innovation in bakery and cereals 2010

DESCRIPTION

aetswTRANSCRIPT

1

Innovation in Bakery and Cereals

Emerging markets, key trends and future product innovation Reference Code: BI00012-025

Publication Date: December 2010

2

About the author Business Insights has a team of in-house consumer goods analysts drawn from consulting, R&D and

competitive intelligence backgrounds. Our analysts specialize in providing detailed insight into the future of

the industry and have extensive analytical, forecasting and research experience in the food & drinks,

ingredients and packaging sectors. Our team maintains regular contact with industry executives to track

market developments and base their market models on a wide range of proprietary databases to provide up

to date, accurate strategic insight on the future of the consumer goods market.

Disclaimer Copyright © 2010 Business Insights Ltd

This report is published by Business Insights (the Publisher). This report contains information from reputable

sources and although reasonable efforts have been made to publish accurate information, you assume sole

responsibility for the selection, suitability and use of this report and acknowledge that the Publisher makes

no warranties (either express or implied) as to, nor accepts liability for, the accuracy or fitness for a particular

purpose of the information or advice contained herein. The Publisher wishes to make it clear that any views

or opinions expressed in this report by individual authors or contributors are their personal views and

opinions and do not necessarily reflect the views/opinions of the Publisher.

3

Table of Contents

About the author 2

Disclaimer 2

Executive summary 11

Market drivers and resistors 11 Growth opportunities in bakery and cereals 12 Innovations and NPD in bakery and cereals 13 Key trends and product examples 14

Chapter 1 Introduction 15

What is this report about? 15 The market defined 16 Report structure 19

Chapter 2 Market drivers 20

Summary 20 Introduction 21 Mature markets 22 Competitive pressures 22 Economic recession 22 Raw materials prices 23 Tightening of health regulations 24

Growing sophistication of consumer demand 25 Ethical consumerism 26 Shift to mass customization 28 Requirements for better targeting and credibility 32

Immature markets 33 Socioeconomic drivers 33 Middle class expansion 33 Smaller households 35

4

The increasing proportion of women in the labor force 36

Impact on consumption 38 Emergence of premium bakery and cereals 38 Changes in consumption patterns 39

Chapter 3 Growth opportunities in the bakery and cereals market 40

Summary 40 Introduction 41 Bakery and cereals market overview 41 Value by geography 42 Market value by country 43 Market value by category 45 Value by sub-category 47 The bakery and cereals market in Europe 52 The bakery and cereals market in the Americas 53 The bakery and cereals market in Asia-Pacific 56 Emerging markets for bakery and cereals 58 Russia 58

Mexico 59

Brazil 60

China 60

India 60

Chapter 4 Innovation and NPD in bakery and cereals 61

Summary 61 Introduction 61 Innovation type 62 Regional analysis 63 Europe 65

Asia-Pacific 69

North America 72

5

Category analysis 76 Cookies 78

Breakfast cereals 80

Bread and rolls 82

Cakes and pastries 83

Crackers 86

Cereal bars 88

Morning goods 90

Packaging analysis 93 The changing position of bakery and cereal products 94 Flavor trends 96

Chapter 5 Key trends and product examples 98

Summary 98 Introduction 99 Health and wellness 99 Using healthy ingredients found in other food categories 99 Probiotics 99 Energy bakery and cereal products 100

Targeting niche markets 101 Gluten-free products 101 Alternative-sweetener-based bakery and cereals 102

Wellness ingredients 106 Plant sterols 106 Palm oil – the new alternative to hydrogenated oils 107 Whole grains 108 Use of fruits and superfoods 110

Weight management 112 Portion control 112 Satiety products 113

Private label 115 Sustainability 116

6

Packaging developments 116

Provenance 118

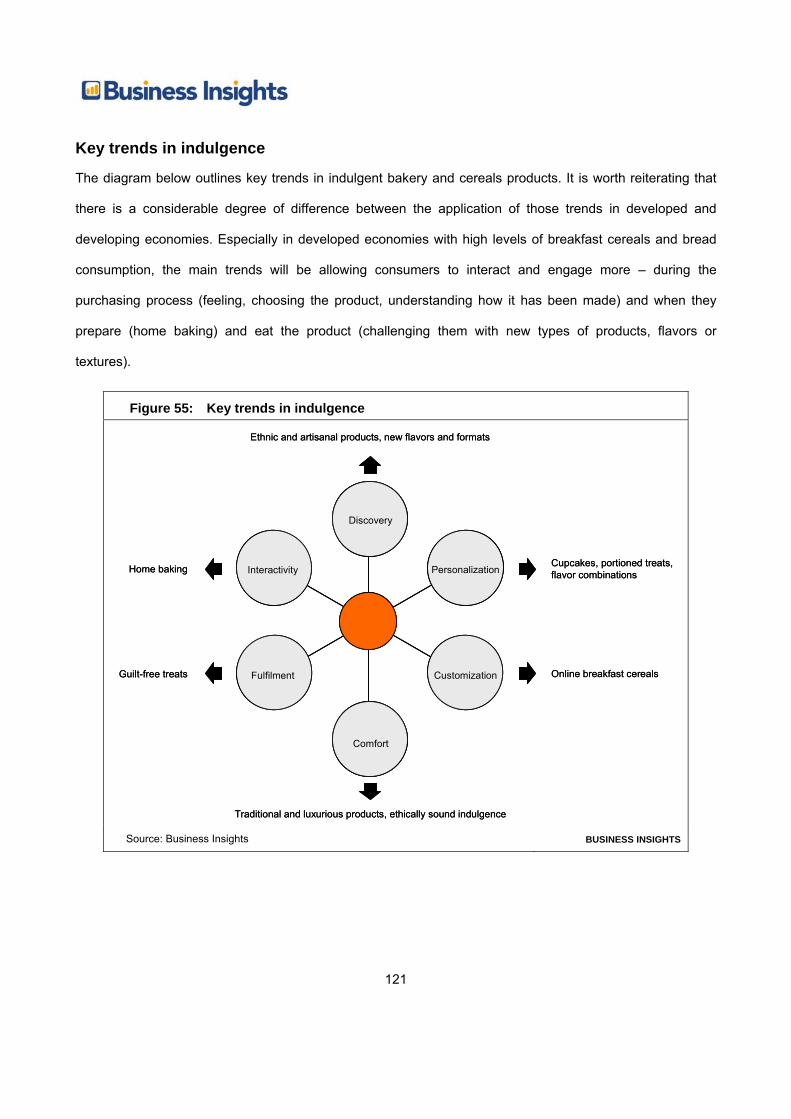

Indulgence 120 Tiers of premiumization 120

Key trends in indulgence 121

Chapter 6 Conclusions 123

Five key trends for the future 123 1 - Alternative natural sweeteners 123

2 - Whole grains and healthier ingredients 123

3 - Indulgence in developed and developing markets 124

4 – Crossover with other product categories 124

5 - Provenance 124

7

Table of figures Figure 1: US wheat prices ($ per metric ton), 2005-2010 23 Figure 2: Premiumization in mature bakery and cereals markets 25 Figure 3: Number of farmers’ markets in the US, 1994-2010 27 Figure 4: The growth of online grocery retail – UK market 29 Figure 5: Mymuesli website 30 Figure 6: Me & Goji custom artisanal cereal website 31 Figure 7: Marketing health – the increased importance of specificity and credibility 32 Figure 8: Trends in global middle class growth 33 Figure 9: Global bakery and cereals market value ($bn), 2009–14 42 Figure 10: Top 10 bakery and cereal markets, by value ($bn), 2009–14 45 Figure 11: Global bakery and cereals market value, by category (%), 2009 and 2014 47 Figure 12: Growth in top 10 bakery and cereals sub-categories, CAGR (%) 2009–14 51 Figure 13: Emerging bakery and cereal markets, by value ($bn), 2009–14 59 Figure 14: Share of new product launches by innovation type (%), 2007–10 63 Figure 15: Share of new product launches by region (%), 2007–10 64 Figure 16: Share of top 10 countries in NPD in Europe (%), 2007–10 65 Figure 17: Share of products launched in Europe, by category (%), 2007–10 67 Figure 18: Food For Life's Ezekiel 4:9 Sprouted 100% Whole Grain Bread 69 Figure 19: Share of products launched in Asia-Pacific (%), by category, 2007–10 70 Figure 20: Sunfeast Marie Light Oats biscuits 71 Figure 21: Share of products launched in North America (%), by category, 2007–10 73 Figure 22: Hot-Kid Organic Toddler Mum-Mum caramel flavored rice biscuits 75 Figure 23: Share of new bakery and cereal launches, by category (%), 2007 and 2010 77 Figure 24: Lotte's Margaret Five Grains Black Cookie 78 Figure 25: Sentir Bem Biscoito Integral 80 Figure 26: Ik Wil Bolletje Brod in de Melk breakfast cereal 81 Figure 27: Woolworths sandwich bread 83 Figure 28: Nestlé's Toll House Ready to Bake Brownie Limited Edition Fudgy Brownies 86 Figure 29: Kashi's Heart to Heart Whole Grain Crackers 88 Figure 30: Mareblu Naturals' Premium Crunch Bar Strawberry Pomegranate Trail Mix 90 Figure 31: Vitalicious' VitaTops Muffin Tops 91

