growth in challenging times maximising customer value in wealth management

TRANSCRIPT

GROWTH IN CHALLENGING TIMES: MAXIMISING CUSTOMER VALUE IN

WEALTH MANAGEMENT

INSTRUCTIONS

The font size on the slide master

has been increased by 1pt, so

that text sizes are applied to the

standard two column layout in

the correct font size.

Go to the View menu and select

Header and Footer… to update

the Proposal title and Date.

SEYMOUR SLOAN IDEAS THAT MATTER

THE WEALTH MANAGEMENT MARKET

2

INSTRUCTIONS

The font size on the slide master

has been increased by 1pt, so

that text sizes are applied to the

standard two column layout in

the correct font size.

Go to the View menu and select

Header and Footer… to update

the Proposal title and Date.

SEYMOUR SLOAN IDEAS THAT MATTER

Profitable growth is on the agenda of most financial services providers, with Wealth Management the focus of increasing competition

3 CONFIDENTIAL

► Since the 2008 economic crisis, the richest 10% have recovered significantly faster than the rest of the economy. This has

increased the concentration of wealth into even fewer hands.

► In building a platform for growth, the large Wealth Managers are focused on acquiring and servicing a smaller number of

customers that hold an increasing share of the wealth.

► Those less able to compete focus on larger numbers of wealthy/affluent customers and varying their service model to optimise

returns.

► The market is in a state of transition as providers seek to define their strategy and approach to the markets.

► There are opportunities for successful operators to build a strong competitive proposition and acquire significant market share.

Future Prime

Customers – high

product holding, with a

hope that their worth

will increase.

Prime Customers –

should be retained at

all costs

Potentially Prime

Customers – focus is

on deepening the

relationship to

maximise wallet spend

Investible Assets

Low High Low

High

Pro

du

ct

Ho

ldin

gs

Current Competitive Landscape ► Currently, providers are focused on retaining and acquiring

„prime‟ customers in order to increase and secure their

Assets Under management

► In addition, they are protecting their high potential

customers, while seeking to deepen their relationship with

these customers

► With „future prime‟ customers cost effective service and

loyalty propositions are being developed to reward

customer loyalty.

► In addition, sophisticated CRM systems are coming online

that identify when a customer moves up the value chain,

allowing sales agents to intervene at an early stage.

In a growing market there are numerous opportunities for organisations dedicated to delivering true customer value.

The strongest competitors are already planning for tomorrow‟s success today.

INSTRUCTIONS

The font size on the slide master

has been increased by 1pt, so

that text sizes are applied to the

standard two column layout in

the correct font size.

Go to the View menu and select

Header and Footer… to update

the Proposal title and Date.

SEYMOUR SLOAN IDEAS THAT MATTER

Wealth Management – Trends and challenges

4

► The US remains the largest wealth market but India has the fastest growing HNWI population. Asia and Latin America

fuelling the overall increase in AUMs

► Expansion in emerging markets will shift to secondary centres of the region. Increasing economic activity in Indonesia is

creating opportunities in markets not previously considered.

► In The increase in Islamic wealth increases the focus on Islamic financing propositions. The same will be true within

other cultures.

► Changing demographics towards a younger wealthy population (often with high female representation) in emerging

markets has seen investment patterns change

► In Asia Pacific (excluding Japan) 41% of HNWI were 45 years or younger as compared to US where 68% population

was more than 55 years old

► The younger generation have a different investment attitude and is more likely to make riskier investments. They are

also more comfortable with digital channels and more likely to be active on social networking and internet based

platforms

Global Industry Trends

Source: Western European Wealth Markets Database, (Datamonitor)

► In 2010, the 1.5 million affluent individuals in Sweden

held $292bn or 77% of the total liquid assets. They also

accounted for 21% of the total adult population, roughly in

line with the Northern European average

► The value of liquid assets is forecast to increase to

$340bn by 2016 at a compound annual growth rate of

4.8%

► By 2016 the assets held by the mass affluent in Sweden

will over $225bn

► Building the propositions to secure the biggest share of

this asset pool as possible is the challenge for most

providers as customer attitudes and behaviours change

Swedish Trends

INSTRUCTIONS

The font size on the slide master

has been increased by 1pt, so

that text sizes are applied to the

standard two column layout in

the correct font size.

Go to the View menu and select

Header and Footer… to update

the Proposal title and Date.

SEYMOUR SLOAN IDEAS THAT MATTER

Wealth Management – Trends and challenges

5

Global Industry Trends

Source: Western European Wealth Markets Database, (Datamonitor)

► In 2010, the 1.5 million affluent individuals in Sweden

held $292bn or 77% of the total liquid assets. They also

accounted for 21% of the total adult population, roughly

in line with the Northern European average

► The value of liquid assets is forecast to increase to

$340bn by 2015 at a compound annual growth rate of

4.8%

► By 2015 the assets held by the mass affluent in Sweden

will over $225bn

► Building the propositions to secure as large as share of

this asset pool as possible will be the challenge for most

providers as customer attitudes and behaviours change

Swedish Trends

The US remains the largest wealth market but

India has the fastest growing HNWI population.

