internet broadband: a new source of growth · internet broadband: a new source of growth . ......

TRANSCRIPT

Olivier Anstett, Director of Multimedia & Value-Added Services INTERNET BROADBAND: A NEW SOURCE OF GROWTH

Agenda

2

2

3

4

HTS opening new horizons

Eutelsat’s Broadband activity

Eutelsat internet broadband strategy

Conclusions

1

HTS: a step change, opening the Broadband market to satellite

3

(1) Based on capacity of c.3 Gbps for a regular capacity satellite and 90 Gbps for KA-SAT (2) Price per unit of capacity sold (3) Based on a peak download throughput of c.5Mbps for a regular satellite and C. 50Mbps for KA-SAT profressional offers

Significant improvement in economics for KA-SAT versus regular capacity

Further improvement to come with future generations of HTS satellites

x30 Much higher capacity1

/8 Significantly reduced price2

x10 Improved peak throughput3

for users with small terminals

/10 Cost of terminals

Ongoing rise in global internet traffic…

4

(1) Source: eMarketer, Nov. 2014 (2) Source: internetsociety.org- Global Internet Report 2014

(3) Source: Cisco VNI, May 2015

Growing internet penetration

INTERNET USERS WORLDWIDE1 (Bn)

TRAFFIC PER FIXED BROADBAND CONNECTION2 (GB/month)

Rising consumption per user

GLOBAL CONSUMER INTERNET TRAFFIC3 (Pb/months)

Rapid growth in internet traffic

2.9 3.1 3.3 3.4 3.6

40% 42%

44% 46%

48%

2014 2015 2016 2017 2018

34 41 52

67 87

2014 2015 2016 2017 2018

% of population

Internet users

Sub-Saharan Africa Latin America and Caribbean Developed Asia-Pacific North America

Middle East and North Africa Emerging Asia-Pacific Central and Eastern Europe Western Europe Global

2010 2011 2012 2013 2014 2015 2016 2017 2018 0

20

…but needs are unaddressed in many areas

5

► Increasing consumer usage and public policy leading to new market standards • Download speed of >30 Mbps, ie Very High Broadband (VHB)

► Telco capex and public initiatives will improve the quality of the networks, but the addressable market will remain significant in remote areas • High marginal cost of rolling-out terrestrial networks • Limited footprint and risk of saturation of 4G

► Internet access is a now a ‘must have’ everywhere

► Many fast-growing markets massively underserved with inadequate infrastructures

Opportunity for satellite in areas under-served or un-served by terrestrial networks

Agenda

6

2

3

4

HTS opening new horizons

Eutelsat’s Broadband activity

Eutelsat internet broadband strategy

Conclusions

1

Broadband Internet: a new business for Eutelsat with strong growth potential

7

A NEW BUSINESS WITH DIFFERENT DRIVERS… …WHERE EUTELSAT HAS FIRST MOVER ADVANTAGE

► Providing Internet access to individuals and corporates in underserved areas

► Bandwidth-hungry at peak time

► More ground infrastructure to support role as network operator

► Regional markets with different specificities

► Different business model than regular capacity

► 2000s: broadband service launched in Ku-Band building on VSAT technologies

► 2011: KA-SAT, Europe’s first HTS satellite

► 2014: Eutelsat 3B with dedicated broadband payload

Eutelsat track record and first mover advantage to seize this significant opportunity

