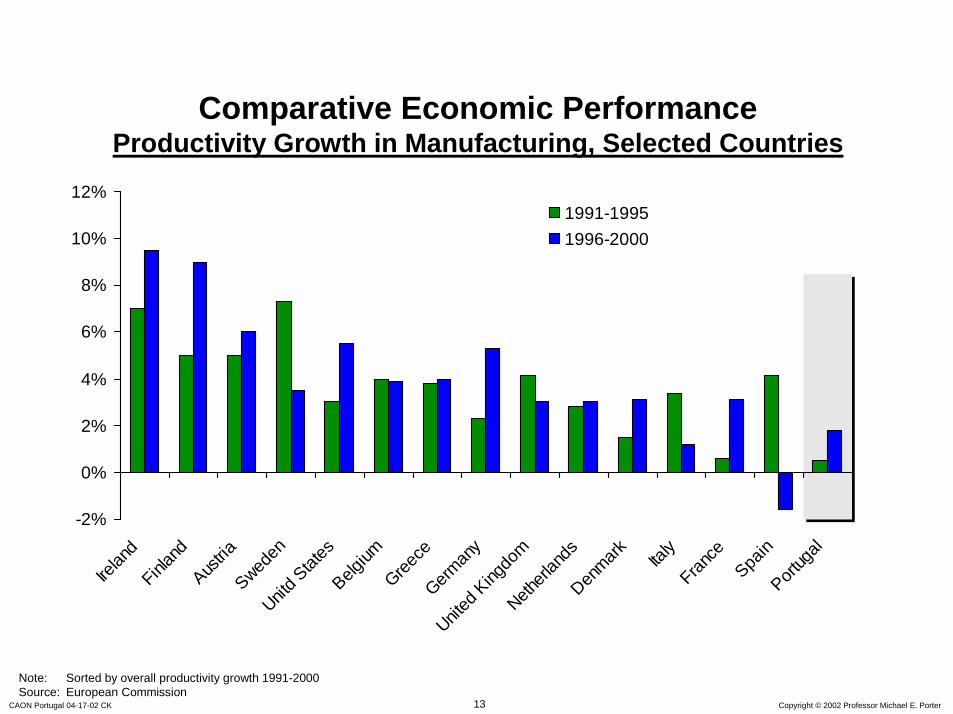

Comparative Economic PerformanceProductivity Growth in Manufacturing, Selected Countries

