hih case study on conglomerates: letters of credit · hih case study on conglomerates: letters of...

TRANSCRIPT

�

HIH Case Studyon Conglomerates:Letters of Credit

Round 3

A Core Curriculum for Insurance Supervisors

Copyright © 2006 International Association of Insurance Supervisors (IAIS).All rights reserved.

The material in this module is copyrighted. It may be used for training by competent organi-zations with permission. Please contact the IAIS to seek permission.

�

HIH Case Study on Conglomerates: Letters of Credit (Round 3)

Attached is a new briefing note prepared by the senior manager of your branch respon-sible for HIH. Your tasks for this third round are to:

• Identify the issues that need to be considered in the treatment of financial in-struments such as Letters of Credit (LOCs), for the purposes of solvency

• Identify the additional regulatory issues that may arise uniquely as a result of the provision of LOCs in support of foreign operations of a local parent company

• Draft a response to KPMG (bullet points identifying the issues and what will be covered in the letter are sufficient) on whether or not you agree with the sug-gested treatment for solvency purposes of LOCs and why

• Assess the implications of the information provided in this exercise and make recommendations for an action plan.

Note that information from round 2 may be useful in carrying out the tasks of this round.

Insurance Superv�s�on Core Curr�culum

�

MEMORANDUM FOR GENERAL MANAGERBRIEFING NOTE ON REQUEST FOR RULING ON THE SOLVENCY TREATMENT OF LETTERS OF CREDIT

1 July 2000

APRA has received an email from a partner at KPMG requesting a meeting to discuss the regulatory treatment of Letters of Credit (LOC). At this stage, APRA has not issued a Prudential Standard on the treatment of LOCs, given that it has no formal standard making powers under the Insurance Act (1973).

The attached e-mail follows a conversation that the Executive general manager (EGM) of DID had with a partner from KPMG. The e-mail requests a meeting to dis-cuss the regulatory treatment of LOCs. While the contact was on a “no names” basis, it is fairly clear from the context that the client is HIH. I suspect the approach is with respect to LOCs issued to support HIH’s UK subsidiaries.

I have attached the following for your information:

• Attachment 1 - The email from a partner a KPMG seeking a meeting to discuss APRA’s position on the treatment of Letters of Credit for the purposes of sol-vency.

• Attachment 2 - Relevant sections from the Insurance Act (1973).• Attachment 3 - A briefing note on LOCs.• Attachment 4 - An extract of the required treatment by banks of similar instru-

ments for capital purposes (to provide some guidance).• Attachment 5 - A briefing Note on HIH and it use of Letters of Credit.

Senior Analyst

HIH Case Study on Conglomerates (Round 3)

3

Attachment 1

E-mail from KPMG

To: [email protected]: Treatment of Letters of Credit for Solvency Purposes

As discussed by phone, I have been approached by a major general insurer seeking clarification from APRA of its interpretation and views as to how letters of credit should be treated for Insurance Act solvency purposes under both the current regulations and those presently under consideration.

Initially, I have been asked to approach APRA on an in principle “no names” basis but with a view to the insurer subsequently meeting with APRA to work through the current and proposed requirements.

BackgroundFor general insurers underwriting business in the United States and also with the

Lloyd’s Syndicates in the UK, it is often a regulatory requirement and/or accepted prac-tice that the underwriter issue a letter of credit, generally supported by a bank and/or term deposit, which provides the insured with additional comfort as to the insurer’s ability to meet claims arising under the applicable insurance contracts.

On a going concern basis where insurers are settling their liabilities in the normal course of business the circumstances under which a letter of credit would be called is remote and the letters of credit are typically only callable in the event of failure by the insurer to meet a valid demand for payment and where a call has been made but not satisfied by the insurer.

We also note that claims liabilities in respect of business supported by letters of credit are met out of normal cash flow and not by cashing in the assets supported by the letters of credit.

On the normal ongoing basis, which is a fundamental principle on which financial statements are prepared, an insurer brings to account claims liabilities in respect of all policies of insurance for events occurring to balance date including business where let-ters of credit may be involved.

Current Regulatory and Disclosure RequirementsAs the actual claims liabilities in respect of business supported by letters of credit

are, or should be, reflected on the balance sheet of the insurer, current market practice is that letters of credit are not considered to be contingent liabilities either by their nature or by the fact that the actual liabilities are provided for.

