icra online ltd - mutual fundmutualfundindia.com/images/research/pdfpaths... · icra online ltd a...

TRANSCRIPT

ICRA Online LtdA group ICRA company

April, 2015

Mutual Fund Screeners

MUTUAL FUND INDUSTRY OVERVIEW

Section I

ICRA Online Limited22/05/2015 2

Industry AUM expands again in Apr’15

ICRA Online Limited22/05/2015 3

1. Second consecutive month of correction in

equity markets during April ‘15 couldn’t deter

the MF players from buying as the industry

AUM breached Rs. 11 lakh crore mark for the

fourth time since Nov ‘14.

2. Selling by the Foreign Institutional Investors

(FIIs) amid uncertainties on tax issues hurt

market sentiment.

3. Industry corpus grew 10% during Apr’15, after

witnessing a steep fall in the previous month.

4. The top-10 AMCs contributed close to 80% of

the industry corpus.

5. While the AUM of top-10 rose by 8.6%

during the month, the next-10 (corpus range

7K-25K Crore) surpassed the bigger AMCs

with a growth rate of 13.2%.

-5%

9%

2%

-10%

10%

-15%

-10%

-5%

0%

5%

10%

15%

1,000,000

1,050,000

1,100,000

1,150,000

1,200,000

1,250,000

Dec-14 Jan-15 Feb-15 Mar-15 Apr-15

Ch

an

ge i

n c

orp

us

(M-o

-M)

Ind

ust

ry

Co

rp

us

(In

Rs.

Cro

re)

MF Industry Corpus

Industry Corpus % Change (M-o-M)

Source: MFI Explorer

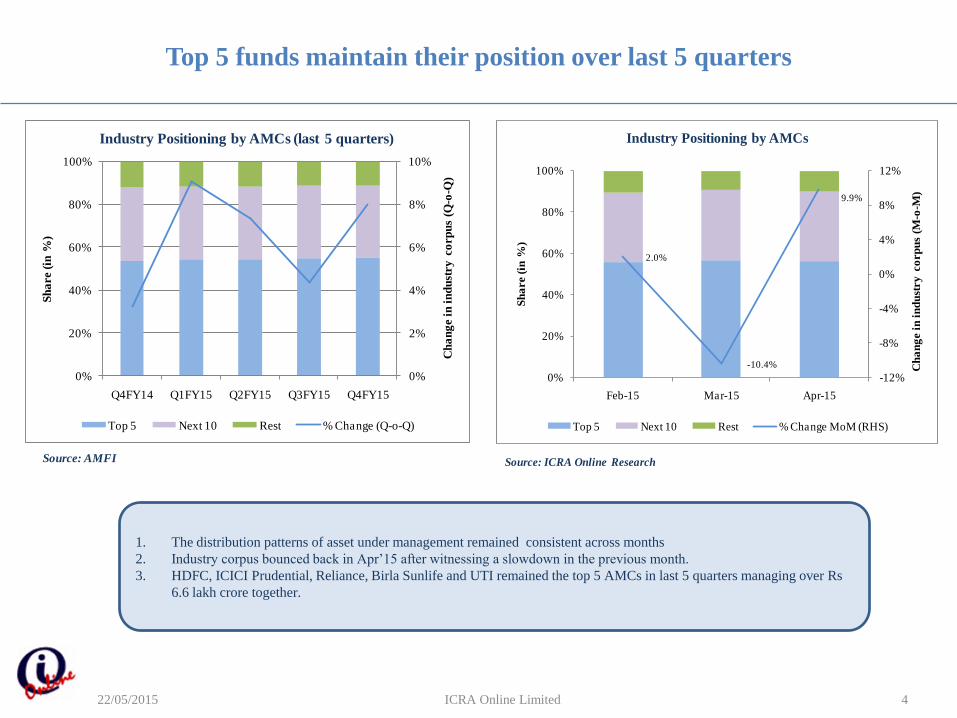

Top 5 funds maintain their position over last 5 quarters

ICRA Online Limited22/05/2015 4

1. The distribution patterns of asset under management remained consistent across months

2. Industry corpus bounced back in Apr’15 after witnessing a slowdown in the previous month.

3. HDFC, ICICI Prudential, Reliance, Birla Sunlife and UTI remained the top 5 AMCs in last 5 quarters managing over Rs

6.6 lakh crore together.

