isbe 2003-04 annual financial report · america, although not reasonably determinable, are presumed...

TRANSCRIPT

Lincolnwood, Illinois

(Continued)

INDEPENDENT AUDITORS' REPORT

We have audited the accompanying basic financial statements as listed in the table of contents of theAnnual Financial Report Form of Lincolnwood School District 74 (the District) as of and for the yearended June 30, 2011. These financial statements are the responsibility of Lincolnwood School District74's management. Our responsibility is to express an opinion on these financial statements based on ouraudit.

We conducted our audit in accordance with auditing standards generally accepted in the United States ofAmerica and the standards applicable to financial audits contained in Government Auditing Standards,issued by the Comptroller General of the United States. Those standards require that we plan andperform the audit to obtain reasonable assurance about whether the financial statements are free ofmaterial misstatement. An audit includes examining, on a test basis, evidence supporting the amounts anddisclosures in the financial statements. An audit also includes assessing the accounting principles usedand significant estimates made by management, as well as evaluating the overall financial statementpresentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, because of the matter discussed in the preceding paragraph, the financial statementsreferred to above do not present fairly, in conformity with accounting principles generally accepted in theUnited States of America, the financial position of Lincolnwood School District 74 as of June 30, 2011,or changes in its financial position for the fiscal year then ended.

Lincolnwood School District 74

As described more fully in Note A, Lincolnwood School District 74 has prepared these financialstatements using accounting practices prescribed by the Illinois State Board of Education, which practicesdiffer from accounting principles generally accepted in the United States of America. They are intendedto assure effective legislative and public oversight of financing and spending activities of accountableIllinois public school districts. The effects on the financial statements of the variances between theseregulatory accounting practices and accounting principles generally accepted in the United States ofAmerica, although not reasonably determinable, are presumed to be material.

The Members of the Board of Education

To the Members of the Board of EducationLincolnwood School District 74Lincolnwood, Illinois (Continued)

Deerfield, IllinoisOctober 27, 2011

Additionally, in our opinion, the financial statements referred to above present fairly, in all materialrespects, the statements of position of the funds and account groups of Lincolnwood School District 74 asof June 30, 2011, and the revenues and expenditures of its funds for the fiscal year then ended on thebasis of accounting described in Note A.

Our audit was made for the purpose of forming an opinion on the financial statements taken as a whole.The schedules listed in the table of contents as "Supplemental Information" and "Statistical Information"are presented for the purposes of additional analysis and are not a required part of the basic financialstatements of Lincolnwood School District 74. Such information, except for the average daily attendancefigure included in the computation of operating expense per pupil on page 28 and per capita tuitioncharges on page 29, has been subjected to the auditing procedures applied in the audit of the basicfinancial statements and, in our opinion, is fairly stated in all material respects in relation to the basicfinancial statements taken as a whole.

Certified Public Accountants

MILLER, COOPER & CO., LTD.

In accordance with Government Auditing Standards, we have also issued a report, dated October 27,2011, on our consideration of Lincolnwood School District 74's internal control over financial reportingand our tests of its compliance with certain provisions of laws, regulations, contracts and grantagreements, and other matters. The purpose of that report is to describe the scope of our testing ofinternal control over financial reporting and compliance and the results of that testing, and not to providean opinion on the internal control over financial reporting or on compliance. That report is an integralpart of an audit performed in accordance with Government Auditing Standards and should be consideredin assessing the results of our audit.

As discussed in Note O to the audited financial statements, net assets, as of July 1, 2010, have beenrestated as a result of an adjustment to capital assets.

To the Members of the Board of EducationLincolnwood School District 74Lincolnwood, Illinois

Internal Control Over Financial Reporting

(Continued)

We have audited the financial statements of the governmental activities, each major fund, and theaggregate remaining fund information of Lincolnwood School District 74 as of and for the year endedJune 30, 2011, which collectively comprise Lincolnwood School District 74's basic financial statements,and have issued our report thereon dated October 27, 2011. We conducted our audit in accordance withauditing standards generally accepted in the United States of America and the standards applicable tofinancial audits contained in Government Auditing Standards, issued by the Comptroller General of theUnited States.

A deficiency in internal control exists when the design or operation of a control does not allowmanagement or employees, in the normal course of performing their assigned functions, to prevent, ordetect and correct misstatements on a timely basis. A material weakness is a deficiency, or combinationof deficiencies, in internal control such that there is a reasonable possibility that a material misstatementof the entity's financial statements will not be prevented, or detected and corrected on a timely basis. Asignificant deficiency is a deficiency, or combination of deficiencies, in internal control that is less severethan a material weakness, yet important enough to merit attention by those charged with governance.

In planning and performing our audit, we considered Lincolnwood School District 74's internal controlover financial reporting as a basis for designing our auditing procedures for the purpose of expressing ouropinions on the financial statements, but not for the purpose of expressing an opinion on the effectivenessof the District's internal control over financial reporting. Accordingly, we do not express an opinion onthe effectiveness of Lincolnwood School District 74's internal control over financial reporting.

INDEPENDENT AUDITORS' REPORT ON INTERNAL CONTROLOVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS

BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITHGOVERNMENT AUDITING STANDARDS

To the Members of the Board of EducationLincolnwood School District 74Lincolnwood, Illinois (Continued)

Compliance and Other Matters

MILLER, COOPER & CO., LTD.

Certified Public Accountants

Deerfield, IllinoisOctober 27, 2011

This report is intended solely for the information and use of the Board of Education, management, federalawarding agencies, and pass-through entities and is not intended to be and should not be used by anyoneother than those specified parties.

Our consideration of internal control over financial reporting was for the limited purpose described in thefirst paragraph of this section and was not designed to identify all deficiencies in internal control overfinancial reporting that might be deficiencies, significant deficiencies, or material weakness. We did notidentify any deficiencies in internal control over financial reporting that we consider to be materialweaknesses, as defined above. However, we identified a deficiency in internal control over financialreporting, described in a separate letter dated October 27, 2011, that we consider to be a significantdeficiency in internal control over financial reporting.

As part of obtaining reasonable assurance about whether Lincolnwood School District 74's financialstatements are free of material misstatement, we performed tests of its compliance with certain provisionsof laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct andmaterial effect on the determination of financial statement amounts. However, providing an opinion oncompliance with those provisions was not an objective of our audit and, accordingly, we do not expresssuch an opinion. The results of our tests disclosed no instances of noncompliance or other matters thatare required to be reported under Government Auditing Standards.

The more significant of the District's accounting policies are described below.

1. Reporting Entity

2. Measurement Focus, Basis of Accounting, and Basis of Presentation

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

The accounting policies of Lincolnwood School District 74 (the District) conform to the regulatory provisionsprescribed by the Illinois State Board of Education, which is a comprehensive basis of accounting other thanaccounting principles generally accepted in the United States of America, as applicable to local government unitsof this type.

NOTE A - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The District is located in Cook County, Illinois. The District is governed by an elected Board of Education.The Board of Education maintains final responsibility for all personnel, budgetary, taxing, and debt matters.

The District includes all funds of its operations that are controlled by or dependent upon the District asdetermined on a basis of financial accountability. Financial accountability includes appointment of theorganization's governing body, imposition of will, and fiscal dependency. The accompanying financialstatements include only those funds of the District, as there are no organizations for which it has financialaccountability.

Also, the District is not included as a component unit in any other governmental reporting entity, as defined bythe Governmental Accounting Standards Board (GASB) pronouncements.

The accounts of the District are organized on the basis of funds and account groups. A fund is an independentfiscal and accounting entity with a self-balancing set of accounts that comprise its assets, liabilities, reserves,fund balance, revenues, and expenditures or expenses as appropriate. Fund accounting segregates fundsaccording to their intended purpose and is used to aid management in demonstrating compliance with finance-related and contractual provisions. The minimum number of funds are maintained consistent with legal andmanagerial requirements. Account groups are a reporting device to account for certain assets and liabilities ofthe governmental funds not recorded directly in those funds.

Property taxes, interest, and intergovernmental revenues associated with the current fiscal period are allconsidered to be susceptible to accrual and are recognized as revenues of the current fiscal period. All otherrevenue items are considered to be measurable and available only when cash is received by the District.

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

2. Measurement Focus, Basis of Accounting, and Basis of Presentation (Continued)

liquidated with expendable available financial resources.

NOTE A - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

The District reports deferred revenue on its financial statements. Deferred revenue arises when a potentialrevenue does not meet both the "measurable" and "available" criteria for recognition in the current period. Insubsequent periods, when both revenue recognition criteria are met, or when the District has a legal claim tothe resources, the liability for deferred revenue is removed from the combined statement of position andrevenue is recognized.

Governmental funds are used to account for the District's general governmental activities. Governmental fundtypes use the flow of current financial resources measurement focus and the modified accrual basis ofaccounting. Under the modified accrual basis of accounting, revenues are recognized when susceptible toaccrual, i.e., when they are both "measurable and available". "Measurable" means that the amount of thetransaction can be determined and "available" means collectible within the current period or soon enoughthereafter to be used to pay liabilities of the current period. The District considers property tax revenues andmost other revenues available if they are collected within 60 days of the end of the current fiscal period.Revenues that are paid to the District by the Illinois State Board of Education are considered available ifvouchered by year-end. Expenditures are recorded when the related fund liability is incurred, except forunmatured principal and interest on general long-term debt which is recognized when due, and certaincompensated absences, claims, and judgments which are recognized when the obligations are expected to be

Funds are classified into the following categories: governmental and fiduciary.

Governmental funds are used to account for all of the District's general activities, including the collection anddisbursement of earmarked monies (special revenue funds) and the servicing of general long-term debt (debtservice funds), and the acquisition or construction of major capital facilities (capital projects funds). TheGeneral Fund is used to account for all activities of the general government not accounted for in some otherfund.

