guyana goldfields inc. goldfields inc. and its wholly owned subsidiaries are engaged in the...

TRANSCRIPT

GUYANA GOLDFIELDS INC. Condensed Consolidated Interim Financial Statements

THIRD QUARTER 2017

THIRD QUARTER 2017

1

GUYANA GOLDFIELDS INC. Condensed Consolidated Interim Statements of Financial Position (Unaudited - Expressed in thousands of U.S. Dollars)

September 30, 2017 December 31, 2016 ASSETS

Current assets

Cash and cash equivalents (Note 4) $ 64,162 $ 73,151 Available for sale security (Note 5) 46,348 30,699 Accounts receivable, prepaid expenses and other assets 8,269 5,531 Deposits with suppliers 1,318 7,081 Inventories (Note 6) 36,561 28,904

Total current assets 156,658 145,366

Non-current assets

Restricted cash 1,184 1,184 Mineral properties, plant and equipment (Note 7) 286,403 275,370 Derivative asset (Note 8) 287 1,025 Deferred tax asset 14,616 15,890

Total assets $ 459,148 $ 438,835

LIABILITIES AND EQUITY

Current liabilities

Accounts payable and accrued liabilities $ 9,272 $ 14,320 Current portion of long-term debt (Note 9) 19,466 19,603

Total current liabilities 28,738 33,923

Non-current liabilities

Long-term debt (net) (Note 9) 44,456 58,810 Asset retirement obligations 5,034 4,988 Share based compensation 637 28 Deferred tax liability 9,651 4,242

Total liabilities $ 88,516 $ 101,991

EQUITY

Share capital (Note 10) $ 500,663 $ 490,600 Stock options (Note 11) 5,910 5,999 Contributed surplus 26,824 26,824 Accumulated other comprehensive income 31,531 20,698 Accumulated deficit (194,296) (207,275)

Total equity $ 370,632 $ 336,844

Total liabilities and equity $ 459,148 $ 438,835

The accompanying notes are an integral part of these condensed consolidated interim financial statements. Commitments and Contingencies (Note 14)

THIRD QUARTER 2017

2

GUYANA GOLDFIELDS INC. Condensed Consolidated Interim Statements of Comprehensive Income (Unaudited - Expressed in thousands of U.S. Dollars)

Three months ended Nine months ended September 30 September 30 2017 2016 2017 2016 Revenues

Metal sales $ 50,207 $ 44,403 $ 138,063 $ 139,344

Cost of sales Production costs 23,195 16,615 66,925 57,066 Royalty 4,005 3,540 11,012 11,110 Depreciation 9,433 6,841 27,269 20,742

Earnings from mine operations 13,574 17,407 32,857 50,426 Corporate general and administrative expenses 1,375 1,907 5,177 4,676 Exploration and evaluation expenses 1,094 270 3,539 873 Stock-based compensation (Note 11) 1,183 384 2,951 1,126 Depreciation 48 69 131 218

Earnings before finance income and taxes 9,874 14,777 21,059 43,533 Net finance (income) expense (Note 12) (639) 2,835 3,155 8,450

Earnings before tax 10,513 11,942 17,904 35,083 Tax expense (Note 13) 4,364 3,021 4,923 11,503

Net earnings 6,149 8,921 12,981 23,580 Other Comprehensive Income

Unrealized (loss) gain on available-for-sale security, net (Note 5)

(5,117)

9,888

10,833

9,888

COMPREHENSIVE INCOME $ 1,032 $ 18,809 $ 23,814 $ 33,468

Net earnings per share Basic $ 0.04 $ 0.05 $ 0.08 $ 0.15 Diluted $ 0.04 $ 0.05 $ 0.07 $ 0.15 Weighted average number of shares outstanding Basic 173,036,629 166,305,804 172,500,614 157,812,115 Diluted 175,581,586 169,959,869 174,656,890 161,282,063

The accompanying notes are an integral part of these condensed consolidated interim financial statements.