-2%

0%

2%

4%

6%

8%

10%

12%

Irelan

dFinla

ndAus

triaSwed

enUnit

d Stat

esBelg

iumGree

ceGerm

any

United

Kingdo

mNeth

erlan

dsDen

mark Italy

France

Spain

Portug

al

1991-19951996-2000

Note: Sorted by overall productivity growth 1991-2000Source: European Commission

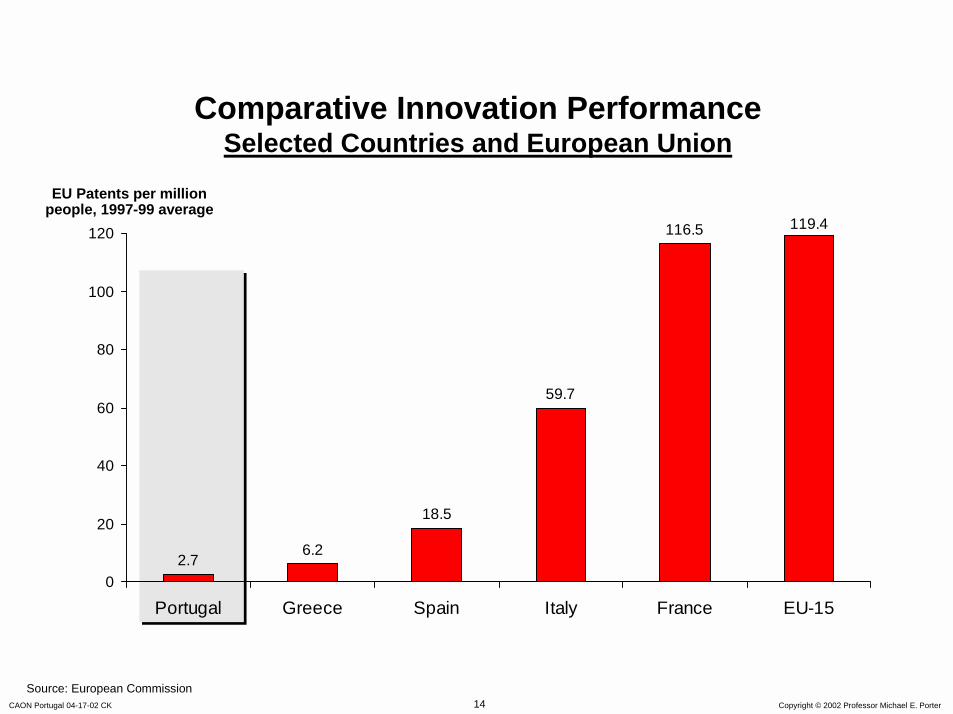

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter14

Comparative Innovation PerformanceSelected Countries and European Union

2.76.2

18.5

59.7

116.5 119.4

0

20

40

60

80

100

120

Portugal Greece Spain Italy France EU-15

EU Patents per million people, 1997-99 average

Source: European Commission

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter15

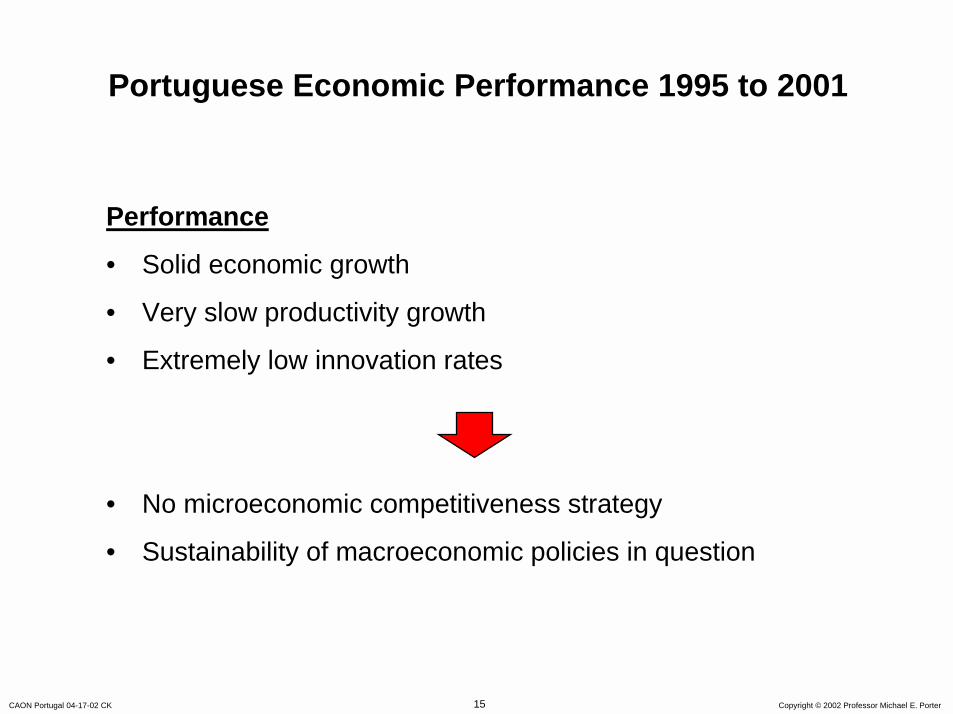

Portuguese Economic Performance 1995 to 2001

Performance

• Solid economic growth

• Very slow productivity growth

• Extremely low innovation rates

• No microeconomic competitiveness strategy

• Sustainability of macroeconomic policies in question

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter16

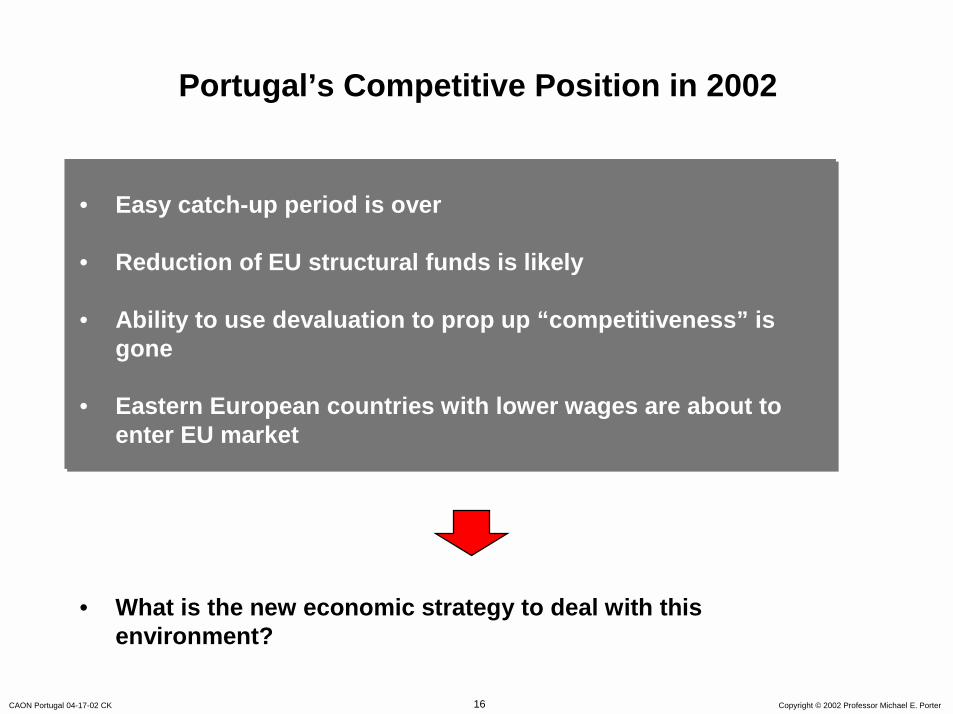

Portugal’s Competitive Position in 2002

• Easy catch-up period is over

• Reduction of EU structural funds is likely

• Ability to use devaluation to prop up “competitiveness” is gone

• Eastern European countries with lower wages are about to enter EU market

• What is the new economic strategy to deal with this environment?