Fiduciary funds are used to account for assets held on behalf of outside parties, including other governments,or on behalf of other funds within the District.

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

2. Measurement Focus, Basis of Accounting, and Basis of Presentation (Continued)

a. General Fund

b. Special Revenue Funds

The following funds are the District's funds:

The General Fund is the District's primary operating fund. It accounts for all financial resources of thegeneral government, except those required to be accounted for in another fund. The General Fund includesthe Educational Fund.

The special revenue funds are used to account for the proceeds of specific revenue sources (other than thoseaccounted for in the Debt Service Fund, Capital Projects Fund, or Fiduciary Funds) that are legallyrestricted to expenditures for specified purposes.

Each of the District's special revenue funds has been established as a separate fund in accordance with thefund structure required by the state of Illinois for local educational agencies. These funds account for localproperty taxes restricted to specific purposes. A brief description of the District's special revenue funds isas follows:

Operations and Maintenance Fund - is used for expenditures made for operations, repair, and maintenanceof the District's building and land. Revenues consist primarily of local property taxes.

NOTE A - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Tort Immunity and Judgment Fund - accounts for all revenues and expenditures related to liabilityinsurance. Revenues consist primarily of local property taxes.

Transportation Fund - accounts for all revenue and expenditures made for student transportation.Revenues are derived primarily from local property taxes and state reimbursement grants.

Municipal Retirement/Social Security Fund - accounts for the District's portion of pension contributions tothe Illinois Municipal Retirement Fund, payments to Medicare, and payments to the Social Security Systemfor noncertified employees. Revenues to finance contributions are derived primarily from local propertytaxes and personal property replacement taxes.

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

2. Measurement Focus, Basis of Accounting, and Basis of Presentation (Continued)

b. Special Revenue Funds (Continued)

c. Debt Service Fund

d. Capital Projects Fund

e. Fire Prevention and Safety Fund

f. Fiduciary Fund

Debt Service Fund - is used for the accumulation of resources for, and the payment of, general long-termdebt principal, interest, and related costs. The primary revenue source is local property taxes leviedspecifically for debt service.

Capital Projects Fund - accounts for financial resources to be used for the acquisition or construction ofmajor capital facilities. Revenues to finance projects are derived from property taxes, bond proceeds, ortransfers from other funds.

Fire Prevention and Safety Fund - accounts for state-approved life safety projects financed through serialbond issues or local property taxes levied specifically for such purposes.

NOTE A - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

The Fiduciary Fund accounts for assets held by the District in a trustee capacity or as an agent forindividuals, private organizations, other governments, or other funds.

Working Cash Fund - accounts for financial resources held by the District to be used as temporaryinterfund loans for working capital requirements to the General Fund and the special revenue fund'sOperations and Maintenance and Transportation Funds. Money loaned by the Working Cash Fund to otherfunds must be repaid within one year. As allowed by the School Code of Illinois, this Fund may bepermanently abolished and become part of the General Fund or it may be partially abated to any fund inneed as long as the District maintains a balance in the Working Cash Fund of at least .05% of the District'scurrent equalized assessed valuation.

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

2. Measurement Focus, Basis of Accounting, and Basis of Presentation (Continued)

e. Fiduciary Fund (Continued)

3. General Fixed Assets and General Long-Term Debt Account Groups

Student Activity Funds (Agency Funds) are custodial in nature (assets equal liabilities) and do not involvemeasurement of the results of operations. These Funds account for assets held by the District which areowned, operated, and managed generally by the student body, under the guidance and direction of adults ora staff member, for educational, recreational, or cultural purposes. They account for activities such asstudent yearbook, student clubs and council, and scholarships.

Account groups are used to establish accounting control and accountability for the District's capital assets andgeneral long-term debt. The accounting and financial reporting treatment applied to the capital assets and long-term liabilities associated with a fund are determined by its measurement focus.

The two account groups are not "funds." They are concerned only with measurement of financial position.They are not involved with measurement of the results of operations.

Capital assets have been acquired for general governmental purposes. At the time of purchase, assets arerecorded as expenditures paid in the governmental funds and capitalized at cost in the General Fixed AssetsAccount Group. Donated capital assets are listed at estimated fair market value as of the date of acquisition.Depreciation accounting is not applicable, except to determine the per capita tuition charge. Interest costsincurred during construction are not capitalized as part of capital assets.

Long-term liabilities expected to be financed from governmental funds are accounted for in the General Long-Term Debt Account Group, not in the governmental funds. The debt recorded in the District's General Long-Term Debt Account Group consists of serial bond issues, long-term debt retirements payable, andcompensated absences.

NOTE A - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

4. Deposits and Investments

5. Property Taxes Receivable

Property taxes are collected by the Cook County Collector/Treasurer who remits them to the School Treasurer. Taxes levied in one year become due and payable in two installments on March 1 and approximatelySeptember 1 during the following year. The first installment is an estimated bill, and is fifty-five percent of theprior year's tax bill. The second installment is based on the current levy, assessment, and equalization, and anychanges from the prior year will be reflected in the second installment bill.

The District must file its tax levy resolution by the last Tuesday in December of each year. The tax levyresolution was approved by the Board on December 7, 2010. The District's property tax is levied each year onall taxable real property located in the District, and becomes a lien on the property on January 1 of that year.The owner of real property on January 1 (the lien date) in any year is liable for taxes of that year.

The County Clerk adds the equalized assessed valuation of all real property in the county to the valuation ofproperty assessed directly by the state (to which the equalization factor is not applied) to arrive at the baseamount (the assessment base) used in calculating the annual tax rates, as described above. The equalizedassessed valuation for the extension of the 2010 tax levy was $778,893,712.

State statutes require the District to use the investment services of the Township School Treasurer andauthorize the District's Treasurer to invest in obligations of the U.S. Treasury, certain highly rated commercialpaper, corporate bonds, repurchase agreements, and money market mutual funds registered under theInvestment Company Act of 1940, with certain restrictions. Investments are stated at fair value. Changes inthe fair value of investments are recorded as investment income.

The Cook County Assessor is responsible for the assessment of all taxable real property within Cook Countyexcept for certain railroad property, which is assessed directly by the state. The county is reassessed everythree years by the Assessor.

The Illinois Department of Revenue has the statutory responsibility for ensuring uniformity of real propertyassessments throughout the state. Each year, the Illinois Department of Revenue furnishes the county clerkswith an adjustment factor to equalize the level of assessment between counties at one-third of market value.This factor (the equalization factor) is then applied to the assessed valuation to compute the valuation ofproperty to which the tax rate will be applied (the equalized assessed valuation). The equalization factor forCook County was 3.3000 for 2010.

NOTE A - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

5. Property Taxes Receivable (Continued)

6. Personal Property Replacement Taxes

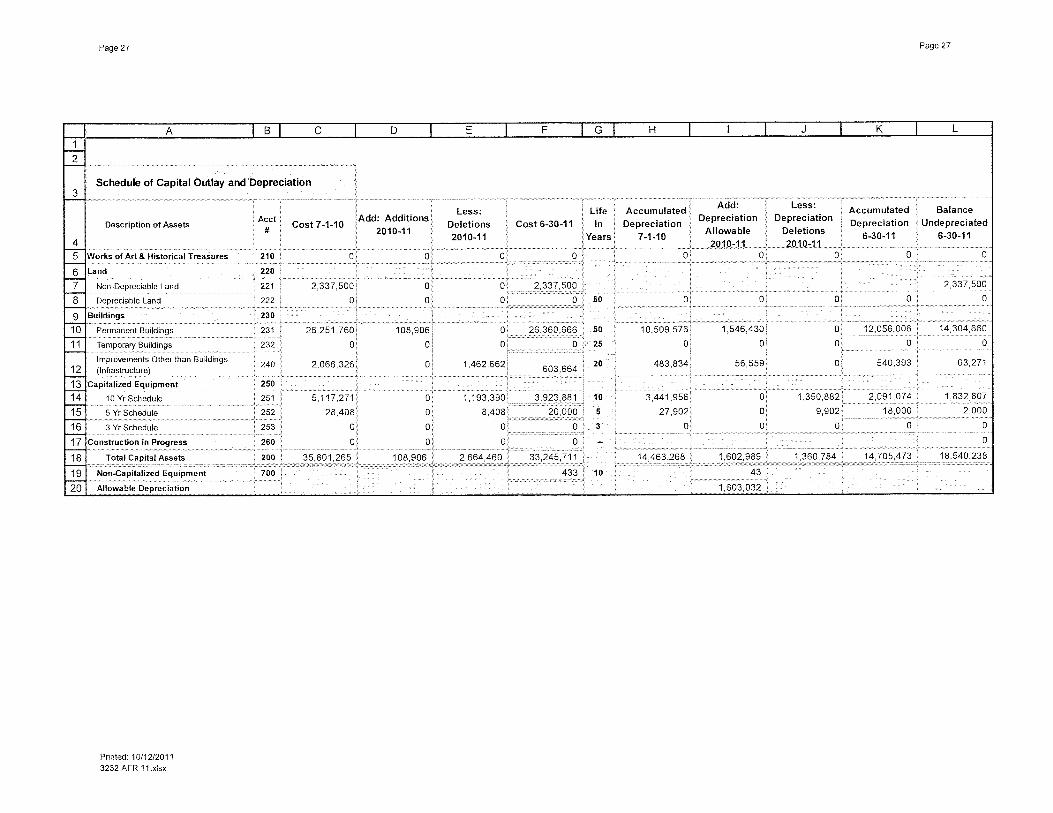

7. Capital Assets

Assets Years

Buildings 50Improvements other than buildings 20 - 40Equipment 5 - 20Transportation equipment 8

Personal property replacement tax revenues are first allocated to the Municipal Retirement/Social SecurityFund, with the balance allocated at the discretion of the District.