THIRD QUARTER 2017

3

GUYANA GOLDFIELDS INC. Condensed Consolidated Interim Statements of Cash Flows (Unaudited - Expressed in thousands of U.S. Dollars)

Three months ended Nine months ended September 30 September 30

2017 2016 (restated)

2017 2016 (restated)

Cash provided by (used in) Operating cash flows Net income $ 6,149 $ 8,921 $ 12,981 $ 23,580

Items not involving cash: Depreciation 9,482 6,910 27,401 20,960 Deferred tax expense 4,364 3,000 4,293 11,377 Finance expense (note 12) (516) 2,536 4,026 7,597 Stock-based compensation 1,194 385 3,315 1,126

Change in operating working capital balances: Change in inventory (6,085) (4,405) (8,264) (8,429) Accounts receivable, prepaid expenses and other assets (1,364) (2,060) (2,852) (2,855) Accounts payable and accrued liabilities (452) 854 (5,047) 6,867

Total cash provided by Operations $ 12,772 $ 16,141 $ 36,483 $ 60,223 Financing cash flows

Repayment of loan facility (5,000) (7,720) (15,000) (20,010) Interest on loan facility (Note 12) (1,015) (2,339) (3,213) (7,219) Proceeds from exercise of stock options - 2,345 4,393 5,618 Proceeds from prospectus offering - 103,462 - 103,462 Cost of issuance for prospectus offering - (5,632) - (5,632)

Total cash (used) generated from Financing $ (6,015) $ 90,116 $ (13,820) $ 76,219 Investing cash flows

Expenditures on development - (3,522) - (24,829) Additions to mineral properties, plant and equipment (8,107) (7,619) (31,613) (17,017) Release of restricted cash, net - (38) - 3,962 Investment in available for sale security - (6,500) - (6,500)

Total cash used in Investing $ (8,107) $ (17,679) $ (31,613) $ (44,384)

Net change in cash and cash equivalents $ (1,350) $ 88,578 $ (8,950) $ 92,058 Effect of exchange rate on cash held in foreign currency 157 - (39) 233 Cash and cash equivalents, beginning of period 65,355 16,612 73,151 12,899

Cash and cash equivalents, end of period (Note 4) $ 64,162 $ 105,190 $ 64,162 $ 105,190

See note 17 for changes to comparative presentation.

The accompanying notes are an integral part of these consolidated financial statements.

THIRD QUARTER 2017

4

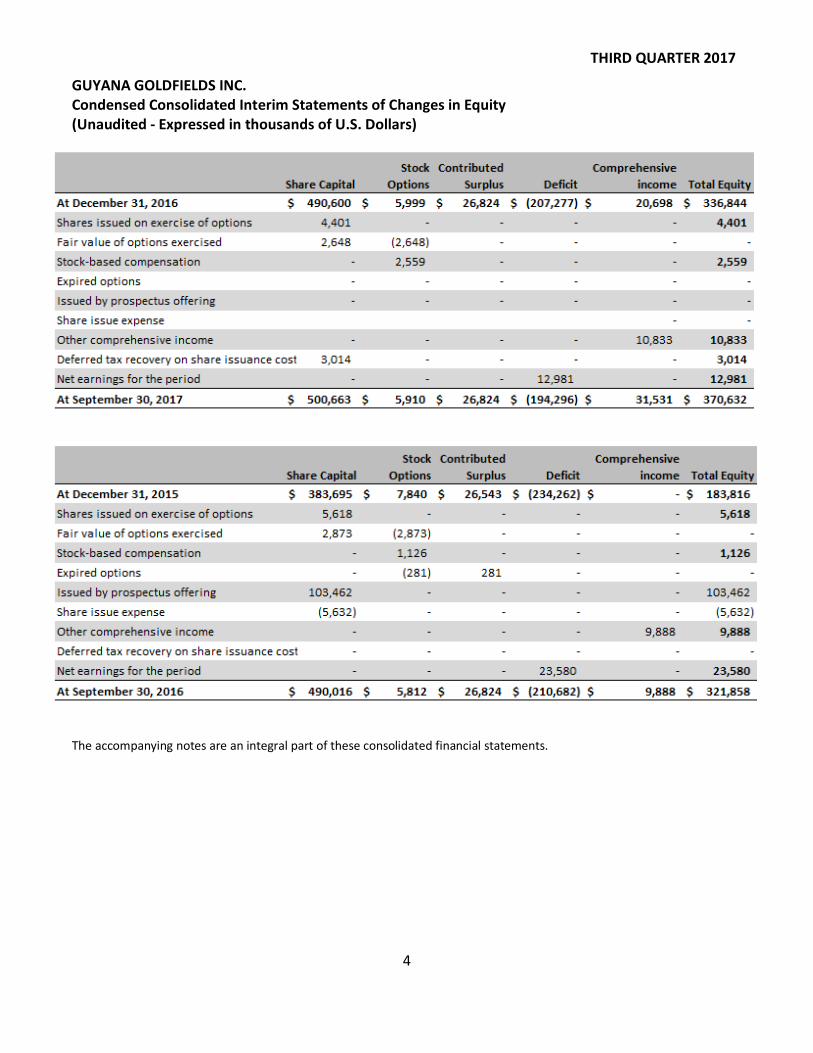

GUYANA GOLDFIELDS INC. Condensed Consolidated Interim Statements of Changes in Equity (Unaudited - Expressed in thousands of U.S. Dollars)

The accompanying notes are an integral part of these consolidated financial statements.