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter17

Agenda

• Portugal’s economic performance

• Portugal’s competitiveness

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter18

Context for Firm

Strategy and Rivalry

Context for Context for Firm Firm

Strategy Strategy and Rivalryand Rivalry

Related and Supporting Industries

Related and Supporting Industries

Factor(Input)

Conditions

FactorFactor(Input) (Input)

ConditionsConditions

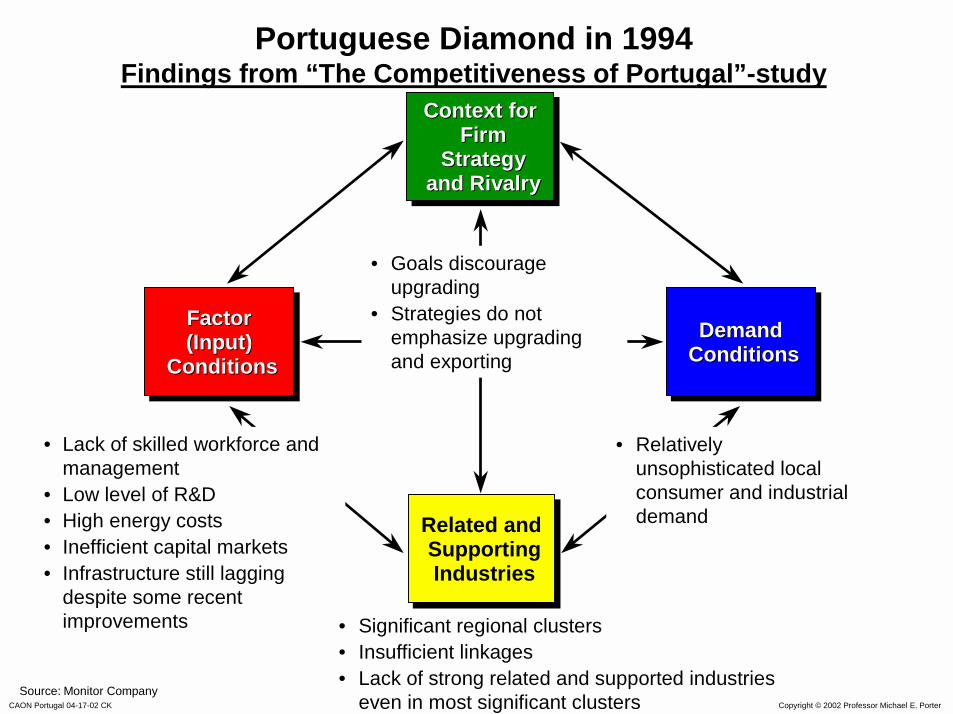

• Relatively unsophisticated local consumer and industrial demand

• Goals discourage upgrading

• Strategies do not emphasize upgrading and exporting

Demand ConditionsDemand Demand

ConditionsConditions

• Lack of skilled workforce and management

• Low level of R&D• High energy costs• Inefficient capital markets• Infrastructure still lagging

despite some recent improvements

Portuguese Diamond in 1994Findings from “The Competitiveness of Portugal”-study

Source: Monitor Company

• Significant regional clusters• Insufficient linkages• Lack of strong related and supported industries

even in most significant clusters

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter19

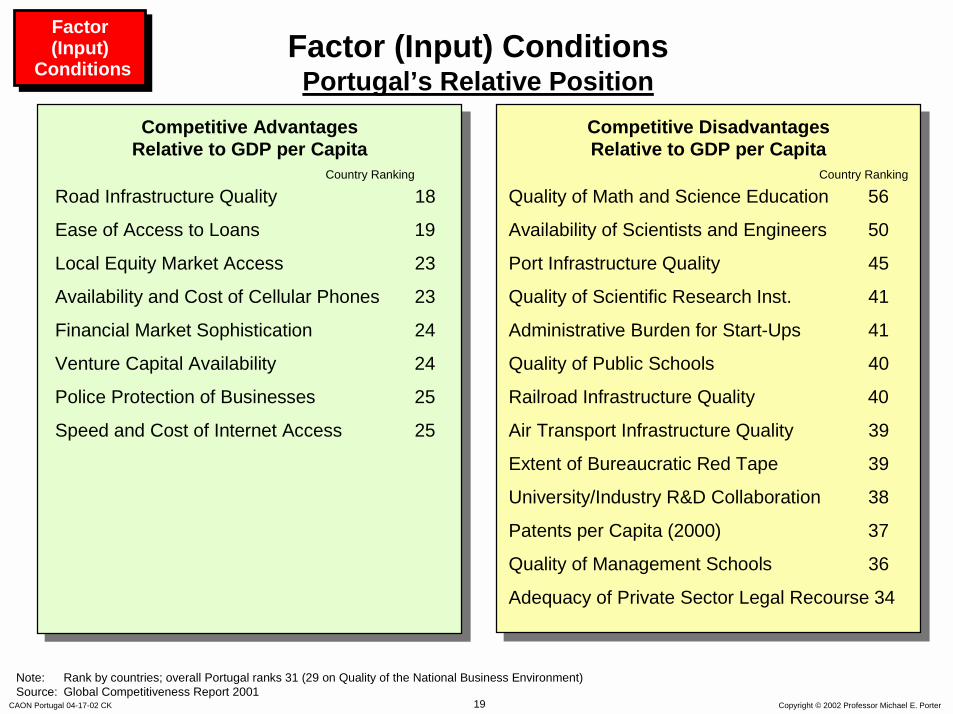

Factor (Input) ConditionsPortugal’s Relative Position

Factor(Input)