The portion of the 2010 property tax levy not received by June 30 is recorded as a receivable, net of estimateduncollectibles of 1%. The net receivables collected within the current year are due and expected to be collectedsoon enough thereafter to be used to pay liabilities of the current period, less the taxes collected soon enoughafter the end of the previous fiscal year, are recognized as revenue. Such time thereafter does not exceed 60days. Net taxes receivable less the amount expected to be collected within 60 days is reflected as deferredrevenue.

Depreciation of capital assets is provided over the estimated useful lives using the straight-line method and isreflected for informational purposes only. Depreciation of capital assets is not charged to operations of theDistrict. The estimated useful lives are as follows:

NOTE A - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Capital assets used in governmental fund types of the District are recorded in the General Fixed AssetsAccount Group. Capital assets are defined by the District as assets with an initial individual or group cost ofmore than $500 and an estimated useful life in excess of one year. Such assets are recorded at historical costor estimated historical cost if purchased or constructed. Donated capital assets are recorded at the estimatedfair market value at the date of donation. In 2011, the District engaged an appraisal company to estimate thehistorical cost of its capital assets acquired to that date.

The costs of normal maintenance and repairs that do not add to the value of the asset or materially extendassets lives are not capitalized.

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

8. Accumulated Unpaid Vacation and Sick Pay

9. Long-Term Obligations

10. Use of Estimates

All certified employees receive a specified number of sick days per year depending on their years of service, inaccordance with the agreement between the Board of Education and the Education Association. Unused sickleave days accumulate indefinitely. Upon retirement, a certified employee may apply up to 340 sick days ofunused sick leave toward service credit for the Teachers' Retirement System (TRS). The employee isreimbursed for any remaining unused sick days at the rate of $50 per day.

Employees who work a twelve-month year are entitled to be compensated for vacation time. Vacations areusually taken within the fiscal year. The liability for unused compensated absences is reported in the GeneralLong-Term Debt Account Group.

For governmental funds, the current portion of the compensated absences is the amount that is normallyexpected to be paid using expendable available financial resources. These amounts are recorded in the fundfrom which the employees who have accumulated vacation leave are paid.

Due to the nature of the policies on sick leave, and the fact that any liability is contingent upon future eventsand cannot be reasonably estimated, no liability is provided in the financial statements for accumulated unpaidsick leave.

NOTE A - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

For governmental fund types, bond premiums and discounts, as well as issuance costs, are recognized duringthe current period. Bond proceeds are reported as an "other financing source" net of the applicable bondpremium or discount.

The District reports long-term debt of governmental funds at face value in the General Long-Term DebtAccount Group. Certain other governmental fund obligations not expected to be financed with currentavailable financial resources are also reported in the General Long-Term Debt Account Group.

In preparing financial statements, management is required to make estimates and assumptions that affect thereported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of thefinancial statements, and the reported amounts of revenues and expenditures during the reporting period.Actual results could differ from those estimates.

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

NOTE B - LEGAL COMPLIANCE AND ACCOUNTABILITY - BUDGETS

a)

b)

c)

d)

e)

f)

g)

The Administration submits to the Board of Education a proposed operating budget for the fiscal yearcommencing July 1. The operating budget includes proposed expenditures and the means of financing them.

Budgets are adopted on a basis consistent with generally accepted accounting principles. Annual budgets areadopted at the fund level for the governmental funds. The annual budget is legally enacted and provides for a legallevel of control at the fund level. All annual budgets lapse at fiscal year-end.

By September 30, the budget is legally adopted through passage of a resolution. By the last Tuesday inDecember each year, a tax levy resolution is filed with the County Clerk to obtain tax revenues.

The Board of Education follows these procedures in establishing the budgetary data reflected in the financialstatements:

Budgetary control is maintained at line-item levels and built up into program and/or cost centers beforebeing combined to form totals by fund. All actual activity compared to budget is available to the District'smanagement in real time. These expenditure reports list each item's fiscal year-to-date expenditure, budgetamount, and account balance.

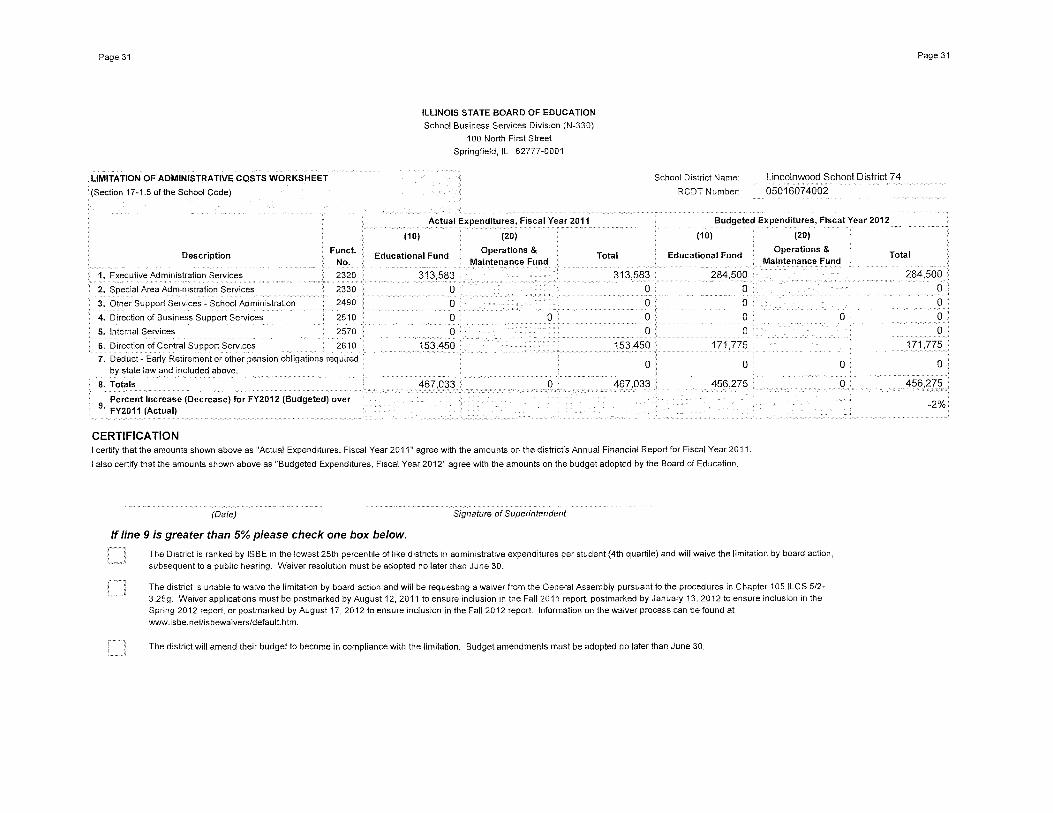

The budget amounts shown in the financial statements are as originally adopted by the Board of Educationon September 7, 2010, and subsequently amended on June 7, 2011.

Public hearings are conducted and the proposed budget is available for inspection to obtain comments.

Formal budgetary integration is employed as a management control device during the year for thegovernmental funds.

Management is authorized to transfer budget amounts, provided funds are transferred between the samefunction and object codes. The Board of Education is authorized to transfer up to a legal level of 10% ofthe total budget between functions within a fund; however, any revisions that alter the total expenditures ofany fund must be approved by the Board of Education after the public hearing process mandated by law.

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

NOTE B - LEGAL COMPLIANCE AND ACCOUNTABILITY - BUDGETS (Continued)

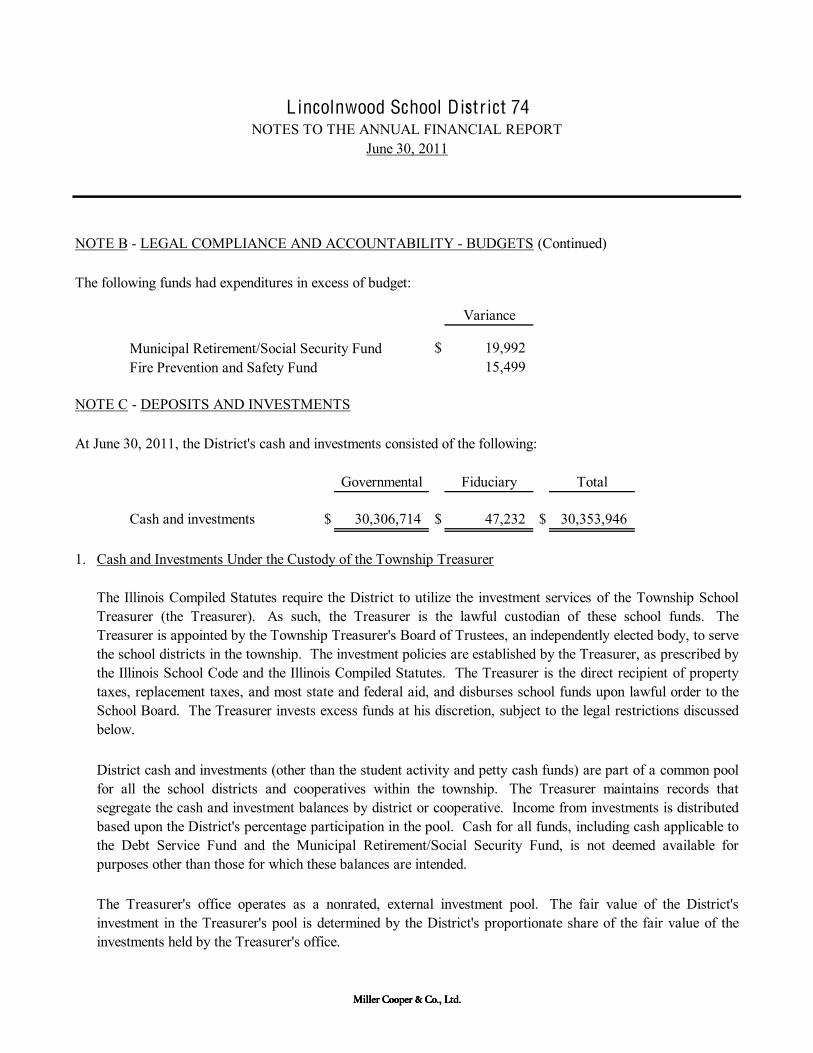

The following funds had expenditures in excess of budget:

Variance

Municipal Retirement/Social Security Fund $ 19,992 Fire Prevention and Safety Fund 15,499

NOTE C - DEPOSITS AND INVESTMENTS

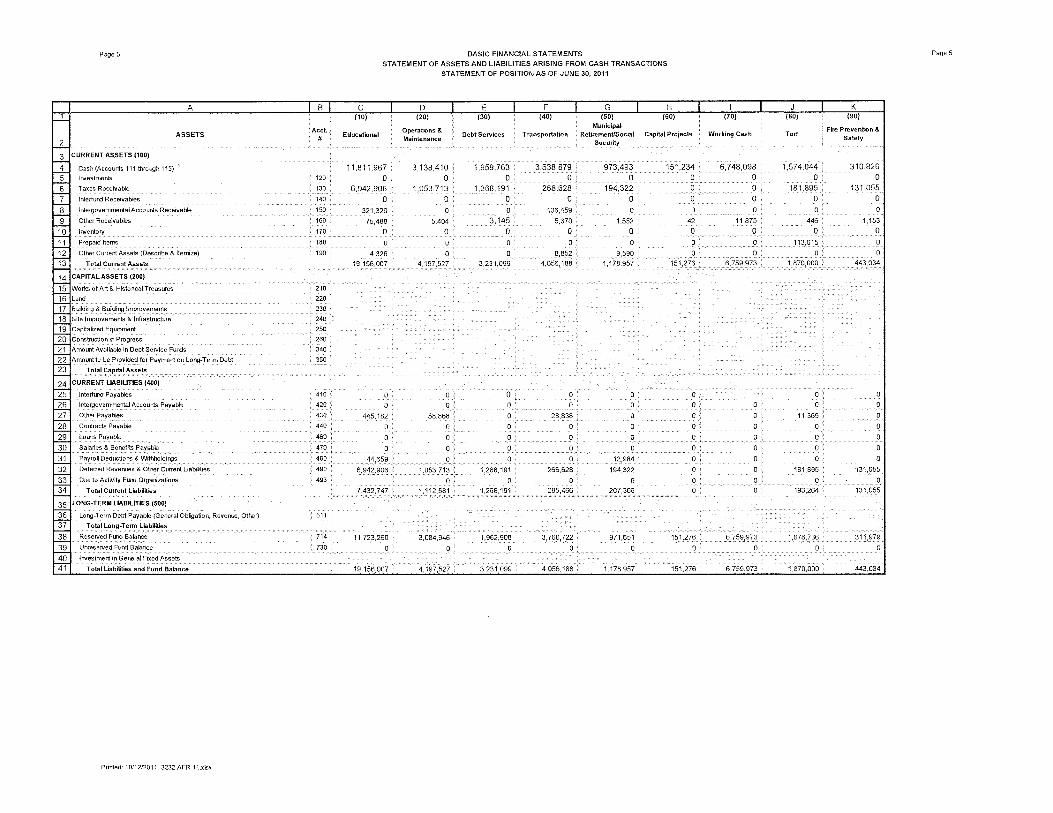

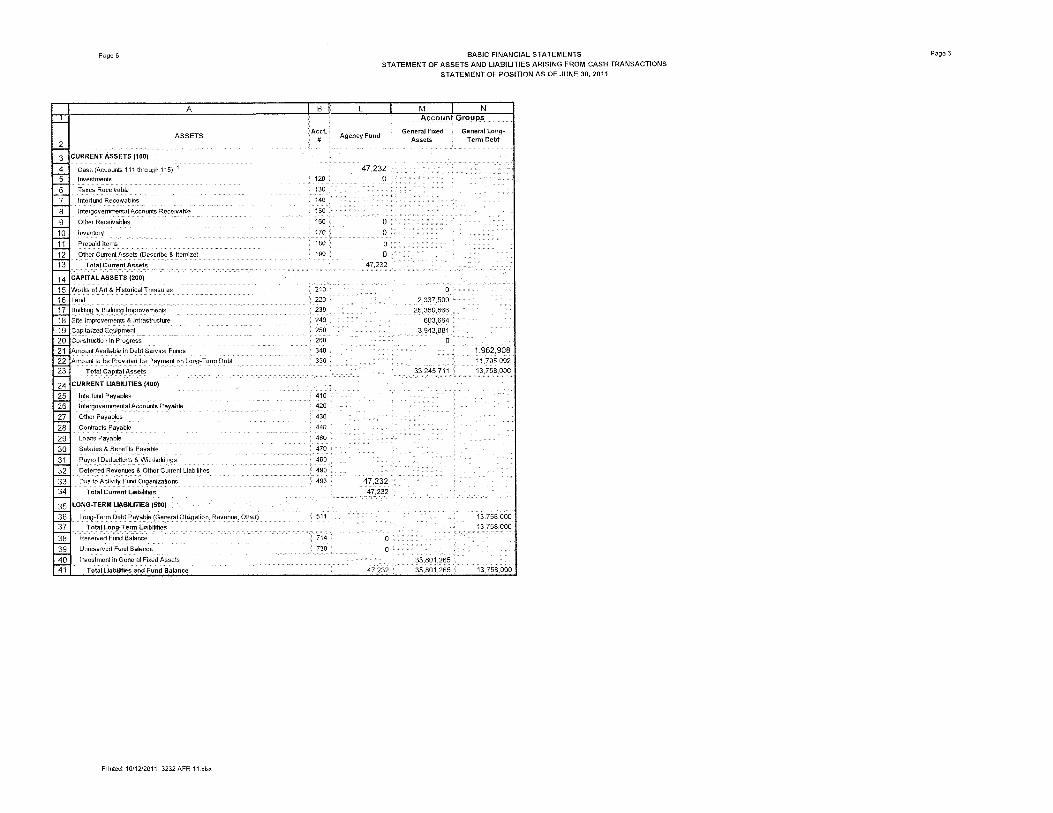

At June 30, 2011, the District's cash and investments consisted of the following:

Governmental Fiduciary Total

Cash and investments $ 30,306,714 $ 47,232 $ 30,353,946

1.

The Treasurer's office operates as a nonrated, external investment pool. The fair value of the District'sinvestment in the Treasurer's pool is determined by the District's proportionate share of the fair value of theinvestments held by the Treasurer's office.

Cash and Investments Under the Custody of the Township Treasurer

The Illinois Compiled Statutes require the District to utilize the investment services of the Township SchoolTreasurer (the Treasurer). As such, the Treasurer is the lawful custodian of these school funds. TheTreasurer is appointed by the Township Treasurer's Board of Trustees, an independently elected body, to servethe school districts in the township. The investment policies are established by the Treasurer, as prescribed bythe Illinois School Code and the Illinois Compiled Statutes. The Treasurer is the direct recipient of propertytaxes, replacement taxes, and most state and federal aid, and disburses school funds upon lawful order to theSchool Board. The Treasurer invests excess funds at his discretion, subject to the legal restrictions discussedbelow.

District cash and investments (other than the student activity and petty cash funds) are part of a common poolfor all the school districts and cooperatives within the township. The Treasurer maintains records thatsegregate the cash and investment balances by district or cooperative. Income from investments is distributedbased upon the District's percentage participation in the pool. Cash for all funds, including cash applicable tothe Debt Service Fund and the Municipal Retirement/Social Security Fund, is not deemed available forpurposes other than those for which these balances are intended.

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

NOTE C - DEPOSITS AND INVESTMENTS (Continued)

1.

2.

3.

The Illinois School District Liquid Asset Fund Plus (ISDLAF+) is an unrated, not-for-profit investment trustformed pursuant to the Illinois Municipal Code and managed by a Board of Trustees elected from participatingmembers. It is not registered with the SEC as an investment company, but operates in a manner consistentwith Rule 2a7 of the Investment Company Act of 1940. Investments are valued at share price, which is theprice for which the investment could be sold.

At June 30, 2011, the carrying value of the District's student activity funds and imprest fund was $62,332, allof which was deposited with financial institutions.

Cash and Investments in the Custody of the District

The District's investment policy requires diversification of the investment portfolio to minimize the risk of lossresulting from overconcentration in a particular type of security, risk factor, issuer, or maturity. The policyrequires diversification strategies to be determined and revised periodically by the District's Investment Officerto meet the District's ongoing need for safety, liquidity, and rate of return.

Credit Risk

Interest Rate Risk

Concentration of Credit Risk

The District's investment policy, which is the same as the Treasurer's office, seeks to ensure preservation ofcapital in the District's overall portfolio. The highest return on investments is sought, consistent with thepreservation of principal and prudent investment principles. The investment portfolio is required to providesufficient liquidity to pay District obligations as they come due, considering maturity and marketability. Theinvestment portfolio is also required to be diversified as to maturities and investments, as appropriate to thenature, purpose, and amount of funds. The District will also consider investments in local financialinstitutions, recognizing their contribution to the community's economic development.

The weighted-average maturity of all pooled marketable investments held by the Treasurer was 2.651 years atJune 30, 2011. The Treasurer also holds money market type investments and deposits with financialinstitutions, including certificates of deposit. As of the same date, the fair value of the District's cash andinvestments held by the Treasurer's office was $30,291,614.