GUYANA GOLDFIELDS INC. THIRD QUARTER 2017 Notes to the Condensed Consolidated Interim Financial Statements For the three and nine months ended September 30, 2017 and 2016 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

5

NATURE OF OPERATIONS Guyana Goldfields Inc. (the "Company" or "Guyana Goldfields") is a company domiciled in Canada and was incorporated on December 12, 1994, under the Canadian Business Corporations Act. The Company shares are publicly traded on the Toronto Stock Exchange (TSX:GUY). The Company’s head office is registered at 141 Adelaide Street West, Suite 1608, Toronto, Ontario, Canada.

Guyana Goldfields Inc. and its wholly owned subsidiaries are engaged in the acquisition, exploration, development and operation of precious metal mineral properties, principally in Guyana, South America. The Company’s primary asset is its wholly owned Aurora Gold Mine, located in Guyana South America. On January 1, 2016 the Company declared commercial production of the Aurora Gold Mine.

BASIS OF PRESENTATION

(a) Statement of compliance

These unaudited condensed consolidated interim financial statements have been prepared in accordance with the International Financial Reporting Standards (“IFRS”), as applicable to the preparation of interim financial statements, including International Accounting Standard 34 (“Interim Financial Reporting”). The condensed consolidated interim financial information should be read in conjunction with the annual audited financial statements for the year ended December 31, 2016, which have been prepared in accordance with IFRS.

The preparation of consolidated financial statements requires management to make judgements, estimates and assumptions that affect the application of policies and reported amounts of assets, liabilities and expenses. See Note 4 for significant judgements, estimates and assumptions.

The condensed interim consolidated financial statements were authorized for issue by the Board of Directors on October 30, 2017.

(b) Functional and presentation currency of presentation

These consolidated financial statements are presented in United States dollars, which is the functional currency of the Company and all its subsidiaries. All financial information presented in United States dollars has been rounded to the nearest thousand. Some figures in these statements have been expressed in Canadian Dollars (Cdn$) for information purposes, and have been denoted as such.

(c) Use of estimates and judgements

The preparation of the financial statements requires management to make judgments, estimates and assumptions that affect the application of accounting policies and the reported amounts of assets, liabilities and contingent liabilities at the date of the financial statements and reported amounts of revenues and expenses during the reporting period. Estimates and assumptions are continually evaluated and are based on management's experience and other factors, including expectations of

GUYANA GOLDFIELDS INC. THIRD QUARTER 2017 Notes to the Condensed Consolidated Interim Financial Statements For the three and nine months ended September 30, 2017 and 2016 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

6

future events that are believed to be reasonable under the circumstances. However, actual outcomes can differ materially from these estimates.

The significant judgments made by management in applying the Company’s accounting policies and the key sources of estimation uncertainty were the same as those that applied to the consolidated financial statements as at and for the year ended December 31, 2016.

ACCOUNTING POLICIES The accounting policies followed in these unaudited condensed consolidated interim financial statements are the same as those applied in the Company’s audited consolidated financial statements for the year ended December 31, 2016.

(a) New Accounting Pronouncements not yet adopted

The following new standards, new interpretations and amendments to standards and interpretations have been issued but are not effective until financial years beginning on or after January 1, 2017 and have not been early adopted. Pronouncements that are not applicable to the company have been excluded from those described below.

IFRS 15 (Revenue Recognition) - The International Accounting Standards Board (“IASB”) has issued a new standard for the recognition of revenue, IFRS 15 – Revenue from Contracts. This standard will replace IAS 18 which covers contracts for goods and services and IAS 11 which covers construction contracts. The new standard is based on the principle that revenue is recognized when control of a good or service transfers to a customer, so the notion of control replaces the existing notion of risks and rewards. The standard permits a modified retrospective approach for the adoption. Under this approach, entities recognize transitional adjustments in retained earnings on the date of initial application (i.e. January 1, 2018), without restating the comparative period. Entities will only need to apply the new rules to contracts that are not completed as of the date of initial application. The standard is effective for annual reporting periods beginning on or after January 1, 2018. Early adoption is permitted. The Company has evaluated the standard and has concluded that the application of IFRS 15 will not have a material impact on its consolidated financial statements.