Asia and Latin America fuelling the overall

increase in AUMs Expansion in emerging markets will shift to

secondary centres of the region. Increasing

economic activity in Indonesia is creating

opportunities in markets not previously

considered.

In The increase in Islamic wealth increases the

focus on Islamic financing propositions. The

same will be true within other cultures.

Changing demographics towards a younger wealthy

population (often with high female representation) in

emerging markets has seen investment patterns

change

In Asia Pacific (excluding Japan) 41% of HNWI

were 45 years or younger as compared to US

where 68% population was more than 55 years

old

The younger generation have a different

investment attitude and is more likely to make

riskier investments. They are also more

comfortable with digital channels and more

likely to be active on social networking and

internet based platforms

INSTRUCTIONS

The font size on the slide master

has been increased by 1pt, so

that text sizes are applied to the

standard two column layout in

the correct font size.

Go to the View menu and select

Header and Footer… to update

the Proposal title and Date.

SEYMOUR SLOAN IDEAS THAT MATTER

6

Common Customer Trends across Financial Services

Seymour Sloan Research Findings Common Customer Trends Customer engagement with WEALTH MANAGEMENT (% of

respondents)

Expectations of customer experience are evolving in a time poor world - convenience and low effort are key

The winners will be those who transform their business to be more relevant, more joined up and more responsive to their customers

Customers demand meaningful and relevant interactions – mastering customer insights is critical

Customer's adoption of digital technologies is shifting control from organisations to customers

Customers are interacting across multiple channels more than ever and expecting integrated experiences

Customer relationships are becoming more complex, with customers becoming less loyal

Transforming customer capabilities drives sustainable growth

6

Are confident they are on track to financially achieve the retirement they would like¹

Have never seen a financial adviser / planner¹

Would ask a friend or colleague for a recommendation when looking for financial adviser²

Drop out of the advice process after the first meeting²

Prefer to receive super advice through a face-to-face meeting²

Of Generation Y are likely / very likely to use simple online advice services²

36% 65% 46% 50% 73% 86%

Financial Advisor

Relationship

Manager

Offered product

based solutions

Transactional Fee

based

Lifelong planning

advisor

Trusted Partner

Consolidated assets

and liabilities

Advisory fee-based

Then Now Today‟s firm focus

► Are we organised the right way to

grow our business and service our

clients?

► Do we have the right solutions for

our clients across different life

stages with the service models to

support them?

► Are we confident that we can satisfy

all our legal, compliance and

regulatory requirements?

► Do we have the right technical and

operational platforms in place to

provide a consistent and distinctive

client experience?

A key change has been the change in relationship between customer

and provider. The fundamental principles governing the relationship are

now based around trust and collaboration

INSTRUCTIONS

The font size on the slide master

has been increased by 1pt, so

that text sizes are applied to the

standard two column layout in

the correct font size.

Go to the View menu and select

Header and Footer… to update

the Proposal title and Date.

