iron ore price

TRANSCRIPT

Prepared by Amber Nelson, Global Mining & Metals Center INTERNAL USE ONLY

August – December 2013

Global Mining & Metals Center

EY iron ore commodity briefcase

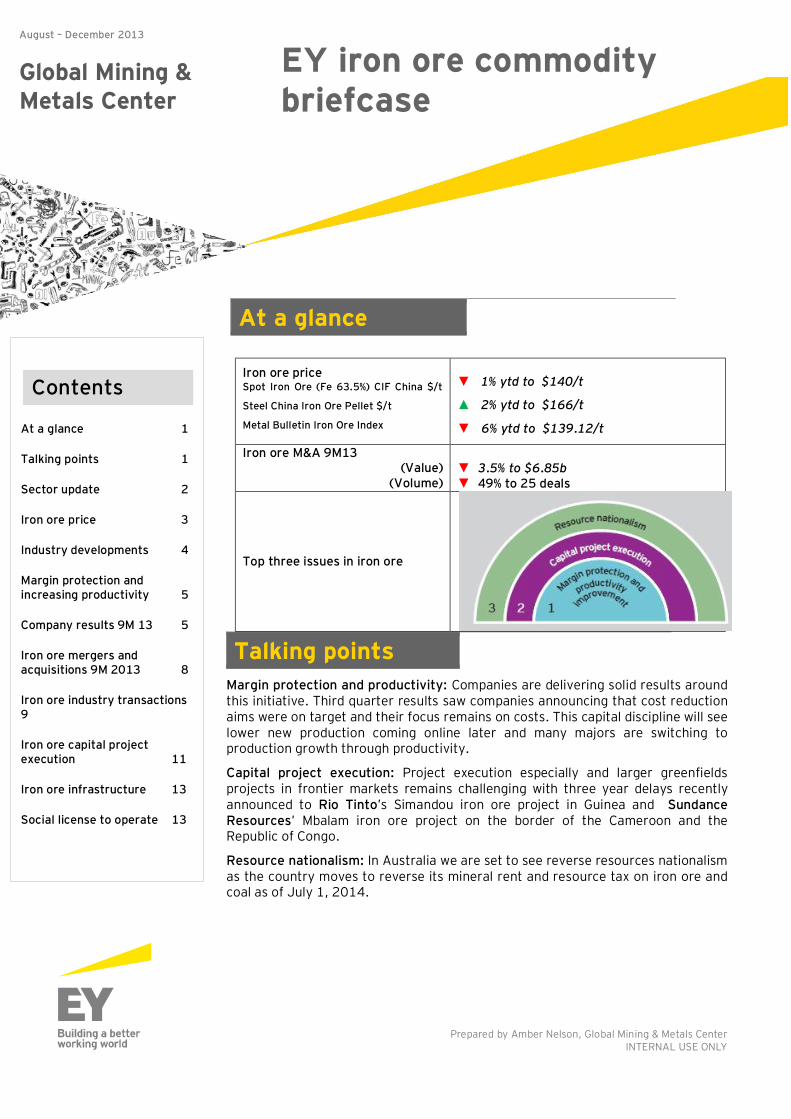

At a glance

Talking points Margin protection and productivity: Companies are delivering solid results around this initiative. Third quarter results saw companies announcing that cost reduction aims were on target and their focus remains on costs. This capital discipline will see lower new production coming online later and many majors are switching to production growth through productivity.

Capital project execution: Project execution especially and larger greenfields projects in frontier markets remains challenging with three year delays recently announced to Rio Tinto’s Simandou iron ore project in Guinea and Sundance Resources’ Mbalam iron ore project on the border of the Cameroon and the Republic of Congo.

Resource nationalism: In Australia we are set to see reverse resources nationalism as the country moves to reverse its mineral rent and resource tax on iron ore and coal as of July 1, 2014.

Iron ore price Spot Iron Ore (Fe 63.5%) CIF China $/t

Steel China Iron Ore Pellet $/t

Metal Bulletin Iron Ore Index

▼ 1% ytd to $140/t

▲ 2% ytd to $166/t

▼ 6% ytd to $139.12/t

Iron ore M&A 9M13 (Value)

(Volume)

