finpro digital africa growth program pre study for kenya - 26052015

TRANSCRIPT

Finpro Digital Africa Growth Program Pre-study: Kenya Market study on opportunities in Kenya for Finnish ICT companies within the sectors of banking and financial services, telecommunications and cyber security

Finpro Digital Africa Growth Program Pre-study: Kenya

2 of 42

Content index:

1 BANKING AND FINANCIAL SERVICES SECTOR ..................................... 5

1.1 Summary ............................................................................................................................................ 5 1.2 Introduction ....................................................................................................................................... 6 1.3 Nature of the market and market size for technology solutions .............................................. 7 1.4 Structure of the market ................................................................................................................... 7

1.4.1 Banks................................................................................................................................................... 7 1.4.2 Savings and Credit Cooperatives (SACCOs) .................................................................................... 7 1.4.3 Mobile Money ...................................................................................................................................... 8 1.4.4 Insurance companies ........................................................................................................................ 8 1.4.5 Money remittance services (from diaspora) ................................................................................... 9

1.5 Overview of companies and products ........................................................................................... 9 1.5.1 Agent banking .................................................................................................................................... 9 1.5.2 Islamic banking .................................................................................................................................. 9 1.5.3 Credit Reference Bureaus (CRBs) .................................................................................................. 10 1.5.4 Deposit Taking Microfinance Institutions ...................................................................................... 10 1.5.5 Revised Prudential and Risk Management Guidelines ................................................................. 10 1.5.6 African Trade Insurance Agency (ATI) products ............................................................................ 10 1.5.7 Key industry players ......................................................................................................................... 10

1.6 Market size....................................................................................................................................... 11 1.7 Competition ..................................................................................................................................... 11 1.8 SWOT analysis ................................................................................................................................. 12

1.8.1 Strengths .......................................................................................................................................... 12 1.8.2 Weakness .......................................................................................................................................... 12 1.8.3 Opportunities .................................................................................................................................... 13 1.8.4 Threats .............................................................................................................................................. 13

2 TELECOMMUNICATIONS INDUSTRY IN KENYA ................................. 14

2.1 Summary .......................................................................................................................................... 14 2.2 Nature of the market and market size for technology solutions ............................................ 14 2.3 Structure of Kenya’s ICT market .................................................................................................. 16

2.3.1 Fixed Telephony - Monopoly ........................................................................................................... 18 2.3.2 Mobile Telephony - Oligopoly .......................................................................................................... 18 2.3.3 Internet/data - Perfect competition .............................................................................................. 18

2.4 Product and services: .................................................................................................................... 19 2.5 Key players, value chain and business models .......................................................................... 19

2.5.1 International network facility providers: ........................................................................................ 19 2.5.2 Internet/Data Market ....................................................................................................................... 20 2.5.3 Mobile telephony market ................................................................................................................. 21 2.5.4 Fixed telephony market ................................................................................................................... 21 2.5.5 Mobile money transfer service ........................................................................................................ 21

2.6 Value chain & business models .................................................................................................... 21 2.7 Estimated market size and value ................................................................................................. 22 2.8 Competition ..................................................................................................................................... 24 2.9 SWOT analysis ................................................................................................................................. 25

Finpro Digital Africa Growth Program Pre-study: Kenya

3 of 42

2.10 Challenges and needs, and the resulting opportunities .......................................................... 26 2.10.1 Potential opportunities stemming from these needs .................................................................. 28

2.11 Buying process and decision making .......................................................................................... 31 2.12 Entry strategy and partners .......................................................................................................... 31

3 CYBER SECURITY IN KENYA ............................................................. 33

3.1 Summary .......................................................................................................................................... 33 3.2 Introduction ..................................................................................................................................... 34 3.3 Laws and regulations ..................................................................................................................... 34 3.4 Top threats in 2013 ........................................................................................................................ 34

3.4.1 Insider threats .................................................................................................................................................. 34 3.4.2 VoIP PBX fraud .................................................................................................................................................. 35 3.4.3 Social media ...................................................................................................................................................... 35 3.4.4 Denial of service attacks ............................................................................................................................... 35 3.4.5 Botnet attacks .................................................................................................................................................. 35 3.4.6 Online and mobile banking ............................................................................................................................ 35 3.4.7 Mobile money fraud ......................................................................................................................................... 35 3.4.8 Cyber espionage ............................................................................................................................................... 35

3.5 Threat landscape analysis ............................................................................................................ 36 3.6 Criminal activity .............................................................................................................................. 36 3.7 Structure and size of the market ................................................................................................. 37 3.8 Nature of the market value chain ................................................................................................ 37 3.9 Overview of key companies and organizations .......................................................................... 38 3.10 Buying process and decision making .......................................................................................... 39 3.11 Business models ............................................................................................................................. 39 3.12 SWOT analysis ................................................................................................................................. 40 3.13 Challenges ....................................................................................................................................... 40 3.14 Business needs ............................................................................................................................... 41 3.15 Opportunities .................................................................................................................................. 41 3.16 Entry strategy and partners .......................................................................................................... 41

Finpro Digital Africa Growth Program Pre-study: Kenya

4 of 42

CONTACT DETAILS For communication concerning this report please contact: GrowthAfrica: Contact person: Address Lenana Towers 843, Ian Lorenzen 5th floor, Lenana Road Business Facilitator & Partner Nairobi, Kenya Email: [email protected] Email: [email protected] Website: www.growthafrica.com Mobile: +254 731513951

ABBRIVIATIONS

ARPU ‐ Average Revenue Per User ASP ‐ Applications Service Provider ATI ‐ African Trade Insurance Agency BPO ‐ Business Process Outsourcing CAGR ‐ Compound Annual Growth Rate CBK ‐ Commercial Bank Of Kenya CCK/CA ‐ Communications Authority Of Kenya CRB ‐ Credit Reference Bureau CSP ‐ Content Service Provider DTM ‐ Deposit Taking Microfinance Institution DTS ‐ Deposit Taking Saccos EAASy ‐ Eastern Africa Submarine Cable System EABS ‐ East African Building Society EIB ‐ European Investment Bank FttH ‐ Fibre to the Home GDP ‐ Gross Domestic Product GSM ‐ Global System for Mobile communication ICT‐ Information Communication And Technology IDC ‐ Industrial Development Corporation IFMIS ‐ Integrated Financial Management Information System IPTV ‐ Internet Protocol Television ISP ‐ Internet Service Provider IXP ‐ Internet Exchange point KENET ‐ Kenya Education Network KIXP ‐ Kenya Internet Exchange Point

LION ‐ Lower Indian Ocean Network LTE ‐ Long Term Evolution MNC ‐ Multinational Corporation MNO ‐ Mobile Network Operator MVNO ‐ Mobile Virtual Network Operator NFP ‐ Network Facilities Provider NOFBI ‐ National Optic Fibre Backbone Infrastructure PBX ‐ Private Branch Exchange PDCC ‐ Public Data Communications Carrier SACCO ‐ Savings And Credit Cooperative SASRA ‐ Sacco Society Regulatory Authority SIM ‐ Subscriber Identity Module SME ‐ Small And Medium‐Sized Enterprises TESPOK ‐ Telecommunication Service Providers Association Of Kenya ULF ‐ Unified Licencing Framework VAR ‐ Value Added Reseller VOIP ‐ Voice Over IP VPN ‐ Virtual Private Network VSAT ‐ Very Small Aperture Terminal WAN ‐ Wide Area Networking WiMAX ‐ Worldwide Interoperability For Microwave Access WTO ‐ World Trade Organization

CURRENCY All numbers are presented in EURO (EUR) and calculated as follows: 1.00 USD = 0.900648 EUR, 1.00 KES = 0.00931433 EUR

The material is developed based on the conducted interviews and available information and data. This document represents the latest publicly available information. As often is the case in Africa the data and information may not be absolutely up to date.