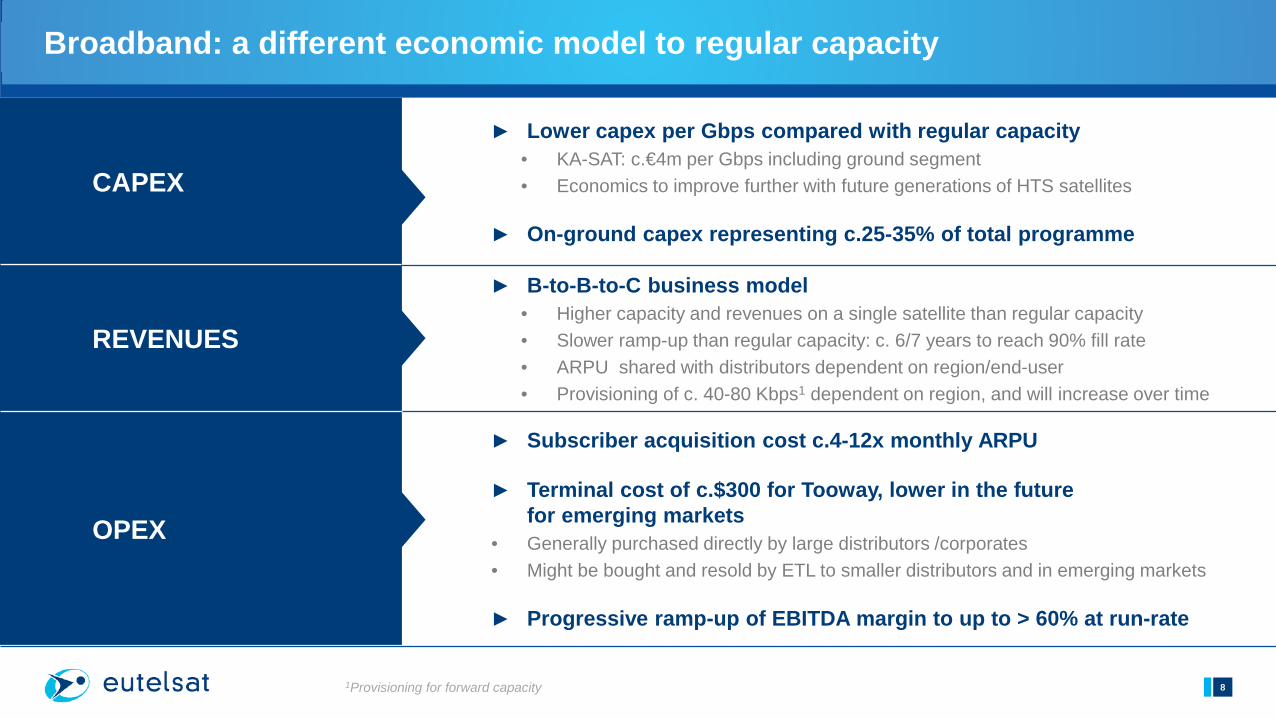

Broadband: a different economic model to regular capacity

8 1Provisioning for forward capacity

► Subscriber acquisition cost c.4-12x monthly ARPU

► Terminal cost of c.$300 for Tooway, lower in the future for emerging markets

• Generally purchased directly by large distributors /corporates • Might be bought and resold by ETL to smaller distributors and in emerging markets

► Progressive ramp-up of EBITDA margin to up to > 60% at run-rate

CAPEX

REVENUES

OPEX

► B-to-B-to-C business model • Higher capacity and revenues on a single satellite than regular capacity • Slower ramp-up than regular capacity: c. 6/7 years to reach 90% fill rate • ARPU shared with distributors dependent on region/end-user • Provisioning of c. 40-80 Kbps1 dependent on region, and will increase over time

► Lower capex per Gbps compared with regular capacity • KA-SAT: c.€4m per Gbps including ground segment • Economics to improve further with future generations of HTS satellites

