impact of camel ratios toward profitability of sharia

TRANSCRIPT

IMPACT OF CAMEL RATIOS TOWARD

PROFITABILITY OF SHARIA BANKS IN INDONESIA

By

Sarah Ruen Soekarno

014201400116

A Skripsi presented to the

Faculty of Business President University

in partial fulfillment of the requirement for

Bachelor Degree in Management

April 2018

PANEL OF EXAMINERS

APPROVAL SHEET

The Panel of Examiners declare that the skripsi entitled “IMPACT OF

CAMEL RATIOS TOWARD PROFITABILITY OF SHARIA BANK IN

INDONESIA” that was submitted by Sarah Ruen Soekarno majoring in

Management from the Faculty of Business was assessed and approved to

have passed the Oral Examinations on April 18, 2018.

Christina Liem, S.T., M. Comm

Chair - Panel of Examiners

Liswandi, S.Pd., M.M., Ph.D

Examiner 1

Liswandi, S.Pd., M.M., Ph.D

Examiner 2

SKRIPSI ADVISER

RECOMMENDATION LETTER

This skripsi entitled “IMPACT OF CAMEL RATIOS TOWARD

PROFITABILITY OF SHARIA BANK IN INDONESIA” prepared and

submitted by Sarah Ruen Soekarno in partial fulfillment of the

requirements for the degree of Bachelor in the Faculty of Business has been

reviewed and found to have satisfied the requirements for a skripsi fit to be

examined. I therefore recommend this skripsi for Oral Defense.

Cikarang, March 29th, 2018

Acknowledged by, Recommended by,

Dr. Dra. Genoveva, M.M Purwanto, ST., MM

Head of Management Study Program Adviser

DECLARATION OF

ORIGINALITY

I declare that this skripsi, entitled “IMPACT OF CAMEL RATIOS

TOWARD PROFITABILITY OF SHARIA BANKS IN INDONESIA” is,

to the best of my knowledge and belief, an original piece of work that has

not been submitted, either in whole or in part, to another university to

obtain a degree.

Cikarang, March 29th, 2018

Sarah Ruen Soekarno

i

ABSTRACT

The development of the banking world in Indonesia has undergone significant

transformation, for example, the establishment of Sharia banks. Profitability becomes

a tool for a business to maintain its continuity in the long term. This research will study

about the impact of CAMEL ratios toward profitability of sharia banks in Indonesia.

Ratios that is being applied in this research is Capital Adequacy Ratio, Non Performing

Financing, Net Profit Margin, Net Operating Margin and Financing to Deposit ratio.

Methodology sampling used is purposive sampling. Sample of this research are 11

Sharia Banks in Indonesia from 2015 until 2017. This research uses descriptive

analysis, multi regression analysis, classical assumption test, coefficient of

determination, and hypothesis testing using F-test and T-test. T-test results show that

NPM have positive and significant influence toward ROA of Sharia Bank. And CAR

and NOM variable has positive but not significant towards ROA on Sharia bank

operating in Indonesia. While FDR has negative and significant towards ROA of Sharia

Bank and NPF has negative but not significant towards ROA. F-test shows that CAR,

NPF, NPM, NOM, and FDR simultaneously has influence on profitability. Coefficient

of determination shows the independent variables explains 73,2% variance in

profitability. And NPM is variable that has the most influence toward profitability.

With the result of this research, thus management of Sharia bank should pay attention

to CAR, NPF, NPM, NOM, and FDR because those variable have influence on ROA.

Keywords: CAMEL, Ratios, Profitability, Sharia Bank, Regression.

ii

DEDICATION

I would like to dedicate this thesis to my family who always support me and

helping me finish this study. And to President University as my contribution as a

student.

iii

ACKNOWLEDGMENT

Thanks to Allah SWT who has given me his gifts and strengths, so that I can finish this

thesis. The completion of this thesis is not only because of my hard work alone, but

those around me who have provided support in any form. So I also want to thank people

who play a role in completing this thesis

First and foremost, I would like to thank my family. Especially to my mother, Endang

Rukmiati. She is the one who have provided moral and material support to me so as to

facilitate my process in submitting this thesis. Without her support, this thesis could not

be finished.

Not to forget also to sir Pandu and sir Purwanto who have been willing to be my thesis

advisors. They have given their time, energy, support and mind whenever and wherever

to help me finish this thesis. Thank you for the guidance so far.

Thanks to the lecturers of other lecturers who have been willing to help me through the

knowledge that has been given during science studying in this campus. To mam Marie

Ann Jinenea, and other lecturers who are not quite my name I mention here.

Not to forget also, for Wiwin, Rahmah Maulinda, Geovany and Hemas Amelita who

have contributed by providing his knowledge for this thesis and always provide help

and spirit starting from the first day of admission until my day thesis trial. And to friends

of the Faculty of management for 4 years that is not forgotten.

During my college days, I also met a great friend Lisa, Dani Siwi, and Helga Fairuz.

Thank you for your support and making my day in college fun.

I also want to express my gratitude to people who have been present in my life until

this moment and still willing to accompany me in joy and sorrow. My second family

(Untitled) namely Kartika Findra Resiandi, Farhena Allya, Pavita Raudina Sari. And

thanks to Rizky who has passed us because of his illness, I want to realize his dream

for college who couldnt finished because of lupus through this thesis i made for her.

Last but not least, to everyone who is not enough I mention here who also provide

assistance to me so far. Thank you for your support and prayers until I get my bachelor

degree.

iv

TABLE OF CONTENT

ABSTRACT ............................................................................................................... i

DEDICATION .......................................................................................................... ii

ACKNOWLEDGMENT ......................................................................................... iii

TABLE OF CONTENT ........................................................................................... iv

LIST OF TABLES ................................................................................................... vi

LIST OF FIGURES ................................................................................................. vii

LIST OF EQUATION ........................................................................................... viii

LIST OF ACRONYM .............................................................................................. ix

CHAPTER I INTRODUCTION ............................................................................... 1

1.1. Background of Study ....................................................................................... 1

1.1.1. Need of Study ................................................................................................. 7

1.2. Problem Statement .......................................................................................... 7

1.3. Research Question ........................................................................................... 8

1.4. Research Objectives ........................................................................................ 8

1.5. Significance of Study ...................................................................................... 9

1.6. Scope and Limitation ...................................................................................... 9

1.7. Thesis Organization....................................................................................... 10

CHAPTER II LITERATURE REVIEW ................................................................. 12

2.1 Theoritical Review ........................................................................................ 12

2.1.1. Agency Theory.............................................................................................. 12

2.1.2. Profit Sharing Theory ................................................................................... 13

2.2. Variable Review ............................................................................................ 13

2.2.1 CAMEL Ratios ............................................................................................. 13

2.2.2. Profitability ................................................................................................... 20

2.3. Research Gap................................................................................................. 21

CHAPTER III RESEARCH METHODOLOGY .................................................... 27

3.1. Research Framework ..................................................................................... 27

3.2. Hypotheses .................................................................................................... 27

3.3. Operational Definition................................................................................... 28

3.4. Research Design ............................................................................................ 31

3.5. Sampling plan ................................................................................................ 39

3.5.1. Population and Sample .................................................................................. 39

3.5.2. Data Collection Method ................................................................................ 47

v

CHAPTER IV RESEARCH ANALYSIS ............................................................... 48

4.1. Descriptive Analysis ......................................................................................... 48

4.2. Inferential Analysis ....................................................................................... 51

4.2.1. Classical Assumption Test ............................................................................ 51

4.2.2. The Goodness of Fit ...................................................................................... 57

4.2.3. Interpretation Result ...................................................................................... 62

CHAPTER V CONCLUSION AND RECOMMENDATION ............................... 69

References ............................................................................................................... 73

Appendix ................................................................................................................. 80

vi

LIST OF TABLES

Table 2.1 Previous Research ........................................................................................ 21

Table 3.1 Operational Definition ................................................................................. 31

Table 3.2 Population of Research ................................................................................ 40

Table 3.3 Sample of Research ..................................................................................... 41

Table 4.1 Descriptive Statistics (Before Data Elimination) ......................................... 49

Table 4.2 Descriptive Statistics (After Data Elimination) ........................................... 50

Table 4.3 Result of Normality Test (Before Data Elimination)................................... 52

Table 4.4 Result of Normality Test (After Data Elimination) .................................... 53

Table 4.5 Result of Multicollinearity test ................................................................... 53

Table 4.6 Result of Heteroscedasticity test ................................................................. 54

Table 4.7 Result of Autocorrelation Test .................................................................... 55

