backoffice.phillipcapital.inbackoffice.phillipcapital.in/backoffice/researchfiles/pc_-_fmcg_sec… ·...

TRANSCRIPT

India Consumer Exuberant Valuations, languid pricing and volume growth‐ A recipe for de‐rating 8 May 2013

PhillipCapital (India) Pvt. Ltd.

We rate the Indian FMCG sector Sell as we believe the sector is entering a phase of protracted period of slowdown in volume growth accompanied by sluggish price growth on account of rising competitive intensity. The decline in certain commodity prices will help in gross margin improvement but the slower‐than‐expected volume and pricing growth will offset the benefits of benign input costs. The rising competitive activity will lead to increase in advertising and promotional expenses limiting the benefits of gross margin expansion to EBIDTA margins. Considering the rich sector valuations at 32x FY14E earnings, aggressive consensus estimates and sluggish operating environment, we believe the sector de‐rating is imminent over the medium term. Notwithstanding our Sell rating on the sector we find certain volume plays like Dabur, Emami and Bajaj Corp attractive. Our key reasons are as follows: The return of Pricing pressure and rise in competitive intensity in a challenging operating environment: The correction in certain commodities and sluggish economic environment has led to a significant increase in promotion activity and pricing actions. According to our distributor survey across India, the trading environment continues to remain challenging and no respite is seen in the near term. We believe the promotional activities will persist in the medium term and the sector is likely to witness a slower pricing growth while the sluggish consumption environment could mean lower‐than‐expected volume off‐take. Thus, the sector could surprise negatively on both volume and price growth which could significantly offset the strong earnings growth trend of the past 3 years. Election year but very little to cheer for the consumer companies: It is generally believed that during an election year consumer spending increases because of the cash spending by the contesting political parties and the ruling government’s endeavors by populist programs. While the election year phenomenon is intuitively appealing but we find little impact on the listed FMCG companies. We have statistically analysed the data for 5 election years over the last 20 years and have not found the financial or stock performances of the FMCG sector to be significantly different than the mean. Apart from statistical analysis it is important to note that election spending is largely bunched closer to the election date and the election spending on Below Poverty Line does not significantly help the FMCG companies. Prefer niche plays with higher sensitivity to advertising spends; Large cap stocks likely to languish for protracted periods: We generally hold a negative view on the large capitalization stocks as macroeconomic headwinds will significantly impact them. We rate Dabur, Emami and Bajaj Corp as our top sector picks as they have higher advertising spends to volume growth sensitivity as compared to the sector.

Companies Covered

ITC (Sell) CMP Rs 331Target Price Rs 290

Hindustan Unilever (Sell) CMP Rs 572Target Price Rs 507

Nestle India (Neutral) CMP Rs 4910Target Price Rs 4400

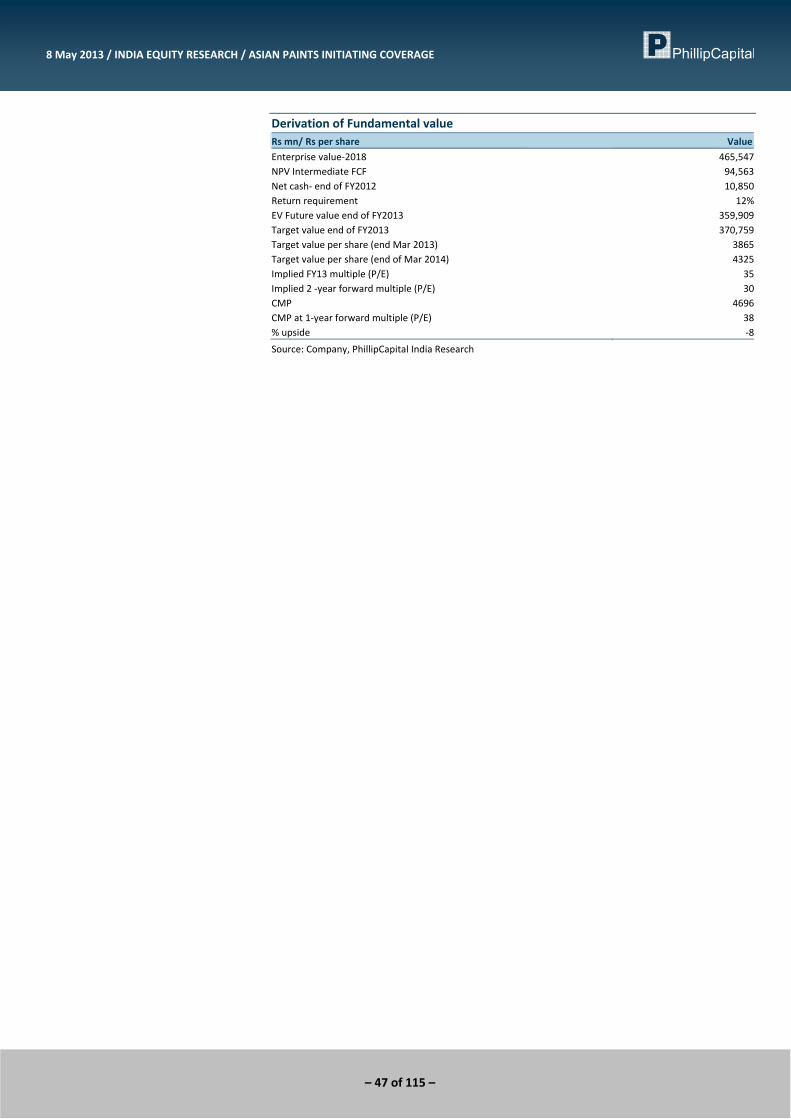

Asian Paints (Neutral) CMP Rs 4696Target Price Rs 4300

GCPL (Sell) CMP Rs 844Target Price Rs 740

Dabur (Buy) CMP Rs 160Target Price Rs 170

Colgate (Sell) CMP Rs 1509Target Price Rs 1250

GSK Consumer (Sell) CMP Rs 4067Target Price Rs 3700

Marico (Sell) CMP Rs 217Target Price Rs 190

Emami (Buy) CMP Rs 660Target Price Rs 760

Britannia (Buy) CMP Rs 574Target Price Rs 635

Bajaj Corp (Buy) CMP Rs 253Target Price Rs 335

Zydus Wellness (Buy) CMP Rs 447Target Price Rs 535

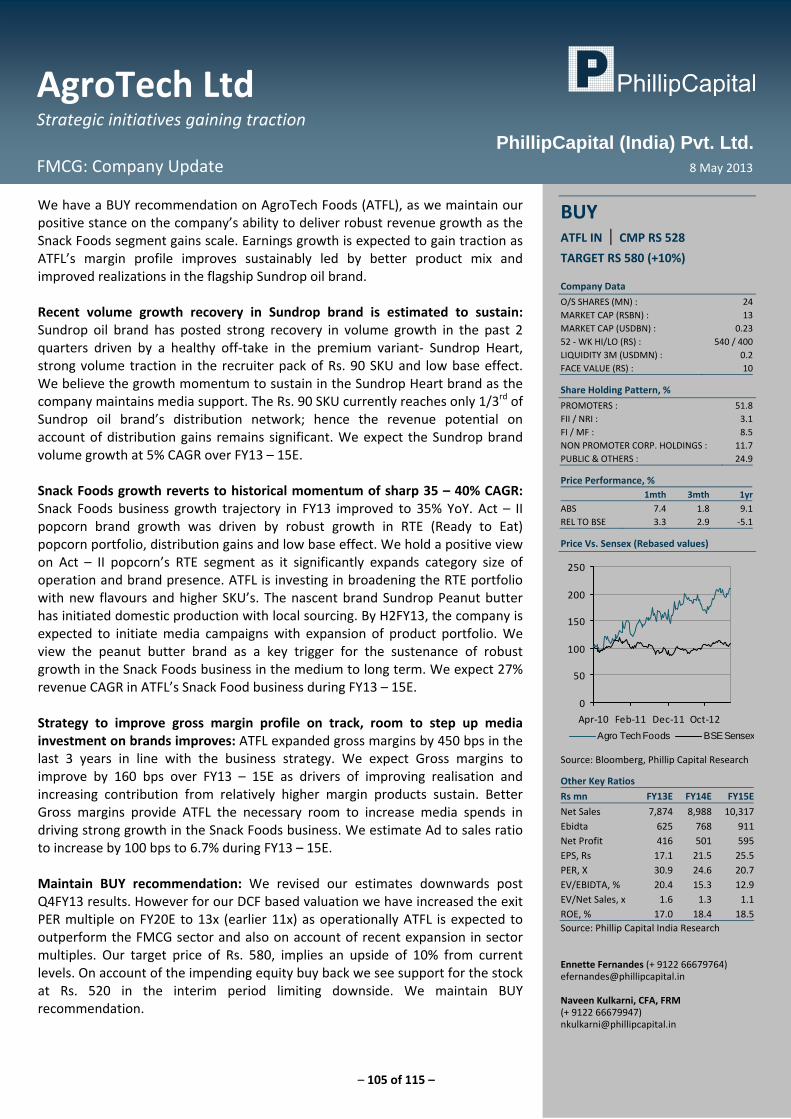

Agrotech Foods (Buy) CMP Rs 528Target Price Rs 580 Report priced as of 3rd May 2013 Naveen Kulkarni, CFA, FRM (+ 9122 66679947) [email protected] Ennette Fernandes (+ 9122 66679764) [email protected]

– 2 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / FMCG SECTOR UPDATE

Table of Contents Return of the pricing pressure; Competitive activity rising ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 3

Channel checks and Distributor survey corroborate volume growth and pricing pressure ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 7

Distributor Survey portends to tepid demand scenario ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 13

Election year but very little to cheer about for the consumer companies ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 14

Statistical analysis of election impact ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 18

Limited positive impact of input cost inflation‐ Too little to cheer…………………………… 19

Consensus estimates continue to remain aggressive and disappointments to consensus will lead to a de‐rating ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 20

Companies Section ITC ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 25

Hindustan Unilever ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 34

Nestle India ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 39

Asian Paints ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 44

Godrej Consumer Products Limited ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 50

Dabur India ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 55

Colgate Palmolive India ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 60

GlaxoSmithKline Consumer ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 65

Marico Industrires ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 70

Emami ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 75

Britannia Industries Ltd ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 87

Bajaj Corp ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 92

Zydus Wellness ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 98

AgroTech Foods∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 105

Appendix ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 110

– 3 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / FMCG SECTOR UPDATE

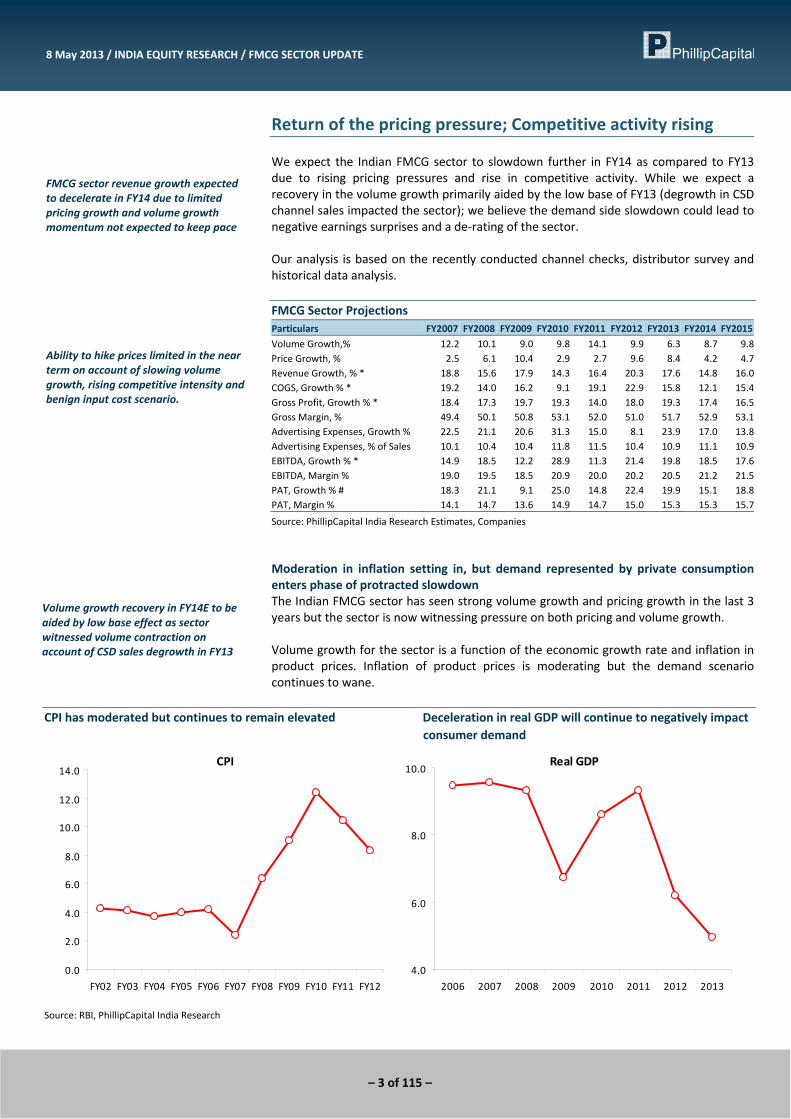

Return of the pricing pressure; Competitive activity rising We expect the Indian FMCG sector to slowdown further in FY14 as compared to FY13 due to rising pricing pressures and rise in competitive activity. While we expect a recovery in the volume growth primarily aided by the low base of FY13 (degrowth in CSD channel sales impacted the sector); we believe the demand side slowdown could lead to negative earnings surprises and a de‐rating of the sector. Our analysis is based on the recently conducted channel checks, distributor survey and historical data analysis. FMCG Sector Projections Particulars FY2007 FY2008 FY2009 FY2010 FY2011 FY2012 FY2013 FY2014 FY2015