▼ 3.5% to $6.85b ▼ 49% to 25 deals

Top three issues in iron ore

At a glance 1

Talking points 1

Sector update 2

Iron ore price 3

Industry developments 4

Margin protection and increasing productivity 5

Company results 9M 13 5

Iron ore mergers and acquisitions 9M 2013 8

Iron ore industry transactions 9

Iron ore capital project execution 11

Iron ore infrastructure 13

Social license to operate 13

Contents

EY Iron Ore Briefcase August – December 2013

2 Produced by Amber Nelson, Global Mining & Metals Center

INTERNAL USE ONLY

Sector update The recent iron ore price rally was greater than expected due to strong restocking by Chinese steel mills. Prices could be sustained with continued restocking ahead of the Chinese winter before possibly dropping back due to lower Chinese steel production during its winter. Growing production As iron ore production is increasing many analysts now see the market being balanced as new supply is absorbed by growth in steel demand. Australia is a key driver of this supply growth with Rio Tinto’s increasing production to 290mtpy, BHP Billiton completing the ramp up of its 35mtpy Jimblebar expansion (taking its capacity to 220mtpy), and Fortescue Metals Group (FMG) reaching production of 155mtpy. Fourth quarter exports are expected to be around 68.5mt compared to 56.5mt in the second quarter. Stronger 2013 supply growth is however offset by the loss of around 40mt of domestic supply in China. In total over the next three years there is a potential 440mtpy of iron ore capacity due online however delays due to a range of issues including permitting, environmental hold ups, execution challenges and production cuts from high cost producers, will make that closer to 350mtpy. In 2014, 12mtpy of new production is due from Vale's 40mtpy Northern System and a further 7mtpy from African Minerals. There will also be 12mt of supply hitting the market from India after the country’s Supreme Court recently cleared the export of stockpiled iron ore from the state of Goa. This trend continues into 2015 with production increase from BHP Billiton in Australia and around 40mt of capacity will be added in Brazil by Anglo American, Vale and Usiminas. Higher cash costs to push Chinese production out of the market Chinese producers will be hardest hit by the new supply as they are at the top of the iron ore cost curve. Deutsche Bank estimates that 50% of Chinese production has cash costs between $95–100/t and this is likely to increase with ongoing grade decline in the country combined with inflation at around $10/t. It is estimated by Metallurgical Mines’ Association of China (MMAC) that the iron ore industry is currently at around 80% of capacity. MMAC also estimates that by 2015 55mtpy of this capacity will be uncompetitive. Thus new cheaper production is likely to push some of this out of the market cushioning some of the supply additions. Steel remains in oversupply Despite a similarly oversupplied market, crude steel production is still increasing at a higher rate than expected. Global production growth forecasts for 2013 have been increased to 3.6% in 2014, with China driving most of this production growth (an increase of 8% year on year (yoy) to August). Another consequence of the supply and demand uncertainty is a subdued M&A market for iron ore. Numbers are substantially down yoy by 49% to only 25 deals for the first nine months of the year as a result of market uncertainty.

EY Iron Ore Briefcase August – December 2013

Produced by Amber Nelson, Global Mining & Metals Center INTERNAL USE ONLY 3

Iron ore price

Source: Thomson Datastream, Company reports, Ernst & Young

Iron ore price forecasts For iron ore prices, forecasts and much more, please see our new Iron ore CHS page (Internal EY only)

80

100

120

140

160

180

US

$ pe

r ton

ne

Metal Bulletin Iron Ore Index

Steel China Iron Ore Pellet $/t

2013 average $136/t 2012 average $129.5/t

EY Iron Ore Briefcase August – December 2013

Produced by Amber Nelson, Global Mining & Metals Center INTERNAL USE ONLY 4

Industry developments India ► India's Supreme Court has allowed the sale of over 11mt of stockpiled iron ore but has upheld a ban on iron

ore mining in Goa which has now been ongoing for over 14 months. The low grade inventory held by Goa’s miners could now be auctioned and it is likey to be exported as it is unsuitable for most Indian steel mills and also likely to have a large discount to spot prices. The Court proceedings also set up a panel to determine an output limit for Goa which will submit an interim report by 15 February 2014. Analysts see some recovery in India’s iron ore exports with Macquarie forecasting 25mt in 2014 increasing to as much as 40mt in 2015, down from the record 117mt exported to the year ending March 2010.1

► Seperately the Indian Government has said it will not be removing the 30% duty on iron ore exports as whilst it is keeping iron ore shipments lower it does help availability for local steel mills.There had been earlier calls to find ways to revive iron ore exports, as India has fallen from being the third largest exporter to only exporting 18mt last fiscal year.2

► The Indian Steel Ministry has reviewed its plan to reach steel production of 300mtpy by 2025 and identified iron ore availability as one of the key challenges. The Ministry believes it will have to import iron ore to meet growing domestic demand. India’s current production capacity is around 90mtpy, for which it requires around 140mt of iron ore.3

China ► China is set to launch the first yuan denominated iron ore futures contract however the move could threaten

the $28b swaps market. The Dalian Commodity Exchange is set to offer the contract before the end of 2013. Being yuan-denominated the futures contract will tap a growing hedging appetite in China. So far a lack of a domestic hedging mechanism has meant Chinese companies are using US dollar cash-settled swaps from the Singapore Exchange and CME Group.4

► China Iron and Steel Association (CISA) has said that miners are manipulating index pricing by reducing volumes sold by long-term tenders in order to push up global index prices. To stop this CISA is pushing Chinese steel mills to buy more iron ore using spot trading platforms. The accusations follow ones in March accusing top miners and traders of manipulating prices. China has been trying to encourage more trade on its platform run by China Beijing International Mining Exchange (CBMX), but trading on the platform has remained relatively low.5

► China also has plans to launch a daily iron ore index from 2014 apart from the weekly index it has been publishing since 2011. However its weekly pricing index has not been popular as mills, traders and miners prefer index prices from popular suppliers like Platts and Metal Bulletin.6