IFRS 9 (Financial Instruments) - IFRS 9 addresses the classification, measurement and de-recognition of financial assets and financial liabilities and introduces new rules for hedge accounting. In July 2014, the IASB made further changes to the classification and measurement rules and also introduced a new impairment model. These latest amendments now complete the new financial instruments standard. IFRS 7 (Financial Instruments: Disclosure) addresses the disclosure of financial assets and financial liabilities in the financial statements. IFRS 7 will be amended to require additional disclosures on transition from IAS 39 to IFRS 9, effective on adoption of IFRS 9. IFRS 9 is effective for annual periods beginning on or after January 1, 2018 with early adoption permitted. The Company has evaluated the standard and has concluded that the application of IFRS 9 will not have a material impact on its consolidated financial statements.

GUYANA GOLDFIELDS INC. THIRD QUARTER 2017 Notes to the Condensed Consolidated Interim Financial Statements For the three and nine months ended September 30, 2017 and 2016 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

7

IFRS 16 (Leases) - In January 2016, the IASB issued IFRS 16 – Leases which establishes the principles that an entity should use to determine the recognition, measurement, presentation and disclosure of leases for both parties to a contract: the customer (‘lessee’) and the supplier (‘lessor’). IFRS 16 replaces the previous leases Standard, IAS 17, Leases, and related Interpretations. IFRS 16 is effective from January 1, 2019 though a company can choose to apply IFRS 16 before that date but only in conjunction with IFRS 15 Revenue from Contracts with Customers. The Company is currently assessing the impact of this standard.

CASH AND CASH EQUIVALENTS At September 30, 2017, the Company held $64.1 million of cash (December 31, 2016 - $73.2 million) with approximately $58.1 million (December 31, 2016 - $56.8 million) denominated in United States dollars, with the remaining predominantly in Canadian dollars. Cash is deposited primarily in Canadian chartered banks and financial institutions.

AVAILABLE FOR SALE SECURITY During 2016 the Company purchased a combined 103.1 million shares of SolGold Plc (“SolGold”) for total consideration of $10 million pursuant to SolGold’s capital raises that closed on September 2, 2016 and October 17, 2016.

Fair market value of the shares at the date of these consolidated financial statements is $46.3 million, resulting in accumulated other comprehensive income of $31.5 million recorded in equity, which is presented net of tax.

Current period unrealized (loss)/gain presented through other compressive (loss) income breaks down as follows:

Three months ended Nine months ended September 30 September 30 2017 2016 2017 2016 Unrealized (loss) gain $ (5,899) $ 9,888 $ 15,649 $ 9,888 Tax asset (liability) (Note 13) 782 - (4,816) - Other comprehensive (loss) income $ (5,117) $ 9,888 $ 10,833 $ 9,888

GUYANA GOLDFIELDS INC. THIRD QUARTER 2017 Notes to the Condensed Consolidated Interim Financial Statements For the three and nine months ended September 30, 2017 and 2016 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

8

INVENTORIES

September 30, 2017 December 31, 2016 Ore stockpiled $ 2,421 $ 5,180 In-circuit 3,097 2,082 Finished goods 3,619 1,709 Materials and supplies 27,424 19,933 Total $ 36,561 $ 28,904

The amount of depreciation included in inventory at September 30, 2017 is $2.2 million (December 31, 2016 – $2.5 million).

MINERAL PROPERTIES, PLANT AND EQUIPMENT

GUYANA GOLDFIELDS INC. THIRD QUARTER 2017 Notes to the Condensed Consolidated Interim Financial Statements For the three and nine months ended September 30, 2017 and 2016 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