Finpro Digital Africa Growth Program Pre-study: Kenya

5 of 42

1 BANKING AND FINANCIAL SERVICES SECTOR

1.1 Summary The Kenyan Financial and banking sector has registered impressive performance, with the size of assets standing at EUR 22.05 billion, loans and advances amounting to EUR 12.85 billion, while the deposit base stood at EUR 16.54 billion and profit before tax of EUR 258.89 million as at 31st March 2013. During the same period, the number of bank customer deposit and loan accounts stood at 17.3 million and 2.3 million respectively a steady increase from previous figures. The sector has had immense innovations with the most outstanding being mobile money transfer and agency or satellite banking initiatives that have gradually put the sector on the global map. In the first quarter of 2015, the number of mobile money transfer subscriptions stood at 26.0 million while the number of agents increased by 4.6 % to reach 121,924 up from 114,988 agents recorded in 2014. In 2014, the value of mobile payments grew by nearly a third to EUR 21 billion compared to EUR 8 billion of 2013. This means that consumers moved an average of EUR 1.71 billion monthly or EUR 56.7 million per day compared to the EUR 43.84 million a day they moved in a similar period in 2013. Cash deposits through commercial bank agents in 2012 stood at 13 million transactions, valued at EUR 10.52 billion. On the other hand, cash withdrawals were valued at EUR 517.92 million. Agents made transactions of payment of retirement social benefits worth EUR 11.41 million and bill payments worth EUR 2.45 million. As at March 31, 2013, there were 11 commercial banks that had contracted 18,082 active agents facilitating over 48.4 million transactions valued at EUR 2.63 billion. This is an increase from the 10 banks that had contracted 16,333 active agents facilitating over 38.7 million transactions valued at EUR 2.1 billion in December 2012. The sector continues to present a favourable outlook for the future due to solid macroeconomic fundamentals. This is seen through continued expansion of Kenyan banks into the region, further expansion of the branch network and agency banking in the domestic market, entry of foreign (regional and international) banks, and higher demand for banking services as financial inclusion leads to more individuals banked across the country and region. Proper guidelines and frameworks have been put in place by the relevant bodies to harbour a healthy and competitive environment for increased growth. Merging of corporate tax and value‐added tax procedures, as well as the digitization of the registrar’s records in 2011 has increased efficiency in the sector. As a result new entrants are able to secure their place with a reduced bureaucratic probe. Amidst the changing landscape in the sector and technological innovations put in place, there is a need to improve operational efficiency and enhance control of operations. As a result diverse opportunities lie for Finnish ICTs which wish to provide solutions in various gaps in the sector. Key sector trends and opportunities: Consolidation of data, systems and processes Internet and mobile payment solutions / concepts / innovations / services Process automation IT solutions and software Leasing solutions / products System for online, real‐time trading on the stock exchange Solutions driving down the cost of receiving remittances from abroad (for example through BitCoins) Credit sharing solutions E‐learning solutions and content for financial institutions branch employees Vulnerable core banking servers Printed passwords to the Central Bank Virtual Private Network Favourable public‐private partnerships in the execution of infrastructure projects Finnish ICT companies can therefore take up the opportunities in an environment that wishes to foster new experiences for their consumers through technological development. This is due to new customer centric models of innovation as banks evolve from a product oriented value addition to the latter.

Finpro Digital Africa Growth Program Pre-study: Kenya

6 of 42

1.2 Introduction Financial sectors on the African continent remain largely underdeveloped, while banking industries continue to dominate the landscape in terms of total assets and services. Nonetheless, financial sector development has been on the agenda of African policy makers for some time. Various policy reforms over the past decade have contributed to an environment more conducive to financial sector development. Governments have made progress in introducing much needed legal regulatory frameworks, information infrastructure and regulatory institutions. As a result, the depth and coverage of financial systems, when measured by the ratios of broad money volumes of bank deposits and private sector credit to GDP, have improved over the past two decades.i Nevertheless, Africa’s financial sector continues to be less developed compared to other emerging market regions. However, Africa enjoys certain key advantages that will enable the continent to equal or even surpass at least some of its emerging market counterparts in terms of financial sector development in the coming decade and beyond. Most African financial markets are open to new entrant including foreign players compared to other emerging market economies. The growing presence of subsidiaries of major global banks on the continent has undoubtedly improved the quality of financial services in recent years; the focus here has largely, but not exclusively, been on high margin corporate businesses as opposed to retail banking sector. Kenyan is the third largest financial market in sub Saharan Africa after Nigeria and South Africa however, the larger two are dominated by large local players. The continent has also often been at the forefront of new technological advances and other innovative methods to reach new customers and simplify access to banking, especially in more rural locations. However, more than anything else, Kenya represents massive financial sector growth potential due to the fact that the market is still largely unsaturated. According to the World Bank, only 14.9% of adults in sub‐Saharan Africa had deposit accounts with commercial banks in 2012. Africa’s flourishing middle class, forecast to triple over the next two decades, further supports the massive potential that lies within Africa’s growing consumer base. Indeed, with real GDP per capita in many African countries having climbed past the critical EUR 886‐level, a rapid expansion in retail banking is foreseen in coming years. The World Bank projected retail banking in sub‐Saharan Africa to grow at a compound annual rate of 15% between 2013 and 2020, bringing the sector’s contribution to the continent’s collective GDP to 19% from an estimated 11% in 2009. To do so however, institutions will continually need to embrace innovative strategies so as to shape banking products to fit consumers’ rising financial sophistication needs as well as to tap into the continent’s massive ‘unbanked’ population. Kenya leads the way in the region’s financial sector and is the only country whose local banks have achieved a significant presence throughout the region. In most other countries, local banks focus predominantly on domestic markets. Most of the banking sectors in the region with the exception of Kenya, have significantly more foreign banks than local banks operating in local markets. The Kenyan banking sector comprises of 43 commercial banks. The sector is relatively well developed and dynamic, while access to credit has been boosted over the past decade by the advent of mobile and agency banking. A number of Kenyan banks have also expanded into neighbouring countries. Prudential guidelines introduced in 2012 have helped to improve banks’ risk management practices. The sector has continued to record strong growth during 2013, seeing as the deposit base expanded by 12.5%, while gross loans grew by 17.65% year‐over‐year in December 2013. Also, the demand for credit picked up significantly following the peaceful conclusion of elections in March 2013. Credit demand was further boosted by lower interest rates and an upbeat macroeconomic outlook. Kenya’s banking sector has a favourable outlook for the future. This view is supported by solid macroeconomic fundamentals, continued expansion of Kenyan banks into the region, further expansion of the branch network and agency banking in the domestic market, and higher demand for banking services due to the government’s devolution process. In the Kenya Revenue Authority Top 10 largest taxpayers 2011, banks occupied four of the top position. This simply reflects the sector’s economic dominance in Kenya. Regional integration is taking hold within Kenya's banking sector. The latest foray into Kenya by Nigeria's United Bank for Africa (UBA) signifies West Africa's increasing appetite to participate in the East African markets. UBA is the second bank from West Africa to enter into the Kenyan banking industry. Togo‐based Ecobank entered Kenya last year after acquiring a 75% stake in East African Building Society (EABS) Bank.