1 India keeps ban on Goa iron ore mining, allows inventory sales, Reuters News, 12 November 2013 2 India to keep iron ore export duty at 30 pct -finance minister, Reuters News, 29 September 2013 3 India may have to start importing iron ore soon: Steel Ministry, The Hindu, 25 November 2013 4 China's planned iron ore futures a threat to dominant swaps market, Reuters News, 8 October 2013 5 China urges mills to buy more iron ore via spot platforms, Reuters News, 24 September 2013 6 China plans daily iron ore price index in 2014 -CISA official, Reuters News, 11 December 2013

EY Iron Ore Briefcase August – December 2013

Produced by Amber Nelson, Global Mining & Metals Center INTERNAL USE ONLY 5

Corporate Vale to pay $9.61b in back taxes Vale has agreed to pay 22.325b reais ($9.61b) in back taxes from profits from overseas operations. A payment plan has been agreed with tax authorities which will see payments made over 15 years, starting with 5.965b reais, or 27%, due November 2013. The rest will be made in 179 monthly payments.7 ArcelorMittal looses case against government of Senegal Senegal has won a case against ArcelorMittal after the International Chamber of Commerce ruled in its favour saying it was entitled to terminate a $2.2b agreement to develop an iron ore project with the company. A new arbitration will now rule on ArcelorMittal’s liability and the amount of damages that could be awarded. The Company has said it will vigorously defend itself against any such claims. The Senegal government could seek up to $750m in relief according to reports. In 2007 the government of Senegal and ArcelorMittal signed an agreement to develop a 25mtpy iron ore project including a port and rail line, ArcelorMittal put the project on hold in 2009 due to the economic environment and studies showing the project to be less attractive than envisaged.8 Kumba and ArcelorMittal settle supply deal after years of dispute After years of ongoing dispute ArcelorMittal South Africa (AMSA) and Anglo American majority owned Kumba Iron Ore have signed what is described as a “holistic” iron ore pricing deal. The agreement will remove the need for any arbitration over a disputed 2001 supply agreement. The deal is effective from the start of 2014 and regulates the sale of 6.25mtpy of iron ore from Kumba’s Sishen and Thabazimbi mines to AMSA’s steel mills. The ore must be supplied to specification and at a price which is the cost of production at the Sishen’s dense media separation with a 20% margin and a maximum price equal to the Sishen export parity price at the mine gate. The agreement covers the life of the Sishen mine, currently estimated at over 18 years.9 BSGR to face corruption and other allegations in December BSG Resources (BSGR) has been given a month to respond to allegations including that it paid bribes to secure contracts in Guinea with a hearing date of December 10. BSGR is fighting for the right to develop half of the Simandou iron ore deposit in Guinea and has been accused of bribing officials to win its Simandou concession in 2008. The claims have been denied by BSGR who has in turn accused the Guinean government of using the review of mining contracts to confiscate its licences.10

7 Brazil's Vale to pay $9.61bn back tax bill on overseas units, Mining Weekly, 28 November 2013 8 Senegal wins arbitration case against ArcelorMittal, Mining Journal, 13 September 2013 9 Kumba, AMSA ink 'holistic' iron-ore pricing deal following years of dispute, Mining Weekly, 5 November 2013 10 Guinea calls BSGR to December hearing on mining contracts, Mining Weekly, 6 November 2013

EY Iron Ore Briefcase August – December 2013

Produced by Amber Nelson, Global Mining & Metals Center INTERNAL USE ONLY 6

Margin protection and increasing productivity

Rio Tinto improves productivity Rio Tinto has announced good progress on cost cutting and capital allocation. These include:

• $1.8b improvement in operating cash costs in the ten months to October, and tracking to deliver a $2b target for 2013.

• $800m cut in exploration and evaluation spend in the ten months to October, exceeding the 2013 target of $750m.

• Forecast 2013 capex of less than $14b, down over 20% on 2012. In 2014 capex should fall to $11b then to $8b in2015.

• $3.3b of divestments of non-core assets announced or completed in 2013. • Headcount reduction of 3,800 since June 2012. Another 3,000 positions have been cut with divested

assets.11 Seperately Rio Tinto has said it is planning to cut cash costs at its Pilbara operations from $47/t in 2012 to as low as $35.50/t, including capital to maintain the business, by 2020. Substantial capex savings are proposed with plans to spend $140/t for each additional tonne of capacity in its plans to increase production from 290mt to 360mt down from original forecast captial intensity of $150/t. Easing inflation in Australia on labour, contractors and services along with a lower Dollar have allowed the lower forecast, along with economies of scale and technology improvements.12 See ‘Iron ore capital project execution’ section for more detail. BHP Billiton slashes capital expenditure spending BHP Billiton has said it is looking to limit its capital expenditure spending to $15b down from $21.7b in the last financial year. Chief Executive Andrew Mackenzie said the company aims to be "more clever with capital”. The budget for the FY14 year was $16.2b. Iron ore has been targeted as a key division for productivity increases where BHP Billiton is looking to grow production by around 30mt through more efficient practices.13

Company results – 9M 2013

Vale ► A strong recovery in iron ore and pellet shipments, the third largest in history, saw Vale deliver solid third quarter results.

