housekeeping items - cpa firms | accountant · bkd corporate finance webinar february 19, 2013 tony...

TRANSCRIPT

2/12/2013

1

Merger, Acquisition & Capital Market Strategic OptionsBKD Corporate Finance Webinar

February 19, 2013

Tony GiordanoSenior Vice PresidentBKD Corporate FinanceDenver, CO

Housekeeping Items

• To receive CPEo Participate in entire webinaro Answer all 4 polling questions when they are provided

• Technical Issueso To help prevent technical issues, please close any

unnecessary programs currently running on your computer

o If you experience any technical issues, immediatelycontact L&D (via BKD [email protected])

2

2/12/2013

2

Housekeeping Items

• Other Itemso This presentation will last approximately 50 minutes,

followed by 10 minutes of questions & answerso If your question was not answered, please contact either

today’s presenter (contact information will be provided on the last slide) or our Learning & Development Team at [email protected]

3

Merger, Acquisition & Capital Market Strategic OptionsBKD Corporate Finance Webinar

February 19, 2013

Tony GiordanoSenior Vice PresidentBKD Corporate FinanceDenver, CO

2/12/2013

3

Welcome & Overview

• Privately held companies, by their nature, have less perpetuity than their public counterparts

o Founder/CEO energies & shifts in personal desireso Wealth concentration; desire to diversifyo Competitive landscape & cost of growth

5

Welcome & Overview

• Ultimately, business owner is confronted with many important decisions, including

o How do I monetize value I’ve built in my company for the past 10, 20, 30+ years?

o What is my company worth?o Who are potential buyers (best partner) & what’s

the best way to contact them?o What are my goals from a transaction & my role

post-transaction?o Who will help through this process?

6

2/12/2013

4

Where BKD Can Assist

• Broad spectrum of experienced personnel, helping clients navigate through succession planning & execute transactions

• BKD’s specific transaction specialty groups includeo BKD Corporate Finance, LLC

Leading advisory group in M&A, capital raising & strategic consulting

o BKD’s ESOP Advisory Group Has helped more than 150 companies transition over $2.7B in wealth by selling

100% of their stock to leveraged ESOP

o BKD’s Transaction Services Group Multidisciplinary buy-side & sell-side diligence services & operational consulting

o BKD Wealth Advisors, LLC Wealth management services; $2B in assets under management

o BKD, LLP National CPA & advisory firm

7

BKD Corporate Finance, LLC

• Leading M&A advisory group assisting with sales & divestures, acquisitions, capital-raising transactions & strategic options consulting

• Have closed more than $4 billion in transactions

• Typical deal values—$5 - $250(+) million range

• Industry expertise covering manufacturing & distribution, business services, health care, energy, financial services, technology, etc