Accordingly, current market practice supported by our client and KPMG’s inter-pretation is that the current solvency requirements of the Insurance Act 1973 do not require any specific allowance for letters of credit on issue in determining compliance with the minimal solvency requirements of the Act.

We would appreciate your comments and confirmation on this point.

Insurance Superv�s�on Core Curr�culum

�

Going forward, our client is aware that other financial institutions and in particular banks that also use letters of credit as a financing arrangements do set aside an amount of capital to support their letters of credit on issue.

Because of the increasingly significant nature of our clients foreign operations and the likelihood that usage of letters of credit will continue to grow in importance, they wish to bring certainty to their capital/solvency position and to determine from a philo-sophical point of view the level of capital, if any, that APRA considers under the pro-posed regulatory changes should be set aside.

I would very much appreciate your prompt consideration of this matter and con-firm that my client is available to meet with you at short notice once you have had an opportunity to consider your initial views.

Thank you for your agreement to consider this matter and in the meantime if you require any further information or explanation please contact me by email or on 9335 xxxx.

RegardsKPMG Partner

HIH Case Study on Conglomerates (Round 3)

�

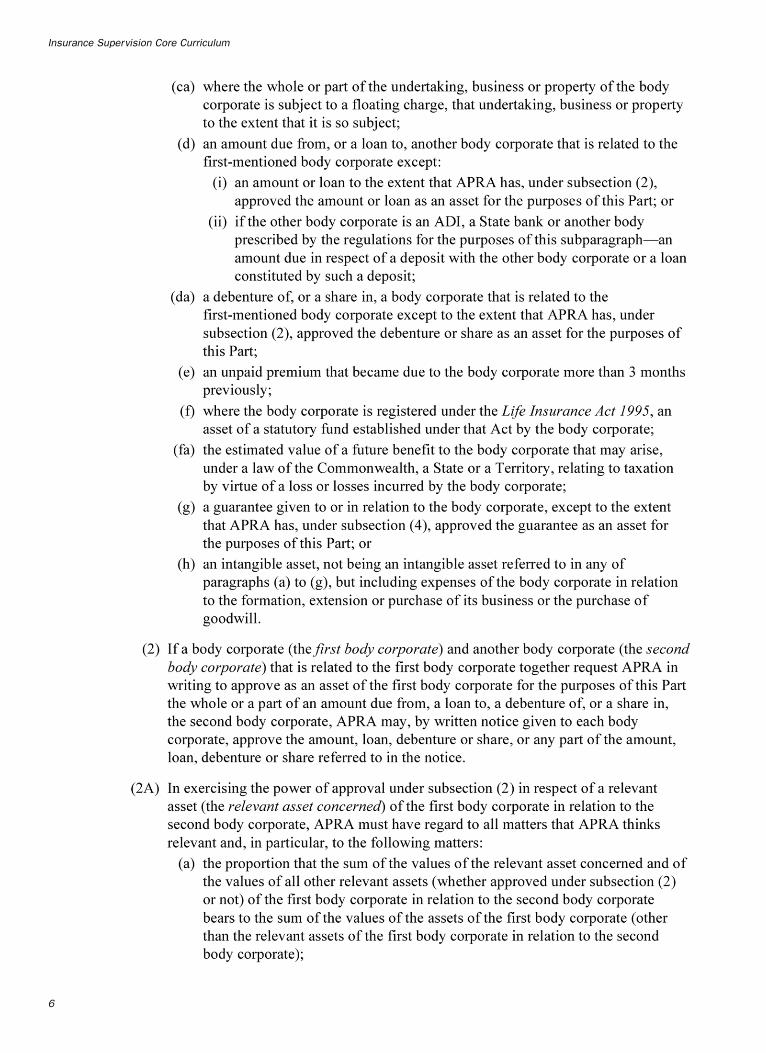

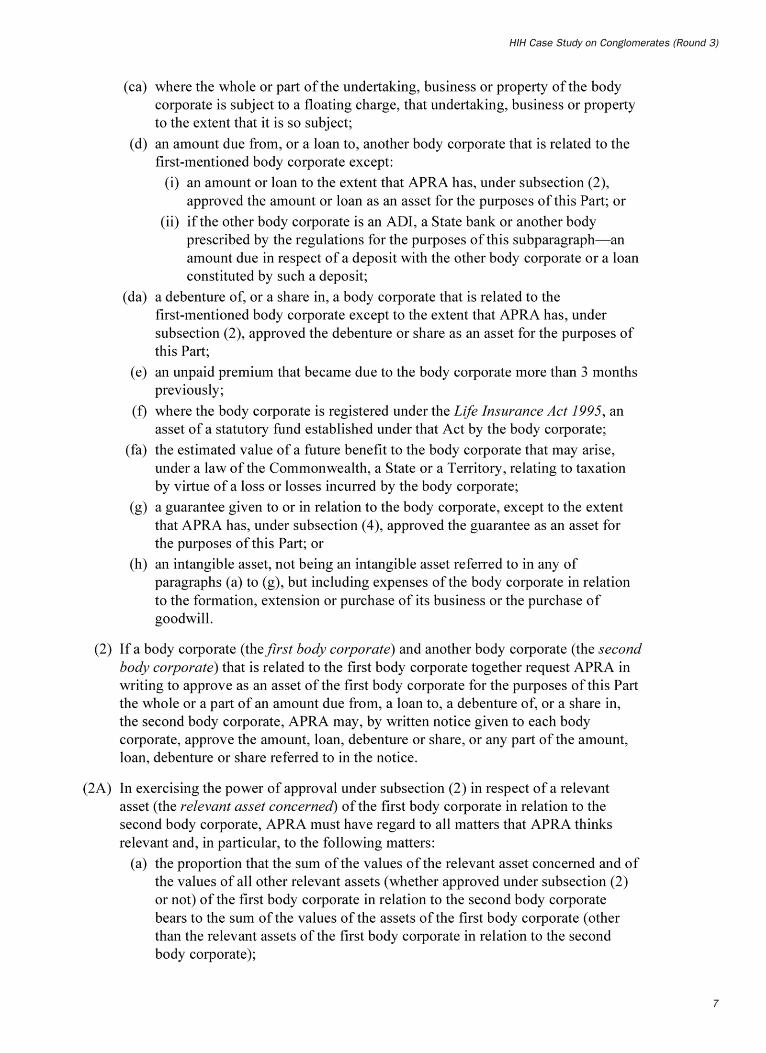

Attachment 2

Insurance Superv�s�on Core Curr�culum

�

HIH Case Study on Conglomerates (Round 3)