8

Figure 32: Isabella's Healthy Bakery Activate Probiotic Raisin Bran enriched muffins 92 Figure 33: Kellogg's Frosted Flakes space-saving cereal box 94 Figure 34: Attune's All Natural Digestive Health Probiotic Granola Munch 100 Figure 35: Isostar Pulse Easy Power cereal bars 101 Figure 36: Vitalin Racao Humana Quinoa e Amaranto 102 Figure 37: GrandyOats Goji Agave Organic Granola 103 Figure 38: Granix Cereal Free 104 Figure 39: Nickanedit Gluten-free Chocolate Torte a la Cocoa Gourmet Dessert 105 Figure 40: Kashi's Heart to Heart Whole Grain Crackers 107 Figure 41: Coppenrath's Diatgenuss Wiener Sandringe cookies 108 Figure 42: Wasa's Whole Grain Crispbread 109 Figure 43: Carrefour's Musli cu Fructe 110 Figure 44: New England Naturals' Organic Granola – Antioxidant and Gluten-Free variants 111 Figure 45: Doctor in the Kitchen's Flax Seed Crackers, packaging and nutrition information 112 Figure 46: FullBar - 100% Natural Bar - Cinnamon Roll 113 Figure 47: Otsuka Soyjoy Snack Bar – strawberry variant 114 Figure 48: Gardenia's Slim 'n Fit Wheaten Bread 114 Figure 49: Share of private labels in new product launches (%), 2007–10 115 Figure 50: Casino's Sans Gluten Tartines Craquantes Riz et Mais 116 Figure 51: Pure NRG's Fresh Baked Vegan Nutrition Chia Breakfast Bar 117 Figure 52: Immaculate Baking's Dark Chocolate Biscotti Crunch 118 Figure 53: Sustainability and provenance bringing in wider values of health and exclusivity 119 Figure 54: Tiers of premiumization in food and drinks 120 Figure 55: Key trends in indulgence 121

9

Table of tables Table 1: Definition of bakery and cereal categories 16 Table 2: Middle class population size (m) & share of global total (%), 2009-2030 34 Table 3: Average household size by selected countries, (number of people), 1990–2015 36 Table 4: Proportion of labor force which is female (%), 1990-2015 37 Table 5: Global bakery and cereals market value ($bn), 2009–14 41 Table 6: Global bakery and cereals market shares, by geography ($bn), 2009–14 43 Table 7: Top 10 bakery and cereals markets, by value ($bn), 2009–14 44 Table 8: Global bakery and cereals market value, by category (%), 2009 and 2014 46 Table 9: Global bakery and cereals market value, by category and sub-category ($bn), 2009–14

49 Table 10: European bakery and cereals market value ($bn), by category and sub-category,

2009–14 52 Table 11: Americas bakery and cereals market value ($bn), by category and sub-category,

2009–14 54 Table 12: Asia-Pacific bakery and cereals market value ($bn), by category and sub-category,

2009–14 57 Table 13: Share of new product launches (%), by innovation type, 2007–10 62 Table 14: Share of new product launches, by region (%), 2007–10 64 Table 15: Share of products launched in Europe (%), by category, 2007–10 66 Table 16: Top 10 claims made by bakery and cereal products launched in Europe, 2007–10 68 Table 17: Share of products launched in Asia-Pacific (%), by category, 2007–10 69 Table 18: Top 10 claims made by bakery and cereal products launched in Asia-Pacific, 2007–10

71 Table 19: Share of products launched in North America (%), by category, 2007–10 72 Table 20: Top 10 claims made by bakery and cereal products launched in North America, 2007–

10 74 Table 21: Share of new bakery and cereal launches, by category (%), 2007 and 2010 76 Table 22: Top 10 claims for cookies (%), 2007–10 79 Table 23: Share of new breakfast cereals launches by regions (%), 2007 and 2010 81 Table 24: Top 10 claims for breads and rolls (%), 2007–10 82 Table 25: Share of new cakes and pastries launches, by region, 2007 and 2010 84

10

Table 26: Top 20 claims for cakes and pastries (%), 2007–10 85 Table 27: Top 10 claims for crackers (%), 2007–10 87 Table 28: Top 10 flavors for crackers (%), 2007–10 89 Table 29: Share of new morning goods launches (%), by region, 2007 and 2010 90 Table 30: Top 10 pack types for new bakery and cereal launches (%), 2007–10 93 Table 31: Top 20 claims for new bakery and cereals launches (% of products with claims),

2007–10 95 Table 32: Top 20 flavors for new product introductions (% of bakery and cereal product

launches), 2007 and 2010 97

11

Executive summary

Market drivers and resistors Regulatory and consumer awareness campaigns promoting the health benefits of baked goods

and cereals that are largely made from whole grains have increased new product development

(NPD) in healthier products.

Tighter health claims regulation in Europe will restrict the development of functional bakery and

cereals products. However, this will also create opportunity for companies looking to capitalize on

this precarious market niche.

Rising consumer demand for 100% natural and organic foods has increased NPD in bakery and

cereals that are free from artificial additives.

The combination of longer working and commuting hours has increased consumer demand for

convenient yet nutritional meal alternatives, such as ready-to-bake or ready-to-eat cereals and

baked goods.

Emulating the mass customization initiatives of foodservice chains, bakery and cereals

manufacturers are trying harder to involve consumers in choosing the ingredients used in their

products through novel distribution channels, such as the internet.

12

Growth opportunities in bakery and cereals The global bakery and cereals market was worth $358bn in 2009, an increase of 3.2% over 2008.

Business Insights forecast this market to grow at a compound annual growth rate (CAGR) of

3.4% to reach $423bn in 2014.

Europe was the largest market for bakery and cereals in 2009, worth $165bn, and is forecast to

grow at a CAGR of 2.3% to reach $185bn in 2014. As part of the staple diet for European

consumers, bread will continue to drive demand for baked goods in the region.

The top 10 countries together accounted for over 65.6% of the global bakery and cereals market

by value in 2009, with the US being the largest market, worth $60bn.

Bread and rolls is the largest bakery and cereals category, $179bn in 2009 and forecast to grow

at a CAGR of 2.3% to reach $201bn in 2014. This expansion will be primarily driven by increased

demand for products that fall under the artisanal and industrial bread and rolls sub-categories.

India is a low value but high growth country. With more middle class consumers working longer

hours, breakfast cereals provide a convenient option as a breakfast. As a consequence it will be

the fastest growing category in India, although per capita consumption will still be very low.

13

Innovations and NPD in bakery and cereals Among all new product launches during 2007–10, only 0.5% were innovative. Innovations in

formulation accounted for 83.3% of all innovations in bakery and cereals in 2010, an increase of

15.1 percentage points over 2007.

Europe accounted for 43.2% of all new product launches in bakery and cereals in 2010, an

increase of 9.4 percentage points over 2007.

The majority of NPD has taken place in the cookies category over 2007–10, which accounted for

34.5% of new launches globally in 2010.

Packaging innovation has taken a back seat, with little significant development since 2008. Boxes

have been the most commonly used packaging for bakery and cereals products launched over

2007–10.

Chocolate has continued to dominate among all flavors since 2007, with a share of 9.6% in 2010,

but there is a growing trend of dual and fused flavors, such as chocolate vanilla and strawberry

banana.

14

Key trends and product examples Manufacturers’ growing focus on reducing fat, sodium and sugar in bakery and cereals has led to

the development of trans-fat-free products, calorie-counted portion packs and the further

fortification of baked goods and cereals with nutritious ingredients such as whole grains.

Regulatory pressures in developed markets such as Europe, which require bakery and cereals

manufacturers to provide sufficient evidence for functional claims, are driving the use of

ingredients found in rival categories, such as dairy products and soft drinks. By using established

ingredients such as prebiotics, probiotics and guarana, companies are avoiding having to conduct

new and expensive research and development.

Bakery and cereals manufacturers are targeting niche segments such as children, and health-

cautious and ailing consumers by offering healthier alternatives such as low calorie sweeteners,

superfoods and gluten-free products.

Innovations in packaging are being driven by sustainability and the potential of recyclable and

biodegradable materials to help limit environmental impact.

The ‘natural’ tag is increasingly being used for new product launches, to display product

characteristics such as traditional and authentic ingredients.

15

Chapter 1 Introduction

What is this report about? The global bakery and cereals market was worth $358bn in 2009, an increase of 3.2% over 2008. The

market will grow at a CAGR of 3.4% over 2009–14 to reach a value of $423bn in 2014. Emerging markets

such as Mexico, Russia, Brazil, China and India will play a pivotal role in the development of the bakery and

cereals industry, driven by the growing influence of Western culture, a rising demand for staple foods, and a

growing acceptance of alternative forms of bakery and cereals as opposed to traditional meal products. In

Europe and the US, meanwhile, the growing demand for bakery and cereals is primarily being driven by

health conscious and time-constrained consumers.