Table 4.8 Result of Multiple linear regression Analysis ............................................. 56

Table 4.9 Result of Adjusted R Square ........................................................................ 58

Table 4.10 Result of F-Test ......................................................................................... 59

Table 4.11 Result of T-Test ......................................................................................... 60

vii

LIST OF FIGURES

Figure 1.1 Q.S. Al Baqarah: 275 ............................................................................... 3

Figure 1.2 The Development of Commercial and Sharia banks Assets .................... 5

Figure 1.3 Graph of ROA on Sharia Bank ................................................................ 6

Figure 2.1 Theoretical Framework .......................................................................... 26

Figure 3.1 Research Framework ............................................................................. 27

viii

LIST OF EQUATION

Equation 2.1 Capital Adequacy Ratio Formulation ................................................ 14

Equation 2.2 Non Performing Financing Ratio Formulation .................................. 16

Equation 2.3 Net Profit MarginRatio Formulation ................................................. 18

Equation 2.4 Net Operating Margin Ratio Formulation ......................................... 19

Equation 2.5 Financing to Deposit Ratio Formulation ........................................... 20

Equation 2.6 Return on Assets Ratio Formulation .................................................. 21

Equation 3.1 Multiple Regression Analysis Equation ............................................ 37

Equation 4.1 Multiple Regression Analysis Result Equation ................................. 56

ix

LIST OF ACRONYM

CAR : Capital Adequacy Ratio

NPF : Non Performing Financing

NPL : Non Performing Loan

NPM : Net Profit Margin

NIM : Net Interest Margin

NOM : Net Operating Margin

LDR : Loan to Deposit Ratio

FDR : Financing to Deposit Ratio

1

CHAPTER I

INTRODUCTION

In the first chapter is an introduction that contains its background, need of study,

problem statement, research questions, research objectives, significant of study, scope

and limitation, and thesis organization.

1.1. Background of Study

By dominating 80% of the financial market, Bank has facilitated economic growth and

has an important role in maintaining the economic movement of a country by becoming

an intermediary institution (Jaseviciene, 2012). According to (Kasmir, 2009), Bank is

a financial institution that has functions to collect and channel funds in the community

through the authority. It has to receive a deposit and provide a loan to improve the lives

of many people. Fund raising activities such as in the form of savings, demand deposits,

or deposits, funding activities such as lending, and provide other banking services.

Banks are getting their profit by collecting funds from the public in the form of a

deposit. Banks make deposits as a source of capital and funds to provide credit.

Therefore, banks should attract customers to deposit their money by offering bank

interest. Depositors will take the money along with the interest of the bank that has been

promised to be given by the bank as a sign of merit. Funds collected in the form of

deposits will be lent to borrowers who have been selected in advance to receive the

loan. Accepting credit proposals from untrusted borrowers can lead to failure to repay

a loan and ended with lowering bank's income. Strict policies needed to protect bank

income. However, too strict policy can lead to lower income as well as making it

difficult for banks to use available funds. With a time of period that has been set, the

borrower will return the borrowed money along with the current interest applied by the

bank, which the amount is greater than the interest of the bank to depositors. If the

interest rates given by the bank to the loan are greater than the bank's interest offered

to depositors, the bank will able to generate income. Profit generated from the bank is

2

from the difference between bank’s interest given to depositors and bank’s interest

arranged for the borrower (Central for Financial Training, 2010). The other incomes

such as income from investment on government stock investment and other first class

industrial securities in accordance with OJK rule No.36/POJK.03/2017 which said that

the bank's equity participation activities is one part of the bank's investment activities

in addition to other activities such as credit distribution or financing, fund placements

in the form of securities, and interbank money market activities. As a fund-raising

activity, beside receive benefits in the form of revenue from equity participation, it is

also potentially exposed to risk from such activities.

In addition, banks also provide services that apply fee and commission to its users or

commonly referred to as fee-based income. Examples include locker rent for customers

to store their valuables, underwriting shares for companies who issue their shares, card

fees that comes from joining fees, payment fees, fines imposed for late payment or

others, commission from the guarantee between two parties’ transaction administration

fee. There is also foreign services such as travel check, letter of credit, act as brokers

on foreign exchange, etc (Drs.Ismail, 2010). The banking in Indonesia has undergone

significant development, for example, the emergence of Sharia banks. According to

(Kasmir, 2009), there are several types of banking that can be divided from various

aspects. Type of bank when viewed in terms or ways in determining the price of

products or services can be divided into two, those are bank based on conventional and

Sharia principles

Bank based on haria principle is bank that implement Islamic law in bank activities

with other parties to deposit funds or business financing or other banking activities.

Banks based on Sharia principles in determining the price of its products are very

different from conventional banks based on, profit sharing principle (Mudarabah and

Wadiah), equity participation (Musyarakah), buying and selling of goods with gain

(Murabahah), pure lease without option (Ijarah).

Sharia banks themselves have the meaning of a financial institution that operates based

on the principles of Sharia, namely by making the Quran and Hadith as a guide

(Wangsawidjaja, Pembiayaan Bank Syariah, 2013). Quran and Hadis forbid “Riba” or

to take interest in its verses including with cause and effect. One of the verses is Q.S.

Al Baqarah verse 275 as shown in Figure 1.1,

3

Figure 1.1 Q.S. Al Baqarah: 275

Source: https://tafsirq.com/2-al-baqarah/ayat-275

Which means that “Those who consume interest cannot stand [on the Day of

Resurrection] except as one stands who is being beaten by Satan into insanity. That is

because they say, "Trade is [just] like interest." But Allah has permitted trade and has

forbidden interest. So whoever has received an admonition from his Lord and desists

may have what is past, and his affair rests with Allah. But whoever returns to [dealing

in interest or usury] - those are the companions of the Fire; they will abide eternally

therein” (Sudaryo & Yudanegara, 2017).

For its products, it can be divided into 3 kinds of fund raising products, the distribution

of funds products based on the principles of lease, sale and purchase, and the products

of services consisting of Sharf and Ijarah (Ikit, 2015).

The product of fund raising in Islamic banks includes demand deposits, savings

accounts, and time deposits with 2 principles those are Wadiah Principle and

Mudharabah principle, Wadiah is a deposit from one party to another party (in this case

is Sharia bank), the deposit should be kept and return whenever the depositor wants.

Implementation of Wadiah principle on Sharia bank is using Wadiah Yad Dhamanah

and Wadiah Yad Amanah. Wadiah Yad Dhamanah is a principle that allow the bank to

take advantage on the deposit but have to be responsible for it. While on Wadiah Yad

Amanah. The deposit cannot be utilized by the bank and the bank not responsible for

any kind of damage. In Mudarabah principle, the depositor acts as the owner of the

capital while the bank acts as the manager. The funds saved by the bank are then used

4

for financing, in which case the bank uses it for Mudharabah financing, the bank is

responsible for any possible losses.

The product of fund raising in Islamic banks based on 3 principles those are principles

of sale and purchase (Ba'i) which means because of the transfer of ownership of goods.

The bank's profit is mentioned in front & includes the price of the sold price, and rental

principles (Ijarah) which means an agreement for the transfer of use rights to goods or

services through lease without being followed by transfer of ownership of leased goods.

In this case the bank rents the equipment to the customer at a predetermined fee. And

profit sharing principle (Syirkah) which consists of 2 kind of products consists of

Musharakah and Mudharabah .

For the history of Sharia bank themselves, starting from in the past where bank had a

meaning of a financial institution that used the concept of credit where credit must be

followed by interest based on Law no. 14 of 1967. Then the government had a problem

with the bank stability and interest control caused by conventional bank has triggered

the enactment of Sharia principles with 0% interest in Indonesia.

First by Deregulation that issued in June 1, 1967. And then followed by PAKTO

(Package of Government Policy in October) issued by the government that support the

establishment of new banks with low budget in purpose of mobilizing public funds to

support development. Law Number 10 Year 1998 also contributed to the development

of Sharia bank (Marimin, Romdhoni, & Fitria, 2015).

The development of Islamic banks began in 1990, in which the Indonesian Ulema

Council (MUI) formed a working group to establish Islamic Banking in Indonesia. As

a result of the work of MUI, the first syariah bank in Indonesia is established namely

PT Bank Muamalat Indonesia (BMI). At the end of 2013, the banking regulatory and

supervisory functions moved from Bank Indonesia to the Financial Services Authority

(OJK). As the financial services sector authority, OJK continues to refine the vision and

strategy of sharia finance sector development policy (Otoritas Jasa Keuangan, 2018).

