investment research weekly focus - danske bank · global macro and market themes ... ice brent oil...

TRANSCRIPT

Important disclosures and certifications are contained from page 16 of this report. www.danskeresearch.com

Investment Research

Market Movers ahead

Nonfarm payrolls and PCE inflation – both monitored closely by the Fed – are due for

release next week. Last month’s labour market report disappointed but we expect a

strong September reading due to low jobless claims and high ISM employment

indices. We expect core PCE to come out at 0.0% m/m and 1.4% y/y which is still

below the 2% target.

We expect the US ISM manufacturing index to decline slightly from 59.0 to 58.5,

which is still very high, indicating higher activity in the US.

The ECB meeting will deliver further details on the upcoming purchase programme of

asset-backed securities (ABS).

We expect euro area HICP inflation to decline from 0.4% y/y to 0.3% y/y due to

further decline in oil prices – a new cycle low.

The Danish FX reserves may attract some attention due to the strong krone.

Global macro and market themes

Weak euro surveys for September showed further weakness, adding to the downside

risks to growth. The weak surveys combined with very low inflation are adding to the

pressure on the ECB.

The Fed’s asset purchases programme comes to an end next month and, in this

connection, we expect the Fed to adjust its forward guidance.

The manufacturing PMI in China suggests that the Chinese slowdown may not be as

severe as previously feared.

Focus

During the week, we have published our quarterly Nordic Outlook including our new

forecasts on the Nordic economies, see Nordic Outlook – September 2014,

25 September. We have revised down our forecasts on Denmark and Sweden mainly

due to the European stagnation. In Norway, domestic demand is keeping activity on

track despite lower oil investments. The Russian recession and austerity measures are

weighing on the Finnish economy.

26 September 2014

Editors Allan von Mehren +45 4512 8055 [email protected] Steen Bocian +45 45 12 85 31 [email protected]

Weekly Focus

Tough job ahead for the ECB

Contents

Market movers ..................................................... 2

Global Macro and Market Themes .......... 6

Scandi update .................................................... 10

Latest research from Danske Bank Markets ................................................................. 11

Macroeconomic forecast ........................... 12

Financial forecast ............................................ 13

Calendar ................................................................ 14

Financial views

Source: Danske Bank

We expect a strong job report New forecasts on the Nordics

Source: US BLS, Danske Bank Markets Source: Danske Bank Markets

Major indices

26-Sep 3M 12M

10yr EUR swap 1.14 1.15 1.30

EUR/USD 127 127 125

ICE Brent oil 97 102 98

26-Sep 6M 12-24M

S&P500 1966 0-3% 5-8%

2 | 26 September 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Market movers

Global

We are heading towards a very busy week in the US, with the release of both the

September labour market report and the latest PCE figures.

Last month’s labour market report disappointed severely with an increase in non-farm

payrolls of only 142,000 despite very optimistic labour market indicators. Even if

correcting for the job loss of 17,000 due to the supermarket store strike, we still

believe the August report was too bad to be true. Low jobless claims, high ISM

employment indices as well as the increasing jobs plentiful versus hard to get balance

all suggest that the US labour market is in a considerably better condition than

reflected in last month’s report. Our model estimates an increase in non-farm payroll

in September of around 250,000 and we expect the unemployment rate to stay at

6.1%.

Moreover, we will get the latest update on the inflation pressure as the PCE figures

are due for release on Monday. The headline PCE has been closing in on the Fed’s

2.0% target through the first half of the year and the 3m AR rate is now of around

2.2%. But the consumer prices did not rise much in July and our models is suggesting

that August is going to be a low inflation month as well. We forecast a core PCE of

0.0% m/m and 1.4% y/y and low gasoline prices contribute to an expected headline

PCE of -0.1% m/m and 1.4% y/y.

The ISM manufacturing index rose to 59.0 in August – the highest level since

February 2011 – and upbeat comments in the latest report indicate optimism across a

large range of industries. We expect the ISM manufacturing index to stay at a high

level but make a small downward adjustment to 58.5. The markit PMI index is

expected to close in on the ISM with an increase to 58.5 as well. Moreover, the ISM

non-manufacturing index is also doing well, but we expect it to adjust slightly to 59.0

from 59.6 in August.

Finally, we expect consumer confidence to increase to 94.5 from 92.4 last month and

personal income and personal consumption is forecast to increase by 0.3% m/m and

0.5% m/m, respectively.

In the euro area, the ECB meeting next week will deliver further details on the

upcoming purchase programme of asset backed securities (ABS) and covered bonds.

We expect most focus to be on the new ECB soft target on the size of its balance sheet

that Draghi mentioned at the previous ECB meeting and which has been repeated by

several ECB members over the past month – an expansion of the ECB’s balance sheet

‘towards the dimensions it used to have at the beginning of 2012’. Although most

market participants view the first TLTRO take (82.6bn) as disappointing, Draghi has

commented that this allotment was well within the ECB’s expectations and that the

December auction was needed before assessing the success of the programme. We

expect him to repeat this message at the meeting. Lastly, we expect Draghi to reiterate

the Governing Council’s unanimous commitment to using additional unconventional

instruments if needed and thereby keeping the QE speculation alive.

Euro area September HICP inflation is expected to decline to 0.3% y/y from 0.4% y/y

due to a further decline in oil prices. Looking ahead, we expect inflation to pick up in

the coming months and, for that reason, the expected low September print will

Non-farm payrolls to bounce back

after last month’s weak report

Source: Macrobond

Italian sentiment points to nil growth

in Q3

Source: Macrobond

3 | 26 September 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

probably also be at a cycle low. German HICP is expected to move sideways at 0.8%

y/y with some downside risk from the movement in energy prices.

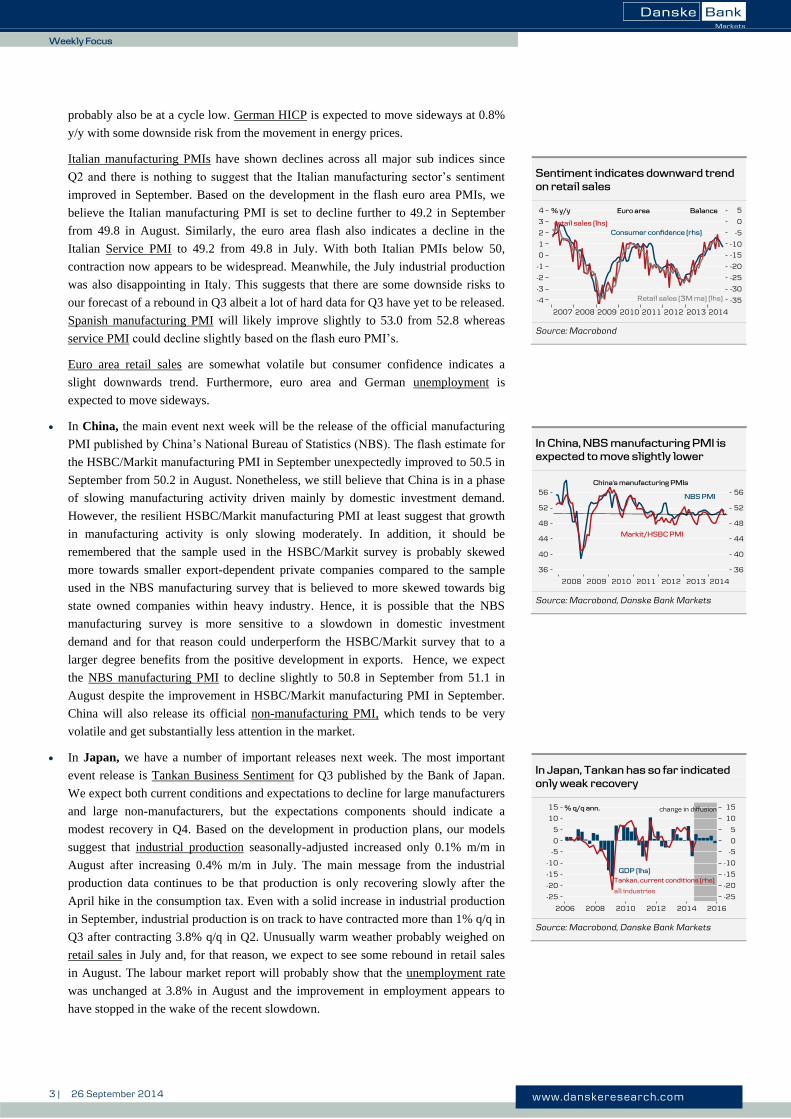

Italian manufacturing PMIs have shown declines across all major sub indices since

Q2 and there is nothing to suggest that the Italian manufacturing sector’s sentiment

improved in September. Based on the development in the flash euro area PMIs, we

believe the Italian manufacturing PMI is set to decline further to 49.2 in September

from 49.8 in August. Similarly, the euro area flash also indicates a decline in the

Italian Service PMI to 49.2 from 49.8 in July. With both Italian PMIs below 50,

contraction now appears to be widespread. Meanwhile, the July industrial production

was also disappointing in Italy. This suggests that there are some downside risks to

our forecast of a rebound in Q3 albeit a lot of hard data for Q3 have yet to be released.

