flair study - florida department of financial services department of financial services flair study...

TRANSCRIPT

FLORIDADEPARTMENTOFFINANCIALSERVICES

FLAIRSTUDY

DELIVERABLE5

Date: 04/09/2014Version: 100

FloridaDepartmentofFinancialServices FLAIRStudy Pagei

TableofContentsEXECUTIVESUMMARY.............................................................................................................................................1

CHAPTER1 BACKGROUND............................................................................................................................1

1.1 FLAIRStudyPurpose..............................................................................................................................2

1.1.1 ProjectScope............................................................................................................................................2

1.1.2 FLAIRStudyApproach.........................................................................................................................3

1.2 FFMISOverview.......................................................................................................................................4

1.2.1 FFMISGovernanceStructure............................................................................................................5

1.2.2 PlanningAndBudgetingSubsystem(LAS/PBS).....................................................................6

1.2.3 CashManagementSubsystem(CMS)............................................................................................7

1.2.4 PersonnelInformationSubsystem(PeopleFirst)....................................................................7

1.2.5 ProcurementSubsystem(MyFloridaMarketPlace)................................................................8

1.2.6 FLAIRSubsystem(FLAIR)...................................................................................................................9

1.2.7 ProjectAspire........................................................................................................................................10

1.3 CurrentStatePerformance...............................................................................................................12

1.4 LimitationswithFLAIRToday.........................................................................................................14

1.4.1 ConsequencesofFLAIRLimitations............................................................................................22

1.4.2 StatusQuoisNotanOption............................................................................................................23

1.5 SolutionGoalsandBenefitsMustSupportTheAgency’sMission....................................23

1.5.1 TheCFO’sMission................................................................................................................................23

1.5.2 CurrentStateChallengesandRisksRequireActionToBeTakenNow......................23

1.5.3 GuidingPrinciplesShapeTheDefinitionofSuccess............................................................24

1.5.4 LongTermVision.................................................................................................................................25

1.5.5 Go‐ForwardSolutionGoalsandBenefits..................................................................................26

1.6 OutsourcingConsideration...............................................................................................................29

1.7 IndexofFFMISRelatedLegalCitations.......................................................................................29

1.8 Chapter1Appendix.............................................................................................................................31

1.8.1 CMSBusinessApplicationSummary..........................................................................................31

CHAPTER2 OPTIONSANALYSIS..................................................................................................................1

2.1 SummaryofCurrentSituation............................................................................................................3

2.2 MarketConditionsandTrends...........................................................................................................4

2.2.1 TrendsinPublicSector........................................................................................................................4

2.2.2 TechnologyTrends..............................................................................................................................15

2.2.3 OtherConsiderations.........................................................................................................................19

2.3 CostBenefitAnalysis...........................................................................................................................28

FloridaDepartmentofFinancialServices FLAIRStudy Pageii

2.3.1 MinimumCapabilitiesofaNewFinancialSystem...............................................................28

2.3.2 ExpectedBenefits.................................................................................................................................31

2.3.3 OptionDescriptions............................................................................................................................33

2.4 OptionsAnalysis....................................................................................................................................63

2.4.1 OptionAlignmentToVision,Goals,andObjectives.............................................................63

2.4.2 CostComparison..................................................................................................................................64

2.4.3 BenefitsComparison..........................................................................................................................67

2.4.4 RiskAnalysis...........................................................................................................................................72

2.4.5 SummaryAnalysis...............................................................................................................................78

2.5 APPENDIX................................................................................................................................................79

2.5.1 KeyThemesfromStateResearch.................................................................................................79

2.5.2 AdditionalStateResearch...............................................................................................................86

2.5.3 DetailedStateProjectProfiles.......................................................................................................90

2.5.4 RequiredSystemCapabilityJustification.................................................................................98

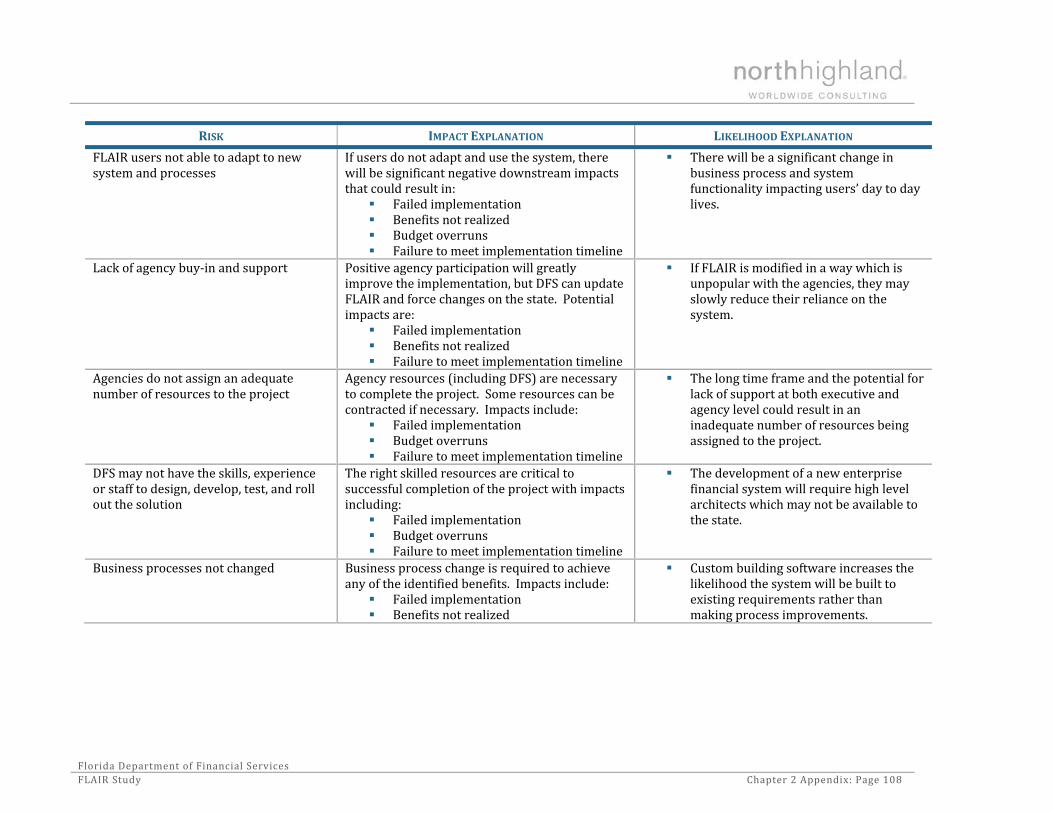

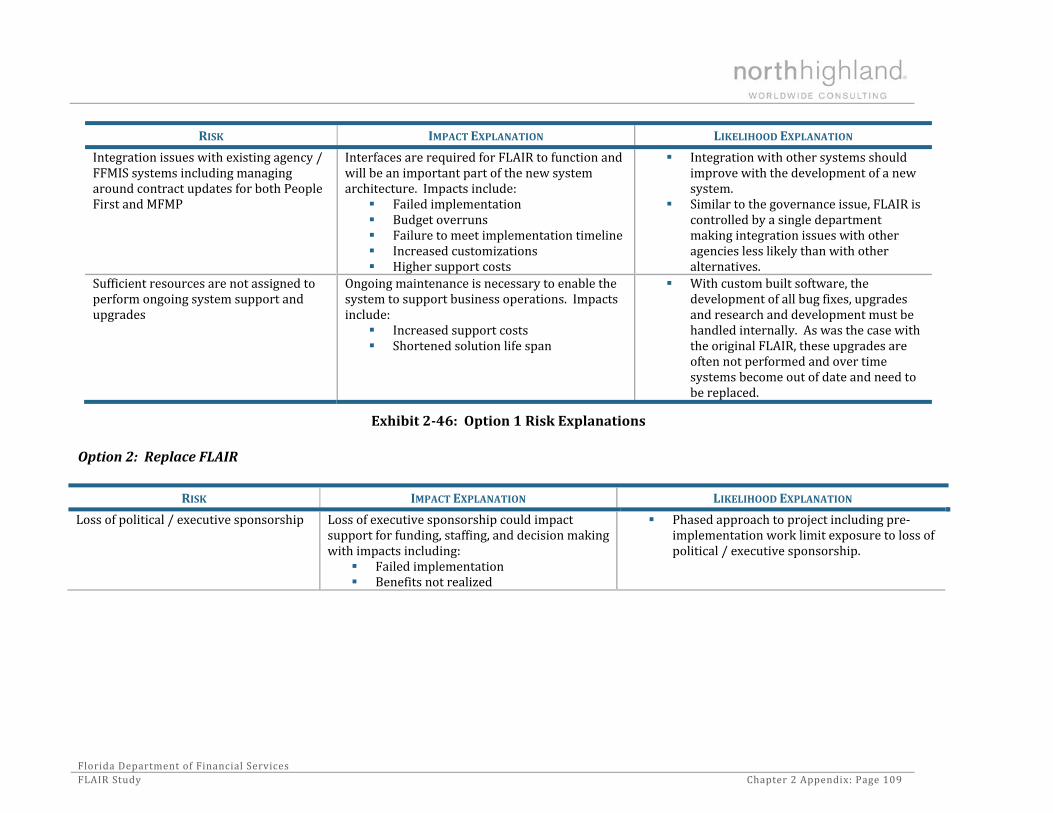

2.5.5 RiskJustifications...............................................................................................................................107

2.5.6 ListofSources......................................................................................................................................118

CHAPTER3 RECOMMENDATION................................................................................................................1

3.1 SupportforTakingActionNow.........................................................................................................1

3.1.1 SystemArchitecture..............................................................................................................................1

3.1.2 LackofNecessaryFunctionality......................................................................................................2

3.2 Recommendation–Option3:ReplaceFLAIRandCMSwithanERPSolution...............2

3.3 ProjectCriticalSuccessFactors.........................................................................................................7

3.3.1 EstablishaComprehensiveMulti‐TieredGovernanceModel.............................................7

3.3.2 ConfirmProjectFundingSource..................................................................................................15

3.3.3 ManageSystemCustomizations...................................................................................................17

3.3.4 InitiallyDeployaLimitedScopeofCoreFunctionality......................................................17

3.3.5 UtilizeaControlledPilottoValidatetheSolution...............................................................17

3.3.6 LeveragePhasedRollouttoAgencies.........................................................................................18

3.4 ChangesinStatuteandFinancialBusinessPractices.............................................................18

3.5 OutsourcingConsideration...............................................................................................................18

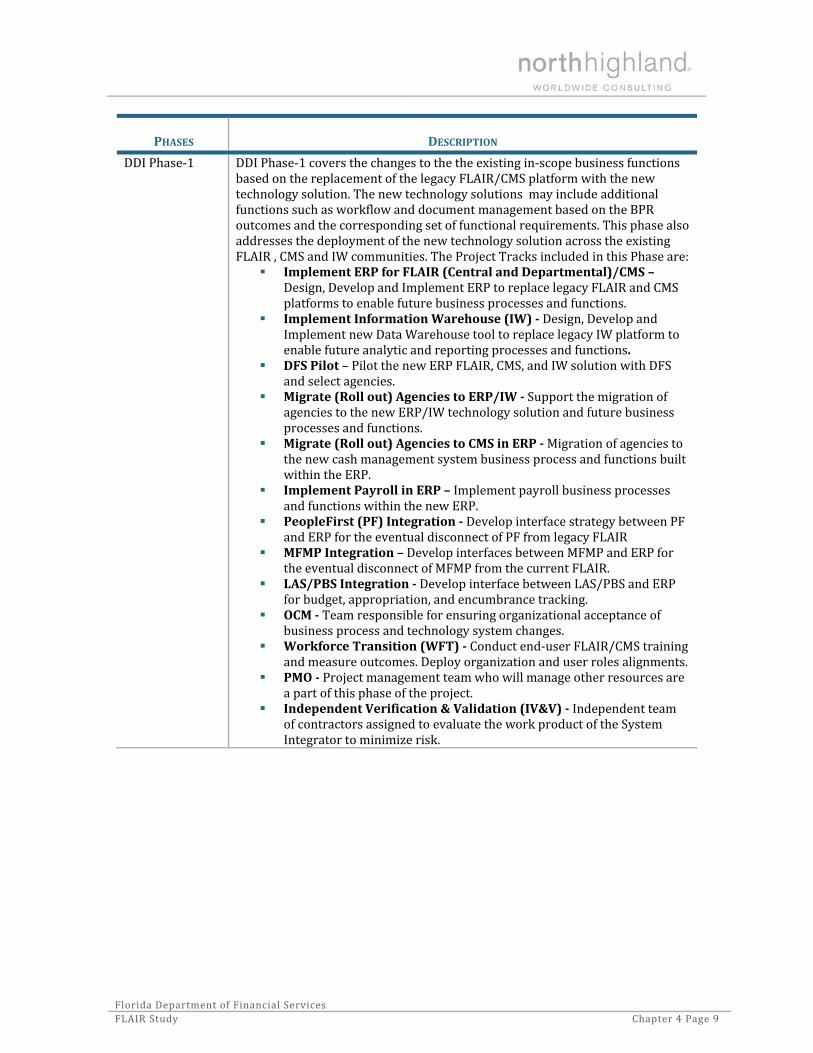

CHAPTER4 IMPLEMENTATIONSTRATEGY...........................................................................................1

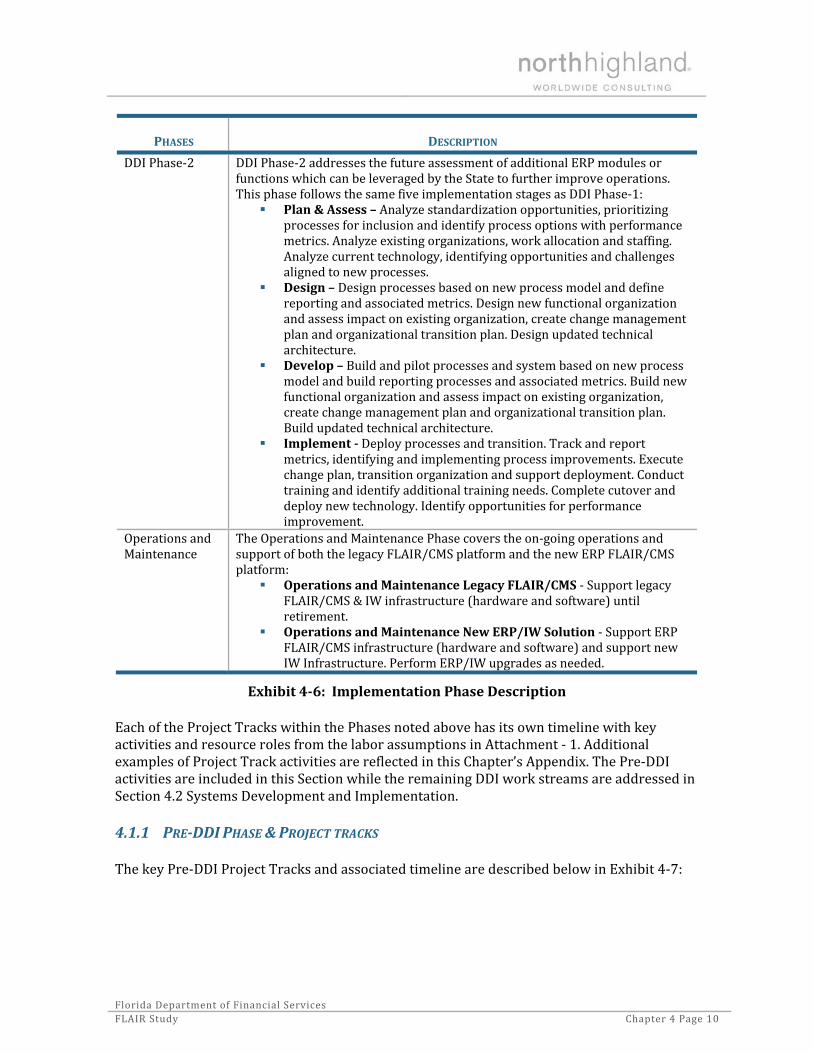

4.1 ImplementationTimeline.....................................................................................................................6