This report contains a summary of the important and novel bakery and cereal products launched between

June 2006 and May 2010, as reported by Product Launch Analytics, an in-house database of new product

launches in the fast moving consumer goods industry. This allows the analysis of innovation and NPD by

region and category. In addition, market data on the value growth of the bakery and cereals market is

examined and emerging market trends are highlighted, thereby enabling manufacturers to identify key

growth opportunities.

16

The market defined Within this report, the bakery and cereals market is segmented into seven categories:

Table 1: Definition of bakery and cereal categories

Categories Definition

Bread and rolls

Artisanal bread and rolls Bread products produced by small local bakeries. Associated with the fundamentals of the age-old bread-making tradition with greater attention to ingredients and the baking process.

Industrial bread and rolls Pre-packed industrially manufactured bread products generally made at dedicated premises and sold through retail outlets. For example Warburton's, Hovis and Sara Lee.

In-store bakery Bakery products sold through non-specialist stores that have been baked or semi-baked ('finished off') at the point of sale.

Breakfast cereals Hot cereals Breakfast cereal that requires heating before consumption.

Includes traditional products (e.g. porridge oats), instant mixes (e.g. Ready Brek), and ready-to-heat products (e.g. Quaker Instant Oatmeal Express)

Ready-to-eat cereals Breakfast cereal that does not require heating. Includes dry cereals and prepackaged cereal/milk kits (e.g. Kellogg's Cornflakes and Weetabix).

Cakes & pastries Artisanal cakes & pastries Cakes and pastries produced by small local bakeries for sale on

the premises. Excludes morning goods. Industrial cakes & pastries Pre-packed industrially manufactured cakes and pastries generally

made at dedicated premises and sold through retail outlets (e.g. Mr Kipling cakes, Entenmann's cakes). Excludes frozen cakes and pastries, and morning goods.

In-store bakery Cakes and pastries sold through non-specialist stores that have been baked or semi-baked ('finished off') at the point of sale. Excludes morning goods.

17

Categories Definition Cookies (sweet biscuits) American cookies A small, usually flat and crisp biscuit made from sweetened dough

(e.g. Maryland cookies, Chips Ahoy!). Artisanal cookies Cookies produced by small local bakeries for sale on the premises. Assortments Variety boxes usually packaged in metal tins. Examples include

Veno's Danish butter biscuits and Delacre Assorted Biscuits. Butter-based cookies Products that position themselves as butter-based (e.g. Leibniz

Butter) or as shortbread (e.g. Walker's Shortbread). Chocolate cookies Products coated with chocolate on one or both sides, such as

chocolate digestives. Only includes products sold in the cookie section of retail outlets: product lines such as Kit-Kat are excluded.

Cream filled A cream-based filling sandwiched between two cookies and not coated in chocolate (e.g. Custard Creams, Oreos).

In-store bakery Cookies sold through non-specialist stores that have been baked or semi-baked ('finished off') at the point of sale.

Plain cookies Also known as 'semi-sweet.' Slightly sweet crackers made with whole-wheat flour (e.g. McVities' Digestives, Keebler Graham crackers).

Wafer biscuits A light, sweet product slightly thicker than a wafer, with a creamy filling (e.g. Manner).

Other cookies All other sweet biscuit products. Crackers (savory biscuits)

Bread substitutes Dry, thin, crisp biscuits generally used as an alternative to bread, also known as dry wafers (e.g. Ryvita).

Cheese-flavored crackers Cheese-flavored savory biscuits of any kind (e.g. Cheez-It, Cheddars).

Plain crackers Hard, dry savory biscuits, generally hard or crisp. Can be salted, such as Ritz, or unsalted such as Jacobs' Cream Crackers. Does not include cheese flavored crackers.

Other crackers All savory biscuits other than cheese, plain crackers, and bread substitutes.

18

Categories Definition Morning goods Artisanal morning goods Breakfast bakery products created by small local bakeries.

Includes bagels, croissants (plain and flavored), donuts, muffins, and scones. Excludes Danish pastries.

Industrial morning goods Pre-packed industrially manufactured breakfast bakery products generally made at dedicated premises and sold through retail outlets. Includes bagels, croissants (plain and flavored), donuts, muffins, and scones. Excludes frozen products and Danish pastries.

In-store bakery Breakfast bakery products sold through non-specialist stores that have been baked or semi-baked ('finished off') at the point of sale. Includes bagels, croissants (plain and flavored), donuts, muffins, and scones. Excludes frozen products and Danish pastries.

Cereal bars Sports and energy bars Bars made from a mixture of cereals, fruits and active ingredients

for performance enhancement bound together by syrup and designed specifically for active consumers.

Granola/muesli bars Bars made from a mixture of cereals, fruits and nuts bound together by syrup.

Other bars All other cereal bars.

Source: Business Insights BUSINESS INSIGHTS

19

Report structure The chapters of this report are structured as follows:

Introduction – report overview and methodology.

Market drivers – highlighting the factors that are influencing consumer demand and helping to

drive and restrict NPD in the bakery and cereals industry.

Growth opportunities in bakery and cereals – review of market value by region, country and

category, with market projections to 2014 (using 2009 as the base year), including an evaluation

of growth potential.

Innovation and NPD – review of innovation by category, region and type. This chapter also

identifies flavor trends and analyzes the use of key product tags on product packaging.

Key trends – overview of emerging trends within the bakery and cereals market.

Conclusions – summary of key trends and future opportunities within the bakery and cereals

market.

20

Chapter 2 Market drivers

Summary Regulatory and consumer awareness campaigns promoting the health benefits of baked goods

and cereals that are largely made from whole grains have increased new product development

(NPD) in healthier products.

Tighter health claims regulation in Europe will restrict the development of functional bakery and

cereals products. However, this will also create opportunity for companies looking to capitalize on

this precarious market niche.

Rising consumer demand for 100% natural and organic foods has increased NPD in bakery and

cereals that are free from artificial additives.

The combination of longer working and commuting hours has increased consumer demand for

convenient yet nutritional meal alternatives, such as ready-to-bake or ready-to-eat cereals and

baked goods.

Emulating the mass customization initiatives of foodservice chains, bakery and cereals

manufacturers are trying harder to involve consumers in choosing the ingredients used in their

products through novel distribution channels, such as the internet.

21

Introduction Broadly speaking there are two distinct sections of the global bakery and cereals market: mature and

immature markets. With stark differences in their level of development, the driving forces for each can be

quite different. As a staple product, bakery and cereals have reached a level of saturation in many markets.

In these areas manufacturers are under pressure to add value to their products and appeal to the growing

sophistication of consumer demand. In immature markets there are fundamental socio-economic shifts which

serve as the primary influencers of change.

Mature markets

o Competitive pressures

Economic recession

Wheat prices

Tightening of health regulations

o Growing sophistication of consumer demand

Ethical consumerism

Shift to mass customization

Requirements for better targeting and credibility

Immature markets

o Socioeconomic forces

Middle class expansion

Smaller households

Growing female workforce

22

o Impact on consumption

Changing consumption patterns

Emergence of premium bakery and cereals

Mature markets

Competitive pressures

In mature markets, there are a wide range of internal competitive pressures as well as changes in consumer

behavior and lifestyles which are currently influencing the bakery and cereals market. The core pressures

include the recent recession, rising raw material price increases and tightening health regulations.

Economic recession

Given the maturity of Western consumer goods markets, the recent economic downturn represented the key

threat to overall market growth. European and US demand for many products contracted in the immediate

aftermath of the financial crisis towards the end of 2008. However, unlike many consumer areas, the bakery

and cereals market has been relatively well insulated against the impact of the recession. Product categories

classed as ‘essentials’, such as bread, breakfast cereals have proved resilient, helped by a downward

movement in prices from their 2008 peak.

In some cases, where consumers have traded down from foodservice – such as eating out or buying

takeaway food, products that offer a sense of indulgence or luxury have actually benefited: a good example

of this is premium ready meals. At the same time, in some markets artisanal bread or more premium cereals

have also seen growth as consumers cut back on more conspicuous luxuries but indulge on groceries

brought into the home.

23

Raw materials prices

The rising cost of staples such as corn, rice and wheat since June 2010 has raised fears of a global food

crisis, with even the US government warning of “dramatically” lower supplies. The US is the world’s largest

corn grower and its exports make up the majority of global trade in the grain. The USDA had forecast a

record corn crop for 2010 but unfavorable heat and heavy rains forced a re-evaluation of yields. Wheat

prices have soared following poor harvests in several countries, including Russia and Brazil, while heavy rain

in Canada and Europe damaged the production of many grain and oilseed crops through 2010. Commodities

prices are forecast to continue to rise through the next few years, but are not expected to reach 2008 levels.

Nevertheless, combined with the effects of the recession, food manufacturers are under mounting

competitive pressures and this has already brought an impact to food prices on supermarket shelves. In the

bakery and cereals market this leaves companies particularly vulnerable to the threat of private-label.