SEYMOUR SLOAN IDEAS THAT MATTER

7

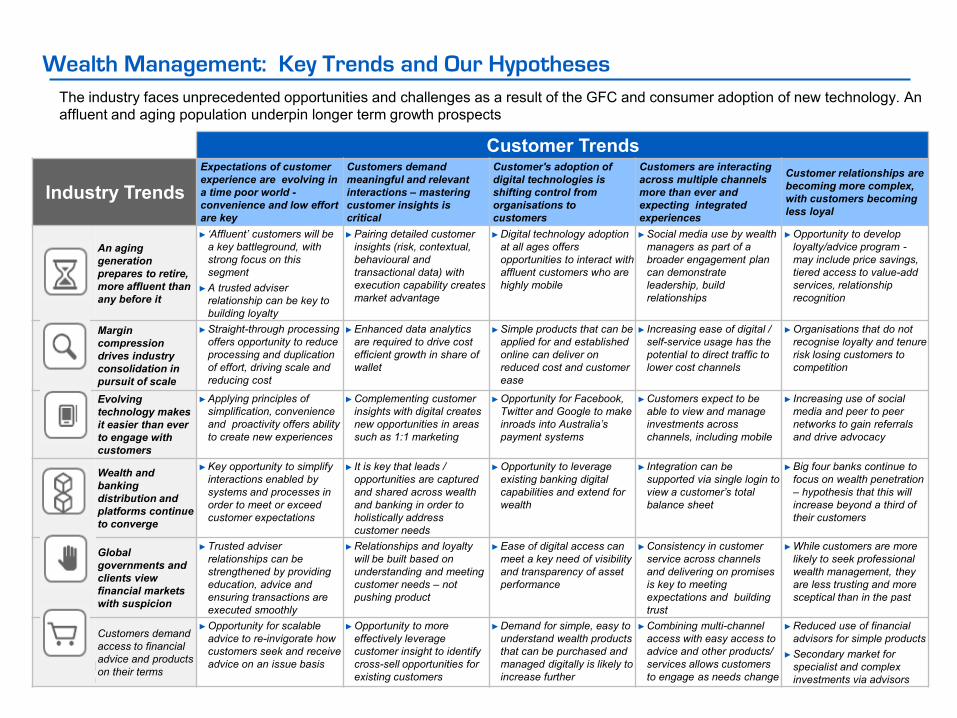

Customer Trends

Industry Trends

Expectations of customer

experience are evolving in

a time poor world -

convenience and low effort

are key

Customers demand

meaningful and relevant

interactions – mastering

customer insights is

critical

Customer's adoption of

digital technologies is

shifting control from

organisations to

customers

Customers are interacting

across multiple channels

more than ever and

expecting integrated

experiences

Customer relationships are

becoming more complex,

with customers becoming

less loyal

An aging

generation

prepares to retire,

more affluent than

any before it

► ‘Affluent’ customers will be

a key battleground, with

strong focus on this

segment

► A trusted adviser

relationship can be key to

building loyalty

► Pairing detailed customer

insights (risk, contextual,

behavioural and

transactional data) with

execution capability creates

market advantage

► Digital technology adoption

at all ages offers

opportunities to interact with

affluent customers who are

highly mobile

► Social media use by wealth

managers as part of a

broader engagement plan

can demonstrate

leadership, build

relationships

► Opportunity to develop

loyalty/advice program -

may include price savings,

tiered access to value-add

services, relationship

recognition

Margin

compression

drives industry

consolidation in

pursuit of scale

► Straight-through processing

offers opportunity to reduce

processing and duplication

of effort, driving scale and

reducing cost

► Enhanced data analytics

are required to drive cost

efficient growth in share of

wallet

► Simple products that can be

applied for and established

online can deliver on

reduced cost and customer

ease

► Increasing ease of digital /

self-service usage has the

potential to direct traffic to

lower cost channels

► Organisations that do not

recognise loyalty and tenure

risk losing customers to

competition

Evolving

technology makes

it easier than ever

to engage with

customers

► Applying principles of

simplification, convenience

and proactivity offers ability

to create new experiences

► Complementing customer

insights with digital creates

new opportunities in areas

such as 1:1 marketing

► Opportunity for Facebook,

Twitter and Google to make

inroads into Australia’s

payment systems

► Customers expect to be

able to view and manage

investments across

channels, including mobile

► Increasing use of social

media and peer to peer

networks to gain referrals

and drive advocacy

Wealth and

banking

distribution and

platforms continue

to converge

► Key opportunity to simplify

interactions enabled by

systems and processes in

order to meet or exceed

customer expectations

► It is key that leads /

opportunities are captured

and shared across wealth

and banking in order to

holistically address

customer needs

► Opportunity to leverage

existing banking digital

capabilities and extend for

wealth

► Integration can be

supported via single login to

view a customer’s total

balance sheet

► Big four banks continue to

focus on wealth penetration

– hypothesis that this will

increase beyond a third of

their customers

Global

governments and

clients view

financial markets

with suspicion

► Trusted adviser

relationships can be

strengthened by providing

education, advice and

ensuring transactions are

executed smoothly

► Relationships and loyalty

will be built based on

understanding and meeting

customer needs – not

pushing product

► Ease of digital access can

meet a key need of visibility

and transparency of asset

performance

► Consistency in customer

service across channels

and delivering on promises

is key to meeting

expectations and building

trust

► While customers are more

likely to seek professional

wealth management, they

are less trusting and more

sceptical than in the past

Customers demand

access to financial

advice and products

on their terms

► Opportunity for scalable

advice to re-invigorate how

customers seek and receive

advice on an issue basis

► Opportunity to more

effectively leverage

customer insight to identify

cross-sell opportunities for

existing customers

► Demand for simple, easy to

understand wealth products

that can be purchased and

managed digitally is likely to

increase further

► Combining multi-channel

access with easy access to

advice and other products/

services allows customers

to engage as needs change

► Reduced use of financial

advisors for simple products

► Secondary market for

specialist and complex

investments via advisors

Wealth Management: Key Trends and Our Hypotheses

The industry faces unprecedented opportunities and challenges as a result of the GFC and consumer adoption of new technology. An

affluent and aging population underpin longer term growth prospects

INSTRUCTIONS

The font size on the slide master

has been increased by 1pt, so

that text sizes are applied to the

standard two column layout in

the correct font size.

Go to the View menu and select

Header and Footer… to update

the Proposal title and Date.

SEYMOUR SLOAN IDEAS THAT MATTER

Key regulatory changes that have shaped the market

Dodd Frank Act, FATCA

Facets such as registration of

investment advisors with SEC,

introduction of fiduciary standards

(which are conflicting with DOL’s

standard) and reporting of financial

assets outside the US will

substantially increases compliance

requirements and costs

Singapore: Private Banker

Code of Conduct

The code focuses on areas

such as ethics and client

relationship management,

which is expected to push

up compliance costs

Hong Kong: New Rules for

Wealth Management

The new rules, which

include registration of

structured products with the

Securities and Futures

Commission and about

defining a private client.