4.1.1 Pre‐DDIPhase&Projecttracks....................................................................................................10

4.1.2 Pre‐DDIIntegrationWithDDIPhase.........................................................................................14

4.2 SystemDevelopmentandImplementation................................................................................15

FloridaDepartmentofFinancialServices FLAIRStudy Pageiii

4.2.1 Design,DevelopandImplement‐Phases.................................................................................15

4.2.1.1 ImplementFLAIR/CMSERPProjectTrack..............................................................................17

4.2.1.2 ImplementInformationWarehouse(IW)ProjectTrack..................................................18

4.2.1.3 Pilot‐FLAIR/CMSReplacementProjectTrack....................................................................18

4.2.1.4 CMSRolloutProjectTrack..............................................................................................................19

4.2.1.5 FLAIR/IWRolloutProjectTrack..................................................................................................20

4.2.1.6 ImplementPayrollERPProjectTrack.......................................................................................21

4.2.1.7 MFMPIntegrationProjectTrack.................................................................................................22

4.2.1.8 PeopleFirst(PF)IntegrationProjectTrack...........................................................................23

4.2.1.9 LAS/PBSIntegrationProjectTrack............................................................................................24

4.2.1.10 IndependentValidationandVerificationProjectTrack..............................................25

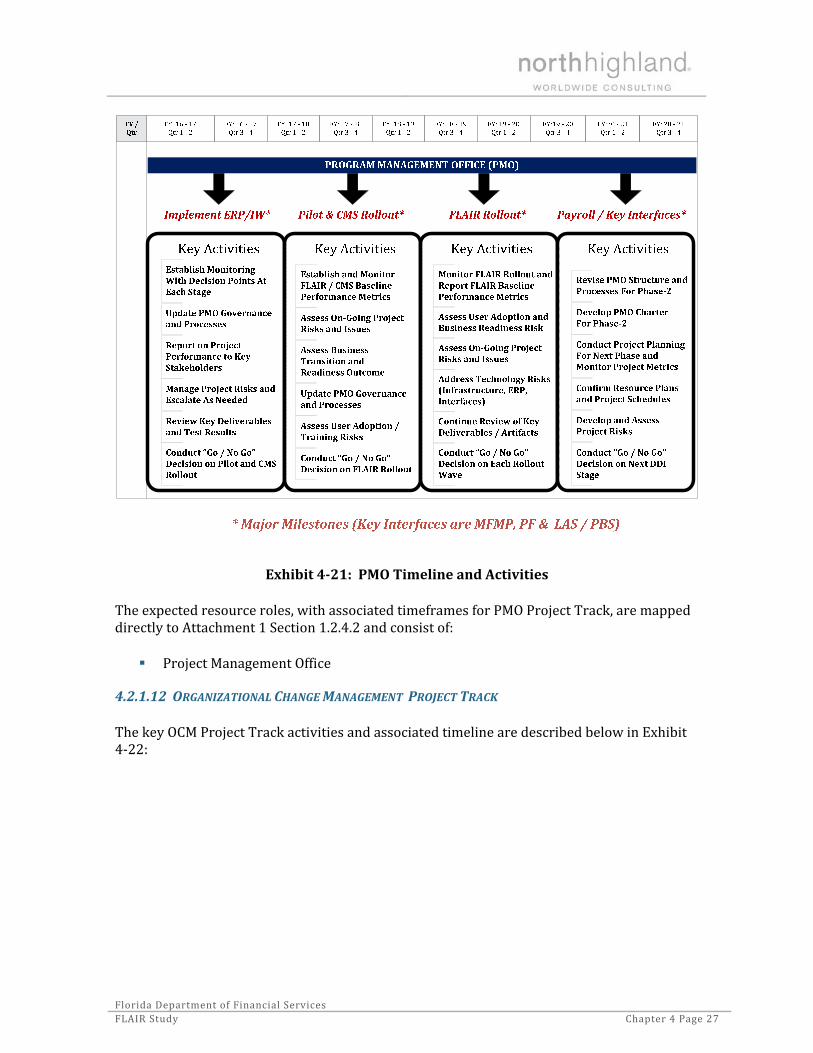

4.2.1.11 ProjectManagementOfficeProjectTrack..........................................................................26

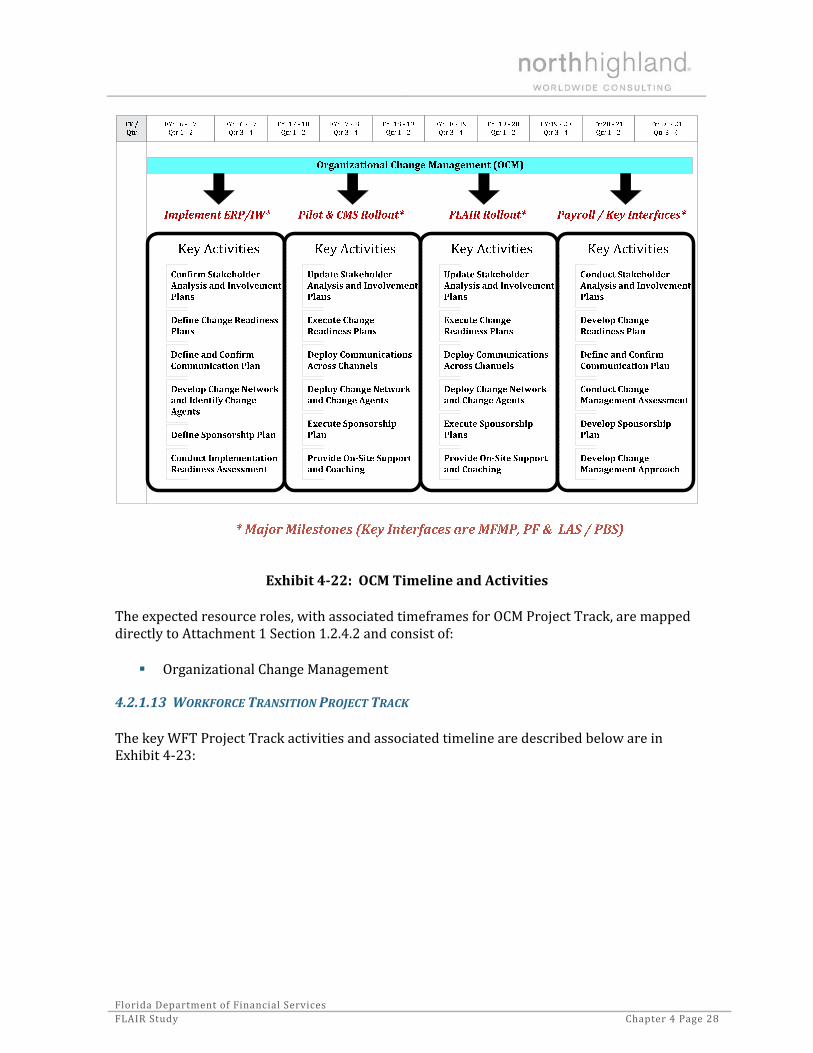

4.2.1.12 OrganizationalChangeManagementProjectTrack....................................................27

4.2.1.13 WorkforceTransitionProjectTrack.....................................................................................28

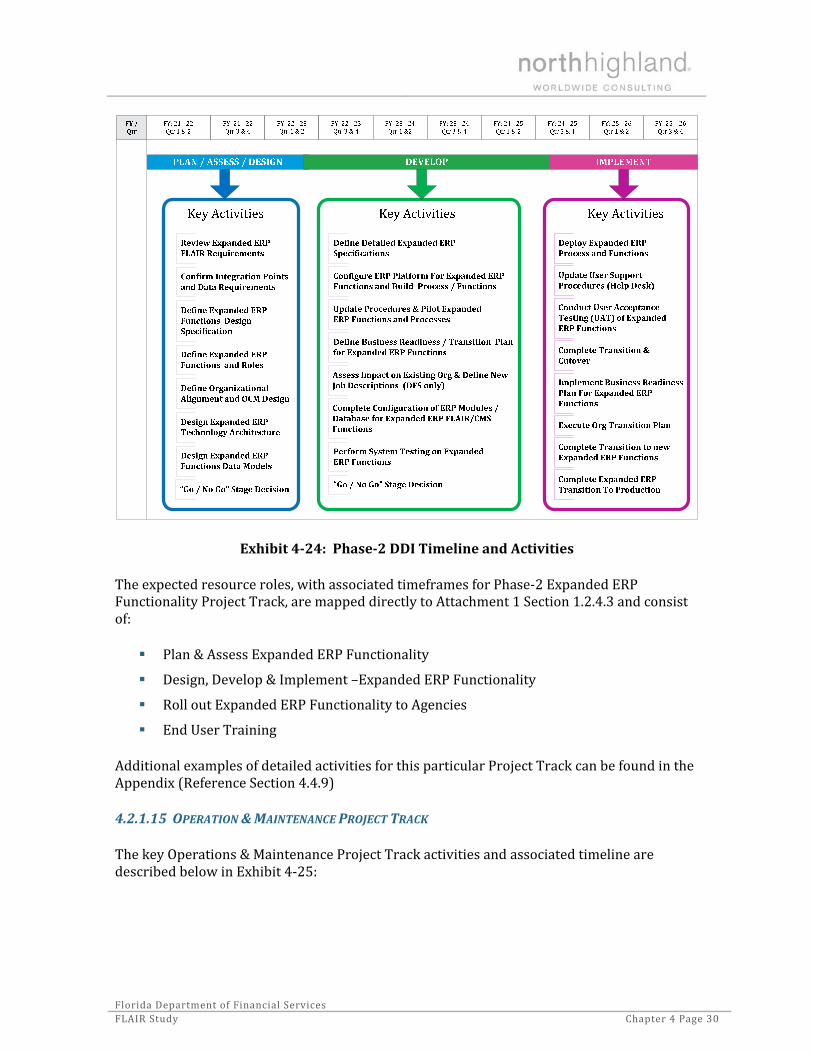

4.2.1.14 Phase‐2ExpandedERPFunctionalityProjectTrack.....................................................29

4.2.1.15 Operation&MaintenanceProjectTrack.............................................................................30

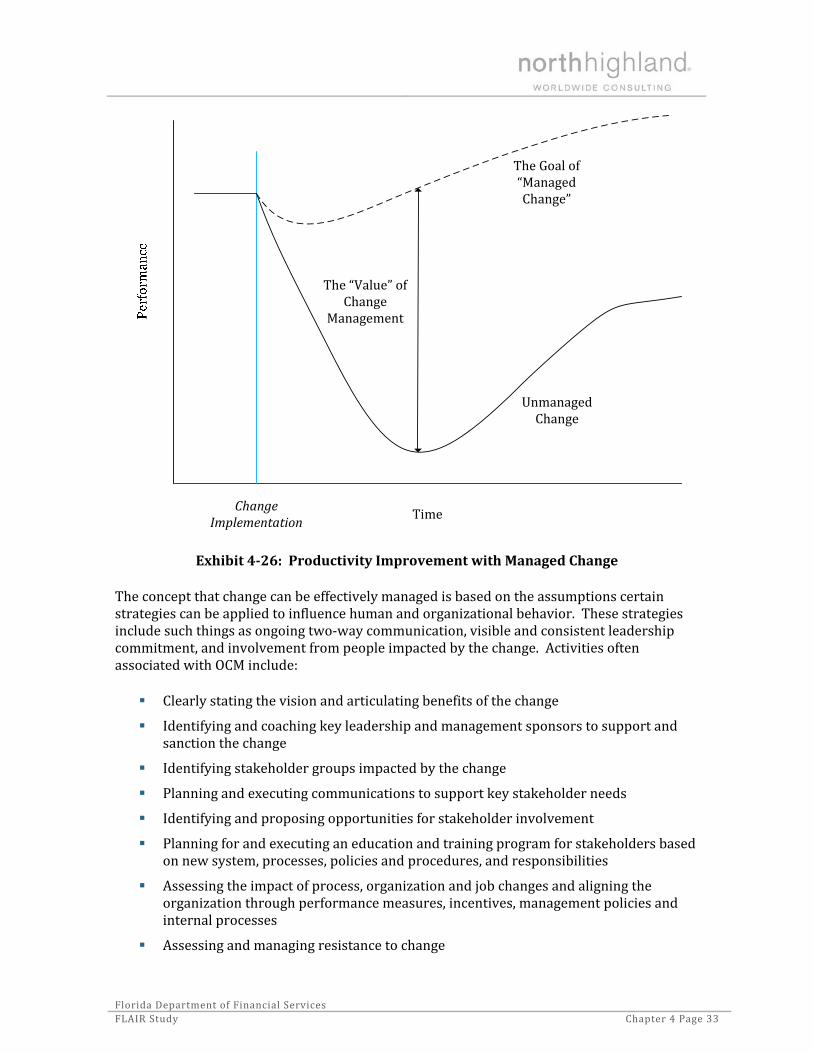

4.3 OrganizationalChangeManagementandWorkforceTransition....................................32

4.3.1 OrganizationalChangeManagement........................................................................................32

4.3.1.1 OCMFunctionalModel......................................................................................................................34

4.3.1.2 OCMandWFTFrameworkandDeliverables.........................................................................35

4.3.1.3 CommunicationPlanning&Implementation........................................................................39

4.3.2 WorkforceTransition........................................................................................................................42

4.3.2.1 WorkforceTransitionStrategy.....................................................................................................42

4.3.2.2 WorkforceTraining............................................................................................................................44

4.3.2.3 DetailedDepartmentalImpactsandTransitionImplementationPlans...................45

4.4 Appendix...................................................................................................................................................48