Figure 1: US wheat prices ($ per metric ton), 2005-2010

100

150

200

250

300

350

400

450

500

Dec

05

Mar

06

Jun

06

Sep

06

Dec

06

Mar

07

Jun

07

Sep

07

Dec

07

Mar

08

Jun

08

Sep

08

Dec

08

Mar

09

Jun

09

Sep

09

Dec

09

Mar

10

Jun

10

Sep

10

Mar

ket p

rice

per t

on ($

)

Average

100

150

200

250

300

350

400

450

500

Dec

05

Mar

06

Jun

06

Sep

06

Dec

06

Mar

07

Jun

07

Sep

07

Dec

07

Mar

08

Jun

08

Sep

08

Dec

08

Mar

09

Jun

09

Sep

09

Dec

09

Mar

10

Jun

10

Sep

10

Mar

ket p

rice

per t

on ($

)

Average

Source: International Monetary Fund BUSINESS INSIGHTS

24

The impact of rising wheat prices in developed markets will be clear: there will be consumer demand for

budget products that help mitigate the impact of rising prices. At the same time, manufacturers will seek to

add value to bakery and cereals products as a way increasing prices and maintaining margins.

Manufacturers with no clear price positioning between budget and premium products will suffer.

Tightening of health regulations

Functional bakery and cereals manufacturers in Europe are awaiting the full impact of impending health

claim legislation. According to the Article 13 of the Nutrition and Health Claims made on Foods Regulation,

the European Food Safety Authority (EFSA) will evaluate all claims other than those referring to “the

reduction of disease risk and to children’s development and health". This article states that all functional

claims made by manufacturers on the label of their products must be supported by appropriate evidence.

This regulation requires companies to provide data to support:

The role of a nutrient or substance and its effects on the functioning of the body;

Possible benefits to psychological and behavioral functions;

Products that claim to increase satiety, reduce weight and offer energy to consumers.

EFSA’s recommendations will be used by the European Commission to form the foundation of necessary

legislative measures, with a ‘positive list’ of permitted claims. Although this overall process has been delayed

due to the large number of claims submitted, the net result will be the same - more stringent health claim

regulation will force food manufacturers to invest in research and development in order to prove new claims.

Tighter regulations may be particularly damaging for private label manufacturers with higher R&D costs

threatening the price point advantage associated with such products. Moreover, the positive list of functional

health claims will restrict manufacturers to using only those claims that have already been approved. This will

lead to a decrease in flavor innovation and a subsequent decline in innovative product introductions in this

market.

25

While it will be difficult for manufacturers to launch foods and beverages with functional claims in Europe,

such product launches will be much more straight-forward in other parts of the world. Although regulations

are present in other developed markets, such as the US and Japan, they are not as stringent as in Europe.

Competition will intensify in the US and Japan with industry leaders trying to increase revenues to

compensate for difficulties in Europe.

Growing sophistication of consumer demand

The growing sophistication of consumers ensures that the demand for greater choice, particularly in value-

added products continues to be a key driver of product innovation.

Figure 2: Premiumization in mature bakery and cereals markets

• Mass customization• Premium ingredients• New flavor combinations

• Organic and artisanal• Focus on ingredients• Simple

• Made with love• Ethical as safe

• New occasions• Competition with confectionery

• Performance management• Weight management• Credible health claims

• With fruit and vegetables• Alternative healthy formats

Indulgence

Ethical & sustainable

Healthy

Convenient

• Mass customization• Premium ingredients• New flavor combinations

• Organic and artisanal• Focus on ingredients• Simple

• Made with love• Ethical as safe

• New occasions• Competition with confectionery

• Performance management• Weight management• Credible health claims

• With fruit and vegetables• Alternative healthy formats

Indulgence

Ethical & sustainable

Healthy

Convenient

Source: Business Insights BUSINESS INSIGHTS

26

Ethical consumerism

The bakery and cereals market is, inevitably, being influenced by the growing ethical awareness among

consumers. Across a wider range of product categories, consumer interest in the sourcing and

manufacturing process is growing – and not only for more premium products. The pervasive belief that

ethical products are ‘better for you’ is also filtering down into mainstream products and creating opportunities

in natural and organic foods to target health conscious consumers.

Sustainability

Environmental concerns are driving ethical awareness among consumers, with manufacturers taking greater

measures to reduce their environmental footprint. These not only involve reductions in packaging waste, but

also include cutting the resources and energy used in the manufacturing process. One controversial issue

central to the bakery and cereal market is intensive farming, characterized by the high inputs of capital,

labor, or heavy usage of technologies such as pesticides and chemical fertilizers relative to land area.

The sensitivity to such farming techniques was seen recently with the incorporation of palm oil in bakery and

cereals as an alternative to the harmful hydrogenated oils. In 2009, the World Wildlife Fund (WWF) warned

manufacturers about the importance of sustainability after the production of palm oil was found to have had a

huge environmental impact in South Asia, where forests were being cleared to make way for more

plantations. Promoting sustainability has become a key – and in some cases almost mainstream - marketing

tool being used by bakery and cereal manufacturers. Production methods, along with the provenance of

ingredients, are prominently highlighted on product packaging to emphasize the amount of care that has

been taken in overall production process. In December 2009, Unilever, the world's largest user of palm oil for

food, cleansers and cosmetics, canceled its $32.6m supply contract with Sinar Mas after independently

verifying a 2008 Greenpeace report implicating the Indonesian palm oil provider in rainforest destruction.

Moreover, the company also pledged to use only certified sustainable palm oil by 2015 without passing on

any added costs to consumers.

27

Local sourcing

In the wider food and drinks industry there has been an increased focus on the source and supply chain of

food and drinks. The increasing significance of sustainability and local sourcing to consumers can be seen in

the continued growth of farmers’ markets, both in Europe and North America. New markets appear regularly,

and existing markets—some well over a century old—are enjoying somewhat of a revival.

Figure 3: Number of farmers’ markets in the US, 1994-2010

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1994 1996 1998 2000 2002 2004 2006 2008 2009 2010

Num

ber o

f far

mer

s’m

arke

ts

+249%4,377 more farmers’ markets

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1994 1996 1998 2000 2002 2004 2006 2008 2009 2010

Num

ber o

f far

mer

s’m

arke

ts

+249%4,377 more farmers’ markets

Source: USDA-AMS-Marketing Services Division BUSINESS INSIGHTS

The importance of local sourcing is crucial to the bakery and cereals market, given the growth of the

supermarket and hypermarket retailing as a share of grocery sales in developed markets. Sales of bread

products supermarkets have risen at the expense of local bakers – but across all channels ‘artisanal bread

and rolls’ continue to represent the largest sub-category by value in the global bakery and cereals market.

This is an interesting paradox, because as consumers continue to challenge the ethical credentials of the

products they buy, the “artisanal” nature of supermarket bakeries will come under some scrutiny. Already, in

countries such as France, artisanal bakers are seeking to emphasize the true artisanal nature of their

products. The challenge for major manufacturers and the supermarkets is to introduce more artisanal

28

qualities, and proper artisanal credentials, into the products they sell. One example of this is UK retailer

Waitrose’s agreement with legendary baker Poilâne to sell artisanal sourdough loaves – a move which dates

as far back as 2002. At the same time, several other UK retailers, including market leader Tesco, are

creating “local produce” programs to mitigate concerns that they are not sufficiently sensitive to local

concerns around the survival of small scale food producers.

Shift to mass customization

Another key trend is the shift towards mass customization. Although this is still a minor trend at present,

mass customization is becoming a more mainstream tool for manufacturers to encourage consumer

engagement in their products. In particular, there are two areas in which consumers are being given the

chance to actively select particular products or product features and interact with their food more:

Interactive online product sales;

Cereal kits.

More bakery and cereal manufacturers are using the internet as a platform for consumers to customize their

diet and order products that are delivered directly to their home. The internet has given companies such as

Nature's Path the ability to allow the consumer to customize the meals they receive (to some extent) and at

the same time, provide nutritious, gourmet meals that consumers do not always have time to prepare. This

process is also designed to increase consumer loyalty and encourage repeat purchasing. The figure below

provides a clear example the fast growth of the online grocery channel. In the UK, forecast growth over the

period 2000-2014 is nearly 2000%, and from a tiny base the online market will capture over 5% of total

grocery sales. This familiarization with online grocery shopping, both its convenience and, increasingly,

additional benefits (such as the store remembering your regular purchases) underpins the use of the online

channel for mass customization efforts in food.

29

Figure 4: The growth of online grocery retail – UK market

0%

1,000%

2,000%

Overall grocery Online grocery

62.3%

1,924.9%

0%

1%

2%

3%

4%

5%

6%

2000 2014

0.4%

5.2%

Forecast market growth, 2000-2014Online retail share of grocery market

0%

1,000%

2,000%

Overall grocery Online grocery

62.3%

1,924.9%

0%

1%

2%

3%

4%

5%

6%

2000 2014

0.4%

5.2%

0%

1%

2%

3%

4%

5%

6%

2000 2014

0.4%

5.2%

Forecast market growth, 2000-2014Online retail share of grocery market

Source: Verdict Research BUSINESS INSIGHTS

However, there have been notable failures also: General Mills introduced mycereal.com in 2001 to allow

consumers to mix up their own cereals. This service has since been discontinued. In 2007, Kellogg’s

launched Coco Pops Creations in the UK, a new 'pick n mix' cereal targeted at children, in the UK. The

product came with a choice of four different cereal shapes and sizes (Coco Pops, Crunchers, Coco Rocks

and Mega Munchers), and allowed children to mix and match according to their preference. However, in

February 2010 Kellogg’s announced it would pull Coco Pops creations as part of an exercise to pare back its

ranges. The message is clear: while consumers want customization, customization alone is not enough. At

the moment, the additional costs implied by customization can only support true premium products.