► Operating revenues for the quarter was $12.9b up 14.5% qoq and 10.8% yoy. Underlying earnings were $3.71b up 12.9% qoq and 58.8% yoy The cash cost of iron ore – mine, plant, railway and port, after royalties – dropped to $22.10/t from $24.15/t in the previous quarter.

► For the first nine months of the year operating revenues were slighly down, 2.3%, to $35.4b but adjusted EBIT was up 9.4% to $12.5b.

► In the first nine months of the year Vale has reported total savings of $2b compared to 2012. This is through reducing operating costs by $1.126b; sales, general and administrative expenses by $621m and R&D spending by $479m.

► Iron ore produciton for the quarter was 85.89mt up 17% qoq and 2.3% yoy.14 15

Rio Tinto ► Rio Tinto had a solid quarter for iron ore with record production, shipments and rail volumes. ► Initial shipments from Cape Lambert wharf B started in August 2013, four months ahead of

schedule. ► Rio Tinto is on target to reach full run-rate production of 290mtpy by the end of the first half

of 2014. ► Iron ore production for the quarter was 68.3mt up 2% qoq and 3% yoy, production for the first

nine months of the year was 195.5mt up 4% yoy.16

BHP Billiton ► BHP Billiton produced 48.848mt up 23% yoy and 2% qoq, following record production from Western Australian Iron Ore (WAIO) for the September quarter.

► The result included first production from the Jimblebar mine, ahead of schedule.

11 Rio Tinto is delivering on its commitment to create greater value for shareholders, Rio Tinto, 3 December 2013 12 Rio set to slash costs across Pilbara iron ore production, The Australian, 4 September 2013 13 BHP Billiton CEO Looks to Cut Annual Spend Below US$15 Bln, Dow Jones Institutional News, 9 December 2013 14 Vale’s performance in 3Q13, Vale, 6 November 2013 15 A strong performance: 3Q production report, Vale, 6 November 2013 16 Rio Tinto announces strong third quarter production results, Rio Tinto, 15 October 2013

EY Iron Ore Briefcase August – December 2013

Produced by Amber Nelson, Global Mining & Metals Center INTERNAL USE ONLY 7

► Supply chain optimisation at Pilbara continues to unlock substantial value and WAIO is now expected to produce 212mt in FY14 up 5mt on previous guidance.

► The Company’s Samarco’s pellet plants in Brazil continued to operate at capacity during the quarter.17

ArcelorMittal ► ArcelorMittal has reported an EBITDA of $1.7b in 3Q13 up 24% yoy however an overall net loss of $0.2b was reported compared to a net loss of $0.8b for 3Q 2012.

► Iron ore production for the quarter was 14.9mt, up 4.5% yoy. ► Net debt increased from $16.2b as of June 30, 2013 to $17.8b as of September 30, largely

driven by investment in operating working capital and dividends paid.18

Fortescue Metals Group

► Fortescue produced 34.7mt of iron ore during the September quarter up 2% on the previous quarter and 91% yoy

► Fortescue secured a average realised cost and freight iron ore price of $121/t up from $113/t the previous quarter.

► Cash costs were down to $33.17/t due to a lower strip ratios, cost reductions and a weaker Australian Dollar.19

Anglo American

► Anglo American has announced its third quarter iron ore production has fallen 24% yoy and 16% qoq to 12.5mt, due to lower production at Sishen in South Africa.

► Sishen’s production was impacted by pit constraints and safety stoppages. Production at Kolomela however increased by 12% yoy to 2.8mt.20

► Year to date production was 31,087mt down 9% yoy.

Cliffs Natural Resources

► Cliffs Natural Resources has reported strong third quarter results, lower costs and stronger iron ore prices. Revenue were equal to 2013 at $1.55b and operating income increased by over 193% to $224m. Costs of goods sold fell 11% during the quarter and iron ore prices increased 17%.

► Iron ore production for the quarter was 10.255mt equal to 2012 and year to date production was 29.7mt down 2% on 2012.21

Top iron ore miners’ production for 9M 2013

Company Country 9M13 (mt)

Change y-o-y

Vale Brazil 226.7 -3.3% Rio Tinto UK 195.5 4%

BHP Billiton Australia 128.7 17% Fortescue Metals Group Australia 94.1 84% ArcelorMittal Luxembourg 43 2.6% Cliffs Natural Resources USA 29.7 -2%

Anglo American UK 31.09 -9% Source: Raw Materials Group, Stockholm/ www.rmg.se; company reports

17 BHP Billiton operational review for the quarter ended 30 September 2013, BHP Billiton, 22 October 2013 18 ArcelorMittal reports third quarter 2013 and nine-months 2013 results, ArcelorMittal, 7 November 2013 19 Quarterly report for the period ending 30 September 2013, Fortecue Metals Group, 17 October 2013 20 Anglo American's iron ore output down 24% in Q3, Metal Bulletin News Alert Service, 21 October 2013 21 Cliffs Natural Resources Inc. Reports Strong 2013 Third-Quarter Results on Lower Costs, Cliffs Natural Resources, 24 October 2013

EY Iron Ore Briefcase August – December 2013

Produced by Amber Nelson, Global Mining & Metals Center INTERNAL USE ONLY 8

Iron ore mergers and acquisitions – 9M 2013

► With the recovery of the iron ore price over

2013 both deal values and volumes have showed signs of recovery however are still down on 2012.

