hih case study on corporate governance

TRANSCRIPT

�

HIH Case Studyon Corporate Governance

Teach�ng Note

A Core Curriculum for Insurance Supervisors

Copyright © 2006 International Association of Insurance Supervisors (IAIS).All rights reserved.

The material in this module is copyrighted. It may be used for training by competent organiza-tions with permission. Please contact the IAIS to seek permission.

Author Jeffrey Carmichael is chief executive officer of Promontory Australasia. Until recently a full-time consultant, he was previously chairman of the Australian Prudential Regulation Au-thority. His career also includes senior positions with the Reserve Bank of Australia, seven years as professor of finance at Bond University, and appointment to a number of government and private sector boards and inquiries, including the Wallis Inquiry into the Australian financial system. He has published in a number of the world’s top economics and finance journals, in-cluding the American Economic Review and Journal of Finance.

���

Contents

Round One . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Round Two . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Round 2 Assessment and Strategy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Round Three . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Round 3 Assessment and Strategy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Summary of Lessons from the Case . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Comments from the Royal Commission . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

APRA’s New Prudential Standards on Governance . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

A Final Note . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

�

HIH Case Study on CorporateGovernance (Teaching Note)1

TEACHING NOTE1

After the completion of each round, the instructor should bring the groups together to compare their action plans and proposed strategies and to discuss the major issues en-countered. Participants should be encouraged to debate vigorously their interpretations of the information available at each stage. The instructor should use the following guide to help direct the discussion and to sum up his or her own assessment of the informa-tion and possible courses of action in each round. As much as possible the experience should be one of discovery by participants.

Governance is largely about how a business is run. The more specific definitions of governance refer to resolution of conflicts of interest. According to the Organisation for Economic Co-operation and Development (OECD), corporate governance is “the system by which business corporations are directed and controlled.”2 It involves the “set of relationships between a company’s management, its board, its shareholders and other stakeholders. Corporate governance also provides the structure through which the objectives of the company are set, and the means of attaining those objectives and monitoring performance are determined.”3

Given that the board of an institution delegates much of its decision-making power to management, governance requires effective internal controls to reassure the board that management is executing its delegated powers in a way that is consonant with, rather than in conflict with, the objectives of the board. Similarly, management needs internal controls to ensure that its delegations are exercised as intended. Thus, internal controls typically limit the amount of risk that an institution can take, impose approval processes on significant decisions, and establish policies and procedures for exercising

1. This Teaching Note should be read in conjunction with the General Teaching Note for the set of HIH case studies.2. OECD (2001), p. 1.3. OECD (1999), p. 2.

Insurance Superv�s�on Core Curr�culum

�

delegated authorities. The internal control framework typically required in a financial institution encompasses controls to address these “delegation” conflicts as well as con-trols to ensure that the institution is compliant with external requirements of regula-tors.

That corporate governance is more than just a set of rules and structures was em-phasized by Justice Owen in his report on the failure of HIH, in which he observed:

At its broadest, the governance of corporate entities comprehends the framework of rules, relationships, systems and processes within and by which authority is exercised and controlled in corporations. It includes the practices by which that exercise and con-trol of authority is in fact effected.…The board must also ensure that the corporation has in place the necessary controls over its activities and, of equal importance, ensure that the controls are working.

In short, governance is not just about having systems of accountability and stew-ardship in place, it is about making sure that they are working. In HIH they were not.

While it is possible for a poorly governed financial institution to survive and even prosper, the correlation between poor governance and financial failure is extremely high. Operating a financial institution with inadequate governance and controls is like sailing a boat without any navigating equipment; there is a chance that it will reach port, but the probability is not high.

Poor governance in an insurance company is usually an indicator of other problems (and likewise, other problems are often a sign of governance failure). Thus, a company that is often late with its returns, makes frequent errors in those returns, is unable to respond quickly to supervisory requests, has staff or management with conflicting re-sponsibilities, and so on is highly likely to fail at some point unless these shortcomings are addressed. Where governance failings are accompanied by other signs of financial distress, the probability of failure increases markedly.

Round One

Participants have a wealth of relevant information available to them for the first round. None of the information provided is conclusive, although there are many warning sig-nals and issues to be followed up. The challenge is to prioritize them and to follow up in the more critical areas.

The two primary warning signals are the litany of governance concerns raised by the 15 August memo from the asset risk visit (attachment 4) and the concerns about the accuracy of HIH’s quarterly returns (attachment 5). The other documents also raise many issues related to poor governance and internal controls.

HIH Case Study on Corporate Governance (Teach�ng Note)

�

The Asset Risk Visit (Attachment 4)

The report of the asset risk visit is remarkable for the extensive corporate governance failures that it identifies. While none of the individual items identified is numerically critical, the extent of the governance and risk management failures uncovered demand further investigation. In summary:

• There were significant breaches of HIH’s investment guidelines, arising largely from investments acquired in the FAI acquisition. There was no plan or time-table for bringing these exposures within the limits of the HIH guidelines. In-deed there appeared to be no structure for dealing with breaches of investment limits or for reporting them to internal audit or the board.

• HIH’s internal audit function appeared to have a “bottom line” and operational focus rather than a risk management focus. It was “out of the loop” with respect to investment guideline breaches.

• There were control issues particular to the FAI acquisition, including high levels of FAI staff turnover and a resulting lack of knowledge about certain FAI hold-ings.

• There were general weaknesses in the risk management framework in place at HIH, including a lack of clear responsibility and ownership for ensuring that the framework was effective and up to date.

• There were clear instances where practice deviated from internal guidelines in the approval process for investments.

• There were shortcomings in documented policies, including guidelines on how existing loans were to be monitored and how provisions were to be assessed and authorized.

• A number of other fairly basic weaknesses and gaps in documented policies were listed, including no approved listing of authorized dealing counterparties, lack of detail and benchmarks for externally managed equity portfolios, and confusion over the definition of “property” in the investment guidelines.

In addition to these policy issues, a number of specific problems were identified, despite the high-level focus of the review. Some were identified in a review of a very small sample of loan files which took place in the course of the visit. These include:

• A reference in an internal audit report to incorrect elimination entries in HIH Holdings (US) Inc.

• Information in an internal audit report showing a decline in shareholders’ funds in one of the U.S. subsidiaries of US$60 m and a decline in investments in sub-sidiaries of nearly US$45 m. The asset risk team was unable to obtain further information about these U.S. adjustments, even from the CFO of HIH who par-ticipated in the asset risk visit. A particular concern was whether the U.S. ad-

Insurance Superv�s�on Core Curr�culum

�

justments had been booked in the group financial statements, but no one could answer this question.

• The FAI equity portfolio included a large number of what might be called “dot com” companies whose price volatility was much greater than the various ASX benchmarks used by HIH in its investment guidelines.

• Reference was made to many classification and reporting issues in the APRA quarterly returns, some of which were discussed during the visit. The APRA supervisory team was assured in the March prudential consultation that these problems would cease, but evidently they were continuing.

• From the few investment files that were briefly reviewed, problems were found suggesting consistent overvaluations of assets. In one file involving a property development, the file showed a total exposure to HIH on the development of A$110.4 m, including guarantees of A$47.5 m. However, an internal HIH re-port showed the exposure to be A$82 m on 31 March 2000. The team expressed concern that it did not appear to be HIH’s policy to treat guarantees as a com-mitment or exposure for the calculation of asset risk.