These would result in an

increase in compliance

costs

China: New Rules for Wealth

Management

The new rules will significantly

restrict the ability of banks to

provide wealth management

services and force them to

focus on alternative ways to

attract customers

UK RDR

Implementation of RDR will

have a significant impact on

the training costs and

overall higher staff pay for

wealth managers, and

improving cost transparency

may result in clients

becoming extremely price

sensitive

INSTRUCTIONS

The font size on the slide master

has been increased by 1pt, so

that text sizes are applied to the

standard two column layout in

the correct font size.

Go to the View menu and select

Header and Footer… to update

the Proposal title and Date.

SEYMOUR SLOAN IDEAS THAT MATTER

Key regulatory changes that have shaped the market

• Fiduciary Duty: The regulation provides SEC the authority to impose a fiduciary duty on brokers who give investment advice --the

advice must be in the best interest of their customers.

• Registration of investment advisors: Due to the regulation, the thresholds for determining whether an adviser is to register under

federal or state law will change and may force most of the investment advisors to register with the either state regulators or the SEC.

• Change in charging mode: Advisers generally may only charge performance-based fees (i.e. fees based on investment success rather

than the usual percentage-of-managed-assets fees) to “qualified clients.”

• Significant increase in recordkeeping and bookkeeping activities: Dodd-Frank requires sponsors of private funds to maintain

voluminous records for the funds, available for SEC examination and to the new Financial Stability Oversight Council, as well as to

investors

• Consumer Protection with Authority and Independence: A new independent supervisor, housed at the Federal Reserve, with the

authority to ensure accurate information is presented.

• Foreign Account Tax Compliance Act (FATCA) was enacted to combat tax evasion by US persons holding investments in offshore

accounts.

• Under FATCA, US taxpayers holding financial assets outside the US will report those assets to the IRS. In addition, FATCA will require

foreign financial institutions to report directly to the IRS certain information about financial accounts held by US taxpayers, or by foreign

entities in which US taxpayers hold a substantial ownership interest.

US: Dodd Frank Act

US: FATCA

INSTRUCTIONS

The font size on the slide master

has been increased by 1pt, so

that text sizes are applied to the

standard two column layout in

the correct font size.

Go to the View menu and select

Header and Footer… to update

the Proposal title and Date.

SEYMOUR SLOAN IDEAS THAT MATTER

Key regulatory changes that have shaped the market

The Retail Distribution Review (RDR) will become affective from 1 January 2013 for all retail investment products and to the companies

that produce or distribute these products and services, such as banks, product providers, Independent Financial Advisers and wealth

managers.

RDR is based on the following three key goals:

Clear services description: Companies will need to describe their services as either “Independent advice” or “Restricted

advice”

Transparent industry charges: Under RDR, all payments are supposed to be made through „adviser charges,‟ and directly reflect

the services being provided to clients.

Greater adviser professionalism: Enhanced professional standards and accountability of individual investment advisers.

Advisers will have to possess a Qualifications and Credit Framework (QCF) Level 4 qualification.

Singapore's Private Banking Advisory Group introduced the code of conduct for private banking industry in 2011 and the Code is based on

the following two main pillars:

1. Competency: Highlights the key relevant competencies required for a financial advisor

2. Market Conduct: Market conduct standards to ensure professionalism, client due diligence, appropriate advisory standards and

resolution of client complaints.

UK RDR

Singapore: Private Banker Code of Conduct

INSTRUCTIONS

The font size on the slide master

has been increased by 1pt, so

that text sizes are applied to the

standard two column layout in

the correct font size.

Go to the View menu and select

Header and Footer… to update

the Proposal title and Date.

SEYMOUR SLOAN IDEAS THAT MATTER

Key regulatory changes that have shaped the market

• The new rules were effective from 1 January 2012. Following are the highlights of the rules:

• Banks cannot use wealth products to attract deposits or bundle products in other promotions Banks cannot lure deposits by raising

interest rates in "disguised" forms.

• Promotions cannot be aired on television and they must be fair and open, and explain potential risks

• Sales tactics such as price discounts and free gifts have been discouraged

• Banks cannot promise investment returns or vow to undertake losses when selling products

China: New Rules for Wealth Management

Under the new rules, If a structured product is offered to Hong Kong‟s retail public, it must be approved by the Securities and Futures

Commission (SFC), although exemptions exist for offers to professional investors.

However, the definition of professional investors has become more confusing as a clear distinction between retail and private investors is

now even harder to make.

High-net-worth investors will face tougher accreditation standards under the revised code. These standards include demonstrating

knowledge, expertise and awareness of the risks involved in “relevant products and markets”, as well as a separate written assessment for

each product type and market. That assessment must be repeated where an investor has ceased to trade in that product or market for

more than two years.

Hong Kong: New Rules for Wealth Management

INSTRUCTIONS

The font size on the slide master

has been increased by 1pt, so

that text sizes are applied to the

standard two column layout in

the correct font size.

Go to the View menu and select

Header and Footer… to update

the Proposal title and Date.

