inbound flip transaction

TRANSCRIPT

Preparing Your Foreign Entity for US Venture Funding

October 2012

Inbound “Flip” Transactions

• Forco is a foreign corporation. It has identified and filled a market need and has accelerating year-over-year growth. With proper funding, Forco can rapidly improve its short-term profitability and long-term viability. Without proper funding, Forco remains vulnerable to better-funded emerging competitors.

• Forco needs venture capital funding to continue growing.

The Inbound “Flip” Scenario

Sources: Global Venture Capital Statistic: Ernst & Young, Globalizing Venture Capital: Global venture and insights and trends report; Rankings: The Global Venture Capital and Private Equity Country Attractiveness Index 2012, Alexander Groh, Heinrich Liechtenstein and Karsten Lieser, http://blog.iese.edu/vcpeindex/unitedstates/; “Size of the Economy”: http://www.imf.org/external/pubs/ft/weo/2012/01/weodata/index.aspx; “Size of the Stock Market”: http://data.worldbank.org/indicator/CM.MKT.LCAP.CD; “Stock Market Liquidity”: http://online.wsj.com/mdc/page/marketsdata.html; “IPO Market Activity”: http://www.pwc.com/us/en/press-releases/2012/q2-ipo-watch-press-release.jhtml; “M&A Market Activity”: http://www.marketwatch.com/story/ernst-young-us-ma-activity-falling-2012-07-02.

• Gross Domestic Product, 2011: $15.1 trillion

Size of the Economy

• Stock market cap, 2011: $15.6 trillion

Size of the Stock Market

• Daily trading volume, 10/11/2012: $4.7 billion

Stock Market Liquidity

• Number of IPOs, 2012 first half 71

IPO Market Activity

• Number of M&A deals, 2012 first half: 3,159

M&A Market Activity

Global Venture Capital and Private Equity Country Attractiveness Index ranks the US as the venture capital leader overall and in the following five categories:

Venture Capital Funding in the US

Source: Statistics: Ernst & Young, Globalizing Venture Capital: Global venture and insights and trends report; https://www.pwcmoneytree.com/MTPublic/ns/nav.jsp?page=historical.

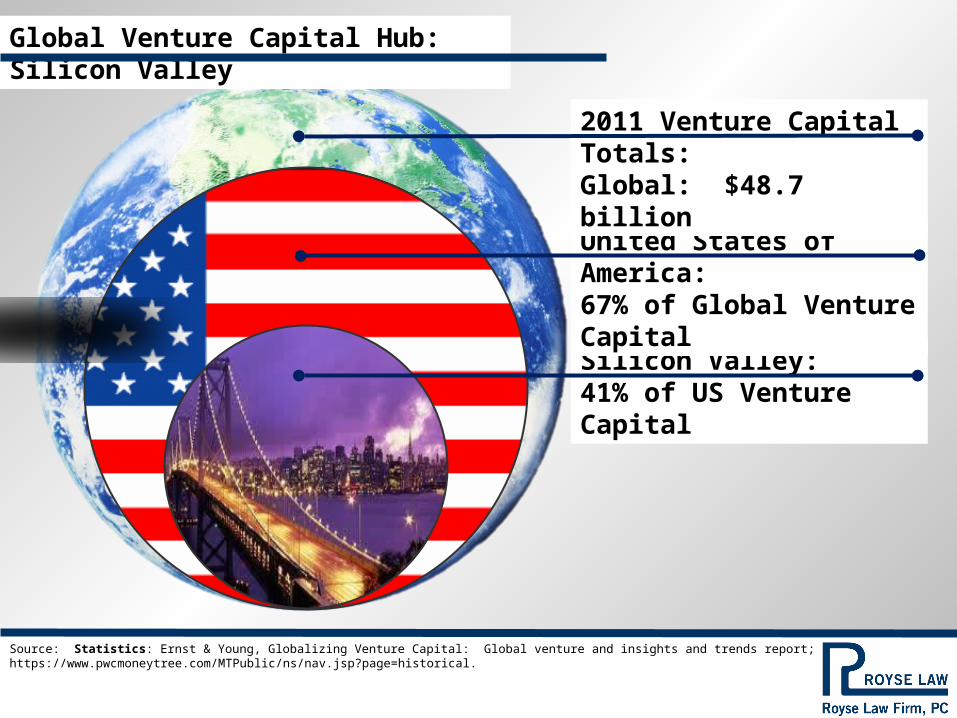

Silicon Valley:41% of US Venture Capital

United States of America:67% of Global Venture Capital

2011 Venture Capital Totals:Global: $48.7 billion

Global Venture Capital Hub: Silicon Valley

• US angel investors and venture capital fund managers’ discomfort or unfamiliarity with foreign entity structures and governing laws may dissuade investment in such entities, rendering them less likely than a similarly situated US company to secure funding.

The Problem

Description: The shareholders create a new US entity (“Domco”), and exchange their Forco stock for Domco stock. After the exchange, the shareholders will own Domco, and Domco will own Forco. Angel investors and venture capital funds would invest at the Domco level.

Domco(US)

Forco(Foreign)

Stock in Domco

Stock in ForcoShareholders

Domco(US)

Shareholders

Forco(Foreign)

The Solution: Inbound “Flip” Transactions

• Angel investors and venture capital funds are much more likely to invest in the corporate group at the new Domco level.

• Royse Law Firm has been performing inbound “flip” transactions since 2006.

• “Flips” can typically be achieved tax free, with only entity creation and legal document costs.

• “Flips” are generally executed quickly, and can be completed within about three weeks.

Shareholders

Results and Details

Domco(US)

Forco(Foreign)

Adobe Systems AMD Apple Cisco eBay

Facebook Google HP Intel Intuit

Nvidia Oracle Sun Microsys. Yahoo! YouTube

Perks of a Physical Move: Silicon Valley Customers, Employees, Acquirors

Source: Statistics: https://www.pwcmoneytree.com/MTPublic/ns/nav.jsp?page=historical; Graphics: http://en.wikipedia.org/wiki/Silicon_Valley.

Connecting founders with investors.

Providing business, tax, and personal finance ideas to founders and executives.

Offering legal document templates and more.

www.RoyseUniversity.com

www.RoyseLink.com

www.rroyselaw.com/ijuris_login_jp.html

Additional Resources

www.rroyselaw.comTwitter: RoyseLaw

PALO ALTO1717 Embarcadero Road

Palo Alto, CA 94306

LOS ANGELES1150 Santa Monica Blvd.

Suite 1200Los Angeles, CA 90025

SAN FRANCISCO135 Main Street

12th FloorSan Francisco, CA 94105

Palo Alto Office: 650-813-9700

Contact Us

The discussion of tax consideration was not intended or written to be used, and cannot be used, by any taxpayer for the purpose of avoiding tax penalties that may be imposed by the Internal Revenue Service. Each party should seek advice based on the party’s particular circumstances from an independent tax advisor.

In accordance with Section 6694 of the Internal Revenue Code of 1986, as amended (the “Code”), we hereby advise you that the positions set forth herein may lack substantial authority and, therefore, may be subject to penalty under Code section 6662(d) unless adequately disclosed on IRS Form 8275.

Circular 230 Disclosure