• Member of FINRA & SIPC8

2/12/2013

5

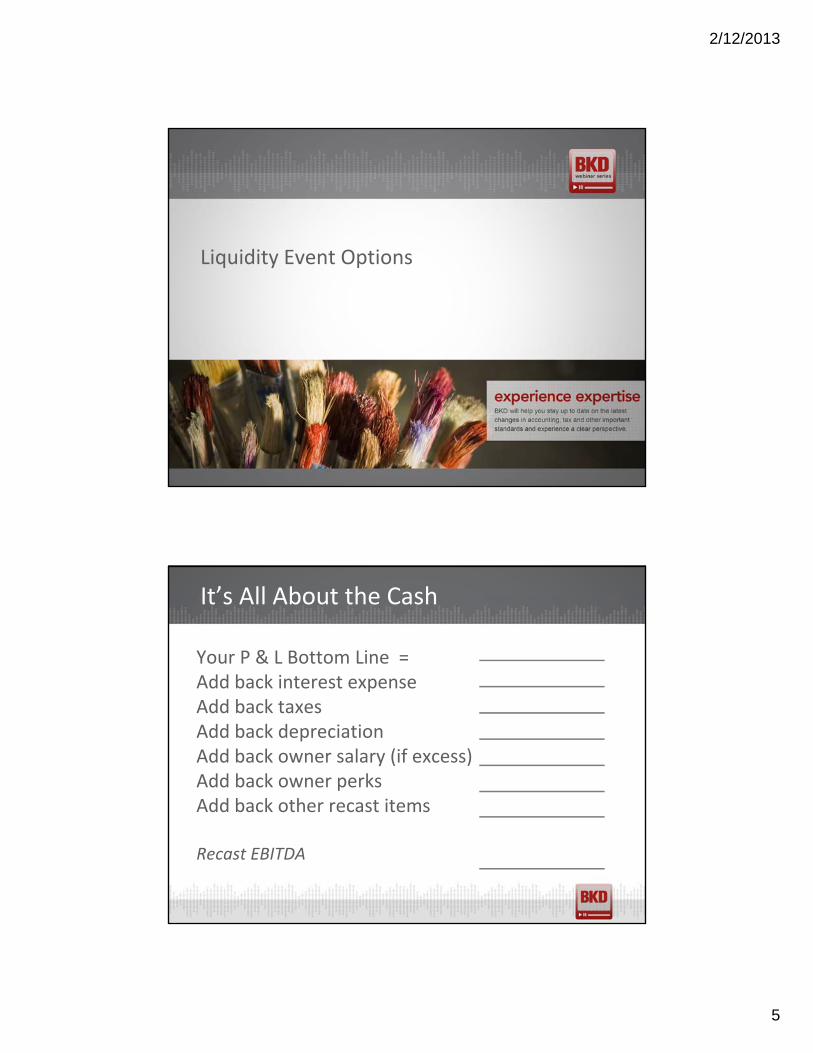

Liquidity Event Options

It’s All About the Cash

Your P & L Bottom Line =Add back interest expense Add back taxes Add back depreciation Add back owner salary (if excess) Add back owner perks Add back other recast items

Recast EBITDA

2/12/2013

6

Liquidity Event Options

• Sale of 100% (or less) to strategic buyer• Sale of 100% (or less) to financial buyer (Private

Equity & Family Office)o Majority recap o Minority recap

• Leveraged recap• Sale to management team (MBO)• ESOPs

11

Strategic Buyers

• Operating companies that provide comparable products & services

o Often competitors, suppliers or customers

• Could also be unrelated to target or its industryo Companies looking to diversify revenue streamso Companies seeking to build upon their business

model &/or competencies to enhance earnings or reduce risks

12

2/12/2013

7

Strategic Buyers

• Buyer motivations are multifaceted & varied, includingo Strategic positioningo Market share; new channelso New products & processeso New customers or deeper penetrationso Technologieso Scale; synergies; earnings enhancementso Management skills; corporate know-howo Diversificationo Accelerated growth; seeking higher margins & earnings

13

Strategic Buyers

• Primary advantages o Potentially, deep universe of buyerso Perspectives of risks & returns among candidate buyers

can vary significantlyo Long-term investment horizonso Often lower return hurdles(typically meaning higher

valuations)o May be motivated to grow in industry with average or

below-average prospectso Often, can bring deeper management talento Typically, cash/stock buyers with lower transitional

demands14

2/12/2013

8

Strategic Buyers

• Issueso Confidentialityo Tire kickers; data seekerso Protecting sensitive performance data, IP, know-howo Industry knowledge—double-edge swordo Consolidation more prevalento What is current management’s role going forward?o Is there a good culture fit?o Potential loss of jobs

15

Financial Buyers/Private Equity/Family Office

• Firms with capital & resources that look to buy companies & utilize value-creation strategies

• Financial buyers can vary significantlyo Traditional buyout fundso Firms with “buy & hold” strategieso Firms with existing holdingso Generalists vs. industry-specific fundso Firms with CEO partnerso Special situation funds