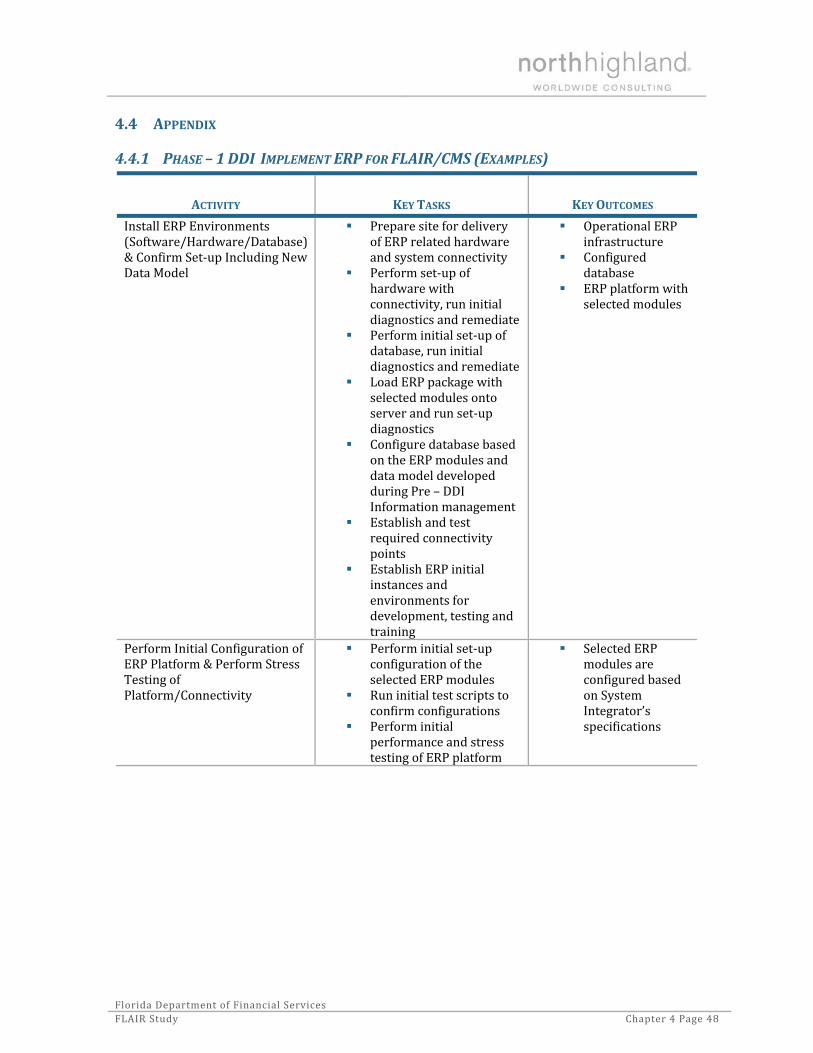

4.4.1 Phase–1DDIImplementERPforFLAIR/CMS(Examples)............................................48

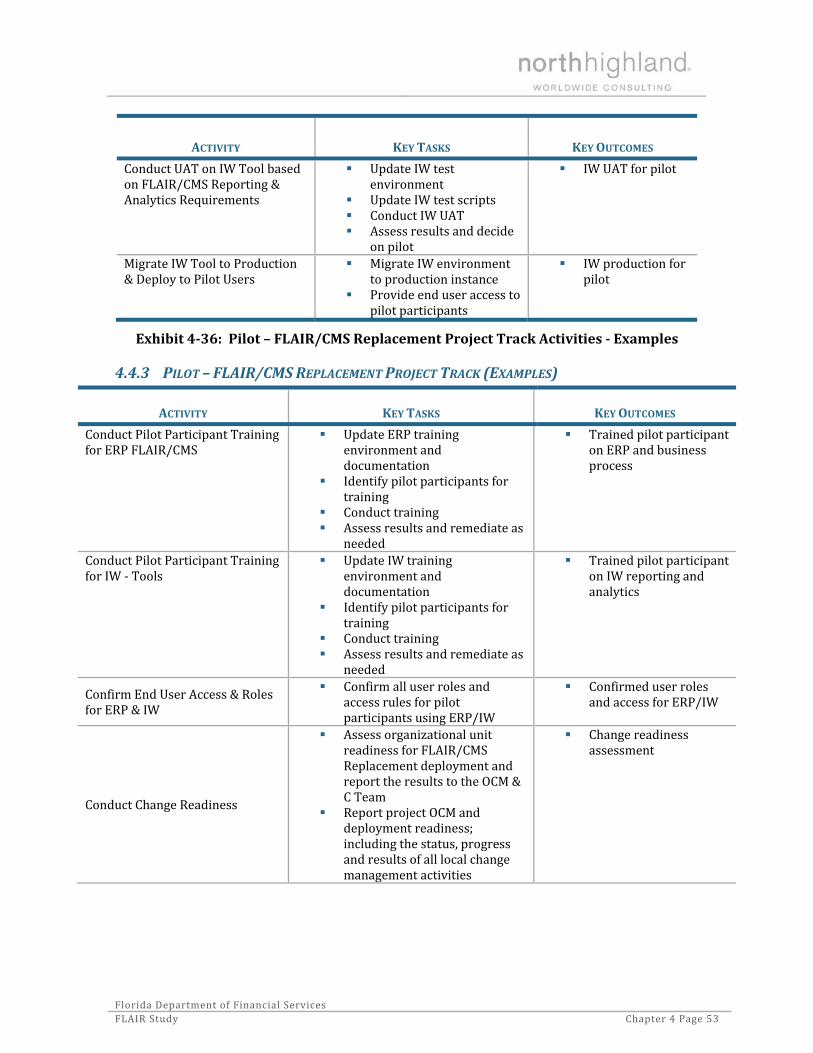

4.4.2 ImplementInformationWarehouse(IW)ProjectTracks(Examples).......................51

4.4.3 Pilot–FLAIR/CMSReplacementProjectTrack(Examples)...........................................53

4.4.4 CMSRolloutProjectTrack(ActivityExamples)....................................................................54

4.4.5 FLAIR/IWRolloutProjectTrack(ActivityExamples)........................................................55

4.4.6 MFMPIntegrationProjectTrack(ActivityExamples).......................................................57

4.4.7 PFIntegration/ImplementPayrollinERPProjectTrack(ActivityExamples)......57

4.4.8 Phase–1DDIIndependentVerificationandValidation.................................................58

4.4.9 Phase–2:ExpandedERPFunctionality(FLAIR/CMS)ProjectTrack........................60

FloridaDepartmentofFinancialServices FLAIRStudy Pageiv

4.4.10 OperationsandMaintenanceProjectTrack(Examples)..................................................61

4.4.11 OCMModel..............................................................................................................................................61

4.4.12 OCMFunctionalModelRoles&Responsibilities...................................................................62

4.4.13 TrainingandPerformanceSupportActivities.......................................................................67

4.4.14 CommunicationPlan..........................................................................................................................68

4.4.14.1 Stakeholders.....................................................................................................................................72

4.4.14.2 CommunicationEvent..................................................................................................................72

4.4.14.3 VehiclesofCommunication........................................................................................................73

4.4.14.4 ManagementofCommunications...........................................................................................73

CHAPTER5 PROCUREMENTANDCONTRACTMANAGEMENT.....................................................1

5.1 SummaryoftheFLAIR/CMSReplacementProject....................................................................2

5.2 GeneralTimelinewithProcurementsIndicated.........................................................................2

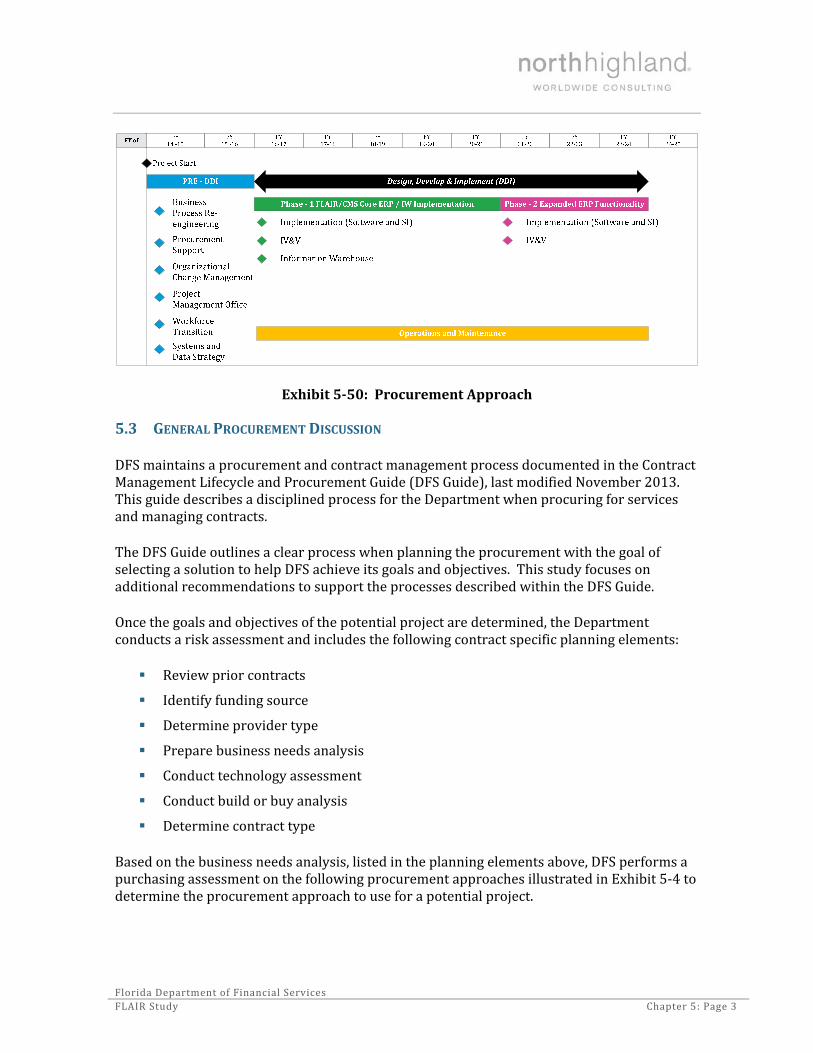

5.3 GeneralProcurementDiscussion......................................................................................................3

5.3.1 ProcurementRisks.................................................................................................................................5

5.4 GeneralContractingInformation......................................................................................................5

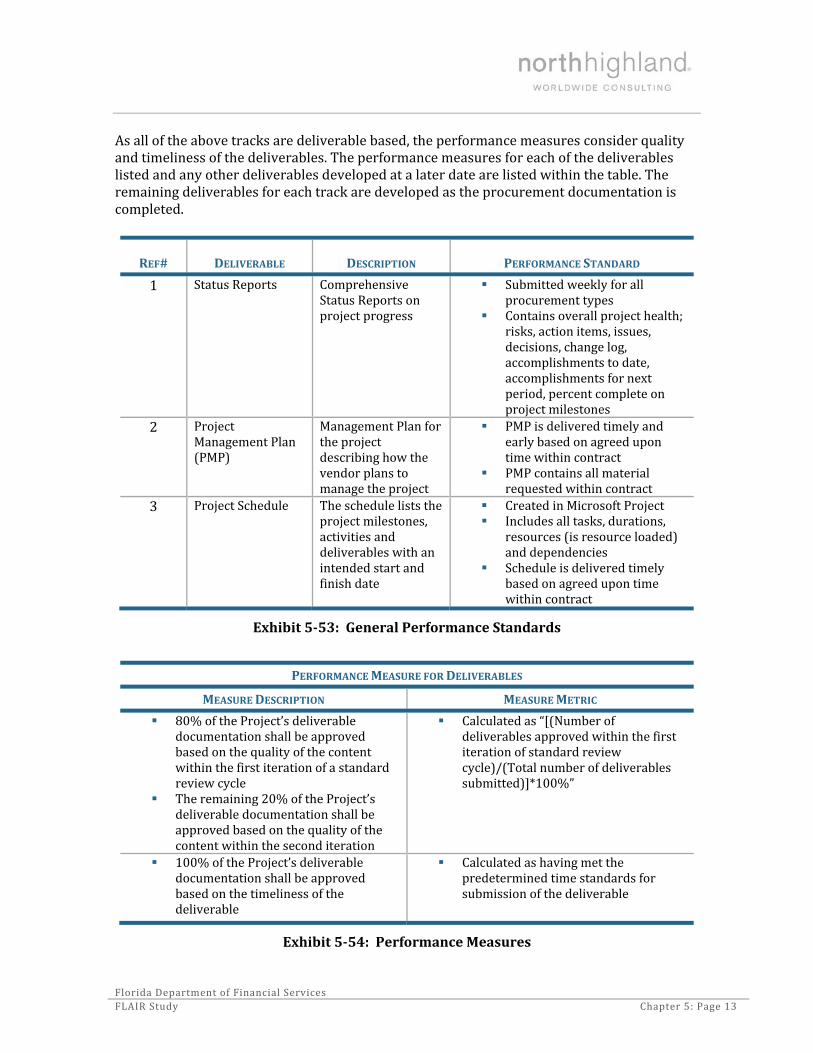

5.4.1 PerformanceStandards.......................................................................................................................5

5.4.2 PublicRecordsPolicy............................................................................................................................6

5.4.3 PersonswithDisabilitiesCompliance...........................................................................................6

5.4.4 ContractorNon‐PerformanceContingencyPlan.....................................................................6

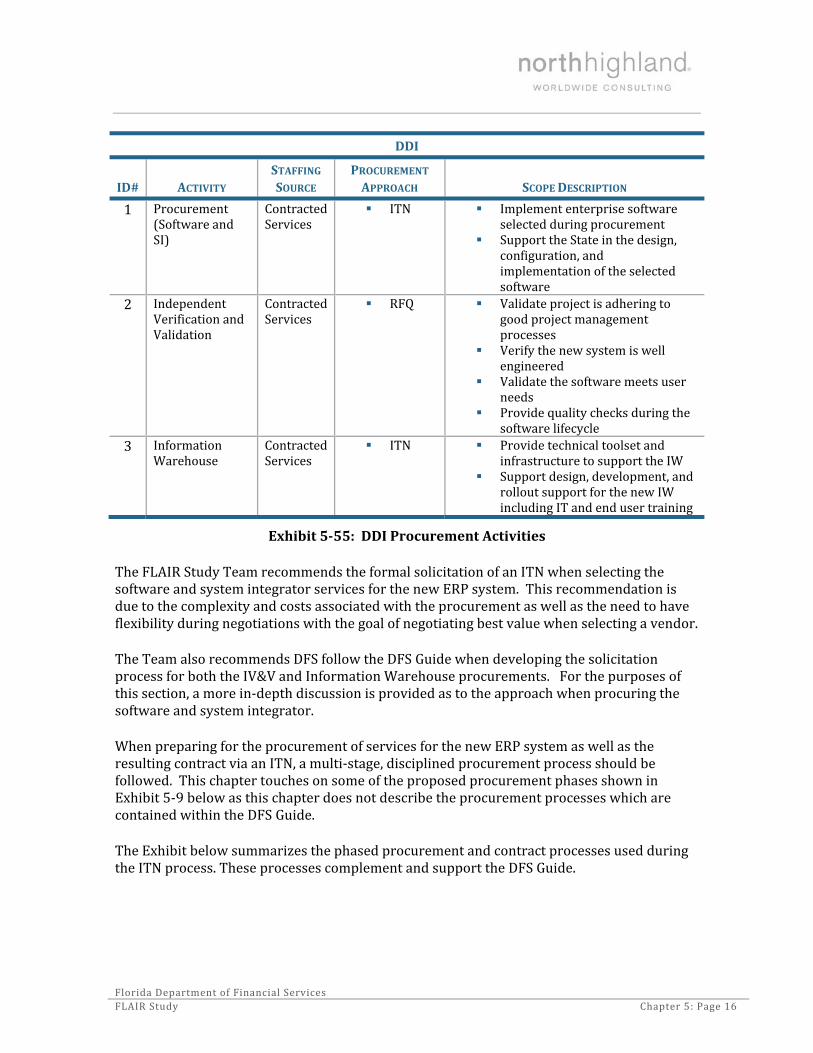

5.5 FLAIR/CMSReplacementProjectandProcurementApproaches.......................................9

5.5.1 Pre‐DDIProcurement...........................................................................................................................9

5.5.2 DDIProcurement.................................................................................................................................14

5.5.3 Post‐DDIProcurement......................................................................................................................32

5.6 Chapter5Appendix.............................................................................................................................34

5.6.1 BusinessProcessRe‐engineeringKnowledgeAreas............................................................34

5.6.2 ProcurementSupportKnowledgeAreas..................................................................................34

5.6.3 OrganizationalChangeManagementKnowledgeAreas..................................................35

5.6.4 ProjectManagementOfficePerformanceandKnowledgeAreas.................................35

5.6.5 WorkforceTransitionKnowledgeAreas...................................................................................36

5.6.6 SystemsandDataStrategyKnowledgeAreas........................................................................37

5.6.7 IV&VKnowledgeAreas.....................................................................................................................37

5.6.8 InformationWarehouse(IW)KnowledgeAreas..................................................................37

ATTACHMENT1 ASSUMPTIONS.......................................................................................................................1

1.1 Methodology..............................................................................................................................................1

1.2 CostModelAssumptions.......................................................................................................................1

FloridaDepartmentofFinancialServices FLAIRStudy Pagev

1.2.1 GeneralSupportingAssumptionsApplicabletoAllOptions.............................................1

1.2.2 Option1:EnhanceFLAIRCostAssumptions...........................................................................4

1.2.2.1 Option1:LaborAssumptions–Pre‐DDI...................................................................................4