Conditions

Factor(Input)

Conditions

Road Infrastructure Quality 18

Ease of Access to Loans 19

Local Equity Market Access 23

Availability and Cost of Cellular Phones 23

Financial Market Sophistication 24

Venture Capital Availability 24

Police Protection of Businesses 25

Speed and Cost of Internet Access 25

Competitive Disadvantages Relative to GDP per Capita

Competitive Advantages Relative to GDP per Capita

Country RankingCountry Ranking

Note: Rank by countries; overall Portugal ranks 31 (29 on Quality of the National Business Environment)Source: Global Competitiveness Report 2001

Quality of Math and Science Education 56

Availability of Scientists and Engineers 50

Port Infrastructure Quality 45

Quality of Scientific Research Inst. 41

Administrative Burden for Start-Ups 41

Quality of Public Schools 40

Railroad Infrastructure Quality 40

Air Transport Infrastructure Quality 39

Extent of Bureaucratic Red Tape 39

University/Industry R&D Collaboration 38

Patents per Capita (2000) 37

Quality of Management Schools 36

Adequacy of Private Sector Legal Recourse 34

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter20

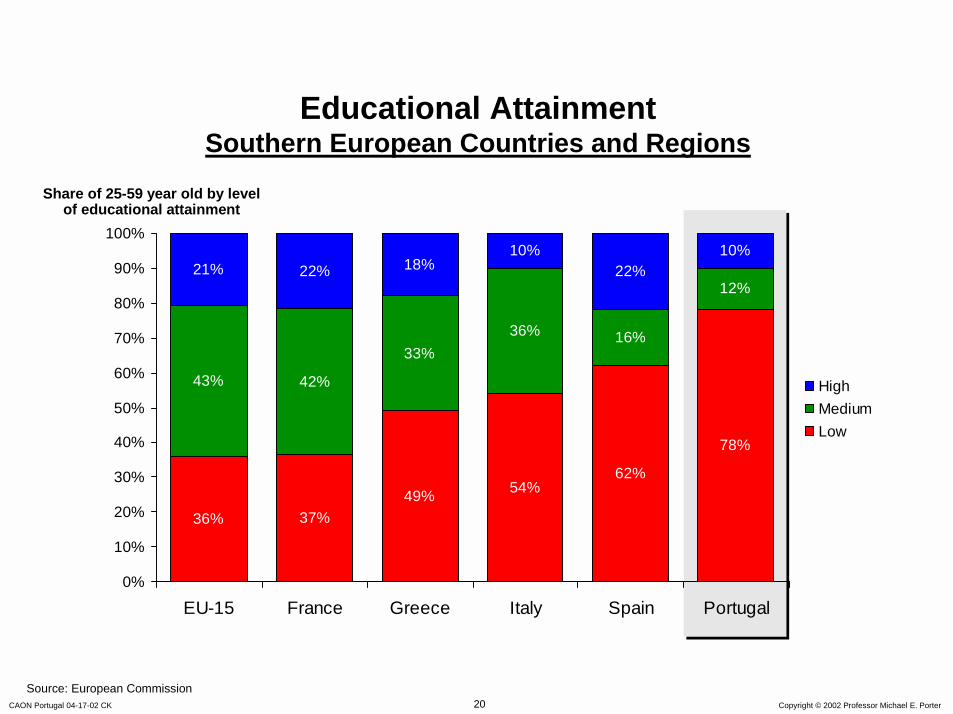

Educational AttainmentSouthern European Countries and Regions

36% 37%49% 54%

62%

78%

43% 42%

33%36% 16%

12%21% 22% 18%

10%22%

10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

EU-15 France Greece Italy Spain Portugal

HighMediumLow

Share of 25-59 year old by level of educational attainment

Source: European Commission

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter21

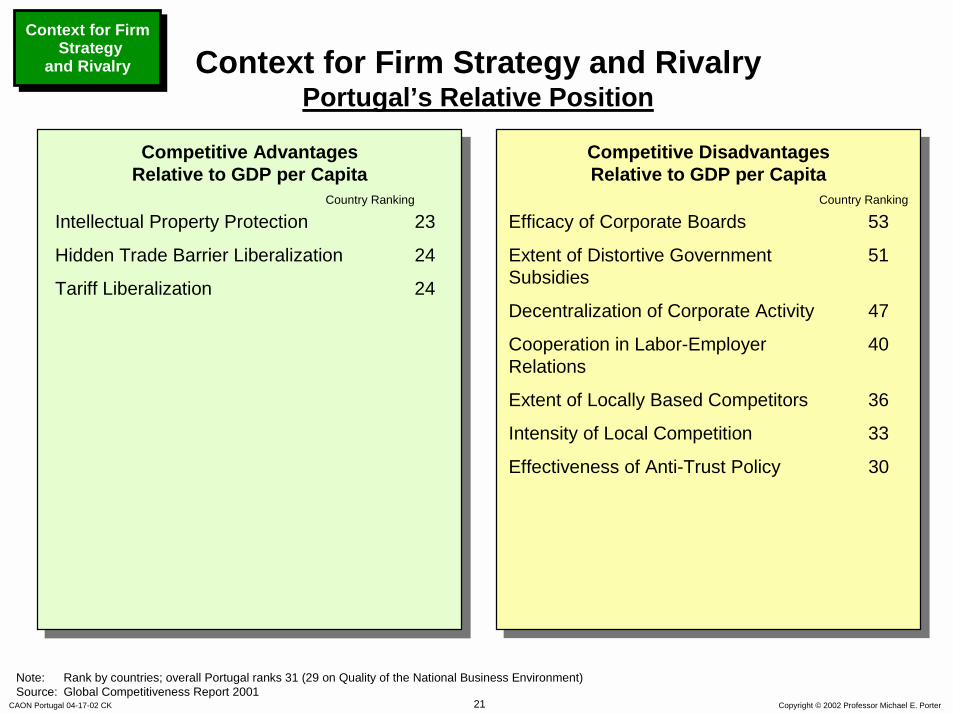

Context for Firm Strategy and RivalryPortugal’s Relative Position

Intellectual Property Protection 23

Hidden Trade Barrier Liberalization 24

Tariff Liberalization 24

Competitive Disadvantages Relative to GDP per Capita

Competitive Advantages Relative to GDP per Capita

Country RankingCountry Ranking

Note: Rank by countries; overall Portugal ranks 31 (29 on Quality of the National Business Environment)Source: Global Competitiveness Report 2001