• Three property loan files were reviewed with loans totalling approximately A$7 m. The team noted an absence of legal documentation, an absence of analysis of the debt-servicing capability of the borrower, and a lack of confirmation of the existence and value of any security in support of the debt. There also appeared to be substantial amounts of capitalized interest accrued on these loans. The con-clusion of the team was that the loans were well past due and probably should have been written off.

• There were breaches of the revaluation policy.• The asset risk team also expressed concerns about an inability to obtain trial

balances for certain subsidiaries, investments in which had been approved for section 30 purposes.

The overall impression from the asset review is of a company in which controls are either ignored or nonexistent, in which there is no clear responsibility for gover-nance issues, and in which there is a dangerously low level of understanding among key personnel about the nature of the company’s investments and risks. This impression is even more alarming given that the focus of the visit was on investments, rather than on governance issues per se.

Quarterly Returns (Attachment 5)

This note raises significant concerns. Not only is there solid evidence that HIH has a history of inaccurate returns (for example, the note about the large discrepancies be-tween the quarterly and annual returns) the errors appear to be material in terms of calculating the company’s solvency. Errors include:

HIH Case Study on Corporate Governance (Teach�ng Note)

�

• Unexplained amounts• Netting of intercompany exposures in calculating Section 30 exclusions from

the solvency calculation• The many misclassifications and overvaluations of assets detected by the asset

risk visit.

Without reliable data there is almost no way of verifying the company’s financial position. The comments from Paul Abela at HIH provide little comfort that the com-pany is taking these errors seriously.

HIH Board of Directors (Attachment 1)

While seemingly innocuous, the HIH board listing raises a couple of issues related to independence:

• Two of the five independent directors, including the chairman, and one of the executive directors are ex-partners of Arthur Andersen—the company’s audi-tors;

• Another independent director, Rodney Adler, came onto the board following the takeover of FAI. While there is nothing intrinsically wrong with having a major shareholder on the board, there is disquieting market rumor about his attempting to destabilize the CEO’s position.

While these connections are not ruled out by law, they do not meet with best prac-tice for independence. Independence is not a guarantee of good decision making. At the same time, independence is the best way of ensuring that directors act in the interests of the shareholders that they represent. Where there is a practice of appointing ex-audi-tors to the board, there is at least a suspicion that audit reviews may be less critical than might other wise be the case—under the (possibly incorrect) assumption that a current auditor is less likely to be appointed to the board at a later stage if he or she has created difficulties for the board or the company during his or her tenure as auditor. In view of other concerns there is a case to test these relationships further.

HIH Corporate Structure (Attachment 2)

The most obvious feature of the HIH corporate structure is that it is complex and un-wieldy. Further, in view of the information in the Background Note that the HIH Group included more than 200 companies, it should be clear that there are many other, nonin-surance companies within the group.

Insurance Superv�s�on Core Curr�culum

�

The 7 March 2000 Briefing Note (Attachment 3)

The Briefing Note makes it is clear that HIH has grown very rapidly from a small under-writer to the second largest general insurance group in the local market. It is important to note that this growth came about as a result of a policy of aggressive acquisition of other insurers. In a single 12-month period HIH appears to have made no fewer than six acquisitions. Given the problems usually faced in absorbing other companies and cultures and the massive task of integrating systems across such companies, HIH ap-pears to be a prime target for a potential breakdown in governance.

Another point worthy of note in the Background Note is the departure of Winter-thur as the major shareholder in June 1999. While the move to a more diverse share-holder base through the stock market is not necessarily a sign of weakness, it does remove a potentially deep parental pocket to draw on in the event that HIH encounters financial difficulties. More generally, it would be useful to know more about the reason for Winterthur’s departure.

Media and Market Assessments (Attachment 7)

This information contains some worrying signals. There is a consistent theme of market concerns about poor management. The focus on Adler and his alleged attempts to de-stabilize Williams is also a concern, in that it is very likely to be a distraction within the company at a time when it can ill afford distraction. While it is important not to put too much weight on media stories, the most significant feature of the media attention is simply that there has been so much of it. This raises a flag of caution without being itself a cause for enforcement action.

Assessment and Strategy

In reviewing the case after it has finished, the instructor should encourage participants to discuss the significance of each of these issues and to revisit their earlier action plans. The idea is to help the groups to use their earlier assessments, plus the assessment above to rethink an appropriate strategy.

It may be productive at this stage to help them with how to go about the construc-tion of an action plan. For example, there is a need to identify the main issues, prioritize them, and devise a plan to pursue them.

The main issues, in rough order of priority, at this stage should be:

a) Lack of clear responsibility for and ownership of risk management frameworkb) Persistent material errors in quarterly returns

HIH Case Study on Corporate Governance (Teach�ng Note)

�

c) Absence of procedures for dealing with breaches of internal investment guide-lines

d) Lack of documentation for some internal investment policies and guidelinese) Lack of policies in some areasf) Concern that these control failings may apply to other areas as well as to invest-

mentsg) Concern about conflicts of interest at board levelh) Concerns about the board’s approach to fulfilling its governance responsibili-

tiesi) Concern about the strategic direction of the companyj) Concern about the quality of the company’s leadershipk) Concern about the potential distraction of senior management while the leader-

ship struggle continues.

In this case, judgment needs to be made about the quality of governance and con-trol mechanisms in operation at HIH and the risks that they pose to the institution. Having reviewed the information available on these issues, the questions for this and future rounds should be:

1) Do I need more information and, if so, what?2) What tools and strategies can I employ to obtain the information?3) Do I have the basis for taking intervention action, and if so, what? What powers

can I make use of to intervene as needed?

1) Do I need more information and, if so, what?

In a broader, real-world exercise, the solvency position of HIH would be of vital impor-tance and there would be a range of issues to follow up related to the valuation of both assets and liabilities. In the current case, however, the focus is exclusively on governance and control issues and participants should assume, for the purpose of this case study only, that HIH exceeds its minimum solvency requirement by an acceptable margin. Thus, the objective should be to follow up the higher priority governance issues in the expectation that they will reveal other problems if they are present.

Key areas worthy of further exploration include:

• The role of the board, including its approach to strategic direction, its approach to governance, its role in setting and monitoring internal guidelines, and its recognition of and approach to conflicts of interest

• The role of management in formulating and monitoring risk management poli-cies and guidelines

Insurance Superv�s�on Core Curr�culum

�

• The quality and reliability of information provided to management and the board

• The source of the errors in the quarterly returns—are they deliberate or the re-sult of poorly integrated information systems?

• The role of the internal and external auditors in the governance and control functions of the company.

2) What tools and strategies can I employ to obtain the information?

First, the nature and extent of the governance failings require a direct approach to the board of HIH. Discussions should start there and proceed down through the institu-tion. There is a prima facie case that the HIH board may not be aware of the governance failing throughout the company’s operations.

Second, appointments should also be set up to discuss matters with both the in-ternal and external auditors.

Third, the head of the asset risk team should also be consulted to hear verbally about any information and concerns that may not have been committed to paper fol-lowing the onsite visit.

Fourth, some useful research by your staff could be directed toward finding out more about the background to the media stories and to following up any market ru-mors.

In preparing a set of informational requests for HIH it is important to decide to whom the request should be directed, how much urgency it should reflect, and how specific the requests should be in terms of who you need to speak with and on what timetable. Work assigned to your own staff is likely to produce results much more quickly than requests to HIH.

Finally, in a situation such as this (serious concerns about the second largest gen-eral insurance company), there is a need to consider what reporting should be done within the regulatory agency and whether or not you should be asking for help from your superiors.