Volume Growth,% 12.2 10.1 9.0 9.8 14.1 9.9 6.3 8.7 9.8Price Growth, % 2.5 6.1 10.4 2.9 2.7 9.6 8.4 4.2 4.7Revenue Growth, % * 18.8 15.6 17.9 14.3 16.4 20.3 17.6 14.8 16.0COGS, Growth % * 19.2 14.0 16.2 9.1 19.1 22.9 15.8 12.1 15.4Gross Profit, Growth % * 18.4 17.3 19.7 19.3 14.0 18.0 19.3 17.4 16.5Gross Margin, % 49.4 50.1 50.8 53.1 52.0 51.0 51.7 52.9 53.1Advertising Expenses, Growth % 22.5 21.1 20.6 31.3 15.0 8.1 23.9 17.0 13.8Advertising Expenses, % of Sales 10.1 10.4 10.4 11.8 11.5 10.4 10.9 11.1 10.9EBITDA, Growth % * 14.9 18.5 12.2 28.9 11.3 21.4 19.8 18.5 17.6EBITDA, Margin % 19.0 19.5 18.5 20.9 20.0 20.2 20.5 21.2 21.5PAT, Growth % # 18.3 21.1 9.1 25.0 14.8 22.4 19.9 15.1 18.8PAT, Margin % 14.1 14.7 13.6 14.9 14.7 15.0 15.3 15.3 15.7

Source: PhillipCapital India Research Estimates, Companies

Moderation in inflation setting in, but demand represented by private consumption enters phase of protracted slowdown The Indian FMCG sector has seen strong volume growth and pricing growth in the last 3 years but the sector is now witnessing pressure on both pricing and volume growth. Volume growth for the sector is a function of the economic growth rate and inflation in product prices. Inflation of product prices is moderating but the demand scenario continues to wane.

CPI has moderated but continues to remain elevated Deceleration in real GDP will continue to negatively impact consumer demand

CPI

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12

Real GDP

4.0

6.0

8.0

10.0

2006 2007 2008 2009 2010 2011 2012 2013

Source: RBI, PhillipCapital India Research

FMCG sector revenue growth expected to decelerate in FY14 due to limited pricing growth and volume growth momentum not expected to keep pace

Volume growth recovery in FY14E to be aided by low base effect as sector witnessed volume contraction on account of CSD sales degrowth in FY13

Ability to hike prices limited in the near term on account of slowing volume growth, rising competitive intensity and benign input cost scenario.

– 4 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / FMCG SECTOR UPDATE

The sector volume growth had peaked in FY11 aided by strong consumption growth of 8.6% YoY. In FY12 also the FMCG sector continued the trend of high value growth as consumption trends continued to be strong but volume growth started waning on rising product prices driven by inflationary pressures in input costs. In FY13 the consumption growth has shown a marked slowdown and the chances of a significant pick‐up in the consumption trend over the medium term appear remote. Consumption growth (%)

(4.0)

(2.0)

‐

2.0

4.0

6.0

8.0

10.0

1952

1957

1962

1967

1972

1977

1982

1987

1992

1997

2002

2007

2012

Source: PhillipCapital India Research

According to our economist Anjali Verma, consumption growth could marginally pick‐up on account of low base and election spending but the overall consumption growth is likely to remain uninspiring. Estimated FMCG sector volume growth bounce back in FY14E is aggressive, can surprise negatively Sequential recovery in sector volume growth is aggressive

0

4

8

12

16

Q1FY09

Q2FY09

Q3FY09

Q4FY09

Q1FY10

Q2FY10

Q3FY10

Q4FY10

Q1FY11

Q2FY11

Q3FY11

Q4FY11

Q1FY12

Q2FY12

Q3FY12

Q4FY12

Q1FY13

Q2FY13

Q3FY13

Q4FY13

Sector price Growth %Volume growth YoY (%)

Source: PhillipCapital India Research, Companies

Volume growth being a function of economic growth and inflation is expected to remain under pressure as macro ‐ economic slowdown and high consumer price inflation persists.

Consumption growth rate a representative of demand has slowed down considerably. Marked improvement in the medium term is remote.

Marginal improvement in Consumption expected in the near term on account of low base effect and elections.

Sequential recovery of sector volume growth is aggressive. Initial results in Q4FY13 signify volume growth has been below expectations.

Pricing growth in Q4FY13 on the basis of results of FMCG companies reported till date indicates higher than expected pricing pressure. Sector pricing growth is to be lower than expectations in Q4FY13.

FMCG sector has been witnessing protracted slowdown since Q1FY13 with significant slowdown in Q3FY13

– 5 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / FMCG SECTOR UPDATE

Volume growth in FY14E estimated to be supported by low base effect, but quantum can surprise negatively

0

2

4

6

8

10

12

14

16

FY2007 FY2008 FY2009 FY2010 FY2011 FY2012 FY2013 FY2014 FY2015

Price Growth YoY %Volume growth YoY (%)

Source: PhillipCapital India Research, Companies

Slower consumption growth has a disproportional impact on various sectors and traditionally FMCG staples and Utility sectors tend to slowdown relatively lesser compared to consumer discretionary like autos and white goods. However FMCG staples and utilities too do underperform in a cyclical slowdown. We note that the Indian FMCG sector is showing strong signs of a protracted period of slowdown since Q1FY13. The sector saw a significant slowdown in Q3FY13 and our expectations of a bounce‐back in Q4FY13 continue to be aggressive. Our expectations of a bounce back in volume growth in Q4FY13E and FY14E are aggressive and the sector could surprise negatively on volume growth as our channel checks indicate that the market continues to remain sluggish and channel inventory levels are high for some of the FMCG companies. Soft input costs, waning consumer demand is driving step up in competitive activity The demand scenario is now waning on account of slowing GDP growth while correction in raw material prices has led to increase in competitive activity. The increase in competitive activity will translate to tepid price growth which could be further compounded by a rise advertising expenses. Ad to sales ratio expected to increase on a YoY basis, Ad spend growth to remain elevated

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

FY2007 FY2008 FY2009 FY2010 FY2011 FY2012 FY2013 FY2014 FY2015

volume growth YoY (%)

Advertising growth YoY (%)

Source: PhillipCapital India Research, Companies

In a phase of cyclical slowdown, FMCG staples sector is the last to be negatively impacted but nevertheless tends to underperform.

Expectations of bounce back in volume growth in the forthcoming quarters due to step up in promotional and brand investments by companies remains fairly stretched as macroeconomic slowdown concerns persist.

Channel checks indicate that real buyer in the market is limited, leading to sluggishness in the market and higher channel inventory. Hence estimates of robust recovery in volume growth in FY14 can surprise negatively.

FMCG companies not in a position to realize benefits of soft input inflation in FY14E as they are expected to channelize savings into promotional offers and higher brand investments to boost flagging volume growth.

– 6 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / FMCG SECTOR UPDATE

Correction in input costs generally tends to increase competitive pressures as market participation from smaller players increases significantly. This generally translates to increase in promotional activity and advertisement expenses for the FMCG companies. We have observed that sector advertising expenses generally increase significantly when input costs soften. We have observed this in FY10 when commodity prices crashed and FMCG companies significantly stepped up their spending. While we expect the FMCG companies to step‐up advertising and promotional spending, we do not expect the spending to be accompanied by a sharp rise in volume growth as the macroeconomic environment continues to remain sluggish.

Competitive intensity has increased in the sector since the past 2 quarters, as companies chase consumers in an environment of slowing consumer demand.

Sector advertising and promotional spend growth is expected to remain elevated in FY14E. However high Ad spends is not expected to translate to robust volume growth on account of sluggish macroeconomic factors.

– 7 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / FMCG SECTOR UPDATE

Channel checks and Distributor survey corroborate volume growth and pricing pressure According to our recently conducted channel checks we observed that the competitive activity is rising but we still have not entered a phase of hyper competition. We note that companies have reacted to correction in raw material prices by initiating promotional offers and price cuts as premium of some branded products had become unsustainable. While competitive activity is rising we believe it is far from reaching hypercompetitive levels. Competitive activity in personal care products, soaps and premium detergents is rising significantly. We believe FY14 price growth for the sector is likely to remain muted. We have noted a flurry of consumer offers. Toilet Soaps category is witnessing the highest promotional activity Competitive activity in soaps has increased significantly as Palm oil prices have come down significantly. The benefits of input cost will be significant but rising competitive activity will translate to limited benefits for the market leaders.

Promotions on Toilet soap is largely broad – based across brands. Smaller regional brands too are competitively active

Channel checks indicate that competitive activity has increased with companies initiating pricing discounts or promotional offers across categories.

Pricing discount relatively higher and broad based in Toilet Soaps category as incumbents pass on input cost savings in Palm oil to consumers. Pricing activity is also being met by smaller regional players.

– 8 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / FMCG SECTOR UPDATE

Promotions on Soaps are a mix of free grammage or pricing offers Brand Company Category SKU (gm) MRP Offer Pricing discount (%)

Lifebuoy Hindustan Unilever Personal Wash 60+10 10 10 gm free ‐14.3Lux Hindustan Unilever Personal Wash 55+10 10 10 gm free ‐15.4Lux Hindustan Unilever Personal Wash 4*(50+5) 40 Rs. 2 off+ 20 gm free ‐14.1Lux Hindustan Unilever Personal Wash 4*100 80 Rs. 10 off ‐12.5 Pears Germshield Hindustan Unilever Personal Wash 75 32 Rs. 5 off ‐15.6Pears Pure & Gentle Hindustan Unilever Personal Wash 75 32 Rs. 5 off ‐15.6Pears Pure & Gentle Hindustan Unilever Personal Wash 175 Rs. 7 off Pears Pure & Gentle Hindustan Unilever Personal Wash 3*125 145 Rs. 10 off ‐6.9Dove Hindustan Unilever Personal Wash 75 42 Rs. 5 off ‐11.9Dove Hindustan Unilever Personal Wash 3*100 138 Rs. 10 off ‐7.2Dettol Reckitt Benckiser Personal Wash 3*125 105 Rs. 12 off ‐11.4Dettol Reckitt Benckiser Personal Wash 4*75 88 Rs. 9 off ‐10.2Dettol Cool Reckitt Benckiser Personal Wash 3*75 69 Rs. 2 off ‐2.9Dettol Skin Care Reckitt Benckiser Personal Wash 3*75 50 Rs. 7 off ‐12.3Santoor Wipro Personal Wash 4*50 44 Rs. 4 off ‐9.1 Fair Glow Godrej Consumer Personal Wash 4*75 80 Rs. 20 off ‐25.0Margo Jyothy Lab Personal Wash 2*100 44 Rs. 4 off ‐9.1Pihu Personal Wash 4*75 48 Rs. 8 off ‐16.7

Source: PhillipCapital India Research, Companies

Deceleration of demand in the discretionary Personal care category has led to step up of promotions primarily by market leaders In personal care the market continues to be very competitive and in certain cases like the Shampoos category hypercompetitive activity cannot be ruled out. Competition is back in the sachets with all the major incumbents carrying free grammage offers.