1.2.2.2 Option1:LaborAssumptions–DDIPhase1...........................................................................6

1.2.2.3 Option1:LaborAssumptions–DDIPhase2........................................................................11

1.2.2.4 Option1:RequiredPurchaseAssumptions.........................................................................13

1.2.2.5 Option1:OngoingSupportAssumptions...............................................................................13

1.2.3 Option2:ReplaceFLAIRwithanERPSolutionCost–BenefitModel........................14

1.2.3.1 Option2:LaborAssumptions–Pre‐DDI................................................................................14

1.2.3.2 Option2:LaborAssumptions–DDIPhase1........................................................................15

1.2.3.3 Option2:LaborAssumptions–DDIPhase2........................................................................17

1.2.3.4 Option2:RequiredPurchaseAssumptions.........................................................................18

1.2.3.5 Option2:OngoingSupportAssumptions...............................................................................19

1.2.3.6 Option2:UpgradeAssumptions................................................................................................19

1.2.4 Option3:ReplaceFLAIRandCashManagementSystemswithanERPSolutionCost–BenefitModel..........................................................................................................................................20

1.2.4.1 Option3:LaborAssumptions–Pre‐DDI................................................................................20

1.2.4.2 Option3:LaborAssumptions–DDIPhase1........................................................................21

1.2.4.3 Option3:LaborAssumptions–DDIPhase2........................................................................25

1.2.4.4 Option3:RequiredPurchaseAssumptions.........................................................................26

1.2.4.5 Option3:OngoingSupportAssumptions...............................................................................27

1.2.4.6 Option3:UpgradeAssumptions................................................................................................27

1.2.5 Option4:ReplaceFLAIR,CMS,MFMPandPeopleFirstwithanERPSolutionCostModelAssumptions............................................................................................................................................27

1.2.5.1 Option4:Pre‐DDILaborAssumptions....................................................................................27

1.2.5.2 Option4:LaborAssumptions–DDIPhase1........................................................................29

1.2.5.3 Option4:LaborAssumptions–DDIPhase2........................................................................31

1.2.5.4 Option4:RequiredPurchaseAssumptions.........................................................................32

1.2.5.5 Option4:OngoingSupportAssumptions...............................................................................33

1.2.5.6 Option4:UpgradeAssumptions................................................................................................33

1.3 UserGuide:BusinessCaseModels................................................................................................34

1.3.1 MiscellaneousVariableDefinitions..........................................................................................34

1.3.2 Variables:Resources(Rows52–150)....................................................................................37

1.3.3 Variables:Weeks(Rows151–250).......................................................................................37

1.3.4 RequiredPurchases(Rows251–258)...................................................................................37

1.3.5 CostTagging(ColumnE)...............................................................................................................37

FloridaDepartmentofFinancialServices FLAIRStudy Pagevi

1.3.6 InflationRates...................................................................................................................................38

1.3.7 OptionDescription..........................................................................................................................38

1.3.8 ScheduleIV‐BCrosswalk..............................................................................................................39

1.3.9 Existing/New...................................................................................................................................40

FloridaDepartmentofFinancialServices FLAIRStudy Pagevii

REVISIONHISTORY

DATE AUTHOR VERSION CHANGEREFERENCE

4/9/2014 NorthHighland 100 FinalacceptedversionoftheFLAIRStudy.

QUALITYREVIEW

NAME ROLE DATE

FloridaDepartmentofFinancialServices FLAIRStudy ExecutiveSummary:Page1

EXECUTIVESUMMARY

TheFloridaConstitution(s.4(c),ArticleIV)andFloridaStatutes(Section17.001and215.94,F.S.)identifytheChiefFinancialOfficer(CFO)asthechieffiscalofficer.Byvirtueoftheposition,theCFOisresponsiblefortheFloridaAccountingInformationResourceSubsystem(FLAIR)andtheCashManagementSubsystem(CMS).Bystatute(Section215.94,F.S.)theDepartmentofFinancialServices(DFS,Department)isthefunctionalownerofFLAIR.AsthedesignatedagencyheadforDFS,theCFOisalsotheExecutiveSponsorforthisstudy.

AsaresultoftheprovisolanguageinSection6ofthe2013GeneralAppropriationsAct,theDepartmentprocuredtheservicesofNorthHighland,anindependentconsultingfirmwithexperienceinplanningpublicsectortechnologyprojects,tocompleteastudy(FLAIRStudy)andtorecommendeitherenhancingorreplacingFLAIR.Forthestudy,thejointteamofDFSandNorthHighlandisreferencedastheFLAIRStudyTeam(Team).Also,thestudyincludesaninventoryofagencybusinesssystemsinterfacingwithFLAIR(Inventory)andanassessmentofthefeasibilityofimplementinganEnterpriseResourcePlanning(ERP)SystemfortheStateofFlorida.

Fundamentally,theprovisolanguageacknowledgeschangesarenecessarytoFLAIR,andperhaps,CMS.Theprovisosummarizesthefouroptionstoevaluateas:

1. EnhanceFLAIR(Option1)2. ReplaceFLAIR(Option2)3. ReplaceFLAIRandCMS(Option3)4. ReplaceFLAIR,CMS,MFMPandPeopleFirstwithastatewideERPsolution(Option4)

TheoutstandingbusinessquestionstoanswerintheFLAIRStudyregardingtherecommendedoptionare:

IsthereanoptiontoenhanceFLAIRfromitscurrentstatetoamoremodernstatebyuseofnewtoolsandfunctionalityeitherbyaddingcomponentsoroverhaulingexistingcomponents?

Givencurrentconditionsandfutureexpectationsandobjectives,shouldFLAIRbereplacedintotalandshouldCMSalsobereplaced?

WhatisthefeasibilityofimplementinganEnterpriseResourcePlanning(ERP)systemfortheStateofFlorida?

WhatistheState’sreadinesstoimplementastatewideERPincludingthePurchasingSubsystem(MyFloridaMarketPlace,MFMP)andPersonnelSubsystem(PeopleFirst)?

ToemphasizetheimpactoftheFLAIRStudy,readersanddecisionmakersshouldconsiderthescaleandscope.Inrelativeterms,iftheStateofFloridawasacountry,itsGrossDomesticProductwouldbeamongthe20largestintheworld.IftheStateofFloridawasaprivatesectorcorporation,its$90billionbudgetwouldearnaspotinthe“Fortune25.”FinancialmanagementforanenterpriseofthesizeandcomplexityoftheStateofFloridahasascopeandscalebestcomparedtotheotherlargestates(i.e.California,Texas,NewYork,Illinois,and

FloridaDepartmentofFinancialServices FLAIRStudy ExecutiveSummary:Page2

Pennsylvania),thelargestUSFederalagencies,andthelargest,mostcomplexnationalandmulti‐nationalprivatesectorcompanies.

TheFLAIRStudyincludesamarketscantouseasinputforthefinalrecommendationinresponsetothebusinessquestions.Themarketscanincluded(1)areviewofotherlargestates’financialsystemmodernizationprojects,(2)inputfromselectStateagencieswithdiversebusinessneeds,(3)marketanalystrecommendationsforviablesoftwaresolutions,and(4)interviewswithrelevantprivatesectorcompaniesincludingsoftwareandserviceproviders.Also,thestudyrepresentsthelatestversionofseveralpreviousstudiescompletedbypublic1andprivate2organizations.Allofthestudies,includingthisstudy,havecometosimilarconclusions.

TheconclusionofthisstudyistheStateofFloridashouldpursuethereplacementofFLAIRandCMSwitha“CommercialofftheShelf”(COTS)ERPsolutionforthefinancialmanagementprocessestosupporttheconstitutionalobligationsoftheCFO.ThereplacementofFLAIRandCMSwill:

Mitigateriskassociatedwithafragileapplicationcodeenvironmentinarapidlychangingbusinessenvironmentwhichcanleadtosignificantoperationalinterruptionsanddowntime(e.g.,creatingnewagencies,consolidatingagencies,modifyingpayrollcalculations,addingnewdataelementstosupportfinancialcodechanges)

Implementastatewideaccountingsystemtoenforcestandardizationresultinginfuturebenefitsfromincreasedintegrationandatrueenterpriseperspectiveofgovernmentfinancialoperations

Actasascalablefoundationtoevolveasbusinessneedschange

PositionFloridaforfutureinnovationwiththeabilitytoconsideratrueenterprisesystem

CURRENTSTATUSOFFLAIRANDCMS

FLAIRandCMSarereferencestoaseriesoftechnicalsubcomponentsperformingvariousfinancialandcashmanagementfunctions.ThesystemssupportthebusinessaspectsoftheDivisionofAccountingandAuditing(A&A),theDivisionofTreasury(Treasury)andstateagencyfinancialaccounting.

Acapable,flexibleandreliablefinancialmanagementsystemisamustforanenterprisethesizeofFlorida.FLAIRisnotkeepingupwiththeState’sevolvingandgrowingbusinessneedsand,astimegoeson,theoperationalriskofrelyingonFLAIRonlyincreases.Thelimitations

1CouncilonEfficientGovernmentReporttotheGovernoronMyFloridaMarketPlace,PeopleFirstandProjectAspire,1/7/20082KPMGModernizationofStateGovernmentFinancialManagementBusinessPracticesStudy,8/2/1999–2/15/2000;KPMGFLAIRReplacementFinalReport,3/8/2001

FloridaDepartmentofFinancialServices FLAIRStudy ExecutiveSummary:Page3

withFLAIRandtheassociatedimpacts(e.g.,proliferationofagencycompensatingsystemsandagencyuniqueprocesses)arenottrivialandnegativelyimpacttheoperationalproductivityandthefinancialmanagementoftheState.

FLAIRisa30‐yearoldsystemwithanarrayoftechnology,oldandnew.Thecoretechnologywasdevelopedinthe1970sandimplementedinthe1980s.Whilethesoftwareandhardwareversionsarerelativelycurrent,theconstructoftheinternalsoftwarecomponentsandconfiguration(codinglanguageisoutdatedwithinthedatabase),andadministrationovertheyearspresentarigidandfragilefoundationinanenvironmentrequiringadynamicresponsetoeconomic,politicalandsocialchanges.

ThisstudyincludedaninventoryofagencysystemsinterfacingwithFLAIR.Toincreasecontextualaccuracy,theinventoryconsideredalsosystemsperformingfinancialmanagementfunctionscommonplaceformoderncorefinancialmanagementsystems.Todaythenumberofagencycompensatingsystemsismorethan400.Thisnumberrepresentsa33%increasefromasimilarstudyinin2000.Furthermore,75%ofthesesystemsareapproachingapointintimetheywillrequiresignificantresourcestomaintainandreplace.

TheFLAIRprogramminglanguageanddatafilestructurearenotcommonplaceandresourcestosupportthetechnologyarescarceinthemarkettoday.Accordingtosoftwareindustryanalysts,thecurrentprogramminglanguagedoesnotrankinthetop50in‐demandtoday.FromanITsupportperspective,approximately42%ofFLAIRtechnicalsupportemployeeshave30ormoreyearsofservice.Astheseemployeesretireitwillrepresentasignificantlossofinstitutionalknowledgeandtechnicalexpertise.Replacingthetechnicalexpertiseofamarketscarceresourceishighlyunlikely.Conclusively,theFLAIRstaffmemberswhomaydepartwithinthenextfiveyearsareseasonedandexperiencedexpertswithmanycombinedyearsofinstitutionalknowledgepresentingasignificantriskforenhancementandsupporttoFLAIRinthenearfuture.

ForCMSthereisasimilar,albeitmoremodernsituation,regardingsupportstaff.WhileasignificantportionofCMSfunctionalityisbeingreplacedbymoremoderntechnology,theresourcepoolsupportinganddevelopingthemoderncomponentsisconstrainedbyasmallnumberofexisting,senioremployees.ThispresentsadditionalriskacrossthedomainandfunctionsoftheTreasury.Mitigatingtheriskbybuildingacompleteprogrammingsupportorganizationisunrealistic.

FLAIRhasnotbeensignificantlyupgradedinthecontextofmodernizingthecoremodules.Codingtechniqueshavechangedandthereisariskofprogramswithoutdatedprogramminglanguagesoftwarestructurenotbeingproperlyupdatedwhenstatutorychangesaremade.Thelastsignificantfunctionalupgradeoccurredinthelate90’swiththeadditionofthepurchasingcard(P‐card)functionality.LesssignificantenhancementscontinueandnonesignificantlyimproveormoveforwardthebaseFLAIRtechnology.

FLAIRiscomprisedoffourcomponentstosupportaccountspayable,accountsreceivable,financialstatements,cashprojectionsandforecastingandstatepayrollprocessing:

CentralAccountingComponent(CentralFLAIR)–mostlyusedbyA&Aforauditing,maintainscashandbudgetarybalances,andfunctionsfortaxreporting

FloridaDepartmentofFinancialServices FLAIRStudy ExecutiveSummary:Page4

DepartmentalAccountingComponent(DepartmentalFLAIR)–usedbyallagenciestoreportgeneralledgerbalances,maintaindetailedaccountingrecords,manageassets,andadministervendorfilesusedforpayments

Payroll–processesemployeepayments,taxreportingandotheragencyadministrativepayrollfunctionsnotperformedbyPeopleFirst

InformationWarehouse(IW)–asthefinancialdataandreportingrepository,maintainsfiveyearsoftransactionhistoryandusedprimarilytosupplydatatoagencyfinancialmanagementsystems

Priorto2013,theTreasuryusedfourteendifferentapplicationswhichweredevelopedatvariouspointsintimebetween1984and20023.Thenetresultofthevariousapplicationdevelopmenteffortswasmultipledatabaseplatformstosupportmultipleprogramminglanguages.Thedifficultytomaintainadequateresourceswiththecomplexskillsetneededtosupportsuchavarietyofplatforms,andintegrationamongplatformscanbecomeachallenge.Furthermore,fromabusinessperspective,processescanbedisjointedandinterruptedcreatingmultipleentrypointsforinefficientandineffectivepractices.TheTreasuryfunctionsCMSservesare:

CashManagement

InvestmentManagement

AccountingManagement

Treasuryembarkedonatwophasemodernizationeffortwhichbeganin20094.Phase1includedanintegratedapplicationtosupportcashmanagementprocessesincludingreceipts,verifications,andchargebacksultimatelyupdatingthebankandstateaccountapplications.ThefirstphaseofthemodernizationeffortwasimplementedinAugust2013.Alsoin2013,theTreasurybeganthesecondphaseofmodernizationandthisphaseincludesvariousprocessesforconsolidatedrevolvingaccounts,investmentaccounting,trustfundaccounting,warrants,disinvestments,archives,agencyrepository,andreplacementofbankandstateaccounts.Thisphaseisinprogresswithanestimatedcompletiondateof2018.