► On-ground capex representing c.25-35% of total programme

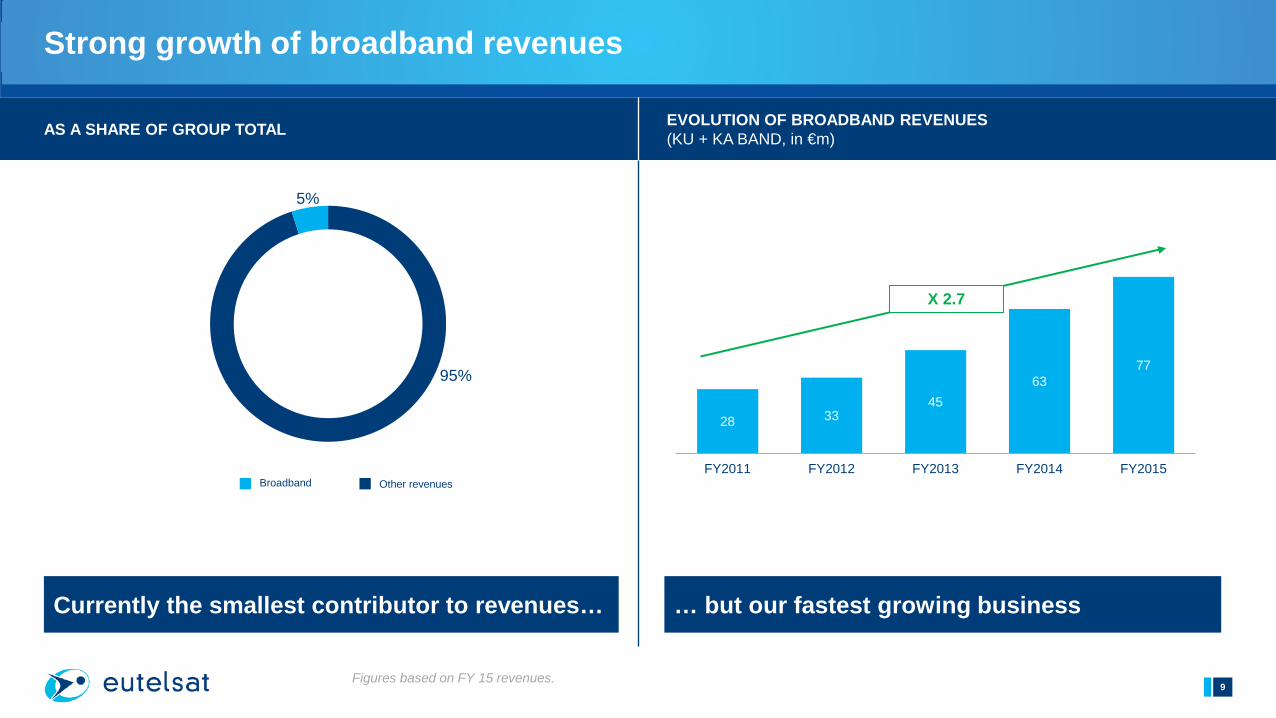

Strong growth of broadband revenues

9 Figures based on FY 15 revenues.

AS A SHARE OF GROUP TOTAL EVOLUTION OF BROADBAND REVENUES (KU + KA BAND, in €m)

95%

5%

Other revenues Broadband

28 33 45

63 77

FY2011 FY2012 FY2013 FY2014 FY2015

X 2.7

Currently the smallest contributor to revenues… … but our fastest growing business

Agenda

10

2

3

4

HTS opening new horizons

Eutelsat’s Broadband activity

Eutelsat internet broadband strategy

Conclusions

1

Eutelsat internet broadband strategy

11

3.2

In Europe

In Fast-growing markets

3.1

3

WESTERN EUROPE: ESTIMATED MARKET FOR SATELLITE BROADBAND IN 2025 (M households)

Europe: significant addressable market

12 Source: Analysys Mason

Total residential and business premises in Europe

Core market • Available download speeds <8 Mpbs • 4G networks capacity-constrained

196m

14m

4m

‘Broader’ market • Available download

speeds < 30 Mpbs

Based on 12 European markets : UK, Ireland , France, Belgium,Netherlands, Luxembourg, Switzerland, Germany, Austria, Italy, Spain and Portugal Estimated market taking into account Governments and Operators announcements

Significant addressable market long-term, even larger today

KA-SAT: addressing European broadband market

13

► First HTS satellite over Europe

► Operational since mid-2011 covering Europe and the Mediterranean Basin

► Addressing internet broadband markets in areas with limited or no internet service

► Total throughput of 90 Gbps

► Network of ten ground stations

► B-to-B-to-C business model with network of distribution partners

KA-SAT FOOTPRINT

Successful ramp-up of customer base

14

► 190,000 subscribers • 90% consumers

► 82k terminals added in the last 2 years

► Strong dynamic from professionals and corporates with higher ARPU

► Estimated capacity for broadband of ~ 300-400,000 subscribers

KA-SAT TERMINALS ACTIVATED (000 UNITS) KA-SAT TERMINALS ACTIVATED BY GEOGRAPHY

► Two thirds of customers in five main western European countries

► High loading of certain beams notably France, UK, Ireland

► Potential remaining in Eastern Europe, Spain, Germany, Italy

62 73

91 108

124 140

154 166 175 180 185 190

Dec'12 Mar'13 Jun'13 Sep'13 Dec'13 Mar'14 Jun'14 Sep'14 Dec'14 Mar'15 Jun'15 Sep'15

Spain

France

UK

Italy

Others

Germany

25%

14%

12% 9%

8%

32%

Tooway: proven Broadband product

15 Source: Degrouptest survey – February 2014

► A viable alternative to DSL

► True high-speed Internet anywhere • Up to 22Mbit/s download • Up to 6Mbit/s upload

► Easy to operate and to install • No telephone line required • No additional software required • Easy installation