There is a tendency in many regulatory agencies for individuals to feel that they should be able to handle issues without reference “up the line.” This is brave but not good practice. This is an issue that should be discussed with the participants. In this case the institution is significant within the general insurance industry (even if not on the broader financial sector scene). A reasonable assessment of who needs to be con-tacted in this case would include the following:

• The executive general manager of the DID and the CEO should be informed immediately of your concerns. The decision as to whether or not the minister should be informed then rests with the CEO.

HIH Case Study on Corporate Governance (Teach�ng Note)

�

• A briefing paper on the seriousness of the situation should be prepared for your board.

• You should discuss with your superiors whether or not resources can be spared from elsewhere in the agency or outside resources contracted in to help deal with what is likely to be a major exercise.

• A schedule should be agreed with the relevant parties for reporting back to your superiors and the board to keep them apprised of developments.

While managers need to be conscious of not “crying wolf ” on every minor concern, it would be extraordinary in a situation as striking and as potentially damaging as this if the manager were to be admonished for wasting time and resources, if the outcome of the investigations were to be a clean bill of health for the institution.

How should I prioritize these needs in view of other demands on my time and that of my branch and any other considerations?

This essentially comes down to the formulation of an action plan. Some useful guide-lines in a case such as this are:

• Keep within the legal powers available but be prepared to push the frontiers informally as much as possible (this last point should be emphasized as much as possible and participants encouraged to use whatever levers they have at their disposal to effect change).

• Prioritize your requests. Long lists of requests tend to be met with either of two responses: no response (on the grounds that they are taking a long time to answer all your questions) or quick responses addressing the least important questions (usually those that are easiest to answer).

• Work on the rule of thumb that, where problems have been identified, their eventual financial impact can be many times the amount initially estimated.

Action Plan

A well thought-out action plan at this stage would include most or all of the following (with a time frame for each reflecting the urgency involved):

1. Request an urgent meeting with your superiors—executive general manager of DID and CEO—to explain the situation and to agree regulatory steps involving the board, minister, etc. (Time frame: immediate)

2. Request a meeting with the asset risk team. This team investigated 3 property loan files out of a possible 58 and found problems with all of them—and major

Insurance Superv�s�on Core Curr�culum

�0

issues in at least two cases. The probability of this being a random outcome is effectively zero. Talk with them about their findings and let them help you pri-oritize where the governance review should focus. (Time frame: within the next few days)

3. Prepare a list of governance issues with documented support in preparation for a meeting with the HIH board. (Time frame: within 1 week)

4. Through the HIH chairman, request a meeting with the nonexecutive members of the HIH board to discuss governance issues. In preparation for this meeting it would be useful to request a copy of HIH board minutes over the past two years. (Time frame: within 1 week for the board minutes and within 2–3 weeks at the latest for the meeting with the nonexecutive board members)

5. Write to the CEO of HIH requesting a meeting to further discuss the reporting problems. This letter should be very stern and should set out the issues uncov-ered in the asset risk visit and other inconsistencies. It should be made clear that this is a significant issue. Late lodgment of the June returns will be unacceptable and will be regarded as grounds for enforcement action under s44 of the Act. (Time frame: send letter immediately with follow-up to occur within days to agree a timetable for meetings and responses)

6. It would be very helpful at this stage to arrange a meeting with the external audi-tors of HIH to discuss the full range of governance issues—especially the lack of reporting and action on breaches of internal guidelines. Although there is no legal power in the Act to conduct such meetings, it would be worthwhile to speak with the auditors to arrange an off-the-record meeting to discuss your concerns. They may, of course, refuse, on the grounds that there is no legal power in the Act to conduct such meetings. Such a meeting is legal provided the company (HIH) agrees to it. Thus, if the auditor refused, the request could be put to the HIH board to approve the meetings, with the implicit threat of more aggressive action if they did not comply. In any case, a refusal by a regulated institution to agree to such a request would be a signal that the problems are probably much more deeply seated than they appear at the surface. (Time frame: 2 to 3 weeks)

7. Arrange a meeting with HIH’s internal auditors. (Time frame: 2 to 3 weeks)8. Commission one of your staff to start gathering any available information about

conflicts of interest among HIH board members. He or she should speak with media contacts, find out if anyone in APRA has a contact within Arthur An-dersen or HIH, track down any information disclosed in annual reports, com-pany publications, and so on. Market gossip is not entirely reliable but it can also be a useful source of leads.

HIH Case Study on Corporate Governance (Teach�ng Note)

��

3) Do I have the basis for taking intervention action, and if so, what? What powers can I make use of to intervene as needed?

As noted in the background material, APRA was operating under an Act that had many weaknesses. It did not generally contemplate onsite examinations unless an insurer was on the verge of commercial insolvency. The main provision of the Act dealing with on-site inspections is Section 52, which gave APRA the power to investigate the whole or any part of the business of the insurer or to appoint an inspector to carry out such an investigation. However, such an inspection could be carried out only where it appeared to APRA that the insurer was, or was about to become, unable to meet its liabilities or had contravened or failed to comply with a provision of the Act.

In short, unless APRA had prima facie evidence of a breach of the Act, an autho-rized insurer had to be on the brink of commercial insolvency (not just statutory insol-vency) for a full onsite inspection to be conducted within the legitimacy of the Act.

As stated earlier, in a broader exercise the solvency position of HIH would be cru-cial at this stage and there would be a range of issues to follow up to determine HIH’s true solvency position. This case study is focused purely on governance and control issues and as such, participants must explore other avenues for intervention action, if deemed necessary.

For example, although the Act did not give APRA the authority to make an inde-pendent verification of information submitted by an insurer, except in extreme circum-stances such as where insolvency was imminent, APRA had “the power to require an insurer to furnish information to the regulator in support of any returns lodged with the regulator (S51).” Alternative action would also be possible under s44 of the Act re-lating to the submission of accounts.

Despite the limited formal powers available to APRA, participants are expected to push the boundaries of these legal powers. The best supervisors begin by trying to define the problem they need to get solved and then make a full inventory of the tech-niques at their disposal for finding a solution. Legal powers are used creatively, not as a series of barriers designed to restrict the actions of the supervisor.

Further, good supervision detects problems and encourages or forces remedial ac-tion without having to resort to legal powers or formal enforcement action. Where a true “rogue institution” is encountered, and HIH was close to being one, enforcement action may be the only option that works. But there will be many situations in which weakness can be detected and remedied through moral suasion or even threats to issue directions, without resorting to the use of formal powers.

A supervisory authority, in trying to encourage and ensure the financial health of the financial institutions that it supervises, needs to go beyond enforcement and make use of a wide variety of supervisory actions. Some of them may fall under the heading of enforcement but most will fall under the broader headings of information gathering and supervisory intervention. Actions under those headings will include informa-tion requests, visits, inspections both informal and using statutory powers, informal

Insurance Superv�s�on Core Curr�culum

��

and formal suggestions, requests and directives directed to senior management or the board.

Round Two

The base information provided in this round should be enough to provoke serious con-sideration of intervention action by the supervisory authority. The situation, however, is complicated by the Allianz deal.

The combination of the long history of late and incorrect returns, the litany of is-sues raised in the asset risk visit, the lack of focus on governance concerns as evidenced in the diary notes and review of board minutes, and now the damning report from the ex-employee (attachment 2), suggests that this is a company that is probably papering over the cracks. This is supported by the media’s assessment of HIH as a distressed seller.