16

2/12/2013

9

• Hold periods often relatively short (generally, three to seven years, although there are many buy & hold firms)

• Family office (typically longer holding period than traditional private equity fund)

• Leverage is often deployed to enhance returns

• Financial buyers usually become strategic buyers as they execute their growth strategies (add on acquisition vs. platform acquisition)

• PEGs have closed roughly 10%-20% of middle market deals in past 10 years

17

Financial Buyers/Private Equity/Family Office

• In general, PEGs have been successful investors in middle market

o Disciplined buyers (pay for quality; shy from average)o Deploy resources to assist growth

• This success has led to expanding universe of PEGs & large pool of capital to deploy

• Current overhang is roughly $348 billion

18

Financial Buyers/Private Equity/Family Office

2/12/2013

10

Financial Buyers

• Primary advantageso Large universe of efficient buyerso Hot deals can garner aggressive biddingo Equity stakes for incumbent management;

noteworthy wealth creationo Solid capital resourceso Pay for excellenceo Very focused growth agendaso Need management teams & infrastructure

19

Financial Buyers

• Issueso More need to sell industry attributes; due diligence

scrutinyo Use of leverageo Aggressive growth & earnings enhancements is hard

worko Must have capable management teamo Center of influence?o Possibility of near-term & medium-term sale

20

2/12/2013

11

Recapitalizations

• Portion of equity is purchased & selling shareholder(s) often retain meaningful stake & continue to operate company

• Popular for owners who desire to diversify their personal wealth, yet remain active in growing business & recognizing future wealth

21

Majority Recap

• Selling majority stake ‒ Advantages o Provide liquidity to ownership o Retain minority equity position that could potentially

double or triple in value in five to 10 yearso New investors provide capital/resources & will work with

management to formulate growth plan & assist in execution

o Key management remains with company (two- to three-year transition period) with board representation

o If platform transaction, company typically continues to operate independently

22

2/12/2013

12

Majority Recap

• Issueso New investor now controls companyo New investor will most likely leverage balance sheet

(but operating risk now lies with new investor)o Could experience major restructuring if acquired by

portfolio company

23

Minority Recap

• Sell minority equity stakeo Advantages Ownership retains control New investor can provide resources (financial & operating)

o Issues Will most likely see lower enterprise valuation due to

minority investment Operate with some leverage Investor will have some minority protections (first right of

refusal, preemptive rights, anti-dilution provisions, redemption rights, board representation, etc.)

24

2/12/2013

13

Leverage Recap

• Leverage recap (leverage company & pay dividend/buy out shareholders)

o Advantages Do not give up any equity (potentially minority stake – 25%) Allows for liquidity event to owners without a sale

o Issues Have to service debt prior to distributions Financial covenants can impact operating flexibility Company more susceptible to macro events—industry or macro

economic events Risk of bankruptcy

25

MBOs

• Owners often recognize team’s leadership contributed greatly to his or her wealth creation

• High-performing teams in solid companies can execute rewarding deals

• Personal capital investments do not need to be large, but they do need to be meaningful

• Capital resources (Sr. & Jr. debt & private equity) to facilitate deals for solid, well-managed companies

• Main element in MBO is control & continuity of management & business operations

o Equity rewards can be far more rewarding if team controls deal & pursues capital partners in competitive process

26

2/12/2013

14

MBOs

• Advantages o Reward most meaningful long-term contributorso Operating team remains in control of processo Company maintains culture & community presenceo Due diligence issues are rare, as are purchase price

modificationso Can retain small equity stake in Newcoo Balance sheet integrity can be maintained

27

MBOs

• Issueso Lack of strategic valueo Requires capable team with demonstrated resultso Team needs to have clear vision & articulate a

compelling plano Operate with some leverage

28

2/12/2013

15

ESOPs

• Advantageso Retain control & continue to run company (regardless of

level of ESOP ownership)o Favorable tax treatment

Reduce or even eliminate corporate income tax Company repays acquisition debt with pre-tax dollars Interest & principal on acquisition debt is tax deductible

o Preserve culture, jobs & communityo Provide stockholder liquidity (over time) tax efficientlyo Reward key management & long-term employeeso Uniquely position company for growth via acquisitions