In addition to the emergence of new sharia banks, OJK as the new bank authority also

makes the regulation of OJK no.64 / POJK.03 / 2016 Year 2016 about the change of

conventional Business Operations into Bank Syariah which stipulates that conventional

banks can do change of business activities to become Sharia Bank. This increases the

number of Sharia banks.

5

With the number of Moslem in Indonesia, which is the largest Moslem population in a

country around the world, also has helped Sharia banking in Indonesia to grow rapidly.

There are 12 Sharia banks, 161 Sharia rural banks, and 22 Sharia business units in

Indonesia by 2015 (Haribowo, 2017).

Figure 1.2 The Development of Commercial and Sharia banks Assets

Source: www.Kompasiana.com

From Figure 1.2, the researcher instead found that the development of Sharia banks

may still relative low compare to the development of commercial bank. Even though

Sharia banks are growing every year, but the other banks are growing as well. The total

amount of Sharia bank assets is 679 trillion in 2016, which means only 5% from what

commercial banksdispose have already had.

Starting from lack of coordination among the authorities in the development of Islamic

banking, many sharia banks that do not have adequate capital, Sharia banking funding

structures that still rely on financing from expensive funds, lack of variance in products

and services that have not met the expectations of society, Fiture of Islamic banks have

not complete as conventional bank, inadequate number and quality of human resources

and lack of information technology to support the development of products and

services. Then the understanding and awareness of the community is still low to Islamic

banks and regulation and supervision that is still not maximum, those became the causes

why the development of Islamic banks is relatively slow compared to conventional

banks (Aditiasari, 2018). So that is why commercial banks become Sharia bank’s hard

competitors.

6

In order to compete with other banks and attract more of the enthusiasm from investors

and customers, Sharia bank should maintain their performance. Besides, Sharia bank

with its no interest system becomes the main alternative solution in maintaining the

stability of financial system and prevent global crisis happen (Sitepu, 2015). Therefore,

Sharia bank’s condition must be monitored for its important role.

Because all business organizations’ main motive is profit (V. Rajasekaran & R.Lalitha,

2011). That is why profitability becomes one of the important things in the healthy bank

and is being used as a parameter of financial soundness in a company.

Investors can see the advantages of investing in the company and the basis of the

decision to continue investing or not. As for potential investors, profitability can be

made for a comparison tool with other companies in the same industry to decide where

they should invest their money. Therefore, profitability also becomes a picture in the

business of a bank to maintain its business continuity in the long term, because

profitability indicates whether the business has a good prospect in the future (Hery,

2017). This is why management must keep on eye on this aspect.

Figure 1.3 Graph of ROA on Sharia Bank

Source: Financial Report of Sharia Banks in Indonesia

Figure 1.3 is showing the average of ROA of Sharia bank in the period of 2015-2017.

As shown in the graph, the profitability of Sharia bank itself is not in a good condition

because of instability in ROA. ROA is one of many ratios that is used to calculate the

profitability in a bank (Gitman & Joenk, 2008).

(0,56)(0,30)

(0,98)

1,47

(0,70)(0,98)

0,65

1,86

1,38

(1,50)

(1,00)

(0,50)

-

0,50

1,00

1,50

2,00

2015Q2 2015Q3 2015Q4 2016Q1 2016Q2 2016Q3 2016Q4 2017Q1 2017Q2

RO

A (

%)

Period

ROA OF SHARIA BANKS

7

Financial report is presented to help assessing a company's condition. By using the

financial report, we can visualize the condition and development of a business currently

(Sugiyono & Untung, 2008). Financial ratios can be used as a tool of assessment for its

performance by using financial report. It can shows the change in financial condition

or operational activity in the past, help to show the trend of the changing pattern, and

show the risk and opportunity that the company has (Fahmi, 2011). Ratio means turning

the financial condition of a company into a measurable number. So it is possible to

compare a company's financial aspects with other companies and financial aspects

between different times. Creating a financial ratio itself utilize financial data of a

company that has been calculated in such a way that produces a number that can

describe a financial aspect in the company. The purpose of analyzing using financial

ratios is to evaluate the current situation and predict the financial (Rangkuti, 2006).

One of the systems in assessing a soundness of bank is CAMEL According to Bank

Indonesia rules No. 9/24/DpBs about assesing the level of healthiness of a bank based

on the Sharia principles can be done by calculating the factor of CAMEL. A healthy

bank is a bank that can manage those five aspects. In case that a bank is in problem due

to a certain aspect, it means that the financial report will get some difficulties (Matnin,

2016).

1.1.1. Need of Study

This research is going to find out the problem on profitability. Profitability is one of the

important aspects in a business, including bank. Although profitability of Sharia bank

is not stable. That condition can be caused by many factor, for example CAMEL aspect.

In case that a bank is in problem due to a certain aspect, it means that the financial

report will get some difficulties. Based on that fact, the researcher wants to know the

problem that caused the instability of its profitability. This research can give useful

information to Sharia bank and the researcher wants to know in detail about profitability

of Sharia bank in Indonesia.

1.2. Problem Statement

In this study, the researcher tries to find out CAMEL ratios effect on profitability on

Sharia bank in Indonesia. As shown in Figure 1.3, the researcher found that there is a

fluctuation in the ROA which is resulting a profitability of Sharia bank. The fluctuation

makes the researcher wants to research what the factors are behind the profitability.

8

According to (Matnin, 2016), if one problem of aspects in CAMEL occurs, then there

will be a problem in financial report of a bank. The financial report contains many

aspects, one of them is profitability. CAMEL itself can be measured using financial

ratio. This research wants to know whether there is a correlation between the effects of

CAMEL ratios with profitability. Therefore, the researcher will use CAMEL ratios to

understand in detail about what factors behind profitability of Sharia Bank.

1.3. Research Question

On the basis of the above thinking, it can be formulated research questions as follows:

1. Is there a significant influence of capital ratio towards profitability of Sharia

bank in Indonesia?

2. Is there a significant influence of asset quality ratio towards profitability of

Sharia bank in Indonesia?

3. Is there a significant influence of management ratio towards profitability of

Sharia bank in Indonesia?

4. Is there a significant influence of earnings ratio towards profitability of Sharia

bank in Indonesia?

5. Is there a significant influence of liquidity ratio towards profitability of Sharia

bank in Indonesia?

6. Is there a significant influence of capital, asset quality, management, earnings,

and liquidity ratios toward profitability of Sharia bank in Indonesia?

7. Which variable has the most significant influence towards profitability of Sharia

bank in Indonesia?

1.4. Research Objectives

This research has 7 objectives that need to be found. Those are:

1. Find out the impact of capital ratio on profitability of Sharia bank in Indonesia.

2. Find out the impact of asset quality ratio on profitability of Sharia bank in

Indonesia.

3. Find out the impact of management ratio on profitability of Sharia bank in

Indonesia.

4. Find out the impact of earnings ratio on profitability of Sharia bank in Indonesia.

9

5. Find out the impact of liquidity ratio on profitability of Sharia bank in Indonesia.

6. Find out the impact of capital, asset quality, management, earnings, and

liquidity ratio on profitability of Sharia bank in Indonesia.

7. Find out which variable has the most significant influence towards profitability

of Sharia bank in Indonesia.

From the objectives above, this research is entitled with “THE IMPACT OF

CAMEL RATIOS TOWARD PROFITABILITY OF SHARIA BANKS IN

INDONESIA”.

1.5. Significance of Study

By finding the effect of camel ratio to profitability on Sharia bank, the result can be

exploited by related party that is:

a. As another reference for decision-making by the management of Sharia banks in

managing the activities of Islamic banks to maintain the continuity of the business.

b. Help OJK in monitoring Sharia bank in order to maintain the country's economic

stability and as a source of information in the formulation of state policy.

c. Assisting current investors in determining investment options and being a

consideration of potential investors to invest in Sharia banks. Because profitability

is one factor of financial performance of a bank that describes the current financial

condition and prospects in the future.

d. As a reference for other researchers to conduct other related studies and as an idea

to conduct similar research but more about profitability in Sharia banks.

e. Increase knowledge for the researcher especially about profitability in Sharia bank

and how to do research so hopefully there will be other research in the future.

1.6. Scope and Limitation

The purpose of this study is to determine the effect of CAMEL ratio to profitability.

The population that is the subject of research is Sharia bank in Indonesia which amounts

to 12 banks. But this study used 11 Sharia banks as samples. The data period of this

study starts from June 2015 until June 2017.

This study will have several limitations, there are:

10

a. Sharia banks used as research samples do not cover all Islamic banks in Indonesia.