Cash and Investments Under the Custody of the Township Treasurer (Continued)

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

NOTE C - DEPOSITS AND INVESTMENTS (Continued)

4.

NOTE D - CAPITAL ASSETS

Capital asset activity for the year ended June 30, 2011 was as follows:

Beginning Balance Ending

(as restated)* Additions Deletions Balance

Land $ 2,337,500 $ - $ - $ 2,337,500 Buildings 25,616,274 744,392 - 26,360,666 Improvements other than buildings 603,664 - - 603,664 Equipment 2,897,631 1,026,250 - 3,923,881 Transportation equipment 20,000 - - 20,000

Total capital assets $ 31,475,069 $ 1,770,642 $ - $ 33,245,711

* See Note M for details.

With respect to investments, custodial credit risk is the risk that, in the event of the failure of the counterparty,the government will not be able to recover the value of its investments or collateral securities that are in thepossession of an outside party. The District's investment policy limits the exposure to investment custodialcredit risk by requiring that all investments be secured by private insurance or collateral.

Custodial Risk

With respect to deposits, custodial credit risk refers to the risk that, in the event of a bank failure, thegovernment's deposits may not be returned to it. The District's investment policy limits the exposure to depositcustodial credit risk by requiring all deposits in excess of FDIC insurable limits to be secured by collateral inthe event of default or failure of the financial institution holding the funds.

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

NOTE E - LONG-TERM LIABILITIES

The following is the long-term liability activity for the District during the year ended June 30, 2011:

Balance BalanceJuly 1, 2010 Additions Deletions June 30, 2011

General obligation bonds $ 8,958,000 $ - $ 2,100,000 $ 6,858,000 Debt certificates 7,000,000 - 100,000 6,900,000 Compensated absences 199,802 138,764 213,690 124,876

Balance at year-end $ 16,157,802 $ 138,764 $ 2,413,690 $ 13,882,876

1.

The summary of activity in bonds payable for the year ended June 30, 2011 is as follows:

Bonds Payable Debt Debt Bonds PayableJuly 1, 2010 Issued Retired June 30, 2011

$ 1,523,000 $ - $ 900,000 $ 623,000

7,435,000 - 1,200,000 6,235,000

Total $ 8,958,000 $ - $ 2,100,000 $ 6,858,000

Bonds Payable

$5,807,728 Life Safety Bonds, Series 1992, due December 1, 2011, interest at 5.50% to 8.20%.

$9,490,000 Refunding Bonds, Series 2004A, due December 1, 2013, interest at 3.00% to 4.50%.

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

NOTE E - LONG-TERM LIABILITIES (Continued)

1.

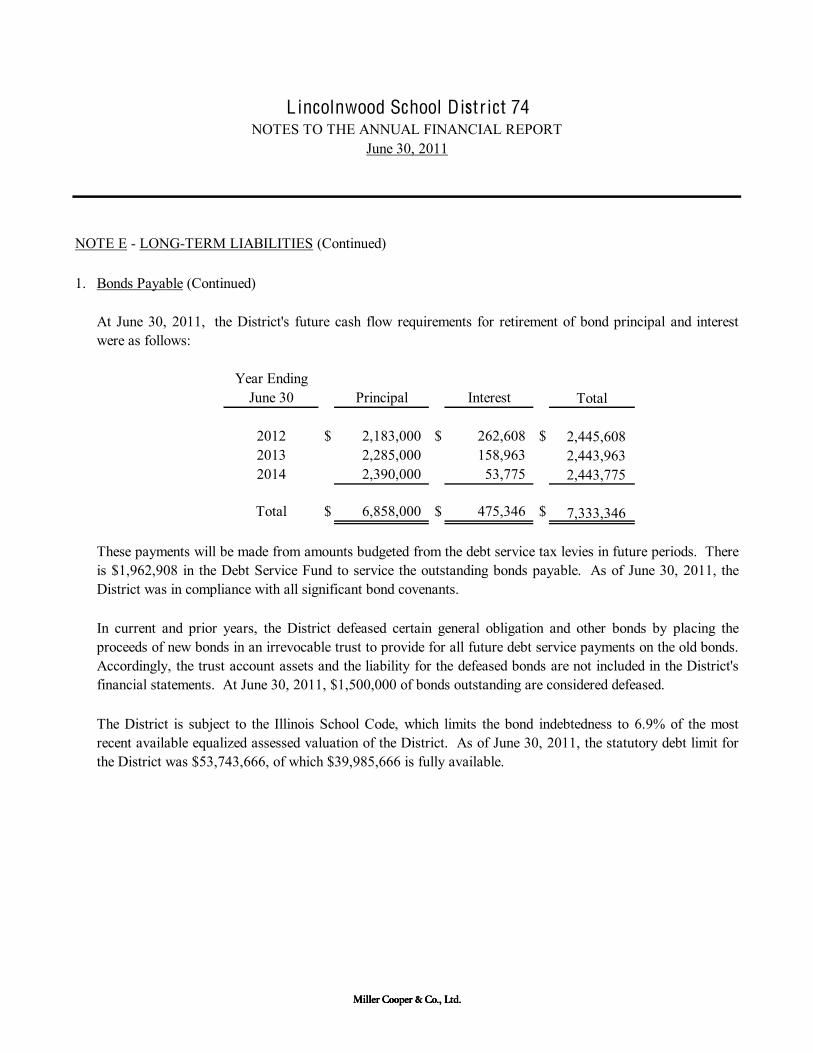

Year EndingJune 30 Principal Interest Total

2012 $ 2,183,000 $ 262,608 $ 2,445,608 2013 2,285,000 158,963 2,443,963 2014 2,390,000 53,775 2,443,775

Total $ 6,858,000 $ 475,346 $ 7,333,346

At June 30, 2011, the District's future cash flow requirements for retirement of bond principal and interestwere as follows:

In current and prior years, the District defeased certain general obligation and other bonds by placing theproceeds of new bonds in an irrevocable trust to provide for all future debt service payments on the old bonds.Accordingly, the trust account assets and the liability for the defeased bonds are not included in the District'sfinancial statements. At June 30, 2011, $1,500,000 of bonds outstanding are considered defeased.

These payments will be made from amounts budgeted from the debt service tax levies in future periods. Thereis $1,962,908 in the Debt Service Fund to service the outstanding bonds payable. As of June 30, 2011, theDistrict was in compliance with all significant bond covenants.

Bonds Payable (Continued)

The District is subject to the Illinois School Code, which limits the bond indebtedness to 6.9% of the mostrecent available equalized assessed valuation of the District. As of June 30, 2011, the statutory debt limit forthe District was $53,743,666, of which $39,985,666 is fully available.

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

NOTE E - LONG-TERM LIABILITIES (Continued)

2.

Year EndingJune 30 Principal Interest

2012 $ 105,000 $ 87,505 $2013 110,000 86,113 2014 115,000 84,579 2015 125,000 83,071 2016 285,000 80,602

2017-2021 2,080,000 330,163 2022-2026 2,475,000 187,201 2027-2029 1,605,000 32,614

Total $ 6,900,000 $ 971,846 $

3.

2,410,163

199,579

Debt Certificates

192,505

7,871,846

Compensated Absences

1,637,614

196,113

2,662,201

208,071 365,602

In June 2010, the Board of Education authorized the issuance of Debt Certificates not to exceed $17,000,000for the purpose of paying the cost of purchasing real or personal property, or both. As of the report date, nodebt has actually been issued.

At June 30, 2011 and 2010, compensated absences amounted to $124,876 and $199,802, respectively. TheDistrict considers the full amount to be long-term. Future payments will be made from the same fund wherethe employee's salary is recorded.

Total

The District has a lease/financing agreement with Northern Trust Bank for $7,000,000 to pay the costs ofacquiring, constructing, and adding equipment for the District's facilities. Interest on these certificates is paidsemiannually based on one-year London InterBank Offered Rate (LIBOR) (.733% at June 30, 2011).

Annual debt service requirements to maturity for debt certificates are as follows:

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

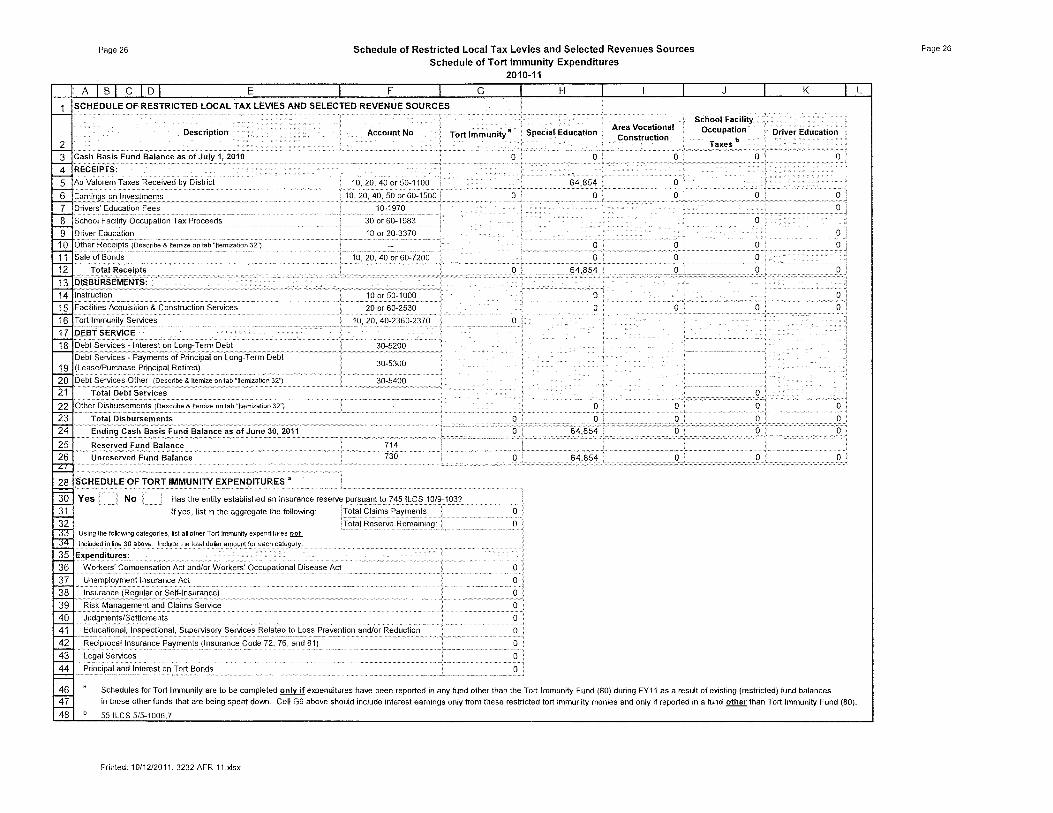

NOTE F - RESTRICTED FUND BALANCES AND SPECIAL TAX LEVIES

1. Special Education Tax Levy

2. Leasing Educational Facilities

NOTE G - RISK MANAGEMENT

NOTE H - JOINT AGREEMENTS

Settled claims have not exceeded commercial insurance coverage for the past three fiscal years.