Competition intensity is back in the shampoo sachet format, with free grammage offer

Free grammage offers in Shampoo sachets similar to CY2011 wherein pricing war in Shampoo category was intense. Promotional offers being extended to limited bottled SKU’s currently

– 9 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / FMCG SECTOR UPDATE

Promotional offers by way of free grammage in sachets and free products with bottled SKU’s make a comeback Brand Company Category SKU (gm) MRP Offer Pricing discount (%)

Dove Hindustan Unilever Shampoo 6.5+1.5 3 20% free ‐18.8Sunsilk Hindustan Unilever Shampoo 5+1 1 20% free ‐16.7Sunsilk Hindustan Unilever Shampoo 180+40 110 Rs. 56 worth conditioner free ‐33.7Head & Shoulders Procter & Gamble Shampoo 6.5+1 3 15% free ‐13.3Pantene Procter & Gamble Shampoo 6.5+1 3 15% free ‐13.3Vatika Dabur Shampoo 5+1 1 20% free ‐16.7Garnier Fructis L'oreal Shampoo 6.5+1.5 3 20% free ‐18.8Garnier Fructis 2 in 1 L'oreal Shampoo 180 + 90 189 Rs. 69 worth conditioner free ‐36.5Garnier Fructis Fall fight L'oreal Shampoo 375+180 340 Rs. 130 worth conditioner free ‐38.2Pantene Pro ‐ V Procter & Gamble Shampoo 340+75 273 Rs. 59 worth conditioner free ‐21.6

Source: PhillipCapital India Research, Companies

Oral care category market leader Colgate India gets aggressive with promotional offers in Toothpaste and Toothbrush segment Promotional activity has visibly increased in the Oral care category. Volume growth rates have slipped to single digits in the category in Q3FY13. Promotions are being carried in both the retail and modern trade channel in a bid to revive volume growth. Market leader Colgate India is currently leading the quantum of promotional offers in both the toothpaste and the toothbrush category.

Colgate carrying extensive promotional offers in Toothpaste and Toothbrush segment in a bid to recover volume growth and maintain market share. Promotional offers present in both the mass and premium end of the category.

– 10 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / FMCG SECTOR UPDATE

Step up in pricing discounts led by market leader Colgate observed in channels. Colgate has also initiated pricing discount in Active Salt post the launch of Babool Salt by Dabur Brand Company Category SKU (gm) MRP Offer Pricing discount (%)

Pepsodent 2 in 1 Hindustan Unilever Toothpaste 2*150 140 Rs. 17 off ‐12.1Close Up Hindustan Unilever Toothpaste 2*150 144 Rs. 17 off ‐11.8Colgate Strong Teeth Colgate Toothpaste 200+100+toothbrush 125 Rs. 16 off ‐12.8Colgate Max Fresh Colgate Toothpaste 80+20 42 20 gm free ‐20.0Colgate Cibaca Colgate Toothpaste 200 38 Rs. 3 off ‐7.9Colgate Total Colgate Toothpaste 2*150 Rs. 21 off Colgate Salt Colgate Toothpaste 100+20 42 20% free ‐16.7 Babool Dabur Toothpaste 400+2 toothbrush 68 Meswak Dabur Toothpaste 100 38 toothbrush worth Rs. 15 free ‐28.3

Source: PhillipCapital India Research, Companies

Largely observed promotional offers on toothbrush by Colgate in the Modern Trade channel Brand Company Category SKU MRP Offer Pricing discount (%)

Colgate 360 Total Surround Colgate Toothbrush 2 piece 150 buy 2 get 1 free ‐33.3Colgate 360 Total Surround Colgate Toothbrush 1 piece 75 Rs. 10 off ‐20.0Colgate 360 Actiflex Colgate Toothbrush 2 piece 138 buy 2 get 1 free ‐33.3Colgate 360 Whole mouth clean Colgate Toothbrush 2 piece 110 buy 2 get 1 free ‐33.3Colgate Sensitive Pro Relief Colgate Toothbrush 2 piece 138 buy 2 get 1 free ‐33.3Colgate Sensitive Colgate Toothbrush 2 piece 80 Rs. 15 off ‐18.8

Source: PhillipCapital India Research, Companies

Premium detergents, key volume drivers of the category, are witnessing increase in promotional activities Lab prices have not corrected materially but we have observed that companies have been offering consumers discounts in the premium detergents. Premium detergents have been key volume growth drivers; hence with increasing pressure on volumes, we observe that main incumbents HUL and Procter & Gamble have stepped up promotions on premium brands Surf Excel and Ariel respectively. P&G and HUL are also offering discounts on the higher grammage SKU of their mass brands Tide and Rin respectively.

Competitive intensity has increased as key input prices have softened; hence volume growth in branded detergents has come under pressure.

Pricing offers initiated in premium brands which have been key volume drivers. Offers also been extended to high grammage SKU of mass brands.

– 11 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / FMCG SECTOR UPDATE

Pricing offers on premium detergent brands prevalent. Price offers also initiated on high grammage SKU’s of mass brands Rin and Tide Brand Company Category SKU (gm) MRP Offer Pricing discount (%)

Surf Excel Top load Hindustan Unilever Detergent 1000 207 Rs. 22 off ‐10.6Surf Excel Front Load Hindustan Unilever Detergent 1000 227 Rs. 32 off ‐14.1Surf Excel Front Load Hindustan Unilever Detergent 2000 447 Rs. 64 off ‐14.3Surf Excel Quickwash Hindustan Unilever Detergent 2000 339 Rs. 54 off ‐15.9Surf Excel Quickwash Hindustan Unilever Detergent 1000 Rs. 27 woth Lifebuoy Clini care free Ariel Complete Front & Top Load Procter & Gamble Detergent 1000 216 Rs. 31 off ‐14.4Ariel Complete Procter & Gamble Detergent 1000 Free pearl pet worth Rs. 85 Ariel Complete Procter & Gamble Detergent 500 89 5 Pantene sachets free ‐14.4Tide Plus Procter & Gamble Detergent 500 45 Rs. 5 off ‐11.1Tide Plus Procter & Gamble Detergent 4000 359 Rs. 61 off ‐16.7Tide Plus Procter & Gamble Detergent 6000 552 Rs. 40 off ‐7.2Tide Plus Jasmine & Rose Procter & Gamble Detergent 4000 368 Rs. 27 off ‐7.3Rin Hindustan Unilever Detergent 6000 444 Rs. 30 off ‐6.8

Source: PhillipCapital India Research, Companies

– 12 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / FMCG SECTOR UPDATE

Modern Trade carrying promotions on specific categories that are competitively intense and on high grammage SKU’s We observed that the scale of promotional offers were higher in the Modern Trade channels. Also promotional offers were directed to higher grammage SKU’s in certain categories. Modern Trade is the key channel for higher grammage SKU’s and healthy volume offtake in higher grammage SKU’s contributes materially to overall volume growth for companies inspite of lower contribution of Modern Trade to sales. We observed that in the intensely competitive segment of deodorants, modern trade channels were offering high pricing discounts particularly in the brand Nivea. Modern retail channels are also carrying promotional offers on higher grammage SKU’s of the Parle – G brand. Volume growth in the Glucose category has decelerated sharply in the recent few years on account of change in consumer preference. Hence we believe that pricing actions in glucose segment are directed to drive recovery in volume growth.

Scale of promotions higher in Modern Trade channels. Several promotions visible in high grammage SKU’s for which Modern Trade is the key point of sale.

Pricing promotions visible in the intensely competitive deodorant category in Modern Trade.

Promotions observed in the high grammage SKU’s of the Glucose category which has been under pressure.

– 13 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / FMCG SECTOR UPDATE

Distributor Survey portends to tepid demand scenario We surveyed 30 distributors of the leading consumer companies across the country and noted similar responses by them. The following are the key responses: Deceleration in consumer demand continues in Q4FY13: Distributors indicated that demand scenario has continued to deteriorate Q4FY13. The volume growth rate has largely been similar on a sequential basis. Consumer demand is not expected to improve in the near term: The muted demand scenario is likely to persist for some more time and distributors do not expect any immediate recovery in demand. Sluggishness more pronounced in the discretionary categories: Demand in the discretionary category primarily Personal Care continues to be significantly weak and some distributors indicated that channel seems to be clogged with increase in inventory days in Q4FY13. Demand in urban markets remains muted: Distributors in smaller towns have indicated that stock from the larger urban markets are being channelized into Tier 2 and Tier 3 cities due to lack of demand in metro cities. This trend has primarily been observed in the Personal Care segment. Inability to meet year end sales targets: FMCG companies had sharply increased distributor sales targets in FY13 which were being successfully met during 9mFY13 as per our previous interactions. However in Q4FY13, certain distributors namely HUL have indicated that they have been unable to meet their monthly sales targets citing demand pressure. Competition from regional brands and unorganized players intensifies in specific categories: Distributors indicated that certain categories like Detergent and coconut hair oil are witnessing increase in competitive activity from regional and unorganized brands. This has led to deceleration in volume growth for the larger branded incumbents. Increase in promotional offers for consumers in the retail channel: As verified by our channel checks, distributors stated that companies have recently stepped up promotional offers for consumers namely HUL, Colgate, Marico and GCPL in specific categories, brands and SKU’s. Election year does not significantly alter the demand scenario: Distributors responded that they have not witnessed any specific pick up in demand primarily during periods of state or Lok Sabha elections. They shared that cash rollouts to voters are utilized for consumption of liquor, foods and white goods. Our channel checks largely substantiate our negative stance on the sector. On the ground consumer demand sluggishness is expected to persist. Recovery is estimated to be protracted in the forthcoming quarters as against current estimates of healthy uptick in volume growth in FY14E.

Post festive season in Q3FY13, consumer demand has decelerated in Q4FY13. Consumer demand is not expected to pick up pace in the near term

Demand in discretionary categories has been negatively impacted. Distributors have mentioned that inventory in channel has increased in Q4FY13

Demand in urban markets being muted as led to stock being dumped into Tier 1 and Tier 2 city markets.

Competition in the market has increased including local and regional players for categories like Detergents and coconut hair oil.

In H1FY13, distributors were able to meet the set aggressive sales targets. However they have been unable to do the same in Q4FY13.

In H1FY13, distributors were able to meet the set aggressive sales targets. However they have been unable to do the same in Q4FY13.

– 14 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / FMCG SECTOR UPDATE

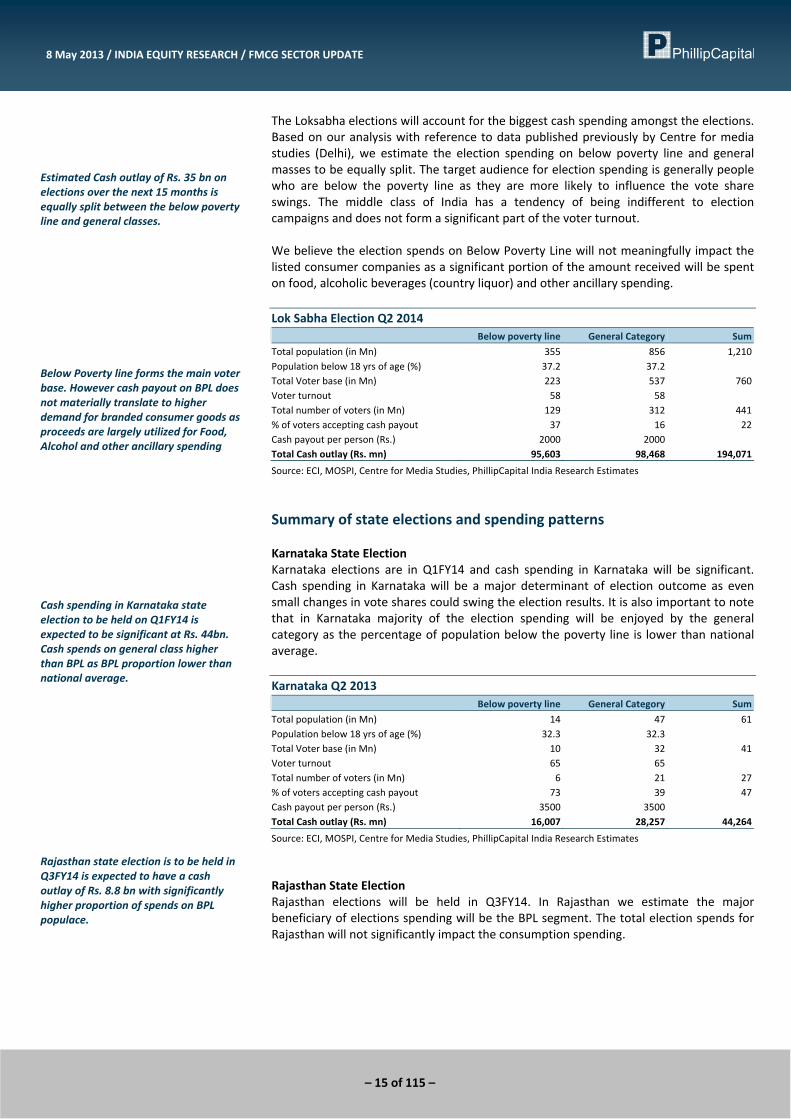

Election year but very little to cheer about for the consumer companies Elections in India involve cash spending by the contesting political parties. The cash spending by the contesting parties is substantial. We estimate the total cash spending during the Loksabha (General Elections) and state elections to be in the range of ~Rs 350bn over the next 14 months. This amount of cash spending can seemingly spur consumption growth but the historical data shows limited impact on the branded consumer companies. We have tried to analyse the impact on consumer companies using statistical tools and qualitative analysis. The scheduled time frame for general Loksabha elections is May 2014 but certain political developments are indicating earlier elections and the time frame for which is likely to be October 2013. Thus it is fair to assume that FY14 is likely to see some or full impact of the general Loksabha elections. Apart from the Loksabha elections, the current fiscal year will be impacted by state elections. We note that that there are 7 state assembly elections over the next 15 months. Karnataka and Andhra Pradesh will be the biggest amongst the 7 states going into elections. The table below provides the summary of the election cash spending over the next 15 months. Estimated cash spending on elections over the next 15 months