Spanish manufacturing PMI will likely improve slightly to 53.0 from 52.8 whereas

service PMI could decline slightly based on the flash euro PMI’s.

Euro area retail sales are somewhat volatile but consumer confidence indicates a

slight downwards trend. Furthermore, euro area and German unemployment is

expected to move sideways.

In China, the main event next week will be the release of the official manufacturing

PMI published by China’s National Bureau of Statistics (NBS). The flash estimate for

the HSBC/Markit manufacturing PMI in September unexpectedly improved to 50.5 in

September from 50.2 in August. Nonetheless, we still believe that China is in a phase

of slowing manufacturing activity driven mainly by domestic investment demand.

However, the resilient HSBC/Markit manufacturing PMI at least suggest that growth

in manufacturing activity is only slowing moderately. In addition, it should be

remembered that the sample used in the HSBC/Markit survey is probably skewed

more towards smaller export-dependent private companies compared to the sample

used in the NBS manufacturing survey that is believed to more skewed towards big

state owned companies within heavy industry. Hence, it is possible that the NBS

manufacturing survey is more sensitive to a slowdown in domestic investment

demand and for that reason could underperform the HSBC/Markit survey that to a

larger degree benefits from the positive development in exports. Hence, we expect

the NBS manufacturing PMI to decline slightly to 50.8 in September from 51.1 in

August despite the improvement in HSBC/Markit manufacturing PMI in September.

China will also release its official non-manufacturing PMI, which tends to be very

volatile and get substantially less attention in the market.

In Japan, we have a number of important releases next week. The most important

event release is Tankan Business Sentiment for Q3 published by the Bank of Japan.

We expect both current conditions and expectations to decline for large manufacturers

and large non-manufacturers, but the expectations components should indicate a

modest recovery in Q4. Based on the development in production plans, our models

suggest that industrial production seasonally-adjusted increased only 0.1% m/m in

August after increasing 0.4% m/m in July. The main message from the industrial

production data continues to be that production is only recovering slowly after the

April hike in the consumption tax. Even with a solid increase in industrial production

in September, industrial production is on track to have contracted more than 1% q/q in

Q3 after contracting 3.8% q/q in Q2. Unusually warm weather probably weighed on

retail sales in July and, for that reason, we expect to see some rebound in retail sales

in August. The labour market report will probably show that the unemployment rate

was unchanged at 3.8% in August and the improvement in employment appears to

have stopped in the wake of the recent slowdown.

Sentiment indicates downward trend

on retail sales

Source: Macrobond

In China, NBS manufacturing PMI is

expected to move slightly lower

Source: Macrobond, Danske Bank Markets

In Japan, Tankan has so far indicated

only weak recovery

Source: Macrobond, Danske Bank Markets

4 | 26 September 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Scandi

In Denmark, a variety of data is on the agenda in the coming week. Most interesting

will be the revised national accounts figures for Q2 after the preliminary release

showed GDP contracting by 0.3%. The revision will be unusual as it follows the

major revision of the national accounts following the implementation of ESA 2010,

the new European system of national accounts. This may mean that we see slightly

bigger changes than normal. Elsewhere, the week brings figures for gross

unemployment (seasonally adjusted) and we expect a slight improvement in the

number of jobless from 134,500 in July to 134,000 in August, giving an unchanged

unemployment rate of 5.1%. There will also be news from industry in the form of

Statistics Denmark’s tendency surveys for September and housing prices for August,

although these are national figures and will not shed light on regional variations. In

addition, the Nationalbank will be releasing currency reserves data for September.

In Sweden, the week ahead kicks off on Monday morning (at 09.30 CEST) with

August retail sales, where we would be surprised not to see continued low y/y growth

as most indicators for the retail sector seem to have lost much of the momentum over

the past few weeks. Alas, we think that private consumption, albeit still positive, will

settle on a new lower pace of growth henceforth considering that 2015 is expected to

produce fiscal policy tightening and as new housing market related regulations put a

damper on growth. On Wednesday (at 08.30 CEST), we will receive another bout of

survey data in the form of manufacturing PMI. We actually do not have anything

intelligent (as if ever...) to say before the outcome other than that we expect it to stay

put in the 50-55 range. The week concludes with what we feel might be among the

most important numbers to keep up with Swedish domestic cyclical developments,

industrial production and orders (Friday, 09.30 CEST). As diligent readers are aware,

the manufacturing industry has posted a long string of disappointing data. A positive

outcome would keep our hopes up for a rebound in industrial activity during H2 but,

alas, it would do little to change the weak trend.

In Norway, the most important releases are retail sales figures for August and PMI

and NAV unemployment data for September. After strong growth earlier in the

summer, retail sales dropped sharply in July, putting paid to any ‘fears’ of an

impending consumer boom. However, we reckon the hot weather and a correction

from the strong growth in May and June were the main reasons for the fall in July.

Based on signals from the trade, we expect retail sales to grow 1.0% m/m in August.

This will still mean more or less zero growth in private consumption in Q3, but will

confirm that there is little downside risk to growth from private consumption going

forward. With oil-related industries slowing but the export industry growing more

quickly, the outlook for industry is uncertain. Time will tell which of these effects

dominates in terms of both industrial activity and GDP. So far this year, actual

industrial production has been surprisingly strong, while the PMI has painted a less

optimistic picture. This discrepancy may be because production is driven by order

books, whereas the PMI captures expectations. It is therefore reassuring that the PMI

picked up somewhat over the summer. We expect it to deteriorate somewhat now,

given the decline in European indicators and the weaker outlook for the oil sector and

predict a score of 51.0 in September. Rather surprisingly, the labour market has been

improving so far this year, but showed signs of levelling off in August. With more

and more redundancies in oil-related industries during the month, we expect

registered unemployment to come out at 2.8%, with the number of jobless rising by

Labour market on the mend

Source: Statistics Denmark

On a downward bound train...

Source: Statistics Sweden

Job losses in the oil sector

Source: Macrobond

5 | 26 September 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

300-400. Taken together, therefore, the week's data will paint a rather mixed picture,

underlining the differences now emerging between sectors, but will also go to show

that growth is holding up relatively well despite lower oil investment.