0%

2%

4%

6%

8%

10%

0%

20%

40%

60%

80%

100%

Q4FY14 Q1FY15 Q2FY15 Q3FY15 Q4FY15

Ch

an

ge i

n i

nd

ust

ry

co

rp

us

(Q-o

-Q)

Sh

are (

in %

)

Industry Positioning by AMCs (last 5 quarters)

Top 5 Next 10 Rest % Change (Q-o-Q)

Source: AMFI

2.0%

-10.4%

9.9%

-12%

-8%

-4%

0%

4%

8%

12%

0%

20%

40%

60%

80%

100%

Feb-15 Mar-15 Apr-15

Ch

an

ge i

n i

nd

ust

ry

co

rp

us

(M-o

-M)

Sh

are (

in %

)

Industry Positioning by AMCs

Top 5 Next 10 Rest % Change MoM (RHS)

Source: ICRA Online Research

Equities witness record inflows in April ‘15

ICRA Online Limited22/05/2015 5

1. Income fund category witnessed a fall in market share from

46.26% in Mar’15 to 45.83% in Apr ‘15.

2. However, equity fund category managed to increase its market

share from 23.86% in Mar ‘15 to 24.50% in Apr ‘15.

1. Equity category continued to attract healthy inflows for past 12

months. The category witnessing record inflow of Rs 10.4K

crore in Apr ’15, second highest since Jul ‘14.

2. Liquid/Money market witnessed an inflow of Rs. 1 lakh crore,

reversing previous month’s 1.1 lakh crore outflow.

45.83%

22.01%

24.50%

3.23%

2.00%

0.68%

0.81%0.26%

0.57%

0.11%

7.66%

Category wide distribution of industry corpus for TTM

Income

Liquid/Money Market

Equity

ELSS - Equity

Balanced

Gold ETF

Gilt

FoFs Investing Overseas

Other ETFs

Infrastructure Debt Fund

Source: AMFI, ICRA Online Research, Data is as on Apr-2015, TTM-Trailing twelve months

Bottom 7 categories

-20,000 0 20,000 40,000 60,000 80,000 100,000

Income

Infrastructure Debt Fund

Equity

Balanced

Liquid/Money Market

Gilt

Elss - Equity

Gold Etf

Other Etfs

FoFs Investing Overseas

In Rs. Crore

Net Inflow/Outflow pattern for TTM

Source: AMFI, Data is as on Apr-2015, TTM-Trailing twelve months

350,000

400,000

450,000

500,000

550,000

Income

50,000

100,000

150,000

200,000

250,000

300,000

Liquid/Money Market

50,000

100,000

150,000

200,000

250,000

300,000

350,000

Equity

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

ELSS - Equity

0

5,000

10,000

15,000

20,000

25,000

30,000

Balanced

0

3,000

6,000

9,000

12,000

Gold ETF

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Gilt

0

1,000

2,000

3,000

4,000

FoFs Investing Overseas

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Other ETFs

0

200

400

600

800

1,000

1,200

1,400

1,600

Infrastructure Debt Fund

Category Movement Monitor for Trailing Twelve Months

ICRA Online Limited22/05/2015 6

Source: AMFI

1. Equity and Balanced fund category see a steady rise in AUM.

Category Specific Deep Dive : Equity & Income

ICRA Online Limited22/05/2015 7

1. Sensex took a hit of 3.4% in Apr’15, posting losses for

second consecutive month.

2. However, the equity fund category managed to see record

inflow of Rs. 10,406 in Apr ‘15.