9

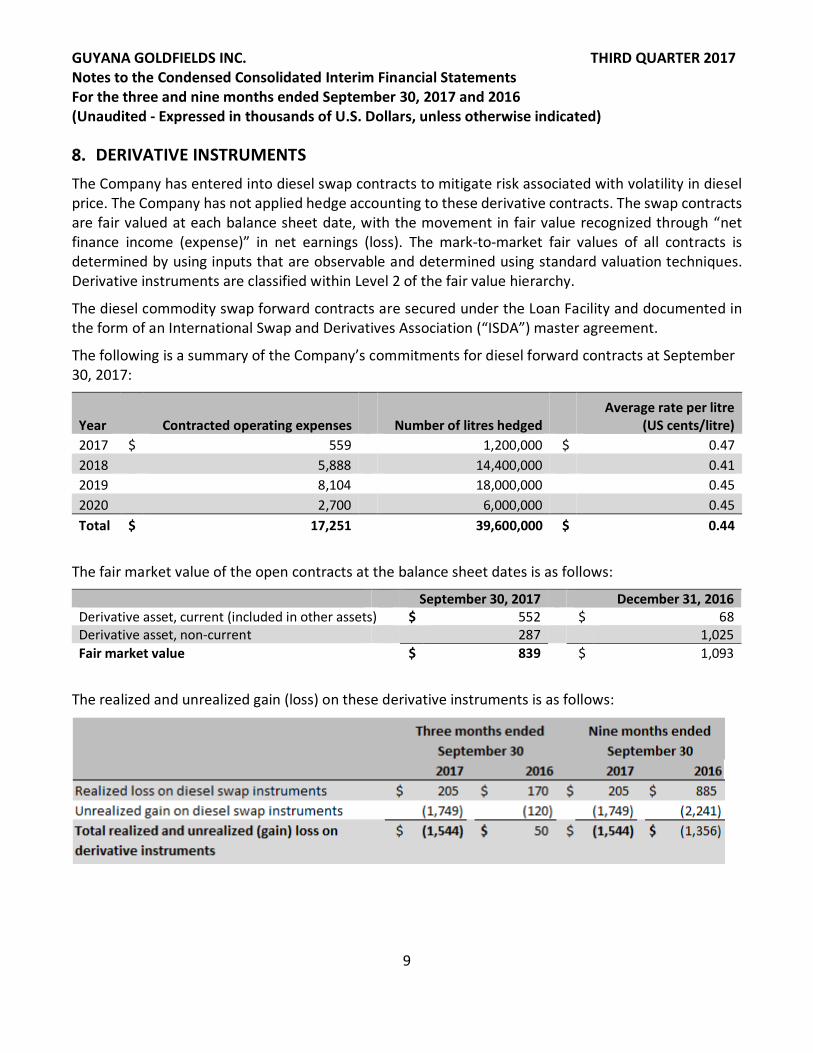

DERIVATIVE INSTRUMENTS The Company has entered into diesel swap contracts to mitigate risk associated with volatility in diesel price. The Company has not applied hedge accounting to these derivative contracts. The swap contracts are fair valued at each balance sheet date, with the movement in fair value recognized through “net finance income (expense)” in net earnings (loss). The mark-to-market fair values of all contracts is determined by using inputs that are observable and determined using standard valuation techniques. Derivative instruments are classified within Level 2 of the fair value hierarchy.

The diesel commodity swap forward contracts are secured under the Loan Facility and documented in the form of an International Swap and Derivatives Association (“ISDA”) master agreement.

The following is a summary of the Company’s commitments for diesel forward contracts at September 30, 2017:

Year Contracted operating expenses Number of litres hedged Average rate per litre

(US cents/litre) 2017 $ 559 1,200,000 $ 0.47 2018 5,888 14,400,000 0.41 2019 8,104 18,000,000 0.45 2020 2,700 6,000,000 0.45 Total $ 17,251 39,600,000 $ 0.44

The fair market value of the open contracts at the balance sheet dates is as follows:

September 30, 2017 December 31, 2016 Derivative asset, current (included in other assets) $ 552 $ 68 Derivative asset, non-current 287 1,025 Fair market value $ 839 $ 1,093

The realized and unrealized gain (loss) on these derivative instruments is as follows:

GUYANA GOLDFIELDS INC. THIRD QUARTER 2017 Notes to the Condensed Consolidated Interim Financial Statements For the three and nine months ended September 30, 2017 and 2016 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

10

DEBT FACILITY On December 23, 2016, the Company renegotiated the Debt Facility (“the Facility”) with its Senior Lenders, paying down the outstanding principal to $80 million. The new Facility is payable in sixteen quarterly principal repayments of $5 million each over a period of four years beginning March 31, 2017. Various covenants and restrictions were removed including the release of $23 million of restricted funds held by the Lenders in the Overrun Equity Account and the elimination of cash flow sweeps. The interest rate has been reduced to 3 month LIBOR average plus 3.5%. There will continue to be no gold hedging requirements or other similar provisions associated with the Facility.

Under the Common Terms Agreement, the Company has entered into security and debenture agreements pursuant to which the wholly owned subsidiary, AGM Inc, has granted and created a lien over all its assets and property of any kind to the benefits of the Senior Lenders. Similarly, the parent company Guyana Goldfields Inc. and certain of its wholly owned subsidiaries, namely Aurora Gold (Barbados) Inc., Guygold (Barbados) Inc., and Guy Gold Inc., (collectively the “Related Entities”) have entered into security agreements to grant and create liens over all their related rights, titles, and interests that are necessary for the Aurora mine, for the benefits of the Senior Lenders. In addition, certain of the Related Entities have entered into subordination agreements whereby any intercompany debt owed by these companies has been subordinated to the Facility.

