investment risks & returns in current environment

TRANSCRIPT

Investment Risks & Returnsin Current Environment

IFSWF, 9 Nov 2016

Tham Chiew Kit

Head, Total Portfolio Strategy

GIC

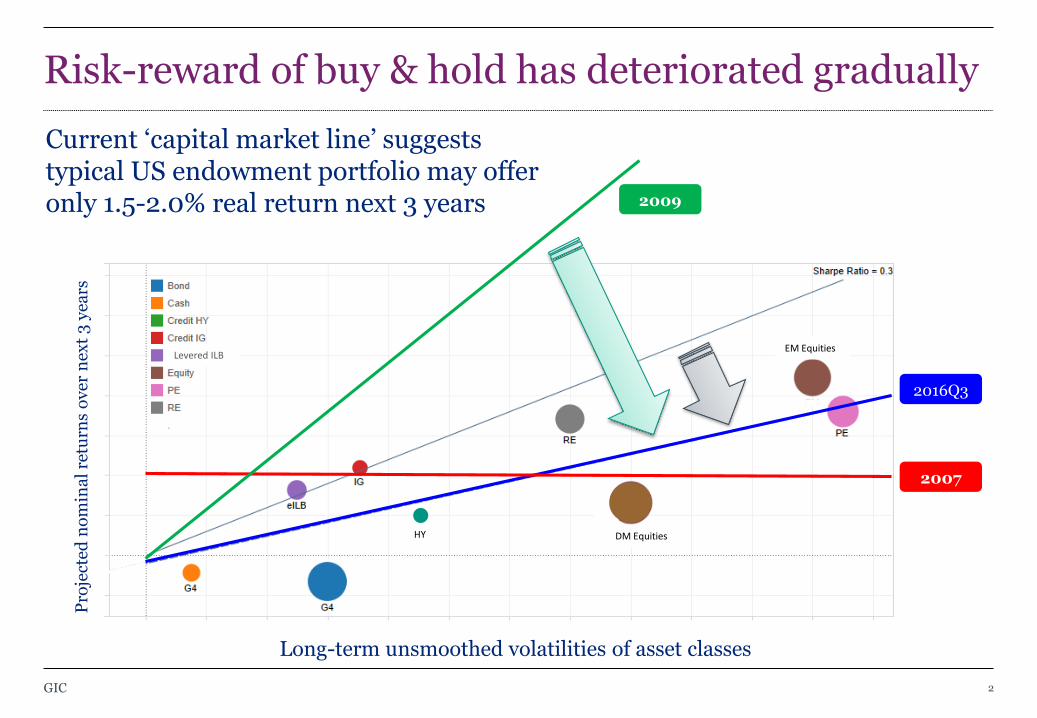

Risk-reward of buy & hold has deteriorated gradually

GIC 2

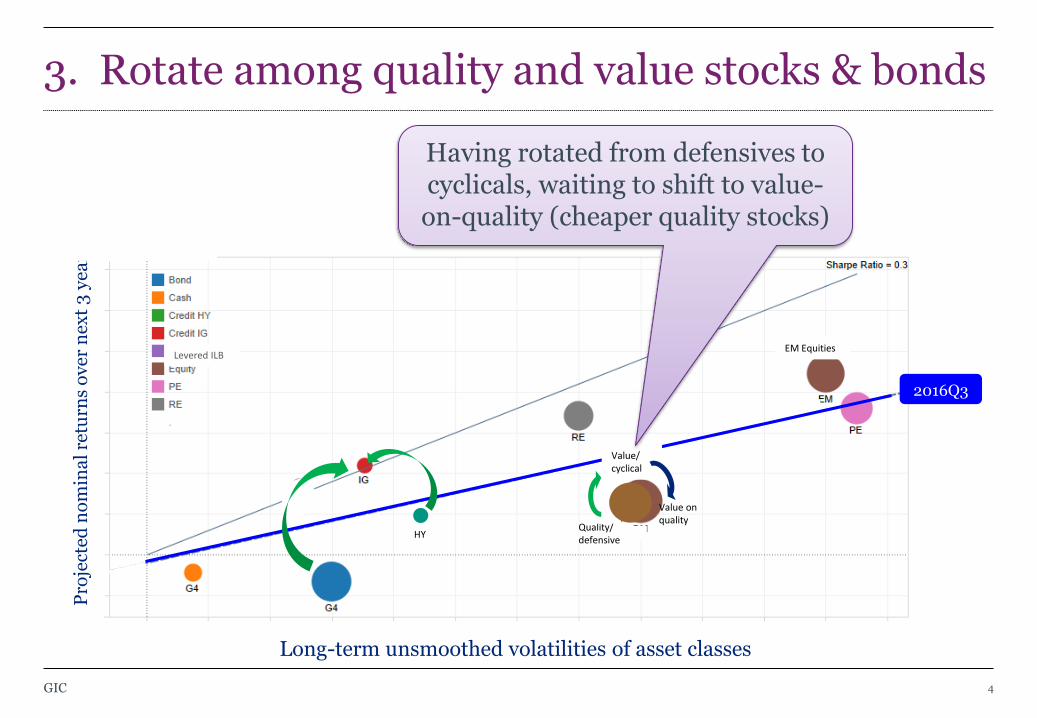

2016Q3

2007

2009

Levered ILB

DM Equities

EM Equities

Long-term unsmoothed volatilities of asset classes

Pro

ject

ed n

om

ina

l re

turn

s o

ver

nex

t 3

yea

rs

Current ‘capital market line’ suggests typical US endowment portfolio may offer only 1.5-2.0% real return next 3 years

HY

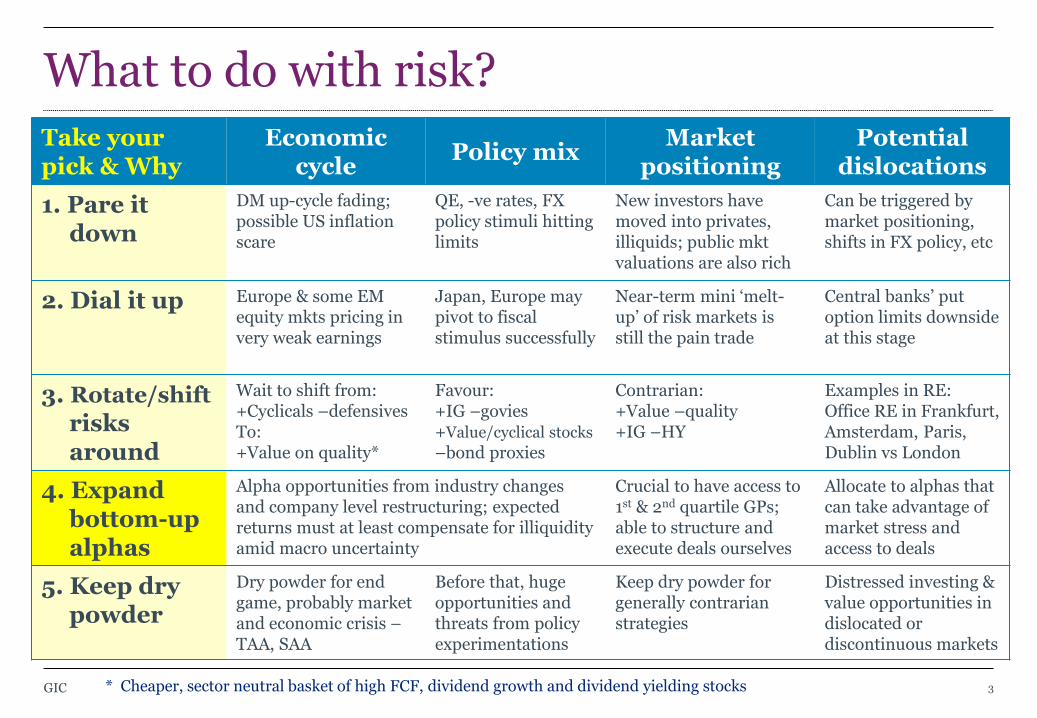

What to do with risk?

GIC 3

Take your pick & Why

Economic cycle

Policy mixMarket

positioningPotential

dislocations

1. Pare it down

DM up-cycle fading; possible US inflation scare

QE, -ve rates, FX policy stimuli hitting limits

New investors have moved into privates,illiquids; public mktvaluations are also rich

Can be triggered by market positioning, shifts in FX policy, etc

2. Dial it up Europe & some EM equity mkts pricing in very weak earnings

Japan, Europe may pivot to fiscal stimulus successfully

Near-term mini ‘melt-up’ of risk markets is still the pain trade

Central banks’ put option limits downside at this stage

3. Rotate/shift

risksaround

Wait to shift from:+Cyclicals –defensivesTo:+Value on quality*

Favour:+IG –govies+Value/cyclical stocks

–bond proxies

Contrarian:+Value –quality+IG –HY

Examples in RE: Office RE in Frankfurt, Amsterdam, Paris, Dublin vs London

4. Expand bottom-up alphas

Alpha opportunities from industry changes and company level restructuring; expected returns must at least compensate for illiquidity amid macro uncertainty

