improving financial awareness among the poor in kooje slums of meru town-final project

TRANSCRIPT

IMPROVING FINANCIAL AWARENESS AMONG THE

POOR IN KOOJE SLUMS OF MERU TOWN

STUDENT NAME: CHIMWANI GEORGE LAWRENCE

REGISTRATION NO: BC555-0056/2010

This research project was done as a partial fulfillment to the award of a degree in

Bachelor of Commerce at Meru University of Science and Technology. The project was

submitted on:

2nd April 2015.

i

DECLARATION AND RECOMMENDATION

Declaration

This research project is my original work and has not been submitted to any other university for

the award of a degree.

Signature: ...................................................... Date: .............................

Chimwani George Lawrence.

BC555-0056/2010

Recommendation

This research project has been submitted for examination with my approval as the university

supervisor.

Signature: ...................................................... Date: ............................

Mr. Njati Ibuathu Charles.

School of Business and Economics

Meru University of Science and Technology.

ii

DEDICATION

To my Father Mr. Inzeyi Shikutwa Julius, I say God richly bless you and grant you your hearts

desires for being my father from my childhood days till date thank you for your support, patience

and belief in me.

iii

ACKNOWLEDGEMENT

In the course of conducting this study, I benefited immensely from the support of individuals and

institutions as well as the dwellers of Kooje slums. I am very grateful to the Almighty God for

his inspiration, mercies, graces and guidance throughout my life and the strength to complete

this study. I am particularly indebted to my Supervisor Mr. Njati Ibuathu Charles for always

reading thoroughly through my work promptly and offering his constructive criticism,

comments and advice towards the successful completion of this study.

I am also grateful to the academic staff members at Meru University Of Science And

Technology for their intellectual inspirations and lectures.

To the residents In Kooje Slums Of Meru Town , I am very appreciative of the information and

data that you willingly gave.

To the Inzeyi and Shikutwa families, I am very grateful for the encouragement, financial and

moral support throughout my life and career development. To my friends particularly Njoki

Njagi and classmates especially Bachelor Of Commerce(2015) class in Meru University Of

Science And Technology I am very grateful for the prayers you offered on my behalf to God and

the constant support and encouragement.

iv

TABLE OF CONTENTS

DECLARATION AND RECOMMENDATION ............................................................................ i

LIST OF FIGURES ...................................................................................................................... vii

LIST OF TABLES ....................................................................................................................... viii

ABBREVIATIONS AND ACRONYMS ...................................................................................... ix

ABSTRACT .................................................................................................................................... x

CHAPTER ONE ............................................................................................................................. 1

INTRODUCTION AND BACKGROUND TO THE STUDY ...................................................... 1

1.1 Background to the Problem ................................................................................................................ 1

1.2 Statement of the Problem .................................................................................................................. 3

1.3 Purpose of the Study ........................................................................................................................... 4

1.4 Study Objectives ................................................................................................................................. 4

1.5 Research Questions ............................................................................................................................ 4

1.6 Significance of the Study ..................................................................................................................... 4

1.7 Limitations and Delimitations of the Study ........................................................................................ 5

1.8 Assumptions of the Study ................................................................................................................... 5

1.9 Definitions of Operational Terms ........................................................................................................ 6

1.10 Summary ........................................................................................................................................... 6

CHAPTER TWO ............................................................................................................................ 7

REVIEW OF RELATED LITERATURE ...................................................................................... 7

2.1 Introduction ........................................................................................................................................ 7

2.1.1 Relationship between Literacy Levels and Financial Awareness ..................................................... 7

2.1.2 Ease of Access to Financial Services ................................................................................................. 8

2.1.3 Understanding the Financial Landscape of the Poor ....................................................................... 9

2.2 Theoretical Framework ....................................................................................................................... 9

2.3 Conceptual Framework ..................................................................................................................... 11

2.5 Summary of Knowledge Gaps ........................................................................................................... 13

CHAPTER THREE ...................................................................................................................... 14

RESEARCH METHODOLOGY.................................................................................................. 14

3.0 Introduction ...................................................................................................................................... 14

3.1 Research Design ................................................................................................................................ 14

3.2 Study Locale or Sampling Frame ....................................................................................................... 15

v

3.3 Target Population.............................................................................................................................. 15

3.4 Sampling Procedures and Sample Size ............................................................................................. 16

3.5 Research Instruments ....................................................................................................................... 17

3.5.1 Financial Awareness Interview Schedules for the Poor in Kooje Slums of Meru Town ............ 17

3.5.2 Financial Awareness Questionnaires for the Poor in Kooje Slums of Meru Town .................... 18

3.6 Piloting .............................................................................................................................................. 18

3.6.1 Validity ....................................................................................................................................... 18

3.6.2 Reliability .................................................................................................................................... 19

3.7 Data Collection Procedures ............................................................................................................... 19

3.8 Methods of Data Analysis ................................................................................................................. 20

3.9 Logistical and Ethical Issues .............................................................................................................. 20

CHAPTER FOUR ......................................................................................................................... 21

4.0 DATA PRESENTATION AND ANALYSES ....................................................................... 21

4.1 Respondent’s Background Information ............................................................................................ 21

4.1.1 Response Rate Analysis .............................................................................................................. 21

4.1.2 Response Analysis Based on Age ............................................................................................... 22

4.1.3 Level of Formal Education .......................................................................................................... 22

4.1.4 Employment Status .................................................................................................................... 23

4.2 Financial Awareness Levels ............................................................................................................... 24

4.2.1 Use of a Budget .......................................................................................................................... 24

4.2.2 Information on Treasury Bills and Bonds ................................................................................... 25

4.2.2 Knowledge on Financial Products .............................................................................................. 26

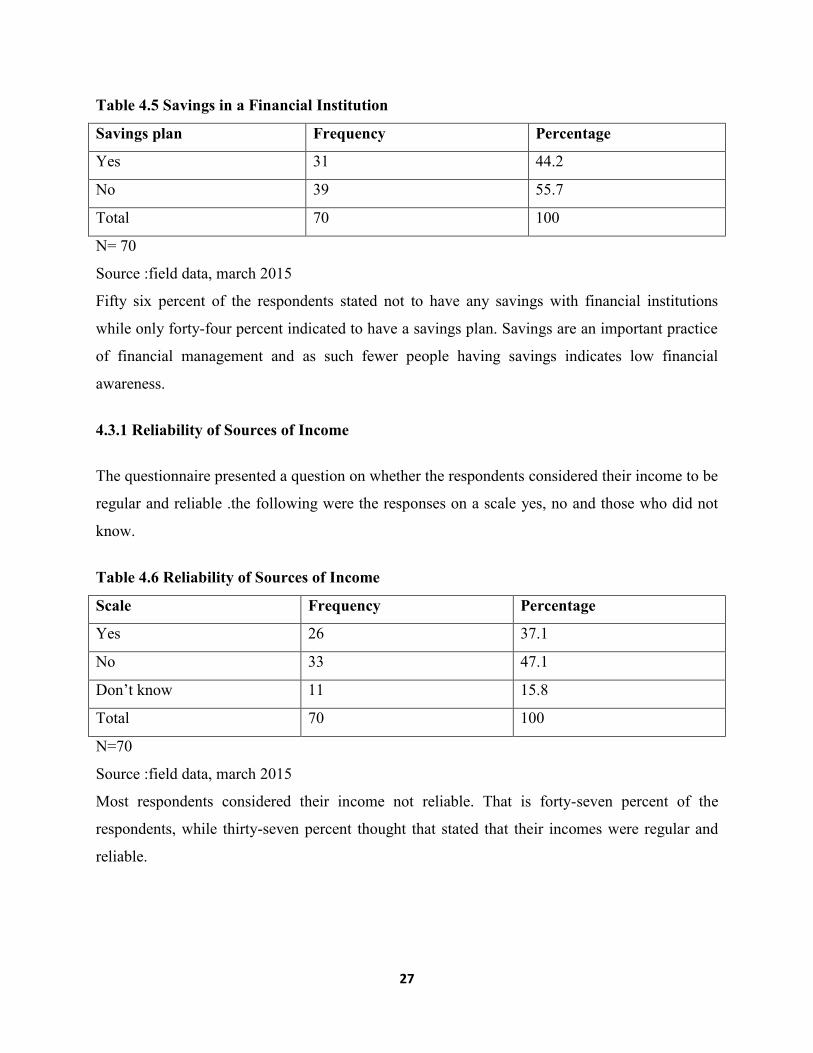

4.3 Savings in Financial Institutions ........................................................................................................ 26

4.3.1 Reliability of Sources of Income ................................................................................................. 27

4.3.2 Income levels ............................................................................................................................. 28

4.3.3 How long the Respondents would survive without their major Source of Income. .................. 28

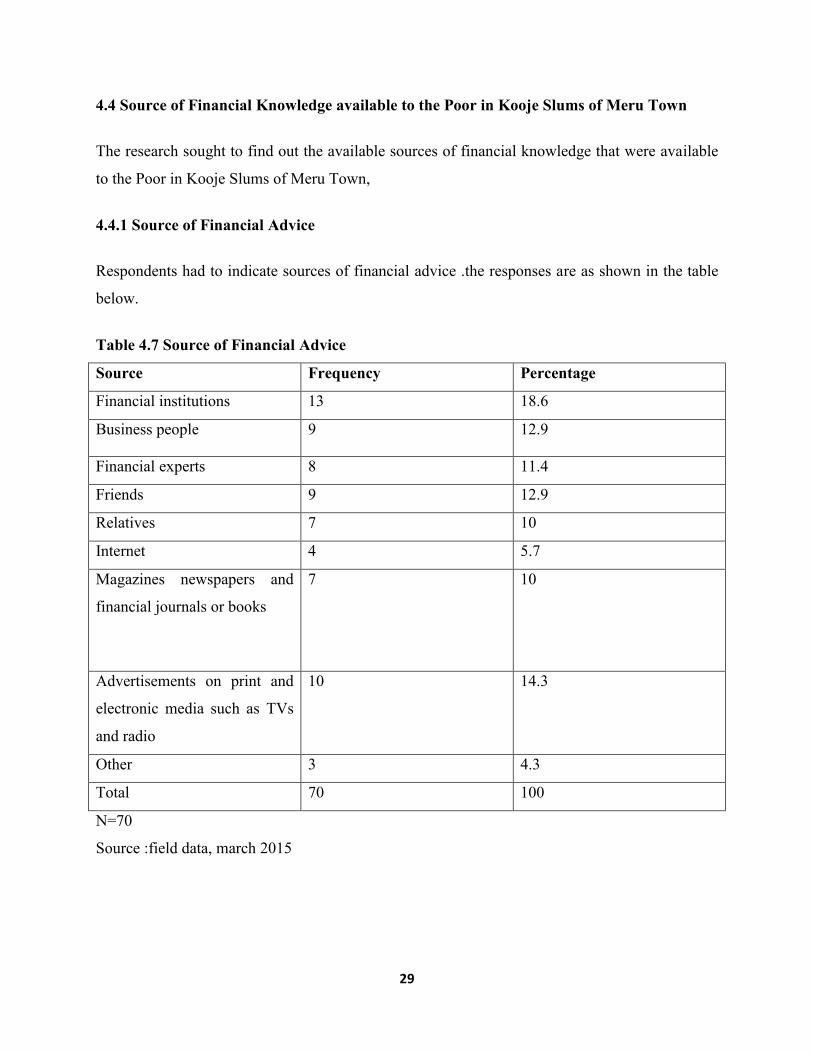

4.4 Source of Financial Knowledge available to the Poor in Kooje Slums of Meru Town ...................... 29

4.4.1 Source of Financial Advice ......................................................................................................... 29