► Optional services • VOIP • IPTV • Multicasting capability and

DTH TV reception from KA-SAT neighbourhood

TOOWAY VS DSL PERFORMANCE

0 10

5

0 4

2

DSL average Tooway

► Average Download speed

► Average Upload speed

A wide range of consumer bundles

16 1Indicative retail Price

22/6Mbps 10/2Mbps 22/6Mbps

10GB 25GB 40GB 40 + 60GB Web & email

Uncapped 8GB 16GB 2GB 5GB 15GB

Free Night Zones (12am – 6am)

€29.90 €44.90 €64.90 €89.90 €79.90 €19.90 €29.90 €18.00 €30.00 €60.00

Tooway B2C Line-up Eastern Europe Pay-as-You-Go

VNO-like offers

TOOWAY PACKAGED OFFER

► Distributor defines all product characteristics according to marketing strategy and target market

1

Examples of KA-SAT corporate solutions

17

Video surveillance of remote sites

Broadband communication for trucks

Backhauling and back-up for PMR infrastructure

Redundancy for terrestrial infrastructure

Temporary broadband communication for disaster recovery

Connection for remote sensor Networks

Broad network of distributors

18

SAMPLE OF DISTRIBUTORS

Broadband in Europe: conclusions

19

Structural growth drivers with millions of underserved households

Proven internet Broadband product

Ramp-up of customer base

Ongoing strengthening of distribution network

Second generation KA-SAT under consideration

Capitalizing on KA-SAT experience to expand into other markets

Eutelsat internet broadband strategy

20

3.2

In Europe

In fast-growing markets

3.1

3

The satellite broadband opportunity in fast-growing markets

21 Sources: United Nations - www.internetlivestats.com/

► Insufficient scale of terrestrial broadband networks • Fixed line infrastructure less developed • Mobile networks for broadband less deployed

and often congested • Roll-out of terrestrial networks takes time and

money

► High cost, limited performance and low reliability services where they exist

► Internet access a necessity for growth and development

3.2bn Connected

4.1bn Offline of which 95% in emerging countries

7.3bn Total world population 2015

Areas with under-developped infrastructure favour satellite

Strong potential regions including LATAM, Russia and Sub-Saharan Africa

22 Source: McKinsey – offline and falling behind, 2014

SIZE OF OFFLINE POPULATION (2013, in million)

USA 50m

Mexico 69m

Brazil 97m

Russia 55m

China 736m

Vietnam 50m

Philippines 62m

Indonesia 210m

Turkey 40m

Egypt 41m

Nigeria 108m

Congo DR 64m

Bangladesh 146m

India 1,063m

Tanzania 47m Myanmar

53m

Ethiopia 92m Thailand

48m

Iran 53m

Pakistan 162m

0 1,200

LATAM: Service since 2014, follow up in 2016

23

► EUTELSAT 3B • KA-band HTS payload of five steerable beams • Flexible coverage: EMEA / LATAM • Capacity: ~4 Gbps • In service since July 2014

► EUTELSAT 65 West A • KA-band HTS payload of up to 24 spotbeams • Coverage: LATAM with focus on Brazil • Capacity: ~37.5 Gbps • Entire HTS payload already presold • To be launched in Q1 2016