► Domestic consolidation continues in China and is likely to do so as cash costs continue to rise as a result of falling grades.

► The low deal values reflect a hesitance to proceed with larger transactions in such an uncertain price environment.

► The volatile price environment is making deal execution difficult ► Contributing factor in the failed bid by

Hanlong Mining for Sundance Resources. ► Lower valuations have seen the emergence of

new types of opportunistic buyers including private equity and financial investors ► A private equity company was part of the

syndicate that bought a minority stake in ArcelorMittal’s Canadian iron ore unit for $1.1b.

Value and volume of iron ore deals

Top five iron ore deals of 9M 2013

Outlook ► Deal values have remained low with the exception of three deals this year, which exceeded $500m, deal

values have averaged only $274m. ► The key activity in the immediate future is likely to be the divestment of assets as miners streamline

portfolios and focus on optimizing existing assets, and as steel producers seek to reduce debt ► For example, ArcelorMittal’s sale of its Canadian operations for $1.1b.

► Beyond the immediate term, steelmakers, especially from China and India, will continue to invest to ensure future supply and may use infrastructure investment to gain offtake.

► Financial investors and commodity traders are also likely to remain active investors in iron ore as lower valuations present unique opportunities.

► Companies are continuing to invest in frontier markets to secure supply.

90

392

470

699

1,115

Other

Russia

Brazil

China

Canada

Value of deals targeting iron ore by destination ($m)

92

80

158

1,109

1,327

Other

Switzerland

Russia

South …

China

Value of deals targeting iron ore by acquirer ($m)

EY Iron Ore Briefcase August – December 2013

Produced by Amber Nelson, Global Mining & Metals Center INTERNAL USE ONLY 9

Iron ore industry transactions

Chalco sells its Simandou stake to parent Chinalco Chalco plans to sell its 44.65% stake in the Simandou iron ore project in Guinea to its parent company Chinalco for $2.2b. The value of Simandou, in which Rio Tinto holds over a 50% stake, has a total value of around $7b. The prime motivator behind the sale is to remove the stake from scrutiny of stockmarket investors.22 Anglo American sells Amapa Anglo American has completed the sale of 100% of the Amapá iron ore operation in Brazil to Zamin Ferrous after securing regulatory approval and $134m. The deal was first announced in January for the sale of Anglo’s 70% interest in the Amapá however following a geological event in March at its port facility which destroyed the port shiploader infrastructure and sampling tower and killed six men the changed circumstances saw Cliffs Natural Resources agree to sell its 30% interest to Anglo. Zamin will pay Anglo a conditional deferred consideration of up to a maximum of $130m in total for this extra stake, payable over a five year period and calculated on the basis of the market price for iron ore. Anglo American will use the proceeds to pay off debt.23 24 Sale of Minas Rio no longer urgent Anglo American may no longer sell a stake of its $8.8bn Minas-Rio iron ore project in Brazil. “We’re not keen to motor too quickly. The way things are going and the better it looks, and the more inclined I am to stick with it ourselves,” said Mark Cutifani CEO of Anglo American. The company has said they still have interested parties and will continue talks.25 Glencore Xstrata takes stake in iron ore project Glencore Xstrata has signed an agreement with Canadian Solid Resources to commence due diligence on the Cehegin iron ore reserve located in Murcia, Spain. The agreement will see Solid Resources retain an 80% interest in the mine, while Glencore will get 20% and the right to purchase all production. Cehegin has a historical proven reserve of around 7mt of iron ore.26 African Minerals secures new Chinese partner in Tonkolili Chinese Tianjin Materials and Equipment Group Corporation (Tewoo), the country’s largest import and exporter will invest almost $1b in African Minerals' Tonkolili mine in Sierra Leone. Tewoo will pay $990m for a 16.5% stake in Tonkolili, valuing the project at $6b. The deal will include a 20 year offtake agreement and the creation of a joint venture to blend and market iron ore through the major Tianjin port facilities. The investment will intitially involve Tewoo paying $390m for a 10% stake in African Minerals.African Minerals will sell Tewoo a 10% stake in the project for $600m. The offtake deal is for a total of 10mtpy of iron ore, or less if the stage two expansion does not reach 35mtpy. Shandong Iron & Steel Group has also invested $1.5b in 2011 but African Minerals has had to pay Shandong compensation for not fullfilling offtake agreements and production targets set for 2012.27 Aquila seeks new project for West Pilbara Australian Aquila Resources is seeking new investors for its $7.14b West Pilbara Iron Ore Project (WPIOP), in Western Australia as there was issues with an existing partner. Partners have failed to sign off for a 2014 financial year after the project was put on hold earlier in 2013. The project is a joint venture between Aquila and AMCI (IO), which in owned by AMCI Investments and POSCO. AMCI investors may be looking to leave the project.28 Divestments