The District is a member of the Niles Township District for Special Education (NTDSE), a joint agreement thatprovides certain special education services to residents of many school districts. It is also a member of the riskmanagement pools listed above. The District believes that, because it does not control the selection of thegoverning authority and because of the control over employment of management personnel, operations, scope ofpublic service, and special financing relationships exercised by the joint agreement governing boards, these are notrequired to be included as component units of the District.

The District continues to carry commercial insurance for all other risks of loss, including torts and professionalliability insurance.

Revenues from the special education tax levy and the related expenditures have been included in the operationsof the Educational Fund. Because cumulative expenditures exceeded cumulative revenues, there is no balancerestriction.

A portion of the fund balance in the Operations and Maintenance Fund, $141,193, represents the excess ofcumulative revenues over cumulative expenditures which is restricted for the lease of educational facilities ortechnology equipment expenditures.

The District is exposed to various risks of loss related torts, theft of, damage to, and destruction of assets, errorsand omissions, injuries to employees, and natural disasters. The District purchases coverage against such risks.To protect the District from such risks, the District participates in the following public entity risk pools: theEducational Benefit Cooperative (EBC) for health benefit claims and the Collective Liability InsuranceCooperative (CLIC) for worker's compensation claims and for property damage and injury claims. The Districtpays annual premiums to the pools for insurance coverage. The arrangements with the pools provide that thepools will be self-sustaining through member premiums, and will reinsure through commercial companies forclaims in excess of certain levels established by the pools.

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

NOTE I - RETIREMENT FUND COMMITMENTS

1.

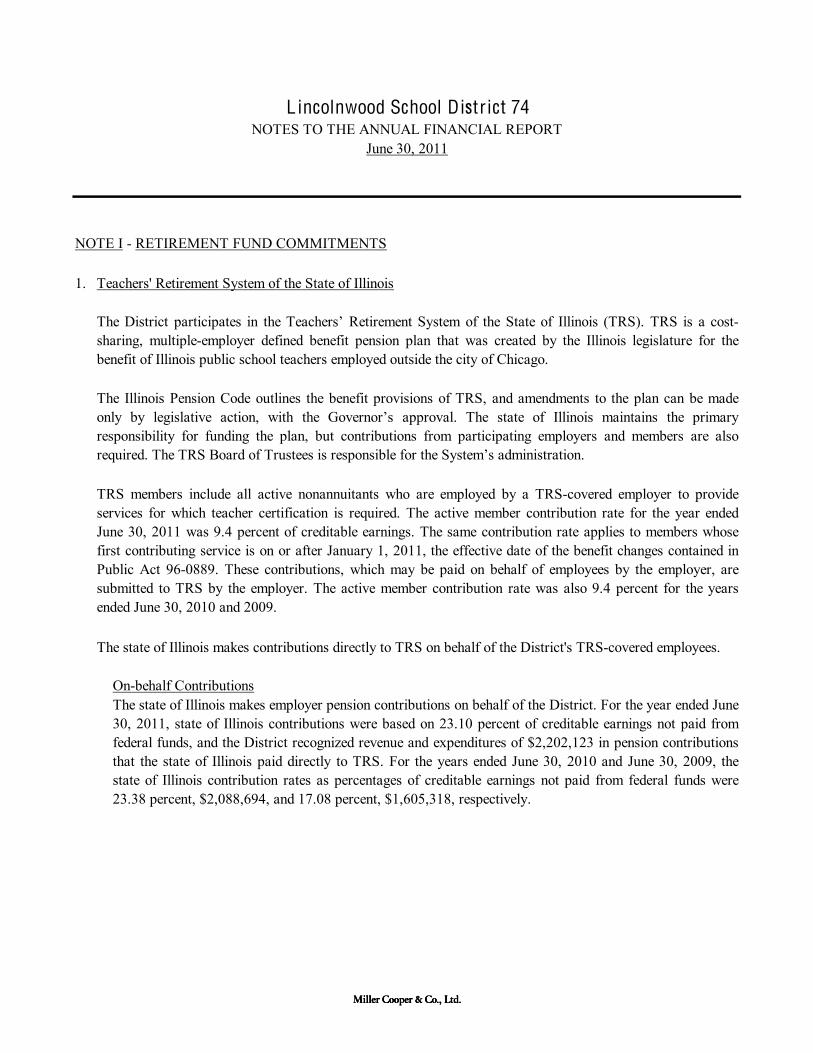

The state of Illinois makes contributions directly to TRS on behalf of the District's TRS-covered employees.

On-behalf ContributionsThe state of Illinois makes employer pension contributions on behalf of the District. For the year ended June30, 2011, state of Illinois contributions were based on 23.10 percent of creditable earnings not paid fromfederal funds, and the District recognized revenue and expenditures of $2,202,123 in pension contributionsthat the state of Illinois paid directly to TRS. For the years ended June 30, 2010 and June 30, 2009, thestate of Illinois contribution rates as percentages of creditable earnings not paid from federal funds were23.38 percent, $2,088,694, and 17.08 percent, $1,605,318, respectively.

TRS members include all active nonannuitants who are employed by a TRS-covered employer to provideservices for which teacher certification is required. The active member contribution rate for the year endedJune 30, 2011 was 9.4 percent of creditable earnings. The same contribution rate applies to members whosefirst contributing service is on or after January 1, 2011, the effective date of the benefit changes contained inPublic Act 96-0889. These contributions, which may be paid on behalf of employees by the employer, aresubmitted to TRS by the employer. The active member contribution rate was also 9.4 percent for the yearsended June 30, 2010 and 2009.

Teachers' Retirement System of the State of Illinois

The Illinois Pension Code outlines the benefit provisions of TRS, and amendments to the plan can be madeonly by legislative action, with the approval. The state of Illinois maintains the primaryresponsibility for funding the plan, but contributions from participating employers and members are also

The District participates in the Retirement System of the State of Illinois (TRS). TRS is a cost-sharing, multiple-employer defined benefit pension plan that was created by the Illinois legislature for thebenefit of Illinois public school teachers employed outside the city of Chicago.

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

NOTE I - RETIREMENT FUND COMMITMENTS (Continued)

1.

The District makes other types of employer contributions directly to TRS.

2.2 Formula Contributions

Federal and Special Trust Fund Contributions

Early Retirement Option (ERO)

Teachers' Retirement System of the State of Illinois (Continued)

The District is also required to make one-time employer contributions to TRS for members retiring underthe Early Retirement Option (ERO). The payments vary depending on the age and salary of the member.

For the year ended June 30, 2011, the District paid $0 to TRS for employer contributions under the EROprogram. For the years ended June 30, 2010 and June 30, 2009, the District paid $0 and $0, respectively, inemployer ERO contributions.

Employers contribute 0.58 percent of total creditable earnings for the 2.2 formula change. This rate isspecified by statute. Contributions for the year ended June 30, 2011 were $55,291. Contributions for theyears ended June 30, 2010 and June 30, 2009 were $51,815 and $54,513, respectively.

For the year ended June 30, 2011, the employer pension contribution was 23.10 percent of salaries paidfrom federal and special trust funds. For the years ended June 30, 2010 and 2009, the employer contribution was 23.38 and 17.08 percent, respectively, of salaries paid from federal and special trust funds. For theyear ended June 30, 2011, salaries totaling $0 were paid from federal and special trust funds that requiredemployer contributions of $0. For the years ended June 30, 2010 and June 30, 2009, required Districtcontributions were $0 and $0, respectively.

The maximum employer ERO contribution is 117.5 percent and applies when the member is age 55 atretirement.

When TRS members are paid from federal and special trust funds administered by the District, there is astatutory requirement for the District to pay an employer pension contribution from those funds. Under apolicy adopted by the TRS Board of Trustees that was first effective for the fiscal year ended June 30,2006, employer contributions for employees paid from federal and special trust funds will be the same asthe state contribution rate to TRS.

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

NOTE I - RETIREMENT FUND COMMITMENTS (Continued)

1.

Salary Increased Over 6 percent and Excess Sick Leave

If an employer grants salary increases over 6 percent and those salaries are used to calculate a finalaverage salary, the employer makes a contribution to TRS. The contribution will cover the difference inactuarial cost of the benefit based on actual salary increases and the benefit based on salary increases of upto 6 percent.

TRS financial information, an explanation of TRS benefits, and descriptions of member, employer, and statefunding requirements can be found in the TRS Comprehensive Annual Financial Report for the year endedJune 30, 2010. The report for the year ended June 30, 2011 is expected to be available in late 2011.