Efficacy of Corporate Boards 53

Extent of Distortive Government 51Subsidies

Decentralization of Corporate Activity 47

Cooperation in Labor-Employer 40Relations

Extent of Locally Based Competitors 36

Intensity of Local Competition 33

Effectiveness of Anti-Trust Policy 30

Context for Firm Strategy

and Rivalry

Context for Firm Strategy

and Rivalry

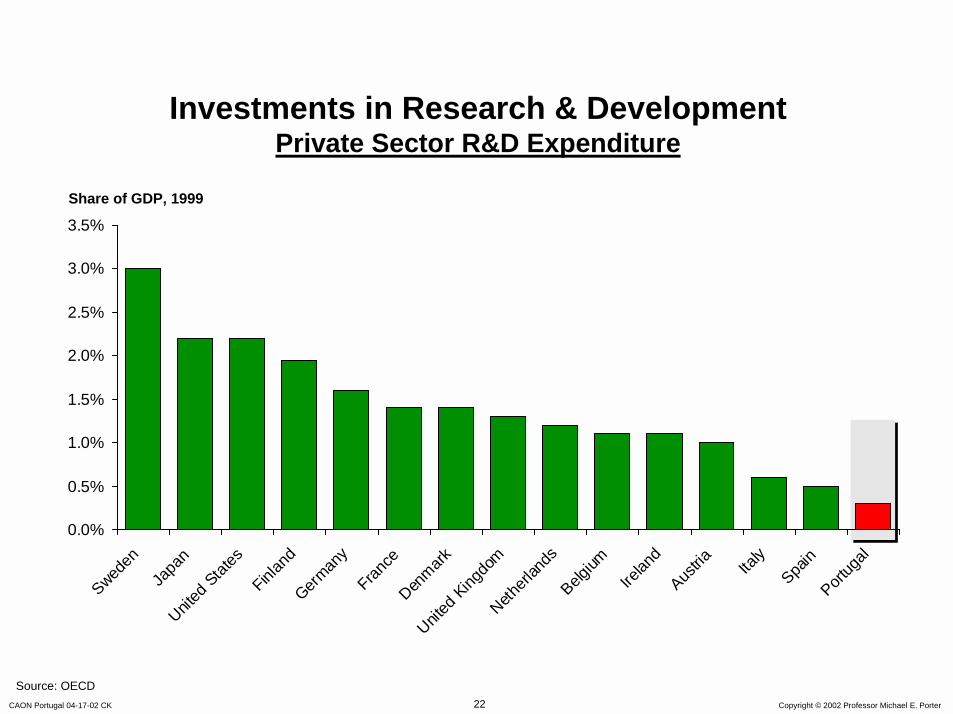

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter22

Investments in Research & DevelopmentPrivate Sector R&D Expenditure

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

Sweden

Japa

nUnit

ed Stat

esFinl

and

German

yFran

ceDen

markUnit

ed King

dom

Netherl

ands

Belgium

Irelan

dAus

tria Italy

Spain

Portug

al

Share of GDP, 1999

Source: OECD