22 Simandou deal hit value, says Chalco, The Australian, 17 October 2013 23 Anglo American completes the sale of Amapá to Zamin, Anglo American, 4 November 2013 24 Anglo American agrees revised terms for sale of Amapá to Zamin, Anglo American press release, 25 September 2013 25 Anglo American in no hurry to sell stake in Minas-Rio iron ore project, Business News Americas, 29 October 2013 26 Glencore takes stake in Spanish iron ore project, Steel Business Briefing, 23 October 2013 27 UPDATE 1-China's Tewoo bets on African Minerals' Tonkolili mine, Reuters News, 26 September 2013 28 Aquila seeks new partner for $7bn Australia iron ore project, Reuters News, 13 September 2013

EY Iron Ore Briefcase August – December 2013

Produced by Amber Nelson, Global Mining & Metals Center INTERNAL USE ONLY 10

► BHP Billiton is still looking at selling its stake in the Mount Nimba iron ore deposit in Guinea. B&A Mineracao, was selected as the preferred bidder in December but talks have dragged on. BHP Billiton CEO Andrew Mackenzie has said B&A had not yet reached a decision but it is in no rush to sell assets cheaply if there is no issue with them. BHP Billiton owns over 40% stake in the joint venture behind the Mount Nimba deposit.29

► Wuhan Iron and Steel Corp (Wisco) is one of the top bidders for Rio Tinto’s Canadian iron-ore assets. The sale is for a 59% stake in Iron Ore Company of Canada (IOCC) which Rio Tinto put on the market in March estimated to be worth around $4b. Wisco is looking at the purchase potentially with partners and shows China’s continued interest in iron ore. Teck Resources and Hebei Iron and Steel have also been named amongst the bidders for IOCC.30 31

Capital raisings and debt repayments ► Brazilian Samarco Mineracao, a joint venture between Vale and BHP Billiton, has raised $700m in a

second overseas bonds issue. The ten year bonds have an annual yield of 5.9%. The raising follows a $1b bond issue in October 2012, at a lower annual yield of 4.2%.32

► Fortescue Metals Group is moving to reduce its debt, initiating early repayment of $1b of its senior unsecured notes. The early repayment of part of the $2.04b senior unsecured notes were due in 2015 and the early redemption will save FMG $70m per year in interest. The rest is expected to be retired in coming months subject to market conditions. The Company has repaid A$140m of preference shares, saving $12m in yearly intrest and the repricing of the $4.95b term loan margin to 3.25%, saving $50m. Fortescue aims to reduce its gearing to 40%.33

► Sundance Resources will raise A$40m in the issue of convertible notes and options to Noble Resources International and a consortium of investors. The money raised will ensure working capital needs are met at Mbalam-Nabeba.34

► BHP Billiton has priced a four tranche Global Bond which comprises $500m Senior Floating Rate Notes due 2016 paying interest at 3 month US Dollar LIBOR plus 25 basis points, $500m 2.050% Senior Notes due 2018, $1,500m 3.850% Senior Notes due 2023, and $2,500m 5.000% Senior Notes due 2043. The proceeds will be used for general corporate purposes.35

► Gina Rinehart’s Roy Hill iron ore project is getting closer to securing $10b in funding wth the Export-Import Bank of the United States approving a $694m funding package. However the US Congress still needs to sign off on the deal in what is seen as a formality. Funding is also being sought in South Korea and Japan. Rhinehart’s Hancock Prospecting owns 70% of Roy Hill with the remainder being owned by Posco and Marubeni Corp who have been providing funding to keep the project on track.36

► Fortescue Metals Group is halting growth in 2014 to pay off debt. Fortescue is targetting repaying between $4b - $5b in 2014 ahead of a further growth phase. Fortescue’s net debt position at 30 September 2013 was $9.3b after taking into account cash on hand of $2.8b and excluding finance leases of $0.6b.37

29 RPT-UPDATE 1-BHP says talks continue over Guinea iron ore stake sale, Reuters News, 24 October 2013 30 Wuhan Iron Mulling Purchase of Rio Tinto's Canadian Iron-Ore Assets, Dow Jones Top Energy Stories, 26 September 2013 31 Teck Resources may acquire 59% stake in Iron Ore Company from Rio Tinto, MarketLine (a Datamonitor Company), Financial Deals Tracker, 30 September 2013 32 Brazil's Samarco Raises $700M From Overseas Bonds Issue –Source, Dow Jones Institutional News, 22 October 2013 33 FMG continues ‘rapid de-gearing’, MiningNewsPremium.net, 13 November 2013 34 Sundance to raise $40M, MiningNewsPremium.net, 22 October 2013 35 BHP Billiton prices US$5.0 billion bond, BHP Billiton, 26 September 2013 36 Roy Hill digs up US credit, MiningNewsPremium.net, 19 November 2013 37 INTERVIEW-Fortescue puts debt pay back ahead of next growth spurt, Reuters News, 2 December 2013

