issues & policies uganda's

TRANSCRIPT

Malta: Commonwealth 3rd Country Training Program

BANKING & FINANCE IN SMALL STATES: ISSUES & POLICIES

Uganda’s case

Presenter – Christopher KIGENYI, FCIB.

Presentation Outline.

-Uganda: General Information;- Institutional Set Up (Forex & Domestic Markets – Money & Capital markets);-The USE – Uganda Securities Exchange;-The BOU – Central Bank;- Other Financial Institutions;- Regulatory Framework;- Uganda: The Basel Framework;-Other Issues (Tax framework, FATF, Regional payments system);-Strengths & Weaknesses;-Conclusion: Continuing debate.

UGANDA: GENERAL INFORMATION

-Full name: Republic of Uganda

- Location: Eastern Africa

- Population: 33.8 million (UN, 2010)

- Area: 241,038 sq km (93,072 sq miles)

- Life expectancy: 55 years (men), 56 years (women) (UN)

Presenter: Christopher KIGENYI, FCIB

- Monetary unit: 1 Ugandan shilling = 100 cents; USD 1 = UGX 2390

- Main exports: Coffee, fish and fish products, tea; tobacco, cotton, corn, beans, sesame

- GNI per capita: US $460 (World Bank, 2009

UGANDA: GENERAL INFORMATION

Presenter: Christopher KIGENYI, FCIB

Emerging market, at an early stage of development .

INSTITUTIONAL SET UP: FINANCIAL MARKETS.

Presenter: Christopher KIGENYI, FCIB

Main categorization:

-Forex market;-‘Domestic’ Markets (Money & Capital Markets);

Authority allotment :

-Central Bank – Banks & Financial Institutions;-Insurance Commission – Insurance Industry;-Capital Markets Authority – ‘Term’ Investments.

The Forex Market.

INSTITUTIONAL SET UP:FINANCIAL MARKETS IN UGANDA.

Presenter: Christopher KIGENYI, FCIB

Four main participants;

1. The Bank of Uganda (the Central Bank);2. The Inter-bank market; 3. The Forex Bureaus (that act as money shops);4. Retail customers or end users of forex.

Legislation: The Foreign Exchange Act, 2004 (reviewed); Market status: Liberalized since 1990 – Bureaus introduced.

The (Gov’t)Securities Market.

INSTITUTIONAL SET UP:FINANCIAL MARKETS IN UGANDA.

Presenter: Christopher KIGENYI, FCIB

Four main markets -

- The Treasury Bill Primary & - Secondary market- The Treasury Bond Primary & - Secondary market

Primary market T-Bills issued at 91, 182 & 364 days;

Bonds introduced in Jan 2005 for 2,3,5 & 10 year tenure, Auctioned every 28 days (aimed at stimulating secondary market, like the fortnightly T-Bill auction vis Weekly auctions)

Notes – Developments on the Govt securities market.

INSTITUTIONAL SET UP:FINANCIAL MARKETS IN UGANDA.

Presenter: Christopher KIGENYI, FCIB

• Central Depository System(CDS) . Bearer T-Bill certificates did not activate secondary market trading because of their security risk; now replaced with an E-registry, the book entry CDS.

•Financial Accountability Act of 2003 – to recognize paperless transactions;

• Primary Dealer ranking system, with monthly pronouncements of ‘Winner’, to stimulate Secondary market

Notes – Developments on the Govt securities market.

INSTITUTIONAL SET UP:FINANCIAL MARKETS IN UGANDA.

Presenter: Christopher KIGENYI, FCIB

•The bonds support monetary policy implementation by improving liquidity management and promoting market development;

•Bonds have also provided an additional saving instrument and have deepened the capital market;

The Repurchase Agreements (Repo) Market .

INSTITUTIONAL SET UP:FINANCIAL MARKETS IN UGANDA.

Presenter: Christopher KIGENYI, FCIB

Repos were introduced to manage intra-auction liquidity variations. The vertical repo market reflects repo transactions between primary dealer commercial banks and the central bank.

This market was introduced in 2002 by the Bank of Uganda as a mechanism to deal with managing liquidity in the banking system in the interval between auctions of treasury bills.

The Capital Market .

INSTITUTIONAL SET UP:FINANCIAL MARKETS IN UGANDA.

Presenter: Christopher KIGENYI, FCIB

…where financial instruments for raising capital are traded e.g. Stocks and Bonds.