4.4.2 Attendance of Financial Management Training ......................................................................... 30

4.4.3 Preferred Modes to Learn Financial Management. ................................................................... 30

4.5 Responses from the Interview Schedules. ........................................................................................ 30

4.5.1 Responses on Financial Topics covered in Financial Training .................................................... 31

4.5.2 Responses on Financial Product Information ............................................................................ 31

vi

4.5.3 Responses on understanding of the Financial Products ............................................................ 31

CHAPTER FIVE .......................................................................................................................... 32

SUMMARY CONCLUSIONS AND RECOMMENDATIONS ................................................. 32

5.0 Introduction ...................................................................................................................................... 32

5.1 Summary of Main Findings ............................................................................................................... 32

5.1.1 Level of Financial Awareness among the Poor in Kooje Slums of Meru Town .......................... 32

5.1.2 Savings in a Financial Institution among the Poor in Kooje Slums of Meru Town ..................... 33

5.1.3 Source of Financial Knowledge available to The Poor in Kooje Slums of Meru Town ............... 33

5.2 Conclusions ....................................................................................................................................... 33

5.3 Recommendations ............................................................................................................................ 34

5.4 Suggestions for further Research ...................................................................................................... 35

REFERENCES ............................................................................................................................. 36

APPENDIX 1:QUESTIONNAIRE .............................................................................................. 38

APPENDIX II: INTERVIEW SCHEDULE ................................................................................. 41

APPENDIX III: RESEARCH SCHEDULE ................................................................................. 43

APPENDIX IV: RESEARCH BUDGET ..................................................................................... 44

APPENDIX VI: INTRODUCTORY LETTER ............................................................................ 45

vii

LIST OF FIGURES

Figure 2.1 Conceptual Framework................................................................................................11

Figure 4.1 Employment Status ...................................................................................................... 24

Figure 4.2 Use of a Budget ........................................................................................................... 25

Figure 4.3 Information on Treasury Bills And Bonds .................................................................. 25

Figure 4.4 Income Levels ............................................................................................................. 28

Figure 4.5 How long the respondents would survive without their major source of income ....... 28

Figure 4.6 Attendance of Financial Management Training .......................................................... 30

Figure 4.7 Preferred Modes to learn Financial Management ....................................................... 30

viii

LIST OF TABLES

Table 3.1 Target Population of Kooje

Slum……………………………...................................................................................................26

Table 3.2 Sample Individuals to be Selected ................................................................................ 27

Table 4.1 Response Rate Analysis ................................................................................................ 25

Table 4.2 Response Analysis Based on Age ................................................................................. 25

Table 4.3 Level of Formal Education ........................................................................................... 28

Table 4.4 Knowledge on Financial Products ................................................................................ 28

Table 4.5 Savings in a Financial Institution.................................................................................. 37

Table 4.6 Reliability of Sources of Income .................................................................................. 37

Table 4.7 Table 4.7 Source of Financial

Advice………………….………………………………………………………………………...39

ix

ABBREVIATIONS AND ACRONYMS

MFIs refers to Micro-finance Institutions

Sacco’s refer to Savings and Credit Cooperative Unions.

ASIC refers to Australian Securities and Investments Commission

OECD refers to Organization for Economic Co-operation and Development.

ANZ refers to Australia and New Zealand Banking Group.

NGO refers to Non-Governmental Organizations

x

ABSTRACT

This research study was designed to investigate ways to improve financial awareness among the

poor in Kooje Slums of Meru town as the poor face a myriad of financial challenges that

includes financial access problems and low financial awareness The purpose of the study was to

find out financial awareness challenges faced by the Poor in Kooje Slums of Meru Town and

find out ways to improve their financial awareness The main objectives of the study were to find

out the level of financial awareness among the Poor in Kooje Slums of Meru; to find out the

number of people in Kooje slums of Meru town have a Savings plan with a financial institution

in Meru;to find out the source of financial knowledge available to the Poor in Kooje Slums of

Meru Town; The literature review of this study addressed the relationship between literacy levels

and financial awareness, ease of access to financial services and the understanding of the

financial landscape of the poor from research literature globally narrowing down to Africa and

finally reviewing Kenyan past research literature.

The research was done in Kooje Slums of Meru Town and it involved a sample of 90

respondents. The study used descriptive research design and survey research design. Both

qualitative and quantitative research techniques were employed. Data was collected by use of

questionnaires and interview schedules that were administered to the respondents by the

researcher. quantitative Data was analyzed using descriptive statistics and findings presented in

tables ,figures and percentages, pie charts and bar graphs. Qualitative data was organized into

themes based on the research objectives from which the researcher evaluated the usefulness of

the data in answering the research questions.

The researcher analyzed the field data collected with the aim of answering the research

questions. The findings were summarized and the researcher made the conclusions and

recommendations.Finally the researcher concluded that the respondents financial awareness was

low and their financial skills were poor. The researcher recommended for the stakeholders

including the government and financial institutions to carry out financial awareness campaigns

,incorporate financial management subjects at every level of school curriculum and provide

financial training to the poor.

1

CHAPTER ONE

INTRODUCTION AND BACKGROUND TO THE STUDY

1.1 Background to the Problem

‘failing to plan is planning to fail’, this popular quote attributed to Benjamin Franklin(the father

of time management) may sound like music to our ears but the importance of financial awareness

planning cannot be underestimated in solving our societal social and economic problems.

Financial awareness is beneficial both to the poor and the wealthy in the society. Financial

prosperity does not come easy but through strategic initiatives that are inclusive of the

marginally poor communities in the society. Fostering a culture of financial planning is one of

such an initiative

“[financial education] … can help to inculcate individuals with the financial knowledge

necessary to create household budgets, initiate savings plans, and make strategic

investment decisions. Such financial planning can help families meet near term

obligations and maximize their longer term well-being and is especially valuable for

populations that have traditionally been underserved by our financial system.”

(Alan Greenspan, 2002)

Poor people in Kenya share the same goals as all people, economic security for themselves, their

families, and future generations. The main difference is that they have lesser resources and

chances in life. Most live in high-risk and unpredictable environments (Rutherford 2000).

Compared to others, they have less money. Thus, managing the little money that they have is

very important. Financial management is critical for meeting daily needs, dealing with life cycle

events and unexpected emergencies, taking advantage of opportunities when they present

themselves, and planning for the future (Rutherford, 2000).

Building assets is important for poor people in Kenya because they provide the basis for

economic security. Common ways that poor people build assets are through savings, and

investments in land, businesses, and housing. They also build assets by investing in children‟s

education, health, and the maintenance of reciprocal social relationships that provide support in

2

times of need. Good money management is critical to the process of accumulating all kinds of

assets and preserving them. Access to appropriate financial products and services, along with the

financial skills to manage these resources well, are key to the process of asset accumulation

(Cohen and Sebstad, 2003).

For some years now, training in cash flow management and record keeping was integral to many

microenterprise programs involving credit. Since then, with the widespread adoption of

minimalist microfinance approaches, many business development services beyond financial

services have been dropped. However, as microfinance markets become more competitive and

financial portfolios more complex, many clients find themselves juggling an array of financial

products that they do not fully understand. They lack skills to cost out individual products, assess

their best use, and compare alternatives. Henceforth, determining appropriate financial strategies

to achieve investment and other economic goals becomes little more than guesswork (Cohen and

Sebstad, 2003).

The promotion of financial literacy in developing countries is timely and can be a win-win

situation for poor people and financial service providers alike. It can help poor people build

assets and create wealth. Financial literacy skills can be applied in managing a wide range of

individual, household, business, and community resources. Moreover, once people have acquired

financial literacy skills, they cannot be taken away. A one-time course in financial awareness can

have longer-term, even permanent, benefits.

At a basic level, good money management involves keeping a little money aside when it comes

in, avoiding unnecessary expenditure, and finding a safe place to store what is left over. In this

respect, poor people are like everyone else. But they are at a disadvantage because they lack

access to many formal financial institutions such as banks, insurance companies, and government

systems of social protection (Rutherford 2000; Lund and Srinivas 2000).

However, poor people do not lack access to finance altogether. Diversity and complexity perhaps

best describes the financial landscape of poor people. Their financial services, largely invisible to

the surveyor of formal financial systems, are provided through family, friends, moneylenders,

pawnshops and a wide range of informal systems. A growing number of poor people throughout

3

Kenya also have access to semi-formal financial services through microfinance institutions and

Sacco‟s. Together they make up significant networks of savings, credit and insurance services.

These systems typically provide small sums of money, often, as little as one hundred Kenya

shillings. While these informal and semi-formal systems are innovative and in many cases

responsive to people‟s needs, they are far from perfect. Informal systems can be expensive,

insecure, and inaccessible to some groups. They can be inefficient and inadequate in providing

enough money when it is needed (Murdoch 1999). Nevertheless, these informal financial

systems play an important role in the financial lives and money management strategies of the

poor.

1.2 Statement of the Problem

This research study attempted to make a case for financial literacy for the Poor in Kooje Slums

of Meru Town and proposed an agenda for action. In essence this research aimed to explore how

financial planning, good money management and financial awareness can help improve lives and

promote development among the Poor in Kooje Slums of Meru Town in tackling the following

problems:

The poor in slums face a myriad of challenges that span from financial awareness access

problems to practical issues such as complexity to obtain credit, loans and other financial

services such as insurance pension schemes and housing mortgages from major financial

institutions.

Inadequate participation of the poor in economic decision making in the country leads to them

having low knowledge about what they can do to improve their lives, not knowing what financial

packages from government they can invest in?, the available financing that they can obtain from

low interest government funds?, and the utilization of such funds?

The poor face challenges such as inability to access and obtain credit facilities poor credit ratings

poor savings plan mismanagement of financial resources, uninformed investment plans and poor

investment decisions

4

1.3 Purpose of the Study

The purpose of the study was to find out financial awareness challenges faced by the Poor in

Kooje Slums of Meru Town and find out ways to improve their financial awareness. To teach

people concepts of money and how to manage it wisely and to enable people to become more

informed financial decision makers, develop awareness of personal financial issues and choices,

and learn basic skills related to earning, spending, budgeting, saving, borrowing, and investing

money, and to help people set financial goals and optimize their financial options.

1.4 Study Objectives

1. To find out the level of financial awareness among the Poor in Kooje Slums of Meru

2. To find out the number of people in Kooje slums of Meru town have a Savings plan with

a financial institution in Meru?

3. To find out the source of financial knowledge available to the Poor in Kooje Slums of

Meru Town

1.5 Research Questions

1. What is the level of financial awareness among the Poor in Kooje Slums of Meru Town?

2. What is the number of people in Kooje Slums of Meru Town who have savings with

financial institutions in Meru Town?

3. What is the source of financial knowledge available to the Poor in Kooje Slums of Meru

Town?