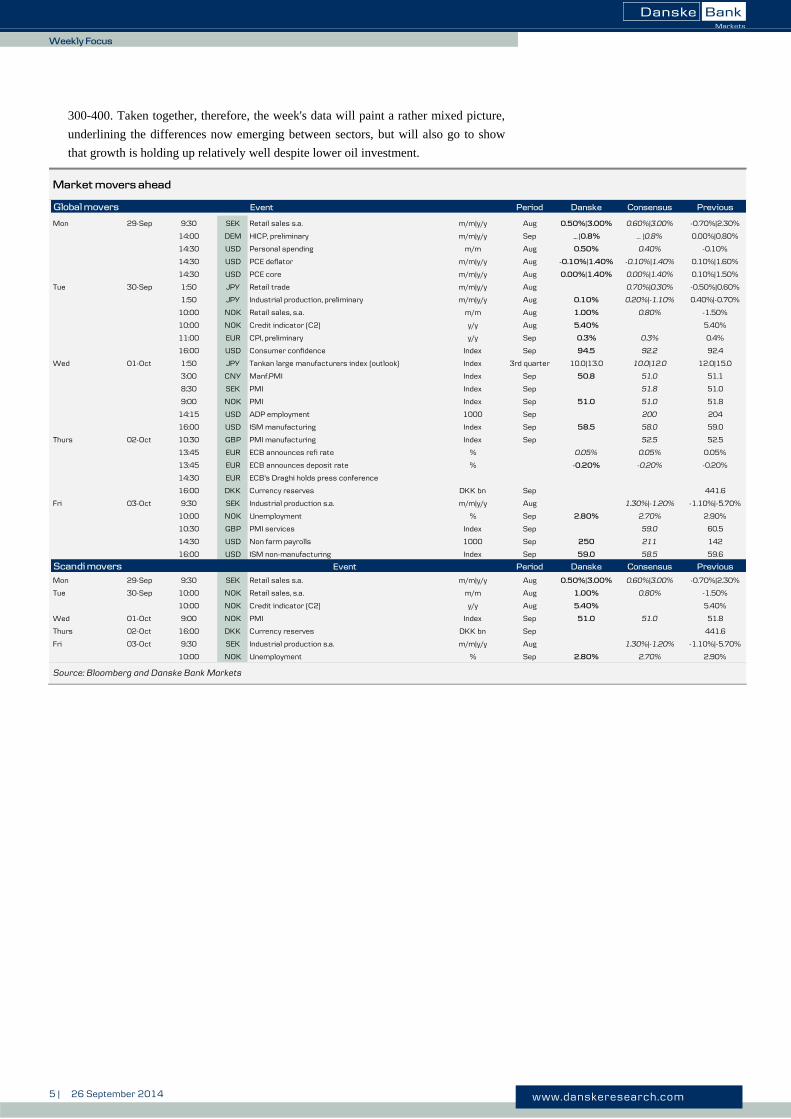

Market movers ahead

Source: Bloomberg and Danske Bank Markets

Global movers Event Period Danske Consensus Previous

Mon 29-Sep 9:30 SEK Retail sales s.a. m/m|y/y Aug 0.50%|3.00% 0.60%|3.00% -0.70%|2.30%

14:00 DEM HICP, preliminary m/m|y/y Sep … |0.8% … |0.8% 0.00%|0.80%

14:30 USD Personal spending m/m Aug 0.50% 0.40% -0.10%

14:30 USD PCE deflator m/m|y/y Aug -0.10%|1.40% -0.10%|1.40% 0.10%|1.60%

14:30 USD PCE core m/m|y/y Aug 0.00%|1.40% 0.00%|1.40% 0.10%|1.50%

Tue 30-Sep 1:50 JPY Retail trade m/m|y/y Aug 0.70%|0.30% -0.50%|0.60%

1:50 JPY Industrial production, preliminary m/m|y/y Aug 0.10% 0.20%|-1.10% 0.40%|-0.70%

10:00 NOK Retail sales, s.a. m/m Aug 1.00% 0.80% -1.50%

10:00 NOK Credit indicator (C2) y/y Aug 5.40% 5.40%

11:00 EUR CPI, preliminary y/y Sep 0.3% 0.3% 0.4%

16:00 USD Consumer confidence Index Sep 94.5 92.2 92.4

Wed 01-Oct 1:50 JPY Tankan large manufacturers index (outlook) Index 3rd quarter 10.0|13.0 10.0|12.0 12.0|15.0

3:00 CNY Manf.PMI Index Sep 50.8 51.0 51.1

8:30 SEK PMI Index Sep 51.8 51.0

9:00 NOK PMI Index Sep 51.0 51.0 51.8

14:15 USD ADP employment 1000 Sep 200 204

16:00 USD ISM manufacturing Index Sep 58.5 58.0 59.0

Thurs 02-Oct 10:30 GBP PMI manufacturing Index Sep 52.5 52.5

13:45 EUR ECB announces refi rate % 0.05% 0.05% 0.05%

13:45 EUR ECB announces deposit rate % -0.20% -0.20% -0.20%

14:30 EUR ECB's Draghi holds press conference

16:00 DKK Currency reserves DKK bn Sep 441.6

Fri 03-Oct 9:30 SEK Industrial production s.a. m/m|y/y Aug 1.30%|-1.20% -1.10%|-5.70%

10:00 NOK Unemployment % Sep 2.80% 2.70% 2.90%

10:30 GBP PMI services Index Sep 59.0 60.5

14:30 USD Non farm payrolls 1000 Sep 250 211 142

16:00 USD ISM non-manufacturing Index Sep 59.0 58.5 59.6

Scandi movers Event Period Danske Consensus Previous

Mon 29-Sep 9:30 SEK Retail sales s.a. m/m|y/y Aug 0.50%|3.00% 0.60%|3.00% -0.70%|2.30%

Tue 30-Sep 10:00 NOK Retail sales, s.a. m/m Aug 1.00% 0.80% -1.50%

10:00 NOK Credit indicator (C2) y/y Aug 5.40% 5.40%

Wed 01-Oct 9:00 NOK PMI Index Sep 51.0 51.0 51.8

Thurs 02-Oct 16:00 DKK Currency reserves DKK bn Sep 441.6

Fri 03-Oct 9:30 SEK Industrial production s.a. m/m|y/y Aug 1.30%|-1.20% -1.10%|-5.70%

10:00 NOK Unemployment % Sep 2.80% 2.70% 2.90%

6 | 26 September 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Global Macro and Market Themes

More soft euro data adds pressure on the ECB

This week’s euro surveys for September showed further weakness adding to the

downside risks to growth. PMI data for the euro area weakened further, driven by

weakness in German manufacturing and the German ifo expectations index dropped yet

again more than expected, highlighting downside risks to Q4 growth (following a

technical rebound in Q3). The German ZEW sentiment index already warned of a weak

reading for ifo last week when it showed a continued drop. Although many commentators

do not like the ZEW index because it is a survey of financial analysts, it is better than its

name suggests (see chart). We expect surveys to move a bit lower in the coming months

before staging a moderate rebound in early 2015, driven by a positive spill-over effect

from US growth, the easing Ukraine crisis and a weaker currency.

Along with very low inflation, yet lower inflation expectations and a further decline

in oil prices, the weak surveys are adding to the pressure on ECB to ensure it

provides a meaningful stimulus to underpin the recovery and lift inflation. It is

increasingly questionable whether the current measures will be enough and hence the

likelihood of real quantitative easing (a bigger programme of government bond

purchases) is going up; not least because it appears to be difficult for the ECB to increase

the balance sheet as much as it might hope with the current measures.

Tough job ahead for the ECB

It is not an easy task the ECB has of getting inflation back to 2%. First, the end of the

super cycle in commodities continues to put downside pressure on commodity prices

and thus inflation. Brent oil prices resumed the decline that started in July and, at

USD96.6, trades at the lowest level in two years. Industrial metals have also fallen back

recently due to weaker Chinese data.

Second, high unemployment and low inflation continue to put downward pressure

on wage growth in the euro area. In Q2 14, wage compensation fell to a new cycle low

of 1.1% y/y – the lowest level in many decades. With inflation as low as it is, consumers

are actually getting a decent real wage gain even with this level of nominal wage growth.

This is one of the challenges for the ECB. When inflation is lower for a longer period,

wage earners become satisfied with lower wage increases, which in turn makes it even

more difficult to get inflation higher. In this sense, inflation is shifting to a lower

equilibrium level below the ECB’s 2% limit. This is also the reason why ECB president

Mario Draghi has repeatedly stated that persistent low inflation is a problem for the ECB

because of the risk it will get anchored in expectations. For the ECB to get inflation

higher, it will need to provide enough stimulus to a) convince wage earners that they

should expect 2% inflation and b) to generate enough demand to get unemployment down

and dampen the downside pressure on wage increases.