Finpro Digital Africa Growth Program Pre-study: Kenya

7 of 42

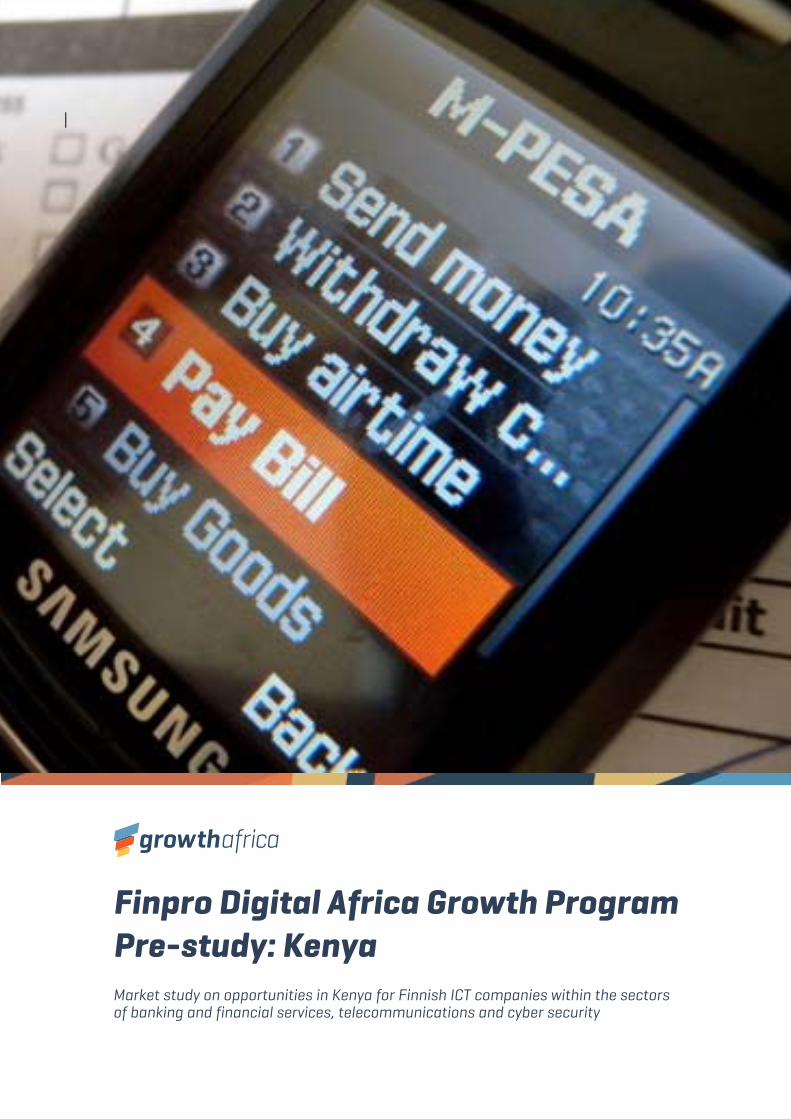

1.3 Nature of the market and market size for technology solutions The advent of modern technology and other innovations have successfully enabled a handful of pioneers to provide banking services to a far wider income customer base than ever before. More specifically, the emergence of mobile technology as an alternative to more traditional banking has allowed for services to be provided to lower income households often residing at distant rural locations. This was made possible by the rapid diffusion of affordable cellular technology on the African continent. According to a study completed by the African Development Bank during 2012, “the number of subscribers on the continent has grown almost 20% each year for the past five years. Mobile telephony penetration in Africa has increased exponentially from less than 2 million subscribers in 1998 to over 500 million in 2011.” Mobile banking has achieved the broadest success in sub‐Saharan Africa, where 16% of adults reported having used a mobile phone in the 12‐months leading to April 2012 to pay bills or send or receive money. This is compared to less than 5% in other regions. One of the most successful mobile banking models in Africa is considered to be Kenya’s MPESA, which caters to more than 14 million customers (70% of Kenya’s adult population). Developed by Vodafone and launched commercially by the company’s Kenyan affiliate Safaricom, MPESA is an electronic payment system accessible from ordinary mobile phones. MPESA account holders can use their mobile phones to transfer funds, pay bills, and purchase mobile airtime credit. This is widely aired as successful but the success has not been replicated in any other African country to date.

1.4 Structure of the market Kenya’s banking sector consists of 43 commercial banks and 1 mortgage finance company whereby 31 are locally owned and 13 are foreign owned. These are further split into private and public owned institutions. The leading banks in terms of asset ownership are Kenya Commercial Bank (KCB), which has regional foothold in all of East Africa with branches in all South Sudan’s ten provinces. KCB has EUR 4.05 billion in assets. Equity is the second largest with EUR 2.84 billion in assets with Barclays and Cooperative Banks taking the third and fourth positions with a share of EUR 2.25 billion and EUR 2.063 billion respectively.

1.4.1 Banks

The latest data reveals that Kenya’s banking industry is going strong. In 2011, the industry recorded a EUR 822.96 million pre‐tax profit and paid up EUR 236.3 million in total. According to Habil Olaka, CEO of Kenya Banker’s Association, they are expecting the banking sector to increase its contribution to the country’s coffers. He adds that Kenya’s economy is reliant to the banking industry, and that it is likely to continue to develop. Based on the data released by the Central Bank of Kenya, the banking industry recorded a 20% increase in profit last year, amounting to EUR 993 million. Therefore, if the tax payment increase by the same margin, then the tax from the banking industry is expected to surpass EUR 275.6 million.

1.4.2 Savings and Credit Cooperatives (SACCOs)

There are over 6,000 registered Savings and Credit Cooperatives (SACCOs) in Kenya. 1,995 SACCOs filed audited financial statements for the year ending 31 December 2013 with the Ministry of Industrialization and Enterprise Development. There are 215 deposit taking SACCOs (DTS), out of which 135 have been licensed by the Sacco Society Regulatory Authority (SASRA). The remaining 80 are yet to meet statutory requirements to be licensed. These DTS account for 78% of the total assets and deposits of the entire SACCO sector, the DTS command 82% of the SACCO membership.ii The financial performance of the 1,995 SACCOs that filed returns has recorded growth. Membership served by SACCOs increased to 3.3 Million as at December 2013 from 2.97million in 2012. Total Assets increased by 14% to EUR 3.08 billion (2.7 billion in 2012). Deposits grew by 13% to EUR 2.2 billion (1.95 billion in 2012). Loans and advance grew by 13.7% to EUR 2.32 billion (2.05 billion in 2012). Total Capital grew by 11% to EUR 230.4 million (193.8 million in 2012) The performance of the 235 licensed deposit taking SACCOs is as below: Total assets grew by 17% from EUR 1.9 billion in 2012 to EUR 2.23 billion in 2013 Income also grew by 32% to EUR 313.6 million, from the EUR 258.3 million recorded in 2012 Financial expenses grew by 14% to stand at EUR 147.6 million Non‐Performing loans (NPLs) declined from 7.4% in 2012 to 4.7% in 2013. Total capital grew by 30% to EUR286.4 million from 221.7 million in 2012

Finpro Digital Africa Growth Program Pre-study: Kenya

8 of 42

Loans and advances remain the biggest component of total assets of SACCOs contributing 76% of the total

Finance expenses to total income ratio stands at 47% of total income, which does not compare favourably with banks at 31% and Micro finance institutions at 21% but it is expected as most earnings are paid out as interest and rebates to members.

Operating expenses grew by 18% from EUR 91.5 million to EUR 108.1 million All the 135 licensed SACCOs complied with minimum core capital requirement of EUR 92,369.9 On average the SACCOs in 2013 exceeded core capital to total assets regulatory ratio of 10% to stand at

10.47% SACCOs in addition exceeded Core Capital to Total deposit liabilities statutory ratio of 8% to record

14.66% performance

1.4.3 Mobile Money

In 2014, the Central Bank of Kenya’s (CBK) report showed the value of mobile payments grew by nearly a third to EUR 21.3 billion compared to EUR 8.06 billion of 2013. This means that consumers moved an average of EUR 1.72 billion monthly or EUR 57.4 million per day compared to the EUR 44.4 million a day they moved in a similar period in 2013. Kenya has five main mobile money platforms: Safaricom’s M‐Pesa, Airtel Money, Orange Money, MobiKash and Tangaza Pesa ‐ backed by a network of about 120,781 agents.iii Interestingly for a middle class economy like Kenya, CBK data shows card payments plunged 17.4% to EUR 11.11 billion last year compared to EUR 13.9 billion in 2013. People trust mobile money more than they trust cards and with the increasing opportunities for paying with mobile money across consumer and business sectors mobile appear to be winning market shares at the expense of cards. Four MNVO licenses were sold in 2014 and for two of the licensees it anticipated that the licenses’ primary target is to establish a significant presence in the mobile money space. It is important to note that there still remains 2 million unbanked individuals despite the various inclusion initiatives. Financial inclusion has therefore led to a strategy where the formerly “unbanked” population has been propelled towards incorporating banking services in their banking strategies. More than double the number of adults use mobile phone financial services (11.5 million) compared with banks (5.4 million). As a result: Use of mobile phone financial services more than doubled from 28% in 2009 to 62% in 2013 Bank use has been rising over time from 13.5% in 2006 to 29.2% in 2013 Use of MFIs has remained at 3.5% between 2009 and 2013 Use of SACCOs has decreased since 2006, from 13.5% in 2009 to 9.1% in 2013 Use of informal groups has decreased from 39.1% in 2006 to 27.7% in 2013

1.4.4 Insurance companies

Total expenses in the insurance industry amounted to EUR 193.4 million in 2013 compared to EUR 157.4 million in 2012. Medical and motor classes in the insurance industry continue to be the main drivers of the sector contributing 63% of the total gross premiums in 2013, hitting EUR 1.2 billion in 2013 compared to EUR 1.01 billion in 2012. Individuals may collide with health practitioners to fake illnesses and medical operations while health centres over price insured individuals. This is also facilitated as half the claims paid are not insured. According to the Annual Insurance Industry Report by the Association of Kenya Insurers (AKI), motor insurance accounted for 39% of total gross premiums or EUR 313.1 million including commercial and private, while medical class recorded a 24% or EUR 192.71 million of the total premiums. At the same time medical insurance recorded the highest growth of 59% to EUR 194.7 million from EUR 120.5 million in 2012. The growth of the medical class was exceptionally high because of newly licensed medical insurance underwriters who were not included in 2012. The two classes are under the general insurance or Non‐Life segment which recorded a gross premium worth EUR 797.2 million compared to EUR 661.7 million in 2012. Other classes include fire, work injury benefit, personal accident, marine, theft and aviation. The life insurance business on the other hand recorded a premium income of EUR 407.9 million up from EUR 343 million in 2012. The segment carries the ordinary life, group life, pension business and investment contracts. Meanwhile, claims increased to EUR 315.2 million in the year under review from EUR 269 million in 2012 with medical insurance recording the highest loss of 75% or EUR 89.1 million followed by motor private at 70%, equivalent to EUR 83.5 million.