Because there are several criteria that are not met by the bank and not able to to

meet the classical assumption test that requires researchers to use only a few Sharia

banks from all Sharia banks operating in Indonesia

b. The results are based on data from 2015Q2 to 2017Q2.

1.7. Thesis Organization

This thesis consists of 5 chapters. The chapters contained in this essay consist of

introduction, methodology, literature study, analysis, conclusions, and

recommendations.

The contents of each chapter are outlined in the following lines:

CHAPTER 1 – INTRODUCTION

In the first chapter is an introduction that contains the explanation of what is the

background of the research, need of study, problem statement, research questions,

research objectives, significant of study, scope and limitation, thesis organization. In

the background of the research, there is an explanation of the topic to be researched.

Need of study contains the importance of doing this research. The problem statement

contains the explanation of problem source and the thing you want to find out the

answer to. Research questions also show the things to be researched and it confirms in

the form of questions. Then research’s objectives contain what this research is looking

for and what it wants to discover through this research. Significant of study contains

the parties who can take advantage of the results of this research when it has already

found the answer and how they use the results of research. The next one is scope and

limitation which contains what you want to examine in detail about the subject and the

period will be used. Scope and limitation also contain the limitation of research and

things that are not included in the study. Thesis organization is an outline thesis which

contains an explanation of the contents in each chapter. In either the subject, time or

topic.

CHAPTER 2 - LITERATURE STUDY

11

Chapter 2 of the literature review contains relevant previous research studies that can

be used for reference in diagnosing discussion and supporting the results of research as

a process of finding answers to the problem. The contents of this chapter consist of

theoritical review, variables review and research gap. The subject discussed in this

chapter is the theory, formulas, and explanation from previous research related to

variables, object and topic in this research.

CHAPTER 3 – RESEARCH METHODOLOGY

This chapter 3 contains a research methodology that explains what methods are used in

both data processing and analysis. The contents of this chapter are research framework,

hypotheses, operational definition, research design, and sampling plan.

CHAPTER 4 - DATA ANALYSIS

This chapter contains the core of the research itself is a process of data analysis that has

been prepared using SPSS software and research methods that have been determined

and described in Chapter 3. The process is classical assumption testing consisting

normality test, heteroscedasticity, autocorrelation, and multicollinearity. Then it will be

continued with coefficient of determination and hypothesis testing using T-test and F-

test. And explanation and interpretation of the results obtained.

CHAPTER 5 CONCLUSION AND RECOMMENDATION

This chapter contains the result of the analysis is formed into the conclusion of the

answer to the problem contained in the problem statement. Then it contains the

recommendations indicated for the company and what can be added in the futures

research.

12

CHAPTER II

LITERATURE REVIEW

Chapter 2 of the literature review contains relevant previous research studies that can

be used for reference in diagnosing discussion and supporting the results of research as

a process of finding answers to the problem. The contents of this chapter consist of

theoritical review, variables review, research gap. The subject discussed in this chapter

is the theory, formulas, and explanation from previous research related to variables,

object and topic in this research.

2.1. Theoritical Review

2.1.1. Agency Theory

It is known as principal-agent relationship. the thory is about a contract between two or

more parties where one or more persons able to do things to delegate their behalf in

decision making. There are two parties involved, those are agent which are the

managers or employees who working in an organization and is responsible for

managing the business activities of the company to the owner. The second is principal

who is the owners of a company that delegates and transfers responsibilities or capital

to the appointed agent. in this case, shareholders will become the principal and bank

management as the agent. Management is a party contracted by shareholders to work

in the interests of shareholders. Because they are elected, the management must account

for all of their work to shareholders (Shamsuddin & Ismail, 2013).

The agency relationship always creates a problem between the owner and the agent

because of the difference of mindset and the difference of the prominent interest. the

company has many contracts, for example the contract of work between the company

and its managers and the loan contract between the company and its creditors. The work

contract referred to in the writing of this paper is the employment contract between the

owner of capital and the manager of the company. Where between agent and principal

want to maximize their utility with information owned. But on the one hand, the agent

has more information than the principal on the other hand, resulting in asymmetry

13

information. More information owned by managers can trigger to perform actions in

accordance with the wishes and interests to maximize its utility. As for investors in this

case investors, it will be difficult to effectively control the actions taken by management

because it has little information available. Therefore, sometimes certain policies are

carried out by the management company without the knowledge of the owners of capital

or investor (Scott, 2000).

2.1.2. Profit Sharing Theory

Sharing System Based on Revenue is a revenue sharing system based on revenue

(revenue) earned before the costs incurred in the production process. The revenue

sharing scheme used as the basis for calculation is the sales / business income. Thus the

risks faced by the contracting parties are low. The owner of the fund only faces

uncertainty over the high low income of the business and does not face uncertainty over

business costs (cost of goods sold / production costs, sales costs and general and

administrative costs). The low risk in the revenue sharing scheme is certainly

accompanied by a decrease in the potential for the owners of funds to enjoy a higher

surplus which is contributed by the efficiency of business costs or the decrease in costs

at the time of the business activity down. Profit sharing scheme is a profit-sharing

scheme that should be used in sharia banking such as mudharabah or musyarakah

financing. On mudharabah financing is at least a gross profit sharing scheme. But now

the profit sharing scheme is not widely used because some sharia banks assume that the

risk is high. In addition, Islamic banks are still difficult to apply the scheme of profit

sharing because the reality does not generate great enthusiasm on the depositors who

are afraid of losing savings (Aswad, 2014).

2.2. Variable Review

2.2.1. CAMEL Ratios

This research use CAMEL ratio as its independent variables. CAMEL itself is one of

the approaches to analyze a bank that has been used in many countries. Assessment is

done in quantitative or qualitative method and is to ensure whether the bank is classified

as safe or not in accordance with the conditions specified (Gandapradja, 2004). It is

formed so that the level of bank health can be assessed. Through this approach, bank

14

can be categorized into a healthy bank, healthy enough, or unhealthy. For a healthy

bank, it should maintain its performance. In contrast, an unhealthy bank should increase

its performance. This valuation is important because to keep the bank able to perform

its functions properly by having sufficient capital, maintaining good asset quality, well

managed and operated on the basis of prudential principles, generate sufficient profit to

maintain its business continuity, and maintain its liquidity so that it can fulfil the

regulation of Bank Indonesia rules No. 9/24/DpBs about assesing the level of

healthiness of a bank based on the Sharia principles can be done by calculating the

factor of CAMEL. CAMEL consists of Capital, Asset Quality, Management, Earnings,

and Liquidity. This approach covers the aspects that can be used to assess the stability

of a bank (Fight, 2004). And each of these aspects can be measured through financial

ratios.

2.2.1.1. Capital

Banks must sets aside some of capital funds to be kept as reserve. According to Bank

Indonesia regulation No. 20/3/PBI/2018 about rupiah and foreign currencysStatutory

reserve requirements, reserve on Sharia bank should be more than 3% from its third

party fund. And later the capital will be used to anticipate when the bank is experiencing

any unexpected losses. Adequate capital is very important for the bank to ensure the

bank can remain well operated and perform its function properly. Capital aspect can be

measured using Capital Adequacy Ratio (Laluas, Mangantar, & Mekel, 2014).

CAR is the ratio derived from dividing the capital against risk weighted assets. Risk

weighted assets are assets measured with its risk (Fatima, 2014). Asset owned will be

categorized into several classes and calculated according to the respective weight. The

function is to tell bank's capability to absorb all loses before going bankrupt and lose

deposit funds. According to (Ikatan Bankir Indonesia, 2013), CAR can be measured

using this method:

𝐶𝑎𝑝𝑖𝑡𝑎𝑙

𝑅𝑖𝑠𝑘 𝑊𝑒𝑖𝑔ℎ𝑡𝑒𝑑 𝐴𝑠𝑠𝑒𝑡𝑠× 100%

(Eq. 2.1)

15

Since bank has important role in economy as what I have already explained in

background of the research. It is important to have regulations to ensure the funds

availability in meeting customer demand and need (Chinonye, 2011). Basel Committee

on Banking Supervision sets a minimum CAR 8% for every bank in Basel accord 1

which is then adopted by Bank Indonesia as the bank supervisory authority in

Indonesia. Keeping the CAR above 8% means that the bank has maintained overall

financial system stability and protects its customers. Bank which has a CAR above the

standard can be said that the bank can manage its capital well. The higher the CAR

ratio, the higher the bank's ability to support business growth, including covering

unexpected losses (Yusmad, 2018).