�

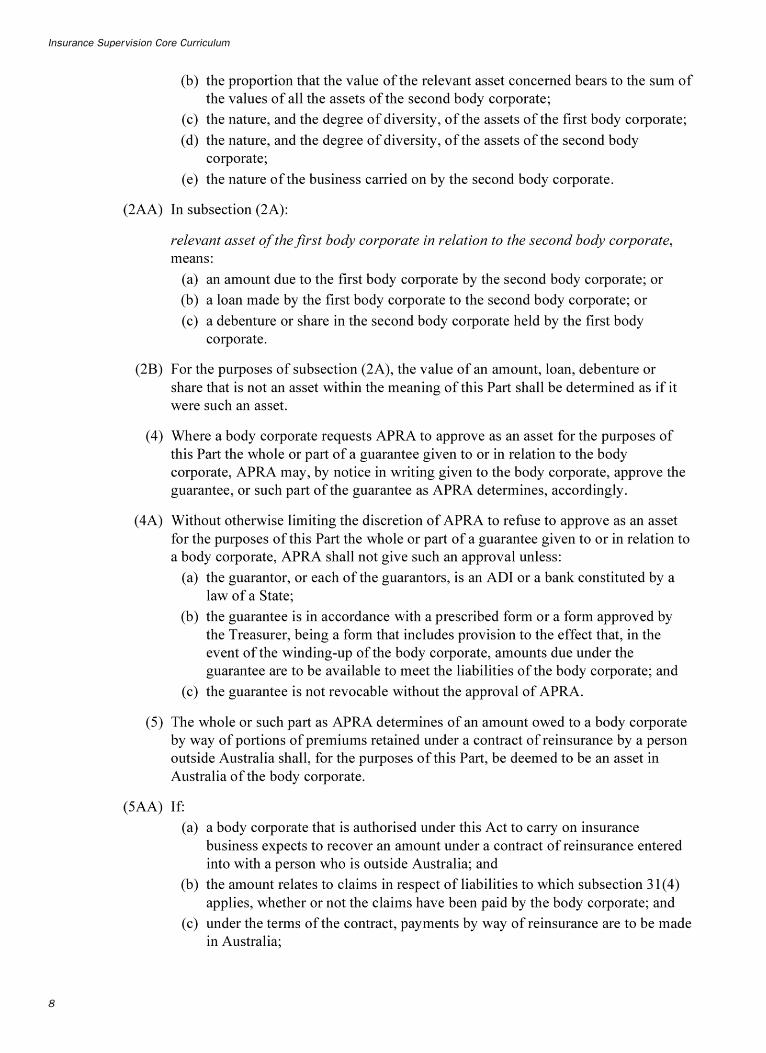

Insurance Superv�s�on Core Curr�culum

�

HIH Case Study on Conglomerates (Round 3)

�

Insurance Superv�s�on Core Curr�culum

�0

HIH Case Study on Conglomerates (Round 3)

��

Insurance Superv�s�on Core Curr�culum

��

Attachment 3

Briefing Note — Letters of Credit

In international finance, the purpose of either a commercial or standby letter of credit is to facilitate trade by substituting the credit of a bank for that of the customer.

Commercial Letters of Credit

A commercial letter of credit is a contractual agreement between a bank, known as the issuing bank, on behalf of one of its customers, authorizing another bank, known as the confirming bank, to make payment to the beneficiary. The issuing bank, on the request of its customer, opens the letter of credit. The issuing bank makes a commitment to honour drawings made under the credit. The beneficiary is normally the provider of goods and/or services. Essentially, the issuing bank replaces the bank’s customer as the payee. The issuing bank will charge the customer a fee for any undrawn line and takes security in accordance with its usual arrangements with that customer.

Letters of credit used in international transactions are governed by the Interna-tional Chamber of Commerce Uniform Customs and Practice for Documentary Credits. The general provisions and definitions of the International Chamber of Commerce are binding on all parties.

Main ElEMEnts of a lEttEr of CrEdit

• A payment undertaking given by a bank (issuing bank)• On behalf of a buyer (applicant)• To pay a seller (beneficiary) for a given amount of money• On presentation of specified documents • Within specified time limits• Documents must conform to terms and conditions set out in the letter of

credit• Documents to be presented at a specified place

Characteristics of Letters of Credit

nEgotiability

Letters of credit are usually negotiable. The issuing bank is obligated to pay not only the beneficiary, but also any bank nominated by the beneficiary. Negotiable instruments are passed freely from one party to another almost in the same way as money. To be nego-

HIH Case Study on Conglomerates (Round 3)

�3

tiable, the letter of credit must include an unconditional promise to pay, on demand or at a specified time. The nominated bank becomes a holder in due course. As a holder in due course, the holder takes the letter of credit for value, in good faith, without notice of any claims against it.

rEvoCability

Letters of credit may be either revocable or irrevocable. A revocable letter of credit may be revoked or modified for any reason, at any time by the issuing bank without notifica-tion.

The irrevocable letter of credit may not be revoked or amended without the agree-ment of the issuing bank, the confirming bank, and the beneficiary. An irrevocable letter of credit from the issuing bank insures the beneficiary that if the required docu-ments are presented and the terms and conditions are complied with, payment will be made.

transfEr and assignMEnt

The beneficiary has the right to transfer or assign the right to draw under a letter of credit only when the letter of credit states that it is transferable or assignable.

sight and tiME drafts

All letters of credit require the beneficiary to present a draft and specified documents in order to receive payment. A draft is a written order by which the party creating it, orders another party to pay money to a third party.

Standby Letters of Credit

A standby letter of credit serves a different function to that of a commercial letter of credit. Whereas a commercial letter of credit is the primary payment mechanism for a transaction, a standby letter of credit serves as a secondary payment mechanism. A bank will issue a standby letter of credit on behalf of a customer to provide assurances of his ability to perform under the terms of a contract between the customer and a ben-eficiary. The parties involved in the transaction do not normally expect that the letter of credit will ever be drawn upon.