Further Information on TRS

If an employer grants sick leave days in excess of the normal annual allotment and those days are used asTRS service credit, the employer makes a contribution to TRS. The contribution is based on the number ofexcess sick leave days used as service credit, the highest salary used to calculate final average salary, andthe TRS total normal cost rate (18.03 percent of salary during the year ended June 30, 2011, as recertifiedpursuant to Public Act 96-1511).

The reports may be obtained by writing to the Retirement System of the State of Illinois, 2815 WestWashington Street, P.O. Box 19253, Springfield, Illinois 62794-9253. The most current report is alsoavailable on the TRS Web site at http://trs.illinois.gov.

For the year ended June 30, 2011, the District paid $0 to TRS for sick leave days granted in excess of thenormal annual allotment. For the years ended June 30, 2010 and June 30, 2009, the District paid $0 and $0,respectively, in employer contributions granted for sick leave days.

For the year ended June 30, 2011, the District paid $0 to TRS for employer contributions due on salaryincreases in excess of 6 percent. For the years ended June 30, 2010 and June 30, 2009, the District paid $0and $0, respectively, to TRS for employer contributions due on salary increases in excess of 6 percent.

Teachers' Retirement System of the State of Illinois (Continued)

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

NOTE I - RETIREMENT FUND COMMITMENTS (Continued)

1.

On-behalf Contributions to the THIS Fund

THIS Fund Employer Contributions

The percentage of employer-required contributions in the future will be determined by the Director of HFS andwill not exceed 105 percent of the percentage of salary actually required to be paid in the previous fiscal year.

Teachers' Retirement System of the State of Illinois (Continued)

The state of Illinois makes employer retiree health insurance contributions on behalf of the District. Statecontributions are intended to match contributions to the THIS Fund from active members, which were 0.88percent of pay during the year ended June 30, 2011. State of Illinois contributions were $83,890, and theDistrict recognized revenue and expenditures of this amount during the year.

The District participates in the Teachers' Health Insurance Security (THIS) Fund, a cost-sharing, multiple-employer defined benefit postemployment healthcare plan that was established by the Illinois legislature for thebenefit of Illinois public school teachers employed outside the city of Chicago. The THIS Fund providesmedical, prescription, and behavioral health benefits, but it does not provide vision, dental, or life insurancebenefits to annuitants of the Retirement System (TRS). Annuitants may participate in the state-administered participating provider option plan or choose from several managed care options.

The State Employees Group Insurance Act of 1971 (5 ILCS 375) outlines the benefit provisions of the THISFund and amendments to the plan can be made only by legislative action, with the approval. TheIllinois Department of Healthcare and Family Services (HFS) and the Illinois Department of CentralManagement Services (CMS) administer the plan, with the cooperation of TRS. The Director of HFSdetermines the rates and premiums for annuitants and dependent beneficiaries and establishes the cost-sharingparameters. Section 6.6 of the State Employees Group Insurance Act of 1971 requires that all activecontributors to the TRS who are not employees of the state make a contribution to the THIS Fund.

State contributions intended to match active member contributions during the years ended June 30, 2010and June 30, 2009 were 0.84 percent of pay. State contributions on behalf of District employees were$75,043 and $78,950, respectively.

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

NOTE I - RETIREMENT FUND COMMITMENTS (Continued)

1.

Employer Contributions to the THIS Fund

2.

Funding Policy

Further Information on the THIS Fund

THIS Fund Employer Contributions (Continued)

Plan DescriptionThe District's defined benefit pension plan for regular employees provides retirement and disability benefits,postretirement increases, and death benefits to plan members and beneficiaries. The District's plan is affiliatedwith the Illinois Municipal Retirement Fund (IMRF), an agent, multiple-employer plan. Benefit provisions areestablished by statute and may only be changed by the General Assembly of the State of Illinois. IMRFissues a publicly available financial report that includes financial statements and required supplementaryinformation. That report may be obtained on-line at www.imrf.org.

The District also makes contributions to the THIS Fund. The employer THIS Fund contribution was 0.66percent during the year ended June 30, 2011 and 0.63 percent during the years ended June 30, 2010 andJune 30, 2009. For the year ended June 30, 2011, the District paid $62,918 to the THIS Fund. For the yearsended June 30, 2010 and June 30, 2009, the District paid $56,282 and $59,213, respectively, to the THISFund, which was 100 percent of the required contribution.

The publicly available financial report on the THIS Fund may be obtained by writing to the Department ofHealthcare and Family Services, 201 S. Grand Ave., Springfield, Illinois 62763-3838.

Illinois Municipal Retirement Fund

Teachers' Retirement System of the State of Illinois (Continued)

As set by state statute, the District's regular plan members are required to contribute 4.5 percent of theirannual covered salary. The statute requires the District to contribute the amount necessary, in addition tomember contributions, to finance the retirement coverage of its own employees. The contribution rate forcalendar year 2010 used by the employer was 8.50 percent of annual covered payroll. The District annualrequired contribution rate for calendar year 2010 was 14.20 percent. The District also contributes fordisability benefits, death benefits, and supplemental retirement benefits, all of which are pooled at the IMRFlevel. Contribution rates for disability and death benefits are set by the IMRF Board of Trustees, while thesupplemental retirement benefits rate is set by state statute.

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

NOTE I - RETIREMENT FUND COMMITMENTS (Continued)

2.

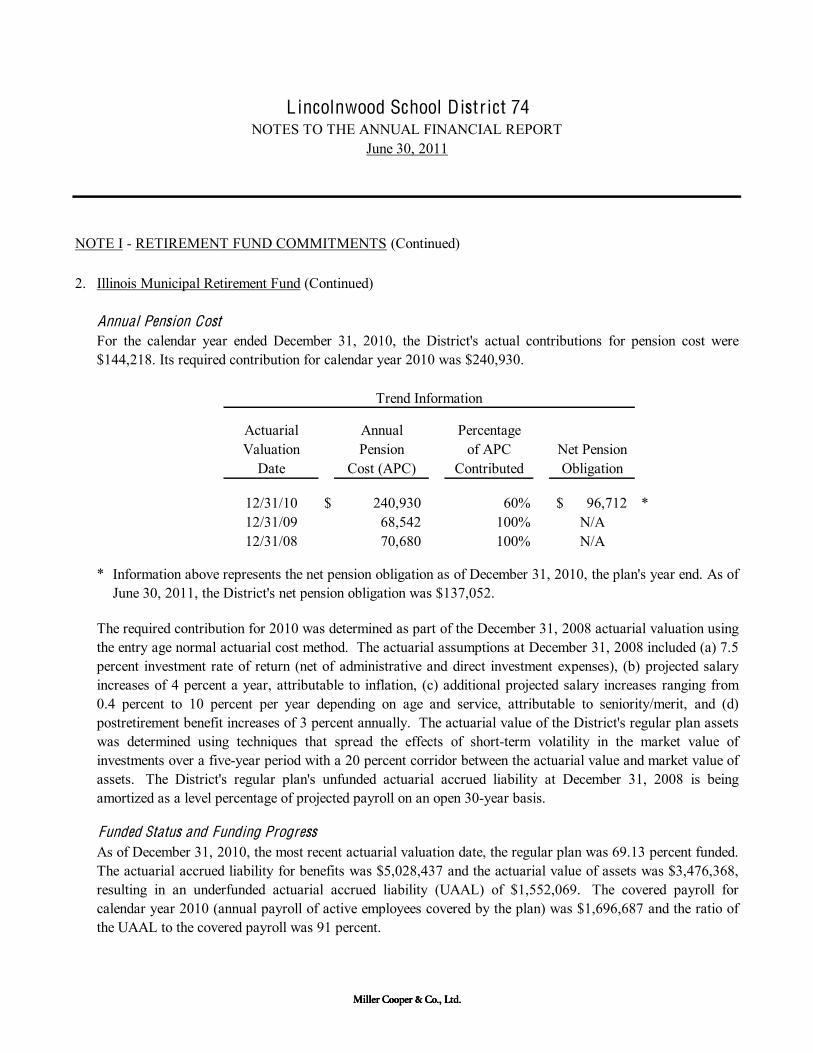

Actuarial Annual PercentageValuation Pension of APC Net Pension

Date Cost (APC) Contributed Obligation

12/31/10 $ 240,930 60% 96,712$ *12/31/09 68,542 100% N/A12/31/08 70,680 100% N/A

*

Trend Information

Annual Pension Cost

Illinois Municipal Retirement Fund (Continued)

For the calendar year ended December 31, 2010, the District's actual contributions for pension cost were$144,218. Its required contribution for calendar year 2010 was $240,930.

As of December 31, 2010, the most recent actuarial valuation date, the regular plan was 69.13 percent funded.The actuarial accrued liability for benefits was $5,028,437 and the actuarial value of assets was $3,476,368,resulting in an underfunded actuarial accrued liability (UAAL) of $1,552,069. The covered payroll forcalendar year 2010 (annual payroll of active employees covered by the plan) was $1,696,687 and the ratio ofthe UAAL to the covered payroll was 91 percent.

Information above represents the net pension obligation as of December 31, 2010, the plan's year end. As ofJune 30, 2011, the District's net pension obligation was $137,052.

The required contribution for 2010 was determined as part of the December 31, 2008 actuarial valuation usingthe entry age normal actuarial cost method. The actuarial assumptions at December 31, 2008 included (a) 7.5percent investment rate of return (net of administrative and direct investment expenses), (b) projected salaryincreases of 4 percent a year, attributable to inflation, (c) additional projected salary increases ranging from0.4 percent to 10 percent per year depending on age and service, attributable to seniority/merit, and (d)postretirement benefit increases of 3 percent annually. The actuarial value of the District's regular plan assetswas determined using techniques that spread the effects of short-term volatility in the market value ofinvestments over a five-year period with a 20 percent corridor between the actuarial value and market value ofassets. The District's regular plan's unfunded actuarial accrued liability at December 31, 2008 is beingamortized as a level percentage of projected payroll on an open 30-year basis.