Examples of online, customized retailers include:

Breakfast cereals: MyMuesli; MeAndGoji.com;

Custom energy bars: Element Bars; YouBar.

30

Mymuesli

www.mymuesli.com was the first platform worldwide that allowed consumers the option of choosing the

ingredients that they wanted and then to purchase the final product online. Launched in 2007 in Germany, it

allows consumers to choose from 80 ingredients to create their combinations. The ingredients on offer

include eccentric and exotic ingredients such Tibetan goji berries, cedar nuts and jelly babies. Additionally,

consumers can also name their creation.

Figure 5: Mymuesli website

Source: Mymuesli website BUSINESS INSIGHTS

31

Me & Goji

A similar website was introduced in the US in 2008 called Me & Goji. Targeted at consumers who have strict

dietary requirements, such as athletes, the ingredients are stamped as US Department of Agriculture

(USDA) certified, to reinforce the brand’s health credentials. In addition to naming the cereal, the site also

allows consumers to upload their picture. Moreover, the store also has a range of pre-mixed cereals

available in gluten-free and energy varieties to cater to health conscious consumers.

Figure 6: Me & Goji custom artisanal cereal website

Source: Meandgoji BUSINESS INSIGHTS

32

Requirements for better targeting and credibility

EFSA’s impact manufacturers’ use health claims in Europe will be profound. Elsewhere, however,

manufacturers have also had to reevaluate health claims. For example, Danone has come under scrutiny in

the US for claims made against some of its probiotic products. Even with these changes, some terms – such

as “natural” are used heavily to the point of becoming almost generic. Changing consumer expectations and

a harsher regulatory landscape will drive development on two fronts: specificity and credibility of claims. Of

the two, credibility of health claims will be more important. Soft claims will have to become even softer to the

point of being both vague and generic and in many cases will be rejected by consumers. By contrast, R&D-

supported, more credible health claims will allow manufacturers to mine niches and develop proprietary

positionings, although the specificity of the benefit – will determine how quickly products commoditize.

Figure 7: Marketing health – the increased importance of specificity and credibility

Credibility

Spec

ifici

ty

Lack of credibility: needs further R&D

Credible and specific:Opportunities to mine

niche and develop proprietary positioning

and/or ingredients

Credible, but possibly vulnerable to

commoditization

Generic soft claims, increasingly rejected

as credible

Credibility

Spec

ifici

ty

Lack of credibility: needs further R&D

Credible and specific:Opportunities to mine

niche and develop proprietary positioning

and/or ingredients

Credible, but possibly vulnerable to

commoditization

Generic soft claims, increasingly rejected

as credible

Source: Business Insights BUSINESS INSIGHTS

33

Immature markets The rapid pace of economic development of many countries in Asia and South America will have a massive

impact on consumption patterns. Across these emerging markets, urban populations are rising; more women

are entering the workforce; the emerging middle classes are driving consumption of more sophisticated,

premium products.

Socioeconomic drivers

The single most important factor influencing the development of immature markets is the rise in disposable

incomes and the growth of the middle class.

Middle class expansion

The rise in disposable income in the newer economies is closely allied to the development of the middle

class. As economies have developed and moved from a situation of primarily export-led growth to one in

which industries develop to feed domestic consumer demand, increasing numbers of the population have

been able to move up into the middle classes, with a corresponding rise in income and consumption.

Figure 8: Trends in global middle class growth

Middle class expansion in Asia particularly China and India

Current/futureMiddle class expansion in Asia particularly China and India

Current/futureWorld's middle class concentrated in Europe, North America & Japan

Pre 1970’sWorld's middle class concentrated in Europe, North America & Japan

Pre 1970’s

Rising GDP/disposable income

Rising GDP/disposable income

Convert savings to consumptionConvert savings to consumption

Expanding global middle classExpanding global middle class

Brazil, South Korea, Mexico and Argentina built sizeable middle-class populations

1970’s-1980’sBrazil, South Korea, Mexico and Argentina built sizeable middle-class populations

’sMiddle class expansion in Asia particularly China and India

Current/futureMiddle class expansion in Asia particularly China and India

Current/futureMiddle class expansion in Asia particularly China and India

Current/futureMiddle class expansion in Asia particularly China and India

Current/futureWorld's middle class concentrated in Europe, North America & Japan

Pre 1970’sWorld's middle class concentrated in Europe, North America & Japan

Pre 1970’sWorld's middle class concentrated in Europe, North America & Japan

Pre 1970’sWorld's middle class concentrated in Europe, North America & Japan

Pre 1970’s

Rising GDP/disposable income

Rising GDP/disposable income

Convert savings to consumptionConvert savings to consumption

Expanding global middle classExpanding global middle class

Rising GDP/disposable income

Rising GDP/disposable income

Rising GDP/disposable income

Rising GDP/disposable income

Convert savings to consumptionConvert savings to consumptionConvert savings to consumptionConvert savings to consumption

Expanding global middle classExpanding global middle classExpanding global middle classExpanding global middle class

Brazil, South Korea, Mexico and Argentina built sizeable middle-class populations

1970’s-1980’sBrazil, South Korea, Mexico and Argentina built sizeable middle-class populations

’sBrazil, South Korea, Mexico and Argentina built sizeable middle-class populations

1970’s-1980’sBrazil, South Korea, Mexico and Argentina built sizeable middle-class populations

’s

Source: Business Insights BUSINESS INSIGHTS

34

In China and India middle class expansion is most marked, although in other areas, such as South America,

Russia and East European countries there have also been significant increases in disposable income.

The OECD’s definition of middle class is households with daily expenditure between $10 and $100 per

person in purchasing power parity terms. It estimates that there were 1.8bn people in the global middle class

in 2009. Europe has the highest share of the global middle class population at 36%, with North America on

18% as shown below. In both cases, these account for almost all the entire population of the region. The

largest opportunity is Asia-Pacific, where 28% of the global middle class, lives amounting to 525m people –

or less than a quarter of the region’s total population. Over the next 10 years, the OECD forecasts that 1.2bn

people in the Asia-Pacific region will be born into or move into the global middle class. This represents the

largest single expansion in consumer spending power ever recorded, with the number of global middle class

consumers increasing by 75% between 2009-2020 due to rising incomes in India, China, Indonesia, and

across the region. Although relatively poorer, the number of middle class consumers in Africa is nonetheless

forecast to almost double between 2009–20, representing further opportunities.

Table 2: Middle class population size (m) & share of global total (%), 2009-2030

2009 2020 2030 Actual

(m) Share Actual

(m) Share Actual

(m) Share

North America 338 18% 338 10% 332 7%Europe 664 36% 706 22% 680 14%Central & South America 181 10% 251 8% 313 6%Asia-Pacific 525 28% 1,740 54% 3,228 66%Sub-Saharan Africa 32 2% 57 2% 107 2%Middle East North Africa 105 6% 165 5% 234 5%Overall 1,845 100% 3,257 100% 4,894 100%

Source: OECD Development Centre BUSINESS INSIGHTS

35

In ten years' time, the proportion of the global middle classes living in the traditional western markets of

North America and Europe will have fallen from over half in 2009 to less than one-third, as the proportion

living in Asia-Pacific increases to 54% and onto 66% by 2030.

Smaller households

Another feature of the rising levels of disposable income in emerging markets is the decreasing size of the

average household. Globally, the number of people living alone has increased from 153.5m in 1996 to

202.6m in 2006. The trend to small or single person households reflects economic and cultural standards.

Living alone is more expensive than sharing; there is a direct correlation between wealth and the proportion

of people living alone. Smaller households are more likely to buy more expensive or premium products for

three reasons:

A great likelihood of buying convenience and single serve foods which tend to be premium

priced;

Fewer members of household, invariably children, to support hence a greater discretionary

income;

People are far more likely to buy premium goods for themselves or their partner than children.

Research undertaken in the UK in 2007 found that 81% of shoppers will buy premium products

for themselves, 60% will buy for their partner but only 26% would buy premium products for their

children.

The table below shows the change in the average household size from 1990 to 2015 in a range of significant

economies.

36

Table 3: Average household size by selected countries, (number of people), 1990–2015

1990 2000 2010 2015 est. % change 1990-2015 Brazil 4.04 3.2 2.82 2.74 -32%China 3.87 3.4 2.97 2.82 -27%Germany 2.31 2.19 2.11 2.09 -10%India 5.76 5.49 5.3 5.28 -8%Japan 2.78 2.71 2.71 2.71 -3%Spain 3.2 2.89 2.82 2.82 -12%United Kingdom 2.43 2.39 2.17 2.09 -14%United States 2.61 2.5 2.44 2.44 -6%

Source: Business Insights BUSINESS INSIGHTS

Even in highly westernized societies where this trend has been evident since the 1970s the average

household size continues to fall by around ten percent (the only exception being Japan, estimated to fall by

just 3% over this 25 year period). In many of the developing economies, illustrated here by Brazil and China,

household size is falling rapidly.