When a number of independent sources reinforce the perception of problems such as poor governance, misclassification of assets and liabilities, questionable accounting practices, overvaluation of assets, and so on, there is a strong likelihood that things are much worse than they appear on the surface. Although not usually included in any legal document or even in internal regulatory procedures, utilizing these sources is funda-mental to good forensic supervision.

The conundrum at this point is the deal that has been announced with Allianz. Any regulator faced with a problem institution usually looks first for buyers of all

or part of its operations as a way of protecting policyholders. If buyers cannot be found, provided commercial solvency is still intact, there is still the prospect that some parts of the business may be put into run-off. If commercial solvency is breached, liquidation may be the only alternative. Liquidation is a worst-case option that virtually ensures the destruction of value and exposes policyholders to loss.

Discussion Point

Although this case study requires the participants to develop action plans and strategies

in the context of the legal framework under which APRA operated, a valuable exercise

would be to discuss how those strategies would be affected if the participants faced a

similar scenario in their own jurisdictions and under their own legal frameworks.

In a more modern legal framework additional strategies may include in-depth inspec-

tions, verification of regulatory returns, information requests, expanded audits by internal

or external auditors, meetings with senior management or board to express concerns,

strong requests to take specific remedial action, requests to comply, directives to senior

management and the board, imposing fines, increasing capital, removal of management

or directors, formal investigations, or taking control of the institution.

HIH Case Study on Corporate Governance (Teach�ng Note)

��

The Allianz deal can logically be viewed as the first step in selling down the HIH business. The attraction of the Allianz deal is that it provides safety for the bulk of HIH’s retail insurance portfolio by moving the policies to a joint venture that will be under the protection of a stronger company. What is important is that it is highly likely that Allianz will eventually become the sole owner of the portfolio. The Allianz deal also extracts some value from HIH’s very high level of goodwill.

The wrinkle in this interpretation is that the Allianz deal contains an escape clause that is triggered by a number of events, including the event of regulatory action against HIH. Thus action against HIH at this stage could harm the policyholders that APRA is required to protect.

This is a difficult issue that should be discussed by the cohort during the review session. They should be encouraged to think of creative ways of dealing with the problem.

The Allianz Joint Venture (Attachment 1)

As noted earlier, the Allianz joint venture signals a major sell-down of the company’s business. The critical factor here is the clause that allows Allianz to walk away from the transaction in the event of regulatory action against HIH.

The transaction raises a number of governance issues. First, APRA was not noti-fied about the transaction before its announcement. While there is no requirement in law for it to do so, in view of the close attention being given to HIH it is more than a little surprising that there was not some discussion of this significant transaction and an opportunity for APRA to assess its impact on the company as a whole. The regulatory trigger and the possible liquidity impact are matters that should have been discussed before the announcement.

Second, the lack of detail in the announcement and the company’s inability to re-spond to the media’s questions about detail points to a deal that may have been hur-riedly thrown together to enable its announcement alongside the disappointing profit release (a point made repeatedly in the media). The throwaway comment by the senior analyst about his discussion with a couple of HIH board members could be telling. It will be important to find out quickly what role the board played in the decision and how much due diligence was carried out before the announcement.

The Ex-Employee’s “Whistleblower” Document (Attachment 2)

Whistleblower documents should always be handled with caution. There are many cases in which disgruntled ex-employees have caused significant financial upheaval by making unsubstantiated and malicious claims about companies or individuals. They

Insurance Superv�s�on Core Curr�culum

��

should not, however, be ignored; experienced supervisors, auditors, and tax officials know that some of the most useful information comes from disgruntled employees.

While few of the issues raised are new, the memorandum demonstrates such a deep knowledge of the company that each of the concerns raised warrants investigation. It is customary to follow up on such information, without necessarily rushing to judgment.

The real significance of the report is the extent to which it supports and corrobo-rates concerns raised from other sources. This sort of reinforcement provides powerful support for enforcement action.

The governance issues raised are many. The comments on poor management and conflicts of interest among board members do not provide new information, but they suggest that the market’s perceptions of conflicts may be close to the reality. The com-ments about HIH’s lack of due diligence in its purchase of FAI and its refusal to allow others to carry out due diligence on its operations is a serious flag, both of poor man-agement practices and of possible hidden problems.

Most importantly, the whistleblower document provides a road map of issues and estimates to use in testing its substance with HIH and its auditors. This is a significant advantage in heading into any investigation.

In the short term, this whistleblower could be a very useful source of information about many of the governance issues that APRA is pursuing.

Letter to Abela – Data Inaccuracies (Attachment 3)

This e-mail reinforces one of the most worrying trends in the regulatory relationship—continuing inaccuracies in data returns. The message should be becoming very clear by this stage. Either there is deliberate manipulation of information going on or HIH’s data systems are simply not capable of producing properly reconciled group-wide figures. Either outcome is a cause for major concern. Given the recent absorption of several acquisitions it is likely that group-wide consolidation is the problem. Nevertheless, if the group is unable to produce audited consolidated figures on a consistent basis, it is highly unlikely that anyone in the company understands the true state of the company’s financial position.

The Asset Risk Team’s Discovery (Attachment 4)

This note is particularly significant in terms of governance. If the board members were aware of the implications of the SocGen transaction then they are guilty of deliberately violating the law on disclosure. If they were not aware, then a significant commitment was entered into by the company without the board’s knowledge. Either way there is ev-idence of a major breakdown in governance. This must be followed up with the board.

HIH Case Study on Corporate Governance (Teach�ng Note)

��

Meeting with Asset Risk Team (Attachment 5)

This memo is most significant for the strength of opinion passed by the team leader about the poor governance involved at HIH with respect to their investment files and for what she had to say about the attitude of staff and management at HIH—namely, that they were uncooperative, evasive, and apparently unfamiliar with their responsibilities. While not the sort of evidence that is needed in court when defending a “show cause” letter, this is a further indictment of the way in which the company is run, a further indication that things are probably much worse than they appear on the surface, and a further warning that HIH is unlikely to be cooperative with efforts to resolve issues. The sting in the tail about the way in which the visit was terminated is a serious flag.

It is clear from this action that HIH is not cooperating with the regulator and is likely to use legalistic tactics to block any attempt by the regulator to take enforcement action. The exit of Williams may improve that situation a little.

Meeting with Nonexecutive Board Members (Attachment 6)

This Diary Note is governance dynamite. It is clear from the list of responses that the HIH board has no concept of good governance:

• They claim to have governance systems in place but have no idea whether or not they are working in practice.

• They are uninformed about breaches—in other words there are no monitoring mechanisms in place to test the controls.

• There is no documented strategy. It is a key role of any board to provide stra-tegic direction. Discussion of strategy in the context of annual budgets is almost certain to focus on minutiae. The lack of a corporate strategy is particularly alarming in view of the company’s recent rapid growth by way of takeovers.

• There are no formal delegations. It is through making delegations, parameter-izing them, and monitoring their execution that a board meets its responsibili-ties. The chair was not even aware of any delegations from the CEO to staff.

• Remuneration of senior management is the province of the board. It is ulti-mately the board’s responsibility in its role as steward of the company’s resources to ensure that its executives are not remunerated at levels that cannot be justified as a proper application of shareholders’ funds.

• The audit committee fails any test of independence. First, the chair of the com-pany should not even be on the audit committee (though he or she may be in-vited to attend). Second, two members of a three-person audit committee were ex-partners of the audit firm. Third, the timing of meetings and the fact that all members (including executive members) were invited to join the meetings means that they were hopelessly compromised in terms of independence.