Finally,therespectivesystemsandsubsystemsforFLAIRandCMSarenotintegrated.Theyinteractthroughexternalprogramsandfileexchanges.ThisistrueforeachofthesubsystemsoftheFloridaFinancialManagementInformationSystem(FFMIS)including:

PlanningandBudgeting

FLAIR

CashManagement

Purchasing

3DFSTreasuryCashManagementSystemModularRedesignProjectJustification,10/27/20094CashManagementSystem,ProjectManagementPlan,DepartmentofFinancialServices,12/16/2011

FloridaDepartmentofFinancialServices FLAIRStudy ExecutiveSummary:Page5

Personnel

FRAMEWORKFORTHEFLAIRSTUDYRECOMMENDATION

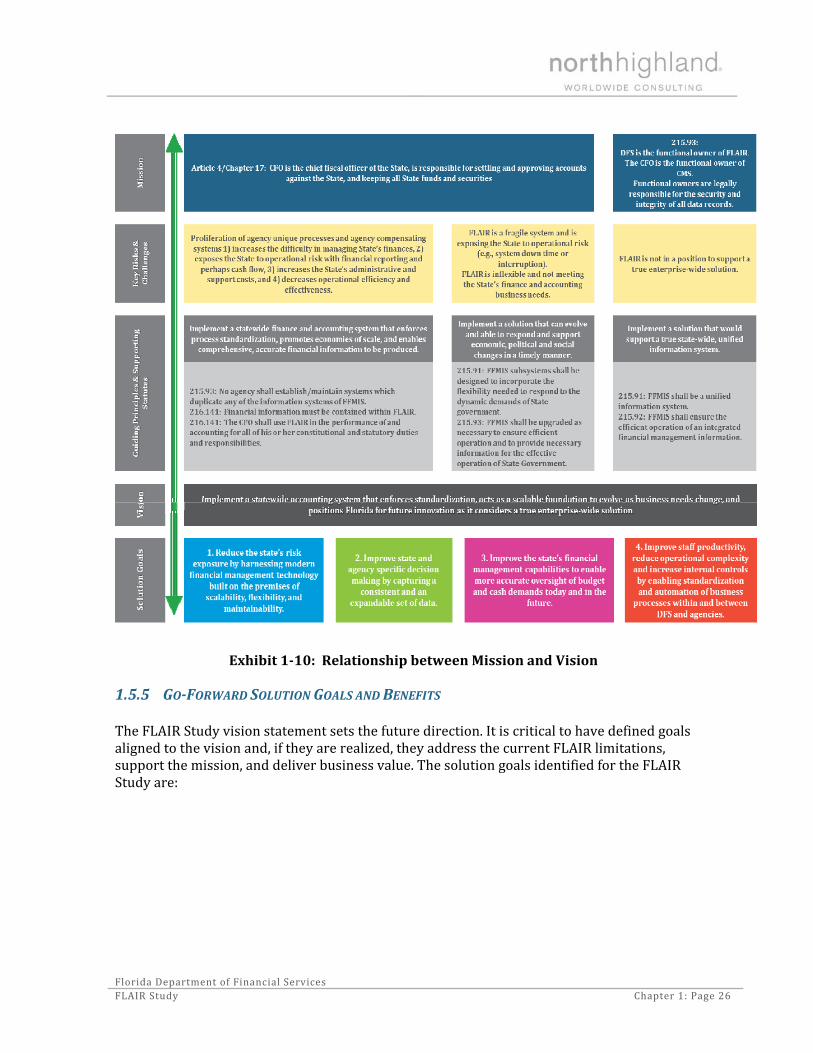

ThrougharigorousexercisefacilitatedfortheDFSexecutiveteam,avisionandcomprehensivesetofgoalswasestablishedasthebasistoevaluatethealternativesforFLAIRfromthe2013GAAproviso.Theselectionofalternativesfromthe2013GAAprovisolanguagemustsupport:

1. AreductionoftheState’sfinancialriskexposurethroughtechnologybuiltonthepremisesofscalability,flexibility,andmaintainability

2. ImprovementintheState’sspecificdecisionmakingbycapturingaconsistentandanexpandablesetofdata

3. ImprovementintheState’sfinancialmanagementandaccountingcapabilitiestoenablemoreaccurateoversightofbudgetandcashdemandstodayandinthefuture

4. Improvementinstateemployeeproductivity,reductionofoperationalcomplexityandanincreaseofinternalcontrolsbyenablingstandardizationandautomationofbusinessprocesseswithinandbetweenDFSandtheState’sothergovernmentalagencies

Thefinancial,operational,andotherbenefitsofimplementingnewtechnologyforFLAIRwillhaveasignificantimpactuponstategovernmentfromtheperspectiveofbusinessandtechnology.Benefitsinclude:

Establishmentofthenecessarycornerstoneforanewintegratedfinancialmanagementsystemwithtightlyintegratedfunctions(e.g.,generalledger,accountspayable,etc.)

InclusionofasignificantnumberofdatafieldswiththeabilitytodefineandchangethefieldstoimprovetheState’smanagementofbudgetandunitcosts

Realizationofcostavoidanceduetoreducedagencyadministrativecoststhroughprocessstandardization,overallsystemmaintenancecosts,andareducedneedforagency‐runfinancialmanagementsystemsandexternalfinancialdatarepositories

BUSINESSCASEFINDINGSANDRECOMMENDATIONS

TheFLAIRStudyaddressestheprimaryelementsforbusinesscasesinthePlanningandBudgetingInstructionsontheFloridaFiscalPortal5relativetothe2013GAAfortheFLAIRStudy.Specifically,asdocumented,tosupportthefinalrecommendation,theFLAIRStudyincludes:

5StateofFloridaFiscalPortal,PlanningandBudgetingInstructions,BusinessCaseGuidelines&Instructions

FloridaDepartmentofFinancialServices FLAIRStudy ExecutiveSummary:Page6

AnoptionsanalysisfortheenhancementorreplacementofFLAIRandCMSincludingtheimplementationofastatewideERPsolution

RecommendationssummarizingtheresultsoftheFLAIRStudy

ImplementationelementstosupporttherecommendationfortheenhancementorreplacementofFLAIRandCMS

ProcurementandcontractingoptionsfortherecommendedcomponentsoftheFLAIRStudy

TheFLAIRStudyTeamconductedanoptionsanalysiswasperformedbyreferencingdatagatheredfromextensivemarketresearch,specificFloridaagencyinterviews,andtargetedinterviewswithcomparablestates.TheanalysiswasbasedonsystemfunctionalityrequiredtomeettheState’sneeds.Commonthemesfromtheoptionsanalysisincludethefollowing:

AllstateswhohavemodernizedtheirsystemswithinthepasttenyearshavemovedtoanERPsolution

Enforcestandardizationofbusinessprocessesthroughgovernanceinsteadofmakingindividualcustomizations

ThelevelofgovernancestrengthisdirectlyrelatedtothelevelofsuccessandoutcomesoftheERPimplementations

Pre‐implementationactivitiesareessentialtotheoveralladoptionoftheERPsolutionsincludingpreparingforenterprise‐widechangeincludingbusinessprocessre‐engineering,workforcetransition,andmanagementoforganizationalchange

Theimplementationcostofthefouroptionsrangebetween$219millionand$467million.Thefouroptionsrangebetweensevenandfifteenyearstofullyimplementandachievetheidentifiedgoalsincludingasignificantreductioninoperationalandfinancialrisk,simplificationoffinancialmanagementprocesses,andimprovedvisibilityandreportingatastatewidelevel.

Basedontheanalysiscompleted,theFLAIRStudyTeamrecommendstheStateofFloridareplaceFLAIRandCMSwithacoreERPsolution(Option3).Thequantitativeandqualitativefactorsconsideredintheanalysisinclude:

Alignmenttodefinedmissionandsolutiongoals:

o Options3and4aremostcloselyalignedtothemissionoftheCFOandthesolutiongoalsspecificallybecausetheyrepresentastatewidesolutionwiththeabilitytoenforcestandardizationandscaletoevolvingandchangingbusinessrequirementsoftheState

o Options3and4improvetremendouslytheState’sfinancialmanagementcapabilitybyenablingmoreaccurateoversightofbudgetandcashdemandswhilereducingoperationalcomplexitiesandincreasingstandardization

o Options1and2donotsupportthemostbasicsystemcapabilityofasinglesystemofrecordforstatewidefinancialtransactionsandcashbalancesandincreasetheoperationalcomplexityoftheotheroptions

FloridaDepartmentofFinancialServices FLAIRStudy ExecutiveSummary:Page7

Riskanalysis:

o Option3presentsthelowestriskratingoftheelementsevaluatedincludingpoliticalandexecutivesponsorship,governance,funding,technicalresourceavailability,agencybuy‐inandsupport,standardizationandintegrationwithFMMISsystems

o Option1hasthehighestriskprofilerelativetotheanalysisbecauseenhancingFLAIRrequiresacompleterebuild

SolutionCosts‐bothimplementationandtotalcostofownershipover15years:

o Option2hasthelowestimplementationcostbyapproximately3%fromOption3($219millionversus$225million)

o Options1and4aresubstantiallymorecostlytoimplement($467millionand$383millionrespectively)

Timelinetoimplementandrealizepotentialbenefits

o Option3hasbestrankingwitha7.9yeartimelineuntilbenefitsarepotentiallyrealizedrepresentinganominalimprovementoverOption2

Irrespectiveoftherecommendedoption,theFLAIRStudyTeamspentconsiderabletimedetermininganimplementationapproachwiththeoverallobjectiveofachievingtheexpectedoutcomesbyreducingtheriskinlarge,complexITprojectsofthisnature.GiventhelessonslearnedfromProjectAspire–goodandbad,inputfromthemarketscanincludingotherlargestatesandFloridaagencies,theimplementationstrategytosupportthereplacementofFLAIRandCMSmustconsiderthefollowing:

Anenhancedandeffectivegovernancestructureattheenterpriseandoverallprojectlevel

ThebusinessandITorganizationalunitswillundergosignificanttransformation

Extensivecommunicationandcoordinationwiththestateagenciesdirectlysupportssuccess

TheInformatonWarehouserequiresanoverhaulstartingwiththecreationofasystemanddatastrategy

BusinessprocessstandardizationisimperativetosupportanyfuturebenefitsgainedfromreplacingFLAIRandCMSwithanERPsolution

BasedontheelementsofsuccessforimplementinganewFLAIRandCMSderivedfromProjectAspirelessonslearned,themarketscan,andindustryexperienceappliedtothelocalenvironment,significantconsiderationwasgiventothereplacementapproach.TheTeamdevelopedandincorporatedthreecommonprinciples.ThefirstprincipleistocreatearealisticplantocompletetheFLAIRandCMSreplacementproject.Thenextprincipleincorporatesanumberofsmallerobjectivesalongadeliberatetimeline.ThefinalprincipleacknowledgesthestatewideaspectoftheprojectandtheimpacttotheotherFloridaagencies.Withthesecoreprinciplesapplied,theFLAIRandCMSreplacementprojectshouldoccurasdescribedbelow:

FloridaDepartmentofFinancialServices FLAIRStudy ExecutiveSummary:Page8

ThefirsttwoyearswillconsistofactivitiestoprepareDFSforimplementationincludingdecisionpointsincorporatedalongthewaytoupdatethebusinesscaseandevaluatedirection

ThefirstimplementationwillconsistofanewERPforcoreFLAIRandselectCMSfunctions

Apilotwillbeheldpriortofullimplementationforadditionalagencies

Staggeredrolloutswilloccurwiththeagencies

ThisapproachallowstheStatetoprepareadequatelyandtoincorporatelessonslearnedwhenmovingthroughthefullimplementation.

Usingresultsfromtheoptionsanalysiswork,Gartner6analystinput,andlessonslearned,themethodofprocurementisamatterofalignmentwiththebuyingorganization.Selectingthesoftwareandservicesseparately(unbundled)isacommonapproachwhenthebasicfunctionalityandusabilityofthesoftwarearepriorities.Otherwise,conductingasingleprocurementforsoftwareandservices(bundled)givesdeferencetoleveragingaserviceprovider’sexperienceandcapabilitytoimplementandsupportERP.BothmethodshavebeensuccessfullyusedtoselectanERPsystem.Likewise,bothmethodswereusedinunsuccessfulprojectssothereisnocleardifferentiatorbetweentheprocurementmethods.

TheFLAIRStudyTeamrecommendsthefollowingmethodforFloridagiventhepastexperiencewithProjectAspireandanappropriatealignmenttocurrentandtofutureobjectives:

ConductasingleprocurementleveragingasoftwareselectionandtheexperienceofanERPsystemintegratorresultinginasinglecontractforsoftwareandservices

Includecontractualrequirementsforthesoftwarevendortoreviewandtoconfirmanycustomizationstotheirproductdoesnotinhibitfutureenhancementsandupgrades

Incorporateperiodicreviewsofprogresswithminimumcriteriaforacceptancetoassessaccuratelywhethertheimplementationiswithintoleranceforsuccessortoidentifysignsoftroubleandpreventcontinuedprogressuntilanyissuesareremedied

Requirefinancialconsequencefornon‐performanceandterminationtoensuretheStateisprotectedandabletocontinuemovingforwardwithoutsignificantadditionalinvestment

TheDepartment’sprocurementandcontractmanagementprocess,whichisdocumentedintheDFSContractManagementLifecycleandProcurementGuide,willbefollowedtodeveloptheprocurementdocumentsandcontract.

6Gartner,Incorporated,Foundedin1979,isatechnologyresearchandadvisorycompany.

FloridaDepartmentofFinancialServices FLAIRStudy Chapter1:Page1

CHAPTER1 BACKGROUND

TheFLAIRStudyadoptedthebusinesscaserequirementsofChapter287oftheFloridaStatutes.TheexhibitbelowprovidesthosestatutesapplicabletoChapter1Background.

FLORIDASTATUTE

287.0571(4)(b)Adescription andanalysisofthestateagency’scurrentperformance,basedonexistingperformancemetricsifthestateagencyiscurrentlyperformingtheserviceoractivity.

287.0571(4)(c) Thegoalsdesiredtobeachievedthroughtheproposedoutsourcingandtherationaleforsuchgoals.

287.0571(4)(d) Acitationtotheexistingorproposedlegalauthorityforoutsourcingtheserviceoractivity.

Exhibit1‐1:Chapter1FloridaStatutes

KeyTakeawaysFromThisChapter

TheabilityoftheCFOandDFStoperformtheirrolesandresponsibilitiesandcompletethestatutorymissionisbecomingincreasinglydifficultgiventhesignificantlimitationsofFLAIR.Anewfinancialmanagementsolutionisneedednowandtheneedforchangecanbeevidencedbythefollowing:

Agenciesareimplementingworkaroundsandfinancialrelatedbusinesssystemstofill“gaps”createdbyFLAIRlimitations.Theproliferationoftheseagencyuniqueprocessesandcomplementarysystemswillcontinueasbusinessneedschange.Theresultingimpactwillincreaseoperationalcomplexitythroughthecontinuedde‐standardizationofstatefinancialprocessesandanincreaseinmaintenanceandadministrativecosts.ThisconditionwillmakeitmoredifficultfortheCFOandDFStomanagetheState’sfinancialresources.

FLAIRisaninflexibleandfragilesystem.ItisnotkeepingupwiththeState’sevolvingandgrowingbusinessneeds,andthestabilityofFLAIRisalsoaconcernwhenchangesorenhancementsaremadetoit.Systeminstabilityintroducessignificantoperationalrisk(i.e.,systemdowntime).

Ascalable,flexibleandmaintainablefinancialmanagementsystemisamustforanenterprisethesizeofFlorida.

Itiscriticalthego‐forwardrecommendationaddressesthecurrentFLAIRlimitations,achievesthedefinedsolutiongoals,andsupportstheCFOandDFSinperformingtheirmission.

FloridaDepartmentofFinancialServices FLAIRStudy Chapter1:Page2

1.1 FLAIRSTUDYPURPOSE

TheFLAIRStudywasconductedinaccordancewithprovisointhe2013GAArequiringtheDepartmenttoanalyzefutureoptionsfortheFLAIRsubsystem.Theprovisodirectedthefollowingoptionsbeanalyzed:

5. EnhanceFLAIR6. ReplaceFLAIR7. ReplaceFLAIRandCMS8. ReplaceFLAIR,CMS,MFMPandPeopleFirst

Theoutcomeofthisstudywillbe1)arecommendationtoreplaceorenhanceFLAIRandanassessmentofthefeasibilityofimplementinganERPsystemfortheStateofFloridaand2)acurrentinventoryofallagencybusinesssystemsinterfacingwithFLAIR(theInventory).