SEYMOUR SLOAN IDEAS THAT MATTER

HOW THE MARKET IS RESPONDING

12

INSTRUCTIONS

The font size on the slide master

has been increased by 1pt, so

that text sizes are applied to the

standard two column layout in

the correct font size.

Go to the View menu and select

Header and Footer… to update

the Proposal title and Date.

SEYMOUR SLOAN IDEAS THAT MATTER CONFIDENTIAL 13

The current market has forced most providers to assess their strengths in the market and as such a range of strategic options are available

Strategic

Option

Description Used By

Organic

Growth

• Increase in customer numbers in core markets

• Increase in Assets under Management per customer

• Increase in average product holdings, per customer

• Migration of high value customers to high profit propositions

Growth by

Acquisition

• Acquisition of books of small private banks, wealth managers

and IFAs

• Acquisition of specialist teams an bankers from existing

leading players

Focus on

International

Expansion

• Acquisition of foreign operations in high growth/value markets

• Establishment of booking offices in profitable markets to

service customers

Rationalisation

of existing

operations

• Investment in IT systems to improve automations and reduce

errors

• Creation of CRM system that provides a single view of the

customer and improves prospect selection

• Investment in mobile and internet technology to improve

customer access and contact

International

Footprint

Optimisation

• Align locations to strategic strengths

• Exit unprofitable markets

• Consolidate functions under a Shared Service Centre

All strategic solutions will incorporate a number of different elements reflecting the challenging market that exists. However, all providers will define

their strategy based on the answer to three key questions:

• What are our strengths and competitive advantages (areas for growth)?

• Where are our competitive strengths and where are we competing unfavourably (exit unprofitable markets)

• How can we reduce operating costs and make the business more agile and responsive to customer need.

INSTRUCTIONS

The font size on the slide master

has been increased by 1pt, so

that text sizes are applied to the

standard two column layout in

the correct font size.

Go to the View menu and select

Header and Footer… to update

the Proposal title and Date.

SEYMOUR SLOAN IDEAS THAT MATTER CONFIDENTIAL 14

A view on how some of the leading players are adapting to the new market 1/2

► Barclays initiated a five year, GBP 350 million investment program to position Barclays

Wealth as a top tier player in the business. Barclays plans to spend 40% of the investment

spend on client facing talent while the remaining on upgrading its technological and physical

infrastructure.

► The bank has clearly defined its target customer segment as clients with investable assets of

more than GBP 5 million and not to compete in retail brokerage or mass affluent

segmentsThe main system change is the migration of all customers to a single platform,

using consistent data, to enhance the CRM platform – giving staff a comprehensive view of

each customer

► Barclays has identified three key market segments for focusing its expansion plans – US, UK

and Global high net worth segment. The Bank aims to service these client segments on a

global basis out of three hubs in London, Geneva and Singapore.

► Barclays Wealth‟s two-thirds of infrastructure costs and one-third of people are already

shared with the Corporate and Investment Bank. This will not only help the bank to improve

productivity and contain costs but also enable them to offer a wide range of services to their

clients because of the reach within different business segmentsProduct propositions were

developed to encourage cross-selling, including discounts for multiple product holdings. In

addition, a loyalty scheme was developed to reward customers with significant relationships

with the bank.

► Bank of America uses different brands to offer services to different customer segments. The

company uses its „Merrill Edge self-directed Investing‟ platform for the retail segment, „Merrill

Edge Advisory Center‟ for the potential mass affluent segment, „Merrill Lynch Wealth

Management‟ for the mass affluent and affluent segments, and „BoA Private Banking and

Investment Group‟ and „U.S. Trust‟ for Global and American HNWI and UHNWIs respectively

► Bank of America disposed off First Republic, an ancillary private bank it acquired as a part of

Merrill Lynch. The bank also disposed off the long term asset management business of

Columbia Asset Management in 2009. Since its acquisition of Merrill Lynch, Bank of America

was been busy integrating and realizing synergies from multiple businesses it already owned

and those it acquired from Merrill Lynch

► In 2010, Bank of America stepped up its marketing effort and launched different advertising

campaigns for its Merrill Lynch Wealth Management as well as for U.S. Trust brands

INSTRUCTIONS

The font size on the slide master

has been increased by 1pt, so

that text sizes are applied to the

standard two column layout in

the correct font size.

Go to the View menu and select

Header and Footer… to update

the Proposal title and Date.