A. The impact of CAR on ROA

Theoretically, CAR describes the company's capital adequacy that serves to

accommodate the loss of the assets that may be risky. The higher this ratio, the

better the bank manages its capital to anticipate the unexpected losse (Ikatan Bankir

Indonesia, 2016). If a bank has a high CAR number, it means that funds set aside

for capital are high. It has a positive impact on the bank's ability on absorb

unexpected losses by using the fund reserve. In addition, Sharia bank involves the

risks derived from the model of financing based on profit-sharing principle where

profit snd losses are divided between the bank which provide financing with the

recipients of financing, Because there is the risk of losses if the project bank losses

and it will give negative impact for the bank (Centre for Strategic and Imternational

Studies, 2005). Reserve funds in the form of capital that already prepared can be

used in the future and affect the profit of the bank (Ismail, 2015). High capital means

high reserve so the amount of losses that can be reduced by using capital is bigger.

With the increasing reserve, the higher the ability of banks in increasing the amount

of profit belonging to banks and led to a rise in ROA (Hadinoto, 2008). It will bring

positive impact to the profitability. Thus, the greater the CAR, will result in

increasing ROA. Vice versa, if CAR decreases, then ROA will decrease (Armereo,

2015).

16

2.2.1.2. Asset Quality

Assessment on this aspect is done to assess the management of financing risk and

condition of bank asset. Asset quality assessment is intended to assess the condition of

bank assets as a mesurement of risk that bank have towards financing default, so bank

management can observe and analyze it periodically. So if there is a problem with asset,

bank management can anticipate immediately (Husein & Hasib, 2016).

For asset quality aspect can be measured by NPF ratio (Wangsawidjaja, 2012) . NPF

itself stands for Non Performing Financing which means status of credit consist of

substandard credit, doubtful, and loss financing. NPF is a term used for Sharia bank in

replacement of NPL which used for conventional bank (Ikatan Bankir Indonesia, 2018)

the ratio of Non Performing Financing is the ratio obtained by calculating total non

performing financing from its total financing. (Yusmad, 2018). There are two types of

NPF, those are gross NPF and NPF net. The difference between these two is NPF net

exclude CKPN from the total of NPF, in the other hand, the gross of NPF is not (Ikatan

Bankir Indonesia, 2014). As a matter of this research, the researcher will use net NPF

as representative for asset quality aspect on CAMEL. Due to net NPF excludes losses

has already recognised by the bank, therefore it represents the potential of additional

loss of the bank (Resolving non-performing loans in Europe, 2017). According to OJK

circular letter No.18/SEOJK.03/2015, the formula of net NPF is stated below

𝑁𝑜𝑛 𝑃𝑒𝑟𝑓𝑜𝑟𝑚𝑖𝑛𝑔 𝐹𝑖𝑛𝑎𝑛𝑐𝑖𝑛𝑔 −𝑃𝑟𝑜𝑣𝑖𝑠𝑖𝑜𝑛 𝑓𝑜𝑟 𝐹𝑖𝑛𝑎𝑛𝑐𝑖𝑛𝑔 𝑙𝑜𝑠𝑠𝑒𝑠

𝑇𝑜𝑡𝑎𝑙 𝐹𝑖𝑛𝑎𝑛𝑐𝑖𝑛𝑔× 100%

(Eq. 2.2)

Banks are required to good standard of net NPF in a bank to maintain the level of trust

from the people (Khotibul, 2016). According to Bank Indonesia Regulation Number

6/10 / PBI / 2004, if the ratio of net NPF is above 5%, meaning that the bank has poor

quality assets. Good bank is the one which has Net NPF below 5% which means the

bank has managed to manage its assets well.

17

A. Impact of NPF toward ROA

Theoretically, NPF describes the quality of assets owned by Islamic banks, low in this

ratio, the better the bank in managing financing with its risk. If a bank has a high NPF

ratio, the number of problem assets owned by the bank is high (Wangsawidjaja,

Pembiayaan Bank Syariah, 2013). It has a bad impact on the profit that will be obtained

by the bank because funds that have been used as financing to borrower will not return,

but it is also profit from financing that failed to get (Arifi, 2012). The funds owned by

these banks are getting smaller and rarely to be used in their daily activities, and that

leads to the decline in profits and its ROA. It will bring negative impact to the

profitability .Thus, the greater the NPF, will result in decreasing ROA. Vice versa, if

NPF decreases, then ROA will increase (Zulfiah & Susilowibowo, 2014).

2.2.1.3. Management

According to Bank Indonesia regulation No. 6/10/PBI/2004 about system rating of

health of commercial banks and management assessment, is done qualitatively and

quantitatively to the following components:

a. General Management

b. Implementation of risk management system

c. Bank's decision on the provisions as well as commitments to Indonesian banks

and / or other parties.

In addition to use the financial statements, the assessment should also be done by

interviewing and filling the survey by the relevant bank.

The assessment conducted by using around a hundred questionnaires is classified into

two major groups, ,there are: general management and the risk management

questionnaire. General management questionnaire is further divided into subgroups of

questions related to strategy, structure, system, human resources, leadership, and work

culture. Meanwhile, risk management questionnaire is divided into sub-categories

related to liquidity risk, market risk, credit risk, operational risk, legal risk and risk of

owners and managers. However, qualitative assessment is quite difficult to use because

it is confidential.

18

Management aspects can be reflected by using Net Profit Margin. Due to operating

income itself reflects the results of strategies made by banks to generate operating

income. Besides, Net income itself is the result of liquidity risk management, credit,

operational risk, legal risk, and owner risk (Jacob, 2013). Net Profit Margin is ratio that

shows financial condition at certain period and the efficiency level of bank (Bellalah &

Masood, 2013). NPM can be found through this formula (Laluas, Mangantar, & Mekel,

2014),

𝑁𝑒𝑡 𝑃𝑟𝑜𝑓𝑖𝑡

𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔 𝐼𝑛𝑐𝑜𝑚𝑒× 100%

(Eq. 2.3)

A. Impact of NPM toward ROA

Theoretically, Net Profit Margin describes the quality of a bank's management in

applying its strategy and managing its risks to generate income. If a bank has high NPM,

then the bank has good management aspect that comes from planning and executing a

strategy nicely and managing all possible risks that cause failure in applying the

strategy. If a strategy of a bank in finding incomes is success, then, the incomes will be

received. If a strategy of quality management from a bank is high, which is represented

by NPM, the income will also be higher. It means that the higher its ratio, the better the

bank's management in generating income. If a bank has a high NPM ratio, the amount

of income received will also be high. It has a good impact on the total profit earned by

the bank. It will bring positive impact to the profitability. Thus, the greater the NPM,

the higher the ROA will be since ROA put profit to its account. Vice versa, if NPM

decreases, then ROA will decrease (Indyarwati, 2017).

2.2.1.4. Earnings

Earnings aspect assesses the condition and ability of banks in obtaining profit in order

to support operational activities and provide capital. A bank can be said to be healthy

if its profit is high, so that it can have a high assessment of earnings aspect too.

Earnings aspect can be represented by Net Interest Margin. NIM is the amount of

interest earned and paid by the bank to average productive assets and banks usually use

19

NIM, but NIM use the amount of interest income earned but Sharia banks adopt 0%

interest (Anwar, 2016). So this research will be using Net Operating Margin or NOM

that include income from profit and loss sharing instead of interest. NOM is a ratio that

measures the ability of banks to process their productive asset to generate income.

According to Bank Indonesia, a healthy bank is a bank which has NOM is 8% and or

greater. According to OJK circular letter No.18/SEOJK.03/2015, NOM can be

measured through this formula:

𝐼𝑛𝑐𝑜𝑚𝑒 𝑓𝑟𝑜𝑚 𝑝𝑟𝑜𝑓𝑖𝑡 𝑠ℎ𝑎𝑟𝑖𝑛𝑔 −𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑜𝑛𝑎𝑙 𝑒𝑥𝑝𝑒𝑛𝑠𝑒

𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝑃𝑟𝑜𝑑𝑢𝑐𝑡𝑖𝑣𝑒 𝐴𝑠𝑠𝑒𝑡× 100%

(Eq. 2.4)

A. Impact of NOM toward ROA

Theoretically, NOM portrays the ability of bank to use their productive asset to generate

operating income (Anwar, 2016). The higher the ratio, more efficient the bank is in

using its productive assets to generate operating income. By using its productive assets

efficiently, bank can get more income from its limited assets. Increasing in operating

income lead to higher net income. It will give positive impact on ROA since ROA also

include net income. It will bring positive impact to the profitability. Thus, the greater

the NOM, will be giving impact on high ROA. Vice versa, if NOM decreases, ROA

will decrease (Trisnigtyas & Mutaher, 2013).