1. Income fund corpus witnessed a marginal fall of 0.2% M-

o-M in Apr’15 (at Rs. 5.14 lakh crore).

2. Income fund category managed to limit the outflow (at Rs

2,510 crore in Apr’15) after witnessing significant outflow

in the previous month.

-10

-5

0

5

10

-

2,000

4,000

6,000

8,000

10,000

12,000

Ap

r-1

4

Ma

y-1

4

Jun

-14

Jul-

14

Au

g-1

4

Sep

-14

Oct-

14

No

v-1

4

Dec-1

4

Jan

-15

Feb

-15

Ma

r-1

5

Ap

r-1

5

Sen

sex

Mo

nth

ly r

etu

rn

(in

%)

Net

flo

w (

in R

s. c

ro

re)

Equity category flow vis-a-vis Sensex

Net Inflow/Outflow Sensex Returns M-o-M (RHS)

Source: AMFI, BSE

-15,000

-10,000

-5,000

0

5,000

10,000

15,000

20,000

25,000

Ap

r-1

4

Ma

y-1

4

Jun

-14

Jul-

14

Au

g-1

4

Sep

-14

Oct-

14

No

v-1

4

Dec-1

4

Jan

-15

Feb

-15

Ma

r-1

5

Ap

r-1

5

420,000

440,000

460,000

480,000

500,000

520,000

540,000

Net

flo

w (

In R

s. c

ro

re)

Co

rp

us

(In

Rs.

cro

re)

Income AUM vis-a-vis net flows

Corpus (RHS) Net Inflow/Outflow

Source: AMFI

SAMPLE ANALYSIS OF SOME SELECT AMC’S/REGION

Section II

ICRA Online Limited22/05/2015 8

Mutual Fund AUM Monitor for BIG-5

ICRA Online Limited22/05/2015 9

1. All the top-5 AMCs witnessed net inflows

during Apr’15, compared to the large

outflows seen in the preceding month.

2. Second consecutive month of correction in

domestic equity market couldn’t deter the

top-5 AMCs from buying equities as

evidenced by the net positive inflows

3. Birla Sun Life MF witnessed the highest

inflow followed up by ICICI and UTI MF.

4. The Big-5 together have close to 56% of the

market share

5. As on Apr’15 there were 10 mutual funds

with AUM below Rs 2,000 crore.

Source: ICRA Online research

6.4

8.27.0

11.7

13.2

0

2

4

6

8

10

12

14

0

30,000

60,000

90,000

120,000

150,000

180,000

HDFC MF ICICI Pru Reliance

MF

Birla MF UTI MF

% G

ro

wth

in

AU

M (

M-o

-M)

AU

M (

In R

s. C

ro

re)

Apr-15 Growth in AUM (M-o-M) RHS

AMC

Net Inflow -

Apr'15

Net Inflow -

Mar'15

AUM -

Apr'15

Net Inflow -

Apr'14

Net Inflow -

Mar'14

AUM -

Apr'14

Net Inflow -

CM/LM

Net Inflow -

CM TY/LY

AUM

TY/LY

HDFC Mutual Fund 9,699 -13,496 161,133 15,748 -8,062 125,613 - -38% 28%

ICICI Prudential Mutual Fund 11,435 -10,499 151,417 12,657 -6,180 111,621 - -10% 36%