1.1.1 PROJECTSCOPE

TheFLAIRStudyadherestotherequirementssetforthinthe2013GAAProvisoandinSection287.0571(4),F.S.Scopeitemsinclude:

PrepareaninventoryofagencybusinesssystemsinterfacingwithFLAIR

AssesstheadvantagesanddisadvantagesofenhancingFLAIR

Assesstheadvantagesanddisadvantagesofreplacing:

o FLAIR(Departmental,Central,IW,andPayrollcomponents)

o FLAIRandCMS

o FLAIR,CMS,MFMP,andPeopleFirst

AssessthefeasibilityofimplementinganERPsystemfortheStateofFlorida

IdentifyanyspecificchangesneededintheFloridaStatutesandtheState’sfinancialbusinesspracticestofacilitatetherecommendedoption

Performastudyofthevariousgo‐forwardoptions,provideago‐forwardrecommendation,andprepareafinalreporttitled“FLAIRStudy”

Completeanddeliverthefollowingbudgetscheduleswithinformationobtainedaspartofthestudywhererequired:

o ScheduleIV‐B–InformationTechnologyProjects

o ScheduleXII–OutsourcingorPrivatizationofaServiceorActivity(ifapplicable)

o ScheduleXIIA,1‐3–Cost/BenefitAnalysis

ThefollowingitemsareoutofscopefortheFLAIRStudy:

Implementationofanyagencysystemenhancementsorreplacementsystems(i.e.,agencybusinesssystems,agencyfinancialsystems,oragencyfinancialreportingsystems)

FloridaDepartmentofFinancialServices FLAIRStudy Chapter1:Page3

TechnicalassessmentofanyFFMISsubsystemorotherStatebusinesssystemsbeyondanythingrequiredinSection287.0571,F.S.andinstructionsforFlorida’sScheduleIV‐BforFiscalYear2014‐15

Businessprocessanalysisanddevelopmentoffunctionalandnon‐functionalrequirementsforanyFFMISsubsystemsorotherStatebusinesssystemsbeyondanythingrequiredinSection287.0571,F.S.andinstructionsforFlorida’sScheduleIV‐BforFiscalYear2014‐15

IdentificationorimplementationofoperationalandprocessimprovementsforDFSoranyotheragencybusinesssystemorfunctionalprocess

Initiationorimplementationofanypolicyandlegalauthoritychanges

1.1.2 FLAIRSTUDYAPPROACH

TheFLAIRStudyemployedaphasedapproach(Exhibit1‐2:FLAIRStudyApproach).Thisapproachallowedforinformationtobegleanedinastructured,objectivemanner,resultinginthedevelopmentoftwoprimarydeliverables:

AbusinesscasestudyonthealternativesfortheFLAIRsubsystemandafinalrecommendationtoreplaceorenhanceFLAIR,includinganyScheduleIV‐B(asrequired)

Aninventory(describedinSection1.4.1)ofagencybusinesssystemsidentifyingthenumberoffinancialmanagementrelatedsystems,outsideofFLAIR,inexistenceacrosstheStateprovidinganindicatorofhowagenciesarecompensatingforFLAIRlimitations

Exhibit1‐2:FLAIRStudyApproach

FloridaDepartmentofFinancialServices FLAIRStudy Chapter1:Page4

1.2 FFMISOVERVIEW

TheFFMISAct,establishedinJuly1997,authorizedinSections215.90‐215.96,F.S.,wasestablishedtoplan,toimplement,andtomanageaunifiedinformationsystemforfiscal,management,andaccountingsupportfortheState’sdecisionmakers.TheFFMISActhasthefollowinggoals:7

Strengthenandstandardizemanagementandaccountingprocedures

Strengtheninternalcontrols

Enablethepreparationofobjective,accurate,andtimelyfiscalreports

Reportonthestewardshipofofficialswhoareresponsibleforpublicfundsorproperty

Providetimelyandaccurateinformationfordecisionmaking

TheFFMISActestablishedtheState’sfinancialmanagementinformationsystemknowncommonlybythesamenamesake,FFMIS.FFMISiscomprisedofLAS/PBS,CMS,PeopleFirst,MFMP,andFLAIR.AnillustrationoftheFFMIStopographyisincludedbelowinExhibit1‐3.

Exhibit1‐3:FFMISTopography

7ListedgoalsareasynopsisofSection215.91(1‐3),F.S.

FloridaDepartmentofFinancialServices FLAIRStudy Chapter1:Page5

EachFFMISsubsystemhasastatutorilyidentifiedfunctionalowneraswellasadditionalstatutoryrequirementsasfollows:

LAS/PBS–TheExecutiveOfficeoftheGovernor(EOG)isthefunctionalowner.Thesystemmustbedesigned,implementedandoperatedpursuanttoChapter216,F.S.

CMS–TheCFOisthefunctionalowner.Thesystemmustbedesigned,implementedandoperatedpursuanttoChapters17and215,F.S.

PeopleFirst–TheDepartmentofManagementServices(DMS)isthefunctionalowner.Thesystemmustbedesigned,implementedandoperatedpursuanttoChapter110.116,F.S.

MyFloridaMarketPlace–DMSisthefunctionalowner.Thesystemmustbedesigned,implementedandoperatedpursuanttoChapter287,F.S.

FLAIR–DFSisthefunctionalowner.Thesystemmustbedesigned,implementedandoperatedpursuanttoChapters17,110,215,216,and287,F.S.

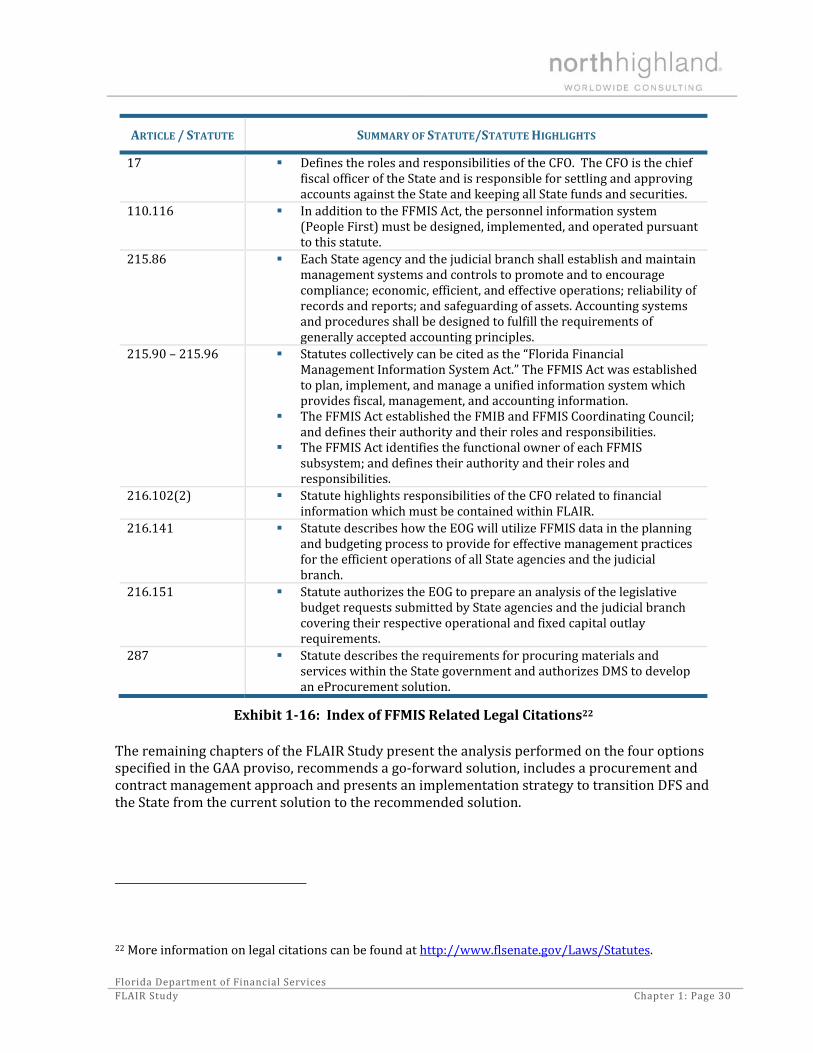

Thefunctionalownerforeachsubsystemisresponsibleformanaging,maintainingandrespondingtothedynamicdemandsofStategovernmentwithintheFFMISframework.AsummaryofrelevantFFMISstatutesisincludedinSection1.6,IndexofFFMISRelatedLegalCitations.

1.2.1 FFMISGOVERNANCESTRUCTURE

TheFFMISActestablishestheFFMISgovernancestructure.FFMISisgovernedbyaFinancialManagementInformationBoard(FMIB,Board)andaFFMISCoordinatingCouncil(FFMISCouncil).TheBoardincludesthe:

Governor,astheChair

CFO

CommissionerofAgriculture

AttorneyGeneral

TheFMIBhasoverallresponsibilityformanagingandoverseeingthedevelopmentofFFMIS,includingestablishingfinancialmanagementpoliciesandproceduresforexecutivebranchagencies.TheFMIBisnotrequiredtomeetatanyspecificfrequency,andtheGovernorortheCFOmaycallameetingoftheBoardatanytimetheneedarises.

TheFFMISCounciliscomposedofthefollowingindividualsortheirdesignees:

TheCFO,astheChair

CommissionerofAgriculture

TheDMSSecretary

TheAttorneyGeneral

TheDirectorofOfficeofPolicyandBudget

FloridaDepartmentofFinancialServices FLAIRStudy Chapter1:Page6

TheAuditorGeneral(non‐votingmember)

TheStateCourtsAdministrator(non‐votingmember)

AnexecutiveofficeroftheFloridaAssociationofStateAgencyAdministrativeServicesDirectors(non‐votingmember)

AnexecutiveofficeroftheFloridaAssociationofStateBudgetOfficersordesignee(non‐votingmember)

TheFFMISCouncilisrequiredbylawtomeetatleastannually.TheprimaryresponsibilityoftheCouncilistoreviewandtorecommendtotheBoardsolutionsandpolicyalternativestoensurecoordinationbetweenfunctionalownersofthevariousFFMISsubsystemstotheextentnecessarytounifyallthesubsystemsintoafinancialmanagementinformationsystem.AdditionaldutiesoftheFFMISCouncilinclude:

Conductstudiesandestablishcommittees,workgroups,andteamstodeveloprecommendationsforrules,policies,procedures,principles,andstandardstotheBoardasnecessarytoassisttheBoardinitseffortstodesign,toimplementandtoperpetuateafinancialmanagementinformationsystem

RecommendtotheBoardsolutions,policyalternatives,andlegislativebudgetrequestissuestoensureaframeworkforthetimely,positive,preplanned,andprescribeddatatransferbetweeninformationsubsystems

TorecommendtotheBoardsolutions,policyalternatives,andlegislativebudgetrequestissuestoensuretheavailabilityofdataandinformationtosupportStateplanning,policydevelopment,management,evaluation,andperformancemonitoring

ToreporttotheBoardallactionstakenbytheCouncilforfinalaction

ToreviewtheannualworkplansofthefunctionalownerinformationsubsystemsbyOctober1ofeachyear.ThereviewistoassessthestatusofFFMISandthefunctionalownersubsystems.TheCouncil,aspartofthereviewprocess,maymakerecommendationsformodificationstothefunctionalownerinformationsubsystemsannualworkplans

1.2.2 PLANNINGANDBUDGETINGSUBSYSTEM(LAS/PBS)LAS/PBSistheState’sbudgetingandappropriationsubsystem.LAS/PBSisusedfordeveloping,preparing,analyzing,andevaluatingagencybudgetrequests.EOG’sOfficeofPolicyandBudget(OPB)usesLAS/PBStodeveloptheGovernor’sbudgetrecommendationsandtoallocateandtocontroltheappropriations.TheLegislatureusesthesubsystemtocreatetheappropriationsbills,includingtheprovisoandothercontrollinglanguageusedtodocumentlegislativeintentandcreatethefoundationtoenabletheagenciestomanageandperformlegislativelyauthorizedorrequiredservicesandactivitiesconsistentwithsuchlegislativeintent.ThebudgetingandappropriationsprocessproducestheGAAanditssupplementsandamendments.

FloridaDepartmentofFinancialServices FLAIRStudy Chapter1:Page7

1.2.3 CASHMANAGEMENTSUBSYSTEM(CMS)

TheTreasuryreceivesanddisbursescash,investsavailablebalances,andperformsrelatedaccountingfunctions,cashmanagementoperations,andconsultations.TheTreasuryoperatesseparateapplicationsknowncollectivelyasCMStocarryoutitsresponsibilitiesofmonitoringcashlevelsandactivitiesinStatebankaccounts,forkeepingdetailedrecordsofcashtransactionsandinvestmentsforStateagencies,andpayingofwarrantsandotherpaymentsissuedbytheCFO.CMSinterfaceswithCentralFLAIR,DepartmentalFLAIR,DepartmentofRevenuesystems,otherStateagencysystems,FLAIRIW,andbankbusinesspartnersystems.

TheTreasuryisintheprocessofupgradingthecurrentCMSplatformtoaweb‐basedsystem.Theupgradewilloccurintwophases.Phase1wentliveinAugust2013andestablishedanewintegratedplatformandreplacedthreeexistingbusinessapplicationsincludingVerifies,Receipts,andChargebacks.Phase2willreplacetheremainingCMSsubsystemapplicationsandaddthecapabilitiestothenewintegratedCMSplatformdevelopedinPhase1.8Phase2isscheduledtoimplementinstagesfrom2014through2018.

1.2.4 PERSONNELINFORMATIONSUBSYSTEM(PEOPLEFIRST)

PeopleFirstisaself‐service,secure,web‐basedpersonnelinformationsystemcomprisedofthefollowingmodules:payrollpreparation,timeandattendance,recruitment,benefitsadministration,humanresourcesmanagement,andorganizationalmanagement.Itisusedbyemployees,managers,retirees,jobapplicants,andStatehumanresources(HR)staff.Thesystemcurrentlysupportsmorethan200,000StateandUniversityusers.

DMSoutsourcedtheState’spersonnelfunctiontoNorthgateArinso,Inc.(NGA).ThecurrentcontractexpiresonAugust20,2016andhasanannualvalueover$36million.9

SAPsoftwareisthecurrentplatformforPeopleFirst.NGAhasperformedmorethan17,000customizationstothesystemplatformandwebapplicationservers,and588interfaceshave

8RemainingCMSapplicationstobereplacedinPhase2include:FundAccounting,BankAccounts,StateAccounts,Dis‐investments,InvestmentAccountingSystem,ConsolidatedRevolvingAccount,andSpecialPurposeInvestmentAccounts.AdescriptionofeachbusinessapplicationcanbefoundintheChapter1Appendix.9PeopleFirstContract.

FloridaDepartmentofFinancialServices FLAIRStudy Chapter1:Page8

beenbuilttoexchangedatabetweenthePeopleFirstsystemandexternalsystems(e.g.,FLAIR,universitypersonnelsystems,insurancecarriers).ThesystemstreamlinesandautomatesmanyoftheState’sHRfunctions,andpromotespaperlessworkprocesses(e.g.,timesheetsubmission,benefitstransactions,anddirectdeposit).

Inaccordancewithprovisointhe2013GAA,DMSprocuredKPMGtoconductabusinesscasestudytodeterminethebestandmostappropriatehumanresourcemodelforDMStoprocureinafuturecompetitivesolicitation.ThebusinesscasestudywascompletedJanuary31,2014.10

1.2.5 PROCUREMENTSUBSYSTEM(MYFLORIDAMARKETPLACE)

MyFloridaMarketPlaceisasecure,web‐basedprocurementsystem.ItprovidesforStateprocurementstaffandvendorstoexchangeproductsandservices.MFMPallowsvendorstoregisterwiththeStateanddisplayandmanagetheircataloguesonline.BuyersuseMFMPtofindproducts,placeorders,approvepurchases,reconcileinvoicesandapprovepaymentallwithinonesystem.Procurementpersonnelcancreatesolicitationsinthesourcingmodulewhiletheanalyticsmoduleprovidesspendanalysisandreporting.ThesystemservesStateandvendorusersandsupportsabroadarrayofprocurementcapabilities.