1.6 Significance of the Study

In today‟s economic uncertainty it is imperative that individuals possess both the financial

knowledge and capability to make sound financial decisions.

Financial literacy may be considered a vital skill for all consumers. Financial literacy is also

crucial for more developed economies, to help ensure consumers save enough to provide an

adequate income in retirement while avoiding high levels of debt that might result in bankruptcy

and foreclosures

5

The information available on consumer financial literacy is worrying for two reasons – not only

do individuals generally lack an adequate financial background or understanding to navigate

today‟s complex market, but unfortunately they also generally believe that they are far more

financially literate than is really the case.

Financial awareness for the poor can lead to wealth creation thereby benefiting both the wealthy

and the poor. This is a win-win case for the society.

1.7 Limitations and Delimitations of the Study

Language barrier

Communicating to respondents who were not fluent in Swahili and English is likely to put a

stumbling block on the research at the time of data collection, especially as the researcher‟s

native language was Luhya rather than the local Meru dialect. Translators from within the

community were sought to help in bridging the language barrier.

Unwillingness of family heads and residents to provide data

Family heads and slum residents were reluctant to provide information in regard to their earnings

their consumption behavior spending patterns and savings. To cover against this limitation

efforts were made to ease up the respondents to willingly provide data like ensuring them of

confidentiality.

Delimitation: the study was limited to an area that was manageable under the objectives laid out

and formed a strong basis for societal welfare improvement.

1.8 Assumptions of the Study

The residents had poor financial awareness that caused them to make uninformed financial

choices. This may have happened due to marginalizing of the poor in financial decisions

The financial knowledge that was passed on to the residents was from unreliable sources that

distorted or misrepresented the financial concepts that would benefit them.

6

The poor residents were hugely disadvantaged in accessing financial services by the financial

systems that were in place. That such systems may have discriminate on the basis of income

levels, perceived risk and target markets for their investments not taking the poor into account.

The area under study depicts the same conditions and characteristics that exist in other Kenyan

slums such as Kibera in Nairobi and Mathare in Nairobi. Any differences existing were

substantially insignificant and not massive to the extent of causing huge research or study

differences.

1.9 Definitions of Operational Terms

The poor refers to the low income residents of Kooje slums, Meru town. People who live below

$1.5 per day (world bank group)

Saving: refers to the difference between disposable income and consumption.

Investment: according to Wikipedia, in economics, investment is the accumulation of newly

produced physical entities, such as factories, machinery, houses, and goods inventories.

In finance, investment is buying or creating an asset with the expectation of capital appreciation,

dividends (profit), interest earnings, rents or some combination of these returns

1.10 Summary

The first chapter introduced the research‟s main issues, scope and the reason for its undertaking.

The chapter introduces topics of good money management, financial awareness programs and

financial literacy importance to society. It has further set the foundation for a great deal of time

to be committed in improving financial awareness research in the region under study through

laying out the objectives and significance of the study.

7

CHAPTER TWO

REVIEW OF RELATED LITERATURE

2.1 Introduction

There has been quite a number of research work, journals, articles and policy briefings on

financial awareness all aimed at improving financial literacy. Note that financial literacy is

different from financial awareness as depicted in the literature review where financial awareness

are the measure that provide solutions to low financial literacy. The literature reviewed

encompasses personal finance activities such as cash flow management, credit management,

savings and investments. The review seeks to clarify on financial awareness levels relationship to

the making of poor financial decisions and how the people can access better information on

finance thereby improve their economic livelihoods as shown by other authors and also reveal

gaps that exist in their studies.

The organization for economic co-operation and development (OECD) (2005) broadly defines

financial education„ as follows: financial education is the process by which financial

consumers/investors improve their understanding of financial products and concepts and,

through information, instruction and/or objective advice, develop the skills and confidence to

become more aware of financial risks and opportunities, to make informed choices, to know

where to go for help, and to take other effective actions to improve their financial wellbeing. And

on the other hand, according to ASIC (2008) consumer and financial literacy is the application of

knowledge, understandings, skills and values in consumer and financial contexts and the related

decisions that impact on self, others, the community and the environment.

2.1.1 Relationship between Literacy Levels and Financial Awareness

Campbell (2006) argues that with financial education poor financial decisions are likely to be

reconciled with economic theory given that households have been found to make sub optimal

decisions which deviate from what economic theory suggests. Campbell further ´concludes that

households with higher education levels (high school, college, graduate school) are likely to be

more active in capital markets due to reduced information asymmetry through regression

8

evidence, higher education levels were found to be significantly related to equity ownership by

households. Educated Swedish households were found to diversify their portfolios more

efficiently than less educated households. In conclusion, poorer and less educated households

were found to have a higher probability of making mistakes than wealthier and better educated

households (Wachira and Kihiu, 2012).

(Wachira and Kihiu, 2012) acknowledge that financial literacy is low in Kenya. Their research

titled “impact of financial literacy on access to financial services in Kenya” suggests for further

research to be done on ways to improve financial literacy in Kenya. Their research on low

financial literacy levels are echoed by the OECD that found poor people scoring poorly on

financial literacy test

2.1.2 Ease of Access to Financial Services

Australia„s financial literacy study, the ANZ survey of adult financial literacy survey 2008 found

out that the “lowest levels of financial literacy are associated with: people with lower levels of

education (year 10 or less) people not working (for a range of reasons) or in unskilled work

people with lower incomes”. This highlighted the plight of the poor and those with low education

as those who have low financial awareness.

According to Wachira & Kihiu(2012) they found out that in particular the probability of an adult

Kenyan accessing formal and semi-formal financial services which are relatively cheaper and

more sustainable compared to the usurious and frequently resource starved services of the

informal sector stood at 6.24% and 39.35% respectively in 2009. For the informal strand, the

probability stood at27.72% in 2009 down from 35.7% in 2006 while for those who are totally

excluded from any form of financial service, the probability stands at 26.69%, and as such these

data showed prevalence of low rates of access to finance to be low in Kenya.

According to ASIC (2011) consumers often overestimate how much they know. In their

Australian survey, they found out that 67% of those taking part claimed to understand the

concept of compound interest but only 28% could find the correct answer to a problem using the

concept. So before they can even start work on providing financial education to their citizens,

governments need to persuade them it is needed

9

2.1.3 Understanding the Financial Landscape of the Poor

According to ASIC (2005) “while some people don„t rely on any information sources, most

people rely on a wide range of information and advice services when researching financial

decisions and/or trying to gain financial knowledge, including informal sources (e.g. Family and

friends, newspapers) and formal sources (e.g. Financial advisers/accountants and product

providers)”. The “some” people that ASIC refers to as not to rely on any information services

represent the bulk of the poor people who need to be imparted with financial awareness. Perhaps

more worryingly, consumers often overestimate how much they know. In an Australian survey

ASIC 2005, 67% of those taking part claimed to understand the concept of compound interest

but only 28% could find the correct answer to a problem using the concept.88% thought they

understood savings while actually only 69% did understand savings, furthermore 90% thought

they were conversant with budgeting yet only 57% were conversant with budgeting: so before

they can even start work on providing financial awareness to their citizens, governments need to

persuade them it is needed( OECD ,2006).

2.2 Theoretical Framework

The researcher with an overview of theoretical research which casts financial knowledge as a

form of investment in human capital. Jappelli and Padula (2011) theoretically take a two-period

model but additionally sketch a multi-period life cycle model with financial literacy

endogenously determined. They assume that life of consumers covers two periods, they earn

income(y) in period 0 and live in retirement in period 1. At the beginning of period 0 they are

endowed with financial literacy, here financial literacy is related to schooling decisions and

parental background. They conclude that holding financial literacy endogenously investment in

financial literacy raises asset returns though at a decreasing rate. They predict that financial

literacy and wealth will be strongly correlated over the life cycle, with both rising until

retirement and falling thereafter. They also suggest that, in countries with generous social

security benefits, there will be fewer incentives to save and accumulate wealth and, in turn, less

reason to invest in financial literacy.

10

Existing empirical evidence shows that adults in both developed and emerging economies who

have been exposed to financial education are subsequently more likely than others to save and

plan for retirement (Bernheim et al., 2001; Coleet al., 2011; Lusardi, 2009). This evidence

suggests a possible causal link between financial education and outcomes and indicates that

improved levels of financial literacy can lead to positive behavior change. Moreover, those who

have greater financial knowledge are more likely to accumulate higher amounts of wealth

(Lusardi and Mitchell, 2011).

Financial literacy is important to economic and financial stability for a number of reasons.

Financially literate consumers can make more informed decisions and demand higher quality

services, which will encourage competition and innovation in the market. They are also less

likely to react to market conditions in unpredictable ways, less likely to make unfounded

complaints and more likely to take appropriate steps to manage the risks transferred to them. All

of these factors will lead to a more efficient financial services sector and potentially less costly

financial regulatory and supervisory requirements. They can also ultimately help in reducing

government aid and taxation aimed at assisting those who have taken unwise financial decisions

or no decision at all (PISA, 2012)

11

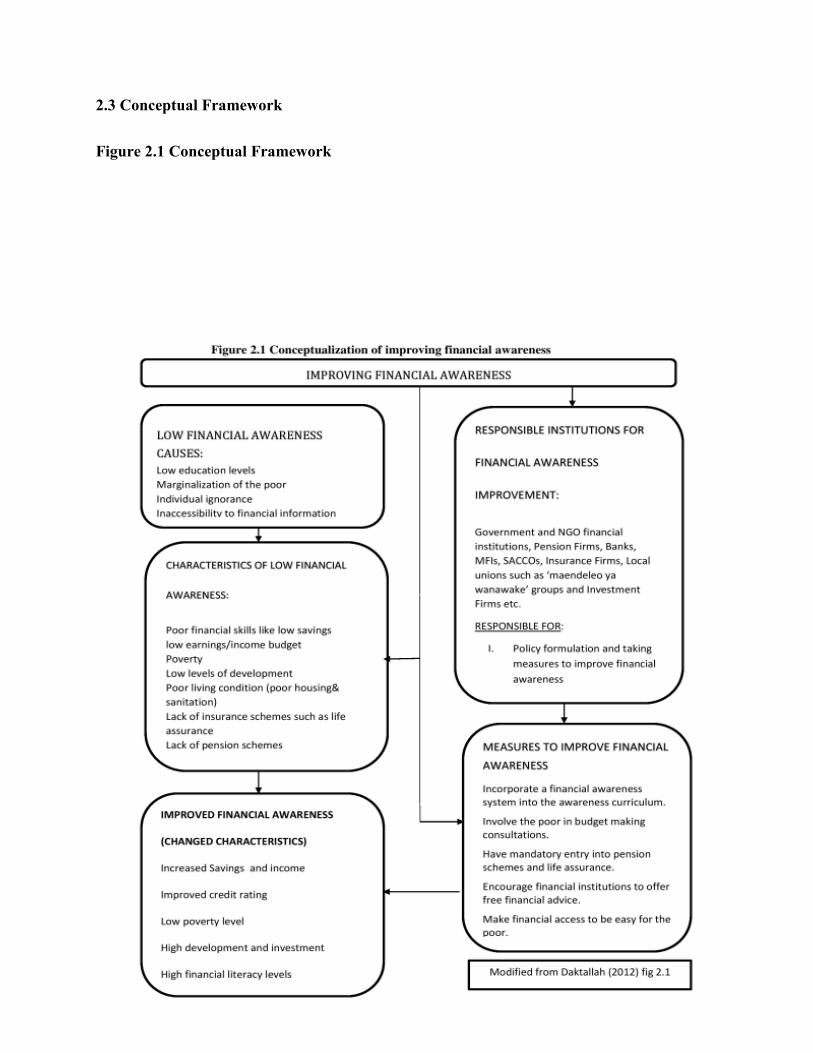

2.3 Conceptual Framework

Figure 2.1 Conceptual Framework

12

The reviewed literature provided the framework for the construction of the conceptual

framework as shown above in fig 1 .on the left of the central flow line there is depiction of low

financial awareness levels and their perceived causes as per the literature review, then the from

the flow from causes of low financial awareness goes to characterize what you expect to find

among a people who have low financial awareness. From this point improving financial

awareness comes into play so as to change these characteristics of low financial awareness.