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter23

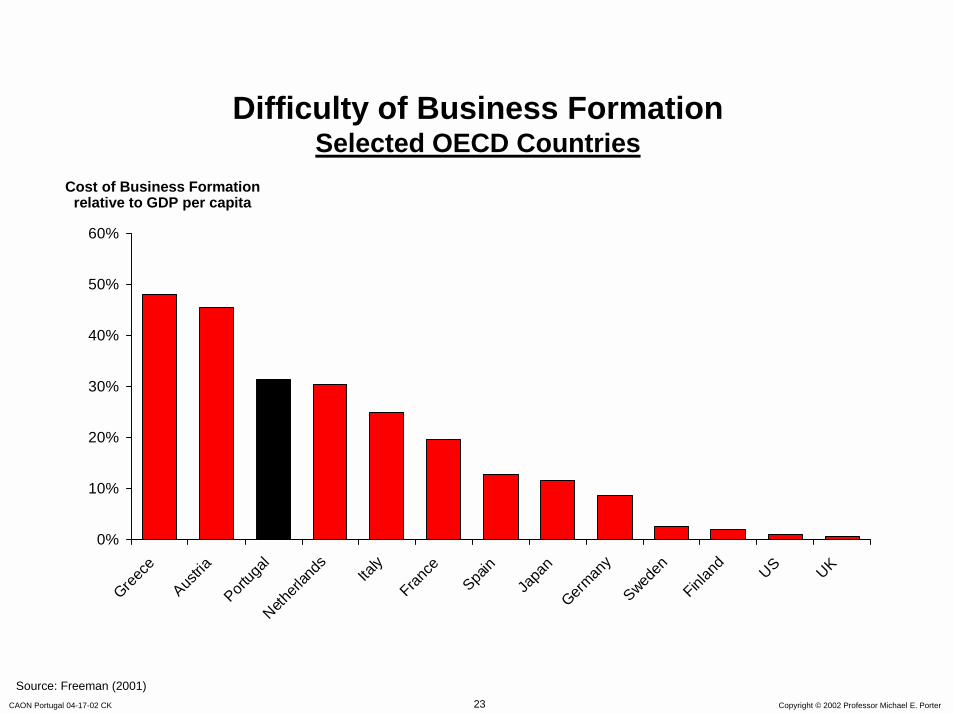

Difficulty of Business FormationSelected OECD Countries

0%

10%

20%

30%

40%

50%

60%

Greece

Austria

Portug

alNeth

erlan

ds Italy

France

Spain

Japa

nGerm

any

Sweden

Finlan

d

US UK

Cost of Business Formation relative to GDP per capita

Source: Freeman (2001)

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter24

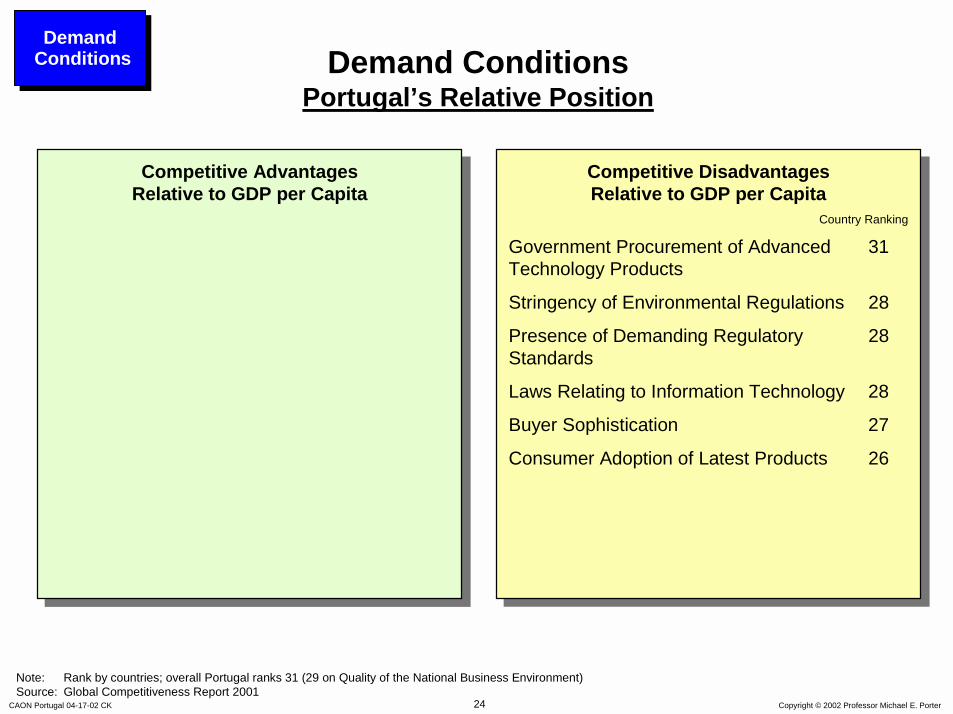

Demand ConditionsPortugal’s Relative Position

Competitive Disadvantages Relative to GDP per Capita

Competitive Advantages Relative to GDP per Capita

Country Ranking

Note: Rank by countries; overall Portugal ranks 31 (29 on Quality of the National Business Environment)Source: Global Competitiveness Report 2001