Funded Status and Funding Progress

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

NOTE I - RETIREMENT FUND COMMITMENTS (Continued)

3.

NOTE J - OTHER POSTEMPLOYMENT BENEFITS

Funding Policy

Social Security/Medicare

The contributions by the District are negotiated between the District and union representatives. The District'sinsurance benefits cease at age 65 for all retirees. Educational Support Retirees who are Medicare eligible mayaccess a Medicare supplemental policy through the District and must pay the entire cost. For fiscal year 2011,total retiree postemployment contributions were $178,892.

The District pays the premium for healthcare insurance in the State of Illinois' Teachers' Retirement System planfor qualified retirees. The teacher must have insurance through the District at the time of retirement. Theemployee moves off the District's plan and onto the TRS insurance program and the District pays the premiumsuntil the employee reaches age 65. Effective in 2009, both the Teachers' Retirement System (TRS) and the IllinoisMunicipal Retirement (IMRF) retirees may access the health insurance plan during retirement years. If a retireeelects to leave the health plan, he/she may not return to the plan in a future year. Retirees also receive dental andlife insurance benefits until age 65. For 2011, a total of 19 former employees, some with spouses, accessed apostemployment benefit through the District.

Plan Description

Employees not qualifying for coverage under the Illinois Teachers' Retirement System or the Illinois MunicipalRetirement Fund are considered "nonparticipating employees". These employees and those qualifying forcoverage under the Illinois Municipal Retirement Fund are covered under Social Security/Medicare. TheDistrict paid the total required contribution for the current fiscal year.

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

NOTE J - OTHER POSTEMPLOYMENT BENEFITS (Continued)

June 30, 2011

$ 481,772

24,611

-

506,383

(284,693)

221,690

492,219

$ 713,909

The District's annual other postemployment benefit (OPEB) cost (expense) is calculated based on the annualrequired contribution of the employer (ARC), an amount actuarially determined in accordance with the parametersof GASB Statement 45. The ARC represents a level of funding that, if paid on an ongoing basis, is projected tocover normal cost each year and to amortize any unfunded actuarial liabilities (or funding excess) over a periodnot to exceed thirty years. The following tables show the components of the District's annual OPEB cost for theyear, the amount actually contributed to the plan, and changes in the District's net OPEB obligation to the RetireeHealth Plan:

Annual OPEB cost

Annual required contribution

Interest on net OPEB obligation

Net OPEB obligation end of year

Contributions made

Adjustment to annual required contribution

Annual OPEB Cost and Net OPEB Obligation

Net OPEB obligation beginning of year

Increase in net OPEB obligation

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

NOTE J - OTHER POSTEMPLOYMENT BENEFITS (Continued)

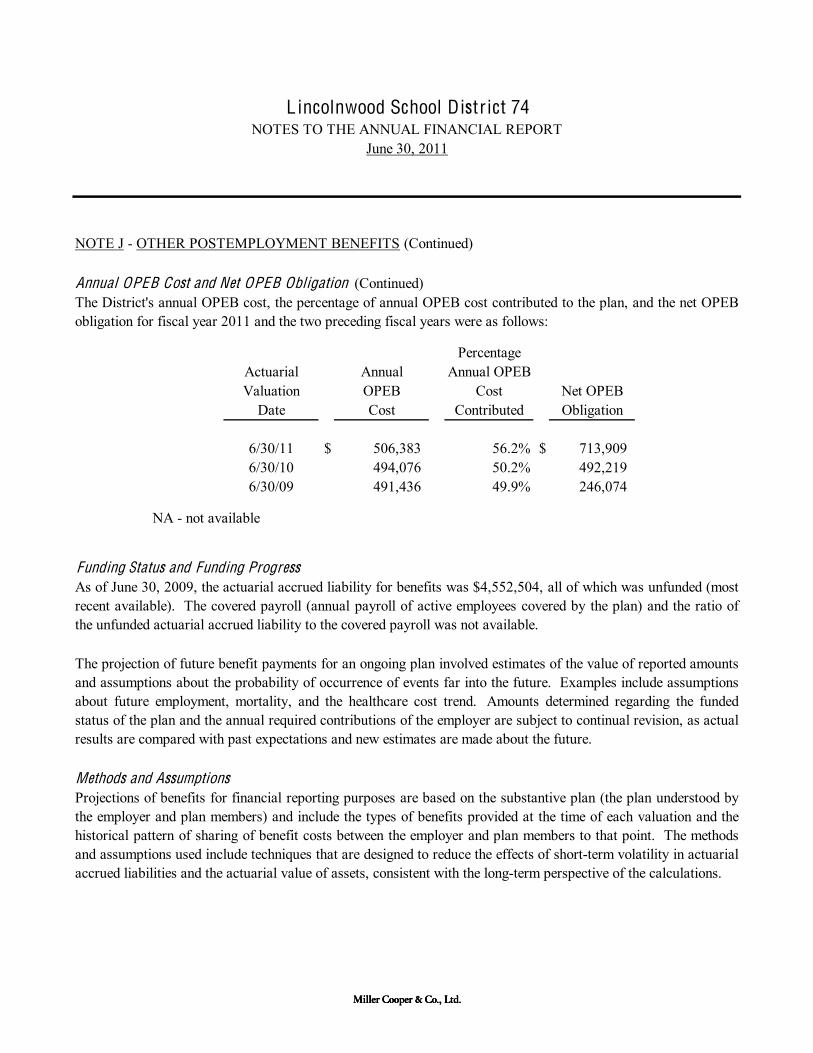

PercentageActuarial Annual Annual OPEBValuation OPEB Cost Net OPEB

Date Cost Contributed Obligation

6/30/11 $ 506,383 56.2% $ 713,909 6/30/10 494,076 50.2% 492,219 6/30/09 491,436 49.9% 246,074

Annual OPEB Cost and Net OPEB Obligation (Continued)The District's annual OPEB cost, the percentage of annual OPEB cost contributed to the plan, and the net OPEBobligation for fiscal year 2011 and the two preceding fiscal years were as follows:

As of June 30, 2009, the actuarial accrued liability for benefits was $4,552,504, all of which was unfunded (mostrecent available). The covered payroll (annual payroll of active employees covered by the plan) and the ratio ofthe unfunded actuarial accrued liability to the covered payroll was not available.

Methods and AssumptionsProjections of benefits for financial reporting purposes are based on the substantive plan (the plan understood bythe employer and plan members) and include the types of benefits provided at the time of each valuation and thehistorical pattern of sharing of benefit costs between the employer and plan members to that point. The methodsand assumptions used include techniques that are designed to reduce the effects of short-term volatility in actuarialaccrued liabilities and the actuarial value of assets, consistent with the long-term perspective of the calculations.

Funding Status and Funding Progress

The projection of future benefit payments for an ongoing plan involved estimates of the value of reported amountsand assumptions about the probability of occurrence of events far into the future. Examples include assumptionsabout future employment, mortality, and the healthcare cost trend. Amounts determined regarding the fundedstatus of the plan and the annual required contributions of the employer are subject to continual revision, as actualresults are compared with past expectations and new estimates are made about the future.

NA - not available

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

NOTE J - OTHER POST EMPLOYMENT BENEFITS (Continued)

0.00%

June 30, 2009

Entry age

30 years

Market

5.00%5.00%

The following simplifying assumptions were made:

Plan members

Retirement ages

Investment rate of return*

Healthcare inflation rate Projected salary increases

Methods and Assumptions (Continued)

Contribution rates:

Level percentage of pay, open

Remaining amortization period

Amortization period

Actuarial cost method

District

Actuarial valuation date

8.00% initial, 6.00% ultimate

*Includes inflation at 3.00%

Percentage of active employees assumed to elect benefit

Actuarial assumptions:

100%

Same rate utilized for IMRF Mortatility, Turnover, Disability,

Explicit: 100% of Premium to age 65Implicit: 20% of Premium to age 65Employer provided benefit

EE+1: $1,241/mo; Single $414/mo

Asset valuation method

Premium: 75% EE+1 +25% Single

L incolnwood School Distr ict 74NOTES TO THE ANNUAL FINANCIAL REPORT

June 30, 2011

NOTE K - INTERFUND TRANSFERS

NOTE L - CONTINGENCIES

1. Litigation

2. Grants

NOTE M - PRIOR PERIOD ADJUSTMENT

NOTE N - SUBSEQUENT EVENTS

The District recorded a prior period adjustment to properly record the value of capital assets based on aninventory taken as of June 30, 2011. The net effect of the prior period adjustment was a decrease in net book valueof capital assets $3,532,212.

Management has evaluated subsequent events through October 27, 2011, the date that these financial statementswere available to be issued. Management has determined that no events or transactions have occurred subsequentto the statement of position date that require disclosure in the financial statements.

Amounts received or receivable from grantor agencies are subject to audit and adjustment by grantor agencies,principally the federal government. Any disallowed claims, including amounts already collected, mayconstitute a liability of the applicable funds. The amount, if any, of expenditures which may be disallowed bythe grantor cannot be determined at this time, although the District expects such amounts, if any, to beimmaterial.

The District is not involved in any significant litigation that would materially affect the balances reported atJune 30, 2011. With regard to other pending matters, the eventual outcome and related liability, if any, are notdeterminable at this time. No provision has been made in the accompanying financial statements for settlementcosts.

The District transferred $200,000 to the Capital Projects Fund from the Operations and Maintenance Fund. Thetransferred amounts were to pay for current and future capital projects.

The District transferred interest earned in the amount of $100,000 to the Debt Service Fund from the WorkingCash Fund at June 30, 2011.