Focus now changes over to the right side where we find responsible institutions for improving

financial awareness through policy formulation and adopting necessary measures to tackle low

financial awareness. Then there is the flow to the measures that can be taken to improve financial

awareness.it is expected that the listed measures will improve the characteristics of the areas with

low financial awareness.

The study splits variables into dependent and independent variables. The independent variables

include government policies, financial institutions policies, financial awareness and incomes of

the poor and financial literacy in general. On the other hand dependent variables include savings,

investments, development levels, poverty index, literacy levels, living conditions and financial

satisfaction. To improve financial awareness among the poor there is need to alter the

independent variables in such a manner that the resultant effect will be the desired condition that

we expect among the poor.

The suggested measures in the conceptual framework are as per the literature review. There is

need for more research to be conducted to investigate the other possible ways or means by which

we can improve the financial awareness across all the poor people who are hampered by

inaccessibility to financial information and services.

13

2.5 Summary of Knowledge Gaps

The study dealt with financial awareness among the Poor in Kooje Slums of Meru Town.

Financial awareness has quite a number of research materials pertaining as to the subject of

financial literacy issues. They both explore challenges that occur due to low financial literacy,

how to improve financial literacy, making cases for how important it is that financial awareness

is relevant for the society‟s economic wellbeing and some trying to measure financial literacy

and identify areas that have low financial literacy and how they are characterized and how

different they are from areas characterized with high financial literacy brought about by financial

awareness.

Although there was research material on this area of study, there was no research material that

had covered issues of financial awareness among the poor. As stated before, the financial

landscape of the poor was different dynamic and most risky of all to make decisions. The ANZ

makes a case for financial awareness among the poor but fail to accurately come out with means

by which their financial awareness can be improved so that they lead better lives than they are

living.

According to Wachira and Kihiu (2012), they recognized that financial literacy levels were very

low and that their needs to be an adoption of effective measures to try and raise financial

awareness .nevertheless there was an inadequate elaboration of the measures that they expected

financial institutions ,governments and individuals to take to improve their financial literacy.

All the above theories reflected on financial awareness issues, their importance to individuals

and nation. But none had outlined specifically how to deal with improving financial awareness

among the poor. Thus there was need to come up with measures that were pro-poor and

sustainable.

14

CHAPTER THREE

RESEARCH METHODOLOGY

3.0 Introduction

The chapter comprises the techniques and procedures used in carrying out the study. It gives a

detailed description of the research design, study locale or sampling frame, target population,

sampling procedures and sample size for data collection, research instruments to be used,

piloting of research instruments, data collection procedures, methods of data analysis and logical

and ethical issues to be observed while carrying out the study.

3.1 Research Design

Research design is defined as the arrangement of conditions of collecting and analyzing data in a

manner that aims to combine the relevance to the research purpose with economy procedure.it is

a systematic plan to tackling the research.

The study used descriptive research design. Both qualitative and quantitative research techniques

were employed. Descriptive research design was deemed appropriate to study ways to improve

financial awareness among the Poor in Kooje slums because:

First the study took place in a real- world situation, where it was impossible to separate the

process (improving financial awareness) from the setting (Kooje slum) in which it took place.

The inability to separate the process from the context implied that the researcher had no control

over the behavior of events.

Secondly, financial awareness as an on-going process meant that, the process of improving

financial awareness taking place in these slum settlements was relatively contemporary. These

thus, unearthed the various development dimensions of the study as well as allowed lessons

learnt from the research to be used in theory formulation.

15

The applicability of descriptive research design in formulation of hypothesis made it an essential

research design that was useful in coming up with definitive answer to existing hypotheses and

gav definitive answers to disapprove existing hypotheses.

Descriptive research design also gave a general overview of what variables are worth testing

quantitatively. Therefore descriptive research design by pointing to quantitative research design

helped to get a good sense of what hypotheses were worth testing.

Under descriptive research design the study employed use of survey research design, historical

research design and observation research design. Survey research design entailed collecting data

from the population so as to determine the current state of the variables in the population.

3.2 Study Locale or Sampling Frame

The area of study was Kooje slums of Meru. Located within Meru municipality the area is

characterized by poor development, poverty illiteracy and poor living conditions that may be

characterized by low financial awareness. The choice of Kooje slums was justified as it may

provide solutions that are applicable in other informal settlements or slums in Kenya. Kooje area

is an area congested with more than 300 households. Water is very scarce because the entire

slum is served by only one water tap. There is also only one pit latrine which leads to use of

paper bags to dispose of waste throughout the slum. Lack of sanitation predisposes the residents

to diseases like cholera, dysentery and typhoid fever. Low education levels immensely contribute

to poor skills of resource management and development.

3.3 Target Population

The target population refers to the entire groups of individuals, events or objects having common

observable characteristic where the research is to be undertaken.

The population of this study comprised of poor people residing within Kooje Slums of Meru

Town. The population was estimated at 1000 residents. These comprised of the men and women

that reside within the study locality.

16

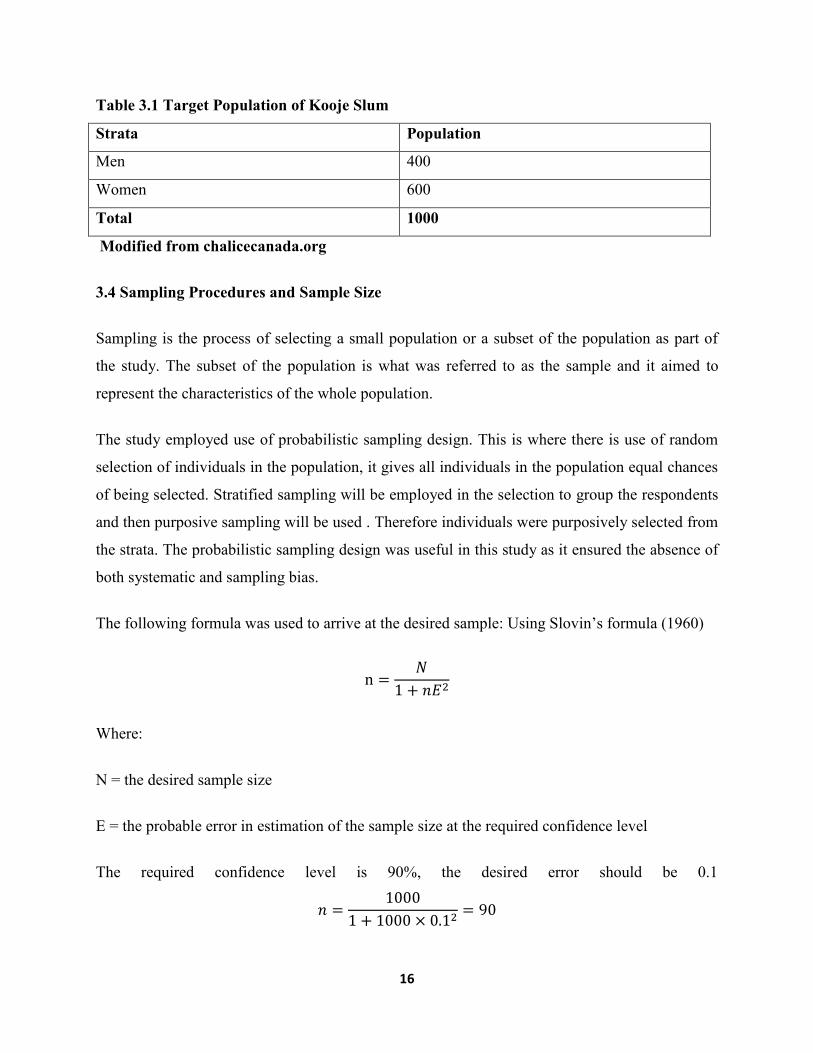

Table 3.1 Target Population of Kooje Slum

Strata Population

Men 400

Women 600

Total 1000

Modified from chalicecanada.org

3.4 Sampling Procedures and Sample Size

Sampling is the process of selecting a small population or a subset of the population as part of

the study. The subset of the population is what was referred to as the sample and it aimed to

represent the characteristics of the whole population.

The study employed use of probabilistic sampling design. This is where there is use of random

selection of individuals in the population, it gives all individuals in the population equal chances

of being selected. Stratified sampling will be employed in the selection to group the respondents

and then purposive sampling will be used . Therefore individuals were purposively selected from

the strata. The probabilistic sampling design was useful in this study as it ensured the absence of

both systematic and sampling bias.

The following formula was used to arrive at the desired sample: Using Slovin‟s formula (1960)

Where:

N = the desired sample size

E = the probable error in estimation of the sample size at the required confidence level

The required confidence level is 90%, the desired error should be 0.1

17

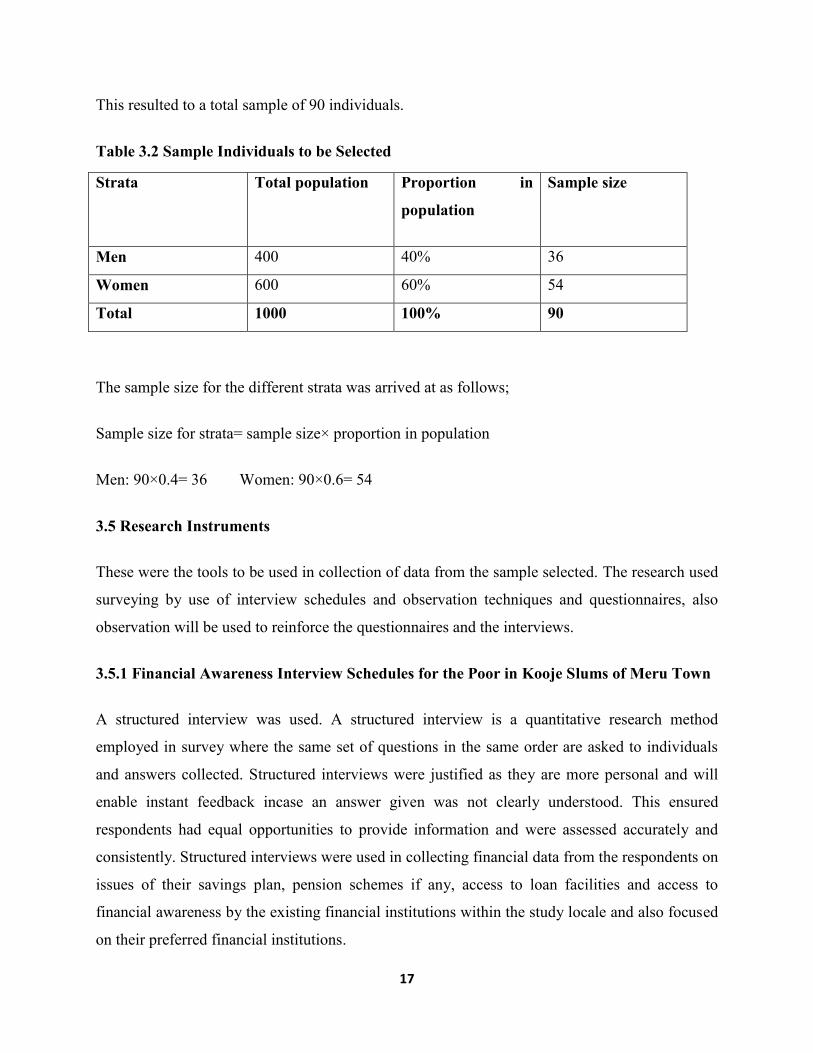

This resulted to a total sample of 90 individuals.