Key points

More weak data adds pressure on

the ECB

Likelihood of real QE from ECB

increasing

The Fed is expected to change

forward guidance in October

Emerging markets in a fragile spot

German ZEW has given good signal

for ifo expectations

Source: Macrobond Financial

Euro wage growth at very low level

Source: Macrobond Financial

7 | 26 September 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

As two of the biggest economies in the euro area – France and Italy – suffer from poor

competitiveness, overvalued house prices (in the case of France) and structural rigidities,

the ECB really needs countries like Germany and Spain to perform. In that light, the

current weak German figures should be of particular concern. On the other hand, it may

help in the attempt to get Germany to ease fiscal policy as Mario Draghi has increasingly

pointed to, albeit in his own cautious way.

German bond yields to stay low for a very long time

With inflation expected to remain very low in the years ahead, a very sluggish recovery

and high unemployment, there will be little pressure for higher bond yields in the euro

area. The ECB will continue to have an easing bias for a long time and investors move

out on the yield curve to get yields. The question we get a lot at the moment is whether

the euro area is the ‘new Japan’. It would be a lengthy discussion to go into and there are

both similarities and differences that we will look closer at it in a couple of forthcoming

papers. However, it is clear that monetary policy rates will be low for a very long time,

global liquidity will be ample and pension funds should continue to get new money in

that needs a home – some of them in the bond market. We should therefore expect bond

yields in the euro area to remain low for a long time.

The Fed to adjust forward guidance in October

This will also work to keep US yields in check as we are also seeing currently. The

current fair value for 10-year US bond yields is around 3%, according to our models. But

in a world with both the Bank of Japan and the ECB likely to stay at the zero rate bound

(or even negative in the ECB’s case) for a long time, it is likely to drive continued

demand for US bonds as well as investors looking globally to get a return.

However, we expect to see some rise in US bond yields as the Fed moves closer to lift-off

on rates. The divergence in monetary policy will continue for many years, in our

view, as the output gap is significantly higher in the euro area relative to the US and

growth is weaker on top. As the Fed starts hiking next year, short-end yields will be

pushed higher and it will have some rub-off effect on the long end. We are likely to see a

significant flattening of the US yield curve, though, as the flood of global liquidity is

likely to keep the rise in long yields limited.

Although the Fed refrained from removing the ‘considerable time’ language, we expect it

to go at the October meeting when the Fed has tapered for the last time and asset

purchases come to an end. Fed governor William Dudley this week reiterated the message

of Janet Yellen that the guidance still implied that policy would be dependent on data.

However, it is becoming increasingly difficult for the Fed to explain the meaning of the

guidance and it would be easier to change it as time goes on and it becomes more

uncertain whether there will be considerable time before lift-off. Job indicators are

generally strong still and we expect non-farm payrolls to mirror this as well in next

week’s report (although admittedly we also believed so prior to the previous weak report).

Our models point to slightly above 250,000 in payroll growth.

Choppy stock markets

With many soft spots in the global economy and the Fed likely to adjust its forward

guidance next month, we would expect some uncertainty in global stock markets to be

intact in coming months. The US continues to be the main driver of the global economy,

which was again confirmed this week when US Markit PMI held up at a very strong level

while PMI in both Japan and the euro area weakened.

Market inflation expectations lower

than before ECB measures

Source: Macrobond Financial

Getting closer to Japanese yield levels

Source: Macrobond Financial

Historical policy divergence coming...

Source: Macrobond Financial

...as US slack is fading while euro area

will have plenty for a long time

Source: Macrobond Financial

8 | 26 September 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

However, we continue to be positive on the stock market in the medium to long term as

we look for growth to recover in both the euro area and Japan on a six-12 month horizon

and expect US growth to continue at a 3-3.5% growth pace. With very cheap liquidity and

lots of it as far as the eye can see, risk assets should continue to perform in the medium

term.

Slowdown not as severe as feared

China’s HSBC manufacturing PMI unexpectedly improved in September (see Flash

Comment - China: Slight improvement in HSBC manufacturing PMI suggests slowdown

less severe than feared, 23 September 2014). It does not change our view that China is

again in a phase of slower growth driven primarily by weaker credit growth and domestic

investment demand and the manufacturing PMIs will continue to edge lower in the

coming months. However, the manufacturing PMI suggests that the slowdown might not

be as severe as we feared. It appears the weakness in domestic demand is to some degree

being offset by stronger export growth. In the HSBC manufacturing PMI, export orders

reached their highest level since March 2010 and exports were also the bright spot in the

overall weak hard data for August. Retail sales in China have also been relatively resilient

in recent months if we adjust for the decline in inflation, suggesting that so far there has

been no substantial negative impact on private consumption from the weak property

market.

Hence, at least for now, the data suggests that the Chinese economy is able to rebalance

without a severe slowdown in growth. This is not necessarily positive for commodity

markets. First, the implications are that we are unlikely to see any major stimulus from

the Chinese government in the short run. Second, demand from China will also be less

resource-intensive with growth gradually shifting away from investment-driven growth.

Another implication is likely to be that the Chinese current account surplus will again

start to increase as indicated by the surge in China’s trade surplus in recent months.

Hence, we expect the Chinese currency to continue to appreciate as long as growth does

not slow severely.

Emerging markets are fragile

With a Fed hike moving closer, growth in China slowing and commodity prices under

pressure across the board, emerging markets are fragile. Among emerging markets,

fundamentals are currently strongest for Asia as it has the strongest external balances and

the Asian region as a whole is benefiting from the recent declines in commodity prices.

In China, surprise increase in PMI

indicates less severe slowdown

Source: Macrobond Financial

Emerging markets in a fragile spot

Source: Macrobond Financial

9 | 26 September 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Global market views

Source: Danske Bank Markets

Asset class Main factors

Equities Moderately positive on 3M view, positive on 12M view The continued recovery in the US, China and, to some extent, Europe combined with stimulus from especially

BoJ and ECB will support equities. On a company level, data is starting to look promising as well. Earnings growth in Q2 showed strong momentum across the board, capex in the US is picking up and earnings revisions are positive for 2014 and 2015 for most regions

Bond market Risk of higher US rates in the near term Lower long-term growth and inflation expectations and hedging flows weigh on long bond yields in the short term US-Euro spread: wider 2-5Y, stable longer maturities Policy divergence drives short-end spread wider, longer-end spread stable as close to historical highs Peripheral spreads to continue gradual tightening Added liquidity, search for yield, improving fundamentals. Volatility to pick up somewhat Credit spread to tighten gradually still, but risk of higher vol Added liquidity, search for yield, good fundamentals. Geopolitical and idiosyncratic risk creates jitters

FX EUR/USD - more downside in short and medium term EUR/USD to fall further on diverging monetary policy, growth and portfolio flows USD/JPY - higher USD/JPY to break higher on pension reforms, portfolio outflows and diverging monetary policy EUR/SEK - lower EUR/SEK to decline on growth and valuation EUR/NOK - more downside especially in the short term EUR/NOK to decline on growth and carry in a world of low global growth and zero interest rates

Commodities Oil prices - stable prices for the rest of the year Substantial supply shock to weigh in 2014. Limited risk of supply disruptions Metal prices sideways before trending up in 2015 Support from global recovery, supply side risks Gold prices to correct lower still Trending down as first Fed hike draws closer. Geopolitical concerns a supportive factor Agricultural risks remain on the upside Near-term stabilisation, extreme weather is key upside risk

10 | 26 September 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Scandi update

Denmark – New forecast from Danske Bank: Fragile recovery

Both Danske Bank and the Nationalbank published updated forecasts for the Danish

economy during the week. Our take is that we are in the early stages of recovery but

recent data have underlined that progress will be slow and fragile and could easily be

derailed. Although the numbers have been disappointing of late, we do not think that the

recovery has been knocked completely off course, but we have revised down our growth

forecast. We now anticipate growth of 0.8% this year and 1.8% next year, which is

closely in line with the 0.8% and 1.7% predicted by the central bank in its Q3 monetary

review.

The week’s data included figures for consumer confidence showing a decrease from 11.4

in August to 7.1 in September, which can be seen in the light of rather less positive

economic news lately, such as the disappointing GDP figures for Q2. The fall should also

be seen as a normalisation, as the indicator had previously climbed for six successive

months, which has never happened before. Despite the fall in September, consumer

confidence remains high.