Finpro Digital Africa Growth Program Pre-study: Kenya

9 of 42

1.4.5 Money remittance services (from diaspora)

About 2.5 million Kenyans living abroad are sending money back to Kenya. Remittance inflows to Kenya in February 2015 increased by 11.6% to EUR 110.89 million from EUR 99.3 million in February 2014 was 7.5% higher than inflows in January 2014. The increase in February 2015 was largely on account of inflows from North America. The 12 month cumulative inflows in February 2015 increased by 10.6% to USD 1,299 million from EUR 1,175 million in the year to February 2014. The 12 month average flow maintained an upward trend during the year peaking at to EUR 108.2 million by February 2015. The market has traditionally been dominated by global remittance services such as Western Union and MoneyGram. Safaricom announced a new service with MoneyGram at the end of 2014 enabling consumers in over 90 countries outside Kenya to send money directly to M‐PESA. It was recently rumoured that Western Union and MoneyGram were in merger or acquisition talks – a move seen as a reaction to an increasingly competitive space. Nation Media Group in partnership with Diamond Trust Bank (DTB) has in the second half of 2013 launched its own money transfer service named Nation Hela (www.nationhela.com). Recently bitcoin remittance provider BitPesa has officially launched its beta test in Kenya. The company offers a 3% cut‐rate fee. BitPesa is just one of a few bitcoin firms that aims to disrupt a traditional remittance market that often imposes high costs on those wishing to use remittance services. For example, the cost of sending money to Kenya by other means can be as much as 9.2% of the value being transferred by services like Western Union and MoneyGram, and 19.8% by banks,

1.5 Overview of companies and products Before 2010, financial institutions focused on their traditional and conservative roles. The market share was rather small and focused on the seemingly banked populations which includes but is not limited to individuals with formal employment and constant income flows. However as mentioned, the introduction of mobile banking pioneered by Safaricom saw a paradigm shift that incorporated the unbanked population as discussed under the mobile banking category. Apart from the lending, and mortgage products offered by the financial institutions, it is important to note some commendable products offered by banks that have seen them incorporate some of the latest technological advances and also allow them capture a larger clientele. This was in a quest for banks to counter and catch up with the strands taken up by the introduction of mobile banking.

1.5.1 Agent banking

Cash deposits through commercial bank agents in 2012 stood at 13 million transactions, valued at EUR 1.07 billion. On the other hand, cash withdrawals were valued at EUR 529.4 million. The agents also made transactions of payment of retirement social benefits worth EUR 11.6 million and bill payments worth EUR 2.51 million. As at March 31, 2013, there were 11 commercial banks that had contracted 18,082 active agents facilitating over 48.4 million transactions valued at EUR 2.69 billion. This was an increase from 10 banks that had contracted 16,333 active agents facilitating over 38.7 million transactions valued at EUR 2.06 billion in December 2012.iv Agency banking model allows banks to liaise with commercial outlets like cybercafés, shops, petrol stations and supermarkets to offer financial services that include depositing and withdrawing cash. The partnership has seen banks in Kenya take financial services closer to people, in particular, to areas that lack them. It is estimated that a third of the country’s 40 million people lack access to banking services. Kenya changed its banking laws in January 2011 to allow commercial banks offer their services through the third‐party businesses. The agents operate as satellite branches.

1.5.2 Islamic banking

Islamic banking is also a unique product that many companies are offering in Kenya. Gulf African Bank and

First Community Bank, each an Islamic bank, commenced operations in Kenya in 2008 offering Sharia‐compliant banking services. Their combined operations now represent approximately 1% of Kenya's gross banking assets. In the current year, Kenya Commercial bank (KCB) also rolled out its Sharia Compliant banking product for both its Islamic and Non Islamic clientele, in an aim to cater to more of the unbanked populations.

Finpro Digital Africa Growth Program Pre-study: Kenya

10 of 42

1.5.3 Credit Reference Bureaus (CRBs)

The Credit Information Sharing (CIS) mechanism, which was launched in July 2010, continues to be used by both commercial banks and individuals. The number of credit reports requested by institutions stood at 2,596,600 in March 2013 up from 2,321,766 reports in December 2012, representing an increase of 11.8% or 274,834 reports. Over the same period, the number of reports requested by customers increased from 28,733 to 35,172 reports. The introduction of the credit information sharing mechanism has further strengthened credit appraisal standards. Banks have now incorporated credit reference reports in the credit risk appraisal. It is also expected that credit referencing will go a long way in inculcating credit discipline in borrowers. There are currently 3 CRBs in Kenya: Just licensed Creditinfo Credit Reference Bureau Kenya Limited (www.creditinfo.com, Icelandic firm), Metropol Corporation Ltd. (www.metropol.co.ke, Kenyan company, worked with Dun & Bradstreet International (D&B) till 2006)) and CRBAfrica (www.crbafrica.com, Kenyan).

1.5.4 Deposit Taking Microfinance Institutions

As at 31st March 2013, 8 Deposit Taking Microfinance Institutions (DTMs) were in operation and had gross loans worth EUR 196.5 million compared to EUR 191 million registered in December 2012 thus translating to a growth of 3.7%. Similarly, the deposits base stood at EUR 152.1 million representing a growth of 6.4% from EUR 142.8 million in December 2012. The long‐term borrowings by DTMs increased from EUR 76.97 million in December 2012 to EUR 81.6 million in March 2013. The number of DTMs deposit accounts and loan accounts stood at 1.79 million and 0.47 million respectively in March 2013 compared to 1.76 million deposit accounts and 0.46 million loans accounts registered at end of December 2012.

1.5.5 Revised Prudential and Risk Management Guidelines

The revised Prudential and Risk Management Guidelines issued in November 2012 came into effect in January 2013. Seven new Prudential Guidelines were issued covering various operating aspects of banks. These include Outsourcing, Representative Offices of Foreign Institutions, Voluntary Liquidation, Consolidated Supervision, Stress Testing, Prompt Corrective Action and Consumer Protection. In addition, the existing nine Risk Management Guidelines were reviewed while two new guidelines on Country and Transfer Risk and Information and Communication Technology Risk Management were introduced. According to the Banking Sector 2013 Outlook the banking sector is expected to sustain its growth momentum on the backdrop of a stable macro‐economic environment, and domestic and regional expansion by banks.

1.5.6 African Trade Insurance Agency (ATI) products

In 2014, NIC Bank and ATI formed a partnership aimed at addressing the lending gap that exists most notably in the SME sector. Under the transaction, NIC Bank will be the first bank to take up ATI’s new insurance cover that will protect NIC’s entire portfolio of trade finance borrowers against the risks of insolvency and non‐payment – risks that have traditionally inhibited most African banks from lending to SMEs. The product will help banks extend credit facilities such as short term loans, invoice discounting, bank guarantees and letters of credit without the requirement of the standard tangible securities as is the current practice by banks. This stands to have a positive impact particularly on the SME sector, which has historically been hindered from accessing working capital due to insufficient security. ATI product stands to impact the financial industry because it provides a risk mitigation against credit default risk, thereby opening up a window of opportunity for both the SMEs and the banks to benefit.

1.5.7 Key industry players:

The strengthening of the Kenyan economy for the last ten years due to a change in governance has seen a major transformation in the banking industry. Commercial banks and investment banks in Kenya have been opened up throughout the country to provide financial services.