EY Iron Ore Briefcase August – December 2013

Produced by Amber Nelson, Global Mining & Metals Center INTERNAL USE ONLY 11

Iron ore capital project execution

Australia BHP Billiton update BHP Billiton has said it will be slower and more efficient with development plans and it will not participate in joint ventures where partners are too eager to push ahead. The Company was not pushing ahead to approve the follow-on expansion in the Pilbara from 220mtpy to up to 270mtpy despite strong results from the company’s iron ore division.38 However the company has approved $301m (BHP Billiton share) to replace two shiploaders at the Nelson Point port operations in Port Hedland for the second half of 2014. The investment is to increase reliability of the inner harbour port facilities. The new shiploaders will each have a capacity of 12,500 tonnes per hour, while the exisiting loaders loaded at around 10,000 tonnes per hour, thus increasing port capacity.39 Rio Tinto slows iron ore expansion in the Pilbara Rio Tinto has announced new plans for its iron ore expansion in Australia which will slow growth and cut costs by $3b. Rio Tinto had planned to increase iron ore production in Western Australia from 260mtpy to 360mtpy by the first half of 2015. Infrastructure will expand to carry 360mtpy but production increases will be slower and come from increasing prodution at browfield sites with decisions on new mines including Silvergrass and Koodaideri deferred. Production will grow 20% by 2017, low cost growth will come on mostly by 2015 seeing production reach over 330mt that year. The new plans will see $400m invested in plant equipment and additional heavy machinery to support boosting productivity. The new production will be brought on at a capital intensity of $120-130/t, including the cost of infrastructure growth and mine capacity.40 41 Sino Iron ore moves into production Chinese CITIC Pacific is moving into production at its A$8b Sino Iron project in Western Australia. The announcement follows significant delays at the magnetite project which is several years behind schedule. There has been significant maintenance and repair issues at the development which has resulted in costly delays.42 Full ramp up delayed again at Karara Gindalbie Metals and joint-venture partner Anshan Iron and Steel (Ansteel) delayed the full ramp up of the $2.8b Karara high-grade magnetite operation in Western Australia and reduced production guidance for the second half of 2013. Magnetite production is now expected at 1.3mt-1.5mt, just below previous guidance but lower-grade hematite shipments have been increased to make up for the shortfall to 2.4mt-2.6mt. It was targetted to reach 75% of production capacity, or 6mtpy, in the March quarter of 2014. With further debottlenecking at the plant, work could take a year to complete after its approval – expected by the end of March.43

38 Mackenzie puts dampener on WA expansion, The Australian, 29 October 2013 39 BHP Billiton invests in two replacement shiploaders at West Australian Iron Ore, BHP Billiton, 25 November 2013 40 UPDATE 2-Rio Tinto to save $3 bln with delayed iron ore expansion, Reuters News, 28 November 2013 41 Rio Tinto unveils breakthrough pathway for iron ore expansion in Australia, Rio Tinto, 28 November 2013 42 CITIC moves into production, The Australian Financial Review, 1 October 2013 43 Gindalbie struggles at Karara, Mining Journal, 22 November 2013

EY Iron Ore Briefcase August – December 2013

Produced by Amber Nelson, Global Mining & Metals Center INTERNAL USE ONLY 12

Americas London Mining secures license for Greenland mine London Mining has secured a 30 year exploitation licence for its Isua iron ore project in Greenland. Isua is expected to produce 15mtpy of premium iron pellet feed concentrate to be shipped from a dedicated deep-water port. The licensing process including environmental and social impact assessments as well as a royalty structure which includes escalating rates: with the first five years at 1%, years 6 to 10 at 3%; years 11 to 15 at 4%; and 16 years and beyond 5%. London Mining will now begin the process of seeking partners for the development of the project.44 Operations start at Vale’s Carajás expansion Vale has commenced operations at Carajás Additional 40mtpy project. Vale is looking to grow its production by 50% from 306mtpy to 450mtpy by 2018. The company is hoping by increasing supply it will reduce price volatility.45

Africa Simandou to cost over $18b Internal reports have indicated that Rio Tinto’s Simandou iron ore project in Guinea will cost around $18.3b and produce for over 35 years. First production is now expected in December 2018, over three year after initial estimates of June 2015. In 2019, the mine is expected to produce 39mtpy of iron ore ramping up to 100mtpy by 2024. Production will then reduce to 50mtpy by 2054 end of the mine's life. Rio Tinto holds a majority stake in Simandou of 50.35%. The completion of Simandou is contingent on an investment framework being negotiated and an infrastructure funding plan, as Guinea has decided not to participate in the financing of the port and railway.46 Sishen expansion could be delayed Majority Anglo American owned Kumba Iron Ore has said the expansion of its Sishen pit in South Africa may be delayed by a failure to secure mining rights over Transnet's rail properties on the site. Without the rights the company would "potentially not be able to access approximately 33% of the Sishen reserve."47 Senegal seeking a new partner to develop Faleme After winning a case against ArcelorMittal to recind a $2.2b deal the government of Senegal is seeking partners to develop the Faleme iron ore mine. Faleme is estimated to have estimated iron ore reserves of about 750mt. It was planned for a port and 750km railway line to be built as part of the project.48 Bellzone in talks to secure Kalia funding Bellzone is working to secure funding for its flagship Kalia iron ore project in Guinea after completing the bankable feasibility study. The study showed that Kalia's phase one development would cost $865m and produce 7mtpy of iron ore from the second half of 2015 for ten years with exports commencing in the first half of 2016. A phase two expansion would extend mine life by 15 years and could be funded by the cash flows from the first phase. Phase two would need additional process facilities to treat lower grade oxide. There was potential for a third phase of development but this requires a bulk transport solution, including rail and port.49