Table 3.2 Sample Individuals to be Selected

Strata Total population Proportion in

population

Sample size

Men 400 40% 36

Women 600 60% 54

Total 1000 100% 90

The sample size for the different strata was arrived at as follows;

Sample size for strata= sample size× proportion in population

Men: 90×0.4= 36 Women: 90×0.6= 54

3.5 Research Instruments

These were the tools to be used in collection of data from the sample selected. The research used

surveying by use of interview schedules and observation techniques and questionnaires, also

observation will be used to reinforce the questionnaires and the interviews.

3.5.1 Financial Awareness Interview Schedules for the Poor in Kooje Slums of Meru Town

A structured interview was used. A structured interview is a quantitative research method

employed in survey where the same set of questions in the same order are asked to individuals

and answers collected. Structured interviews were justified as they are more personal and will

enable instant feedback incase an answer given was not clearly understood. This ensured

respondents had equal opportunities to provide information and were assessed accurately and

consistently. Structured interviews were used in collecting financial data from the respondents on

issues of their savings plan, pension schemes if any, access to loan facilities and access to

financial awareness by the existing financial institutions within the study locale and also focused

on their preferred financial institutions.

18

3.5.2 Financial Awareness Questionnaires for the Poor in Kooje Slums of Meru Town

A questionnaire is a form containing a set of questions especially one addressed to a statistically

significant number of subjects as a way of gathering information for a survey. The questionnaire

is a research instrument that has a set of questions and specific prompts to enable one gather

information from respondents.

A questionnaire as a research instrument was justified because it was cheap and did not require

much effort from the researcher .it was also suitable as it contained standardized answers that

simplified data compilation. Questions provided focused on the availability of financial

awareness classes, loan facilities provided to them by financial institutions, knowledge of

financial markets, knowledge on pension schemes, insurance and life assurance. Questions also

were based on attendance of any financial training conducted in the area by any financial

institution.

3.6 Piloting

This is where the research instruments are pre tested prior to conducting data collection. The

research instruments undergo reliability and validity tests so as to enhance their effectiveness,

reliability and validity. It acts like a small scale preliminary study to evaluate feasibility, time,

cost, adverse events, and statistical variability in order to improve upon the study design. Piloting

was done on a small sample using convenience technique, this is where individuals with the

nearest individuals with the desired characteristics were found and included in the study to act as

a respondents for the already available research instruments. The participants mainly from

around Nchiru location were provided with questionnaires to fill and subjected to answer the

interview schedule questions. The research instruments were also reviewed by experts such as

the principal supervisor and recommendations obtained on how to improve on them.

3.6.1 Validity

The prepared questionnaire and a draft interview schedule were tested on a sample group other

than the actual sample. This improved understanding of the questionnaire and interview schedule

to the actual respondents as validity of questions and tested phenomena were tested and any

19

misinterpreted, confusing or misunderstood questions were corrected to pass the validity tests.

Internal validity of the research instruments were further improved by a thorough review of

related literature so as to ensure measured concepts and items were at par with the study

concepts.

3.6.2 Reliability

Reliability tests will aim to measure the consistency of results or data revealed by the research

instruments. Repeated tests will be done and research instrument questionnaire tested on other

groups other than the actual population to obtain different test results. Then these results will be

tested for correlation. Use of correlation coefficient r and coefficient of determination r2

will be

used to assess the reliability of the questionnaire responses. Also it is of importance to note that

the study focused on the behavior of the variables under study to reinforce the theoretical

assertions of the concepts under study abiding to propositions by other researchers findings

conducted under literature review.

3.7 Data Collection Procedures

Data was collected by the use of the mentioned research instruments. Questionnaires and

interview schedules were conducted on the study population.

Questionnaires were administered first by use of a research assistant read and explained to the

respondents the nature of the study. Where a respondent had limited understanding of English

language used in the questionnaire he/she was instructed in Swahili, in such cases the questions

were asked in the order that they are laid out in the questionnaire. Respondents were never put

under pressure to answer any questions. The research assistant then collected the responses and

records for data analysis to be made.

Interviews were conducted by use of telephone conversation and face to face where the

respondent were easily available. Interviews were performed at different times of the day and all

through the week. The interviewees were not forced or coerced to answer any question

unwillingly.

20

3.8 Methods of Data Analysis

Both qualitative and quantitative methods of data analysis were used. Descriptive analysis was

used to summarize the characteristics of the respondents, and relate them to data.

Quantitative data was analyzed by use of statistical measures such as mean or average,

frequency, ratios and percentages. Use of bar graphs, tabulation and pie charts will be used to

express the population characteristics in access to information financial services from banks ,

microfinance institutions, Sacco‟s and self-help groups. Other variables such as financial

awareness and saving patterns, financial awareness were tabulated and presented by use of

frequency tables.

3.9 Logistical and Ethical Issues

Logistical and ethical issues were part of the whole study from the beginning to the end. While in

the field research ethical issues were observed. All respondents were assured of confidentiality

on the data they provided. They were informed of the purpose of the research and justifications

were made to them as to why the study was being conducted. no payments were offered to any

participants of the research in line with the research guidelines on ethics.

In the field it was also ensured that all respondents were willing participants and agreed to be

subjected to the research instruments.

21

CHAPTER FOUR

4.0 DATA PRESENTATION AND ANALYSES

This chapter focuses on the analysis of data collected from kooje slums of meru town. The data

is analyzed based on the research hypothesis to come up with the findings of the study. This

analysis makes the base upon which summary and conclusions are drawn from. The data analysis

is done by use of descriptive analysis

4.1 Respondent’s Background Information

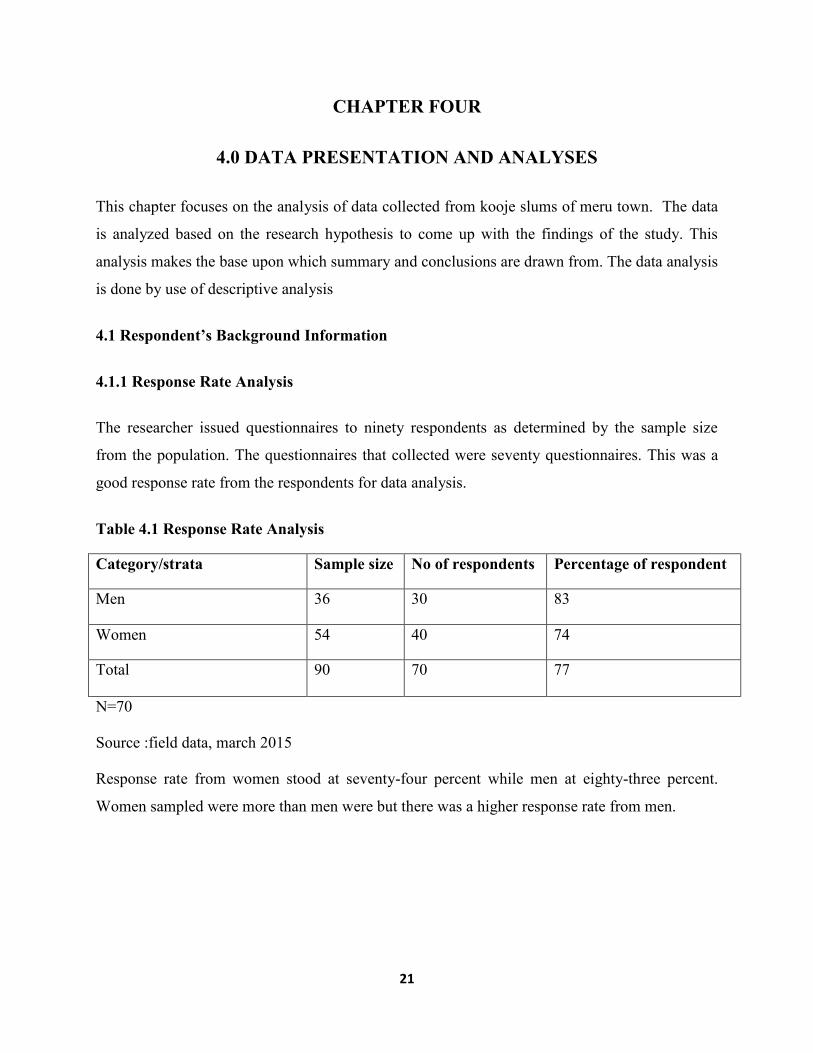

4.1.1 Response Rate Analysis

The researcher issued questionnaires to ninety respondents as determined by the sample size

from the population. The questionnaires that collected were seventy questionnaires. This was a

good response rate from the respondents for data analysis.

Table 4.1 Response Rate Analysis

Category/strata Sample size No of respondents Percentage of respondent

Men 36 30 83

Women 54 40 74

Total 90 70 77

N=70

Source :field data, march 2015

Response rate from women stood at seventy-four percent while men at eighty-three percent.

Women sampled were more than men were but there was a higher response rate from men.