A standby letter of credit assures the beneficiary of the performance of the custom-er’s obligation. The beneficiary is able to draw under the credit by presenting a draft,

Insurance Superv�s�on Core Curr�culum

��

copies of invoices, with evidence that the customer has not performed its obligation. The bank is obligated to make payment if the documents presented comply with the terms of the letter of credit.

Standby letters of credit are issued by banks to stand behind monetary obligations, to ensure the refund of advance payments, to support performance and bid obligations, and to ensure the completion of a sales contract. A standby letter of credit always has an expiration date.

Standby letters of credit are often used to guarantee performance or to strengthen the creditworthiness of a customer. For example, a customer may be provided open account terms subject to a standby letter of credit. If payments are made in accordance with the supply contract or policy, the letter of credit cannot not be drawn against. Under a standby letter of credit the seller pursues the customer for payment directly; only in the event that the customer is unable to pay does the seller presents the draft and copies of invoices to the bank for payment.

Standby Letters of Credit in the Insurance Industry

We are not aware of standby letters of credit being used extensively in the insurance industry within Australia. However, we are aware that several companies, most notably HIH, have used these to support the claims paying ability of their foreign owned sub-sidiary insurance companies. We are not aware whether these have been at the request of the market or the foreign regulators.

Senior Analyst

HIH Case Study on Conglomerates (Round 3)

��

Attachment 4

Extract from APRA’s Prudential Standards for Authorized Deposit-taking Institutions (ADIs) (includes Banks)

Regulating the Treatment of Off Balance Sheet Items for the Purposes of Capital Adequacy

AGN 112.2 - Risk-Weighted Off-Balance Sheet Credit Exposures

CrEdit ConvErsion faCtors for non-MarkEt-rElatEd off-balanCE shEEt transaCtions

Nature of Transact�on: D�rect Cred�t Subst�tutes Cred�t Convers�on Factor

Any irrevocable off-balance sheet obligations which carry the same credit risk as a direct extension of credit, such as an undertaking to make a payment to a third party in the event that a counterparty fails to meet a financial obligation, or an undertaking to a counterparty to acquire a potential claim on another party in the event of default by that party, constitutes a direct credit substitute (i.e. the risk of loss depends on the creditworthiness of the counterparty or the party on which a potential claim is acquired).

This includes potential credit exposures arising from the issue of guarantees and credit derivatives (selling credit protection), confirmation of letters of credit, issue of standby letters of credit serving as financial guarantees for loans, securities and any other financial liabilities, and bills endorsed under bill endorsement lines (but which are not accepted by, or have the prior endorsement of, another ADI).

100%

Insurance Superv�s�on Core Curr�culum

��

Attachment 5

Briefing Note

HIH’s Use of Letters of Credit

In the reasonable knowledge that the “client” of KPMG is HIH we have done some re-search into their possible uses of Letters of Credit (LOCs). We have spoken with their bankers and with their auditors and have pieced together the following as best we could at short notice.

Use of LOCs to Secure their own Commitments

HIH Casualty and General has, for some time, used LOCs to secure some of their com-mitments to third parties. We were not able to ascertain who those third parties might be but it appears that the total of commitments secured by LOCs as at June 1999 was in the order of $80 million.

Use of LOCs to Secure Commitments of Subsidiaries

After HIH acquired the Cotesworth group in 1998, arrangements were made for LOCs to be issued to support the obligations of the Cotesworth syndicates. The LOCs were se-cured by indemnities from companies within the HIH group, including the authorized insurers, supported to an extent by cash deposits or securities owned by the authorized insurers which were lodged with Austraclear Limited or with the Reserve Bank Infor-mation and Transfer System. Similar arrangements had been used previously by FAI to support its overseas operations.

The companies within the group and approximate commitments in mid 1998 (and largely still in place) are, as best we can tell:

• HIH C&G $91m• CIC $154m• FAI General $53m

These figures are at face values and may vary a little (though probably not signifi-cantly) from market values.

HIH Case Study on Conglomerates (Round 3)

��

HIH Prudential Returns

We have checked back through the quarterly and annual returns from HIH and there has been no adjustments made to solvency for LOCs or any requests for exemption under s30 of the Act.

Junior Analyst