Insurance Superv�s�on Core Curr�culum

��

• The chairman was totally passive in the matter of conflicts—on a board that ap-peared to be riddled with conflicts.

Issues Uncovered in Board Minutes (Attachment 7)

The board minutes are almost as much a source of concern as the meeting with the nonexecutive directors. They are totally uninformative. They convey an impression of a board that is detached, dominated by management, and totally focused on financial reports.

Even more worrying, the quote from the minutes refers to a consultancy arrange-ment with Rodney Adler as well as to a number of related-party transactions in which significant sums are involved.

Media (Attachment 8)

The main significance of the media reports is that they clearly see HIH as a company in distress and subject to takeover offers. At the same time they do not say or imply that the residual business will not be viable after the Allianz joint venture. The stories em-phasize a few relevant points:

• The critically low share price (now in the 50 cent range)—to the extent that market information is a leading indicator of problems, the dramatic fall in the share price over the past year or so, and especially the fall since early September, is a strong signal that the market is getting out of HIH as quickly as it can.

• The fact that, without the Allianz deal, HIH should probably have taken a large part of goodwill to P&L in the last account, which would have generated a sig-nificant loss.

• The uncertainty created by Williams’ departure.

Round 2 Assessment and Strategy

Following the same logical decision process outlined above should produce responses along the following lines:

1) Do I need more information and, if so, what?

From a governance perspective, there is still much to be confirmed:

HIH Case Study on Corporate Governance (Teach�ng Note)

��

• To develop a better understanding of the board processes, it would be helpful to see the information that has gone to the board for its quarterly meetings.

• To better understand the board’s role in the company’s strategic direction it would be useful to review the papers prepared in relation to each of the recent acquisitions.

• To pursue the concerns associated with the SocGen transaction it would be useful to review its documentation and approval trail.

• To get a better grip on the conflicts problem it would be useful to see copies of relevant contracts with board members and to have someone follow these through other sources as well, including through the whistleblower.

2) What tools and strategies can I employ to obtain the information?

The issues identified above can be resolved only by spending a considerable amount of time and creative energy with the company and its auditors.

On the basis of the information available, it is not unreasonable to assume that HIH and probably even the auditors will be uncooperative—covertly if not overtly. The only way to deal with this is to approach each meeting with specific, well-researched is-sues and a set of very direct questions. Approaching such a meeting as a “fireside chat” or as a “fishing expedition” is likely to be a waste of time. Meetings need to be sched-uled, with follow-up dates agreed. Specific requests for information should be delivered in advance. The direction of questioning, at least initially, should be held back until the information is provided and the meeting under way, so as to avoid providing too much opportunity for orchestrated responses designed to mislead or cover up the truth.

The other party that should be engaged at this stage is Allianz. Allianz is a licensed, supervised institution. Since its transaction with HIH and the trigger clause are fun-damental to your action plan, it should be a high priority to meet with the CEO and chairman of Allianz to discuss the issues informally. The fact that APRA has to ap-prove the transaction under the Financial Sector Shareholdings Act means that such a meeting will be necessary anyway. If Allianz is willing to continue with the transaction and perhaps accelerate its consummation, that may open the way to initiate enforce-ment action against HIH without endangering those policyholders who already have the prospect of some protection.

All available resources should be harnessed and as much seniority as possible brought to bear to ensure that your demands are taken seriously. If your own board and the board of HIH have not been engaged by now they should be, as a matter of priority.

Insurance Superv�s�on Core Curr�culum

��

Avenues of Follow-up

The following are some of the more obvious avenues for follow-up:

• If not already requested, there should be a request to see all board papers pre-sented to the HIH board over recent years. This should be used to assess:

– The involvement of the board in key decision making (for example, in stra-tegic direction such as acquisitions)

– The quality of information provided to the board, including the amount, if any, of control feedback

– The extent of disclosure of board members’ conflicts of interest.

• Following receipt of the board papers, a meeting should be set up with the HIH board to discuss the SocGen swap transaction in order to ascertain the extent of the board’s knowledge about it.

• Given the concerns raised about the audit committee’s independence in the meeting with the HIH board, the committee’s charter should be requested and reviewed.

• Related-party transactions and conflicts of interest have been a consistent theme of the market investigation. This should be continued, with focus on disclosures in annual reports, discussions with journalists and industry contacts, direct dis-cussions with some selected staff at HIH (including the whistleblower), and any other sources that can be found. The idea is to try to turn up leads in much the way that an investigative journalist might.

All these matters should have a very high priority and should be completed within a month at the latest. All requests for information should be for immediate delivery, notwithstanding that HIH may invoke legal maneuvers to try to slow them down.

3) Do I have the basis for taking intervention action, and if so, what? What powers can I make use of to intervene as needed?

Yes. On the basis of the information provided there is a very strong evidence of serious governance problems within HIH and there can be no confidence in the board or man-agement of HIH to identify and deal adequately with the problems it currently faces. There is a need to follow the identified problems through further and to work with the company very closely to correct the failings. The information provides strong evidence of almost total governance breakdown. It is reasonably clear that the board has little idea of what is going on in the company and it is unlikely that anyone else does.

HIH Case Study on Corporate Governance (Teach�ng Note)

��

The abrupt termination of the asset risk review by the CEO would be a clear signal to an experienced supervisor that the financial institution had something to hide. Under such circumstances, there must be some form of supervisory intervention in response. Failure to act allows the institution to continue to conceal that which it does not wish the supervisor to know and reinforces the loss of authority suffered by the supervisory authority when it allowed its work to be cut short by the institution.

As noted in round 1, formal legal powers available to APRA were limited (assuming we are focused solely on governance issues). However, an effective supervisor should be willing to push the boundaries informally as much as possible, including strong no-tification to the board that the situation must be rectified. Other action could involve sections 44 and 51 of the Act. All available resources should be harnessed and as much seniority as possible brought to bear to ensure that your demands are taken seriously. If your own board has not yet been engaged with the board of HIH, it should be a matter of priority.

If the supervisory authority does not take intervention action at this point it would be largely because of concern that it needed more support for taking such action against a significant company that is likely to resist any such action in the courts—coupled with concern about derailing the Allianz deal.

The best strategy at this stage is still open to debate. There is no right or wrong answer in a situation such as this. Some countries have legislated early action require-ments into their laws to remove discretion from supervisors. Others recognize that pru-dential regulation often requires working with an institution to find the best way out of a problem. The key to serious intervention is likely to lie in the assessed solvency situa-tion, which is not the focus of this case. If solvency is marginal or in breach of statutory requirements, the poor governance of HIH would be sufficient to tip the scales against forbearance.

APRA Involvement with the Appointment of the new CEO

If the decision is taken to work with HIH a little longer, the issue of the replacement CEO becomes important.

The issues are the following:

Discussion Point

As for round 1, although this case study requires the participants to develop action

plans and strategies in the context of the legal framework under which APRA operated,

a valuable exercise would be to discuss how those strategies would be affected if the

participants faced a similar scenario in their own jurisdictions and under their own legal

frameworks.

Insurance Superv�s�on Core Curr�culum

�0

• Given that the company is in such difficulty and that the board has so little knowledge of the company, appointing a complete outsider at this stage would be dangerous. Difficult decisions will be needed in the near future. Someone with knowledge of the company is likely to make those decisions better than a newcomer.

• The market concerns about Rodney Adler appear to be warranted. Given his history with FAI, the possible role he has played in destabilizing Ray Williams, and his list of conflicts, the company’s stakeholders are unlikely to be well served by his appointment.