Reliance Mutual Fund 8,991 -11,398 138,082 10,723 -9,918 105,243 - -16% 31%

Birla Sun Life Mutual Fund 13,107 -8,240 125,050 12,050 -7,037 93,252 - 9% 34%

UTI Mutual Fund 10,396 -15,905 89,405 12,207 -11,126 76,552 - -15% 17%

*CM= Current month, LM = last month, TY = this year, LY = last year

THIS YEAR LAST YEAR GROWTH *

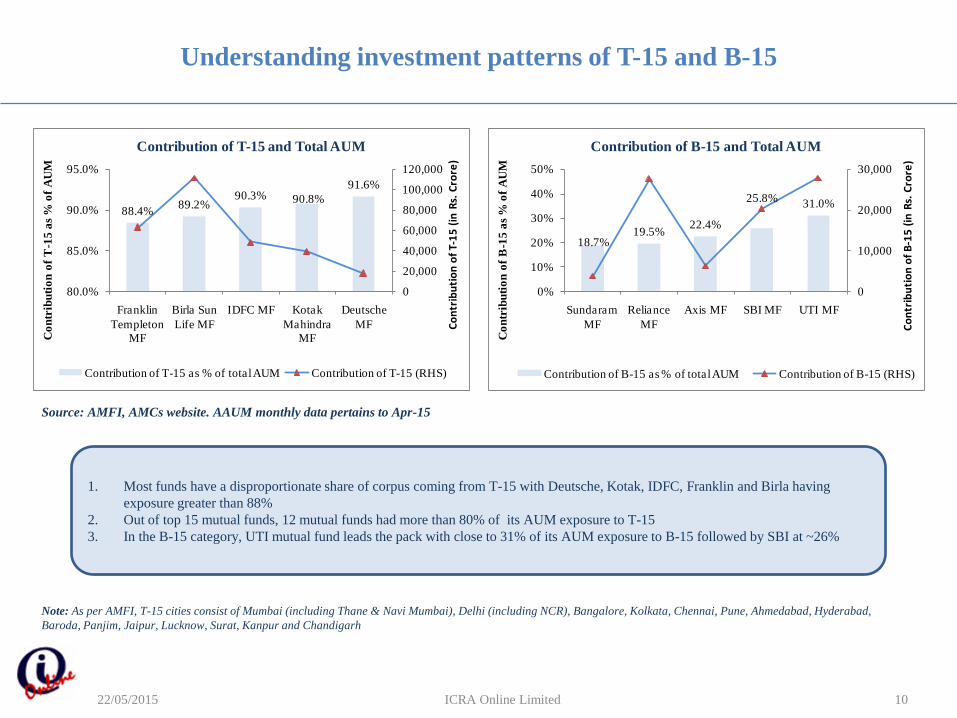

Understanding investment patterns of T-15 and B-15

ICRA Online Limited22/05/2015 10

Source: AMFI, AMCs website. AAUM monthly data pertains to Apr-15

1. Most funds have a disproportionate share of corpus coming from T-15 with Deutsche, Kotak, IDFC, Franklin and Birla having

exposure greater than 88%

2. Out of top 15 mutual funds, 12 mutual funds had more than 80% of its AUM exposure to T-15

3. In the B-15 category, UTI mutual fund leads the pack with close to 31% of its AUM exposure to B-15 followed by SBI at ~26%

Note: As per AMFI, T-15 cities consist of Mumbai (including Thane & Navi Mumbai), Delhi (including NCR), Bangalore, Kolkata, Chennai, Pune, Ahmedabad, Hyderabad,

Baroda, Panjim, Jaipur, Lucknow, Surat, Kanpur and Chandigarh

88.4%89.2%

90.3% 90.8%

91.6%

0

20,000

40,000

60,000

80,000

100,000

120,000

80.0%

85.0%

90.0%

95.0%

Franklin

Templeton

MF

Birla Sun

Life MF

IDFC MF Kotak

Mahindra

MF

Deutsche

MF Co

ntr

ibu

tio

n o

f T-

15

(in

Rs.

Cro

re)

Co

ntr

ibu

tio

n o

f T

-15

as

% o

f A

UM

Contribution of T-15 and Total AUM

Contribution of T-15 as % of total AUM Contribution of T-15 (RHS)

18.7%19.5%

22.4%

25.8%31.0%

0

10,000

20,000

30,000

0%

10%

20%

30%

40%

50%

Sundaram

MF

Reliance

MF

Axis MF SBI MF UTI MF

Co

ntr

ibu

tio

n o

f B

-15

(in

Rs.