Uganda Securities Exchange (USE) remains the ONEapproved Stock exchange in Uganda.

The USE – Uganda Securities Exchange.

INSTITUTIONAL SET UP:FINANCIAL MARKETS IN UGANDA.

Presenter: Christopher KIGENYI, FCIB

Licensed to operate as an approved Stock Exchange in June 1997 by the Capital Markets Authority (CMA) of Uganda, under the CMA Statute, 1996;

The USE is a Self Regulated Organization (i.e. creates, amends and implements its own policies and business, within the Statute guidelines;

16 listed companies; no local one;

The USE – Uganda Securities Exchange.

INSTITUTIONAL SET UP:FINANCIAL MARKETS IN UGANDA.

Presenter: Christopher KIGENYI, FCIB

Equity trades - 16 listed companies (non with local ownership);

Bond listing - Govt, EADB – East African Development Bank; SCB – Standard Chartered Bank & Housing Finance Bank (major shareholder – NSSF). Govt’ remains main player.

Illustration: April 13th 33/30 deals were from trades of one company, contributing 360k/400k shares traded – valued at UGX 102m/= (USD 44K)

Bank of Uganda - The Central Bank’s role.

INSTITUTIONAL SET UP:FINANCIAL MARKETS IN UGANDA.

Presenter: Christopher KIGENYI, FCIB

Supervision and Regulation of banking activity is vested in Bank of Uganda (BOU). Financial Institutions supervised by BOU are grouped under Commercial banks and Non-bank financial institutions.

BOU conducts full on-site examination of all commercial banks using a risk-based supervision methodology; Quarterly Offsite reviews.

(Backdrop – Uganda’s Banking crisis – early 1990’s)

Bank of Uganda - The Central Bank’s role.

INSTITUTIONAL SET UP:FINANCIAL MARKETS IN UGANDA.

Presenter: Christopher KIGENYI, FCIB

During the year 2004/2005 the Bank commenced the deployment of the Bank Supervision Application (BSA) following successful deployment in ten (10) other countries in the Eastern and Southern Africa region;

The Financial Institutions Act 2004 provides for various mandatory Prompt Corrective Actions which the Bank must undertake to correct weaknesses in the financial institutions before they escalate to unacceptable levels;

Note: There are 23 Commercial bank in Uganda.

Bank of Uganda - The Central Bank’s role.

INSTITUTIONAL SET UP:FINANCIAL MARKETS IN UGANDA.

Presenter: Christopher KIGENYI, FCIB

The non-bank financial institutions supervised by the Bank of Uganda are:

- Credit Institutions Micro-finance (3)- Micro Finance Deposit-taking Institutions (3) - Forex Bureaux (167)-Money Remitters (39)

Note: The Banking fraternity is tiered into 4 levels:Tier 1 – Commercial Banks; Tier II – Credit Institutions; Tier III –Micro Deposit taking Institutions; Tier IV – Unregulated (including Money lenders & SACCOs – Savings & Credit Co-operative Organizations)

The ‘Other’ Financial Institutions:

THE ‘OTHER’ INSTITUTIONS IN UGANDA’S FINANCIAL MARKET

Presenter: Christopher KIGENYI, FCIB

These form part of the Financial markets framework, but are not supervised by BOU , for example:

- Insurance Companies; - Insurance Brokers; -Leasing Companies; - Development Banks.

There is an evolving Leasing regulatory framework ,while Development banks e.g. EADB are governed under the EADB Charter …cross border legislation, for the 3 East African countries.

BANKS’ REGULATORY FRAMEWORK.

Presenter: Christopher KIGENYI, FCIB

Particularly since Uganda’s own Banking crisis of the early1990’s, the regulatory environment has been enhanced, Beginning with the BOU Act, 1994 and the Financial Institutions Statute, 1994. These have since been reviewed;

Various attendant regulations have also been promulgated,to take into account Uganda’s local and International Financial markets ‘contextual’ framework.

AGAIN …other FIs are similarly supervised and regulated by relevantAuthorities e.g. The Insurance Act, 1996.

BANKS’ REGULATORY FRAMEWORK.