2.2.1.5. Liquidity

Liquidity is the ability of the bank to meet its financial obligations when it’s due. A

bank is declared liquid if the bank can fulfil its debt obligations, can repay all customer

deposits, and can fulfil the loan request without problem (Rachmawati, 2017). With a

deposit that can be taken at any time, the bank must pay attention to its liquidity that

can be monitored from the Loan to Deposit ratio. LDR can be calculated by comparing

the loan amount to the bank deposit. it is shows the bank's ability to pay all the customer

deposit withdrawal by using credit given as liquidity source. Since this research use

20

Sharia bank as its research subject, then the researcher will use Financing to Deposit

Ratio instead of LDR because Loan to Deposit Ratio is for conventional bank which

use interest for its loan. While Sharia banks adopt 0% of interest financing so the ratio

will be financing deposit ratio.

Financing to Deposit ratio is the ratio of financing to the funds received. This ratio

shows the amount of funds used in financing (Yusmad, 2018). According to OJK

circular letter No.18/SEOJK.03/2015, FDR can be found through this formula

𝑇𝑜𝑡𝑎𝑙 𝐹𝑖𝑛𝑎𝑛𝑐𝑖𝑛𝑔

𝑇ℎ𝑖𝑟𝑑 𝑝𝑎𝑟𝑡𝑦 𝑓𝑢𝑛𝑑× 100%

(Eq. 2.5)

According to Bank Indonesia, a bank with good liquidity is a bank that has LDR

Between 85% - 100%. The lower the FDR ratio, more liquid the bank. So the bank can

easily fulfill its obligations.

A. Impact of FDR toward ROA

Theoretically, FDR visualizes the ability of bank to fulfil their debt obligation. It can

repay all customer deposits, and fulfil the loan request without any problems

(Rachmawati, 2017). The lower this ratio, more funds available to the bank. If a bank

has a low FDR number, it means that the amount of bank funds deposited is more than

the deposit that the bank gives to the borrowers as financing. Thus, the rest of deposit

will remain at bank and cannot be used to generate profits (Suryani, 2011). So if the

FDR of a bank is low, then the likelihood of getting profit is also low. Low in profit

means a negative impact on ROA obtained by banks. It will bring positive impact to

the profitability . Thus, the greater the FDR, will result in the higher of ROA. Vice

versa, if the FDR decreases, the ROA will decrease (Armereo, 2015).

2.2.2. Profitability

This research uses profitability as its dependent variable. Profitability is the ability of

banks in the search for profit. In addition, this aspect also becomes a symbol of

effectiveness and efficiency of the company in conducting its business. Investors are

able to see the profit that they will get from investing in a company and the basis of the

decision to continue with investing or not. As for potential investors, profitability can

21

be made for a comparison tool with other companies in the same industry to decide

where they should invest their money. To measure profitability, various ways can be

used and one of them is using the ratio.

Profitability ratio is a ratio that measures the ability of a company in searching for profit

that are coming from sales and investment income (Kasmir, 2009).

For profitability aspect, the researcher uses return on assets ratio to be a measurement

tool on how effective the management of a business are in generating profit from its

assets. ROA is the ratio derived from dividing the net income against average total

assets. The higher the ratio, more profitable the company (Gitman & Joenk, 2008).

According to OJK circular letter No.18/SEOJK.03/2015, ROA can be measured using

this method:

𝑁𝑒𝑡 𝐼𝑛𝑐𝑜𝑚𝑒

𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝑇𝑜𝑡𝑎𝑙 𝐴𝑠𝑠𝑒𝑡𝑠× 100%

(Eq. 2.6)

2.3. Research Gap

Various studies which use CAMEL ratios as independent variables, profitability as

dependent variables that have been carried out, and summarized in the Table 2.1,

Table 2.1 Previous Research

Name of

Researcher

Year Title of

Research

Independent

Variables

Analysis

Instrument

Result

Cystha

Armereo

2014 Analysis

Factor

Affecting

Profitability of

Syariah Bank

Listed on

Indonesia

CAR

FDR

NPF

Multiple

linear

regression

CAR and

FDR has

positive but

significant

toward ROA.

While NPF

has negative

22

Name of

Researcher

Year Title of

Research

Independent

Variables

Analysis

Instrument

Result

Stock

Exchange

Indonesia

and

significant

toward ROA.

Fathya

Khaira

Ummah and

Edy

Suprapto

2015 Factor

Affecting

Profitability of

Muamalat

Bank

CAR

Cost to

Income Ratio

NPF

FDR

Vector

Error

Correction

First analysis

by using short

term VECM,

the result are

CAR and NPF

not has

significant

influence

toward

probability of

Muamalat

Bank. And

Cost to

Income Ratio

and FDR has

negative and

significant

influence

toward ROA.

Second

analysis by

using long

term VECM,

the result are

CAR and NPF

has negative

but significant

23

Name of

Researcher

Year Title of

Research

Independent

Variables

Analysis

Instrument

Result

influence

toward ROA

Cost to

Income Ratio

and FDR has

negative and

significant

influence

toward ROA.

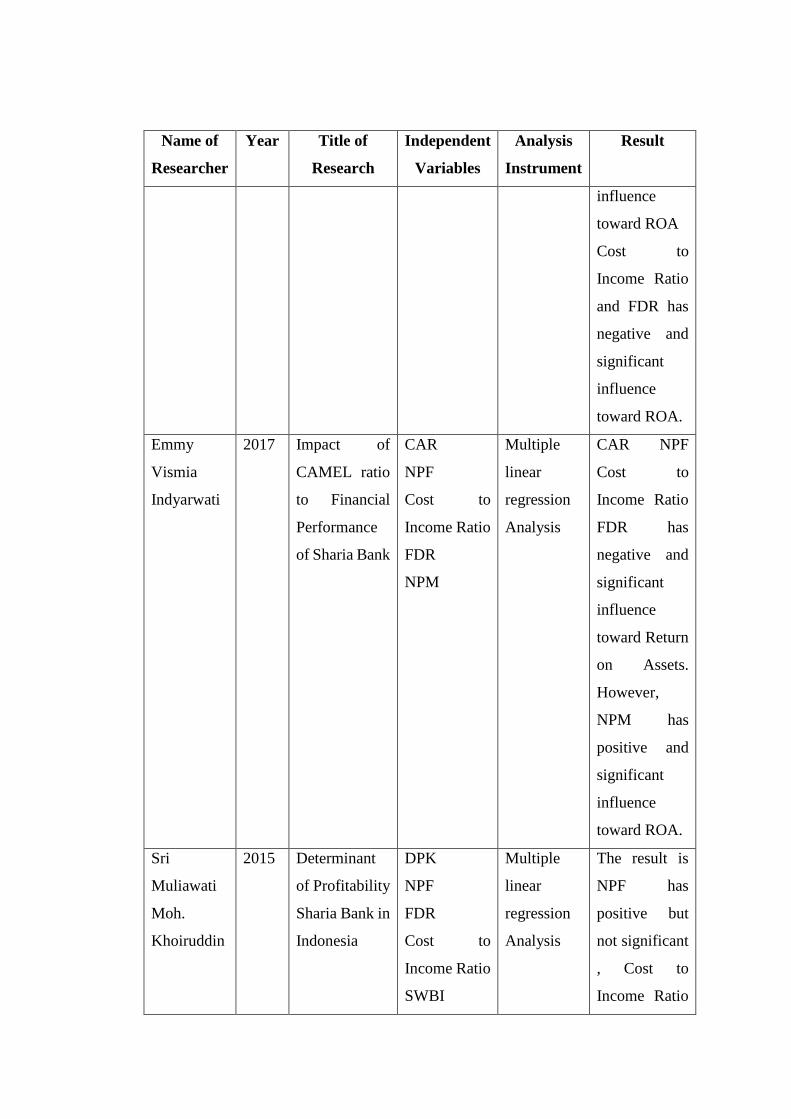

Emmy

Vismia

Indyarwati

2017 Impact of

CAMEL ratio

to Financial

Performance

of Sharia Bank

CAR

NPF

Cost to

Income Ratio

FDR

NPM

Multiple

linear

regression

Analysis

CAR NPF

Cost to

Income Ratio

FDR has

negative and

significant

influence

toward Return

on Assets.

However,

NPM has

positive and

significant

influence

toward ROA.

Sri

Muliawati

Moh.