Cro

re)

Co

ntr

ibu

tio

n o

f B

-15

as

% o

f A

UM

Contribution of B-15 and Total AUM

Contribution of B-15 as % of total AUM Contribution of B-15 (RHS)

Asset Accumulation Pattern – Top 15

ICRA Online Limited22/05/2015 11

Source: AMFI, AMCs website. AAUM monthly data pertains to Apr-15

0%

20%

40%

60%

80%

100%A

xis

MF

Bir

la S

un

Lif

e M

F

DS

P B

lack

Ro

ck

MF

Fra

nk

lin

Tem

ple

ton

MF

HD

FC

MF

ICIC

I P

rud

en

tia

l MF

IDF

C M

F

Deu

tsch

e M

F

Ko

tak

Ma

hin

dra

MF

L&

T M

F

Relia

nce M

F

SB

I M

F

Su

nd

ara

m M

F

Ta

ta M

F

UT

I M

F

Asset Accumulation Pattern as a % of AUM for Top-15 AMCs

Associate Distributor as % of AUM Non-Associate Distributor as % of AUM Direct Plan as % of AUM

Retail Business Share - Industry Level

ICRA Online Limited22/05/2015 12

Source: AMFI. Category AUM data pertains to Apr-15. Retail is inclusive of HNI

1. Balanced and Equity Categories command the highest retail participation at the industry level, whereas

Liquid/Money Market category is dominated by corporate.

2. Investors in Gilt Fund Category lead the pack in the Direct Channel

2.4%

11.0%

6.0% 5.7%

7.2% 6.9%

0%

2%

4%

6%

8%

10%

12%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Liquid/ Money Market

Gilt FMP Other Debt Schemes

Equity (inc ELSS)

Balanced

AU

M

sha

re (

in %

)

AU

M

sha

re (

in %

)

Retail Participation

Retail AUM share (%) - All channels Retail AUM share (%) - Direct Channel (RHS)

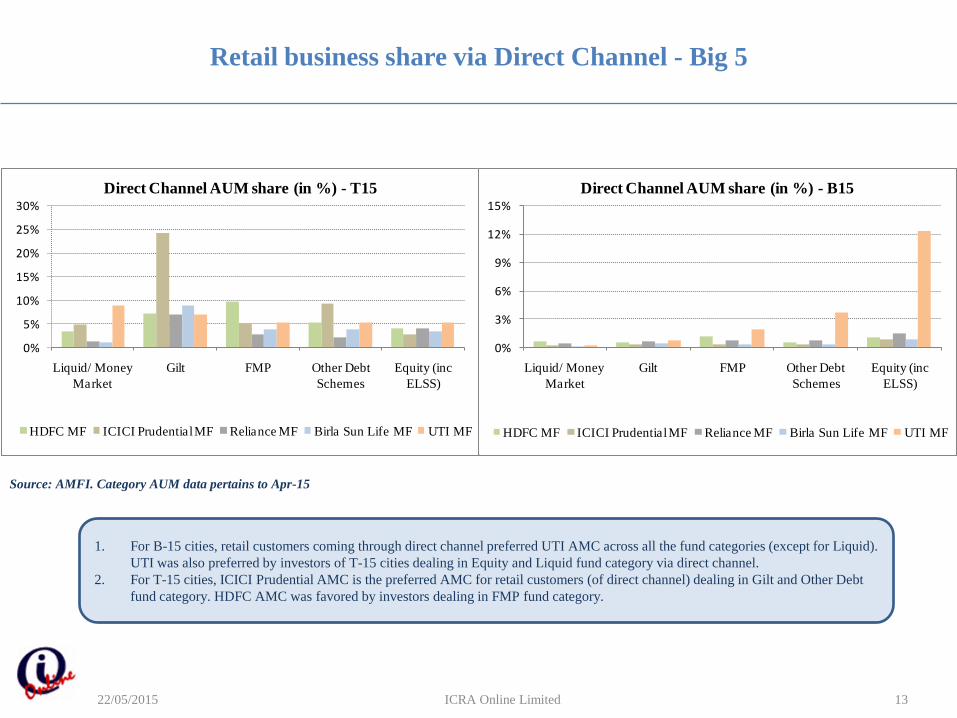

Retail business share via Direct Channel - Big 5

ICRA Online Limited22/05/2015 13

Source: AMFI. Category AUM data pertains to Apr-15

1. For B-15 cities, retail customers coming through direct channel preferred UTI AMC across all the fund categories (except for Liquid).