Time period Elections Below Poverty line cash

outlay for election (Rs. Crore)General category cash

outlay for election (Rs. Crore)

Q2 CY2014 Lok Sabha 95,603 98,468 State Elections Q2 CY2013 ‐ Karnataka 16,007 28,257Q4 CY2013 ‐ Rajasthan 6,246 2,515Q4 CY2013 ‐ Chhattisgarh 5,440 889Q4 CY2013 ‐ Delhi 481 3,129Q4 CY2013 ‐ Madhya Pradesh 7,395 15,936Q2 CY2014 ‐ Andhra Pradesh 27,768 16,140Q2 CY2014 ‐ Orissa 6,109 2,924

Sum total 165,048 168,258 Total Spending 333,306 % proportion of total spends 49.5 50.5

Grand Total 333,306

Source: Election Commission of India (ECI), MOSPI, Centre for Media Studies, PhillipCapital India Research

Estimates

As the cash payout during elections varies across states and classes we initiated our analysis with collating data on state wise population breakup into below poverty line and general classes. Secondly, we gathered data on number of voters and voter turnout ratio for State Assembly elections and Lok Sabha election. Centre for media studies (Delhi) has published researched on proportion of state wise population receiving cash handouts based on classes with indicative data of cash payout per person per state. We have based our analysis on the similar research and derived our observations. Also state wise cash payout factor is defined by the degree of the close contest of the election and the critical contribution of the state to nationwide politics. Our cash payout assumptions take into account these factors.

Cash spending during elections is substantial. We expect cash outlay of ~Rs. 350 bn over the next 15 months on 7 state elections and the Lok Sabha elections

However statistical and qualitative analysis indicates that election cash spending has limited impact in spurring consumer demand primarily for branded consumer companies.

Probability of early Lok Sabha elections in Oct 2013 or if Lok Sabha elections are conducted as scheduled in May 2014, we expect FY14 to witness full or some impact of cash spending in the elections.

Cash payout differs across states and classes. Cash payout is a factor of closely contested elections and critical contribution of the state to nationwide politics.

– 15 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / FMCG SECTOR UPDATE

The Loksabha elections will account for the biggest cash spending amongst the elections. Based on our analysis with reference to data published previously by Centre for media studies (Delhi), we estimate the election spending on below poverty line and general masses to be equally split. The target audience for election spending is generally people who are below the poverty line as they are more likely to influence the vote share swings. The middle class of India has a tendency of being indifferent to election campaigns and does not form a significant part of the voter turnout. We believe the election spends on Below Poverty Line will not meaningfully impact the listed consumer companies as a significant portion of the amount received will be spent on food, alcoholic beverages (country liquor) and other ancillary spending. Lok Sabha Election Q2 2014 Below poverty line General Category Sum

Total population (in Mn) 355 856 1,210 Population below 18 yrs of age (%) 37.2 37.2Total Voter base (in Mn) 223 537 760 Voter turnout 58 58Total number of voters (in Mn) 129 312 441 % of voters accepting cash payout 37 16 22Cash payout per person (Rs.) 2000 2000Total Cash outlay (Rs. mn) 95,603 98,468 194,071

Source: ECI, MOSPI, Centre for Media Studies, PhillipCapital India Research Estimates

Summary of state elections and spending patterns Karnataka State Election Karnataka elections are in Q1FY14 and cash spending in Karnataka will be significant. Cash spending in Karnataka will be a major determinant of election outcome as even small changes in vote shares could swing the election results. It is also important to note that in Karnataka majority of the election spending will be enjoyed by the general category as the percentage of population below the poverty line is lower than national average. Karnataka Q2 2013 Below poverty line General Category Sum

Total population (in Mn) 14 47 61 Population below 18 yrs of age (%) 32.3 32.3Total Voter base (in Mn) 10 32 41 Voter turnout 65 65Total number of voters (in Mn) 6 21 27 % of voters accepting cash payout 73 39 47Cash payout per person (Rs.) 3500 3500Total Cash outlay (Rs. mn) 16,007 28,257 44,264

Source: ECI, MOSPI, Centre for Media Studies, PhillipCapital India Research Estimates

Rajasthan State Election Rajasthan elections will be held in Q3FY14. In Rajasthan we estimate the major beneficiary of elections spending will be the BPL segment. The total election spends for Rajasthan will not significantly impact the consumption spending.

Estimated Cash outlay of Rs. 35 bn on elections over the next 15 months is equally split between the below poverty line and general classes.

Below Poverty line forms the main voter base. However cash payout on BPL does not materially translate to higher demand for branded consumer goods as proceeds are largely utilized for Food, Alcohol and other ancillary spending

Cash spending in Karnataka state election to be held on Q1FY14 is expected to be significant at Rs. 44bn. Cash spends on general class higher than BPL as BPL proportion lower than national average.

Rajasthan state election is to be held in Q3FY14 is expected to have a cash outlay of Rs. 8.8 bn with significantly higher proportion of spends on BPL populace.

– 16 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / FMCG SECTOR UPDATE

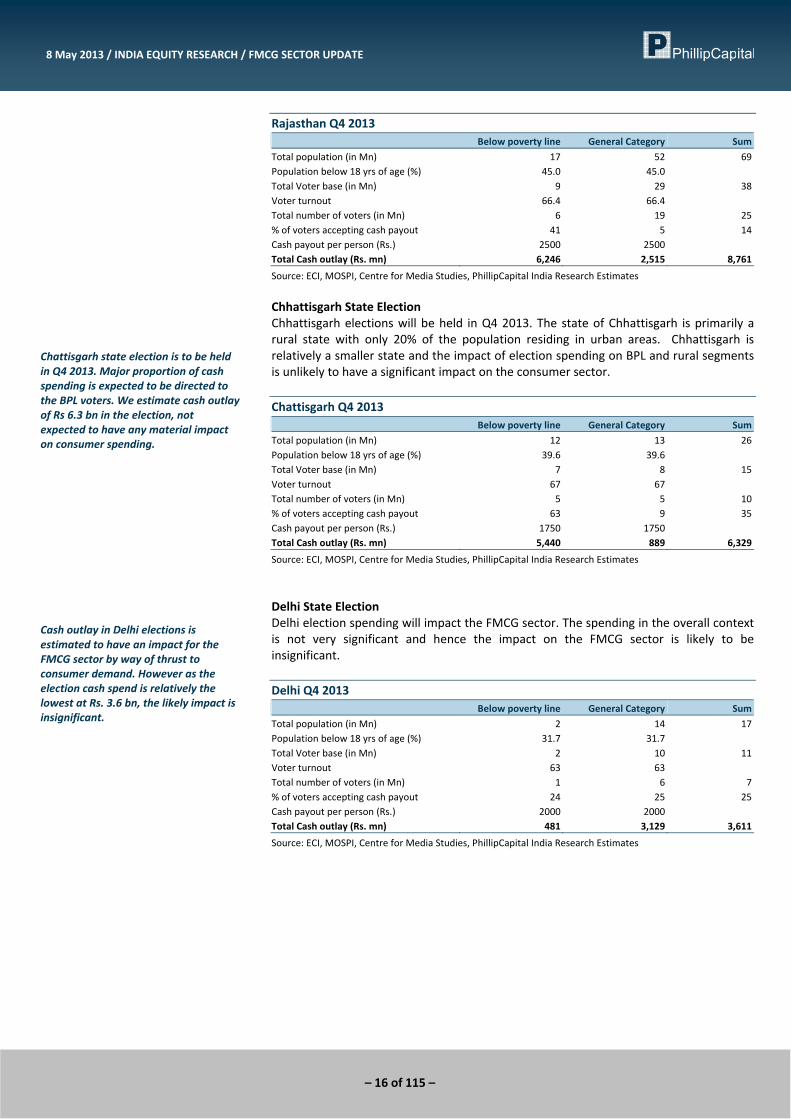

Rajasthan Q4 2013 Below poverty line General Category Sum

Total population (in Mn) 17 52 69 Population below 18 yrs of age (%) 45.0 45.0Total Voter base (in Mn) 9 29 38 Voter turnout 66.4 66.4Total number of voters (in Mn) 6 19 25 % of voters accepting cash payout 41 5 14Cash payout per person (Rs.) 2500 2500Total Cash outlay (Rs. mn) 6,246 2,515 8,761

Source: ECI, MOSPI, Centre for Media Studies, PhillipCapital India Research Estimates

Chhattisgarh State Election Chhattisgarh elections will be held in Q4 2013. The state of Chhattisgarh is primarily a rural state with only 20% of the population residing in urban areas. Chhattisgarh is relatively a smaller state and the impact of election spending on BPL and rural segments is unlikely to have a significant impact on the consumer sector. Chattisgarh Q4 2013 Below poverty line General Category Sum

Total population (in Mn) 12 13 26 Population below 18 yrs of age (%) 39.6 39.6Total Voter base (in Mn) 7 8 15 Voter turnout 67 67Total number of voters (in Mn) 5 5 10 % of voters accepting cash payout 63 9 35Cash payout per person (Rs.) 1750 1750Total Cash outlay (Rs. mn) 5,440 889 6,329

Source: ECI, MOSPI, Centre for Media Studies, PhillipCapital India Research Estimates

Delhi State Election Delhi election spending will impact the FMCG sector. The spending in the overall context is not very significant and hence the impact on the FMCG sector is likely to be insignificant. Delhi Q4 2013 Below poverty line General Category Sum

Total population (in Mn) 2 14 17 Population below 18 yrs of age (%) 31.7 31.7Total Voter base (in Mn) 2 10 11 Voter turnout 63 63Total number of voters (in Mn) 1 6 7% of voters accepting cash payout 24 25 25Cash payout per person (Rs.) 2000 2000Total Cash outlay (Rs. mn) 481 3,129 3,611

Source: ECI, MOSPI, Centre for Media Studies, PhillipCapital India Research Estimates

Chattisgarh state election is to be held in Q4 2013. Major proportion of cash spending is expected to be directed to the BPL voters. We estimate cash outlay of Rs 6.3 bn in the election, not expected to have any material impact on consumer spending.

Cash outlay in Delhi elections is estimated to have an impact for the FMCG sector by way of thrust to consumer demand. However as the election cash spend is relatively the lowest at Rs. 3.6 bn, the likely impact is insignificant.

– 17 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / FMCG SECTOR UPDATE

Madhya Pradesh State Election Madhya Pradesh elections are important and the election spending on the general category will impact the FMCG sector. On account of the high population base and the high voter turnout ratio the estimated total cash outlay on the state election is significant. Madhya Pradesh Q4 2013 Below poverty line General Category Sum

Total population (in Mn) 26 46 73 Population below 18 yrs of age (%) 43.8 43.8Total Voter base (in Mn) 15 26 41 Voter turnout 69.3 69.3Total number of voters (in Mn) 10 18 28 % of voters accepting cash payout 29 35.3 33Cash payout per person (Rs.) 2500 2500Total Cash outlay (Rs. mn) 7,395 15,936 23,331

Source: ECI, MOSPI, Centre for Media Studies, PhillipCapital India Research Estimates

Andhra Pradesh State Election Andhra Pradesh election is expected to be closely contested; hence the level of cash payout is estimated to be significant. Andhra Pradesh and the voter base is predominantly of the general category class. However the cash payout extending to BPL is higher on account of the 90%+ cash acceptance ratio. Andhra Pradesh Q4 2013 Below poverty line General Category Sum

Total population (in Mn) 18 67 85 Population below 18 yrs of age (%) 34.1 34.1Total Voter base (in Mn) 12 44 56 Voter turnout 72.5 72.5Total number of voters (in Mn) 8 32 40 % of voters accepting cash payout 94 14.4 31Cash payout per person (Rs.) 3500 3500Total Cash outlay (Rs. mn) 27,768 16,140 43,907

Source: ECI, MOSPI, Centre for Media Studies, PhillipCapital India Research Estimates

Orissa State Election Orissa state election is to be held in Q2 2014. The proportion of general class voter base is higher, however cash payout is largely directed to the BPL class. Hence we estimate the likely impact on consumption spending to be limited. Orissa Q2 2014 Below poverty line General Category Sum

Total population (in Mn) 15 27 42 Population below 18 yrs of age (%) 30.4 30.4Total Voter base (in Mn) 11 19 29 Voter turnout 65.5 65.5Total number of voters (in Mn) 7 12 19 % of voters accepting cash payout 50 13.8 27Cash payout per person (Rs.) 1750 1750Total Cash outlay (Rs. mn) 6,109 2,924 9,033

Source: ECI, MOSPI, Centre for Media Studies, PhillipCapital India Research Estimates

Madhya Pradesh elections are expected to have significant cash spending on the general category, which is estimated to have a positive impact on the FMCG sector. The estimated total cash outlay is high at Rs. 23 bn on account of higher voter base and voter turnout.