The debt facility outstanding consists of the following as at:

Movement in Debt Facility Principal outstanding as at December 31, 2015 $ 155,600 Principal repayment during 2016 (75,600) Principal outstanding as at December 31, 2016 80,000 Principal repayment during the first nine months in 2017 (15,000) Unamortized deferred financing costs (1,078) Net debt position as at September 30, 2017 (net of deferred financing costs) 63,922 Less: Current portion, net of deferred financing costs 19,466 Non-current portion as at September 30, 2017 (net of deferred financing costs) 44,456

GUYANA GOLDFIELDS INC. THIRD QUARTER 2017 Notes to the Condensed Consolidated Interim Financial Statements For the three and nine months ended September 30, 2017 and 2016 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

11

SHARE CAPITAL The Company is authorized to issue an unlimited number of common shares. The issued and outstanding common shares consist of the following:

Number of Shares Amount At December 31, 2015 152,438,149 $ 383,695 Issued on exercise of options 4,285,324 5,989 Fair value of options exercised 0 3,086 Issued on Prospectus Offering (i) 14,330,000 103,462 Share issue expenses (ii) 0 (5,632) At December 31, 2016 171,053,473 $ 490,600 Issued on exercise of options 1,983,156 4,401 Fair value of options exercised - 2,648 Deferred tax recovery on share issuance costs (Note 12) - 3,014 At September 30, 2017 173,036,629 $ 500,663

(i) On July 19, 2016, the Company closed a bought deal offering (the “Prospectus Offering”) pursuant to which the Company issued 12,830,000 common shares (the “Common Shares”), at a price of Cdn$9.40 per Common Share for gross proceeds of $92.6 million (or approximately Cdn$120.6 million). The Common Shares were sold pursuant to an underwriting agreement with a syndicate of underwriters. On August 22, 2016, the Company closed the over-allotment option by the underwriters and issued an additional 1,500,000 common shares (the “Common Shares”), at a price of $9.40 per Common Share for gross proceeds of 10.9 million (or approximately Cdn$14.1 million).

(ii) Share issue expenses represent underwriters’ commission relating to the Offering, and legal and regulatory costs associated with both the above-mentioned Prospectus Offering.

GUYANA GOLDFIELDS INC. THIRD QUARTER 2017 Notes to the Condensed Consolidated Interim Financial Statements For the three and nine months ended September 30, 2017 and 2016 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

12

STOCK BASED COMPENSATION The following share based payments have been recognized in these statements of comprehensive income:

(a) Stock option plan

The stock option plan of the Company (the “Option Plan”) was approved by the shareholders on May 15, 2015, amended and restated as of February 4, 2016. The exercise price of stock options granted in accordance with the plan will be not less than the closing price of the common shares on the trading day immediately prior to the effective date of grant. All option exercises to be settled in the Company’s shares.

GUYANA GOLDFIELDS INC. THIRD QUARTER 2017 Notes to the Condensed Consolidated Interim Financial Statements For the three and nine months ended September 30, 2017 and 2016 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

13

The following table shows the continuity of stock options during the periods presented:

Number of Options Amortized

Value

Weighted Average

Exercise Price (Cdn$)

At December 31, 2015 9,787,500 $ 7,840 $ 2.40 Stock-based compensation – issued this period 3,281,000 167 5.20 Stock–based compensation – issued prior period - 1,359 - Exercised (4,285,324) (3,086) 1.83 Expired (200,000) (281) 3.95 Forfeited (231,669) - 2.65 At December 31, 2016 8,351,507 $ 5,999 $ 3.75 Stock-based compensation – issued this period 25,000 12 5.99 Stock–based compensation – issued prior period - 2,547 - Exercised (1,983,156) (2,648) 2.97 Expired - - - Forfeited (21,667) - 2.73 At September 30, 2017 6,371,684 $ 5,910 $ 4.02

The following are the stock options outstanding and stock options exercisable as at September 30, 2017:

(b) Restricted share unit (“RSU”) plan

In May 2015, the Company established a restricted share unit (“RSU”) plan, to provide Directors, Senior Officers and Key Employees of the Company in order to allow them to participate in the long-term success of the Company. Each RSU has the same value as on Guyana Goldfields common share. RSU’s issued to date have the following vesting schedule: one third on the first anniversary of the date of grant; one third on second anniversary of the date of grant; and one third on the third anniversary of the date of grant. On vesting, all share units are to be settled by cash of the Company.