22

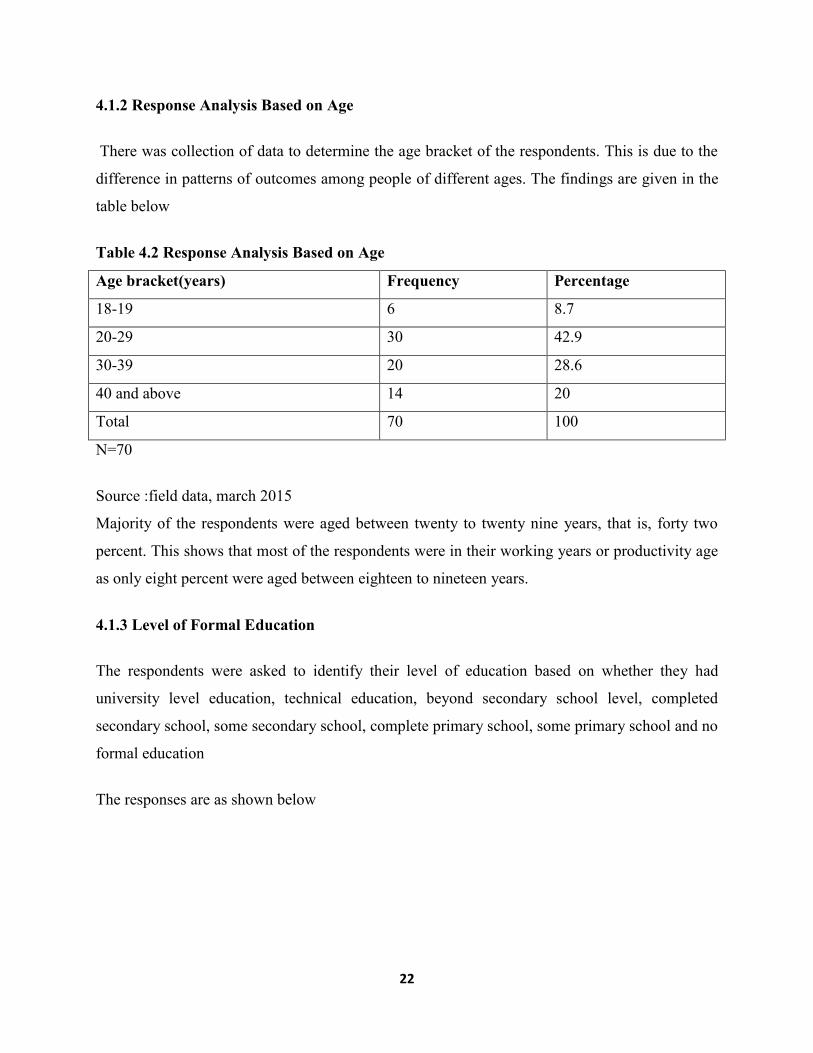

4.1.2 Response Analysis Based on Age

There was collection of data to determine the age bracket of the respondents. This is due to the

difference in patterns of outcomes among people of different ages. The findings are given in the

table below

Table 4.2 Response Analysis Based on Age

Age bracket(years) Frequency Percentage

18-19 6 8.7

20-29 30 42.9

30-39 20 28.6

40 and above 14 20

Total 70 100

N=70

Source :field data, march 2015

Majority of the respondents were aged between twenty to twenty nine years, that is, forty two

percent. This shows that most of the respondents were in their working years or productivity age

as only eight percent were aged between eighteen to nineteen years.

4.1.3 Level of Formal Education

The respondents were asked to identify their level of education based on whether they had

university level education, technical education, beyond secondary school level, completed

secondary school, some secondary school, complete primary school, some primary school and no

formal education

The responses are as shown below

23

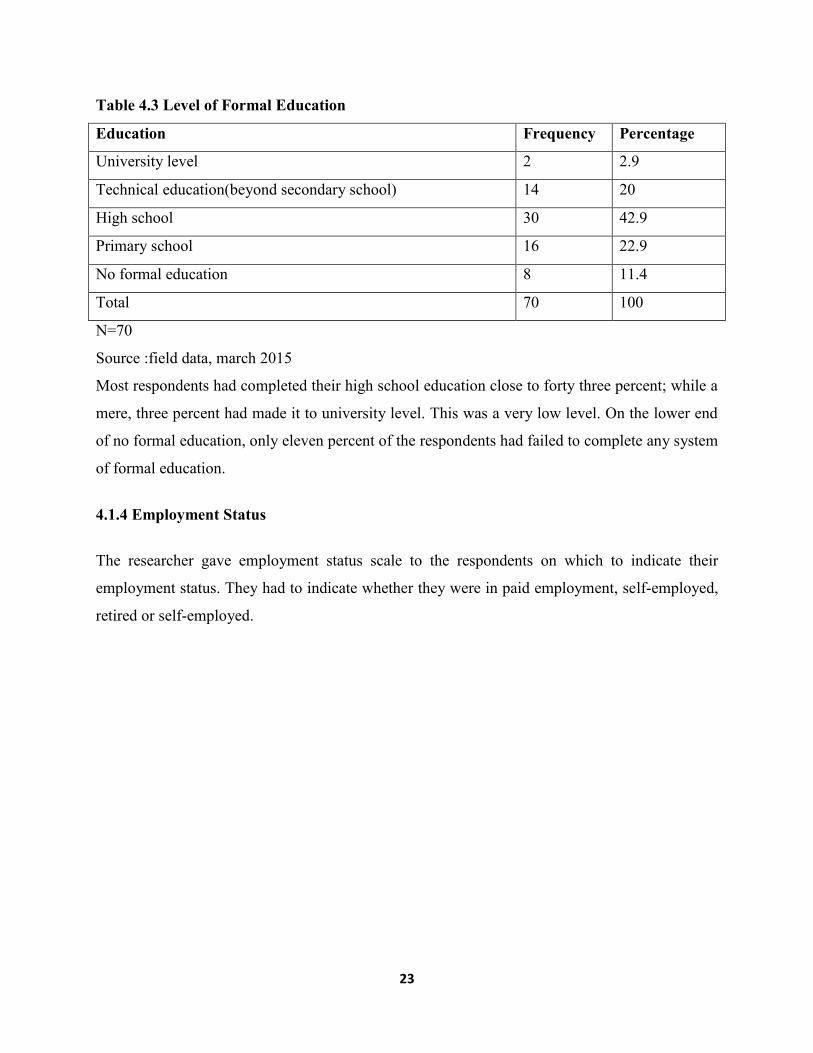

Table 4.3 Level of Formal Education

Education Frequency Percentage

University level 2 2.9

Technical education(beyond secondary school) 14 20

High school 30 42.9

Primary school 16 22.9

No formal education 8 11.4

Total 70 100

N=70

Source :field data, march 2015

Most respondents had completed their high school education close to forty three percent; while a

mere, three percent had made it to university level. This was a very low level. On the lower end

of no formal education, only eleven percent of the respondents had failed to complete any system

of formal education.

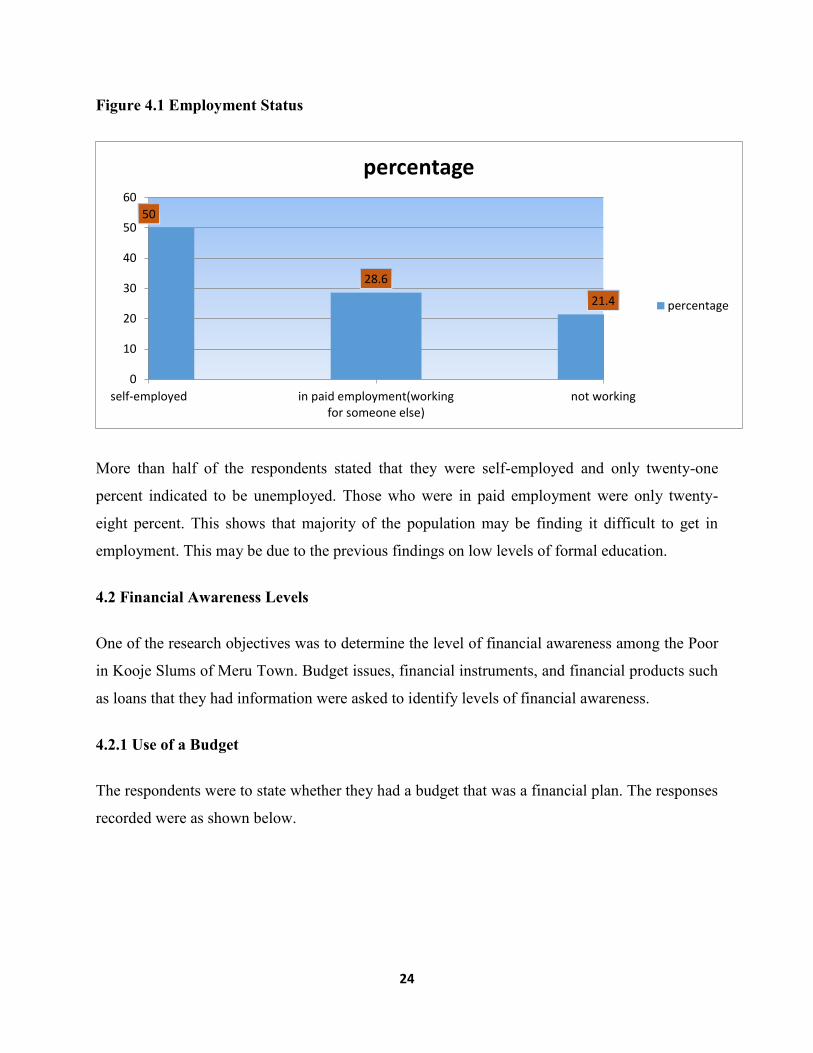

4.1.4 Employment Status

The researcher gave employment status scale to the respondents on which to indicate their

employment status. They had to indicate whether they were in paid employment, self-employed,

retired or self-employed.

24

Figure 4.1 Employment Status

More than half of the respondents stated that they were self-employed and only twenty-one

percent indicated to be unemployed. Those who were in paid employment were only twenty-

eight percent. This shows that majority of the population may be finding it difficult to get in

employment. This may be due to the previous findings on low levels of formal education.

4.2 Financial Awareness Levels

One of the research objectives was to determine the level of financial awareness among the Poor

in Kooje Slums of Meru Town. Budget issues, financial instruments, and financial products such

as loans that they had information were asked to identify levels of financial awareness.

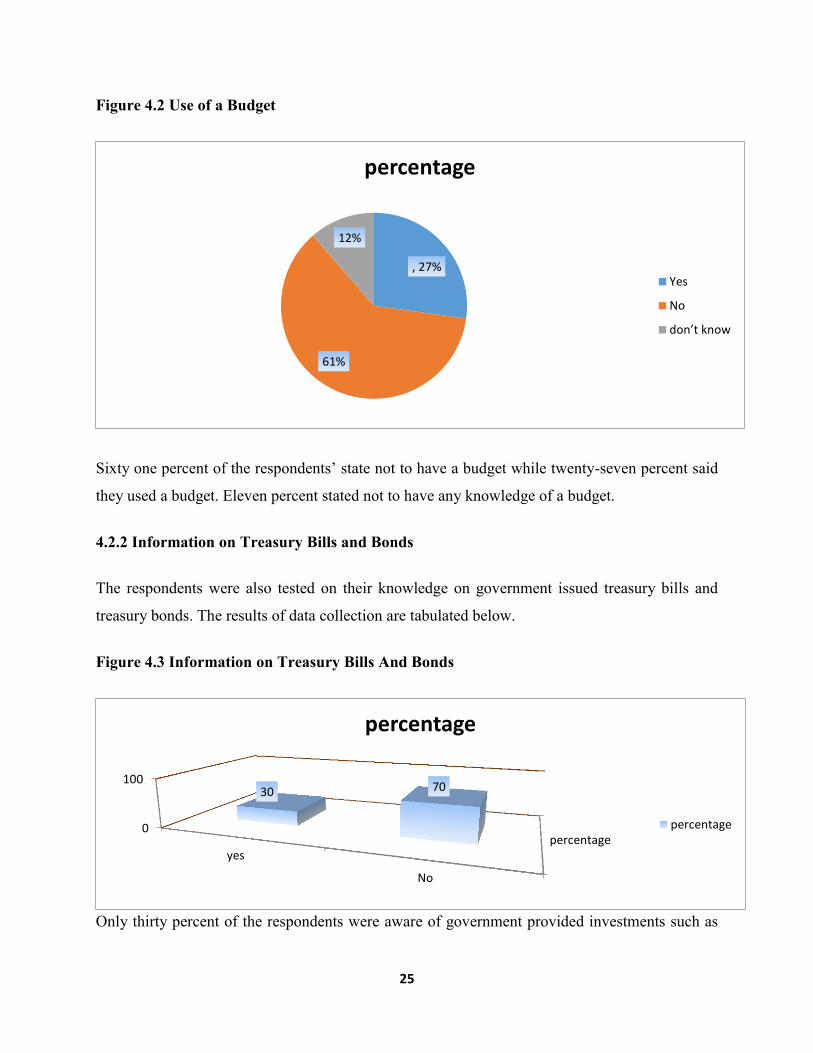

4.2.1 Use of a Budget

The respondents were to state whether they had a budget that was a financial plan. The responses

recorded were as shown below.