SEYMOUR SLOAN IDEAS THAT MATTER CONFIDENTIAL 15

A view on how some of the leading players are adapting to the new market 2/2

► Although the engine of growth in the industry has shifted to emerging markets in Asia and

elsewhere, developed markets retain their importance given their large wealth pool. Credit

Suisse has identified entrepreneurial segment and generation transfer of wealth as market

segments where opportunities for growth remain over the next few years

► Regulators have increased their oversight on the financial sector and offshore wealth

management grabbed headlines over the last two years. Credit Suisse recognizes these

challenges are in shifting to a business model that is more driven by providing on-shore

services

► Credit Suisse is already one of biggest players in the wealth management space in US and

Europe. The bank is, therefore, focusing its expansion efforts in Middle East and Asia. Credit

Suisse extended its coverage in smaller national markets like Bahrain in the Middle East,

upgraded its presence in India to a full service branch and opened a family office in

Singapore

► Driven by the increasing regulatory challenges post the financial crises and an increased

oversight on offshore wealth management business models, UBS focused on improving its

onshore business capabilities in 2010. UBS focused on building onshore capabilities across

key geographies, like Europe, and across all customer segments

► Although UBS is already one of the top players in the segment, the bank aims to increase its

market share further by growing at double the pace compared to the market. The customer

segment remains one of the most profitable client segments. UBS set up a new Global

Family Office group as a partnership between its UHNWI unit and the investment bank to

provide a wide range of services to this specialized group

► UBS has created a new Investment Products and Services unit in Switzerland which

combines expertise from wealth management, retail and corporate bank, investment bank

and the global asset management division. The team delivers high quality investment

content and channels market and product ideas to client advisors as well as clients

► UBS focused its expansion plans in key growth markets in Asia (Hong Kong and Singapore)

and the emerging markets (Middle East, Latin America and the CEE)

INSTRUCTIONS

The font size on the slide master

has been increased by 1pt, so

that text sizes are applied to the

standard two column layout in

the correct font size.

Go to the View menu and select

Header and Footer… to update

the Proposal title and Date.

SEYMOUR SLOAN IDEAS THAT MATTER

BUILDING A WINNING FORMULA

16

INSTRUCTIONS

The font size on the slide master

has been increased by 1pt, so

that text sizes are applied to the

standard two column layout in

the correct font size.

Go to the View menu and select

Header and Footer… to update

the Proposal title and Date.

SEYMOUR SLOAN IDEAS THAT MATTER CONFIDENTIAL 17

Successful providers are strong across 4 key areas while those that struggle have difficulty reaching excellence in these areas

► Segmentation - segmentation aligned to strategic

goals. Effective of matching customers to service

channels based on cost/revenue analysis

► CRM - capability to proactively identify new sales

prospects as well as providing a 360 degree view on the

customer. Ability to migrate customers up and down the

value chain as their circumstances change.

► Proposition - Strong internal products and capabilities

to provide effective investment and portfolio solutions.

Value added options to reward loyalty. Flexible products

to match differing customer need.

► Service and Distribution- Multi-channel servicing

capability to reflect the plurality to customer touch-

points. A front-end sales and service portal that is

integrated into the product platform and to all middle

and back office interfaces. A low ratio of Relationship

Managers to customers to increase contact time

Successful Wealth Managers succeed across the

following areas

► Segmentation – poor segmentation with no overall

strategic goal. Segmentation parameters are ineffective,

selecting low profit customers.

► CRM – fails to provide a singular view of the customer

relationship. System merely provides customer

information without highlighting products to sell. Unable

to identify future HNW customers.

► Proposition – design fails to assess internal delivery

capabilities. Ineffective cost to serve analysis. No added

value in proposition. Ineffective sales force scale and

expertise. Proposition fails to satisfy customer need.

► Service and Distribution– cost to serve is too high for

many customers. Focus is on branch service only. Lack

of integration between RM service and CRM systems.

High value customers have little contact time with RM

due to poor segmentation and proposition build. Service

channels not staffed with suitably qualified staff at the

right scale.

Unsuccessful Wealth Managers struggle wit the

following areas

There are other areas where excellence is part of strong performance. These include:

► Risk Management

► Regulatory Compliance

► Skills, Professional Development and Culture

► Operational Efficiency and

► Reward and Remuneration

INSTRUCTIONS

The font size on the slide master

has been increased by 1pt, so

that text sizes are applied to the

standard two column layout in

the correct font size.

Go to the View menu and select

Header and Footer… to update

the Proposal title and Date.

SEYMOUR SLOAN IDEAS THAT MATTER

Overall success will be driven by succeeding in four key areas and

building initiatives to improve each area

1. Grow & Retain

Client Assets

2. Efficient

Distribution and

Servicing

4. Build a Scalable

Foundation

Business

Strategy

Segmentation

and CRM

Initiatives

Distribution

and Servicing

Initiatives

Product &

Advice

Initiatives

A

B

C

Infrastructure

Initiatives

Cross-Org

Initiatives D

E

3. Enhance the Offer

& Experience

Focus Area Category Key Initiatives

A5. Build and test of CRM

System

A1. Design and Develop

Segmentation Model

A2. Apply Segmentation to

Existing Customers

(Insight)

A3. Identify New

Customers to Target

A4. Design of CRM system

B1. Deliver Competitive

Online & Mobile Capabilities

B3. Client Acquisition

Through Engagement

Programs

B2. Deliver Competitive

Call Center Capabilities

D1. Develop Enhanced Risk

and Compliance Frameworks

D2. Launch Targeted

Marketing / CE&A

E1. Develop Effective Staff

Incentive and Remuneration

Schemes

E2. Enhanced

Relationship Management

Training

C1. Develop Product to

Appeal to Target Segments

C2. Develop Product

Relationships to Cross-Sell

C3. Build Younger

Generation Solutions

C4. Develop Advice

Proposition

C5. Develop Self selection

features

D3. Develop Tax

Reporting Solution

D4. Drive Organisational

Efficiency and Productivity to

Fund Growth

A6. Implementation of

CRM System

C6. Develop Self-Guided

Investment platform

D5. Product and Servicing

Simplification

INSTRUCTIONS

The font size on the slide master

has been increased by 1pt, so

that text sizes are applied to the

standard two column layout in

the correct font size.