Khoiruddin

2015 Determinant

of Profitability

Sharia Bank in

Indonesia

DPK

NPF

FDR

Cost to

Income Ratio

SWBI

Multiple

linear

regression

Analysis

The result is

NPF has

positive but

not significant

, Cost to

Income Ratio

24

Name of

Researcher

Year Title of

Research

Independent

Variables

Analysis

Instrument

Result

has negative

and

significant

influence on

ROA. While

FDR has

negative but

not significant

influence on

ROA and

DPK has

positive and

significant

influence

towards ROA

Suci Inayati

2014 Analysis the

impact of

CAMEL

Ratios to

profitability

Syariah Bank

listed in Bank

Indonesia

CAR

NPF

Cost to

Income Ratio

FDR

NOM

Multiple

linear

regression

Analysis

CAR has

negative but

not significant

influence

toward Return

on Assets.

However,

NPF Cost to

Income Ratio

has negative

and

significant

influence

toward ROA.

Meanwhile,

25

Name of

Researcher

Year Title of

Research

Independent

Variables

Analysis

Instrument

Result

FDR has

positive but

not significant

toward Return

on Assets.

However,

NOM has

positive and

significant

influence

toward ROA.

Source: International journal and books

This study has been made due to research gap from previous research conducted by

other research which has same topic. The gap comes from any difference exist between

those research, for example period, sample, population, variable both independent or

dependent variable, research method, or the result. This research uses internal factor

from a bank thus are CAMEL ratio that consists of CAR, NPF, NPM, NOM, and FDR

as independent variable, while ROA as dependent variable. Instead, research from

(Indyarwati, 2017) used other camel ratios to seek for its impact on profitability of

Sharia bank, which is using Cost to Income Ratio for earnings aspect.

The other researchers have different result on their research, for example as the research

held by research held by (Armereo, 2015), CAR has a positive and significant influence

towards ROA But another study held by (Inayati, 2014), CAR has negative but not

significant towards ROA. Other different result shows from research of (Ummah &

Suprapto, 2015) that shows NPF has negative but not significant influence towards

ROA while research from (Inayati, 2014) that shows NPF has negative but significant

influence towards ROA. Then research from (Anggita, 2012) that shows NPM has

negative and not singificant influence towards ROA while (Indyarwati, 2017) that

26

shows NPM has positive and significant influence towards ROA. Then research from

(Inayati, 2014) shows NOM has positive and significant nfluence towards ROA while

(Purnamasari & Ariyanto, 2016) that shows NOM has positive but not significant

influence towards ROA. Then research from (Muliawati & Khoiruddin, 2015) shows

FDR has negative but not significant influence towards ROA while (Indyarwati, 2017)

that shows FDR has negative and significant influence towards ROA.

This research contains the renewable period which is 2015-2017 and more bank as

samples. Also, the researcher will use some of different ratios for represent CAMEL.

Thus, this research objective is intended to fill the research the gap in the study.

This research wants to find out the influence of every independent variable partially to

variable dependent and find out the effect of independent variables simultaneously to

the dependent variable. There are 6 hypotheses that will be tested out and the result will

be stated in chapter 4. Based on the literature review and problem statement, the

researcher builds a theoretical framework as shown in Figure 2.1. It is based on the

title of this research “Impact of CAMEL Ratios toward Profitability of Sharia Banks in

Indonesia”.

Figure 2.1 Theoretical Framework

Source: The researcher

27

CHAPTER III

RESEARCH METHODOLOGY

This chapter 3 contains a research methodology that explains what methods are used in

both data processing and analysis. The contents of this chapter are research framework,

hypotheses, operational definition, research design, and sampling plan.

3.1. Research Framework

Figure 3.1 Research Framework

Source: The Researcher

3.2. Hypotheses

Hypothesis is preconceived notions about the results of research by researchers. But not

just any hypotheses can made. The hypothesis of this research is taken based on the

background issues, the formulation of problems, the purpose of the research and

literature review which had been done before.The study will be conducted to test the

28

truth of the hypothesis have been made. Then the researcher built the hypothesis for

this research below:

H01= There is a significant influence of CAR towards ROA of Sharia bank.

Ha2 = There is no significant influence of CAR towards ROA of Sharia bank.

H01= There is a significant influence of NPF towards ROA of Sharia bank.

Ha2 = There is no significant influence of NPF towards ROA of Sharia bank.

H01= There is a significant influence of NPM towards ROA of Sharia bank.

Ha2 = There is no significant influence of NPM towards ROA of Sharia bank.

H01= There is a significant influence of NOM towards ROA of Sharia bank.

Ha2 = There is no significant influence of NOM towards ROA of Sharia bank.

H01= There is a significant influence of FDR towards ROA of Sharia bank.

Ha2 = There is no significant influence of FDR towards ROA of Sharia bank.

H01= There is a significant influence of CAR, NPF, NPM, NOM, FDR toward ROA of

Sharia bank.

Ha2 = There is no significant influence of of CAR, NPF, NPM, NOM, FDR toward

ROA of Sharia bank.

3.3. Operational Definition

Operational definition is to explain the variables to be researched with an indicator for

the variables are easily measured (DR. Juliansyah Noor, 2017). Indicator can be

determined by looking at traits characteristics, related aspects, and behaviors. The

indicator will lead us to measure the concept of a variable significantly within the scope

of our research. Variables owned are still vague and too large scope, but in this

operational definition we will reinforce the definition of these variables so that

sampling research will be more accurate in accordance with the purpose of research.

This section will explain more about the variables used are ratio camel and profitability

Sharia bank in detail.

29

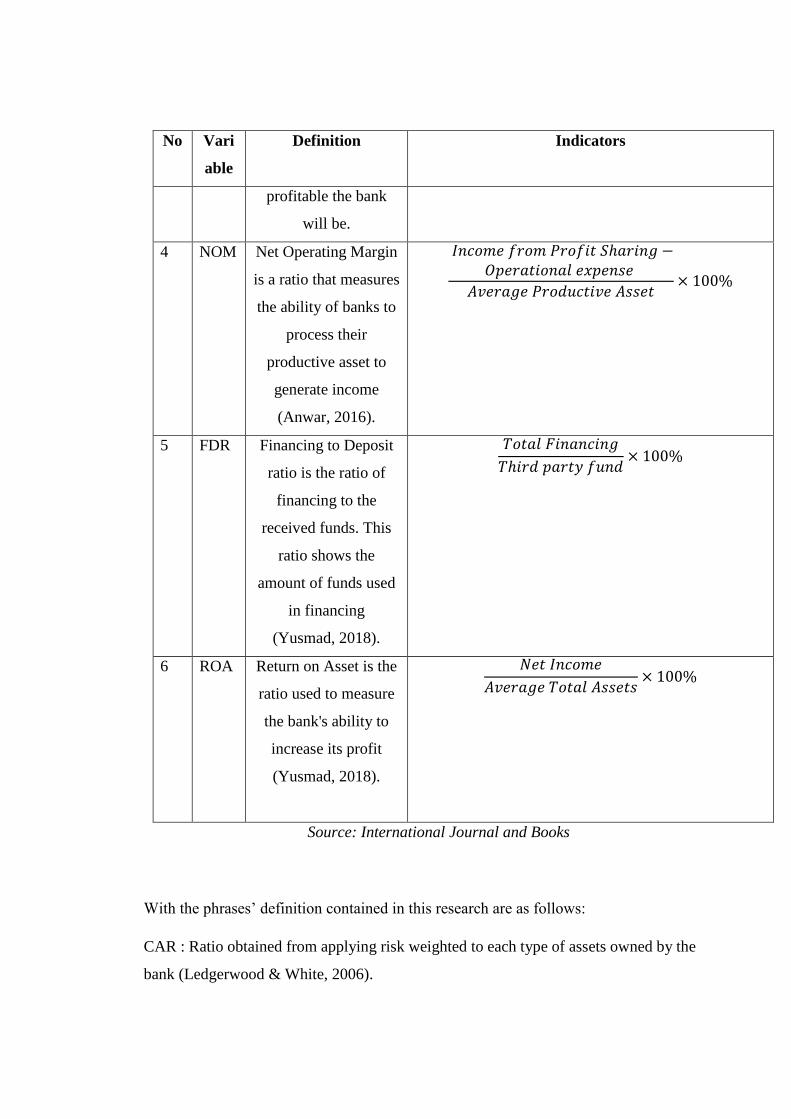

Table 3.1 Operational Definition

No Vari

able

Definition Indicators

1 CAR Capital Adequacy

ratio is the ratio

obtained from

applying risk weighted

to each type of assets

owned by the bank

(Ledgerwood &

White, 2006). This is

done in order to know

the amount of risk

owned by the bank.