50

28.6

21.4

0

10

20

30

40

50

60

self-employed in paid employment(workingfor someone else)

not working

percentage

percentage

25

Figure 4.2 Use of a Budget

Sixty one percent of the respondents‟ state not to have a budget while twenty-seven percent said

they used a budget. Eleven percent stated not to have any knowledge of a budget.

4.2.2 Information on Treasury Bills and Bonds

The respondents were also tested on their knowledge on government issued treasury bills and

treasury bonds. The results of data collection are tabulated below.

Figure 4.3 Information on Treasury Bills And Bonds

Only thirty percent of the respondents were aware of government provided investments such as

, 27%

61%

12%

percentage

Yes

No

don’t know

percentage0

100

yes

No

30 70

percentage

percentage

26

treasury bills and mortgages. Seventy percent of the respondents did not know the treasury bills

and treasury bonds.

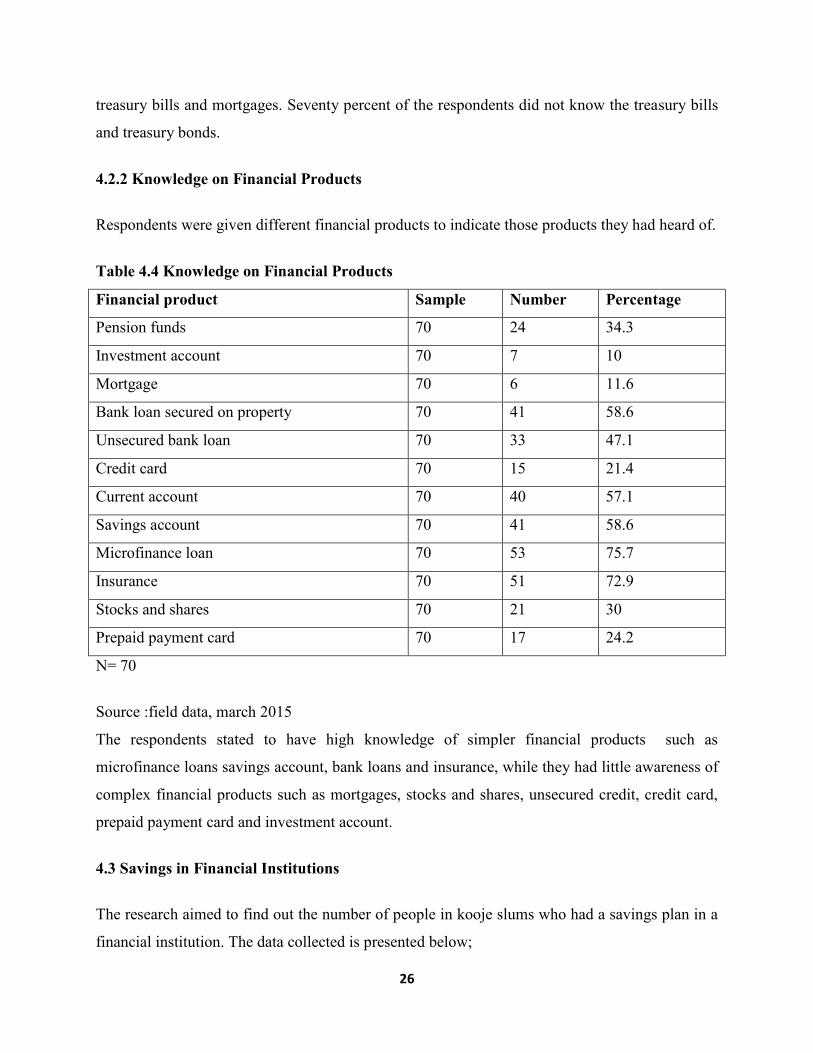

4.2.2 Knowledge on Financial Products

Respondents were given different financial products to indicate those products they had heard of.

Table 4.4 Knowledge on Financial Products

Financial product Sample Number Percentage

Pension funds 70 24 34.3

Investment account 70 7 10

Mortgage 70 6 11.6

Bank loan secured on property 70 41 58.6

Unsecured bank loan 70 33 47.1

Credit card 70 15 21.4

Current account 70 40 57.1

Savings account 70 41 58.6

Microfinance loan 70 53 75.7

Insurance 70 51 72.9

Stocks and shares 70 21 30

Prepaid payment card 70 17 24.2

N= 70

Source :field data, march 2015

The respondents stated to have high knowledge of simpler financial products such as

microfinance loans savings account, bank loans and insurance, while they had little awareness of

complex financial products such as mortgages, stocks and shares, unsecured credit, credit card,

prepaid payment card and investment account.

4.3 Savings in Financial Institutions

The research aimed to find out the number of people in kooje slums who had a savings plan in a

financial institution. The data collected is presented below;

27

Table 4.5 Savings in a Financial Institution

Savings plan Frequency Percentage

Yes 31 44.2

No 39 55.7

Total 70 100

N= 70

Source :field data, march 2015

Fifty six percent of the respondents stated not to have any savings with financial institutions

while only forty-four percent indicated to have a savings plan. Savings are an important practice

of financial management and as such fewer people having savings indicates low financial

awareness.

4.3.1 Reliability of Sources of Income

The questionnaire presented a question on whether the respondents considered their income to be

regular and reliable .the following were the responses on a scale yes, no and those who did not

know.

Table 4.6 Reliability of Sources of Income

Scale Frequency Percentage

Yes 26 37.1

No 33 47.1

Don‟t know 11 15.8

Total 70 100

N=70

Source :field data, march 2015

Most respondents considered their income not reliable. That is forty-seven percent of the

respondents, while thirty-seven percent thought that stated that their incomes were regular and

reliable.

28

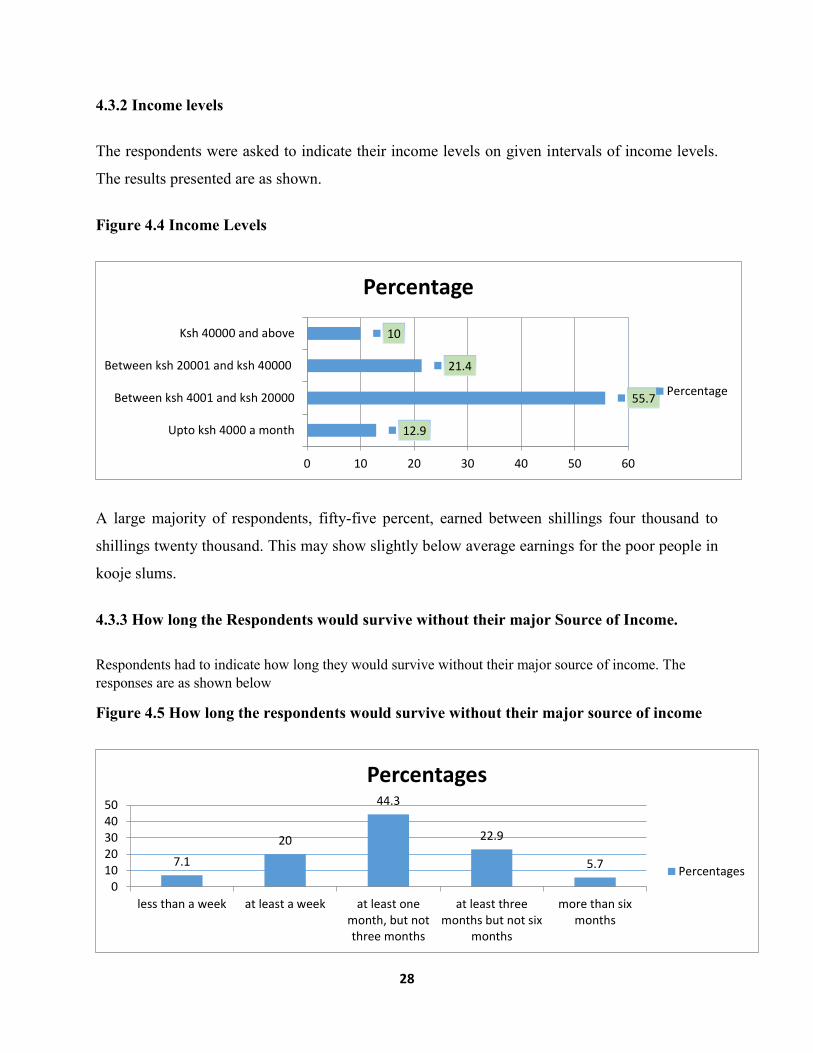

4.3.2 Income levels

The respondents were asked to indicate their income levels on given intervals of income levels.

The results presented are as shown.

Figure 4.4 Income Levels

A large majority of respondents, fifty-five percent, earned between shillings four thousand to

shillings twenty thousand. This may show slightly below average earnings for the poor people in

kooje slums.

4.3.3 How long the Respondents would survive without their major Source of Income.

Respondents had to indicate how long they would survive without their major source of income. The

responses are as shown below

Figure 4.5 How long the respondents would survive without their major source of income

12.9

55.7

21.4

10

0 10 20 30 40 50 60

Upto ksh 4000 a month

Between ksh 4001 and ksh 20000

Between ksh 20001 and ksh 40000

Ksh 40000 and above

Percentage

Percentage

7.1

20

44.3

22.9

5.7

01020304050

less than a week at least a week at least onemonth, but notthree months

at least threemonths but not six

months

more than sixmonths

Percentages

Percentages

29

4.4 Source of Financial Knowledge available to the Poor in Kooje Slums of Meru Town

The research sought to find out the available sources of financial knowledge that were available

to the Poor in Kooje Slums of Meru Town,

4.4.1 Source of Financial Advice

Respondents had to indicate sources of financial advice .the responses are as shown in the table

below.