DMSandAccenture,LLPexecutedacontractonOctober9,2002toimplementanAribaprocurementsolutionfortheStateofFlorida.TheStateofFloridaAribaapplication,knownasMFMP,isaCOTSpackagewithover300customizations.Thelargestshareofthecustomizations(28%)wasrequiredtointerfacewiththeState’saccountingsystem,FLAIR.11MFMPhasover13,000Stateusersandnearly100,000registeredvendors.

ThecurrentMFMPcontractissettoexpireonJanuary31,2017andhasoptionsforrenewal;theannualvalueofthecontractisover$10million.12

10January31,2014KPMGPeopleFirstBusinessCase.11MyFloridaMarketPlaceBusinessCaseoftheeProcurementSolutions,August2011.12MFMPContract.

FloridaDepartmentofFinancialServices FLAIRStudy Chapter1:Page9

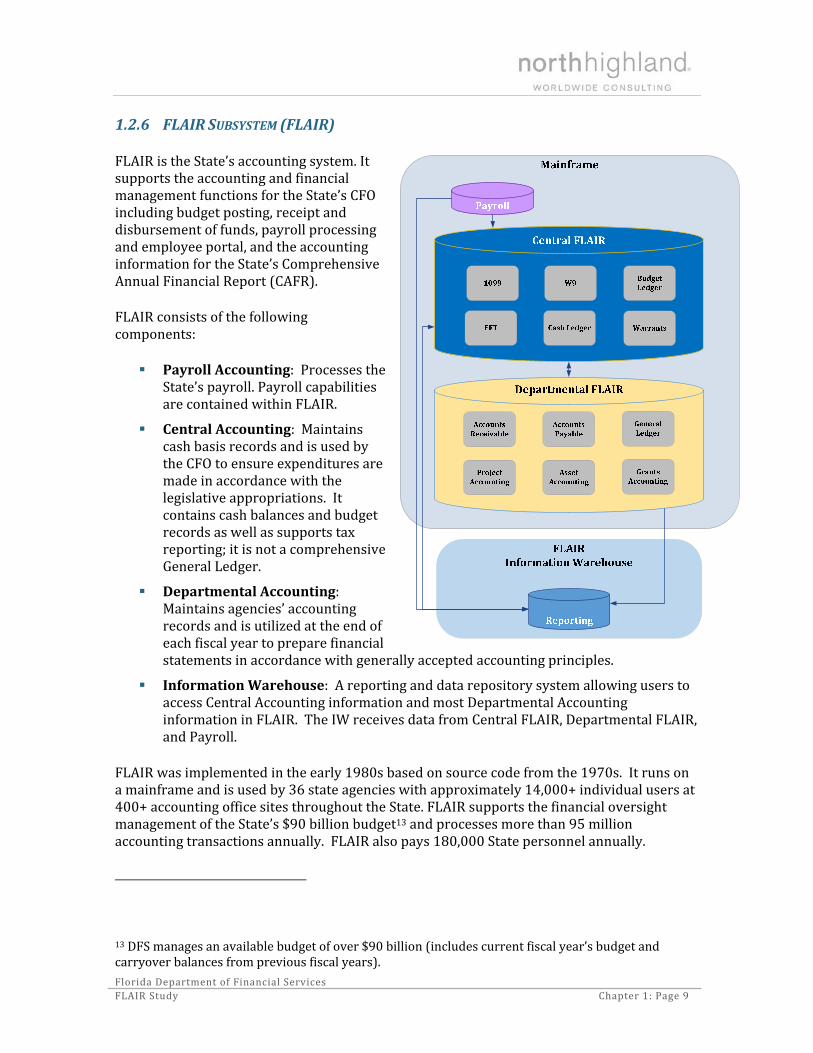

1.2.6 FLAIRSUBSYSTEM(FLAIR)

FLAIRistheState’saccountingsystem.ItsupportstheaccountingandfinancialmanagementfunctionsfortheState’sCFOincludingbudgetposting,receiptanddisbursementoffunds,payrollprocessingandemployeeportal,andtheaccountinginformationfortheState’sComprehensiveAnnualFinancialReport(CAFR).

FLAIRconsistsofthefollowingcomponents:

PayrollAccounting:ProcessestheState’spayroll.PayrollcapabilitiesarecontainedwithinFLAIR.

CentralAccounting:MaintainscashbasisrecordsandisusedbytheCFOtoensureexpendituresaremadeinaccordancewiththelegislativeappropriations.Itcontainscashbalancesandbudgetrecordsaswellassupportstaxreporting;itisnotacomprehensiveGeneralLedger.

DepartmentalAccounting:Maintainsagencies’accountingrecordsandisutilizedattheendofeachfiscalyeartopreparefinancialstatementsinaccordancewithgenerallyacceptedaccountingprinciples.

InformationWarehouse:AreportinganddatarepositorysystemallowinguserstoaccessCentralAccountinginformationandmostDepartmentalAccountinginformationinFLAIR.TheIWreceivesdatafromCentralFLAIR,DepartmentalFLAIR,andPayroll.

FLAIRwasimplementedintheearly1980sbasedonsourcecodefromthe1970s.Itrunsonamainframeandisusedby36stateagencieswithapproximately14,000+individualusersat400+accountingofficesitesthroughouttheState.FLAIRsupportsthefinancialoversightmanagementoftheState’s$90billionbudget13andprocessesmorethan95millionaccountingtransactionsannually.FLAIRalsopays180,000Statepersonnelannually.

13DFSmanagesanavailablebudgetofover$90billion(includescurrentfiscalyear’sbudgetandcarryoverbalancesfrompreviousfiscalyears).

FloridaDepartmentofFinancialServices FLAIRStudy Chapter1:Page10

ThelastsignificantfunctionalupgradetoFLAIRoccurredinthelate90’swiththeadditionofthePurchasingCard(P‐card)functionality.Otherwise,FLAIRhasnotbeensignificantlyupgradedinthecontextofmodernizingthecoremodules.

1.2.7 PROJECTASPIRE

TheStateofFloridabegananefforttoupgradeandmodernizeitscoreoperationalsoftwareandITinfrastructure,specificallyitsaccounting,cashmanagement,procurementandhumanresourcesfunctions,inFebruary2000.AstudywascompletedbyKPMGandprovidedhigh‐leveldirectionforhowtheStatecouldachievethisgoal.Thecoreoftherecommendationwasa“bestofbreed”approachpromotingspecializedapplicationsratedhighlyinspecificfunctionalareasandwouldalsosupportenterprisewideintegration.Thestudyspawnedthreeinitiatives:MFMP,PeopleFirst,andProjectAspire.ProjectAspirewastheprojecttomodernizetheState’sfinanceandaccountingsubsystems,FLAIRandCMS.SomeoftheoriginalgoalsofProjectAspirewereto:

ModernizeandunifytheState’saccountingandcashmanagementplatforms

Createanenterpriseintegrationarchitecturetoallowotherbusinesssystemcomponents(i.e.,Personnel,payroll,LAS/PBS,andeProcurement)tobeintegrated

EstablishflexiblefunctionalityandbeabletosupporttheneedsoftheStatewithminimalornomodifications

Maintainmeaningfulmanagementinformationfordecisionmakers

Eliminate,totheextentpossible,agency‐specificsystemsbuilttoperformcriticalaccountingfunctionsnotavailableinFLAIR

Afterconductingaprocurementforcombinedsoftwareandimplementationservicesinlate2002,DFSselectedBearingPointtoimplementthePeopleSoftsoftwarepackage.TheBearingPointcontractwasforasix‐yeartermfromAugust27,2003toOctober1,2009.Theprojectexperiencedsignificantchallenges.OnMay17,2007,aftercompletingdesignanddevelopment,Aspirewassuspendedduringtestingduetosignificantconcernswithitsabilitytodeploysuccessfully.

GiventhestrongsimilaritiesbetweenProjectAspireandtheintentoftheFLAIRStudyrecommendation,itisimportanttoincludekeystrengthsandlessonslearnedfromAspireintofutureplans.Thestrengthsandlessonslearned,gleanedfromfirsthanddiscussionswithProjectAspireteammembersandtwoStatesponsoredprojectlessonslearnedsessions14,areidentifiedbelowandhavebeenincorporatedintotheFLAIRStudy(seeExhibit1‐4:ProjectAspireStrengthstoReplicateandExhibit1‐5:ProjectAspireLessonsLearned).

14GartnerProjectAspireEvaluation,May2007;andCouncilonEfficientGovernment:ReporttotheGovernoronMyFloridaMarketPlace,PeopleFirstandProjectAspire,January2008.

FloridaDepartmentofFinancialServices FLAIRStudy Chapter1:Page11

PROJECTASPIRESTRENGTHS WHEREINCORPORATEDINFLAIRSTUDY

AgencyEngagementandCommunication: Eachagencyhadaliaisontotheproject,was

supportedbyanactiveagencyadvocacygroup,andwasabletoprovidebusinessrequirements

Projectteamestablishedstrongprojectcommunicationpractices(projectwebsite,regularprojectNewsletter,regularmeetingswithliaisons,andprojectstatusreports)

Chapter4:ImplementationStrategy ProjectPlanning ChangeManagement

GovernanceStructure: Astronggovernancestructurewasinstitutedon

Aspireandrolesandresponsibilitiesweredefinedforeachlayerofthegovernancestructure;however,thecompositionoftheseniorleadershipwasproblematic(seeProjectAspireWeaknessesbelow)

Chapter3: Recommendation GovernanceStructure

Chapter4:ImplementationStrategy ProjectGovernance/Project

ManagementOffice

ContractManagement: Contracttermswithvendorwererigidand

enabledtheStatetowithholdpaymentwhendeliverableswerenotmet

ThecontractenabledDFStorebuffthevendor’srequesttoswitchfromafixedfeecontracttoatimeandmaterial(T&M)contract

Chapter5:ProcurementandContractManagement

PerformanceStandards

Exhibit1‐4:ProjectAspireStrengthstoReplicate

Theexhibit(Exhibit1‐5)belowfocusesonweaknessesinProjectAspireandwheretheyareincorporatedintotheFLAIRStudy:

PROJECTASPIREWEAKNESSES WHEREINCORPORATEDINFLAIRSTUDY

GovernanceandSteeringCommitteeComposition: Didnotholdallmembersaccountabletotheir

responsibilitiesandescalatesituationswherememberswerenotmeetingexpectations

DidnotidentifySteeringCommitteememberswithrelevantoperationalexperienceandwhowereableto“diveintodetails”sodecisionswerewellfounded

DidnotensureSteeringCommitteewasmakingtimelydecisionsandhadtheauthoritytomakeandenforcedecisionsrelatedtothedesign,development,implementationandrolloutoftherecommendedsolution

Chapter3:Recommendation GovernanceStructure

Chapter4:ImplementationStrategy ProjectGovernance/Project

ManagementOffice

Future‐StateVision: Didnotdefineaclearvisionforthefuture‐state

financialenvironmentandalignwithkeystakeholders(FMIB,FFMISCouncil,andkeyagencies)toensurealignmentandtheirsupport

Chapter1:Background SolutionGoalsandBenefits

Chapter4:ImplementationStrategy TransitionPlan

FloridaDepartmentofFinancialServices FLAIRStudy Chapter1:Page12

PROJECTASPIREWEAKNESSES WHEREINCORPORATEDINFLAIRSTUDY

ProcessStandardization/MinimizeCustomization: Didnotaggressivelypromoteprocessre‐

engineering/standardizationandopposecustomizationofsoftwaretomatchexistingbusinessprocessestoreduceimplementationcomplexityandpromoteoperationalefficiencyandconsistencyacrosstheState

Chapter3:Recommendation GovernanceStructure

Chapter4:ImplementationStrategy BusinessProcessRe‐

engineeringChapter5:ProcurementandContractManagement

PerformanceStandardsDisciplinedProcurement:

Didnotdefineandfollowadisciplinedandstructuredprocurementstrategyandapproachtoensureallappropriateduediligencewascompletedandawell‐informedpurchasedecision(s)couldbemade

DidnotdocumentvendorperformancemeasurestoenabletheStatetogaugeprogressobjectivelyandholdthevendoraccountabletoestablishedmilestonesandprojectrequirements

Chapter5:ProcurementandContractManagement

ProcurementApproachandStrategy

QualifiedandExperiencedImplementationTeam: Didnotestablishclearexpectationsaroundtheroles

andresponsibilitiesofallprojectteammemberstoreduceambiguityandgreateralignment

Didnotholdprojectteammembersaccountablefortheirwork;andaddressresourceandskillissuesaggressivelytominimizeimpacttothebroaderproject

Chapter4:ImplementationStrategy ProjectPlanning(Project

Governance)Chapter5:ProcurementandContractManagement

ProcurementApproachandStrategy

Exhibit1‐5:ProjectAspireWeaknesses

1.3 CURRENTSTATEPERFORMANCE

Anobjectivemethodtoassessthecurrentperformanceofafinancialmanagementsystemistoreviewrelevantperformancemetrics.Keyperformancemetricsallowforcomparisonsoflikebusinessfunctionstobemadeacrossindustriesandorganizationsofdifferentsizes.Trackingandreportingonkeyperformancemetricsisonewayorganizationscanevaluatetheiroperationalefficiencyandeffectivenessovertimeaswellasidentifyoperationalprocessestofocusimprovementeffortsupon.

ThedataproducedtodayaboutFLAIRandCMSandthefunctionstheysupportarenotkeyperformancemetrics,rathertheyarevolumestatisticstoindicatethesheernumberandtypeoftransactionsflowingthroughthesystem.ThesevolumemeasuresarenotoptimizedtosupportDFSoragencymanagementdecisionmakingnordotheyallowforoperationalperformancetobeassessed.ExamplesofsomeofthetransactionvolumemeasurescapturedcanbefoundinExhibit1‐6.

FloridaDepartmentofFinancialServices FLAIRStudy Chapter1:Page13

BUSINESSFUNCTION FLAIRSTATISTICS15

AccountsPayable(AP) NumberofWarrantsPrinted=8million NumberofEFTPayments=6.7million NumberofPurchasingCardPayments=700,000 Numberof1099sReported=12,000‐14,000

AccountsReceivable(AR) 54,801ARrecordscreated 25AgenciesrecordARrecords

FinancialStatements TimetoPrepareCAFR =7‐9monthsPayroll PercentofPayrollbyDirectDeposit=96%FinanceFunctionOverall AccountingTransactions=~95million

NumberofUsers=~14,000+ NumberofRecordsinDataWarehouse=1.2billion

TaxReporting NumberofW9Records=~80,000FundsManagement NumberofDepositsProcessed=740,612

AmountofDepositsProcessed=$83.48billion AmountofInterestApportionedtoGeneralRevenue=

$103.5Million

Exhibit1‐6:CurrentFLAIRandCMSStatistics

Floridaisnotaloneinitsabsenceofgeneratingandtrackingoperationalperformancemetrics.Aspartofthisstudy,interviewswereconductedwithsevenotherstates,includingVirginia,Georgia,Pennsylvania,NewYork,Alabama,TexasandOhio.Noneofthestatesinterviewedcurrentlyproduceoperationalperformancemetrics.