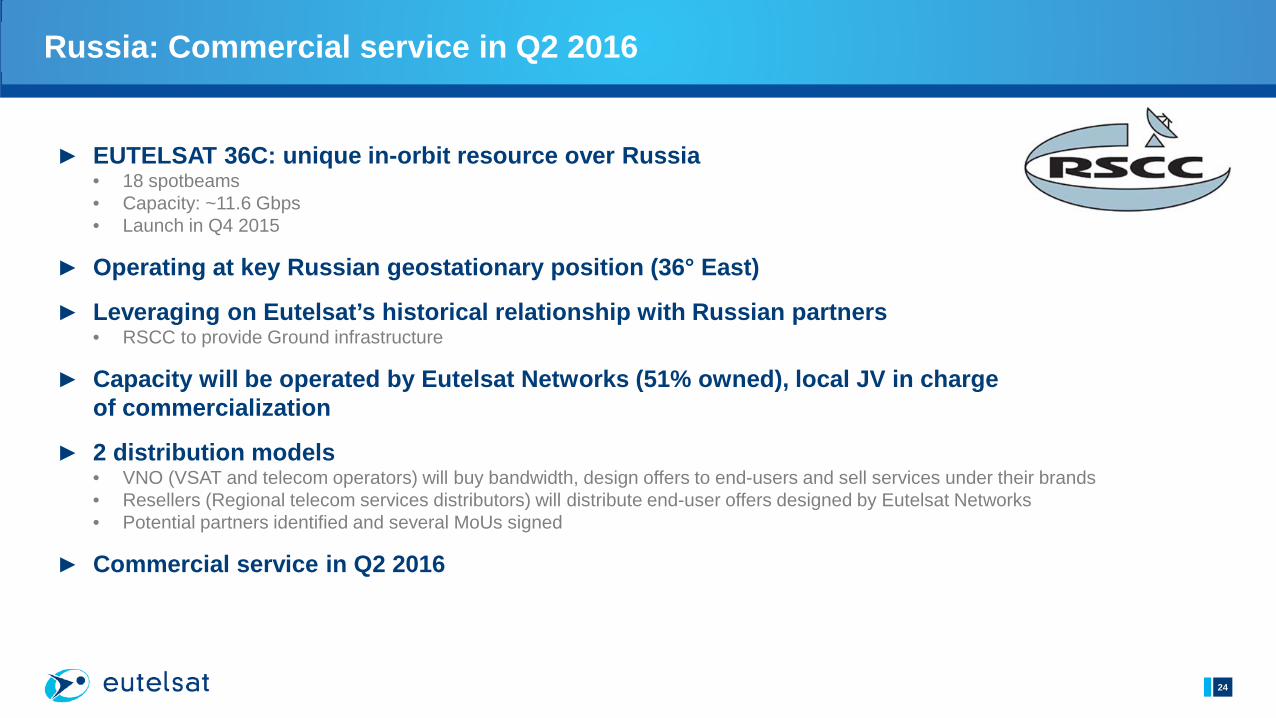

Russia: Commercial service in Q2 2016

24

► EUTELSAT 36C: unique in-orbit resource over Russia • 18 spotbeams • Capacity: ~11.6 Gbps • Launch in Q4 2015

► Operating at key Russian geostationary position (36° East)

► Leveraging on Eutelsat’s historical relationship with Russian partners • RSCC to provide Ground infrastructure

► Capacity will be operated by Eutelsat Networks (51% owned), local JV in charge of commercialization

► 2 distribution models • VNO (VSAT and telecom operators) will buy bandwidth, design offers to end-users and sell services under their brands • Resellers (Regional telecom services distributors) will distribute end-user offers designed by Eutelsat Networks • Potential partners identified and several MoUs signed

► Commercial service in Q2 2016

Africa: Two initiatives for timely access to the market

25

► Multi-year lease of Amos-6 HTS Ka-band payload • 18 HTS Ka-band spot beams • ~18 Gbps o/w c. 50% for Eutelsat

► Facebook secured as an anchor partner

► Service expected to start end-2016

► Timely investment opportunity

AMOS 6 FOLLOW-ON SATELLITE

► Procurement of a a new-generation HTS satellite from TAS • All-electric satellite • New Spacebus Neo platform • Unprecedented flexibility • Baseline mission: 65 spotbeams,

~75 Gbps with option to double capacity

► Quasi-complete coverage of SSA

► Launch expected in 2019

African broadband strategy

26

► Focus on premium consumer and professional segments

► Indirect distribution model (B-to-B-to-C) • Telecom operators, MNOs • Internet Service Providers • VSAT operators, Integrators • Energy providers, IT resellers, individual entrepreneurs

► Ground network owned and operated by Eutelsat to provide services adapted to customer needs • Raw capacity over selected beams (Mhz) • Dedicated IP bandwidth over selected beams (Mbps) • Packaged user services over selected beams

► Ground segment procurement underway

► Commercial prospection started

COVERAGE OF AFRICAN BROADBAND STANDALONE SATELLITE

30 COUNTRIES COVERED OVER SUB-SAHARAN AFRICA

EUTELSAT’S NEW GENERATION HTS SATELLITE

SETTING NEW STANDARDS FOR BROADBAND IN AFRICA

Agenda

27

2

3

4

HTS opening new horizons

Eutelsat’s Broadband activity

Eutelsat internet broadband strategy

Conclusions

1

To sum up

28

4.3

4.4

Internet broadband via satellite a new growth driver for Eutelsat

Ka-band HTS already delivering DSL-like quality today and fiber-like quality tomorrow

Significant future demand both in mature and fast growing markets

Ongoing development of KA-SAT; consideration of second generation

Launch of African broadband strategy; dedicated payloads for LATAM and Russia; other opportunities under consideration

Q&A INTERNET BROADBAND: A NEW SOURCE OF GROWTH