Go to the View menu and select

Header and Footer… to update

the Proposal title and Date.

SEYMOUR SLOAN IDEAS THAT MATTER

DEVELOPING EFFECTIVE SEGMENTATION

19

INSTRUCTIONS

The font size on the slide master

has been increased by 1pt, so

that text sizes are applied to the

standard two column layout in

the correct font size.

Go to the View menu and select

Header and Footer… to update

the Proposal title and Date.

SEYMOUR SLOAN IDEAS THAT MATTER

Customer Insight – Current Challenges

20

As financial institutions have come to realize,

unprofitable customers can be classified into

the following three groups:

► Unprofitable due to lack of profitable

relationships

► Unprofitable due to improper charging or

inappropriate servicing channels

► Truly unprofitable

To avoid the unprofitable pitfalls, financial

institutions must implement processes and tools

that enable them to capture higher wallet share,

migrate customers to more cost effective

channels, and properly identify customers to be

de-marketed or divested.

► provider face the challenge of understanding their current and future customers. They need to understand the existing

relationship and convert it into additional sales and the likely cost to serve for existing customers..

► In addition, most provider require a tool that provides staff with a real-time snapshot of al customer relationships in order to

make relationship management and cross-selling easier.

► To achieve this, providers must invest in market leading segmentation techniques and CRM systems.

For successful and profitable relationships, financial institutions must

understand their customers, anticipate their needs and requirements, and

drive sales. To accomplish these objectives, institutions must be able to

answer the following, all-important questions:

► Who are my best customers?

► What products and services do they require?

► How do their product needs vary across regions and branch trade areas?

► How can I package products, based on these needs, to maximize value

and corresponding fee revenue?

► How can I cultivate a better relationship through communication?

These questions represent the fundamental challenges faced by every

financial institution looking to successfully implement a customer profitability

and segmentation process.

With clean, accurate data, financial institutions can now begin to get a 360° view of their customers. A detailed, chronological

roadmap that focuses on predictive analytic models will help financial institutions:

► • Optimize distribution networks

► • Define untapped opportunities and maximize branch

► performance through a better sales goal-setting process

► • Analyze and visualize market opportunities for sales

► planning activities

► • Identify the next best purchase and profitability for

► individual customers or new prospects

INSTRUCTIONS

The font size on the slide master

has been increased by 1pt, so

that text sizes are applied to the

standard two column layout in

the correct font size.

Go to the View menu and select

Header and Footer… to update

the Proposal title and Date.

SEYMOUR SLOAN IDEAS THAT MATTER

Seymour Sloan has developed a six-step methodology to developing customer segmentation

Segmentation Methodology

► Collect and assess existing information (internal transaction data, external research, etc.)

► Hypothesize segmentation criteria

► Identify additional data sources based on hypotheses

► Collect primary data (surveys, interviews, etc..)

► Perform data mining and statistical analysis

► Test/ modify segment criteria and differentiation factors

► Classify customers into segments based on defined attributes

► Test that segments are mutually exclusive, collectively exhaustive and meet viability criteria through iterations and testing

► Develop diagnostics information to flesh out segments

► Re-evaluate defined segments

► Perform comparative analysis to identify most valuable segments

► Assess the company‟s ability to attract various segments

► Prioritize segments based on analyses

► Develop segment-specific treatment offerings and tactics

► Prioritize initiatives based on segment prioritization and cost/benefit assessments

► Communicate findings

► Confirm immediate and long-term business objectives

► Understand the role segmentation will play in support of the objectives

► Determine timelines and resource requirements to conduct the segmentation exercise

► Migrate scoring model and segment codes to customer information system

► Design and implement segment-specific treatment offerings and tactics

► Define and manage channel delivery

1 2 3 4 5 6

Define Business Objectives

Identify / Build Data Set

Create Segments

Profile Segments

Create Treatments

Operationalize Segmentation

The Seymour Sloan segmentation approach is a powerful means to identify unmet customer needs. We help identify underserved

segments and develop appealing products and services.

The six-step process will develop an in-depth view of your customer base from which, you can develop a strategic approach for

maximising your market opportunity.

INSTRUCTIONS

The font size on the slide master

has been increased by 1pt, so

that text sizes are applied to the

standard two column layout in

the correct font size.

Go to the View menu and select

Header and Footer… to update

the Proposal title and Date.