Under the circumstances there is a good case for regulatory involvement (a) to let the chairman know that Adler would not be acceptable and (b) to ensure that the regu-lator is kept informed of where the decision is heading and thereby has an opportunity to object if the decision is likely to endanger policyholders further.

Round Three

HIH is clearly a company that is in total governance breakdown.

The Pacific Eagle Equities Transaction (Attachment 1)

This note raises several serious governance concerns. The first is the suggestion that the company may be in breach of Corporations Law. Equally worrying is the way in which the HIH board has handled the matter and the lack of good governance processes.

The first issue is that the matter of the investment of money of HIH with PEE was not raised in any substantive way with the directors of HIH, until it was raised by the auditors at the audit committee meeting on 12 October 2000.

This is striking because the investment was made in June 2000. By as early as Au-gust the auditors had questioned management about the validity of the share trading by PEE in HIH and Adler had sought legal advice on the topic.

The issue raised by the auditors was serious. It related to a possible contravention of the Corporations Law by directors, including the chief executive. Its seriousness must have been obvious to management. Yet it was not brought to the attention of the audit committee at its meeting on 12 September 2000, other than by a possible passing refer-ence by Buttle to there being a “matter of the Trust.” Nor was it raised at the meetings of the board early in September 2000. There was no mechanism in place in HIH for a regular report to be made to the board upon the group’s compliance with its legal re-sponsibilities, other than through the internal audit reports.

HIH Case Study on Corporate Governance (Teach�ng Note)

��

The second issue is that, despite being fully aware of the issue and its potential sig-nificance by early November, the chairman did not include it in the board agenda for the meeting on 15 November.

Third, it is clear from the minutes that the legal advice was tabled at the meeting—rather than circulated in advance—which means that the board members were asked to reflect on a possibly significant breach of the law on the run. As such they would have been reliant on the summary of the opinion presented by management.

Fourth, Minter Ellison, the legal firm employed by HIH to provide an opinion on the legality of the transaction, was the very firm that established the trust and gave legal advice to Adler, the perpetrator of the potentially illegal transaction, thereby putting them in a position of conflict.

Fifth, in seeking a legal opinion, management’s concern was to seek legal advice which confirmed that there was no breach, rather than to seek legal advice as to whether or not there was a breach. In particular, the request was narrower than that suggested by Buttle for Andersen. The legal advice should have been commissioned by the board rather than by management and the orientation of the inquiry should have been dif-ferent.

Finally, Adler and Williams were present during the board’s consideration of the issue. This involved a clear conflict of interest given their role in the transactions.

The Preference Share Issue (Attachment 2)

The accounting treatment of the preference share issue is, at best, questionable. FAI Insurances Limited published in its consolidated financial statements for 30

June 2000 a statement of the amount of its capital as at that date. The statement was false and misleading by virtue of the inclusion of A$200 million capital in respect of the pur-ported issue of redeemable preference shares. FAI Insurances Limited might thereby have contravened s1308(1) of the Corporations Law.

From a governance perspective, a greater concern is the fact that the documents for the transaction were received from Andersen Legal on 25 October but were signed 23 June. This appears to be a clear contravention of s180(1) of Corporations Law.

The backdating of documents is a serious matter. It is the backdating, not the inap-propriate accounting treatment of the share issue, that is the central issue here.

Home Security International (Attachment 3)

As much as anything, the HSI saga is testimony to Ray Williams’ incompetence as a manager. It is difficult, for example, to understand why Williams allocated significant monies toward gaining control of both HSI and FFC and then did not seek to exercise it. For example, Williams does not appear to have ever considered seeking to remove

Insurance Superv�s�on Core Curr�culum

��

Cooper and then commencing an orderly run-down of HSI’s business and selling off its assets. This would probably have led to losses on book values but would have been preferable to the “solutions” that were put in place. It brings into question Williams’ ability to adopt a strategy and execute it, to make judgments about individuals, and to act accordingly. It also gives an insight into the way in which he approached transac-tions conferring private benefits to others.

The more significant issue from a governance perspective is the lack of disclosure of the HSI and related transactions to the HIH board. This is even more of a concern given the related party involvement of Adler in the transactions. The acquisition of the further 10 percent of HSI, the lending of further funds between May and August 2000, and the Ness acquisition were all implemented without disclosure to the board. The FFC acquisition was not disclosed. The board had no means of ascertaining what was occurring with HIH’s investment in HSI, much less any means of assessing the perfor-mance of the executives involved in it. It must have been obvious through 1999 and 2000 that HSI was becoming, or had become, a disaster and the deals being proposed were unusual. In those circumstances the board was entitled to expect full disclosure of all relevant and material matters.

The Allianz Deal (Attachment 4)

The almost total lack of board involvement in a transaction that signals a significant shift in the company’s direction is nothing short of mind boggling.

The board made no strategic decisions in this matter. An informal dinner meeting is clearly an inadequate forum to deal with important matters going to the future stra-tegic direction of the company and the disposal of one of its most profitable lines of business. While the issues might have been broached at such a meeting, they called for more detailed elaboration and deliberation. This is particularly the case given that some directors were not present at the dinner and were not otherwise advised of the discus-sions that took place at the dinner.

It is clear that management distributed an information memorandum to possible purchasers and invited tenders before even informing some of the board members.

The Allianz transaction represented a profound change in the strategic direction of HIH. It is simply extraordinary that management pursued a change of that signifi-cance without even informing the board, let alone putting forward a proposal. Further, the board apparently was prepared to accept such a passive role. That the information memorandum was distributed without board approval was a clear sign that manage-ment misconceived the true extent of their proper authority. The board should have reprimanded management for distributing the information memorandum without board approval. Instead they seem to have been swept passively along.

HIH Case Study on Corporate Governance (Teach�ng Note)

��

The Request for an Extension for Lodgment of June Returns (Attachment 5)

Consistent with everything else going on in this company, the request for an extension of time for submitting the quarterly returns is simply unacceptable—notwithstanding the many distractions that the company was going through.

Audit Committee Charter (Attachment 6)

This document is remarkable for what it does not cover. The charter lacks specificity in terms of both the committee’s responsibilities and its relationship to the board. It makes no reference to risk management or compliance—central roles for any audit committee. There is no mechanism for monitoring its performance. It meets too infrequently. In practice, the composition of the committee results in its being compromised.

Consultancy Arrangements (Attachment 7)

The information in this note is dynamite. It should be noted that to track down this much detail would require a lot of luck as well as a very good forensic nose on the part of the supervisor.

The upshot is that the HIH board was riddled with conflicts of interest.The HIH board had no understanding of what was involved in the concept of a

conflict of interest and the critical importance it holds in corporate governance. The fact that the chairman himself had conflicts meant that he was not well placed to deal with conflicts raised by others. In practice they rarely appear to have raised them. The fact that neither Cohen nor Abott declared their consultancies in the annual reports of HIH is arguably a breach of Corporations Law on disclosure. That they did not declare their interests to other board members and that there was no regular mechanism for declaring and dealing with conflicts is an indictment of the governance systems (or lack thereof) of the company.

Where consultancies were disclosed to the board, there is no evidence that they took the trouble to inquire about their terms or appropriateness.

The SocGen Swap Follow Up (Attachment 8)

There is reasonable evidence that the board was misled by Fodera about the true nature of the swap transaction and its implications for disclosure. There is little doubt, how-ever, that as a result of the swap HIH violated Corporations Law on disclosure.