Presenter: Christopher KIGENYI, FCIB

Major Legislation:

-Bank of Uganda Act, 2000 (Revised from 1990);

-Financial Institutions Act, 2004 (Revised from 1994);Various Regulations issued in 2005 e.g. Ownership & Control; Capital

Adequacy; Credit Reference etc

- Micro Deposit taking Institutions Act, 2003;

- Foreign Exchange Act, 2004 (Revised from 1990);

BASEL FRAMEWORK: UGANDA’S ‘BIT’.(‘Nominal Basel II Compliance’)

Presenter: Christopher KIGENYI, FCIB

Uganda is part of the International ‘Financial system’, underthe BIS & Basel Accord framework. The Dec 2009 Proposals by the Basel Committee on Bank Supervision (BCBS) were approved by the Group of Governors and Heads of Supervision, the Oversight body;

There are implications for Uganda’s banking Industry.

Examples: a fully fledged Financial Stability section at BOU; a regular Financial Stability Report, about the economy and Financial sector, in particular.

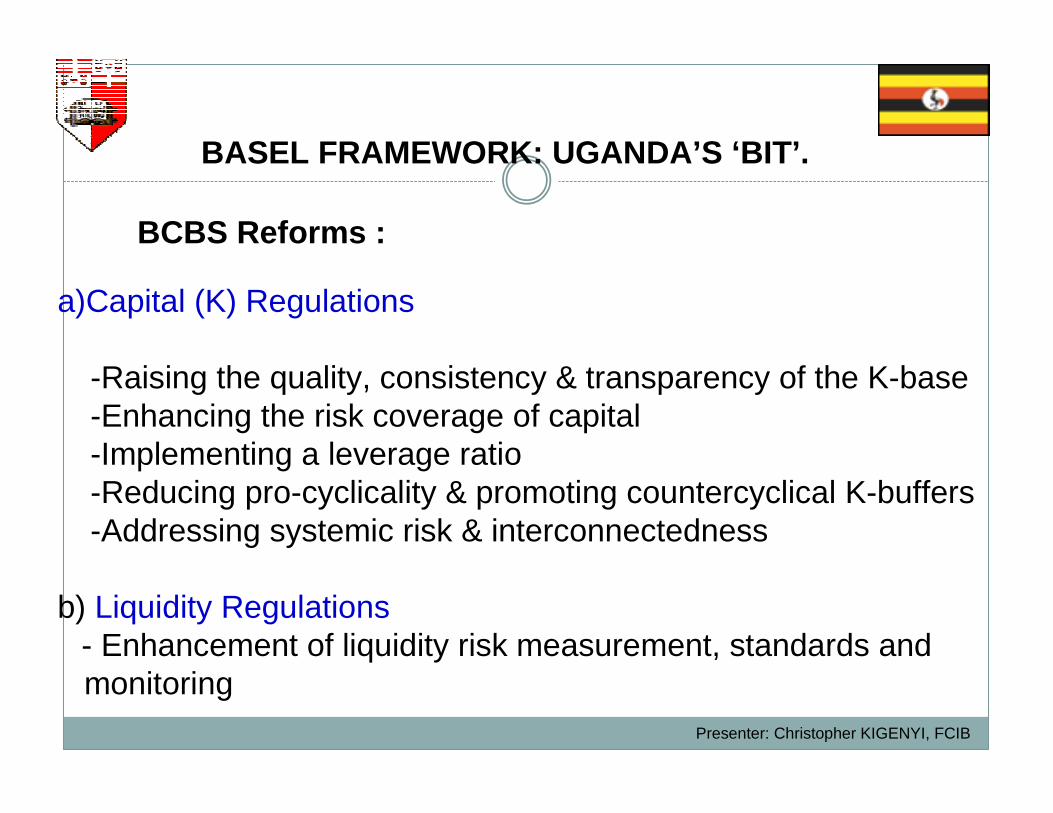

BASEL FRAMEWORK: UGANDA’S ‘BIT’.

Presenter: Christopher KIGENYI, FCIB

BCBS Reforms :

a)Capital (K) Regulations

� -Raising the quality, consistency & transparency of the K-base � -Enhancing the risk coverage of capital � -Implementing a leverage ratio � -Reducing pro-cyclicality & promoting countercyclical K-buffers � -Addressing systemic risk & interconnectedness

b) Liquidity Regulations �- Enhancement of liquidity risk measurement, standards and

monitoring

BASEL FRAMEWORK: UGANDA’S ‘BIT’.

Presenter: Christopher KIGENYI, FCIB

Policy Implications.