SEYMOUR SLOAN IDEAS THAT MATTER

The segmentation design is critical to the usability of the output Successful segmentation lies in effective design. Our approach has been developed over a number of successful engagements

and is designed to give you meaningful insight into the customers to focus on. Our multi-dimensional approach helps unlock real

customer value.

1. Analyze the

competitive

situation

3. Identify and

use strong

variables

2. Understand

your customer

across three

dimensions

4. Apply the

right analytical

approaches

Identify

Customer

Segments

Data

Collection

Define

Segmentation

Scope &

Objective

Analyze the competitive situation

Competitors Customers Capabilities

1

Strength of relationshipNeeds & Behavior

Value

Understand your customers across three dimensions 2

► Value/lifetime value

► Needs and behavior

► Strength of relationship

Identify and use strong variables, which are: 3

► Correlated to behavior (current and

future)

► Stable over time

► Related directly to customers

Apply the right analytical approaches 4

Data Collection

and

Manipulation

Segment

Generation

Basic Advanced

Basic Advanced

Data Mining Tab Analysis

Brainstorming Cluster Analysis

Characteristics(e.g. lifestage,

demographics)

Attitudes(e.g. desire for

convenience, control,

approach to running

business)

Product needs(e.g. product, price)

Brand / service

needs(e.g. channel,

information)

Buying & usage

behavior(What, why, how, how

much, tenure)

Value(Current, potential &

future)

Current & potential customers

INSTRUCTIONS

The font size on the slide master

has been increased by 1pt, so

that text sizes are applied to the

standard two column layout in

the correct font size.

Go to the View menu and select

Header and Footer… to update

the Proposal title and Date.

SEYMOUR SLOAN IDEAS THAT MATTER 23

Understand what a profitable

customer looks like first…

…and use this insight to identify new

high potential customers

Segment existing customer first

Quantify the actual and potential value of existing

customers

Prioritize the customer segments and develop

approaches to optimize value

Understand which needs are currently being met and

where new opportunities exist

Identify potential customer

Align customer segments and offerings to the

organization

Use your customer insight to understand the

characteristics that constitute a profitable customer

Create the customer offering to target the new

customer segment

Identify where new high potential customers segments

exist and how they can be reached

Assess attractiveness of the segment

Getting the segmentation right:

…make the most of what you have first then grow through the external market

Organizations should start by optimizing the value of their existing customer

relationships first and then use this insight to develop profitable relationships with

new customers

► I want a phone to use

in emergencies

► It must be simple to

use and operate

► I like managing my

account “in-store”

► I want a phone to use

in emergencies

► It must be simple to

use and operate

► I like managing my

account “in-store”

► I want a phone to

use in emergencies

► It must be simple to

use and operate

► I like managing my

account “in-store”

► I want a phone to use

in emergencies

► It must be simple to

use and operate

► I like managing my

account “in-store”

► I want a phone to use

in emergencies

► It must be simple to

use and operate

► I like managing my

account “in-store”

► I want a phone to

use in emergencies

► It must be simple to

use and operate

► I like managing my

account “in-store”

► I want a phone to use

in emergencies

► It must be simple to

use and operate

► I like managing my

account “in-store”

► I want a phone to use

in emergencies

► It must be simple to

use and operate

► I like managing my

account “in-store”

► I want a phone to

use in emergencies

► It must be simple to

use and operate

► I like managing my

account “in-store”

► I want a phone to use

in emergencies

► It must be simple to

use and operate

► I like managing my

account “in-store”

► I want a phone to use

in emergencies

► It must be simple to

use and operate

► I like managing my

account “in-store”

► I want a phone to

use in emergencies

► It must be simple to

use and operate

► I like managing my

account “in-store”

► I want a phone to use

in emergencies

► It must be simple to

use and operate

► I like managing my

account “in-store”

► I want a phone to use

in emergencies

► It must be simple to

use and operate

► I like managing my

account “in-store”

► I want a phone to

use in emergencies

► It must be simple to

use and operate

► I like managing my

account “in-store”

► I want a phone to use

in emergencies

► It must be simple to

use and operate

► I like managing my

account “in-store”

► I want a phone to use

in emergencies

► It must be simple to

use and operate

► I like managing my

account “in-store”

► I want a phone to

use in emergencies

► It must be simple to

use and operate

► I like managing my

account “in-store”

INSTRUCTIONS

The font size on the slide master

has been increased by 1pt, so

that text sizes are applied to the

standard two column layout in

the correct font size.

Go to the View menu and select

Header and Footer… to update

the Proposal title and Date.

SEYMOUR SLOAN IDEAS THAT MATTER

TALK

TO US CONTACT:

Terry Chapendama - Director

Read our blog at:

www.seymourthinks.wordpress.com

Follow us on twitter

@seymoursloanuk

Visit us online www.seymoursloan.com

ABOUT Seymour Sloan

We formed the company in order to do

special things for our clients through the

creative use of new technologies and

techniques.

We help companies understand a

complex and ever-changing technology

landscape, along with changing

customer behaviours, developing

strategies and solutions to maximise the

opportunities available. We operate at

the intersection of digital, strategy and

customer, building a track record of

driving customer growth across our

three core industries.