Table 4.7 Source of Financial Advice

Source Frequency Percentage

Financial institutions 13 18.6

Business people 9 12.9

Financial experts 8 11.4

Friends 9 12.9

Relatives 7 10

Internet 4 5.7

Magazines newspapers and

financial journals or books

7 10

Advertisements on print and

electronic media such as TVs

and radio

10 14.3

Other 3 4.3

Total 70 100

N=70

Source :field data, march 2015

30

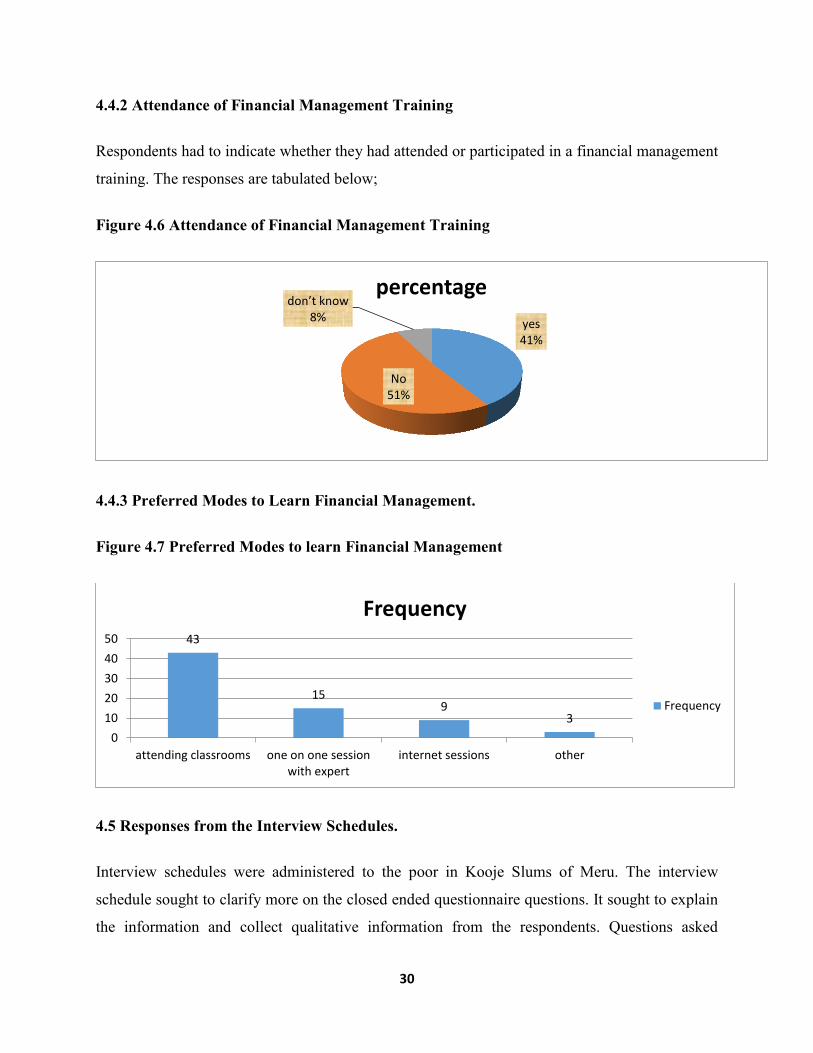

4.4.2 Attendance of Financial Management Training

Respondents had to indicate whether they had attended or participated in a financial management

training. The responses are tabulated below;

Figure 4.6 Attendance of Financial Management Training

4.4.3 Preferred Modes to Learn Financial Management.

Figure 4.7 Preferred Modes to learn Financial Management

4.5 Responses from the Interview Schedules.

Interview schedules were administered to the poor in Kooje Slums of Meru. The interview

schedule sought to clarify more on the closed ended questionnaire questions. It sought to explain

the information and collect qualitative information from the respondents. Questions asked

yes 41%

No 51%

don’t know 8%

percentage

43

15 9

3

0

10

20

30

40

50

attending classrooms one on one sessionwith expert

internet sessions other

Frequency

Frequency

31

touched on issues to do with financial training, financial products and understanding of the

financial products.

4.5.1 Responses on Financial Topics covered in Financial Training

The interview schedule prompted respondents who had attended financial training to indicate the

financial topics that they had covered. Have you ever attended any financial management-

training programme? If yes what were the main financial issues that were covered? .according to

the respondents financial training had played a significant role in improving their awareness, that

they had been taught issues touching on savings, loans, insurance, retirement saving and pension

schemes. The respondents also did not remember most of the financial issues that they were

taught „…it was nice to go to the financial training but really I don’t know how useful it was, I

did go, sat, listen, but then I forgot what was taught…‟

4.5.2 Responses on Financial Product Information

The respondents were asked, „…Which financial products do you frequently use or prefer to

use?, Where did you obtain the information on these financial products?..‟ the respondents

indicated to have used loans, insurance, and pensions. A respondent stated that „…I took up a

loan based on the information I was given by the bank from which I took the loan…‟ that he had

information from the provider of the financial product. However, other respondents had a

different influence on their source of financial product „… I took up a retirement fund at old

mutual because I saw an advertisement that invited me to a financial seminar…‟

4.5.3 Responses on understanding of the Financial Products

The researcher asked the respondents to indicate their understanding of the financial products

that they had taken „…Considering the preferred source of financial information on products, do

you think you fully understand the financial products and their terms?‟ The respondents did not

exude a lot of confidence in answering the question. ‘… I can’t clearly say I fully understand the

pension scheme I took up but I think the provider was convincing as to why I needed the scheme,

and I found the terms to be attractive…‟ the respondents left the thinking to the providers but did

not seem to understand the financial products that they took up.

32

CHAPTER FIVE

SUMMARY CONCLUSIONS AND RECOMMENDATIONS

5.0 Introduction

Chapter five comprises the summary of the findings from the study as well as the conclusions

and recommendations based on the findings.

5.1 Summary of Main Findings

This study was about improving financial awareness among the Poor in Kooje Slums of Meru

Town. The specific objectives included: To find out the level of financial awareness among the

Poor in Kooje slums of Meru .To find out the number of people in Kooje Slums of Meru town

that have a savings plan with a financial institution in Meru.To find out the source of financial

knowledge available to The Poor in Kooje Slums of Meru Town.Based on the study objectives

and the research methodology, the summary findings are as follows:

5.1.1 Level of Financial Awareness among the Poor in Kooje Slums of Meru Town

According to the research findings majority of the respondents did not have a financial budget

while only 27% agreed to use a financial budget. In addition the majority of respondents also had

little information to do with Government Issue treasury bills and bonds that is only 70% of the

respondents. These could indicate inadequate government information provisory and advisory on

their debt instruments. On financial products, majority of the respondents were aware of

financial products such as bank loans secured on property and unsecured bank loans, current

accounts, savings accounts, insurance while fewer than half of the respondents had little

knowledge of pension funds, investment accounts, mortgages credit and debit card, and stocks

and shares. Therefore the overall level of financial awareness based on these findings was found

to be low.

33

5.1.2 Savings in a Financial Institution among the Poor in Kooje Slums of Meru Town

Study findings revealed that most of the respondents did not have a savings account with a

recognized financial institution. 44% of the respondents acknowledged having a savings account

while more than 55% did not have savings with a financial institution. Furthermore 47.1% of the

respondents stated that their sources of income were not reliable while only a few 37% thought

their incomes were reliable. Yet most of the respondents‟ incomes fell between ksh 4001 and ksh

20000 that is 55.7% of the repondents.12.9% earned less than ksh 4000, While 21.4% earned

between ksh 20001 and ksh 40000 and only a lesser 10% earned over ksh 40000. And as such

majority of the respondents, that is 44.3%, indicated that they would only survive without their

major source of income for at least one month but not more than three months. While only 5.7%

of the respondents indicated they would survive for more than 6 months.

Based in these research findings it was found out that the level of savings was low, the

knowledge of financial products was not diverse and in other words the respondents lived from

hand to mouth. Therefore their incomes were unreliable and unsustainable leaving the savings

levels low.

5.1.3 Source of Financial Knowledge available to The Poor in Kooje Slums of Meru Town

The study findings revealed that majority of the respondents source of financial advice to be

financial institutions, friends, business people, advertisements on print and electronic media,

friends ,magazines, newspapers and financial experts in that order. Also majority of the

respondents (58.6%) had not attended any formal financial training while 47.5 had attended

financial training. The respondents went further to indicate that their preferred modes to learn

financial management were attending classrooms and one to one sessions with an expert.

Therefore the source of financial knowledge was not adequate to meet their financial information

requirements.

5.2 Conclusions

This research study has evaluated improving financial awareness among The Poor in Kooje

Slums of Meru Town. Also the study examined the level of financial awareness among The Poor

34

in Kooje Slums of Meru Town, their sources of financial advice and the financial products that

they used. The study also examined their attendance of financial management training and their

preferred mode to learn financial management. The study findings are important to understand

the improvement of financial awareness among The Poor in Kooje Slums of Meru Town and

how their application can be relevant in other similar slums in Kenya. On the basis of the

research findings, the study arrived at several conclusions:

The study concluded that the levels of financial skills such as budgeting was low , government

did not provide enough information on their issuance of treasury bills and bonds, and that was

the reason the levels of awareness on treasury bills and bonds was low. The most common

financial products happened to be simpler products such as loans and savings accounts while

most failed to be aware of more resourceful products such as pensions and investment accounts.

The study also concluded that incomes of The Poor in Kooje Slums of Meru Town were low.and

that it might be the reason why fewer people had a savings account with a financial institution.

They study furthermore concluded that since the incomes were low and savings low, most of the

Poor people in Kooje slums wouldn‟t survive for more than three months without their major

source of income.

The study concluded that a sizeable section of the respondents felt that their financial situation

was out of control, due to this the respondents sought advice from financial institutions, friends,

business people, advertisements on print and electronic media, friends ,magazines, newspapers

and financial experts. Some of these sources such as friends may not have been professional and

did not address the respondents‟ financial problems. The study also concluded that most

respondents had not attended financial management training and even some of those who had

attended financial management training did not understand the financial topics covered.

5.3 Recommendations

This study recommends effective awareness and education campaigns to be regularly carried out

among the Poor in Kooje slums of Meru to improve their financial management literacy. This

can be done through Public awareness and information campaigns by the financial institutions in

partnership with the relevant government institutions such as the Central Bank of Kenya.

35

This study also recommends Development of appropriate financial education content and

delivery channels contributing to the financial capabilities in schools, colleges tertiary

institutions and universities, the financial education should be pro-poor and take into

consideration the specific needs and challenges that the Poor face. Financial education

programmes should focus particularly on important life planning aspects, such as basic savings,

debt, insurance or pensions. The study also recommends financial inclusion of the poor in

financial programs and decisions at different levels of government.

Finally the study concludes that the government should be in make it apriority to develop a

curriculum on financial education at local, middle and higher learning institutions. It should also

follow up these initiatives with campaigns to create awareness on the importance of financial

awareness.

5.4 Suggestions for further Research

This study has tackled improving financial awareness among the Poor in Kooje Slums of Meru

Town. More studies should be encouraged to investigate how financial awareness leads to

behavior change among the poor and how an improvement in financial awareness leads to

improved financial decisions among the poor.

36

REFERENCES

Alan Greenspan (July 14, 2006) The Importance Of Financial Education Today, (Financial

Education) An Article From: Social Education.

Annamaria Lusardi And Olivia S. Mitchell (2013) The Economic Importance Of Financial

Literacy: Theory And Evidence.