Top 10 banks: Top 10 insurance companies:

Equity Bank Kenya Co‐Operative Insurance Company (CIC

Standard Chartered Bank Kenya Blue Shield Insurance Company

Barclay's Bank Kenya Insurance Company of East Africa (ICEA) Lion Group

Kenya Commercial Bank (KCB) Kenindia Assurance Company

Diamond Trust Bank Kenya (DTB) UAP Provincial Insurance Company

Housing Finance Bank of Kenya British American Insurance Company

CFC Stanbic Bank Kenya Heritage Insurance Company

NIC Bank Kenya Jubilee Insurance Company

Finpro Digital Africa Growth Program Pre-study: Kenya

11 of 42

Cooperative Bank of Kenya APA Insurance Services

Commercial Bank of Africa (CBA) Pan Africa Insurance Holdings

1.6 Market size In 2012, the banking industry has been the major contributor to the rise in tax revenue. Apart from corporation tax, banks also pay VAT, stamp duty and income tax for the more than 30,000 people they employ. The Kenyan Banking Sector registered improved performance with the size of assets standing at EUR 22.3 billion, loans and advances amounting to EUR 13 billion, while the deposit base stood at EUR 16.7 billion and profit before tax of EUR 261.4 million as at 31st March 2013. During the same period, the number of bank customer deposit and loan accounts stood at 16.0 million and 2.13 million respectively. Assets:

The banking sector’s aggregate balance sheet expanded by 2.7% from EUR 21.8 billion in December 2012 to EUR 22.4 billion in March 2013. The major components of the balance sheet were loans and advances, government securities and placements, which accounted for 55.8%, 21.1% and 5.5% of total assets respectively.

Loans and advances:

The sector’s gross loans and advances increased from EUR 12.6 billion in December 2012 to EUR 13 billion in March 2013, which translated to a growth of 3.0%. The growth, which stood at EUR 370.7 million, was in 7 sectors registering a marginal decline occasioned by faster loan repayment rate compared with the rate at which new loans were being made in those sectors during the period.

Deposit liabilities:

Deposits, which form the main source of funding for the banking sector, accounted for 73.5% of total funding liabilities. The deposit base grew by 0.8% from EUR 16.31 billion in December 2012 to EUR 16.5 billion in March 2013 mainly due to branch expansion, remittances and receipts from exports. The number of deposit accounts increased from 14,735,836 in December 2012 to 16,036,067 in March 2013 representing a growth of 1.44 million accounts or 9.1%.

Capital and reserves: The banking sector registered improved capital levels in March 2013 with total

capital growing by 6.7% from EUR 3.09 billion in December 2012 to EUR 3.3 billion in March 2013. Shareholders’ funds increased by 3.5% from EUR 3.4 billion in December 2012 to EUR 3.5 billion in March 2013. Similarly, the ratio of total capital to total risk‐weighted assets increased from 21.9% in December 2012 to 23.2% in March 2013 while core capital to total risk weighted assets increased from 18.9% to 20.3% over the same period.v

1.7 Competition Financial institutions are face the emergence of formidable competitors, from companies in the retail and communications sectors that haven’t traditionally operated in this space. Financial institutions have therefore turned to technology to create disruptive banking models that capture the imagination of consumers and erode the market of traditional banks. A slew of new payment technologies with bolstered security features are making it easier for non‐traditional financial companies to cross the chasm of distrust among merchants and consumers. For example; Oracle recognizes these challenges and is working closely with financial institutions on new strategies that focus on a “customer in” versus “product out” approach. The rapidly evolving landscape, while threatening at first glance, actually holds hidden opportunities for traditional players who focus on reinventing the customer experience. As consumers become more accustomed to conducting transactions outside the traditional banking environment, financial institutions can leverage their scale to provide an experience superior to that offered by new entrants.

Finpro Digital Africa Growth Program Pre-study: Kenya

12 of 42

As banking institutions survey the unfolding landscape, the message becomes obvious: To continue to lead on their home turf, financial institutions must not only rethink and improve the customer experience, they must look at new approaches to transform it, from end to end.

1.8 SWOT analysis

1.8.1 Strengths

Recent developments, such as the expansion of mobile phone‐based banking and the spread of pan‐African banking groups, have the potential to significantly change the landscape for banking in much of sub‐Saharan Africa, but also introduce new challenges for financial regulators. A broad sector with a significant number of players catering for various segments. The industry players are relatively technology driven and open to innovations and solutions which can improve their internal processes and drive their customer acquisition or retention.

1.8.2 Weakness

a. Weak controls in the banking sector Impediments to development include the small size of national markets, low income levels, and weak creditor rights and judicial enforcement mechanisms. Examining various indicators in relation to financial system access, depth, efficiency and stability; the findings suggest that sub‐Saharan Africa (SSA) performed weakest on average.

b. Infrastructural weaknesses

The unavailability of efficient infrastructure remains a key challenge for a number of African countries and as such, cost of providing the necessary infrastructure adds significantly to the cost of doing business. Also, payments systems are largely underdeveloped and as such supports process for efficiencies and reduction in cash handling are limited in a number of countries.

c. Weak regulatory frameworks

The global financial crises encouraged many countries on the continent to embark on becoming compliant with international regulatory frameworks (e.g. Basel guidelines). However, progress in this regard varies greatly between countries and regions. In addition to improved regulatory frameworks, African countries need to strengthen oversight and enforcement.

d. Unaffordable banking services

Probably one of the greatest constraints to growth in the African banking sector pertains to the fact that formal banking services remain mostly too expensive for the vast majority of lower income households. Banks have limited incentive to develop products for the poor masses that currently cannot afford banking products and hence mostly compete at the higher end of the income distribution. Increased competition at the higher end of the market could serve to make banking services more cost‐effective for higher income households. However, to bridge the gap between affordability and commercial viability would require an increase in average income and as a result larger middle classes across the continent. Although the evidence suggests that the African middle class is in fact expanding, innovative new banking solutions might serve to speed up this process.

e. Fraud

In 2013, Kenya lost about EUR 18 million to fraudsters who consisted of tech savvy employees. Identity theft, electronic funds transfer, cheques and credit card fraud, forgery of documents and online fraud as among the ways through which financial institutions lost cash. The insurance sector also faced impeccable restraints as the industry recorded that 20% of the claims paid for motor insurance are fraudulent while in the medical insurance sector fraudulent claims paid are between 30 ‐ 40%. Most of the fraud is done by staff members of insurance companies as well as loss assessors colluding with the insured to commit fraud.

Finpro Digital Africa Growth Program Pre-study: Kenya

13 of 42

f. Excess liquidity The European Investment Bank (EIB) notes that in many African countries “banking systems are characterized by significant excess liquidity, reflecting the scarcity of what banks deem to be credit‐worthy borrowers.” Banks in many countries continue to rely on government securities to generate earnings instead of growing loan books. In cases where loans are more prevalent, the interest rate spreads between loans and deposits are mostly large. The situation is compounded by the fact that, in a number of African countries, the necessary enablers to grow retail credit e.g. identification, credit bureaus etc. are absent or where they exist, in a very nascent phase.

g. Technological backlogs

A whitepaper published by the Industrial Development Corporation (IDC) of South Africa in 2013 highlighted information technology as a major operational challenge. The proliferation of multiple systems to deliver on operational needs, without a clear architecture governing interoperability and synergy has resulted in its own unique issues. Many banks in Africa indeed are plagued with reporting and data integration problems resulting from this challenge or the complete lack of requisite technology. “The consolidation of data, systems and processes is, therefore, a key priority for African banks in order to improve operational efficiency and enhance control of their operations”

1.8.3 Opportunities

Mobile payment solutions / concepts / innovations / services Process automation IT solutions and software Leasing solutions / products System for online, real‐time trading on the stock exchange Solutions driving down the cost of receiving remittances from abroad (for example through BitCoins) Credit sharing solutions Mortgage and housing loan products E‐learning solutions and content for financial institutions branch employees

1.8.4 Threats

The convergence and disruptive development in the mobile financial service space continues to challenge the industry. Especially Safaricom’s monopolistic position and utilisation of M‐PESA to leverage own or partnership products and services remains a challenge. Financial institutions will continue to weigh their strategic option – and whether to partner with Safaricom, compete with it or seek to build its current business in other ways.