The fair value of the RSU liability at September 30, 2017 was $0.5 million (December 31, 2016 – $0.1 million).

GUYANA GOLDFIELDS INC. THIRD QUARTER 2017 Notes to the Condensed Consolidated Interim Financial Statements For the three and nine months ended September 30, 2017 and 2016 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

14

(c) Deferred share unit (“DSU”) plan

On February 23, 2017 the Company approved the Deferred Share Unit Plan. The Plan was established to provide Directors of the Corporation with the opportunity to acquire Deferred Share Units in order to allow them to participate in the long-term success of the Corporation and to promote a greater alignment of interests between its Directors and shareholders. Each DSU has the same value as on Guyana Goldfields common share. DSU’s issued vest immediately.

The fair value of the DSU liability at September 30, 2017 was $0.4 million (December 31, 2016 - $nil).

NET FINANCE EXPENSE (INCOME)

INCOME TAXES On an interim basis, income tax expense is recognized based on Management’s estimate of the corporate annual income tax rate expected for the full year applied to the pre-tax income of the interim period. The following is the breakdown of income tax expense:

The deferred income tax benefit recognized during the current period relates to previously unrecognized deferred tax assets that have now been recognized as a result of the deferred tax on the available for sale investment through other comprehensive income. The unrealized gain on available for sale investment (see note 5) recognized through accumulated other comprehensive income has been shown net of the following estimated tax impact.

GUYANA GOLDFIELDS INC. THIRD QUARTER 2017 Notes to the Condensed Consolidated Interim Financial Statements For the three and nine months ended September 30, 2017 and 2016 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

15

COMMITMENTS AND CONTINGENCIES The Company is committed to $78.2 million for obligations under the debt facility, contractual commitments, purchases of equipment goods and services, and operating leases, summarized as follows:

Contractual obligations exist with respect to royalties; however, the amount cannot be estimated with certainty as is dependent on net revenues, which is a function of gold price and volume of ounces sold.

GUYANA GOLDFIELDS INC. THIRD QUARTER 2017 Notes to the Condensed Consolidated Interim Financial Statements For the three and nine months ended September 30, 2017 and 2016 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