44 London Mining awarded exploitation licence for Greenland project, Mining Weekly, 24 October 2013 45 Vale expects 5% surplus in global ore supply by 2020, Steel Business Briefing, 9 October 2013 46 Rio Simandou project tipped to cost $20bn, The Australian, 16 November 2013 47 Kumba says Sishen pit expansion could be delayed, Reuters News, 15 October 2013 48 Senegal seek partners for Faleme iron-ore mine, Reuters News, 29 October 2013 49 Bellzone in talks to secure Kalia funding, Mining Weekly, 17 September 2013

EY Iron Ore Briefcase August – December 2013

Produced by Amber Nelson, Global Mining & Metals Center INTERNAL USE ONLY 13

Iron ore infrastructure access

Australian regulator rules on charges for access to Fortescue infrastructure An Australian state regulator has ruled that FMG can charge Brockman Mining up to A$317m per year for use of its iron ore rail line. FMG can charge between A$84.7m and A$316.9m yearly, well below the A$576m per year FMG had said it wanted to charge.50 Sable works to secure port access for Nimba Sable Mining Africa’s majority owned West Africa Exploration SA (WAE) has signed a memorandum of understanding (MoU) with the Liberian government of Liberia for infrastructure development of its Nimba iron-ore project in Guinea. Under the MOU technical due dilligence, third-party discussions and negotiations for entering into a binding infrastructure development agreement were expected. Production is expected at Nimba in 2015 and the MOU is an important step towards this. Sable has already secured an export decree from the Guinean government authorising the export of iron-ore from Nimba through Liberia to the Port of Buchanan.51

Social licence to operate BHP Billiton fined over miner death BHP Billiton has been given a A$238,000 fine over the death of a miner at its Yandi iron ore mine in 2008. The Perth Magistrates Court also criticised the company’s safety practices and told the company it will need to pay A$125,000 in court costs after pleading guilty to breaches the Mines Safety and Inspection Act.52 BHP Billiton to combat driver fatigue BHP Billiton Iron Ore will spend A$1.5m in an effot to beat driver fatigue across its truck fleet in Western Australia. The move follows a sucessful trial with Driver State System technology which will see the company install the monitoring system across its entire fleet of trucks in the Pilbara. Fatigue is a top safety risk for miners, especially when operationg equipment during extended night shifts and is the number one cause of accidents in open cut mines.53 FMG takes over Christmas Creek operations on safety concerns FMG has taken control of the Christmas Creek ore-processing facilities run by Mineral Resources’ subsidary Crushing Services International (CSI). The move follows a fatality in August and FMG says it is working with CSI and MinRes to ensure the safe and hazard-free operation of the facilities.54 Mining companies to pay for pollution under China’s deposit system China’s deposit system will improve the environment and economy in 262 resource dependent cities by 2020 by ensuring polluters pay for pollution and damage they cause. Chinese mining operations in these regions dependent on resource extraction will pay a deposit to local governments, which will be forfeited if their activities damage the environment. The environment has been identified by the government as one of the biggesta potential sources of instability. Under the regulations covering the Shanxi province which is rich in coal, coal miners have to pay a 10 yuan ($1.64) deposit for every tonne of raw coal produced. The deposit system had accumulated 61.2b yuan by the end of 2012.55

50 Regulator sets A$317 mln cap on Fortescue rail charge for Brockman, Reuters News, 12 September 2013 51 Sable signs MoU with Liberia to develop infrastructure for Nimba, Mining Weekly, 26 November 2013 52 BHP hit with fine over worker's death, The Australian, 26 October 2013 53 BHP’s $1.5M safety investment, MiningNewsPremium.net, 4 September 2013 54 FMG steps in over safety, MiningNewsPremium.net, 24 September 2013 55 Polluting Chinese miners will be made to pay in deposit scheme, Reuters News, 3 December 2013

EY Iron Ore Briefcase August – December 2013

Produced by Amber Nelson, Global Mining & Metals Center INTERNAL USE ONLY 14

For more information please contact:

Amber Nelson Strategic Analyst – Mining and Metals [email protected] +52 55 5283 1400 x 8348

Disclaimer This report is for internal use only. This publication contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment.

The information contained in this report is dated material. Major events may have occurred since original publication that might alter the

accuracy of the report.

Originally published: December 2013 Ernst & Young’s Global Mining & Metals Center With a strong but volatile outlook for the sector, the global mining and metals industry is focused on future growth through expanded production, without losing sight of operational efficiency and cost optimization. The sector is also faced with the increased challenges of changing expectations in the maintenance of its social license to operate, skills shortages, effectively executing capital projects and meeting government revenue expectations. Ernst & Young’s Global Mining & Metals Center brings together a worldwide team of professionals to help you achieve your potential — a team with deep technical experience in providing assurance, tax, transactions and advisory services to the mining and metals sector. The Center is where people and ideas come together to help mining and metals companies meet the issues of today and anticipate those of tomorrow. Ultimately it enables us to help you meet your goals and compete more effectively. It’s how Ernst & Young makes a difference. © 2013 EYGM Limited. All Rights Reserved.