Finpro Digital Africa Growth Program Pre-study: Kenya

14 of 42

2 TELECOMMUNICATIONS INDUSTRY IN KENYA

2.1 Summary The Kenyan telecommunications market is one characterized by a liberal regulatory framework, fierce competition, and rapidly developing infrastructure. This potential market of 44.3 million people consists of 180,000 fixed lines, a bandwidth capacity of 847,523 Mbps which is the highest in Africa, the largest mobile money market in the world at 25 million users, 27 million internet users, and 34 million mobile users which translates into 61% internet, and 80.5% mobile market penetration. These numbers reflect the staggering growth of the telecoms market caused by the overhauled licensing regime, and the arrival of four fibre‐optic international submarine cables resulting in a heavy investment in the National Optic Fibre Backbone Infrastructure (NOFBI). This in turn dramatically increased coverage and resulted in some of the lowest mobile tariffs the world and highest level of internet and telephony competition. The rapid nature with which this has been done however has left considerable gaps in the cyber security realm at almost all levels. In 2013, the ICT market in Kenya reached a value of EUR 4.64 billion, of which telecommunication services accounted for 71.9%, hardware made up 22.3%, and IT services and software represented 3.0% and 2.8%, respectively. The stratification of MNO provider’s services throughout all levels of the market has resulted in a cutthroat business environment based on product and service differentiation. This has spurred on higher quality services, more choice, and more innovative products for the consumer. The introduction of three new MVNO licenses in 2014 is set to shake up this mix and present an opportunity for further differentiation and potential partnerships. This rapid development of infrastructure and services mean that digital engagement which encompasses integration of mobility benefits with those offered by cloud, big data and social networking will be the key to capturing market share in Kenya. Digital engagement will combine social mobility, and big data initiatives, enabled by a cloud‐based approach, and move Africa’s mobility momentum further into the value‐added space. In addition the Kenyan Governments push to consolidate all 47 county governments’ fibre optic networks into one, and digitize their day‐to‐day operations in a non‐technology specific manner poses another huge market entry point for foreign entities. The automation of business processes in all levels of the education and health sector is another mammoth undertaking that will surely present opportunities for foreign software, hardware, and IT consultant services and products alike. Ultimately the coming years will be a large battle for the SME market as they rapidly automate their business processes and operations. In addition with this new modernization comes new IT procurement – new clients, new products, and new markets. The East African market is characterized by new markets, products, and clients, sought after by multinational corporations and African organisations alike driving innovation and entrepreneurship through cloud, the social enterprise, enterprise mobility, and big data as new product sets. However the lack of skilled ICT professionals and training initiatives poses a huge opportunity for foreign businesses to partner, invest, and play a role in the knowledge transfer process necessary in future large scale ICT projects. In summary the Kenyan ICT market is one that has the political will, established infrastructure, and plan in place to grow at an exponential rate. Entry into the market would also establish numerous future opportunities for further expansion into the East African market as terrestrial fibre cables connect deeper into the continent. There are numerous opportunities for Finnish firms to actively foster relationships and showcase their products and services so that they play an integral role in ensuring this exponential growth takes place in an effective and secure way.

2.2 Nature of the market and market size for technology solutions Kenya is often touted as the “Silicon Savannah”. The extent to which that is true is up for debate but the fact of the matter is that the telecommunications market in Kenya has been one of rapidly growing infrastructure, user adoption, market penetration, and increased competition ever since Kenya made a commitment to the WTO of becoming a fully competitive sector by 2004. It was then that the Telkom Kenya fixed‐line market, and international bandwidth market, through its subsidiary JamboNet, essentially ended. This event paved

Finpro Digital Africa Growth Program Pre-study: Kenya

15 of 42

the way for the Communications Commission of Kenya, now known as Communications Authority Kenya (CA), to license extensive backbone infrastructure providers, international gateway operators, and application services providers. The liberalization of the communications sector has had a positive effect on the deployment of communications infrastructure and services in the country. Kenya is now a nation of 44.3 million people, with 180,000 fixed lines, a bandwidth capacity of 847,523 Mbps which is the highest in Africa, the largest mobile money market in the world at 25 million users, 27 million internet users, and 34 million mobile users Which translates into 61% internet, and 80.5% mobile market penetration. In fact Kenya’s internet contribution to GDP (iGDP) is at 2.9%, the highest in Africa as well. In recent years much of this success stems from the installation of four fibre‐optic international submarine cables greatly reducing the industries costly dependency on satellite bandwidth. Kenya’s National Optic Fibre Backbone Infrastructure (NOFBI) now has a total length of over 5,000 km. Satellite capacity on the other hand sits at 273.0 Mpbs. Prior to the cables coming in 2009 East Africa was the only densely populated region globally without international fibre access. By and large at the time internet traffic, international calls and even some regional calls were carried via satellite though Europe or North America at staggering costs as the intercontinental fixed line infrastructure was highly fragmented or simply not there. Thus while bandwidth prices have now fallen upwards of 90% as a result, leading to cheaper phone and internet tariffs, many ISPs have grudgingly passed on these savings to end users and the CA has threatened price caps. Many companies that started out as ISPs have transformed themselves into second‐tier telcos by rolling out national and metropolitan fibre backbones and wireless broadband access networks, offering converged voice, data and video/entertainment services. At least six major deployments of WiMAX technology and four Fibre to the Home (FttH) rollouts have or are currently taking place. As a result advanced services such as IPTV/triple‐play, e‐commerce, e‐learning and e‐government are now rapidly evolving. However, the infrastructure investments have been costly and the market has become more competitive, which has led to takeovers in the sector. Several infrastructure sharing agreements have been forged. A large factor in this evolution has been the simplified and converged licensing regime introduced in 2008 now allows operators to offer any kind of service in a technology‐ and service‐neutral regulatory framework. This greatly reduced entry marries to the market and increased competition. Following the enactment of the Kenya Information and Communication Act, 2013 the CCK rebranded to the CA and vastly expanded their original mandate of the regulation and the management of the country’s radiofrequency spectrum. They are now responsible for the development and implementation of policies and strategies with respect to telecommunications services in Kenya. Which include the following: Telecommunications licensing

Preparation of procedures and regulations to license operators, including; Network Facility Operators, Application Service Providers and Content Service Providers. The Authority also enforces all license conditions and regulations.

Effective competition Maintains and promotes effective competition between commercial entities connected with telecommunication services in Kenya. This ensures efficiency and economy in the provision of such services that promote research and development in the sub‐sector. In addition, the Authority reviews the sector on a continuous basis to ensure that competition is fostered and to guard against anti‐competitive behaviour by licensed operators.

Consumer protection Protecting the interests of all users of telecommunications services in Kenya with respect to the prices charged for and the quality and variety of such services.

Promotion of investment and provision of international transit services Encourages private investment in the telecommunications sector and provision of international transit services by persons providing telecommunications services in Kenya.

Universal service obligations Develops mechanisms to ensure the availability of telecommunications services to all citizens throughout

Finpro Digital Africa Growth Program Pre-study: Kenya

16 of 42

the country.

Tariff regulation Develops pricing guidelines for service providers in order to ensure service affordability.

This competition has led to an all‐out price war in Kenya’s mobile communications sector in recent years resulting in the CA placing tariffs, special offers and promotions. The real trouble began with the introduction in 2008 of Kenya’s third and fourth GSM networks. While this hassled to an explosion of subscriber, it also severely hindered the profitability of operators. This has lead them to race towards more streamlined operations and diversify revenue streams. Exacerbating the issue has been slumping levels of Average Revenue per User which according to The Technology, Media and Telecom (TMT) Predictions 2014: Highlights and Context Report predicts ARPU at EUR 5.8 monthly. Third Generation (3G) mobile broadband, mobile payment and banking services are the primary sources of this added revenue but all segments are highly competitive. The Kenyan government has proposed an open access approach for 4G networks with plans to prohibit licensing of individual operators and instead make service providers lease capacity from an independent company. This was naturally met with heavy resistance from MNOs already in the market. 2014 and the beginning of 2015 saw key developments in the mobile market in particular. First with the sale of four MVNO licenses for a license fee of EUR 930 each to the following companies; Tangaza Pesa which is a mobile money transfer service, Zioncell Limited (the company behind is MODE) which is a technology company that offers value‐add services to different MNOs across Africa, and Finserve a Virtual Network Operator (a subsidiary of Equity Bank, one of East Africa’s largest), all of which would utilize the Airtel network. This was a move opposed by the Consumer Federation of Kenya, Safaricom and Telkom Kenya. A fourth license was subsequently acquired by Kenya Airways also using Airtel’s network. The second big event was the market exit by one of the major mobile operators Essar Telecom Kenya Limited (operating under the brand “yuMobile”) whose assets were ultimately acquired through a joint venture between Safaricom (infrastructure) and Airtel (customers). In the end, Essar was bleeding cash, costs far outnumbered revenues even resulting in some suppliers going to court to recover money owed. Having only entered the market in 2007 with a EUR 179.5 million investment and ultimately cutting their losses by selling for EUR 108. This should serve as a sobering indicator of the volatility inherent in this competitive market. A third major story was France Telcom, the 70% majority shareholder in the fixed and mobile line operator Telkom Kenya made it known of their desire to exit in 2014 but have reached an apparent deadlock with the 30% shareholder that is the Kenyan Government. Disagreement between the Kenyan government and France Telecom intensified last year after the minority shareholder refused to give in to demands that would allow France Telcom to sell its 70% stake to Vietnam based Viettel Group. France Telcom even stated it had lost control of the ability to implement any solutions to the challenges facing the business without the latter’s agreement. The possibly the biggest development was Equity Bank’s purchase of an MVNO license and partnering with Airtel. Equitel, launched in September 2014 under Equity Bank’s wholly owned Finserve has already racked up 786,000 active SIM card users. With the ultimate goal of taking down the juggernaut that is Safaricom’s M‐PESA which controls the lion’s share of the mobile money market. In response to this move Safaricom even slashed transaction charges by 65%. The bank says Equitel will aid users transfer money, access credit and make payments by phone. It also offers typical mobile services of calls, text messages and Internet browsing. According to Reuters, Equity leases Airtel’s telecoms infrastructure network, so it keeps all the revenue. They are also introducing dual SIM cards via a 0.1mm thick film (dubbed “Slim SIM”) which can be layered on an active SIM card without affecting customers’ original service providers’ network reception.