Andhra Pradesh elections are expected to have a high cash outlay of Rs. 44 bn. The election is expected to be closely contested hence the high level of cash payout per person. Major proportion of the cash payout is to the BPL class on account of their 90%+ acceptance ratio

Orissa state election cash outlay is estimated at R. 9bn of which significant proceeds is estimated to be directed to the BPL class. Hence we estimate limited impact on consumer spending.

– 18 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / FMCG SECTOR UPDATE

Statistical analysis of election impact We have analysed the election year phenomenon using statistical tools to assess the impact on the consumer sector. We have analysed whether the revenue growth during an election year is significantly higher from a normal year. We have found that there happens to be just a 22% probability of the event being true. We have used Hindustan Unilever Limited as a proxy for the FMCG sector as it has significant availability of time series data and being the largest consumer goods company with the widest distribution network, HUL is an apt proxy. Using T distribution test we assess the impact of election year impact on HUL and sector growth. T distribution test on Sector growth during election years and HUL revenue growth Sr. No HUL Growth (%) Election year

1 19.3 19.6 2 22.2 19.1 3 16.5 18.5 4 17.4 21.3 5 37.0 1.4 6 36.4 18.0 7 7.0 8 4.5 9 0.6 10 (6.3) 11 (2.1) 12 11.4 13 9.4 14 13.3 15 8.2 16 10.6 17 12.1 18 16.6

Mean 13 16 Standard deviation 11 7 Ttest 21%

Source: PhillipCapital India Research, Companies

We note that the 22% probability for HUL’s revenue growth being higher than a normal year is statistically significant but from the stock market the probability is not very significant to upgrade revenue estimates based on the event. Also in our interactions with various FMCG companies, we have noted that companies have not modeled for growth based on election year spending. Thus while the event appears to be significant, we believe the impact on the FMCG sector is likely to be limited.

– 19 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / FMCG SECTOR UPDATE

Limited positive impact of input cost inflation‐ Too little to cheer We have assessed the impact of decline in input costs for the leading FMCG companies. We note that HUL, Godrej Consumer, Nestle India and Asian paints will benefit the most on account of benign input cost inflation. While the benefits appear to be significant but when we consider the earnings impact on account of decline in input costs in conjunction with the market initiatives we find the impact will not significantly change the earnings profile.

Summary table depicting revision in estimates on volume, pricing, inflation, Ad spends in FY14E for sector coverage and the incremental earnings impact

FY14E Volume Growth YoY %

FY14E Pricing Growth YoY %

FY14E COGS Inflation YoY %

Incremental Input

Cost Savings

Incremental Gross

Profit impact

Gross margin expansion ( in bps) Ad to sales ratio (%)

EPS impact

(%) Company Previous Revised Previous Revised Previous Revised (Rs mn) (Rs mn)* Previous Revised Previous Revised

Hindustan Unilever 7.6 6.9 5.2 3.8 3.5 0.5 5,540 (1,172) 78 161 12.8 13.2 (2.4)Nestle India 9.3 7.2 7.3 7.3 5.4 3.0 679 (1,119) 48 33 4.9 4.5 (6.3)Dabur 12.0 11.8 3.8 3.8 5.0 4.0 1,505 (276) 26 105 13.4 13.4 (2.2)Colgate 10.4 10.0 4.6 2.8 4.8 2.4 413 (331) 62 95 11.2 11.5 (4.2)GSKConsumer 10.5 8.6 4.9 6.3 5.2 4.0 354 188 (2) 82 16.1 16.8 2.4Godrej Consumer** 7.0 11.7 5.0 0.0 5.0 (4.0) 1,709 535 172 144 10.0 10.0 5.0Marico 11.8 11.9 3.5 2.8 4.0 3.5 82 (202) (91) (66) 12.7 13.0 (3.3)Agro tech Foods 9.6 9.3 6.3 4.9 6.5 4.5 227 1 48 107 6.1 6.3 0.2Asian Paints NA 9.0 NA 0.0 NA (1.5) NA NA NA 147 NA 4.9 NABritannia NA 9.4 NA 6.0 NA 2.9 NA NA NA 55 NA 8.3 NAEmami NA 13.3 NA 4.0 NA (0.4) NA NA NA 161 NA 17.7 NABajaj Corp NA 17.3 NA 5.9 NA 3.2 NA NA NA 82 NA 14.5 NAZydus Wellness NA 13.4 NA 1.0 NA 2.1 NA NA NA 40 NA 20.4 NA

Source: PhillipCapital India Research Estimates, Companies

Our key findings are as follows: • ITC: ITC’s input cost basket is dominated by tobacco. ITC tends to hold an inventory

of 12‐14 months of tobacco. Thus, benefits on account of decline in Palm oil and crude prices for ITC will largely be limited.

• HUL: In a benign input cost scenario, the Company generally experiences an increase in competitive activity and the benefits of lower input costs do not translate to significant benefits on profitability as the company’s brand investments and product promotions increase significantly. We estimate the impact on EPS to be limited to 2% only.

• Asian Paints: Benefits of correction in TiO2 prices will be significant but we believe that sluggish demand scenario and flat pricing growth will translate to uninspiring revenue growth.

• Dabur: We estimate marginal positive impact on account of benign input cost inflation in crude related derivatives (c. 40% to COGS), Sugar and fruits & vegetables. We have not included estimates on inflation in Herbs & Spices (c. 50% to COGS) on account of data unavailability, however management has guided for muted inflation of 2 ‐ 3% YoY.

• Nestle: Nestle is expected to benefit from soft inflation in Coffee, Sugar, Cocoa and HDPE. However we have lowered our volume growth estimates for Nestle in CY13E, as we expect growth recovery to remain challenging considering higher than sector pricing growth. Hence our revised earnings remains downward inspite of input cost savings.

To surmise, we do not expect inspiring earnings growth on account of softer input cost inflation as we believe increase in competitive activity and sluggish demand scenario are likely to play truant.

HUL, GCPL, Nestle India and Asian Paints are estimated to benefit the most in terms of input cost savings in FY14E. However on account of market initiatives undertaken the positive impact on EPS is limited

HUL experiences high competitive intensity in benign input inflation scenario. Hence as the company steps up pricing discounts and brand spends, the input cost savings do not translate to significant increase in profitability.

High competitive intensity, limited pricing growth, sluggish demand, increase in brand spends is expected to limit the earnings benefit from input cost savings for the Consumer sector

– 20 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / FMCG SECTOR UPDATE

Consensus estimates continue to remain aggressive and disappointment to consensus will lead to a de‐rating We have seen that in the recent results, earnings downgrade have started. Consensus and our estimates of a volume growth bounce‐back in FY14E are aggressive as the macroeconomic environment continues to remain challenging. Consensus estimates for FY14E ____________FY14E____________ _________Growth YoY %_________Rs mn Sales EBITDA PAT Sales EBITDA PAT

ITC 342,472 125,242 87,220 16.2 18.2 17.8HUL 292,541 45,914 36,379 13.9 14.3 11.0Nestle 95,955 21,229 12,398 15.6 10.9 16.1GCPL 77,114 13,309 8,640 20.7 25.1 23.4Dabur 71,924 12,236 9,197 15.8 19.2 19.9Colgate 36,034 7,887 6,043 16.0 18.0 15.7GSKConsumer 35,557 6,342 5,110 15.5 10.4 17.0Marico 53,934 7,533 4,943 14.9 16.6 21.6Jubilant Foodworks 19,286 3,461 1,973 35.1 36.3 38.4AgroTech Foods 8,999 776 501 14.3 20.8 20.3Asian Paints 130,825 21,837 14,169 16.9 21.0 21.0Britannia 64,550 3,792 2,519 15.2 22.7 24.1Bajaj Corp 7,403 2,073 1,955 22.3 21.0 19.9Zydus Wellness 4,509 1,183 951 17.4 19.2 16.7Emami 20,182 4,359 3,695 17.7 21.5 18.3

Source: Bloomberg

In the recent past after the generally disappointing Q3FY13 results for the FMCG sector, we have seen that earnings have been downgraded for 7 of the 10 major large capitalisation companies. The major downgrades seen were: Hindustan Unilever after the company reported poor volume growth and increase in Royalty charges. Colgate, Marico also saw earnings downgrade on account of slower volume growth and rise in cost structure. Nestle’s results have not been inspiring and the company has further increased royalty charges which has led to earnings downgrade. Asian Paints has seen earnings upgrade on account input cost deflation. ITC has also seen earnings upgrade on account of better than‐expected volume growth in the cigarettes business. Dabur also has seen earnings upgrade on account of robust volume growth and superior margin performance. Thus, overall we see that the sector has entered a phase of earnings downgrades. We believe the downgrade phase for consumer companies is generally protracted and thus a de‐rating of the sector is imminent.

– 21 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / FMCG SECTOR UPDATE

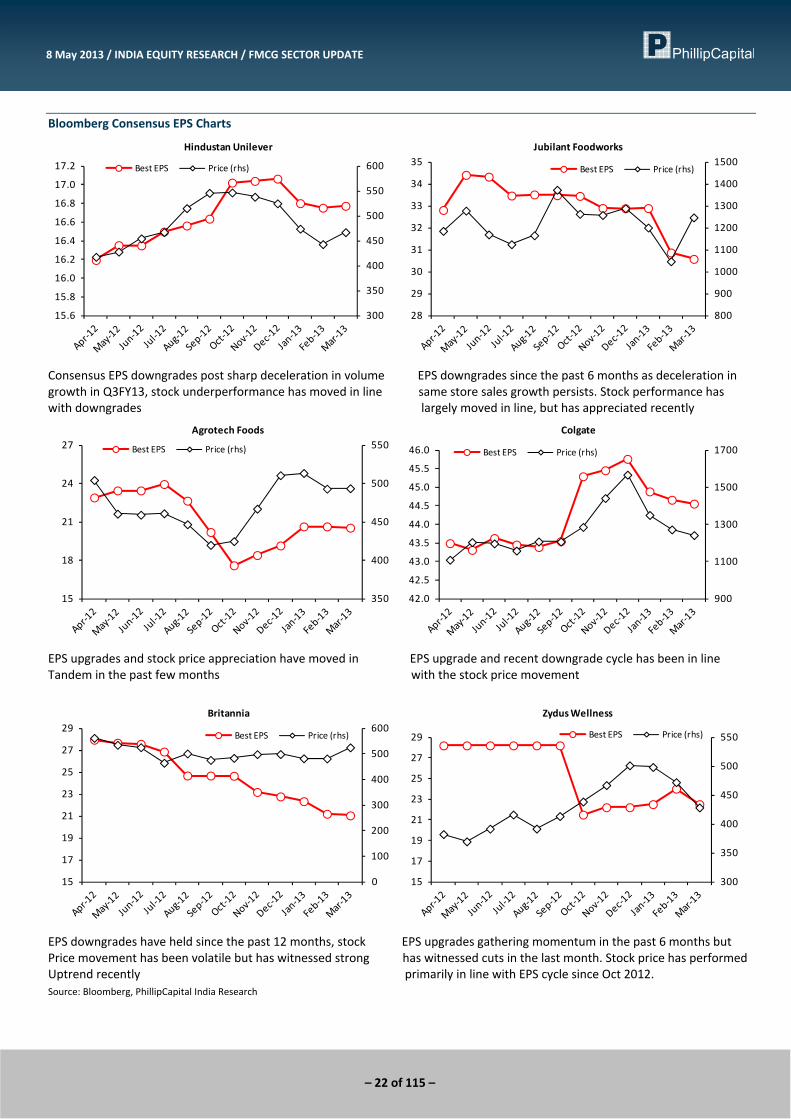

Bloomberg Consensus EPS Charts

100

110

120

130

140

5.15

5.20

5.25

5.30Dabur

Best EPS Price (rhs)

3000

3500

4000

4500

5000

5500

140.00

142.00

144.00

146.00

148.00

150.00Asian Paints

Best EPS Price (rhs)

Upgrades evident in Dabur in the past 6 months, stock price In recent months EPS estimates have been maintained, appreciation is ahead of the upgrades however price has appreciated significantly

150

175

200

225

250

7.50

7.60

7.70

7.80

7.90

8.00

8.10

8.20

8.30

Marico

Best EPS Price (rhs)

300

400

500

600

700

800

900

25.00

25.50

26.00

26.50

27.00

27.50

28.00

GCPL

Best EPS Price (rhs)

EPS downgrade cycle is very evident, however stock price has EPS downgraded post disappointing Q3FY13 results, however not corrected correspondingly stock has appreciated sharply, assigning unjustified premium valuations relative to the sector.