Phased implementation by member countries, Jan 2013, to 2018;

In the main - stricter definition of capital and higher global minimum standards, enhancing risk coverage and introducing a global liquidity standard.

In particular - 3.5 percent common equity/RWAs; 4.5 percent Tier 1 capital/RWAs; 8.0 percent Total capital/RWAs (FSR –June 2010, BOU)

BASEL FRAMEWORK: UGANDA’S ‘BIT’.

Presenter: Christopher KIGENYI, FCIB

Policy Implications – Illustrations from Uganda..

- 2% to 4% tangible common equity to capital, by Jan 2015 (UGX 4bn to 25 bn by Jan 2013). ‘Tier 1 capital’qualifying elements to increase from 4% to 6% by Jan 2015;

- Stock surpluses (share premiums), minority interests, pension fund assets, deferred tax assets, goodwill and other intangibles, and the shortfall of provisions to expected losses will be excluded from Tier 1 capital, ensuring consistency of the regulatory capital base.

BASEL FRAMEWORK: UGANDA’S ‘BIT’.

Presenter: Christopher KIGENYI, FCIB

Policy Implications – Illustrations from Uganda..

However:

The ratio of ‘Tier 1’ capital to risk weighted assets for Ugandan banks was 19.2 percent at end June 2010, far above the new requirement of 6 percent.

Largely because Uganda’s banking is still aligned to Basel 1 recommendations. The FIA 2004 already requires that goodwill and other intangible assets, minority interests, and deficiencies in provisions to be deducted from ‘Tier 1’ capital.

The FIA 2004, provides for Deposit protection …and stringency regarding deposit taking e.g. only 3 MFIs, of hundreds, have qualified to MDIs.

BASEL FRAMEWORK: UGANDA’S ‘BIT’.

Presenter: Christopher KIGENYI, FCIB

As well:

The Uganda Liquidity regulation requires banks to keep liquid assets not less than 20 percent of deposit liabilities –far above the BCBS minimum 7.5% liquidity test recommendations for various categories of liabilities.

While there is an apparent ‘constraint’ to business afforded by current bank regulation, it has provided for the requisite capital buffers for developing economy conditions, and thereby avoided the gradual build-up of excessive on and off-balance sheet leverage by financial institutions – one cause for the recent Global crisis.

Presenter: Christopher KIGENYI, FCIB

OTHER ISSUES: Uganda – Tax Haven?

TaxationWithholding Tax on

Dividends10% taxed at source

Stamp Duty NilCapital Gains Tax Nil

Corporate tax 30%

Currently there are no restrictions to foreign investors in the Ugandan market – quite a ‘Tax haven’, and promoted so, by the UIA – Uganda Investment Authority.

•TAXATION IN THE INDUSTRY

Presenter: Christopher KIGENYI, FCIB

OTHER ISSUES: Uganda – CDD Imperatives.

-Uganda is a signatory to the FATF – Financial Action TaskForce framework;

-Regulation requires a Risk based approach to CDD;

- AML policy guidelines a MUST for all Financial Institutions;

-BOU daily and periodic reports conform this e.g. >USD 10k transactions;

My bank’s ‘Big Movers’ = > UGX 10 million i.e. c. USD 4.5k.

UGANDA’S ECONOMY : SOME STRENGTHS -(Banking & Financial Sector)

Presenter: Christopher KIGENYI, FCIB

Robust regulatory framework, especially since Uganda’s banking crisis of the early 1990s (e.g. BOU Act 1994, revised in 2000; FIA 1994, revised in 2004 etc);

The East African region has weathered the effects of the global crisis

relatively well, because of strong macroeconomic policies in the

region and generally sound banking systems which are not dependent

on international markets for funding. All of the countries in East Africa

recorded positive GDP growth in 2009/10

(Foreword, BOU Financial Stability Report, June 2010);

UGANDA’S ECONOMY : SOME STRENGTHS -(Banking & Financial Sector)

Presenter: Christopher KIGENYI, FCIB

-Low and stable inflation, necessary for underpinning sustainable

economic growth;

-Liberalized economy with a vibrant Private sector / forex market /

competitive environment for the Commercial banking industry;

-Favorable tax regime, for attracting Direct Foreign Investment e.g. Inthe financial year 2008/9, persons who export at least 80% of their finished consumer and capital goods were granted a 10-year tax holiday;