Sweden – We remain positive but are feeling less so

The NIER’s confidence data provided a relief for those worried about the consumption

outlook as consumers apparently were not as pessimistic as we thought and August data

were revised markedly stronger. Alas, the same cannot be said for those of us more

worried about the manufacturing sector and its pervasive importance for Swedish GDP-

growth. Manufacturing confidence continues to point to consecutive growth but not in a

very confident fashion. In addition, the overall economic tendency is just barely positive,

raising some doubt about the expected acceleration in demand during autumn. To further

that proposition, the (August) trade balance was again far below last year and exports are

uncannily weak for a country that has the ‘worst performing’ currency in the G10-

universe!

Norway – Tighter labour market

Norwegian unemployment has been surprisingly stable given the downturn in oil-related

industries. It actually seems to have fallen so far this year after rising towards the end of

last year. Employment growth has also picked up to around 2% annualised over the past

three months. This points to stronger growth in other sectors, such as the export industry,

retail, construction and, of course, the public sector. Given all the downsizing in oil-

related industries over the summer, we nevertheless believe that unemployment could rise

gently during the autumn before falling again next year. Signals seem to suggest that

5,000 people may be made redundant in these industries, equivalent to 0.2% of the labour

force. Since we expect oil investment to pick up again from 2016, our provisional

conclusion is that this will be a one-off effect, pushing up overall unemployment only to a

limited degree, and will peter out over the winter.

Fragile Danish recovery

Source: Statistics Denmark

Isn’t external demand recuperating?

Source: Statistics Sweden. DBM calculations

Falling unemployment

Source: Macrobond

11 | 26 September 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Latest research from Danske Bank Markets

25/9 Nordic Outlook - September 2014

Quarterly update on the Nordic economies.

23/9/14 Flash Comment - China: Slight improvement in HSBC manufacturing PMI

suggests slowdown less severe than feared

The flash estimate for China's HSBC/Markit manufacturing PMI in September

unexpectedly improved to 50.5 (consensus: 50.0, DBM: 49.4) from a final reading of 50.2

in August.

23/9/14 Flash Comment: Euro PMI still soft - German manufacturing weakens further

Euro flash PMI weakened further in September

19/9/14 Monitor - Global: business cycle monitor

Strong divergence - US the only pillar of strength

12 | 26 September 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

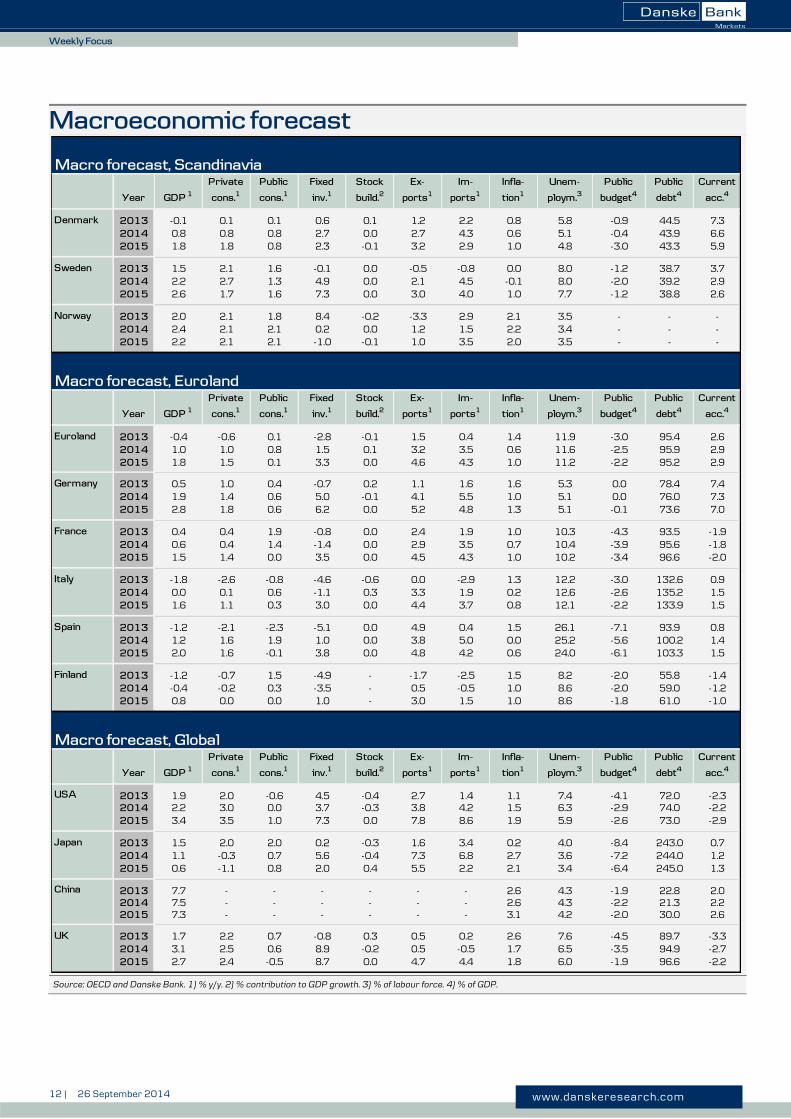

Macroeconomic forecast

Source: OECD and Danske Bank. 1) % y/y. 2) % contribution to GDP growth. 3) % of labour force. 4) % of GDP.

Macro forecast, Scandinavia

Denmark 2013 -0.1 0.1 0.1 0.6 0.1 1.2 2.2 0.8 5.8 -0.9 44.5 7.32014 0.8 0.8 0.8 2.7 0.0 2.7 4.3 0.6 5.1 -0.4 43.9 6.62015 1.8 1.8 0.8 2.3 -0.1 3.2 2.9 1.0 4.8 -3.0 43.3 5.9

Sweden 2013 1.5 2.1 1.6 -0.1 0.0 -0.5 -0.8 0.0 8.0 -1.2 38.7 3.72014 2.2 2.7 1.3 4.9 0.0 2.1 4.5 -0.1 8.0 -2.0 39.2 2.92015 2.6 1.7 1.6 7.3 0.0 3.0 4.0 1.0 7.7 -1.2 38.8 2.6

Norway 2013 2.0 2.1 1.8 8.4 -0.2 -3.3 2.9 2.1 3.5 - - -2014 2.4 2.1 2.1 0.2 0.0 1.2 1.5 2.2 3.4 - - -2015 2.2 2.1 2.1 -1.0 -0.1 1.0 3.5 2.0 3.5 - - -

Macro forecast, Euroland

Euroland 2013 -0.4 -0.6 0.1 -2.8 -0.1 1.5 0.4 1.4 11.9 -3.0 95.4 2.62014 1.0 1.0 0.8 1.5 0.1 3.2 3.5 0.6 11.6 -2.5 95.9 2.92015 1.8 1.5 0.1 3.3 0.0 4.6 4.3 1.0 11.2 -2.2 95.2 2.9

Germany 2013 0.5 1.0 0.4 -0.7 0.2 1.1 1.6 1.6 5.3 0.0 78.4 7.42014 1.9 1.4 0.6 5.0 -0.1 4.1 5.5 1.0 5.1 0.0 76.0 7.32015 2.8 1.8 0.6 6.2 0.0 5.2 4.8 1.3 5.1 -0.1 73.6 7.0

France 2013 0.4 0.4 1.9 -0.8 0.0 2.4 1.9 1.0 10.3 -4.3 93.5 -1.92014 0.6 0.4 1.4 -1.4 0.0 2.9 3.5 0.7 10.4 -3.9 95.6 -1.82015 1.5 1.4 0.0 3.5 0.0 4.5 4.3 1.0 10.2 -3.4 96.6 -2.0

Italy 2013 -1.8 -2.6 -0.8 -4.6 -0.6 0.0 -2.9 1.3 12.2 -3.0 132.6 0.92014 0.0 0.1 0.6 -1.1 0.3 3.3 1.9 0.2 12.6 -2.6 135.2 1.52015 1.6 1.1 0.3 3.0 0.0 4.4 3.7 0.8 12.1 -2.2 133.9 1.5