UTI was also preferred by investors of T-15 cities dealing in Equity and Liquid fund category via direct channel.

2. For T-15 cities, ICICI Prudential AMC is the preferred AMC for retail customers (of direct channel) dealing in Gilt and Other Debt

fund category. HDFC AMC was favored by investors dealing in FMP fund category.

0%

5%

10%

15%

20%

25%

30%

Liquid/ Money

Market

Gilt FMP Other Debt

Schemes

Equity (inc

ELSS)

Direct Channel AUM share (in %) - T15

HDFC MF ICICI Prudential MF Reliance MF Birla Sun Life MF UTI MF

0%

3%

6%

9%

12%

15%

Liquid/ Money

Market

Gilt FMP Other Debt

Schemes

Equity (inc

ELSS)

Direct Channel AUM share (in %) - B15

HDFC MF ICICI Prudential MF Reliance MF Birla Sun Life MF UTI MF

Category Wise Change in Market Share - Big 5

ICRA Online Limited22/05/2015 14

Source: AMFI. Category AUM monthly data pertains to Apr-15

1. Among the top-5 players, ICICI and Birla Sun Life MF registered marginal increase in market share in equities, while in Liquid fund

category, Reliance and Birla Sun Life MF managed to raise their market share by 60.5 and 121 basis points, respectively.

2. Except for ICICI Prudential MF, other 4 AMCs managed to register a marginal rise in their market share in Other Debt fund category.

HDFC

MF

ICICI Pru.

MF

Reliance

MF

Birla Sun

Life MFUTI MF

Liquid -58.65 -93.48 60.52 121.04 -108.32

Equity -25.76 27.49 -4.31 9.72 -7.60

-125

-75

-25

25

75

125

Ch

an

ge i

n B

PS

Market share chg (m-o-m)

HDFC

MF

ICICI

Pru. MF

Reliance

MF

Birla Sun

Life MFUTI MF

FMP 88.38 79.11 62.66 -41.04 48.30

Other Debt 8.14 -5.86 19.94 16.59 1.66

-50

-30

-10

10

30

50

70

90

110

Ch

an

ge i

n B

PS

Market share chg (m-o-m)

Geography wise Analysis

ICRA Online Limited22/05/2015 15

1. Maharashtra alone accounts for more than 42% of the market share

2. Seven states have corpus between Rs 50,000 and Rs 1,10,000 crore

3. The top 15 AMCs hold more than 87% of the market share in Maharashtra with the top 5 alone accounting for over

57% of that

4. The entire distribution is skewed towards one state leaving ample scope for AMCs to increase market share from other

States and Union Territories

5.7%

4.8% 7.1%8.6%

41.9%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0

100,000

200,000

300,000

400,000

500,000

600,000

Gujarat Others Karnataka New Delhi Maharashtra

Shar

e (%

)

AU

M (I

n R

s. c

rore

)

AUM share of top-5 regions

AUM % share (RHS)

Source: AMFI, ICRA Online Research. Data as on Apr-15.

6.2

11.5 11.813.2

14.2

0

2

4

6

8

10

12

14

16

UTI MF Reliance

MF

Birla Sun

Life MF

ICICI

Prudential

MF

HDFC MF

% s

ha

re

% share of top 5 AMCs in Maharashtra

Analytics Group

ICRA Online Limited

Amol Wakekar ([email protected] / 9920665037)

Suman Roy ([email protected] / 9830274008)

ICRA Online Limited22/05/2015 16