The increasing proportion of women in the labor force

The table below shows the percentage of the workforce which is female in a selection emerging markets. In

all countries, except for Russia, China and India, the female proportion of the labor force has increased

significantly since 1990 and continues to increase, most markedly in Brazil (from 32% in 1990 to an

estimated 44% in 2015) and Argentina (28% to 42%). In China and India, it is the equivalent rapid growth in

the number of males in the workforce that has kept the proportion of females unchanged rather than a lack of

growth in the absolute number of women working.

37

Table 4: Proportion of labor force which is female (%), 1990-2015

% 1990 2000 2010 2015 est. Argentina 28.4 38.9 41.9 42.5Brazil 32.1 40.8 44.1 44.7Chile 30.5 33.4 37.1 38.3China 44.8 45.6 45.9 45.8Columbia 37.7 43.8 46.7 47.0India 27.6 27.9 28.6 29.2Mexico 30.0 33.2 37.0 38.8Russia 48.5 48.4 49.9 50.1Saudi Arabia 11.2 12.9 16.0 17.3South Africa 41.9 43.9 45.5 45.8

Source: Business Insights BUSINESS INSIGHTS

The impact of a greater proportion of women working outside the home is well documented. The pressure of

combining work, family life and / or social life means there is less time for cooking and a trend towards

convenience. Women, who continue to be the main grocery shoppers, have been increasingly the source of

the money that they are spending in the supermarket. This and the fact that (until the economic downturn),

there was more money to spend in the supermarket, has led to an increasing comfort with, and desire to

‘trade up’ beyond the products that would have previously been purchased.

38

Impact on consumption

Emergence of premium bakery and cereals

These socioeconomic factors are leading to the emergence of premium bakery and cereals in immature

markets. While the nature of premiumization in western countries post-recession is one of concerned

consumerism, with an interest in health, provenance and even conspicuous altruism, in the developing

countries the more traditional consumer motivations of luxury, indulgence, and conspicuous consumption

dominate.

The effect of the economic and social factors – rising income, smaller households, more women working –

represent the major forces leading to increased demand for more premium products, but other specific

consumer issues have been important:

Continued increase in sophistication of tastes resulting from a higher frequency of eating out; a

greater number of, and variety in, restaurants and takeaways offering food from different cultures,

and increasing foreign travel;

Allied with the above, an increase in food as status; a ‘badge’ to indicate how sophisticated /

refined / knowledgeable one is;

An increased interest in cooking and entertaining. Food has become of much greater interest, as

evidenced by the growth in cooking magazines, cookery books, gastronomy or cooking based

holidays and, more than all else, the rise of the TV chef genre;

Concerns with food safety and production values. In stark contrast to the 1970s and early 1980s

when highly processed foods were embraced for their modernity and time-saving qualities, a

series of concerns has led to a willingness to pay more for food whose quality can be assured.

39

Changes in consumption patterns

While increased wealth and the rising demand for premium products is driving NPD in immature markets,

manufacturers are also being led by the growing influence of Western culture. This has particular

significance in the bakery and cereals market which consists of product categories that are generally

associated with the West. In Asia, the market for bakery and cereals is increasing as consumption patterns

continue to westernize. In India, the popularity of breakfast cereals is expected to continue to increase over

the coming years, with major participants being multinationals such as Kellogg's, Quaker Oats (owned by

PepsiCo), Bagrry's, and Mohan Meakins Limited. China is a good example of the extent of these changes.

In China, although 60% of the population still lives in rural areas, the 40% that reside in its cities (World

Bank, 2008) have embraced many of the consumer behaviour traits seen in Europe and North America.

Harnessing this growth, China hosted Bakery China Expo in 2008, a major exhibition in the country’s

economic hub, Shanghai, which attracted local suppliers and participants along with a growing international

contingent of exhibitors. There are a number of key factors driving the bakery and cereals market in China:

Chinese consumers are starting to eat bread for breakfast instead of traditional rice porridge and meat

buns because they think bread is a better complement to milk and is also a healthy item;

Unpackaged/artisan bread in China is increasingly being sold in hypermarkets and bakery stores;

Western lifestyles and the expanding snacking culture is increasing demand for packaged/industrial

bread in China. Whole-wheat sandwich and white are the two most popular varieties of packaged bread;

most Chinese consumers prefer soft white bread to hard bagels or baguettes. Whole-wheat sandwich

bread is popular among older and young female consumers due to its health benefits;

Green tea and fruit-flavored breads are also growing in popularity. Children and teenagers are the main

consumers of flavored bread.

40

Chapter 3 Growth opportunities in the bakery and cereals market

Summary The global bakery and cereals market was worth $358bn in 2009, an increase of 3.2% over 2008.

Business Insights forecast this market to grow at a compound annual growth rate (CAGR) of

3.4% to reach $423bn in 2014.

Europe was the largest market for bakery and cereals in 2009, worth $165bn, and is forecast to

grow at a CAGR of 2.3% to reach $185bn in 2014. As part of the staple diet for European

consumers, bread will continue to drive demand for baked goods in the region.

The top 10 countries together accounted for over 65.6% of the global bakery and cereals market

by value in 2009, with the US being the largest market, worth $60bn.

Bread and rolls is the largest bakery and cereals category, $179bn in 2009 and forecast to grow

at a CAGR of 2.3% to reach $201bn in 2014. This expansion will be primarily driven by increased

demand for products that fall under the artisanal and industrial bread and rolls sub-categories.

India is a low value but high growth country. With more middle class consumers working longer

hours, breakfast cereals provide a convenient option as a breakfast. As a consequence it will be

the fastest growing category in India, although per capita consumption will still be very low.

41

Introduction This chapter analyzes the value growth projections of the global bakery and cereals market during the period

2010–14. It provides an overview of the major markets for bakery and cereals and analyzes the performance

of the categories and sub-categories within the sector. Additionally, this chapter also highlights the growth

opportunities available to bakery and cereal manufacturers in emerging markets.

Bakery and cereals market overview The global bakery and cereals market was worth $358bn in 2009, an increase of 3.2% over 2008. Business

Insights forecasts the market to grow at a CAGR of 3.4% over 2009–14 to reach $423bn in 2014. Increasing

consumer sophistication in mature markets and socio-economic shifts in emerging markets will drive demand

for bakery and cereals.

Table 5: Global bakery and cereals market value ($bn), 2009–14

2009 2010 2011 2012 2013 2014 CAGR

2009–14Market value ($bn) 358.1 369.9 382.2 395.1 408.6 422.8 Growth rate 3.3% 3.3% 3.4% 3.4% 3.5% 3.4%

Source: Business Insights BUSINESS INSIGHTS

42

Figure 9: Global bakery and cereals market value ($bn), 2009–14

320

340

360

380

400

420

440

2009 2010 2011 2012 2013 2014

Mar

ket s

ize

($bn

)

1%

2%

3%

4%

Gro

wth

rate

(%)

Market Value Growth Rate

Year end December 31, 2009.

320

340

360

380

400

420

440

2009 2010 2011 2012 2013 2014

Mar

ket s

ize

($bn

)

1%

2%

3%

4%

Gro

wth

rate

(%)

Market Value Growth Rate

320

340

360

380

400

420

440

2009 2010 2011 2012 2013 2014

Mar

ket s

ize

($bn

)

1%

2%

3%

4%

Gro

wth

rate

(%)

Market Value Growth Rate

Year end December 31, 2009.

Source: Business Insights BUSINESS INSIGHTS

Value by geography Although Europe and the Americas represent the largest markets in the bakery and cereals industry by

value, Asia-Pacific will have the fastest growth rate, a CAGR of 6.6% during 2009–14. Growth in Asia-Pacific

will be driven by the following factors:

Rising disposable income and middle class expansion;

Increasing exposure to Western culture and dietary habits.

43

In particular, Asia-Pacific’s expanding middle class will create strong demand for premium/gourmet bakery

and cereals. The Middle East and Africa region will have the second highest growth rate, a CAGR of 4.8%,

to reach a market size of $21bn in 2014.

Table 6: Global bakery and cereals market shares, by geography ($bn), 2009–14

Region 2009 2010 2011 2012 2013 2014 CAGR

2009–14Europe 165.0 168.6 172.4 176.4 180.5 184.7 2.3%Americas 118.8 122.2 125.8 129.5 133.3 137.3 2.9%Asia-Pacific 58.0 61.9 66.0 70.3 75.0 80.0 6.6%Middle East and Africa 16.3 17.2 18.0 18.9 19.8 20.7 4.8%Total 358.1 369.9 382.2 395.1 408.6 422.8 3.4%

Source: Business Insights BUSINESS INSIGHTS

Market value by country The top 10 countries together accounted for 65.6% of the global bakery and cereals market value in 2009,

with the US being the largest market, worth $60bn. The US will continue to be the largest market for bakery

and cereals, growing at a CAGR of 2.9% during 2009–14.