DuringthePre‐Design,DevelopmentandImplementationphase(Pre‐DDI)describedinChapter4:ImplementationStrategyandincludedaspartofthebusinessprocessre‐engineeringefforts,itisrecommendedDFSestablishabaselinesetofoperationalperformancemetrics.ThesebaselinemetricsenableDFSandtheStatetoobjectivelyassess(1)themagnitudeofpotentialoperationalimprovementsand(2)operationalimprovementprogress.PotentialoperationalmeasurestoconsiderarecontainedinExhibit1‐7:CommonFinanceandAccountingMetrics.

BUSINESSFUNCTION PERFORMANCECATEGORY POTENTIALPERFORMANCEMETRICS

FinancialReporting

CycleTime ProcessEfficiency ProcessEfficiency

AnnualClose:Daystoclose ManualJournalEntry(JE)percentageof

allJE NumberofFullTimeEquivalents(FTE)

fortheprocessgroup"performfinancialreporting"per$1Billionrevenue

15StatisticsfromFiscalYear2012‐2013.

FloridaDepartmentofFinancialServices FLAIRStudy Chapter1:Page14

BUSINESSFUNCTION PERFORMANCECATEGORY POTENTIALPERFORMANCEMETRICS

AccountsPayable(AP)

ProcessEfficiency

NumberofFTEsfortheprocessgroup"processaccountspayableandexpensereimbursement"per$1Billionrevenue

NumberofAPinvoicesprocessedperAPFTE

AccountsReceivable(AR)

ProcessEfficiency

NumberofFTEsfortheprocessgroup"processaccountsreceivable"per$1Billionrevenue

NumberofremittancesprocessedperARFTE

Payroll CycleTime ProcessEfficiency

Numberofbusinessdaystoprocesspayroll

NumberofFTEsfortheprocessgroup"processpayroll"per$1Billionrevenue

FinanceFunctionOverall

ProcessEfficiency CostEffectiveness

NumberofFinanceFunctionFTEsper$1Billioninrevenue

TotalcosttoperformtheFinanceFunctionperFinanceFunctionFTE

TreasuryManagement

ProcessEfficiency NumberofFTEsfortheprocessgroup"managetreasuryoperations”per$1Billionrevenue

Exhibit1‐7:CommonFinanceandAccountingMetrics16

1.4 LIMITATIONSWITHFLAIRTODAY

Intheabsenceofbeingabletousemetricstoevaluatetheoperationalperformanceofthecurrent‐stateFLAIRsystem,aqualitativeassessmentwascompleted.Thisassessment,leveraginginformationgleanedfromagencyinterviews17anddocumentation,identifiedsignificantchallengesandlimitationswiththecurrentsystem.ThesechallengesandlimitationscanunderminetheState’sabilitytoefficientlyandeffectivelymanageitsfinances,exposingtheStatetooperationalrisk,increasingstatewidemaintenancecosts,andreducingorganizationalproductivityduetoinconsistentbusinessprocesses.

TheidentifiedlimitationsofFLAIRtodayandtheirqualitativeimpactonthebusinessaresummarizedinExhibit1‐8:LimitationswithFLAIRToday.ThefollowingistheLegendforExhibit1‐8.

LEGEND:BusinessImpactScale: ‐Low ‐ Medium ‐High

16Source:AmericanProductivity&QualityCenter(APQC);www.apqc.org.17“Deepdive”interviewswereconductedwiththefollowingagencies:DepartmentofTransportation,DepartmentofRevenue,DepartmentofEnvironmentalProtection,DepartmentofFinancialServices,DepartmentofManagementServices,andDepartmentofChildrenandFamilies.

FloridaDepartmentofFinancialServices FLAIRStudy Chapter1:Page15

FloridaDepartmentofFinancialServices FLAIRStudy Chapter1:Page16

IDENTIFIEDLIMITATION/CHALLENGE IMPLICATION

BUSINESSIMPACT

INCREASEDOPERATIONAL

RISK

DECREASEINOPERATIONALEFFICIENCY/EFFECTIVENESS

INCREASEDCOSTS/LOSTREVENUE

SUBOPTIMALDECISIONMAKING

1.FLAIRdataiscompiledusingMicrosoftAccessandExcelforpreparationoftheFinancialStatements(e.g.,CAFR).

Sourcedataisbeingmanipulatedoutsideofsystemincreasingriskoferrorsbeingintroduced

Effortexpendedtoreconcileandtoconfirmfinancialfiguresincreasestimeandcoststoproducereports

2.FLAIRdoesnotsupportcashforecastingataStatelevel.

Lackofsufficient,reliable,andtimelyinformationresultsinamoreconservativepositionbeingtakenthanisrequiredinfluencingpotentialinvestmentearnings

Lackofsufficient,reliable,andtimelyinformationhindersdecisionmakingandcouldresultinanunfavorableactionbeingtaken

3.FLAIRdoesnotsupporteithertheschedulingorconsolidationofpayments.

Additionaleffortrequiredtosupportpaymentprocess(i.e.,numberofjournalentries)

Stateincursadditionalbankingfeesandcannottakeadvantageoffavorablepaymentterms

4.Accountingtransactionsarenotcapturedataconsistentlevelofdetail.

Differentprocessesandproceduresinuseacrossagenciesincreasesenterprise‐wideoperationalcomplexity

Availabledata/informationcannotbeleveragedinaconsistentmanner

5.CurrentstructureofCentralFLAIRlimitsabilitytointerfaceencumbrancesfromexternalsystems(e.g.,MFMP).

ReducesDFS/CFO’svisibilityintotheState’sliabilitiesandimpactsdecisionmakingrelatedtotheState’scashposition

FloridaDepartmentofFinancialServices FLAIRStudy Chapter1:Page17

IDENTIFIEDLIMITATION/CHALLENGE IMPLICATION

BUSINESSIMPACT

INCREASEDOPERATIONAL

RISK

DECREASEINOPERATIONALEFFICIENCY/EFFECTIVENESS

INCREASEDCOSTS/LOSTREVENUE

SUBOPTIMALDECISIONMAKING

6.FLAIRdoesnotcontainareceiptingfunctiontomanageandtotrackinvoices.

Agencieshaveimplementedworkarounds(i.e.,systems,processes)tosupporttheirARneeds

ItisnotpossibletogetastatewideviewofoutstandingARbalanceshinderingoperationaldecisionmaking

7.CentralandDepartmentalFLAIRdonotreconcilewithoutmanualprocesses.

Additionalagencyeffortandresourcesrequiredtocompletereconciliation

Amanualreconciliationeffortincreaseslikelihoodoferrorsbeingintroduced

8.CMSmustbereconciledwithCentralandDepartmentalFLAIRsincetheyarenotonanintegratedfinancialplatform(FLAIRandCMSarenotintegrated;theyinteractthroughexternalprogramsandfileexchanges).

Additionaleffortandresourcesrequiredtocompletereconciliation

Manualreconciliationeffortsincreaselikelihoodoferrorsbeingintroduced

9.FLAIRdoesnothavefunctionalitytokeepinteragencytransfersinbalance.

Requiresreconciliationefforttoensureagencyaccountsarenotoutofbalance(inparticularatyearend)

10.Warrantscannotbechargedtomorethanoneaccount.

Warrantsrequiring paymentfrommultiplefundsrequirejournaltransfersafterthepaymentisinitiallymadeinordertoallocatethechargecorrectlyresultingineffortbeingexpendedandpotentialerrorsbeingmade

Increasescostwithnumberofwarrants

FloridaDepartmentofFinancialServices FLAIRStudy Chapter1:Page18

IDENTIFIEDLIMITATION/CHALLENGE IMPLICATION

BUSINESSIMPACT

INCREASEDOPERATIONAL

RISK

DECREASEINOPERATIONALEFFICIENCY/EFFECTIVENESS

INCREASEDCOSTS/LOSTREVENUE

SUBOPTIMALDECISIONMAKING

11.FLAIRhaslimitedAsset/InventoryManagementfunctionality(e.g.,barcodereading,track“highinterest”itemswithoutneedingafinancialvalueortrackingdepreciation).

Agencieshaveimplementedtheirownsystemstomanagetheannualassetinventoryprocesswhichincreasesupportcostsandprocesscomplexity

12.ThereisnofunctionalityformanagementorstatewidereportingoftheState’sresources:

Assets Grants Projects Contracts

Oversight,management anddecisionmakingrelatedtoStateresourcesismorechallenging

Manualprocessesandworkaroundsarerequiredtosupportreportingrequirementsandmanageresources(e.g.,developmentandprocessingofcostallocations,identificationofeligible/ineligibleactivities)

13.Reportingcapabilitiesarelimited.Unabletoreportatstatewidelevel(i.e.,amountsduetotheState,vendorspend).

Additionalreportingtools/systemsarebeingusedtoproducereportsincreasingsupport/maintenancecomplexity,costandeffort

Dataismaintainedinmultiplesystemsandnotalwaysdefinedandusedconsistentlyraisingcomplexityinusingthedata/informationeffectively(i.e.,betterpricingtermsbasedonvolume)andincreasingthetimeandefforttocreateneededreports

14.Agenciescannotforecastorprojectdifferentfinancialmodelsorscenariosthroughoutthefiscalyear(i.e.,“whatif”analysis).

Analysistoaddressmanagementquestionsmid‐yearrequiresmanualprocessingandadditionalstaffeffortandtime

FloridaDepartmentofFinancialServices FLAIRStudy Chapter1:Page19

IDENTIFIEDLIMITATION/CHALLENGE IMPLICATION

BUSINESSIMPACT

INCREASEDOPERATIONAL

RISK

DECREASEINOPERATIONALEFFICIENCY/EFFECTIVENESS

INCREASEDCOSTS/LOSTREVENUE

SUBOPTIMALDECISIONMAKING

15.BusinessuserscannotcreateandrunadhocreportswithoutITresourceassistance.

Reportcreationbecomesaprocessneedingmanagement

Timelinessofreportcreationisnotalignedwiththeactualneedfortheinformation

IncreasedcostforITsupporttocollectdataandcreatereports

FloridaDepartmentofFinancialServices FLAIRStudy Chapter1:Page20

IDENTIFIEDLIMITATION/CHALLENGE IMPLICATION

BUSINESSIMPACT

INCREASEDOPERATIONAL

RISK

DECREASEINOPERATIONALEFFICIENCY/EFFECTIVENESS

INCREASEDCOSTS/LOSTREVENUE

SUBOPTIMALDECISIONMAKING

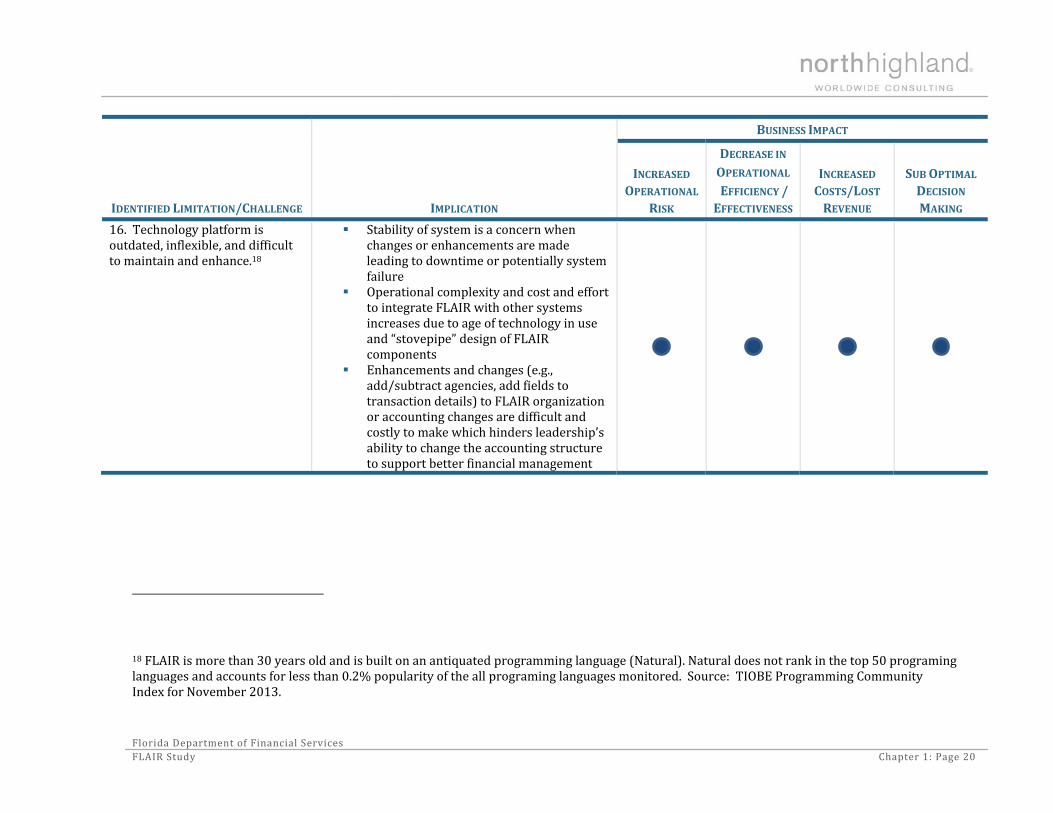

16.Technologyplatformisoutdated,inflexible,anddifficulttomaintainandenhance.18

Stabilityofsystemisaconcernwhenchangesorenhancementsaremadeleadingtodowntimeorpotentiallysystemfailure

OperationalcomplexityandcostandefforttointegrateFLAIRwithothersystemsincreasesduetoageoftechnologyinuseand“stovepipe”designofFLAIRcomponents

Enhancementsandchanges(e.g.,add/subtractagencies,addfieldstotransactiondetails)toFLAIRorganizationoraccountingchangesaredifficultandcostlytomakewhichhindersleadership’sabilitytochangetheaccountingstructuretosupportbetterfinancialmanagement

18FLAIRismorethan30yearsoldandisbuiltonanantiquatedprogramminglanguage(Natural).Naturaldoesnotrankinthetop50programinglanguagesandaccountsforlessthan0.2%popularityoftheallprograminglanguagesmonitored.Source:TIOBEProgrammingCommunityIndexforNovember2013.

FloridaDepartmentofFinancialServices FLAIRStudy Chapter1:Page21

IDENTIFIEDLIMITATION/CHALLENGE IMPLICATION

BUSINESSIMPACT

INCREASEDOPERATIONAL

RISK

DECREASEINOPERATIONALEFFICIENCY/EFFECTIVENESS

INCREASEDCOSTS/LOSTREVENUE

SUBOPTIMALDECISIONMAKING

17.FLAIRlacksnecessaryfunctionalitytosupporttheconstructionofcostallocationsessentialforagenciestoallocatecostsrequiredbynumerousgrantprograms.

Agenciesuseworkarounds(i.e.,manualprocessesorexternaltools/systems)togeneraterequiredcostallocationsandmeetreportingrequirements

Oncecalculatedcostallocationsneedtobere‐enteredintoDepartmentalFLAIRexposingagenciestomanualentryerrorsoradditionalreconciliation

18.ThedesignofFLAIRresultsinfourcashbalancesbeingmaintainedandmanaged(onebankbalanceandthreebookbalances(CMS,CentralandDepartmental)).

Monitoringmultiplecashbalancesrequiresadditionalstaffandmanagementattentionandreducesoperationalfocus

Significanteffortrequiredtokeepcashbalancesreconciled

Entryforerrorofmultiplebookbalancestoreconcile

19.ThedesignofFLAIRresultsinpayrollprocessingactivitiesbeingcompletedinmultipleseparateapplications(PeopleFirst,Payroll,CentralandDepartmentalFLAIR).

Reconciliationeffortsarerequiredbetweensystemsandoperationalcomplexityincreasessincepayrollrelatedcalculationsandactivitiesarebeingcompletedinmultiplesystems

Note:PeopleFirstcontainspayrollcapabilitiescurrentlysuppressedandbeingcompletedbyFLAIRPayroll

20.FLAIRdoesnotsupportworkflow/electronicdocuments.