2.3 Structure of Kenya’s ICT market: Kenya’s Information and Communication Technology (ICT) market structure, and its players, can be categorized by three general provider segments under the CA Unified Licensing Framework (ULF). Both National and International companies are housed under the same overall structure. It goes as follows: a) Network Facilities Provider (NFP) Licensees under this category own and operate any form of

communications infrastructure (based on satellite, terrestrial, mobile or fixed). They largely provide infrastructure systems for long‐distance transmission and for local access;

Finpro Digital Africa Growth Program Pre-study: Kenya

17 of 42

a. Tier 1 NFP (international) i. International Gateway Systems and Services ii. International Sub‐Marine Cable Operators

b. Tier 1 NFP (National) i. National Fixed Network Operator (i.e. TKL) ii. Cellular Mobile Operators

c. Tier 2 NFP i. Data Carrier Network Operators ii. Public Data Network Operators iii. Regional Telecom Operators

d. Tier 3 NFP i. Local Loop Providers

b) Applications Service Provider (ASP) Licensees under this category provide all forms of services to end

users using network services of a facilities provider. These Include: a. GMPCS Service Providers b. Internet Exchange Point (IXP) c. Internet Service Providers (ISPs) d. Resale Service Providers e. Other Value Added Service Providers (VAS)

c) Content Services Provider (CSP) Licensees under this category provide contents services material,

information services and data processing services. These include: a. Premium Rate Service Providers b. Audio‐text Service Providers c. Credit Car Validation Service Providers d. Other Web‐based Public Commercial Information Service Providers e. Business Processes Outsourcing (BPO)

* NFP = Network Facilities Providers This liberalized regulatory framework embraces technological convergence and encourages innovativeness. It was designed to be the best method to meet end‐user needs, especially in respect to new and emerging markets to stimulate innovation and deployment. Under the framework there is no distinction between say mobile or fixed services, satellite or terrestrial, data or voice services, etc. The infrastructure providers have an infrastructure sharing code of practice with clear guidelines that is agreed upon by the operators. It is the spirit of infrastructure sharing that the operators keep local traffic local via the Kenya Internet Exchange point; a centrally monitor network security via the industry computer security response team and have a central manager for the country code top‐level. This public‐private ownership model of shared infrastructure is regionally and globally recognized as best practices.

2014 Market Composition by number of licensees:

Type of licensed provider No. of licenses (2014)

International Submarine Cable Operators 4

International satellite providers 3

National tier 1 NFPs 3

National Tier 2 NFPs 18

National Tier 3 NFPs 13

BPO operators 39

Telecommunications vendors 219

Content Service Providers 168 (as of 2012)

Public Communications Centre 40 as of

2012)

Finpro Digital Africa Growth Program Pre-study: Kenya

18 of 42

In order to break down the market structure further the 3 biggest market services (mobile money is covered under “Banking and financial services”) will be used:

1. Fixed telephony;

2. Mobile telephony

3. Internet/Data Next a basic market structure type will be attributed to each of the aforementioned market services by assessing their respective interconnected characteristics, including the: Number and relative strength of buyers and sellers Degree of collusion among players Level and forms of competition Extent of product differentiation Ease of entry into and exit from the market

2.3.1 Fixed Telephony ‐ Monopoly

The fixed line telephony market in Africa is essentially a monopoly as they are the sole provider. A monopoly exists when a firm has no competitors in its industry. It reduces output to drive up prices and increases profits. By doing so, it produces less than the socially optimal output level and produces at higher costs than competitive firms. Fixed line networks hardly ever invest in spreading their networks much farther from the urban areas than needed and subsequently, they rarely reach the remote rural areas where a substantial %age of the population lives. The fixed telephone service in Kenya is no exception. Until 2004, Telkom had exclusivity (a monopoly) over the provision of fixed line telecommunications services. Although the exclusivity legally has ended since then, thus far there is very limited competition. The government has issued 19 “local loop provider” licenses, but because their operations are restricted in both scope and geography, investment and interconnection having proven challenging, and so few entities holding such licenses have actually launched services. Efforts to issue a SNO license have also stalled. While the situation is changing, the mobile telephony market is significantly more competitive and dynamic.

2.3.2 Mobile Telephony ‐ Oligopoly

Although the mobile telephony market in Kenya is more open, it does not constitute perfect competition. Rather, it is representative of an oligopoly, an industry with only a few major firms: Safaricom

Bharti Airtel (formerly Zain, Celtel)

Orange Kenya (Telkom Kenya)

Finserve (Equity Bank) – recent entrant via MNVO licence Since there are only a few providers controlling a particular commodity, they can influence prices and affect the competition. They are price‐makers but highly interdependent. Safaricom has enjoyed their lion’s share of the market since its inception and several price wars have been sparked. However this benefits neither company as revenues drop and costs remain. Thus the key to their differentiation is in non‐price competition. Through innovative products, value addition, diversified revenue streams, and marketing. This market has been characterized in the past by a race to release the next big thing in the market. Safaricom had a runaway success with M‐PESA and Airtel just might have the same with its recent UnlimiNET bundles.

2.3.3 Internet/data ‐ Perfect competition

The Internet/data market in Kenya would be most representative of perfect competition. In this structure, numerous firms compete against each other, most small. There are numerous Internet Service Providers (ISPs) in Kenya, as listed in the table below.

Operator Subscribers (thousand) Market share

Safaricom (Mobile) 9,638 73%

Bharti Airtel (mobile) 1,945 15 %

Telkom Orange (mobile) 905 6.9%

Finpro Digital Africa Growth Program Pre-study: Kenya

19 of 42

Essar (yuMobile) (SOLD 2014) 603 4.6%

Wananchi (ZUKU) 44 0.3%

Liquid Telecom 15 0.1%

Access Kenya 11 <0.1%

Telkom (fixed) 11 <0.1%

Safaricom (fixed) 7.0 <0.1%

Jamii Telecom 2.3 <0.1%

iWay Africa 2.1 <0.1%

MTN 1.4 <0.1%

Call Key Networks 0.5 <0.1%

Tangerine 0.3 <0.1%

Others 0.8 <0.1%

Total 13,187 100%

When there are more than a few firms in an industry, providers are less likely to collude and reducing output and driving up profits the way a monopoly does. ISPs in Kenya began to feel some competitive pressure especially in the high‐end segment of the market when Safaricom upgraded to EDGE technology in 2006, which provides broadband‐like data rates of up to 384 Kbps. Pressure increased further when Safaricom introduced 3G services in 2008, offering peak data transfer speeds of 7.2 Mbps. The increased number contributes to an environment where providers attempt to outdo each other, driving the prices down and the output up. As such, firms in a competitive industry produce the socially optimal output level at the minimum possible cost per unit. The disparities regarding infrastructure costs requirements between mobile internet access and broadband or fixed line should be noted as key reason for the market share Safaricom holds. Mobil penetration is far higher than computer and internet access penetration so it only makes sense that mobile data would trump the latter.

2.4 Product and services:

In summary the key products in the industry are:

Mobile telephony (very little growth)

Mobile data (growth market)

Cloud services (yet to really take off, Safaricom is pushing SME products)

Mobile money (growth market)

Internet (growth market)

Fixed line telephony (declining, vanishing market)

Internet‐enabled digital television

There is a significant convergence and disruption in the space between telecommunication, content delivery

and financial solutions. Innovative solutions in this space are of interest to companies in telecommunications.

2.5 Key players, value chain and business models The ICT market is inherently complex with a consolidated power structure of distributors consisting of multinational corporations, government and large enterprises that provide infrastructure and networks to vendors who then distribute to tier 1 Value Added Resellers (VARs) & dealers down to tier 2 VARs, right down to the SME, retail, and consumer markets. As one goes down each level the amount of players in the value chain typically gets bigger. For the sake of this analysis the five main segments of the ICT market will be utilized and then broken down to who the major players are and their market share. The covered segments are international network facility providers, internet/data, mobile telephony, fixed telephony, and mobile transactions.