300

350

400

450

500

550

600

650

23.60

23.80

24.00

24.20

24.40

24.60

24.80

25.00Emami

Best EPS Price (rhs)

200

250

300

350

10.20

10.40

10.60

10.80

11.00

11.20

11.40ITC

Best EPS Price (rhs)

EPS upgrade cycle persists corresponding to stock appreciation EPS downgrades seen in the recent months following sharp excise duty and state VAT hikes, stock performance has been volatile Source: Bloomberg, PhillipCapital India Research

– 22 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / FMCG SECTOR UPDATE

Bloomberg Consensus EPS Charts

300

350

400

450

500

550

600

15.6

15.8

16.0

16.2

16.4

16.6

16.8

17.0

17.2

Hindustan Unilever

Best EPS Price (rhs)

800

900

1000

1100

1200

1300

1400

1500

28

29

30

31

32

33

34

35Jubilant Foodworks

Best EPS Price (rhs)

Consensus EPS downgrades post sharp deceleration in volume EPS downgrades since the past 6 months as deceleration in growth in Q3FY13, stock underperformance has moved in line same store sales growth persists. Stock performance has with downgrades largely moved in line, but has appreciated recently

350

400

450

500

550

15

18

21

24

27Agrotech Foods

Best EPS Price (rhs)

900

1100

1300

1500

1700

42.0

42.5

43.0

43.5

44.0

44.5

45.0

45.5

46.0

Colgate

Best EPS Price (rhs)

EPS upgrades and stock price appreciation have moved in EPS upgrade and recent downgrade cycle has been in line Tandem in the past few months with the stock price movement

0

100

200

300

400

500

600

15

17

19

21

23

25

27

29Britannia

Best EPS Price (rhs)

300

350

400

450

500

550

15

17

19

21

23

25

27

29

Zydus Wellness

Best EPS Price (rhs)

EPS downgrades have held since the past 12 months, stock EPS upgrades gathering momentum in the past 6 months but Price movement has been volatile but has witnessed strong has witnessed cuts in the last month. Stock price has performed Uptrend recently primarily in line with EPS cycle since Oct 2012. Source: Bloomberg, PhillipCapital India Research

– 23 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / FMCG SECTOR UPDATE

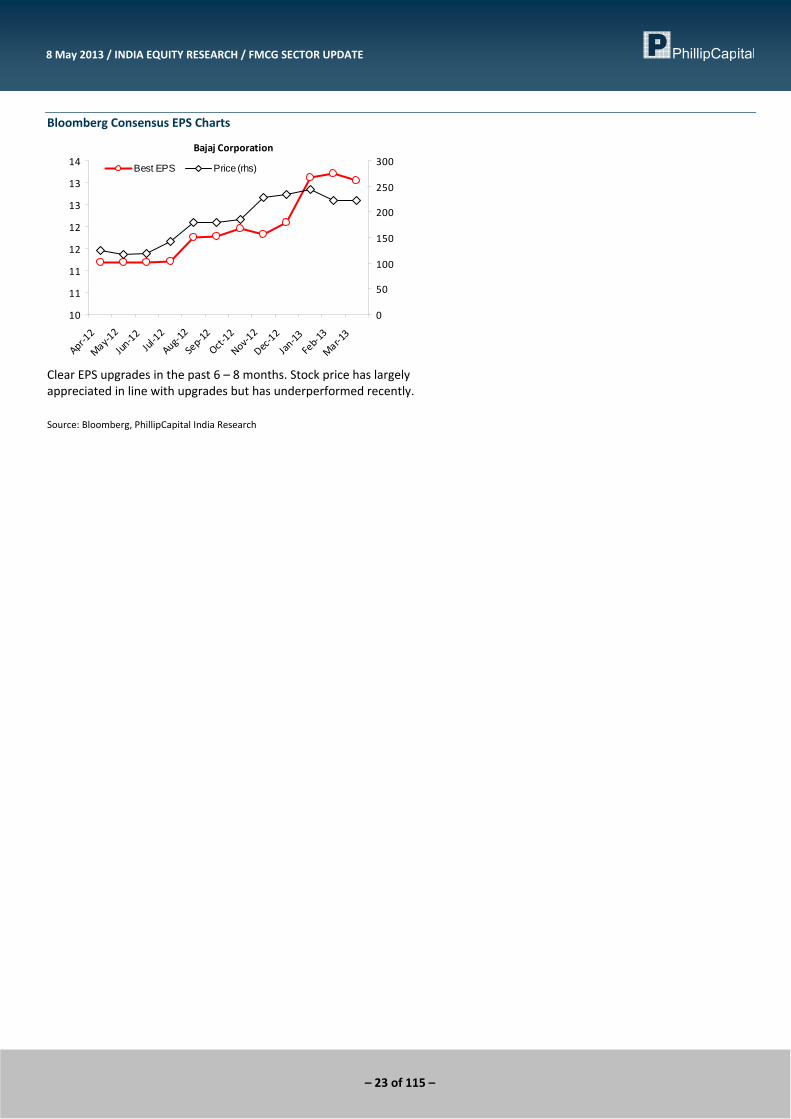

Bloomberg Consensus EPS Charts

Bajaj Corporation

10

11

11

12

12

13

13

14

Apr‐12

May‐12

Jun‐12

Jul‐12

Aug‐12

Sep‐12

Oct‐12

Nov‐12

Dec‐12

Jan‐13

Feb‐13

Mar‐13

0

50

100

150

200

250

300Best EPS Price (rhs)

Clear EPS upgrades in the past 6 – 8 months. Stock price has largely appreciated in line with upgrades but has underperformed recently. Source: Bloomberg, PhillipCapital India Research

– 24 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / FMCG SECTOR UPDATE

Compa

nies Section

– 25 of 115 –

ITC Risks getting amplified

FMCG: Company Update 8 May 2013

PhillipCapital (India) Pvt. Ltd.

We reiterate our Sell stance on ITC notwithstanding the considerable outperformance by the stock in the last 12 months as we believe the stock price appreciation is significantly ahead of company and industry fundamentals. While we note that the company has taken aggressive price hikes in the cigarettes category to safeguard the margins but volume and the subsequent disappointments on margins could surprise the market negatively. We continue to believe that the evolving state VAT taxation scenario will get more adverse which will reduce the pricing efficacy and the introduction of 64mm products is margin dilutive in the medium term. FY14E earnings growth could surprise negatively notwithstanding the 18% YoY price hike: We estimate that ITC has hiked prices by ~16% on blended basis after the union budget excise duty hike of 18% YoY. Considering the carryover effect of price hikes initiated in FY13, we estimate the total effective price hike for FY14E is ~18% YoY. While the 18% YoY price hike is steep consensus continues to envisage that volumes may not de‐grow and earnings growth will continue to be in high teens. We differ from consensus as we believe that volume de‐growth in such a high price inflation scenario is a perceptible risk and rising state VAT (up ~300bps YoY) will also impact profitability. We model for a volume growth of 0% and an earnings growth of 14% which is significantly lower than consensus expectations of 17‐20% earnings growth. VAT rate hikes are a long‐term negative; risks are increasing at an accelerated pace: 10 states exercised state VAT rate hikes in CY13 impacting ITC’s VAT rate by ~300 bps YoY to 23%. This is estimated to translate to an incremental burden of ~Rs22.8 bn in FY14E as compared to ~Rs 17.6 bn in FY13 on ITC consumers. It is also important to note that while excise duty hike increase at Rs 20bn for FY14E is significant but VAT burden increase is now significantly higher than excise duty. We believe the VAT regime will get more adverse in the future as in FY14 Karnataka (c.9%) and AP (c.9%) would have increased VAT rates, but for assembly elections refrained from raising any tax rates. State VAT hikes are a structural negative for ITC’s pricing power which should fundamentally translate to de‐rating of the category and the sock. Downtrading to 64mm products imminent and margin dilutive in the medium term: The pricing differential between 69mm and 64 mm has increased significantly after the recent round of price hikes in 69 mm while the prices of 64mm have been maintained. For the most profitable product Goldflake Premium (69mm, c.30% of volumes) the premium is now 96% and downtrading will translate to significant margin erosion and profitability. Maintain negative stance with SELL rating on ITC, Revise target price: We believe the market is not taking into cognizance the rising risks associated with VAT rate hikes and downtrading. We also find the stock expensive at current valuation which is at a premium of 50% as compared to the 5 year PER average. We maintain our Sell recommendation with a price objective of Rs 290 which implies a downside of 12% from the current levels.

SELL ITC IN | CMP RS 331

TARGET RS 290 (‐12%) Company Data

O/S SHARES (MN) : 7902MARKET CAP (RSBN) : 2614MARKET CAP (USDBN) : 47.252 ‐ WK HI/LO (RS) : 325 / 224LIQUIDITY 3M (USDMN) : 42.4FACE VALUE (RS) : 1

Share Holding Pattern, %

FII / NRI : 51.1FI / MF : 33.4NON PROMOTER CORP. HOLDINGS : 4.9PUBLIC & OTHERS : 10.6

Price Performance, % 1mth 3mth 1yr

ABS 7.4 7.0 36.6REL TO BSE 3.3 8.0 22.5

Price Vs. Sensex (Rebased values)

70

100

130

160

190

220

250

Apr‐10 Feb‐11 Dec‐11 Oct‐12ITC Rel. to BSE

Source: Bloomberg, Phillip Capital Research

Other Key Ratios

Rs mn FY13E FY14E FY15E

Net Sales 293,079 340,081 393,812Ebidta 105,680 124,303 145,650Net Profit 73,344 83,689 99,651EPS, Rs 9.4 10.6 12.6PER, X 35.3 31.2 26.2EV/EBIDTA, % 23.9 20.4 17.1EV/Net Sales, x 8.6 7.4 6.3ROE, % 33.6 32.7 32.4Source: Phillip Capital India Research Naveen Kulkarni, CFA, FRM (+ 9122 66679947) [email protected] Ennette Fernandes (+ 9122 66679764) [email protected]

– 26 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / ITC COMPANY UPDATE

FY14E earnings growth could surprise negatively notwithstanding the 18% YoY price hike: Effective pricing growth YTD in ITC’s cigarette segment

FY2014 Brands Size

(in mm)New MRP

Old MRP

Price hike Month

Revenue Contribution (%)

Gold Flake 69 55 48 14.58 4/1/2013 30.00Gold Flake Kings 84 68 58 17.24 4/1/2013 12.50Classic 84 136 116 17.24 4/1/2013 16.00Wills 74 59 49 20.41 4/1/2013 11.00Benson & Hedges 84 120 120 0.00 4/1/2013 1.00Capstan 69 34 28 21.43 4/1/2013 9.00Bristol 69 39 35 11.43 4/1/2013 9.00555 84 120 120 0.00 4/1/2013 1.00Scissors 69 40 35 14.29 4/1/2013 10.00Flake Excel 69 34 29 17.24 4/1/2013 1.00Weighted average price hike 16.09Carry forward pricing from FY13 Post Budget 13.75 4/15/2012 100.00Gold Flake 69 48 44 9.09 8/1/2012 30.00Carry forward impact in FY14 1.94Total pricing growth for FY14E 18.03

Source: Company, PhillipCapital India Research Estimates

We estimate the recent price hikes for the current fiscal year work out to 16.1%. The carry over price impact from the previous year works out to 1.9%. Thus, we estimate the effective price hike for the year will translate to 18%. We have analysed the per stick impact taking into account the increase in price hike and increase in VAT rate. We note that the EBIT per stick will increase by 14% YoY. The total EBIT for cigarettes segment will increase by 14% for the assumption of no volume de‐growth. We believe that assuming no de‐growth in volumes is aggressive considering the significant price hikes and we believe some volume de‐growth is plausible. We believe volume de‐growth will translate to negative surprise on earnings which could lead to a possible de‐rating for the stock. Per stick analysis FY12 FY13 FY14