𝐶𝑎𝑝𝑖𝑡𝑎𝑙

𝑅𝑖𝑠𝑘 𝑊𝑒𝑖𝑔ℎ𝑡𝑒𝑑 𝐴𝑠𝑠𝑒𝑡× 100%

2 NPF

Net

Net NPF is the ratio

after the non

performing financing

is reduced the

allowance for

impairment losses

(Ikatan Bankir

Indonesia, 2014).

𝑁𝑜𝑛 𝑃𝑒𝑟𝑓𝑜𝑟𝑚𝑖𝑛𝑔 𝐹𝑖𝑛𝑎𝑛𝑐𝑖𝑛𝑔 −𝑃𝑟𝑜𝑣𝑖𝑠𝑖𝑜𝑛 𝑓𝑜𝑟 𝑓𝑖𝑛𝑎𝑛𝑐𝑖𝑛𝑔 𝑙𝑜𝑠𝑠𝑒𝑠

𝑇𝑜𝑡𝑎𝑙 𝐹𝑖𝑛𝑎𝑛𝑐𝑖𝑛𝑔× 100%

3 NPM Net Profit Margin is

ratio that shows

financial condition at

certain period and the

efficiency level of

bank (Bellalah &

Masood, 2013). The

higher the NPM ratio,

more efficient and

𝑁𝑒𝑡 𝑃𝑟𝑜𝑓𝑖𝑡

𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔 𝐼𝑛𝑐𝑜𝑚𝑒× 100%

30

No Vari

able

Definition Indicators

profitable the bank

will be.

4 NOM Net Operating Margin

is a ratio that measures

the ability of banks to

process their

productive asset to

generate income

(Anwar, 2016).

𝐼𝑛𝑐𝑜𝑚𝑒 𝑓𝑟𝑜𝑚 𝑃𝑟𝑜𝑓𝑖𝑡 𝑆ℎ𝑎𝑟𝑖𝑛𝑔 −𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑜𝑛𝑎𝑙 𝑒𝑥𝑝𝑒𝑛𝑠𝑒

𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝑃𝑟𝑜𝑑𝑢𝑐𝑡𝑖𝑣𝑒 𝐴𝑠𝑠𝑒𝑡× 100%

5 FDR Financing to Deposit

ratio is the ratio of

financing to the

received funds. This

ratio shows the

amount of funds used

in financing

(Yusmad, 2018).

𝑇𝑜𝑡𝑎𝑙 𝐹𝑖𝑛𝑎𝑛𝑐𝑖𝑛𝑔

𝑇ℎ𝑖𝑟𝑑 𝑝𝑎𝑟𝑡𝑦 𝑓𝑢𝑛𝑑× 100%

6 ROA Return on Asset is the

ratio used to measure

the bank's ability to

increase its profit

(Yusmad, 2018).

𝑁𝑒𝑡 𝐼𝑛𝑐𝑜𝑚𝑒

𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝑇𝑜𝑡𝑎𝑙 𝐴𝑠𝑠𝑒𝑡𝑠× 100%

Source: International Journal and Books

With the phrases’ definition contained in this research are as follows:

CAR : Ratio obtained from applying risk weighted to each type of assets owned by the

bank (Ledgerwood & White, 2006).

31

NPL: ratio used to measure asset quality of a conventional bank (Ikatan Bankir

Indonesia, 2018)

NPF: ratio used to measure asset quality of a Sharia bank (Wangsawidjaja, Pembiayaan

Bank Syariah, 2012)

NPM: ratio that shows financial condition at certain period and the efficiency level of

bank (Bellalah & Masood, 2013).

NIM : ratio can be used to measure earnings aspect in a conventional bank (Anwar,

2016)

NOM : ratio that measure measures the ability of Sharia banks to process their

productive asset to generate income (Anwar, 2016).

LDR: ratio used to measure liquidity condition of a conventional bank (Yusmad, 2018).

FDR: ratio of financing to the received funds. This ratio shows the amount of funds

used in financing (Yusmad, 2018).

ROA: ratio used to measure profit earned. This ratio can measure the bank's ability to

earn its profit (Yusmad, 2018).

3.4. Research Design

Design research is a strategy that holds the method, processes, procedures, and

techniques that researchers need in conducting a study. This will be used for providing

specific direction for procedures in a research study including data measurement,

collection, and analysis. The research design also means the process of research process

which can be divided into two, namely research planning that starts from identification,

choosing and problem formulation, up to the formulation of hypothesis and its relation

with existing theory and reference. Second is the implementation of research or

operational research process (Sekaran & Bougie, 2013).

Research problem will determine the research design used. The usefulness of research

design is as a guide for researchers in the process of research so that the evidence

collected can effectively address the problem in a study in accordance with the purpose

of research (Vogt, Gardner, & Haeffele, 2012). When research is made without research

32

design, then the problem cannot be delivered properly which leads to the conclusion

drawn will be weak and not convincing.

Research design has 3 methods to choose, there are: Quantitative methods, Qualitative

methods, and Mixed method. Quantitative method is a research method has objective

to test the existed theory by making hypothesis from the data collected and make a

summarization from the hypothesis. Qualitative method is used to identify an issue or

to describe a certain phenomenon from the participant’s point of view. While Mixed

method is a research method that use both quantitative and qualitative method. It can

be quantitative design and supported by qualitative, or qualitative design that is

supported by quantitative or to use both of them in a balance (Creswell & Creswell,

2017).

Quantitative research method will be used for this research because this research is to

test the existed theory and to use the data collected in which it will be analyzed using

statistic, clear planning of research which has been set before the research started as a

guideline of the research. It matches with the criteria of research that uses quantitative

method.

By using quantitative research method, the data are analyzed with descriptive analysis

and inferential analysis that will be done with the help of Statistical Package for Social

Science (SPSS) 20.0 software and can be described as follows:

A. Descriptive Analysis

Descriptive analysis is an analysis that seeks to describe data that have been collected

first without any conclusion (Purwanto, 2007). In this analysis, the presentation of data

are more emphasized in the form of statistical measurements for example mean,

minimum, maximum, and standard deviation. However, this kind of analysis is created

to visualize or analyze the statistic of the data, and is not just getting its summary. It is

done in order to make the data easier to be summarized and interpreted (Juliandi, Irfan,

& Manurung, 2014).

In this case, the researcher will use minimum, maximum, mean, and standard valuation.

Minimum is the smallest value from a data set, while maximum is the largest value.

33

Mean is the average from a data set and standard deviation is a variance of data set

around its mean (Tampomas, 2003).

B. Inferential Analysis

Inferential analysis is an analysis derived from research on the sample data held

(Purwanto, 2007). The usage of inferential analysis in quantitative research is as a basic

of hypothesis and to support the development of the research’s instrument, as a basic

of the planning of the research, as an analyses in creating a planning of research, as an

analyses in deciding the sample of research, and as a tool to manage and analyze the

result of research.

Sample of the research is used to draw general conclusions on the population according

to the problem of the research. This part of analysis will test the significance and level

of inferential error. Both of them will be used to identify an error in generalization. At

the end, the researcher will make a conclusion based on the result from inferential

analysis (Sutopo & Slamet, 2017).

1. Classical Assumption Test

The classical assumption is the statistical requirement that must be fulfilled in the use

of multiple linear regression with ordinary least square method (Sutopo & Slamet,

2017). There are 4 types of test in the classical assumption test. These tests are tested

for normality, heteroscedasticity, autocorrelation, and multicollinearity tests (Juliandi,

Irfan, & Manurung, 2014). There are many tests to choose from for those four test types.

Further details about the test can be seen below:

a. Normality Test

Normality test is a test to determine whether the research data has a normal distribution

or not (Juliandi, Irfan, & Manurung, 2014). This test is used to test whether a particular

value is significantly different or not with the average of a sample (Purwanto, 2007).

This study used a parametric statistic that requires normal distributed data. In other

words, the data which will be analyzed using parametric statistic must satisfy the

assumption of normality. Because if the data is not normally distributed then the usage

of T-test and F-test are invalid. The research should use non parametric statistic because

34

the T-test and the F-test are derived from the assumption of y or e are normally

distributed. The reason for abnormal data is because the data contained extreme data

(Sahai & I, 2007).

Testing of normality can be done with Kolmogorov Simonov. This research uses

statistical methods are compared with chart method because it can more easily

determine normality by using figures identified as determining normality, whereas the

graphic method is too subjective. By creating a null hypothesis that has been formed,

then data will be tested by the criteria below:

1. By comparing Kolmogorov Smirnov with Kolmogorov Smirnov table. When

Kolmogorov Smirnov smaller than Kolmogorov Smirnov from the table then a null