Spain 2013 -1.2 -2.1 -2.3 -5.1 0.0 4.9 0.4 1.5 26.1 -7.1 93.9 0.82014 1.2 1.6 1.9 1.0 0.0 3.8 5.0 0.0 25.2 -5.6 100.2 1.42015 2.0 1.6 -0.1 3.8 0.0 4.8 4.2 0.6 24.0 -6.1 103.3 1.5

Finland 2013 -1.2 -0.7 1.5 -4.9 - -1.7 -2.5 1.5 8.2 -2.0 55.8 -1.42014 -0.4 -0.2 0.3 -3.5 - 0.5 -0.5 1.0 8.6 -2.0 59.0 -1.22015 0.8 0.0 0.0 1.0 - 3.0 1.5 1.0 8.6 -1.8 61.0 -1.0

Macro forecast, Global

USA 2013 1.9 2.0 -0.6 4.5 -0.4 2.7 1.4 1.1 7.4 -4.1 72.0 -2.32014 2.2 3.0 0.0 3.7 -0.3 3.8 4.2 1.5 6.3 -2.9 74.0 -2.22015 3.4 3.5 1.0 7.3 0.0 7.8 8.6 1.9 5.9 -2.6 73.0 -2.9

Japan 2013 1.5 2.0 2.0 0.2 -0.3 1.6 3.4 0.2 4.0 -8.4 243.0 0.72014 1.1 -0.3 0.7 5.6 -0.4 7.3 6.8 2.7 3.6 -7.2 244.0 1.22015 0.6 -1.1 0.8 2.0 0.4 5.5 2.2 2.1 3.4 -6.4 245.0 1.3

China 2013 7.7 - - - - - - 2.6 4.3 -1.9 22.8 2.02014 7.5 - - - - - - 2.6 4.3 -2.2 21.3 2.22015 7.3 - - - - - - 3.1 4.2 -2.0 30.0 2.6

UK 2013 1.7 2.2 0.7 -0.8 0.3 0.5 0.2 2.6 7.6 -4.5 89.7 -3.32014 3.1 2.5 0.6 8.9 -0.2 0.5 -0.5 1.7 6.5 -3.5 94.9 -2.72015 2.7 2.4 -0.5 8.7 0.0 4.7 4.4 1.8 6.0 -1.9 96.6 -2.2

Current

acc.4

GDP 1

Private

cons.1

Public

cons.1

Fixed

inv.1

Stock

build.2

Ex-

ports1

Im-

ports1

Infla-

tion1

Unem-

ploym.3

Public

budget4

Public

debt4

Year

Year GDP 1

Private

cons.1

Public

cons.1

Fixed

inv.1

Stock

build.2

Ex-

ports1

Im-

ports1

Infla-

tion1

Unem-

ploym.3

Public

budget4

Current

acc.4

Public

debt4

Current

acc.4

Im-

ports1

Public

debt4

Public

budget4

Ex-

ports1

Infla-

tion1

Unem-

ploym.3

Year GDP 1

Private

cons.1

Public

cons.1

Fixed

inv.1

Stock

build.2

13 | 26 September 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Financial forecast

Source: Danske Bank Markets

Bond and money markets

Currencyvs USD

Currencyvs DKK

USD 26-Sep - 583.9

+3m - 586.4

+6m - 590.9+12m - 595.6

EUR 26-Sep 127.5 744.4

+3m 127.0 744.8

+6m 126.0 744.5+12m 125.0 744.5

JPY 26-Sep 109.0 5.36

+3m 110.0 5.32

+6m 112.0 5.28+12m 114.0 5.21

GBP 26-Sep 163.2 952.7

+3m 163.0 954.8

+6m 164.0 966.9+12m 164.0 979.6

CHF 26-Sep 94.7 616.7

+3m 95.3 615.5

+6m 96.8 610.2+12m 99.2 600.4

DKK 26-Sep 583.9 -

+3m 586.4 -

+6m 590.9 -+12m 595.6 -

SEK 26-Sep 722.0 80.9

+3m 716.5 81.8

+6m 714.3 82.7+12m 704.0 84.6

NOK 26-Sep 640.7 91.1

+3m 626.0 93.7

+6m 623.0 94.8+12m 620.0 96.1

Equity Markets

Regional

Price trend12 mth.

Regional recommen-dations

USA (USD) Strong growth & earnings, expensive 5-8% Neutral

Emerging markets (local curr) Commodity-related equities are pressured 0-5% Underweight

Europe (ex. Nordics) Recovering economy, fair valuation 5-10% OverweightNordics Strong cyclical profile 5-10% Overweight

Commodities

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 2014 2015

NYMEX WTI 99 103 96 93 93 94 94 95 98 94

ICE Brent 108 110 102 98 97 98 98 99 104 98

Copper 6,996 6,768 6,850 6,850 7,000 7,150 7,300 7,450 6,866 7,225

Zinc 2,024 2,080 2,300 2,350 2,400 2,450 2,500 2,550 2,189 2,475

Nickel 14,723 18,529 18,500 18,500 18,750 19,000 19,250 19,500 17,563 19,125

Aluminium 1,754 1,839 2,000 2,000 2,050 2,100 2,150 2,200 1,898 2,125

Gold 1,292 1,291 1,275 1,250 1,240 1,230 1,220 1,210 1,277 1,225

Matif Mill Wheat (€/t) 201 200 170 167 173 177 178 180 185 177

Rapeseed (€/t) 383 372 325 304 315 321 324 326 346 321

CBOT Wheat (USd/bushel) 618 651 530 520 530 540 545 550 580 541

CBOT Corn (USd/bushel) 453 478 360 360 370 380 385 390 413 381CBOT Soybeans (USd/bushel) 1,358 1,470 1,140 1,050 1,070 1,090 1,100 1,110 1,254 1,093

315

Average

Key int.rate

0.25

0.25

0.250.75

1.50

0.00

0.05

0.05

0.100.10

0.50

10-yr swap yield

0.47

0.20

0.200.20

3m interest rate

1.75

0.05

0.10

0.50

0.00

0.20

0.05

0.75

0.911.42

0.000.00

0.05

0.75

0.50

0.25

0.10

0.29

0.05

1.25

0.050.05

0.20

0.21

0.20

0.45

0.45

1.50

0.25

0.250.25

1.50

1.50

1.75

1.75

0.24

0.08

0.12

0.56

0.01

0.30

0.581.07

0.05

0.05

0.20

0.15

0.20

1.95

2.05

0.55

2.20

0.70

1.801.66

0.35

0.350.35

0.05

0.050.05

0.54

0.50

1.452.10

1.50

1.702.20

0.20

0.200.25

127.5

-

-

--

139.0

744.8

744.5744.5

920.4

816.8

775.0

910.0

785.0

900.0880.0

795.0

120.7

744.4

78.0

77.076.0

121.0

122.0124.0

127.0

126.0125.0

140.0

141.0143.0

High

Medium

Currencyvs EUR

2-yr swap yield

Risk profile3 mth.

Medium 0-3%

Price trend3 mth.