16

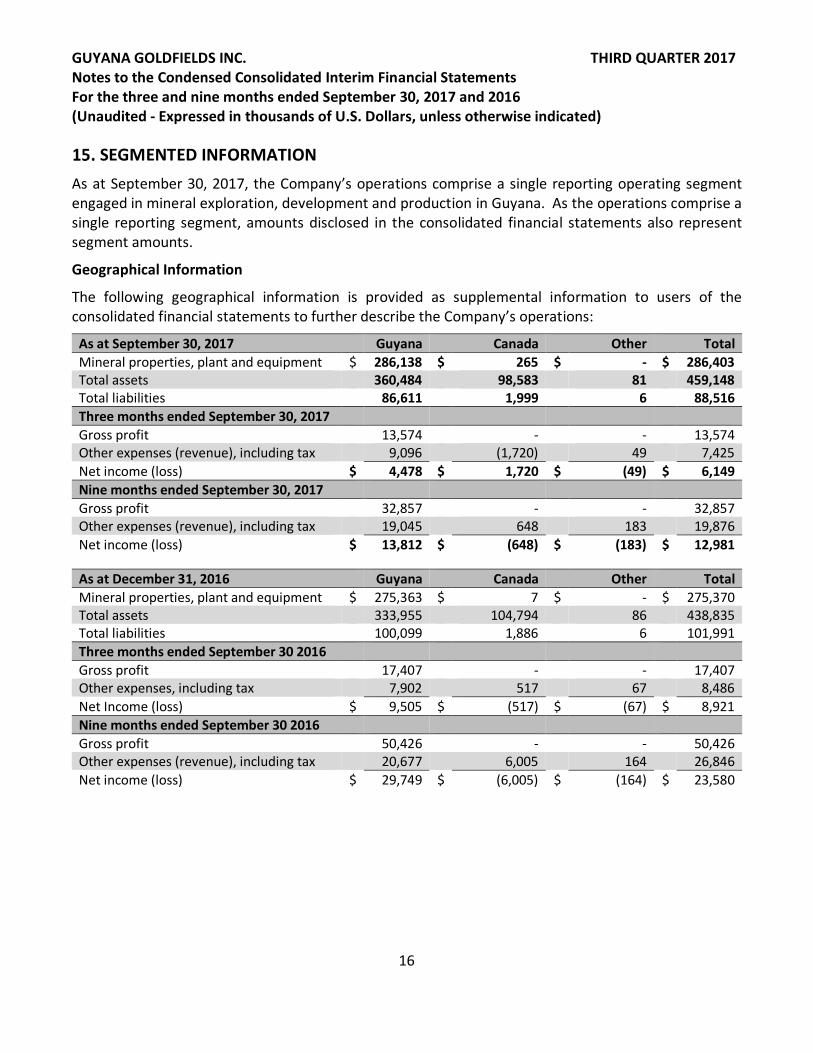

SEGMENTED INFORMATION As at September 30, 2017, the Company’s operations comprise a single reporting operating segment engaged in mineral exploration, development and production in Guyana. As the operations comprise a single reporting segment, amounts disclosed in the consolidated financial statements also represent segment amounts.

Geographical Information

The following geographical information is provided as supplemental information to users of the consolidated financial statements to further describe the Company’s operations:

As at September 30, 2017 Guyana Canada Other Total Mineral properties, plant and equipment $ 286,138 $ 265 $ - $ 286,403 Total assets 360,484 98,583 81 459,148 Total liabilities 86,611 1,999 6 88,516 Three months ended September 30, 2017 Gross profit 13,574 - - 13,574 Other expenses (revenue), including tax 9,096 (1,720) 49 7,425 Net income (loss) $ 4,478 $ 1,720 $ (49) $ 6,149 Nine months ended September 30, 2017 Gross profit 32,857 - - 32,857 Other expenses (revenue), including tax 19,045 648 183 19,876 Net income (loss) $ 13,812 $ (648) $ (183) $ 12,981

As at December 31, 2016 Guyana Canada Other Total Mineral properties, plant and equipment $ 275,363 $ 7 $ - $ 275,370 Total assets 333,955 104,794 86 438,835 Total liabilities 100,099 1,886 6 101,991 Three months ended September 30 2016 Gross profit 17,407 - - 17,407 Other expenses, including tax 7,902 517 67 8,486 Net Income (loss) $ 9,505 $ (517) $ (67) $ 8,921 Nine months ended September 30 2016 Gross profit 50,426 - - 50,426 Other expenses (revenue), including tax 20,677 6,005 164 26,846 Net income (loss) $ 29,749 $ (6,005) $ (164) $ 23,580

GUYANA GOLDFIELDS INC. THIRD QUARTER 2017 Notes to the Condensed Consolidated Interim Financial Statements For the three and nine months ended September 30, 2017 and 2016 (Unaudited - Expressed in thousands of U.S. Dollars, unless otherwise indicated)

17

RELATED PARTY TRANSACTIONS Remuneration of key management personnel of the Company was as follows:

Three months ended

September 30 Nine months ended

September 30 2017 2016 2017 2016

Compensation – salaries and related benefits $ 478 $ 486 $ 1,487 $ 1,404

Directors fees 92 67 243 194 Share-based compensation 633 210 2,073 622 Total $ 1,203 $ 763 $ 3,803 $ 2,220

Key management personnel are defined as the senior management team and members of the Board of Directors. All the above related party transactions are in the normal course of operations and are measured at the exchange amount, which is the amount of consideration established and agreed to by the related parties.

CHANGES TO COMPARATIVE PRESENTATION The condensed interim consolidated statement of cash flows for three and nine months ended September 30, 2016 reflects the retrospective application of a voluntary change in accounting policy adopted in 2017 to classify, in the consolidated statements of cash flows, interest paid as a financing activity, instead of within operating activities, as previously reported.

The change in accounting policy was adopted in accordance with IAS 7, Statement of Cash Flows, which provides a policy choice to classify interest paid as either an operating activity, or a financing activity. The Company considers the classification of these interest payments within financing activities to be the most useful to financial statement users and, consequently, that this presentation results in reliable and more relevant information.

The following table outlines the effect of this accounting policy change for the three and nine months ended September 30, 2017:

Three months ended September 30, 2016

Previously reported

Amount of restatement

Restated September 30, 2016

Cash used by operating activities $ 13,802 $ 2,339 $ 16,141 Cash used by financing activities $ 92,455 $ (2,339) $ 90,116

Nine months ended September 30, 2016

Previously reported

Amount of restatement

Restated September 30, 2016

Cash used by operating activities $ 53,004 $ 7,219 $ 60,223 Cash used by financing activities $ 83,438 $ (7,219) $ 76,219