Insurance Superv�s�on Core Curr�culum

��

Media (Attachment 9)

The media is becoming increasingly outspoken about the lack of leadership at HIH. Ep-ithets such as “incompetent,” “apathetic,” and “dismal,” are hardly a sign that the market is viewing the events of recent times with favor.

Round 3 Assessment and Strategy

The evidence about poor governance has become overwhelming. HIH is clearly a com-pany out of control. All internal controls and governance systems, to the extent that they ever existed, have clearly broken down.

Despite these concerns, ignoring the question of solvency, APRA’s formal powers are limited. A more useful discussion at this point is the intervention action that could be taken under a more modern legal framework, such as may exist for participants in their own jurisdictions.

Summary of Lessons from the Case

After finishing the review and discussion of all the material available in the case, par-ticipants should be encouraged to write down the top 5 to 10 lessons that they have derived from the case and the review discussion. Lessons might include some or all of the following (in no particular order):

• Governance is more about substance than form—the focus of a supervisor’s ef-forts should be to ascertain how the governance systems are working in prac-tice.

• Governance starts with the board. A well-governed institution will have a board that is cognizant of the underlying principles of good governance—openness, integrity, and accountability—and committed to their application.

• A well-governed board will have a clear and well-documented understanding of its role. That role should take responsibility for everything that it can reasonably

Discussion Point

As for rounds 1 and 2, although this case study requires the participants to develop ac-

tion plans and strategies in the context of the legal framework under which APRA oper-

ated, a valuable exercise would be to discuss how those strategies would be affected if

the participants faced a similar scenario in their own jurisdictions and under their own

legal frameworks.

HIH Case Study on Corporate Governance (Teach�ng Note)

��

be involved with—at a minimum this should include strategic direction, man-agement accountability, and compliance.

• Where the board delegates responsibility (for example, for the day-to-day run-ning of the organization), it should document those delegations, parameterize how the delegations are to be exercised, and establish a process under which management will account to the board for the exercise of its delegated au-thority.

• A well-governed board will establish subcommittees that have clear charters of responsibility and are demonstrably independent of management in carrying out those responsibilities. The independence and effectiveness of both the board and its subcommittees should be subject to regular review. While board sub-committees usually provide expertise and advice (in some cases from outside experts who are independent of management) to the main board, it is important that not usurp authority from the main board.

• A well-governed institution will ensure that the information coming to the board is relevant and timely. The chair should have a role in setting the agenda, with input from time to time from other board members. The information frame-work should be reviewed regularly by the board.

• A well-governed organization will have a regular process of review of its gover-nance principles and practices—ideally this should involve outsiders.

• A well-governed board will have addressed key governance issues and have de-veloped and documented a policy on each. Issues covered should include mat-ters such as identifying, declaring, and dealing with conflicts of interest and disclosure of conflicts to the public.

• A well-governed institution will have a system in place for monitoring and re-porting breaches of internal policies.

• A well-governed institution will have a process for reviewing the effectiveness of its monitoring and reporting systems.

• In terms of investigating governance problems several avenues should be ex-plored:

– Direct discussion with nonexecutive members—or even one-on-one discus-sions if needed;

– Board minutes– Board papers– Annual reports (for disclosures)– Board policies, strategy documents, and governance documentation (the

absence of these is a strong flag that there could be problems)– Discussions with staff, internal and external auditors, media, industry con-

tacts, etc.

• Signs to recognize as indicators of governance problems:

Insurance Superv�s�on Core Curr�culum

��

– Absence of documentation about governance issues– Poor understanding on the part of board members and management about

their respective roles– Evidence of failures in the reporting and acting on breaches of guidelines– Absence of a clear responsibility structure for compliance– Absence of documented delegations– Conflicting evidence or opinions about how certain governance structures

operate (in a well-functioning system everyone should be aware of the sys-tems and how they work)

– Signs that the information systems are not functioning properly (this is a particular concern when a company is still absorbing acquisitions)

– Evidence from inspections (or other sources) that files are disarray, docu-mentation is missing, or there are consistent errors in returns

– Evidence of reluctance on the part of the board and senior management to act quickly and decisively in the face of evidence that the governance system or controls may not be operating as intended or that breaches are occur-ring—a commitment to good governance must involve a commitment to expeditious action in response to failings.

– Evidence of important policy decisions not escalated to the board– Evidence that important policy decisions are escalated to the board for dis-

cussion or information rather than for approval– Evidence that important policy decisions are escalated for board approval

but the briefing material is inadequate, the board is given too little time to consider it, or board discussion (as evidenced from the minutes) is perfunc-tory

– When making important decisions, there is no evidence that board mem-bers challenge top management

– When approving an important policy decision, the board does not set mile-stones and criteria for evaluating the results of the policy decision.

Comments from the Royal Commission

As part of the review session it would be useful to include discussion of some of the is-sues by reference to some of the conclusions drawn by Justice Owen in the Royal Com-mission. Edited excepts follow.

Corporate Culture

A cause for serious concern arises from the group’s corporate culture. By “corporate culture” I mean the charisma or personality—sometimes overt but often unstated—that

HIH Case Study on Corporate Governance (Teach�ng Note)

��

guides the decision-making process at all levels of an organisation. In the case of HIH, the culture that developed was inimical to sound management practices. It resulted in decision making that fell well short of the required standards.

The problematic aspects of the corporate culture of HIH—which led directly to the poor decision making—can be summarised succinctly. There was blind faith in a leadership that was ill-equipped for the task. There was insufficient ability and indepen-dence of mind in and associated with the organisation to see what had to be done and what had to be stopped or avoided. Risks were not properly identified and managed. Unpleasant information was hidden, filtered or sanitised. And there was a lack of scep-tical questioning and analysis when and where it mattered.

The Board and Strategy

An experienced Australian company director recently commented that if a director could not articulate the strategy of the company he or she should not be on the board. I share that view, and I consider that this is an area in which the governance of HIH was deficient.

At board level, there was little, if any, analysis of the future strategy of the company. Indeed, the company’s strategy was not documented and it is quite apparent to me that a member of the board would have had difficulty identifying any grand design. If the HIH board discussed strategy at all, it was in the context of an annual budget meeting. But budget sessions are generally about numbers, and there is no indication that the board seriously grasped the opportunity to analyse the direction in which the company was heading.

Generally speaking, it is for management, rather than the board, to propose strategy. This is not an impediment to the board taking the initiative in an appropriate case. But management is best able to dedicate time to strategic thinking and is likely to have greater industry knowledge and experience. Nevertheless, it is the board’s responsibility to understand, test and endorse the company’s strategy. In monitoring performance, the board needs to measure management proposals by reference to the endorsed strategy, with any deviation in practice being challenged and explained. This is what the HIH board failed to do.

A long-term strategy or plan was never submitted formally to the board for critical analysis. Nor did one emerge or evolve informally. In the absence of a framework within which investment and other decisions could be evaluated, the growth of the group was opportunistic and lacking in direction.

There is a related problem. A board that does not understand the strategy may not appreciate the risks. And if it does not appreciate the risks it will probably not ask the right questions to ensure that the strategy is properly executed. This occurred in the governance of HIH. Sometimes questions simply were not posed; on other occasions the right questions were asked but the assessment of the responses was flawed. The

Insurance Superv�s�on Core Curr�culum

��

absence of a well-understood strategy compounds the difficulties that arise in oppor-tunistic development. The failure of operations in the United Kingdom and the United States and the acquisition of FAI provide ample evidence of this.