2.85

2.63

3.15

0.79

0.20

0.17

1.25

0.02

0.47

0.15

0.150.15

0.95

78.1

3.40

326

26-Sep

0-3%

0-3%

92

17,325

6,695

2,266

1,223

150

97

1,951

20152014

Medium 0-3%

1.15

1.201.30

0.75

0.800.85

2.51

2.75

0.64

918

471

1.14

1.801.95

2.59

3.00

3.05

2.953.30

0.82

0.95

1.051.25

3.35

1.471.57

1.42

1.73

1.65

1.46

14 | 26 September 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Calendar

Source: Danske Bank Markets

Key Data and Events in Week 40

During the week Period Danske Bank Consensus Previous

Mon 03 - 09 JPY Bank lending y/y Mar 2,20%

Sat 04 - 04 JPY Official reserves assets USD bn Mar 1288.2

Sat 27 - 01 DEM Retail sales m/m|y/y Aug -1.10%|1.00%

Monday, September 29, 2014 Period Danske Bank Consensus Previous

9:00 ESP HICP, preliminary m/m|y/y Sep ...|-0.50%

9:00 DKK Confidence indicator, industry Index Sep -2 -6

9:30 SEK Retail sales s.a. m/m|y/y Aug 0.50%|3.00% 0.60%|3.00% -0.70%|2.30%

10:30 GBP Broad money M4 m/m|y/y Aug 0.30%|-1.00%

11:00 EUR Business climate indicator Net bal. Sep 0.2

11:00 EUR Industrial confidence Net bal. Sep -5.5 -5.3

11:00 EUR Economic confidence Index Sep 100.0 100.6

11:00 EUR Consumer confidence, final Net bal. Sep -11.4

11:00 EUR Service confidence Net bal. Sep 2.5 3.1

14:00 DEM HICP, preliminary m/m|y/y Sep … |0.8% … |0.8% 0.00%|0.80%

14:30 USD Personal income m/m Aug 0.30% 0.30% 0.20%

14:30 USD Personal spending m/m Aug 0.50% 0.40% -0.10%

14:30 USD PCE deflator m/m|y/y Aug -0.10%|1.40% -0.10%|1.40% 0.10%|1.60%

14:30 USD PCE core m/m|y/y Aug 0.00%|1.40% 0.00%|1.40% 0.10%|1.50%

15:00 USD Fed's Evans (non-voter, dovish) speaks

16:00 USD Pending home sales m/m|y/y Aug -1.50%|… 0.40%|... 3.30%|-2.70%

18:15 USD Former chairman Bernanke speaks

Tuesday, September 30, 2014 Period Danske Bank Consensus Previous

1:05 GBP Gfk Consumer confidence Index Sep 0 1.0

1:30 JPY Household spending y/y Aug -3.60% -5.90%

1:30 JPY Unemployment rate % Aug 3.80% 3.80% 3.80%

1:30 JPY Job-to-applicant ratio Aug 1.1 1.1 1.1

1:50 JPY Large retailers' sales y/y Aug 0.30% -0.60%

1:50 JPY Retail trade m/m|y/y Aug 0.70%|0.30% -0.50%|0.60%

1:50 JPY Industrial production, preliminary m/m|y/y Aug 0.10% 0.20%|-1.10% 0.40%|-0.70%

3:30 JPY Labor cash earnings y/y Aug 1.00% 2.40%

3:45 CNY HSBC manf. PMI, final Index Sep 50.5 50.5

7:00 JPY Small business confidence Index Sep 47.7

7:00 JPY Housing starts y/y Aug -13.70% -14.10%

8:00 GBP Nationwide House Prices m/m|y/y Sep 0.50%|10.40% 0.80%|11.00%

8:45 FRF Household consumption m/m|y/y Aug ...|...

9:00 DKK GDP, quarterly figure (ESA 2010 main revision) q/q|y/y 2nd quarter -0.30%|-0.10%

9:00 DKK Gross unemployment s.a. K (%) Aug 134.0 (5.1%) 134.5 (5.1%)

9:30 SEK Wages (blue collars/white collars) y/y Jul 2.20%

9:55 DEM Unemployment % Sep 6.70% 6.70% 6.70%

10:00 NOK Retail sales, s.a. m/m Aug 1.00% 0.80% -1.50%

10:00 NOK Credit indicator (C2) y/y Aug 5.40% 5.40%

10:30 GBP GDP, final q/q|y/y 2nd quarter 0.80%|3.20% 0.80%|3.20%

11:00 ITL HICP, preliminary m/m|y/y Sep -0.20%|-0.20%

11:00 EUR Unemployment % Aug 11.50% 11.50% 11.50%

11:00 EUR CPI - core, preliminary % Sep 0.90% 0.90% 0.90%

11:00 EUR CPI, preliminary y/y Sep 0.3% 0.3% 0.4%

14:30 CAD GDP m/m|y/y Jul ...|...

14:30 CAD GDP m/m|y/y Jul 0.20%|... 0.30%|3.10%

15:00 USD S&P Case Shiller House prices Index Jul 172.3

15:45 USD Chicago PMI Index Sep 61.0 64.3

16:00 USD Consumer confidence Index Sep 94.5 92.2 92.4

15 | 26 September 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Calendar - continued

Source: Danske Bank Markets

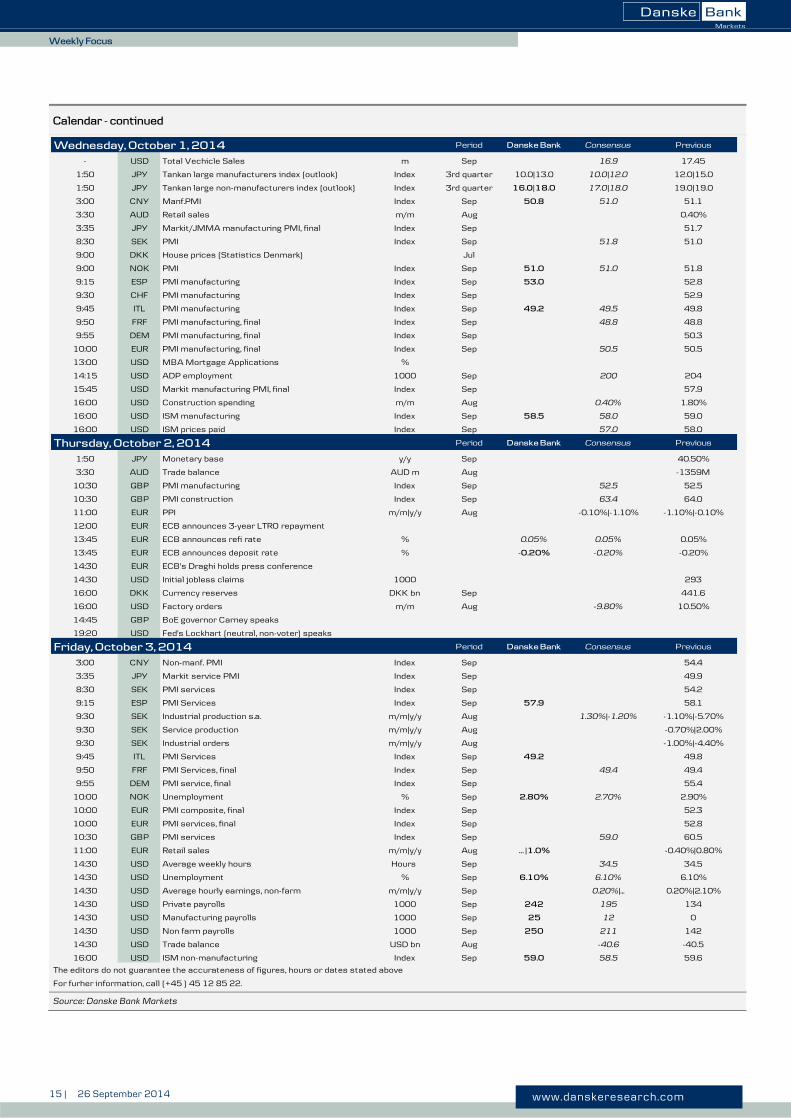

Wednesday, October 1, 2014 Period Danske Bank Consensus Previous

- USD Total Vechicle Sales m Sep 16.9 17.45

1:50 JPY Tankan large manufacturers index (outlook) Index 3rd quarter 10.0|13.0 10.0|12.0 12.0|15.0

1:50 JPY Tankan large non-manufacturers index (outlook) Index 3rd quarter 16.0|18.0 17.0|18.0 19.0|19.0