Crucial to have access to 1st & 2nd quartile GPs; able to structure and execute deals ourselves

Allocate to alphas that can take advantage of market stress and access to deals

5. Keep dry powder

Dry powder for end game, probably market and economic crisis –TAA, SAA

Before that, huge opportunities and threats from policy experimentations

Keep dry powder for generally contrarian strategies

Distressed investing & value opportunities in dislocated or discontinuous markets

* Cheaper, sector neutral basket of high FCF, dividend growth and dividend yielding stocks

3. Rotate among quality and value stocks & bonds

GIC 4

2016Q3

Levered ILB

Quality/defensive

EM Equities

Long-term unsmoothed volatilities of asset classes

Pro

ject

ed n

om

ina

l re

turn

s o

ver

nex

t 3

ye

ars

HY

Value/cyclical

Value on quality

Having rotated from defensives to cyclicals, waiting to shift to value-on-quality (cheaper quality stocks)

4. Focus on idiosyncratic, bottom-up alphas

GIC 5

2016Q3

Levered ILBEM Equities

Long-term unsmoothed volatilities of asset classes

Pro

ject

ed n

om

ina

l re

turn

s o

ver

nex

t 3

ye

ars

HYDM Equities

Positive alpha

Negative alpha

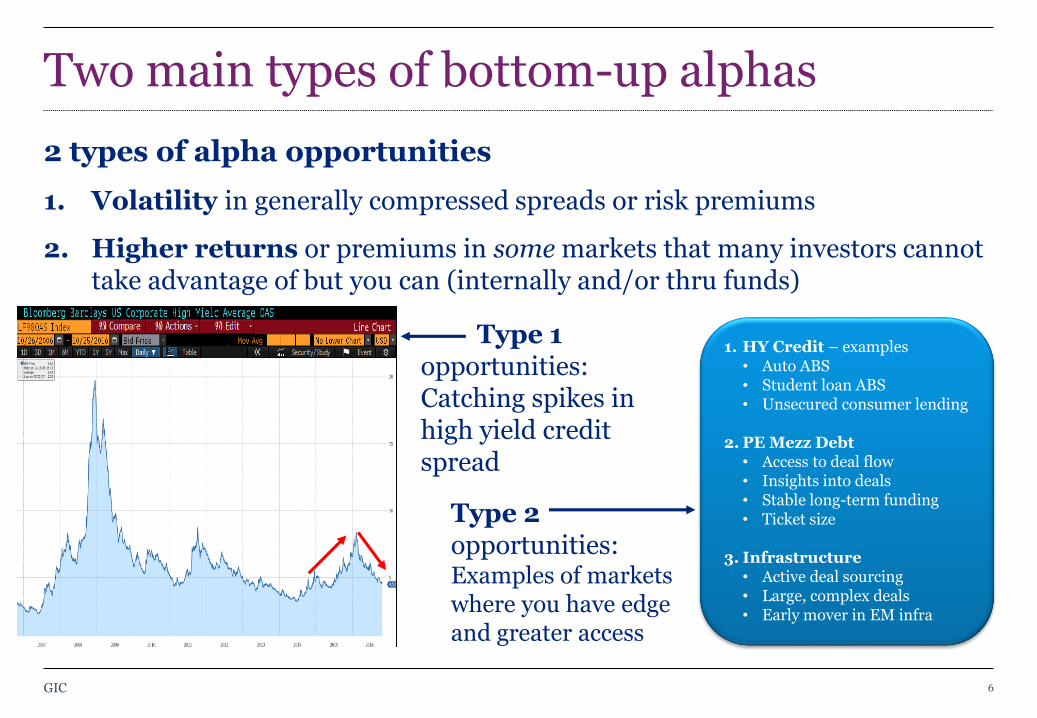

Type 2 opportunities: Examples of markets where you have edge and greater access

Two main types of bottom-up alphas

6

2 types of alpha opportunities

1. Volatility in generally compressed spreads or risk premiums

2. Higher returns or premiums in some markets that many investors cannot take advantage of but you can (internally and/or thru funds)

Type 1 opportunities: Catching spikes in high yield credit spread

1. HY Credit – examples• Auto ABS• Student loan ABS• Unsecured consumer lending

2. PE Mezz Debt • Access to deal flow• Insights into deals• Stable long-term funding• Ticket size

3. Infrastructure• Active deal sourcing• Large, complex deals• Early mover in EM infra

GIC