44

Table 7: Top 10 bakery and cereals markets, by value ($bn), 2009–14

Country 2009 2010 2011 2012 2013 2014 CAGR

2009–14United States 59.7 61.4 63.1 65.0 66.9 69.0 2.9%China 23.1 25.4 27.9 30.8 33.9 37.3 10.1%Germany 31.5 32.0 32.5 33.1 33.6 34.1 1.6%Russia 27.3 28.3 29.4 30.5 31.8 33.1 3.9%Mexico 15.7 16.3 17.0 17.7 18.3 19.0 3.9%Brazil 20.2 20.8 21.4 22.0 22.6 23.2 2.8%Italy 16.8 17.1 17.4 17.7 18.0 18.3 1.7%United Kingdom 15.6 16.1 16.5 17.0 17.5 18.0 2.9%France 13.3 13.5 13.6 13.7 13.8 14.0 0.9%Japan 13.2 13.3 13.5 13.7 13.8 13.9 1.1%Rest of the world 121.7 125.7 129.8 134.1 138.5 142.9 3.3%Total 358.1 369.9 382.2 395.1 408.6 422.8 3.4%

Source: Business Insights BUSINESS INSIGHTS

China and Japan are the only two Asian countries that make it into the list of the top 10 bakery and cereals

markets. From a market value of $23bn in 2009, China will grow at a CAGR of 10.1% during 2009–14 (the

highest among all of the top 10 countries) to become the second most valuable national market with a value

of $37bn in 2014.

45

Figure 10: Top 10 bakery and cereal markets, by value ($bn), 2009–14

0

10

20

30

40

50

60

70

80

US

Ger

man

y

Rus

sia

Chi

na

Bra

zil

Italy

Mex

ico

UK

Fran

ce

Japa

n

Mar

ket s

ize

($bn

)

0%1%2%3%4%5%6%7%8%9%10%11%

CA

GR

(200

9–14

)

Year end December 2009.

2009 Additional value in 2014 CAGR 2009–14

0

10

20

30

40

50

60

70

80

US

Ger

man

y

Rus

sia

Chi

na

Bra

zil

Italy

Mex

ico

UK

Fran

ce

Japa

n

Mar

ket s

ize

($bn

)

0%1%2%3%4%5%6%7%8%9%10%11%

CA

GR

(200

9–14

)

Year end December 2009.

2009 Additional value in 2014 CAGR 2009–142009 Additional value in 2014 CAGR 2009–14

Source: Business Insights BUSINESS INSIGHTS

Market value by category Bakery and cereals comprises seven different categories: bread and rolls; cakes and pastries; cookies;

breakfast cereals; morning goods; crackers; and cereal bars. Bread and rolls is the largest category, $179bn

in 2009. The category is forecast to reach $201bn in 2014, growing at a CAGR of 2.3% through 2009–14,

with artisanal bread and rolls being the largest sub-category in value terms. Stated below are some of the

factors that will drive demand for bread and roles:

Increasing demand for handmade and fresh bread and rolls led by sophistication in consumer

preference in matured markets;

46

Shift away from traditional breakfasts in Asia-Pacific towards more bread-based breakfasts; and

Smaller households is driving demand for industrial bread and rolls in immature markets.

The cakes and pastries category was worth $65bn in 2009 and will outperform the overall industry growth

rate (with a CAGR of 5.2%, during 2009–14) to reach $84bn in 2014. Countries such as Japan will be one of

the major contributors to this growth, due to high consumption and acceptance of cakes in the region. Cereal

bars, many of which are positioned as healthy and/or convenient, will be the fastest growing category

growing at a CAGR of 5.3% during 2009–14 to reach a market value of $9bn.

Table 8: Global bakery and cereals market value, by category (%), 2009 and 2014

Category 2009 2010 2011 2012 2013 2014 CAGR

2009–14Bread & rolls 178.6 182.6 186.8 191.2 195.7 200.4 2.3%Cakes & pastries 64.9 68.1 71.6 75.4 79.4 83.7 5.2%Cookies 44.9 46.5 48.2 49.9 51.6 53.5 3.6%Breakfast cereals 28.5 29.7 31.0 32.3 33.6 35.0 4.2%Morning goods 17.4 18.0 18.6 19.2 19.9 20.6 3.4%Crackers 16.8 17.5 18.2 18.9 19.6 20.4 3.9%Cereal bars 7.01 7.42 7.83 8.25 8.66 9.08 5.3%Total 358.1 369.9 382.2 395.1 408.6 422.8 3.4%

Source: Business Insights BUSINESS INSIGHTS

47

Figure 11: Global bakery and cereals market value, by category (%), 2009 and 2014

49.9% 47.4%

18.1% 19.8%

12.5% 12.6%8.0% 8.3%4.9% 4.9%4.7% 4.8%2.0% 2.1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2009 2014

Mar

ket v

alue

by

cate

gory

200

9 &

201

4 (%

)

Bread & rolls Cakes & pastries Cookies Breakfast cereals

Morning goods Crackers Cereal bars

Year end is December 2009.

Note: Legend depicts categories from bottom to top

49.9% 47.4%

18.1% 19.8%

12.5% 12.6%8.0% 8.3%4.9% 4.9%4.7% 4.8%2.0% 2.1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2009 2014

Mar

ket v

alue

by

cate

gory

200

9 &

201

4 (%

)

Bread & rolls Cakes & pastries Cookies Breakfast cereals

Morning goods Crackers Cereal bars

Year end is December 2009.

Note: Legend depicts categories from bottom to top Source: Business Insights BUSINESS INSIGHTS

Value by sub-category Artisanal bread and rolls is the largest sub-category of the total bakery and cereals market. Worth $98bn in

2009, it is forecast to grow at a CAGR of 2.3% during 2009–14 to reach a value of $105bn. Some of the

main factors driving this sub-category are as follows:

Innovations in new flavors and ingredient combinations;

Locally sourced ingredients and a more ethical, sustainable and authentically artisanal

positioning;

48

Use of particularly nutritional ingredients, such as rye and spelt;

Awareness campaigns by government bodies such as the FDA on the benefits of whole grains.

In-store bread and rolls will see the highest level of growth within the bread and rolls category at a CAGR of

3.8%, to reach a market value of $21bn in 2014. Future demand will be mainly driven by higher consumption

by “grab and go” consumers. With a CAGR of 7.1% during the period 2009–14, artisanal cookies will see the

fastest growth within the bakery and cereals market and will be worth around $1.4bn in 2014. Sports and

energy bars will equal the growth of artisanal cookies and reach a market value of $4bn in 2014.

Increasingly, consumers are snacking on sports and energy bars to:

Get an energy enhancement;

Stave off hunger;

Get a healthier snack and help manage their weight; and

Feel healthier – where they are buying products with functional ingredients.

49

Table 9: Global bakery and cereals market value, by category and sub-category ($bn), 2009–14

Category/subcategory 2009 2010 2011 2012 2013 2014 CAGR

2009–14Bread & rolls 178.6 182.6 186.8 191.2 195.7 200.4 2.3%Artisanal bread & rolls 98.3 99.6 100.9 102.2 103.6 105.0 1.3%Industrial bread and rolls 62.8 64.9 67.1 69.4 71.9 74.4 3.5%In-store bakery 17.5 18.1 18.8 19.5 20.2 21.0 3.8%Cakes & pastries 64.9 68.1 71.6 75.4 79.4 83.7 5.2%Industrial cakes & pastries 30.0 31.7 33.6 35.7 37.9 40.4 6.2%Artisanal cakes & pastries 20.6 21.5 22.3 23.2 24.2 25.1 4.0%In-store bakery 14.3 15.0 15.7 16.5 17.3 18.2 5.0%Cookies 44.9 46.5 48.2 49.9 51.6 53.5 3.6%Plain cookies 7.5 7.9 8.3 8.7 9.1 9.6 4.9%Butter-based cookies 7.3 7.6 7.9 8.3 8.6 9.0 4.3%Chocolate cookies 7.6 7.8 7.9 8.1 8.3 8.4 2.0%Cream filled 5.4 5.6 5.8 6.0 6.2 6.4 3.3%American cookies 4.7 4.9 5.0 5.2 5.4 5.6 3.4%Wafer biscuits 4.5 4.6 4.7 4.9 5.0 5.1 2.7%Assortments 3.4 3.5 3.6 3.8 3.9 4.0 2.9%Other cookies 3.2 3.3 3.4 3.5 3.6 3.7 3.3%Artisanal cookies 1.0 1.1 1.1 1.2 1.3 1.4 7.1%In-store bakery 0.2 0.2 0.3 0.3 0.3 0.3 4.2%Breakfast cereals 28.5 29.7 31.0 32.3 33.6 35.0 4.2%Ready-to-eat cereals 24.9 26.0 27.1 28.2 29.4 30.7 4.3%Hot cereals 3.6 3.7 3.9 4.0 4.2 4.3 3.8%Morning goods 17.4 18.0 18.6 19.2 19.9 20.6 3.4%Industrial morning goods 8.6 8.9 9.3 9.7 10.0 10.5 4.1%Artisanal morning goods 4.8 4.9 5.1 5.3 5.5 5.7 3.6%In-store bakery 4.1 4.1 4.2 4.3 4.4 4.4 1.7%