Finpro Digital Africa Growth Program Pre-study: Kenya

20 of 42

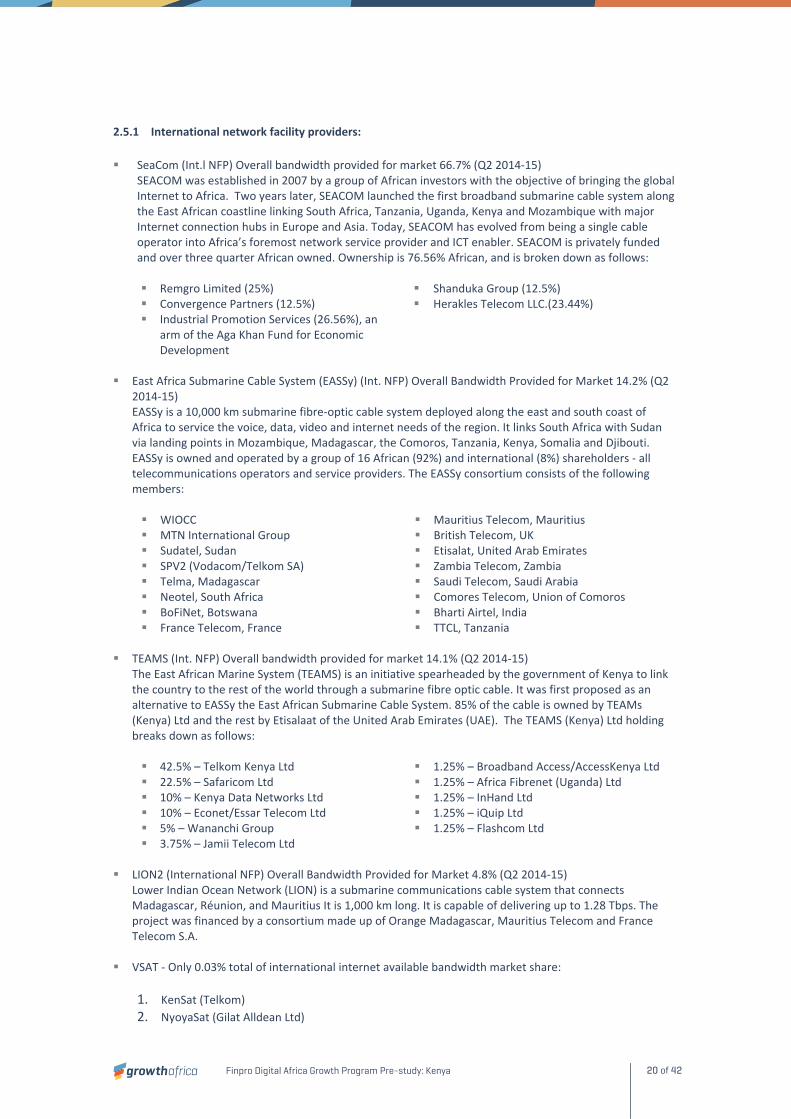

2.5.1 International network facility providers:

SeaCom (Int.l NFP) Overall bandwidth provided for market 66.7% (Q2 2014‐15)

SEACOM was established in 2007 by a group of African investors with the objective of bringing the global Internet to Africa. Two years later, SEACOM launched the first broadband submarine cable system along the East African coastline linking South Africa, Tanzania, Uganda, Kenya and Mozambique with major Internet connection hubs in Europe and Asia. Today, SEACOM has evolved from being a single cable operator into Africa’s foremost network service provider and ICT enabler. SEACOM is privately funded and over three quarter African owned. Ownership is 76.56% African, and is broken down as follows: Remgro Limited (25%) Shanduka Group (12.5%) Convergence Partners (12.5%) Herakles Telecom LLC.(23.44%) Industrial Promotion Services (26.56%), an

arm of the Aga Khan Fund for Economic Development

East Africa Submarine Cable System (EASSy) (Int. NFP) Overall Bandwidth Provided for Market 14.2% (Q2

2014‐15) EASSy is a 10,000 km submarine fibre‐optic cable system deployed along the east and south coast of Africa to service the voice, data, video and internet needs of the region. It links South Africa with Sudan via landing points in Mozambique, Madagascar, the Comoros, Tanzania, Kenya, Somalia and Djibouti. EASSy is owned and operated by a group of 16 African (92%) and international (8%) shareholders ‐ all telecommunications operators and service providers. The EASSy consortium consists of the following members: WIOCC Mauritius Telecom, Mauritius MTN International Group British Telecom, UK Sudatel, Sudan Etisalat, United Arab Emirates SPV2 (Vodacom/Telkom SA) Zambia Telecom, Zambia Telma, Madagascar Saudi Telecom, Saudi Arabia Neotel, South Africa Comores Telecom, Union of Comoros BoFiNet, Botswana Bharti Airtel, India France Telecom, France TTCL, Tanzania

TEAMS (Int. NFP) Overall bandwidth provided for market 14.1% (Q2 2014‐15)

The East African Marine System (TEAMS) is an initiative spearheaded by the government of Kenya to link the country to the rest of the world through a submarine fibre optic cable. It was first proposed as an alternative to EASSy the East African Submarine Cable System. 85% of the cable is owned by TEAMs (Kenya) Ltd and the rest by Etisalaat of the United Arab Emirates (UAE). The TEAMS (Kenya) Ltd holding breaks down as follows: 42.5% – Telkom Kenya Ltd 1.25% – Broadband Access/AccessKenya Ltd 22.5% – Safaricom Ltd 1.25% – Africa Fibrenet (Uganda) Ltd 10% – Kenya Data Networks Ltd 1.25% – InHand Ltd 10% – Econet/Essar Telecom Ltd 1.25% – iQuip Ltd 5% – Wananchi Group 1.25% – Flashcom Ltd 3.75% – Jamii Telecom Ltd

LION2 (International NFP) Overall Bandwidth Provided for Market 4.8% (Q2 2014‐15)

Lower Indian Ocean Network (LION) is a submarine communications cable system that connects Madagascar, Réunion, and Mauritius It is 1,000 km long. It is capable of delivering up to 1.28 Tbps. The project was financed by a consortium made up of Orange Madagascar, Mauritius Telecom and France Telecom S.A.

VSAT ‐ Only 0.03% total of international internet available bandwidth market share:

1. KenSat (Telkom)

2. NyoyaSat (Gilat Alldean Ltd)

Finpro Digital Africa Growth Program Pre-study: Kenya

21 of 42

3. iWay Africa (Gondwana International Networks)

2.5.2 Internet/Data Market:

Wananchi Telecom Limited (retail brand “ZUKU”) (PDCC)/ Internet and data market share 48.8% Liquid Telecom Limited / Internet and data market share 15.7% Telkom Kenya / Internet and data market share 10.5% Safaricom Limited / Internet and data market share 7.2% Jamii Telecommunication Limited (“JTL”) / Internet and data market share 2.2% iWay Africa / Internet and data market share below 1.5% TESPOK (Telecommunication Service Providers Association of Kenya) plays a vital role in the market with

its operation of the KIXP (Kenya Internet Exchange Point):

2.5.3 Mobile telephony market:

Safaricom (MNO) mobile market share 67.4% (Q2 2014‐15) Bharti Airtel (MNO) mobile market share 22.6% (Q2 2014‐15) Telkom Kenya (Orange) (MNO) mobile market share 10% (Q2 2014‐15) Finserve (Equity Bank) (MVNO) mobile market share 1.5% (Q2 2014‐15)

2.5.4 Fixed telephony market:

Telkom Kenya (MNO) / Fixed telephony market share 100% (Q2 2014‐15)

2.5.5 Mobile money transfer service:

Safaricom (M‐PESA) market Share of mobile money services 77.4% (Q2 2014‐15) Airtel (Airtel M Commerce Services Ltd) market share of mobile money services 12.4% (Q2 2014‐15) Mobikash (MobiKash Afrika) market share of mobile money services 5.9% (Q2 2014‐15) Tangaza (Mobile Pay Limited) Market Share of Mobile Money Services 1.9% (Q2 2014‐15) Finserve (Equity Bank) Market Share of Mobile Money Services 1.5% (Q2 2014‐15) Orange Money (Telkom) Market Share of Mobile Money Services 0.7% (Q2 2014‐15)