UGANDA’S ECONOMY : SOME WEAKNESSES -(Banking & Financial Sector)

Presenter: Christopher KIGENYI, FCIB

-Vulnerability to International exogenous factors remains, although not well integrated in the International Financial system

-Developing financial market with shallow depth e.g. Financial Instruments available;

-Banking and Financial industry not ‘domesticated’;

-Even devoid of Political Interference, the Government remainsthe main player in the market

Presenter: Christopher KIGENYI, FCIB

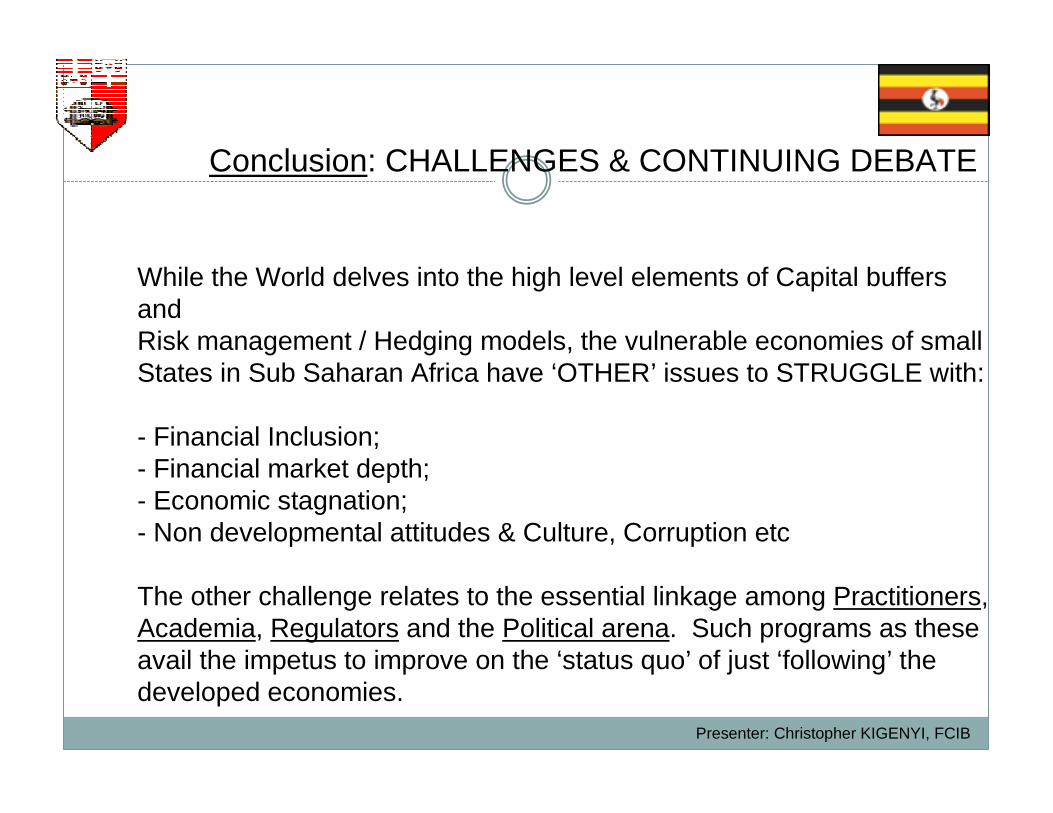

Conclusion: CHALLENGES & CONTINUING DEBATE

While the World delves into the high level elements of Capital buffers and Risk management / Hedging models, the vulnerable economies of smallStates in Sub Saharan Africa have ‘OTHER’ issues to STRUGGLE with:

- Financial Inclusion;- Financial market depth;- Economic stagnation;- Non developmental attitudes & Culture, Corruption etc

The other challenge relates to the essential linkage among Practitioners,Academia, Regulators and the Political arena. Such programs as these avail the impetus to improve on the ‘status quo’ of just ‘following’ the developed economies.

Presenter: Christopher KIGENYI, FCIB

Reference:

www.bou.or.ug Bank of Uganda / Central Bank

www.use.or.ug Uganda Securities Exchange / Stock exchange;

www.cmauganda.co.ug Capital Markets Authority

Malta: Commonwealth 3rd Country Training Program

BANKING & FINANCE IN SMALL STATES: ISSUES & POLICIES

Uganda’s case

DISCUSSION

Presenter – Christopher KIGENYI, FCIB.