29

ESOPs

• Issueso Sell company at fair market value; could potentially

“leave money on the table”o Stockholder liquidity may be realized over time, not

immediate

30

2/12/2013

16

Liquidity Events Conclusions

• Often once-in-a-lifetime decision• Issues are complex & impact many who have contributed to

success of enterprise• Emotional aspects are real• Getting it right is perfect stepping stone to next chapter of

life• There are no go-to plans or established formulas/rules

o Assessing client’s situation, objectives, dynamics of company & its industry are critical steps

o Approach should be tailored to client’s desires

31

Strategic Options Consulting

• Assist clients with understanding liquidity options available to them based on their goals & unique characteristics of company or industry

• Determine valuation range for their company & potential interest level from buyer/investor/lenders

• Prepare after-tax proceeds analysis & tax strategies for various options

• Identify value drivers of the company that could be leveraged in negotiations with buyer/investor/lenders

• Identify potential red flags that might have an impact on success of a transaction or impact valuation

• Discuss liquidity event process, timing & probability of a successful transaction

32

2/12/2013

17

Current Market Conditions

Current Market Conditions

• Challenges of last recession have caused many to take very strategic look at their industry

o What are growth prospects of industry?o What will it take to become or remain competitive in

industry?o How will profits be affected by changing landscape?

• Many are making decision of whether they should be, or could be, a consolidator

• Others are assessing strategic alternatives

34

2/12/2013

18

General M&A Trends

• Deal activity will continue to be fueled byo Ongoing access to capital & financing

o Strengthened balance sheets of strategic buyers

o Increasing private equity activity

• S&P 500 companies have $2 trillion in cash on balance sheets & are increasing acquisition activity

• Private equity firms have $348 billion in capital to invest

• Relatively healthy debt markets with lenders active & competitive in M&A lending

35

General M&A Trends

• Current M&A market presents both opportunities & challenges o Companies that maintained or improved earnings over last 24 to 36

months can be highly valued in today’s M&A environment

o Strong competition for quality assets as both corporates & private equity continue to seek deals to fuel growth & deploy capital

o General worldwide macro events & general trends in U.S. economy, reflected in volatility of U.S. debt & equity markets, have a direct impact on M&A market activity

o Assuming a relatively stable economy, we anticipate 2013 & 2014 to be an active M&A market with attractive valuation multiples

36

2/12/2013

19

U.S. M&A Activity

Source: Dealogic and William Blair & Company, L.L.C. Mergers and Acquisitions market analysis

37

$348B of Private Equity Cash to Invest

Source: Pitchbook

38

2/12/2013

20

Private Equity EBITDA Multiples

Source: GF Data ResourcesIndustries covered by this graph include Manufacturing, Business Services, Healthcare Services, Retail, Distribution, Publishing/Media, Technology and Other

39

Private Equity EBITDA Multiple by Industry

40

INDUSTRY 2003-07 2008 2009 2010 2011 2012 YTD Total N =

Manufacturing 5.9 5.8 5.7 5.9 5.9 5.9 5.9 651Business Services 6.1 6.1 5.9 5.9 6.7 6.2 6.1 261Health Care Services 6.7 6.6 6.3 6.6 7.3 7.7 6.8 140Retail 6.5 6.4 5.2 6.1 6.1 6.8 6.5 48Distribution 5.9 6.3 5.5 5.3 6.0 6.3 5.9 153Publishing / Media 7.5 6.1 7.4 4.2 6.1 NA 7.3 32Technology 5.5 6.5 6.6 5.7 4.6 8.1 6.2 29Other 5.8 5.4 6.4 5.6 5.0 6.2 5.7 181