Government Procurement of Advanced 31 Technology Products

Stringency of Environmental Regulations 28

Presence of Demanding Regulatory 28Standards

Laws Relating to Information Technology 28

Buyer Sophistication 27

Consumer Adoption of Latest Products 26

Demand ConditionsDemand

Conditions

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter25

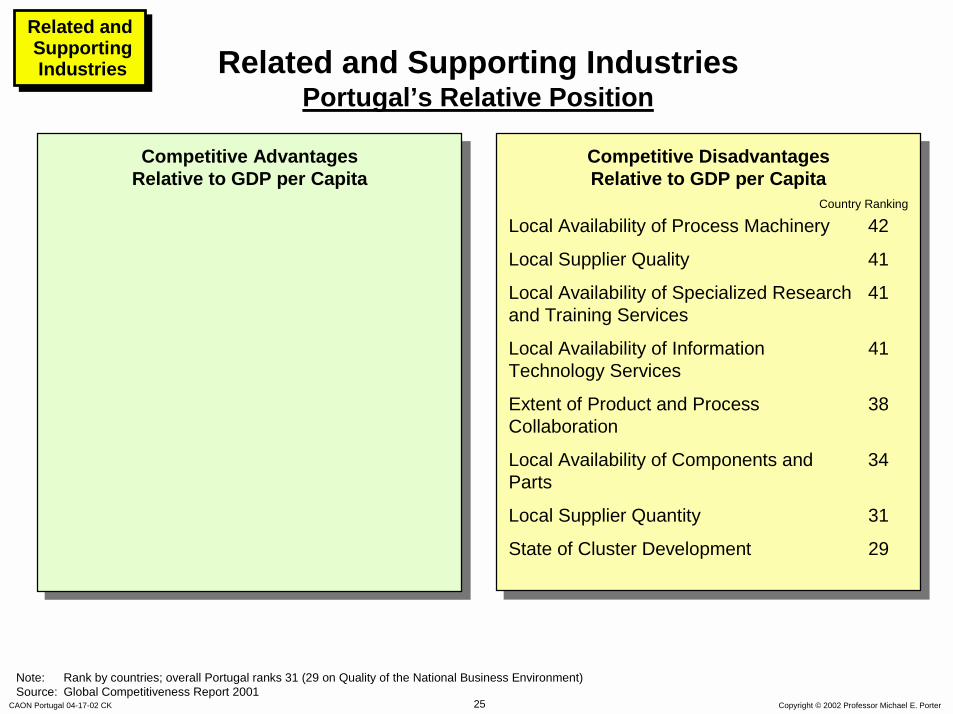

Related and Supporting IndustriesPortugal’s Relative Position

Competitive Disadvantages Relative to GDP per Capita

Competitive Advantages Relative to GDP per Capita

Country Ranking

Note: Rank by countries; overall Portugal ranks 31 (29 on Quality of the National Business Environment)Source: Global Competitiveness Report 2001

Local Availability of Process Machinery 42

Local Supplier Quality 41

Local Availability of Specialized Research 41and Training Services

Local Availability of Information 41 Technology Services

Extent of Product and Process 38Collaboration

Local Availability of Components and 34Parts

Local Supplier Quantity 31

State of Cluster Development 29

Related and Supporting Industries

Related and Supporting Industries

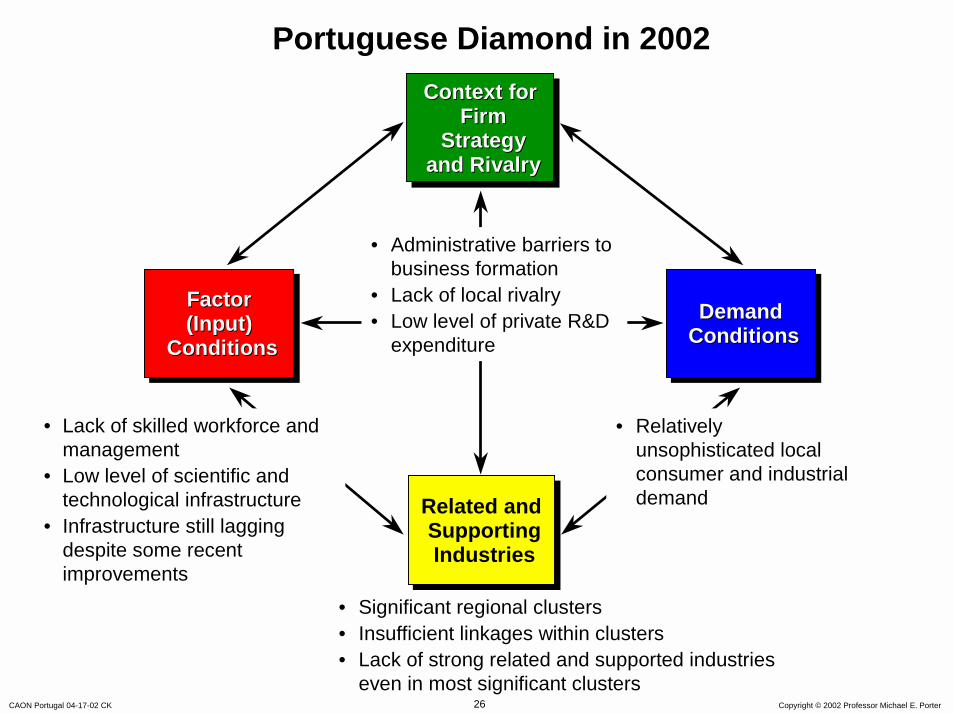

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter26

Context for Firm

Strategy and Rivalry

Context for Context for Firm Firm

Strategy Strategy and Rivalryand Rivalry

Related and Supporting Industries

Related and Supporting Industries

Factor(Input)