50

Category/subcategory 2009 2010 2011 2012 2013 2014 CAGR 2009–14

Crackers 16.8 17.5 18.2 18.9 19.6 20.4 3.9%Plain crackers 6.5 6.7 7.0 7.2 7.5 7.8 3.8%Cheese-flavored crackers 5.1 5.3 5.5 5.7 6.0 6.2 4.1%Bread substitutes 2.8 2.9 3.0 3.1 3.2 3.3 3.7%Other crackers 2.5 2.6 2.7 2.8 2.9 3.1 4.2%Cereal bars 7.0 7.4 7.8 8.2 8.7 9.1 5.3%Sports and energy bars 2.5 2.6 2.8 3.1 3.3 3.5 7.1%Other bars 2.5 2.7 2.9 3.0 3.2 3.3 5.5%Granola/muesli bars 2.0 2.1 2.1 2.2 2.2 2.3 2.6%Total 358.1 369.9 382.2 395.1 408.6 422.8 3.4%

Source: Business Insights BUSINESS INSIGHTS

51

Figure 12: Growth in top 10 bakery and cereals sub-categories, CAGR (%) 2009–14

1.3%

3.5%

6.2%

5%

4.1%

2%

4%

4.3%

3.8%

4.9%

0 10 20 30 40 50 60 70 80 90 100

Artisanal bread and rolls

Industrial bread and rolls

Industrial cakes and pastries

Ready-to- eat cereals

Artisanal cakes and pastries

In-store bakery bread and rolls

In-store bakery cakes and pastries

Industrial morning goods

Chocolate cookies

Plain cookies

Market size 2009 ($bn)

0% 1% 2% 3% 4% 5% 6% 7%

CAGR 2009–14 (%)

2009 CAGR 2009–14

Year end December 31, 2009.

1.3%

3.5%

6.2%

5%

4.1%

2%

4%

4.3%

3.8%

4.9%

0 10 20 30 40 50 60 70 80 90 100

Artisanal bread and rolls

Industrial bread and rolls

Industrial cakes and pastries

Ready-to- eat cereals

Artisanal cakes and pastries

In-store bakery bread and rolls

In-store bakery cakes and pastries

Industrial morning goods

Chocolate cookies

Plain cookies

Market size 2009 ($bn)

0% 1% 2% 3% 4% 5% 6% 7%

CAGR 2009–14 (%)

2009 CAGR 2009–14

1.3%

3.5%

6.2%

5%

4.1%

2%

4%

4.3%

3.8%

4.9%

0 10 20 30 40 50 60 70 80 90 100

Artisanal bread and rolls

Industrial bread and rolls

Industrial cakes and pastries

Ready-to- eat cereals

Artisanal cakes and pastries

In-store bakery bread and rolls

In-store bakery cakes and pastries

Industrial morning goods

Chocolate cookies

Plain cookies

Market size 2009 ($bn)

0% 1% 2% 3% 4% 5% 6% 7%

CAGR 2009–14 (%)

2009 CAGR 2009–142009 CAGR 2009–14

Year end December 31, 2009.

Source: Business Insights BUSINESS INSIGHTS

52

The bakery and cereals market in Europe Bread and rolls is the largest category in Europe, with artisanal bread and rolls accounting for the biggest

share within this category. Worth $59bn in 2009, artisanal bread and rolls are forecasted to grow at just 0.6%

CAGR in Europe, to reach $61bn in 2014. Cereal bars consumption in Europe, will have the highest growth

rate of all categories, at a CAGR of 6.9%, to reach a market value of $3.1bn in 2014, up from $2.2bn in

2009. This growth will be powered by consumers switching to healthier and convenient products.

Table 10: European bakery and cereals market value ($bn), by category and sub-category, 2009–14

Category/subcategory 2009 2010 2011 2012 2013 2014 CAGR

2009–14Bread & rolls 105.9 107.7 109.6 111.5 113.6 115.8 1.8%Artisanal bread & rolls 58.9 59.2 59.6 59.9 60.3 60.8 0.6%Industrial bread and rolls 37.3 38.4 39.6 40.8 42.1 43.5 3.1%In-store bakery 9.7 10.0 10.4 10.8 11.2 11.6 3.5%Cookies 19.5 20.1 20.7 21.4 22.0 22.7 3.1%Butter-based cookies 3.8 4.0 4.2 4.3 4.5 4.7 4.0%Chocolate cookies 4.3 4.3 4.4 4.4 4.5 4.6 1.4%Cream filled 2.4 2.5 2.6 2.7 2.8 2.9 3.3%Plain cookies 2.2 2.3 2.4 2.4 2.5 2.6 3.4%Wafer biscuits 1.6 1.7 1.8 1.9 1.9 2.0 4.3%Assortments 1.7 1.8 1.8 1.9 1.9 1.9 2.2%American cookies 1.5 1.6 1.6 1.7 1.8 1.9 4.4%Other cookies 1.3 1.4 1.4 1.4 1.5 1.5 2.8%Artisanal cookies 0.4 0.4 0.4 0.4 0.4 0.4 4.1%In-store bakery 0.1 0.2 0.2 0.2 0.2 0.2 5.1%Cakes & pastries 17.5 18.0 18.5 19.0 19.4 20.0 2.7%Industrial cakes & pastries

7.9 8.1 8.3 8.6 8.8 9.0 2.7%

Artisanal cakes & pastries 7.1 7.2 7.4 7.5 7.7 7.9 2.2%In-store bakery 2.6 2.7 2.8 2.9 3.0 3.1 3.6%

53

Category/subcategory 2009 2010 2011 2012 2013 2014 CAGR 2009–14

Breakfast cereals 8.6 8.9 9.2 9.5 9.9 10.2 3.4%Ready-to-eat cereals 7.6 7.8 8.1 8.4 8.6 8.9 3.4%Hot cereals 1.1 1.1 1.1 1.2 1.2 1.3 3.6%Morning goods 6.8 7.0 7.2 7.3 7.5 7.7 2.5%Industrial morning goods 3.0 3.1 3.2 3.3 3.4 3.5 2.9%Artisanal morning goods 2.9 2.9 3.0 3.1 3.1 3.2 2.1%In-store bakery 0.9 0.9 1.0 1.0 1.0 1.0 2.5%Crackers 4.4 4.5 4.7 4.8 5.0 5.2 3.4%Plain crackers 1.8 1.9 1.9 2.0 2.0 2.1 2.9%Cheese-flavored crackers 1.2 1.3 1.3 1.4 1.4 1.5 3.8%Other crackers 0.7 0.8 0.8 0.8 0.8 0.9 3.0%Bread substitutes 0.6 0.6 0.6 0.7 0.7 0.7 4.4%Cereal bars 2.29 2.46 2.64 2.82 3.01 3.19 6.9%Sports and energy bars 0.94 1.03 1.12 1.21 1.3 1.39 8.1%Other bars 0.85 0.93 1.01 1.08 1.16 1.24 7.8%Granola/muesli bars 0.49 0.51 0.52 0.53 0.54 0.56 2.7%Total 165.0 168.6 172.4 176.4 180.5 184.7 2.3%

Source: Business Insights BUSINESS INSIGHTS

The bakery and cereals market in the Americas As in Europe, bread and rolls is the largest category in the Americas, with a market value of $47bn in 2009.

Sales of bread and rolls will reach $52bn in 2014, a CAGR of 2.1% over the five year period. Although a

mature and highly saturated market, growth in artisanal bread and rolls category will still be almost three

times the rate of that in Europe.

54

Sales of morning goods will rise from $10bn in 2009 to $12bn in 2014, growing at a CAGR of 3.8% during

2009–14. Artisanal morning goods will have the highest growth within this category, recording a CAGR of

5.8% during 2009–14 to reach a market value of $2bn.

Breakfast cereals and cereal bars will be the two fastest growing categories in the Americas, with a forecast

CAGR of 4.3% over 2009–14. Sales of healthier products have been supported by the launch of products

with higher fruit or nut contents. Sports and energy cereal bars will be the fastest growing sub-category in the

Americas, with a CAGR of 6.4% during 2009–14, to reach $1.5bn.

Table 11: Americas bakery and cereals market value ($bn), by category and sub-category, 2009–14

Category/subcategory 2009 2010 2011 2012 2013 2014 CAGR

2009–14Bread & rolls 46.6 47.6 48.6 49.6 50.7 51.8 2.1%Artisanal bread & rolls 28.4 28.8 29.2 29.6 30.0 30.4 1.4%Industrial bread and rolls 14.4 14.8 15.2 15.7 16.2 16.8 3.1%In-store bakery 3.8 4.0 4.1 4.3 4.5 4.6 3.9%Cakes & pastries 18.2 18.8 19.5 20.2 20.8 21.6 3.4%Industrial cakes & pastries

9.4 9.7 10.0 10.4 10.7 11.1 3.4%

In-store bakery 6.5 6.6 6.8 7.0 7.2 7.5 2.9%Artisanal cakes & pastries 2.4 2.5 2.6 2.8 2.9 3.0 4.6%Breakfast cereals 16.6 17.3 18.1 18.9 19.7 20.5 4.3%Ready-to-eat cereals 14.7 15.3 16.0 16.7 17.5 18.2 4.5%Hot cereals 2.0 2.0 2.1 2.1 2.2 2.3 3.1%

55

Category/subcategory 2009 2010 2011 2012 2013 2014 CAGR 2009–14