N = 792 167 90 171 163 112 1,495

Source: GF Data, 3Q 2012

2/12/2013

21

Credit Markets

Source: Dealogic and William Blair & Company, L.L.C. Mergers and Acquisitions market analysis

41

Credit Markets

Source: GF Data Resources, November 2012

42

2/12/2013

22

Conclusion

• We understand o Privately held businesses & different succession

alternatives availableo Importance of tailoring succession solution that fits

client’s unique goals & objectiveso Importance of coordinating with estate, tax & overall

wealth planning• BKD strives to provide seamless approach to solving our

clients’ succession needs• We see an active M&A market for the next couple of years

43

Questions?

2/12/2013

23

About BKD Corporate Finance, LLC

• Subsidiary of BKD, LLP• 18-year history

• Member of FINRA & SIPC

• Professional team includeso Investment bankers

o Financial analysts

o Market analysts

BKD Corporate Finance Profile

46

2/12/2013

24

Breadth & Depth of Resources

• 30 offices in 12 states

• Approximately 250 partners

• More than 2,000 employees

• Six industry niche groupso Manufacturing & Distribution, Construction & Real Estate,

Energy, Financial Services, Health Care & Not-for-Profit

• Clients in all 50 states & internationally

• End-to-end client service proposition47

Our Services

48

2/12/2013

25

• Client revenue range—$5 million to $2 billion• National & international buyers• Praxity Alliance

o Global alliance of more than 100 independent firms in 72 countries

o Allows BKDCF & its clients direct access to foreign markets & potential counter parties

• More than $4 billion in transaction value• Completed hundreds of engagements• Many transactions significantly exceeded client

value expectations

Experience

49

Experience

o Manufacturingo Business Services/Consultingo Wholesale Distributiono Oil & Gaso Health Careo Food Processing &

Distributiono Auto Parts Distributiono Flexible Packagingo Telecom & Technologyo Transportation

o Constructiono Building Materialso Printingo Financial Institutionso Scrap Processingo Chemical o Grocery & Convenience

Storeso Restauranto Retailo Advertising

50

2/12/2013

26

Experience – Recent Transactions

51

Performance & Reliability

“McKesson is paying a substantial premium for the McQueary’s business. The purchase price of the deal was $190 million, implying a price/revenue ratio of 0.27x. This ratio is more than twice the comparable figures of other recent acquisitions, such as D&K by McKesson or Bellco by AmerisourceBergen. I presume an EBITDA (earnings before interest, tax, depreciation and amortization) multiple would reflect a similar 2x+ premium.”

— Adam J. Fein, Ph.D., Founder & PresidentPembroke Consulting, Inc.

Has been acquired by

The undersigned acted as financial advisor to McQueary Bros. in this

transaction

52

2/12/2013

27

“BKD Corporate Finance did an outstanding job helping us restructure our existing debt and secure new growth capital. Because of our rapid expansion, we were beginning to outgrow our current lenders. We needed a new lender that could refinance our existing debt and support our aggressive business plan. The BKDCF team was instrumental in this process and we couldn’t be happier about the way things have played out. BKDCF was able to create a competitive process that provided us with multiple options to consider with competitive terms. We would certainly recommend BKDCF for any business owner or management team needing help refinancing or seeking growth capital for their business.”

— Clint Lopez, CFO, ABox4U, LLC

Performance & Reliability

53

BKD Corporate Financebkdcorporatefinance.com

Thank You

2/12/2013

28

55

Continuing Professional Education (CPE) Credits

BKD, LLP is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: www.learningmarket.org.

The information in BKD webinars is presented by BKD professionals, but applying specific information to your

situation requires careful consideration of facts & circumstances. Consult your BKD advisor before acting

on any matters covered in these webinars.

55

56

CPE Credit

• This presentation may be eligible for CPE credit upon verification of participant attendance; however, credits may vary depending on state guidelines

• For questions or comments regarding CPE credit, please email BKD Learning & Development Department at [email protected]

56