Per Stick Breakup Gross MRP 3.46 4.13 4.88VAT 0.54 0.74 0.98Dealer Margins 0.34 0.41 0.49Reported Gross MRP 2.58 2.98 3.41Excise 1.14 1.37 1.60Net MRP 1.44 1.61 1.81RM 0.27 0.29 0.32Manufacturing & Freight 0.33 0.34 0.38Depreciation 0.03 0.03 0.03EBIT per Stick 0.81 0.96 1.09EBIT growth YoY % 18.41 13.97EBIT Margin % 56.23 59.29 60.21 Assumption Volume growth YoY 6.30 0.65 0.00Price Growth YoY (Ex VAT) 6.25 15.75 14.50Price Growth YoY (Inc VAT) 7.00 18.00 18.00

Source: Company, PhillipCapital India Research Estimates

– 27 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / ITC COMPANY UPDATE

VAT burden is increasing at an exponential growth rate ITC’s VAT burden is growing at an exponential pace. We have estimated the VAT paid by ITC has increased by more than 4x over the last years. State VAT is paid as a percentage of the Maximum Retail Price (MRP) and the percentage rate has almost doubled from 12.5% in FY09 to 23% in FY14E while the product prices have also doubled over the last 5 years. ITC’s incremental VAT burden is the highest in FY14 with increase of 40% YoY

10

15

20

25

30

35

40

45

FY2010 FY2011 FY2012 FY2013 FY2014

‐

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000State VAT (Rs. Mn) ITC VAT paid growth YoY (%)

Source: Company, PhillipCapital India Research Estimates

ITC’s incremental State VAT burden significantly exceeds excise duty in FY14E FY2009 FY2010 FY2011 FY2012 FY2013 FY2014

State VAT 22,586 28,135 33,626 47,198 64,799 87,650Excise Duty 74,997 79,915 92,509 99,007 119,668 139,821Sum total 97,583 108,050 126,135 146,205 184,466 227,470 Growth YoY % Total 10.7 16.7 15.9 26.2 23.3State VAT 24.6 19.5 40.4 37.3 35.3Excise duty 6.6 15.8 7.0 20.9 16.8 Absolute increase (in rs. Mn) State VAT 5,549 5,491 13,572 17,601 22,851Excise Duty 4,918 12,594 6,498 20,661 20,153Sum total 10,467 18,085 20,070 38,262 43,004

Source: Company, PhillipCapital India Research Estimates

Ten states have increased the VAT (Value Added Tax) rate on cigarettes in the recently announced state budgets but Uttar Pradesh has recently announced a state VAT cut from 50% to 25%. Effectively the state VAT will increase by 300bps in FY14E notwithstanding Andhra Pradesh (AP, c. ~10%) and Karnataka (c. 9%) not changing the tax rates because of the upcoming assembly elections. AP and Karnataka are major contributors to ITC volumes.

– 28 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / ITC COMPANY UPDATE

State wise VAT hikes in CY13 and impact on ITC’s effective VAT rate for FY14E Sr. No. State Revenue ______Duties %______ Increase % Contribution % Contribution % From To to VAT Increase

1 Uttar Pradesh 2.5 50 25 ‐25 ‐0.632 Rajasthan 2.5 50 65 15 0.383 Jammu & Kashmir 1 30 40 10 0.104 Gujarat 3 25 30 5 0.155 Bihar 2 20 30 10 0.206 West Bengal 10 20.0 25.0 5 0.507 Assam 3 20.0 25.0 5 0.158 Kerala 8 15 21 6 0.489 Punjab 2 22.0 55.0 33 0.6610 Himachal Pradesh 2 18.0 36.0 18 0.3611 Maharashtra 10 20.0 25.0 5 0.50

Sum 2.85 CY12 ending VAT Rate % 19.9 Current CY13 VAT rate % 22.8

Source: PhillipCapital India Research

We believe Karnataka and AP will significantly hike VAT rates next year. Apart from AP and Karnataka, Delhi (c.2%), Madhya Pradesh (c.2‐3%), Orissa (c.2%) and Chhattisgarh (c.1‐2%) also did not change on account of upcoming assembly elections. Thus VAT rates will continue to rise and the VAT burden on consumers will continue to rise at an exponential pace. The rising VAT burden will impact the category growth negatively as VAT reduces the pricing power of the highly inelastic category.

– 29 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / ITC COMPANY UPDATE

Downtrading to 64mm from 69mm: Risks are getting amplified The current price difference between 69mm and 64mm has widened significantly which is likely to lead to a pronounced down‐trading over the medium to long‐term. Per stick analysis brand wise indicative of significantly lower margins in 64 mm relative to 69 mm. _______Gold Flake______ ____Bristol_____ ____Scissors____ ____Capstan____ 84 mm 69 mm 64 mm 69 mm 64 mm 69 mm 64 mm 69 mm 64 mm

Gross MRP 6.8 5.5 2.8 4.0 1.9 4.0 2.0 3.5 2.0Excise duty 2.73 1.41 0.67 1.41 0.67 1.41 0.67 1.41 0.67VAT 1.56 1.27 0.64 0.92 0.44 0.84 0.42 0.81 0.46Dealer Margins 0.68 0.55 0.28 0.40 0.19 0.40 0.20 0.35 0.20Net Realisations 1.83 2.28 1.21 1.27 0.60 1.35 0.71 0.94 0.67RM 0.44 0.37 0.34 0.30 0.28 0.32 0.30 0.25 0.23Manufacturing and Freight 0.33 0.33 0.33 0.33 0.33 0.33 0.33 0.33 0.33EBIT per stick 1.03 1.55 0.52 0.61 ‐0.02 0.67 0.07 0.33 0.10EBIT Margin % 56.50 67.93 43.28 48.07 ‐2.88 49.67 9.99 35.36 15.08

Source: Company, PhillipCapital India Research Estimates

We note that EBIT margin and EBIT per stick in 69mm GoldFlake have reached an all time high of ~68%. Down‐trading or even up‐trading is likely to impact the margins of the company. We believe that down‐trading from 69mm to 64mm is a highly likely scenario and considering the current price differential, down‐trading will not only lead to margin compression but more importantly will lead to slower profit growth as the EBIT per stick for 64mm products is significantly lower than 69mm products. In our sensitivity analysis of we note that a mere 10% down‐trading from 69mm to 64mm products leads to a decline in EBIT margin by ~85bps but more importantly absolute EBIT declines by 4.5%. We believe down‐trading is likely to be much more pronounced than the 10% indicative numbers. We expect down‐trading of by ~30% over the next 2‐3 years. Cigarette EBIT impact assuming 10% downtrading from 69mm to 64 mm Assuming 10 % downtrading in 69 mm to 64 mm Gold Flake Bristol Capstan Scissors

RSFT (69 mm) Revenue contribution 30.5 9.0 9.3 10.0 69 mm Brand revenue (Rs. Mn) 47,872 14,126 14,597 15,696 69 mm EBIT (Rs. Mn) 32,518 6,791 5,162 7,796 69 mm EBIT margins (%) 67.9 48.1 35.4 49.7 Brand revenue (69 mm + 64 mm) (Rs. Mn) 45,522 13,385 13,972 14,911 Brand EBIT (69 mm + 64 mm) (Rs. Mn) 30,321 6,092 4,772 7,094 Brand EBIT (69 mm + 64 mm) margins (%) 66.6 45.5 34.2 47.6 Brand EBIT degrowth due to 64 mm (%) ‐6.76 ‐10.28 ‐7.56 ‐8.99Brand EBIT margin contraction (%) (1.3) (2.6) (1.2) (2.1) ITC Cigarette Segment EBIT degrowth ‐4.46 ITC Cigarette Segment EBIT margin contraction 0.85

Source: PhillipCapital India Research Estimates

Thus, we believe that ITC is losing its pricing power because of rising state VAT but on the other hand its strategy of launching 64mm products to win more consumers is margin dilutive. ITC currently trades at very rich valuations which are not sustainable over the medium and long‐term. As, structural changes will start playing out a significant de‐rating is imminent. Hence our Sell recommendation.

– 30 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / ITC COMPANY UPDATE

Fair Value Calculation We have valued ITC on a DCF based method at Rs 298 per share. We estimate the 7 year Consolidated revenue CAGR of 14.5% YoY with Cigarette business growth robust at 12.5% CAGR and Other FMCG business growth expected to maintain traction at ~18.6% CAGR. We estimate normalized (long‐term) consolidated EBIT margins of 34.5%. Medium‐term forecasts

Rs mn Sales

FY2013CAGR

(7 years)Sales

2020 E EBIT

margin (%) EBIT (N) EBIT %

Cigarettes 139,528 12.5 317,828 58.0 184,340 70.8Other FMCG 69,953 18.6 230,523 10.0 23,052 8.8AgriBusiness 46,906 13.9 116,300 17.0 19,771 7.6Hotels 10,760 13.1 25,535 30.0 7,660 2.9PaperBoards 25,933 14.3 65,893 39.0 25,698 9.9Group 293,079 14.5 756,079 34.5 260,523 100

Source: Company, PhillipCapital India Research Estimates

Our exit multiple for Cigarettes business is 20x implying an earnings yield of 5% (terminal growth rate of 7.5%). Our exit multiple for FMCG others business is lower considering limited potential to expand EBIT margins. Our exit multiples for Hotels and Agribusiness are conservative. Derivation of Enterprise value 2020 (excluding intermediate FCF) Rs mn EBIT (N) Yield req (%) P/E EV/EBIT EV (2020)

Cigarettes 184,340 5.0 20 14.0 2,580,766Other FMCG 23,052 7.0 14 10.0 230,523AgriBusiness 19,771 20.0 5 3.5 69,198Hotels 7,660 10.0 10 7.0 53,623PaperBoards 25,698 9.0 11 7.8 199,876Group 260,523 5.8 17 12.0 3,133,987

Source: Company, PhillipCapital India Research Estimates

We have discounted the cash flows at 12.5%, considering a risk free rate of 8% and market risk premium of 6%, implying a beta of 0.75. Medium‐Term cash flow generation Rs mn 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E

EBIT 103,982 122,181 143,431 168,092 194,864 225,326 256,946 292,157NOPLAT 73,344 83,689 99,651 115,820 133,152 153,806 175,223 199,045Depreciation 8,030 8,925 9,752 10,619 11,526 12,474 13,465 14,498Capex 17,500 25,000 15,000 15,500 16,000 16,500 17,000 17,500FCF 63,875 67,614 94,403 110,939 128,678 149,781 171,688 196,043% conversion 61.4 55.3 65.8 66.0 66.0 66.5 66.8 67.1Discount factor 1.0 0.9 0.8 0.7 0.6 0.6 0.5 0.4PV 63,875 60,101 74,590 77,916 80,333 83,118 84,689 85,957NPV 63,875 123,976 198,566 276,482 356,815 439,933 524,621 610,579

Source: Company, PhillipCapital India Research Estimates

On the basis of our DCF valuation, the fair value of the company is computed at Rs 298, marginally higher than our SOTP valuation of Rs. 290 providing downside of 10% from current levels. Hence SELL recommendation