3:00 CNY Manf.PMI Index Sep 50.8 51.0 51.1

3:30 AUD Retail sales m/m Aug 0.40%

3:35 JPY Markit/JMMA manufacturing PMI, final Index Sep 51.7

8:30 SEK PMI Index Sep 51.8 51.0

9:00 DKK House prices (Statistics Denmark) Jul

9:00 NOK PMI Index Sep 51.0 51.0 51.8

9:15 ESP PMI manufacturing Index Sep 53.0 52.8

9:30 CHF PMI manufacturing Index Sep 52.9

9:45 ITL PMI manufacturing Index Sep 49.2 49.5 49.8

9:50 FRF PMI manufacturing, final Index Sep 48.8 48.8

9:55 DEM PMI manufacturing, final Index Sep 50.3

10:00 EUR PMI manufacturing, final Index Sep 50.5 50.5

13:00 USD MBA Mortgage Applications %

14:15 USD ADP employment 1000 Sep 200 204

15:45 USD Markit manufacturing PMI, final Index Sep 57.9

16:00 USD Construction spending m/m Aug 0.40% 1.80%

16:00 USD ISM manufacturing Index Sep 58.5 58.0 59.0

16:00 USD ISM prices paid Index Sep 57.0 58.0

Thursday, October 2, 2014 Period Danske Bank Consensus Previous

1:50 JPY Monetary base y/y Sep 40.50%

3:30 AUD Trade balance AUD m Aug -1359M

10:30 GBP PMI manufacturing Index Sep 52.5 52.5

10:30 GBP PMI construction Index Sep 63.4 64.0

11:00 EUR PPI m/m|y/y Aug -0.10%|-1.10% -1.10%|-0.10%

12:00 EUR ECB announces 3-year LTRO repayment

13:45 EUR ECB announces refi rate % 0.05% 0.05% 0.05%

13:45 EUR ECB announces deposit rate % -0.20% -0.20% -0.20%

14:30 EUR ECB's Draghi holds press conference

14:30 USD Initial jobless claims 1000 293

16:00 DKK Currency reserves DKK bn Sep 441.6

16:00 USD Factory orders m/m Aug -9.80% 10.50%

14:45 GBP BoE governor Carney speaks

19:20 USD Fed's Lockhart (neutral, non-voter) speaks

Friday, October 3, 2014 Period Danske Bank Consensus Previous

3:00 CNY Non-manf. PMI Index Sep 54.4

3:35 JPY Markit service PMI Index Sep 49.9

8:30 SEK PMI services Index Sep 54.2

9:15 ESP PMI Services Index Sep 57.9 58.1

9:30 SEK Industrial production s.a. m/m|y/y Aug 1.30%|-1.20% -1.10%|-5.70%

9:30 SEK Service production m/m|y/y Aug -0.70%|2.00%

9:30 SEK Industrial orders m/m|y/y Aug -1.00%|-4.40%

9:45 ITL PMI Services Index Sep 49.2 49.8

9:50 FRF PMI Services, final Index Sep 49.4 49.4

9:55 DEM PMI service, final Index Sep 55.4

10:00 NOK Unemployment % Sep 2.80% 2.70% 2.90%

10:00 EUR PMI composite, final Index Sep 52.3

10:00 EUR PMI services, final Index Sep 52.8

10:30 GBP PMI services Index Sep 59.0 60.5

11:00 EUR Retail sales m/m|y/y Aug … |1.0% -0.40%|0.80%

14:30 USD Average weekly hours Hours Sep 34.5 34.5

14:30 USD Unemployment % Sep 6.10% 6.10% 6.10%

14:30 USD Average hourly earnings, non-farm m/m|y/y Sep 0.20%|... 0.20%|2.10%

14:30 USD Private payrolls 1000 Sep 242 195 134

14:30 USD Manufacturing payrolls 1000 Sep 25 12 0

14:30 USD Non farm payrolls 1000 Sep 250 211 142

14:30 USD Trade balance USD bn Aug -40.6 -40.5

16:00 USD ISM non-manufacturing Index Sep 59.0 58.5 59.6

The editors do not guarantee the accurateness of figures, hours or dates stated above

For furher information, call (+45 ) 45 12 85 22.

16 | 26 September 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

Disclosures This research report has been prepared by Danske Bank Markets, a division of Danske Bank A/S (‘Danske

Bank’). The authors of the research report are Allan von Mehren, Chief Analyst and Steen Bocian, Chief

Economist.

Analyst certification

Each research analyst responsible for the content of this research report certifies that the views expressed in the

research report accurately reflect the research analyst’s personal view about the financial instruments and issuers

covered by the research report. Each responsible research analyst further certifies that no part of the compensation

of the research analyst was, is or will be, directly or indirectly, related to the specific recommendations expressed

in the research report.

Regulation

Danske Bank is authorised and subject to regulation by the Danish Financial Supervisory Authority and is subject

to the rules and regulation of the relevant regulators in all other jurisdictions where it conducts business. Danske

Bank is subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority

(UK). Details on the extent of the regulation by the Financial Conduct Authority and the Prudential Regulation

Authority are available from Danske Bank on request.

The research reports of Danske Bank are prepared in accordance with the Danish Society of Financial Analysts’

rules of ethics and the recommendations of the Danish Securities Dealers Association.

Conflicts of interest

Danske Bank has established procedures to prevent conflicts of interest and to ensure the provision of high-

quality research based on research objectivity and independence. These procedures are documented in Danske

Bank’s research policies. Employees within Danske Bank’s Research Departments have been instructed that any

request that might impair the objectivity and independence of research shall be referred to Research Management

and the Compliance Department. Danske Bank’s Research Departments are organised independently from and do

not report to other business areas within Danske Bank.

Research analysts are remunerated in part based on the overall profitability of Danske Bank, which includes

investment banking revenues, but do not receive bonuses or other remuneration linked to specific corporate

finance or debt capital transactions.

Financial models and/or methodology used in this research report

Calculations and presentations in this research report are based on standard econometric tools and methodology

as well as publicly available statistics for each individual security, issuer and/or country. Documentation can be

obtained from the authors on request.

Risk warning

Major risks connected with recommendations or opinions in this research report, including a sensitivity analysis

of relevant assumptions, are stated throughout the text.

Date of first publication

See the front page of this research report for the date of first publication.

General disclaimer This research has been prepared by Danske Bank Markets (a division of Danske Bank A/S). It is provided for

informational purposes only. It does not constitute or form part of, and shall under no circumstances be

considered as, an offer to sell or a solicitation of an offer to purchase or sell any relevant financial instruments

(i.e. financial instruments mentioned herein or other financial instruments of any issuer mentioned herein and/or

options, warrants, rights or other interests with respect to any such financial instruments) (‘Relevant Financial

Instruments’).

The research report has been prepared independently and solely on the basis of publicly available information that

Danske Bank considers to be reliable. While reasonable care has been taken to ensure that its contents are not

untrue or misleading, no representation is made as to its accuracy or completeness and Danske Bank, its affiliates

and subsidiaries accept no liability whatsoever for any direct or consequential loss, including without limitation

any loss of profits, arising from reliance on this research report.

The opinions expressed herein are the opinions of the research analysts responsible for the research report and

reflect their judgement as of the date hereof. These opinions are subject to change, and Danske Bank does not

17 | 26 September 2014 www.danskeresearch.com

Weekly Fo

cus

Weekly Focus

undertake to notify any recipient of this research report of any such change nor of any other changes related to the

information provided in this research report.

This research report is not intended for retail customers in the United Kingdom or the United States.

This research report is protected by copyright and is intended solely for the designated addressee. It may not be

reproduced or distributed, in whole or in part, by any recipient for any purpose without Danske Bank’s prior

written consent.

Disclaimer related to distribution in the United States This research report is distributed in the United States by Danske Markets Inc., a U.S. registered broker-dealer

and subsidiary of Danske Bank, pursuant to SEC Rule 15a-6 and related interpretations issued by the U.S.

Securities and Exchange Commission. The research report is intended for distribution in the United States solely

to ‘U.S. institutional investors’ as defined in SEC Rule 15a-6. Danske Markets Inc. accepts responsibility for this

research report in connection with distribution in the United States solely to ‘U.S. institutional investors’.

Danske Bank is not subject to U.S. rules with regard to the preparation of research reports and the independence

of research analysts. In addition, the research analysts of Danske Bank who have prepared this research report are

not registered or qualified as research analysts with the NYSE or FINRA but satisfy the applicable requirements

of a non-U.S. jurisdiction.

Any U.S. investor recipient of this research report who wishes to purchase or sell any Relevant Financial

Instrument may do so only by contacting Danske Markets Inc. directly and should be aware that investing in non-

U.S. financial instruments may entail certain risks. Financial instruments of non-U.S. issuers may not be

registered with the U.S. Securities and Exchange Commission and may not be subject to the reporting and

auditing standards of the U.S. Securities and Exchange Commission.