The way the group managed its entry into and expansion in overseas markets was extremely imprudent and ultimately very costly. It involved bad decision making and a lack of business judgment in circumstances of adverse insurance market conditions. Similarly, the decision to acquire FAI was impetuous and based on completely inad-equate information.

The Board and Governance

HIH had a corporate governance model. The directors said so in the annual reports. But there is little, if any, evidence that the board periodically assessed the company’s corpo-rate governance practices to ensure that they were, and continued to be, suited to the changing environment in which the company operated. For example, what might have been adequate for a group that was primarily Australian based, as it was in 1996, might not have been so as the overseas operations burgeoned in subsequent years. The danger of this practice is that, among other things, it can lead to the ‘tick the box’ approach just mentioned. There is little point in having a corporate governance model if the directors fail to examine periodically its practical effectiveness.

As noted earlier, the HIH board failed to understand long-term strategy. That went to the heart of corporate governance. Apart from that general observation, however, some specific matters arose during the inquiry that do not reflect well on the way HIH was managed:

• An odd feature of the way HIH was organised was the relative dearth of clearly defined and recorded policies or guidelines. There may have been some, but they did not deal with areas essential to the proper running of such a large or-ganisation In any case, where they did exist they were often ignored.

• There were no clearly defined limits on the authority of the chief executive in areas such as investments, corporate donations, gifts, and staff emoluments. In some of these areas the system was out of control but the board did not appre-ciate it. Nor did the board have a well-understood policy on matters that would be reserved to itself. Apart from obvious things—such as financial statements and approvals for large transactions—matters seem to have come forward at the discretion of the chief executive.

• There was a lack of independent critical analysis. The board was heavily depen-dent on the advice of senior management: there were very few occasions when the board either rejected or materially changed a proposal put forward by man-agement.

HIH Case Study on Corporate Governance (Teach�ng Note)

��

• The board’s independence was compromised by the influence of management in relation to its deliberations.

• I was left wondering whether the board as a whole really understood what was involved in the concept of a conflict of interest and the critical importance it holds in corporate governance. Some members may have grasped the theory, but when the activities of the board are examined in detail the position is not at all clear. It seems that from time to time there were disputes even about whether a board member should absent himself during discussion of a particular matter. Some members remained present when, on any objective view, their private in-terests were clearly at issue in a way that might be quite different from the inter-ests of the company.

• There were similar problems associated with related-party transactions. One director considered his personal interests were so well known that in some in-stances he did not have to declare an interest in a transaction to which the com-pany was also a party. In the case of another director, the fact of the interest was disclosed but the paucity of the information provided would have made it very difficult for the other members of the board to decide whether it was in the in-terests of the company to permit the transaction in question to proceed.

• The absence of disclosure by board members did not in itself permit the chairman to assume there was no conflict of interest in a transaction. Nor is disclosure a matter exclusively for the director concerned. The chairman abdicated respon-sibility for taking the lead in securing full disclosure by all directors. Avoidance of conflicts goes directly to the integrity of the board’s processes.

Auditor Independence

Actual independence was defined in the relevant auditing standard, AUP 32, as ‘the achievement of actual freedom from bias, personal interest, prior commitment to an interest, or susceptibility to undue influence or pressure’.

It is rare that there will be definitive evidence that an auditor acted in a particular manner because he or she lacked independence. Unless the auditor has deliberately sought to compromise his or her independence, the auditor is unlikely to identify or acknowledge that an adjustment to attitude or behaviour was made by reason of a lack of independence. There is no suggestion, nor could there be, that any member of the Andersen audit team deliberately or consciously acted in a manner that compromised their independence. That is not to say that I agree with individual decisions they took during the course of the respective audits, but at a general level the evidence did not lead me to conclude they were actually swayed.

Nonetheless, a subjective assessment cannot provide a complete answer in a situa-tion where a person can unknowingly be compromised. Both the auditor and the audit firm must be, and be seen to be, independent.

Insurance Superv�s�on Core Curr�culum

�0

As I have already said, I have no doubt that the circumstances were sufficient to raise a perception of lack of independence. The factors leading to that conclusion in-clude that three members of the HIH board were former partners of Andersen; the reactions of HIH management and then Andersen itself to the meeting between Davies, Gooley, Head and Gardener in March 1999, including Davies’ replacement as audit en-gagement partner; and the pressure upon Andersen partners to procure additional fees from non-audit work by maintaining their relationship with audit clients.

Audit Committee

An effective audit committee needs to evaluate the performance of the external audi-tors on a regular basis. The audit committee of HIH had as its members from early 1999 Gardener and Cohen. Both were former Andersen partners. Cohen had also been a consultant to Andersen following his retirement. In my opinion, this presented dif-ficulties with respect to the HIH audit committee’s ability to perform, and to be seen to perform, an objective assessment of the external audit function.

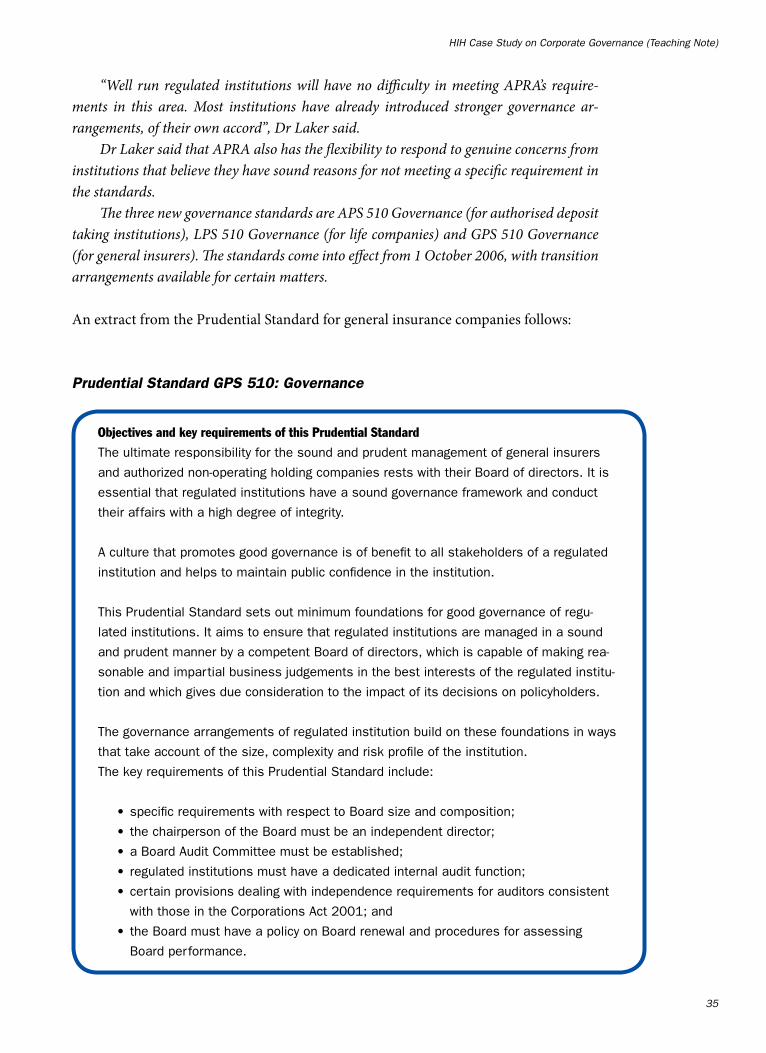

APRA’s New Prudential Standards on Governance