– 31 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / ITC COMPANY UPDATE

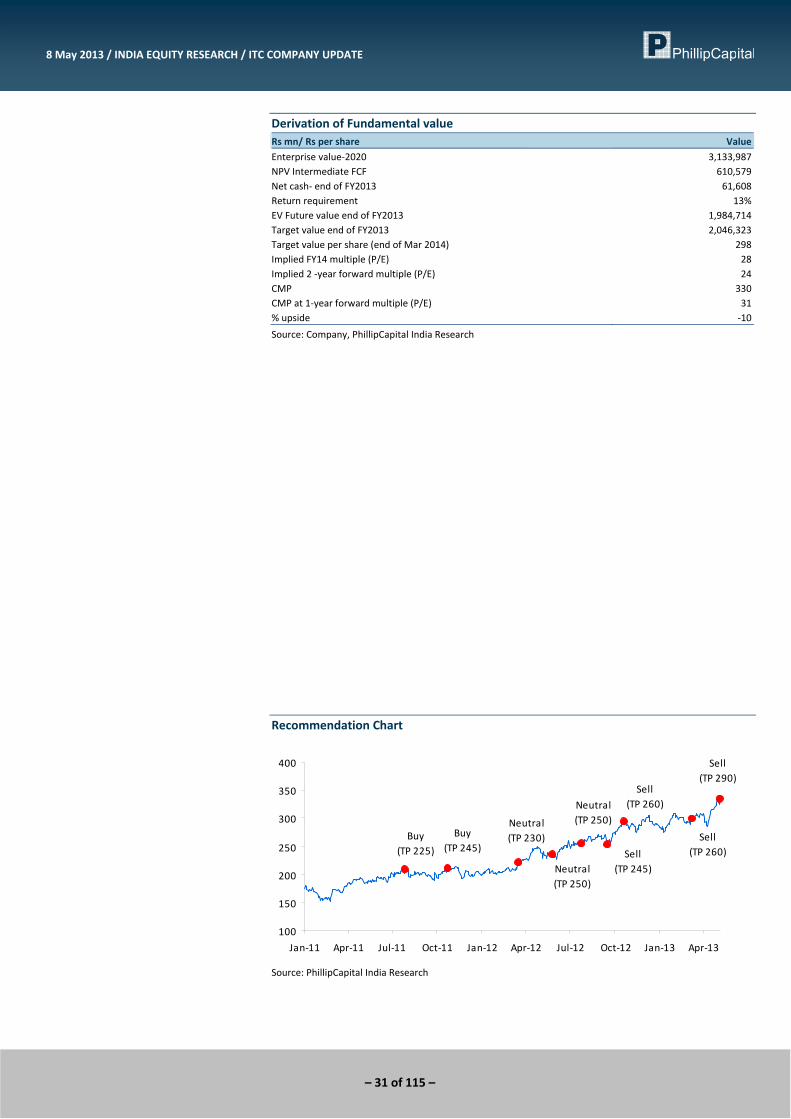

Derivation of Fundamental value Rs mn/ Rs per share Value

Enterprise value‐2020 3,133,987NPV Intermediate FCF 610,579Net cash‐ end of FY2013 61,608Return requirement 13%EV Future value end of FY2013 1,984,714Target value end of FY2013 2,046,323Target value per share (end of Mar 2014) 298Implied FY14 multiple (P/E) 28Implied 2 ‐year forward multiple (P/E) 24CMP 330CMP at 1‐year forward multiple (P/E) 31% upside ‐10

Source: Company, PhillipCapital India Research

Recommendation Chart

Sell(TP 290)

Sell(TP 260)

Buy(TP 225)

Buy(TP 245)

Neutral(TP 230)

Neutral(TP 250)

Neutral(TP 250)

Sell(TP 245)

Sell(TP 260)

100

150

200

250

300

350

400

Jan‐11 Apr‐11 Jul‐11 Oct‐11 Jan‐12 Apr‐12 Jul‐12 Oct‐12 Jan‐13 Apr‐13

Source: PhillipCapital India Research

– 32 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / ITC COMPANY UPDATE

Absolute Rolling Valuation Band Charts

PE band

15x

20x

25x

30x

0

50

100

150

200

250

300

350

400

Apr‐04

Apr‐05

Apr‐06

Apr‐07

Apr‐08

Apr‐09

Apr‐10

Apr‐11

Apr‐12

Apr‐13

Rs

PBV band

4x

6x

8x

10x

0

50

100

150

200

250

300

350

400

450

Apr‐04

Apr‐05

Apr‐06

Apr‐07

Apr‐08

Apr‐09

Apr‐10

Apr‐11

Apr‐12

Apr‐13

(Rs)

MCap/Sales band

2x

4x

6x

8x

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

Apr‐04

Apr‐05

Apr‐06

Apr‐07

Apr‐08

Apr‐09

Apr‐10

Apr‐11

Apr‐12

Apr‐13

(Rs mn)

EV/EBIDTA band

9x

12x

15x

18x

0

500000

1000000

1500000

2000000

2500000

3000000

Apr‐04

Apr‐05

Apr‐06

Apr‐07

Apr‐08

Apr‐09

Apr‐10

Apr‐11

Apr‐12

Apr‐13

Rs mn

EV/Sales band

2x

4x

6x

8x

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

Apr‐04

Apr‐05

Apr‐06

Apr‐07

Apr‐08

Apr‐09

Apr‐10

Apr‐11

Apr‐12

Apr‐13

(Rs mn)

Source: PhillipCapital India Research Estimates

– 33 of 115 –

8 May 2013 / INDIA EQUITY RESEARCH / ITC COMPANY UPDATE

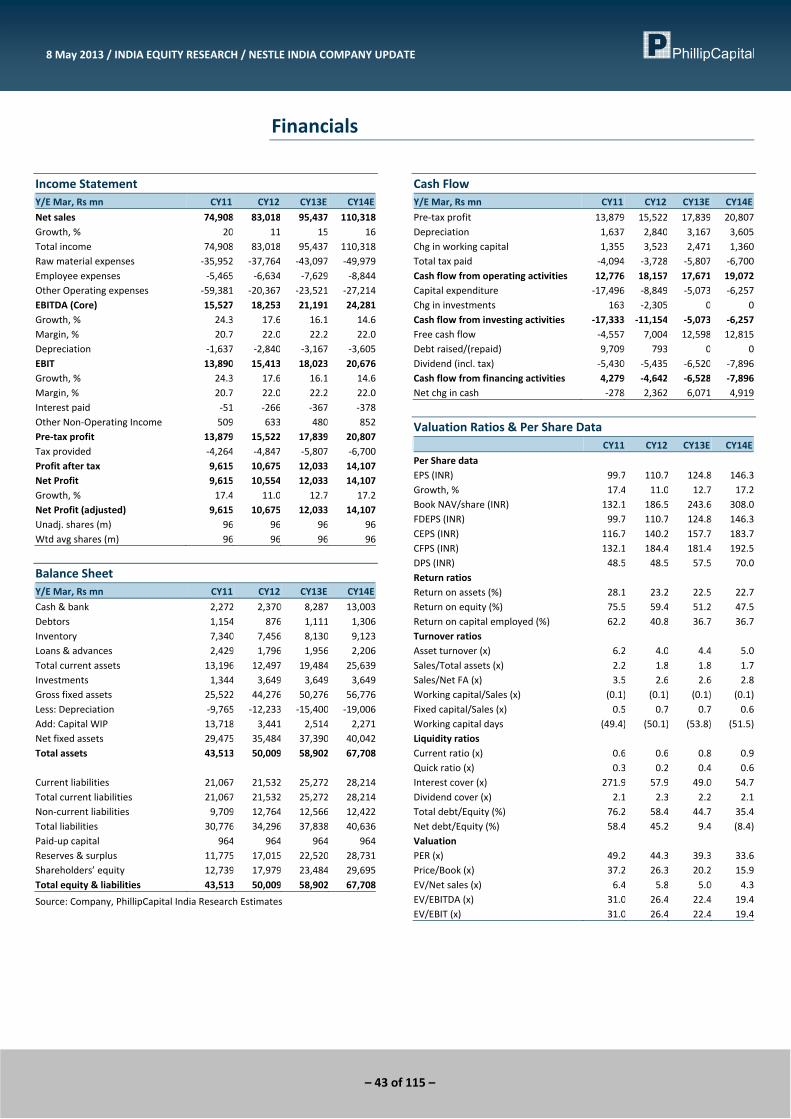

Financials

Income Statement Y/E Mar, Rs mn FY12 FY13E FY14E FY15E

Net sales 247,984 293,079 340,081 393,812Growth, % 17 18 16 16Other income 3,754 3,191 3,669 4,128Total income 251,738 296,270 343,750 397,940Raw material expenses ‐96,325 ‐117,613 ‐133,898 ‐153,562Employee expenses ‐12,654 ‐14,068 ‐15,984 ‐18,312Other Operating expenses ‐54,273 ‐58,909 ‐69,565 ‐80,416EBITDA (Core) 88,486 105,680 124,303 145,650Growth, % 19.4 19.4 17.6 17.2Margin, % 35.7 36.1 36.6 37.0Depreciation ‐6,988 ‐8,030 ‐8,925 ‐9,752EBIT 81,499 97,650 115,378 135,899Growth, % 19.4 19.4 17.6 17.2Margin, % 35.7 36.1 36.6 37.0Interest paid ‐779 ‐877 ‐942 ‐1,013Other Non‐Operating Income 8,253 9,523 10,473 11,660Pre‐tax profit 88,973 106,296 124,908 146,546Tax provided ‐27,352 ‐32,952 ‐41,220 ‐46,895Profit after tax 61,621 73,344 83,689 99,651Net Profit 61,621 73,344 83,689 99,651Growth, % 23.5 19.0 14.1 19.1Net Profit (adjusted) 61,621 73,344 83,689 99,651Unadj. shares (m) 7,738 7,818 7,878 7,878Wtd avg shares (m) 7,541 7,818 7,878 7,878

Balance Sheet Y/E Mar, Rs mn FY12 FY13E FY14E FY15E

Cash & bank 28,189 62,382 78,015 117,394Debtors 9,860 11,442 13,277 14,889Inventory 56,378 68,312 75,203 84,143Loans & advances 18,311 21,152 24,324 27,951Total current assets 112,739 163,288 190,820 244,378Investments 63,166 43,633 43,633 43,633Gross fixed assets 141,519 159,019 184,019 199,019Less: Depreciation ‐50,452 ‐60,880 ‐69,805 ‐79,557Add: Capital WIP 22,763 16,697 19,322 20,897Net fixed assets 113,830 114,837 133,537 140,360Non‐current assets 0 1,487 1,487 2,260Total assets 293,978 323,244 369,476 430,631 Current liabilities 48,087 57,357 62,363 69,418Provisions 44,111 46,918 50,554 53,085Total current liabilities 92,198 104,274 112,917 122,503Non‐current liabilities 13,861 891 891 891Total liabilities 106,059 105,165 113,809 123,395Paid‐up capital 7,818 7,818 7,818 7,818Reserves & surplus 180,100 210,261 247,849 299,418Shareholders’ equity 187,918 218,079 255,668 307,237Total equity & liabilities 293,977 323,244 369,476 430,631

Source: Company, PhillipCapital India Research Estimates

Cash Flow Y/E Mar, Rs mn FY12 FY13E FY14E FY15E

Pre‐tax profit 88,973 106,296 124,908 146,546Depreciation 6,988 8,030 8,925 9,752Chg in working capital 1,324 ‐5,767 ‐3,255 ‐5,367Total tax paid ‐26,643 ‐41,679 ‐41,220 ‐46,895Cash flow from operating activities 70,642 66,880 89,358 104,037Capital expenditure ‐24,029 ‐9,037 ‐27,625 ‐16,575Chg in investments ‐7,621 19,533 0 0Cash flow from investing activities ‐31,650 10,496 ‐27,625 ‐16,575Free cash flow 38,991 77,376 0 0Equity raised/(repaid) 80 0 0 0Dividend (incl. tax) ‐40,890 ‐43,172 ‐46,100 ‐48,082Cash flow from financing activities ‐40,810 ‐43,172 ‐46,100 ‐48,082Net chg in cash ‐1,819 34,204 15,634 39,379Pre‐tax profit 88,973 106,296 124,908 146,546Depreciation 6,988 8,030 8,925 9,752

Valuation Ratios & Per Share Data FY12 FY13E FY14E FY15E

Per Share data EPS (INR) 8.2 9.4 10.6 12.6Growth, % 23.5 14.8 13.2 19.1Book NAV/share (INR) 24.9 27.9 32.5 39.0FDEPS (INR) 8.2 9.4 10.6 12.6CEPS (INR) 9.1 10.4 11.8 13.9CFPS (INR) 8.3 7.5 10.0 11.8DPS (INR) 4.7 4.8 5.0 5.3Return ratios Return on assets (%) 22.5 23.9 24.3 25.1Return on equity (%) 32.8 33.6 32.7 32.4Return on capital employed (%) 27.0 28.9 29.4 30.0Turnover ratios Asset turnover (x) 1.8 1.9 2.0 2.1Sales/Total assets (x) 0.9 0.9 1.0 1.0Sales/Net FA (x) 2.4 2.6 2.7 2.9Working capital/Sales (x) 0.1 0.1 0.1 0.1Working capital days 53.7 54.2 54.1 53.4Liquidity ratios Current ratio (x) 2.3 2.8 3.1 3.5Quick ratio (x) 1.2 1.7 1.9 2.3Interest cover (x) 104.6 111.4 122.4 134.2Dividend cover (x) 1.8 2.0 2.1 2.4Net debt/Equity (%) (15.0) (28.6) (30.5) (38.2)Valuation PER (x) 40.5 35.3 31.2 26.2Price/Book (x) 13.3 11.9 10.2 8.5Yield (%) 1.4 1.4 1.5 1.6EV/Net sales (x) 10.2 8.6 7.4 6.3EV/EBITDA (x) 28.6 23.9 20.4 17.1EV/EBIT (x) 28.6 23.9 20.4 17.1

– 34 of 115 –

Hindustan Unilever Open offer‐ Time to tender

FMCG: Company Update 8 May 2013

PhillipCapital (India) Pvt. Ltd.