Conditions

FactorFactor(Input) (Input)

ConditionsConditions

• Relatively unsophisticated local consumer and industrial demand

• Administrative barriers to business formation

• Lack of local rivalry• Low level of private R&D

expenditureDemand

ConditionsDemand Demand

ConditionsConditions

• Lack of skilled workforce and management

• Low level of scientific and technological infrastructure

• Infrastructure still lagging despite some recent improvements

Portuguese Diamond in 2002

• Significant regional clusters• Insufficient linkages within clusters• Lack of strong related and supported industries

even in most significant clusters

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter27

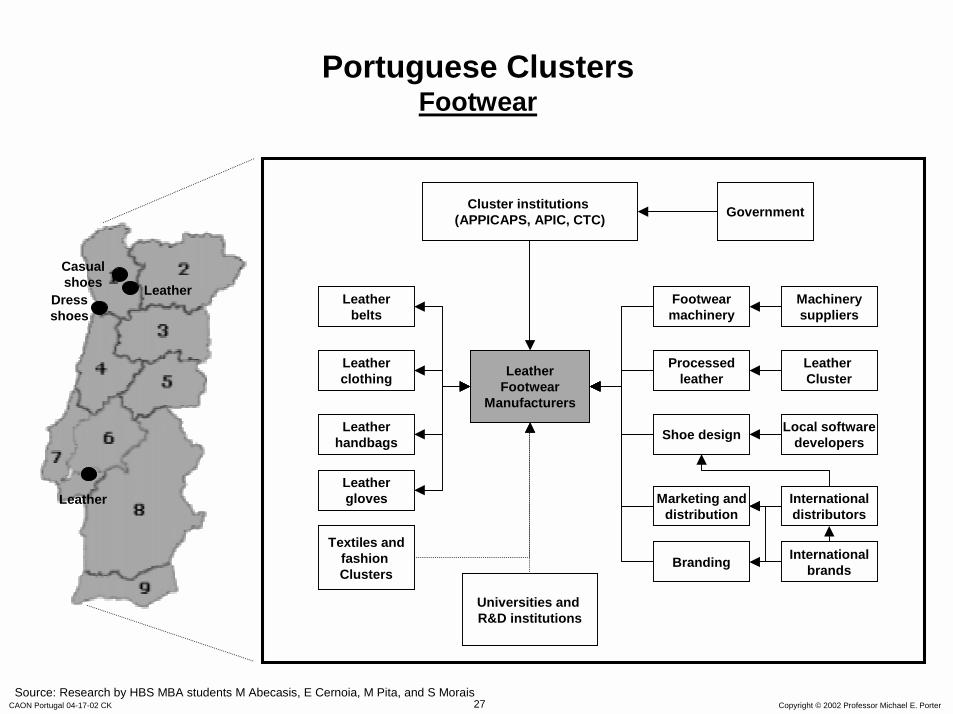

Portuguese ClustersFootwear

LeatherFootwear

Manufacturers

Universities and R&D institutions

Branding

Shoe design

Marketing anddistribution

Processedleather

Cluster institutions (APPICAPS, APIC, CTC)

Footwearmachinery

Internationalbrands

Local softwaredevelopers

Internationaldistributors

Leather Cluster

Machinerysuppliers

Textiles andfashion Clusters

Leatherhandbags

Leathergloves

Leatherclothing

Government

Leatherbelts

Leather

Dress shoes

Leather

Casual shoes

Source: Research by HBS MBA students M Abecasis, E Cernoia, M Pita, and S Morais

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter28

Portuguese ClustersFootwear

• Cluster analyzed in the 1994 study– Concentrated around Porto– Competing on price and low wage– Low productivity, poor relations to suppliers, low level of product

differentiation, and limited understanding of consumer needs

• Situation in 2002– Increasing competition from low cost locations in Asia– Moderate improvements in productivity, response times, and technical

efficiency– Still poor relations to related and supporting industries– Active cluster organization APICCAPS; recently launched “Portugal Quality

Shoes” re-branding initiative– In a contracting world shoe market, Portuguese export market share has

slightly increased to 6.1% between 1995 and 1999

• Progress suggests potential of cluster development in Portugal• No concerted commitment across the country

Note: Draws on research by HBS MBA students M Abecasis, E Cernoia, M Pita, and S Morais

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter29

Portuguese Competitiveness 1994 versus 2002

• Portugal has made important progress on macroeconomic terms

• Progress on the microeconomic foundations of competitiveness has been largely absent – There are exceptions (E.g., reduction of government subsidies,

privatizations, creation of a more independent anti-trust authority) – The exceptions were more a by-product of adopting EU rules than

part of a competitiveness strategy

• Portugal must address its microeconomic weaknesses if it is to improve or even sustain its prosperity

CAON Portugal 04-17-02 CK Copyright © 2002 Professor Michael E. Porter30

Portugal in 2002 The Need for a New Strategy

• The central challenge is microeconomic

• Portugal’s new strategy must focus on competitiveness and productivity

– A long-term program to upgrade the business environment– A long-term program to build innovative capacity

• Aggressive cluster development throughout the economy must become a national priority

• Leaders must create a national economic vision to inspire and motivate the Portuguese people