financial counseling & y vulnerable · ment, the n banco popu invaluable their guida f the...

TRANSCRIPT

Findings from the Assessing Financial

Capability Outcomes (AFCO) Adult Pilot

FINANCIAL COUNSELING &

ACCESS FOR THE FINANCIALLY

VULNERABLE

April 2014

1

FINDINGS FRO

This repor039 for the AuthorsKasey WiNathalie J. MichaeAnita Dre

AcknowThis pilotand MonEmpower(formerlyprovidedCFED fordrafting o We woulimplemenshare wit New York• E• D Popular C• B• D• W New York• P• Jo• A All of theconclusioTreasury

OM THE ASSES

rt was preparee U.S. Depart

s iedrich Gons el Collins ever

wledgementt would not hnica Copelandrment, the Ny Banco Popud invaluable r their guidaof the finding

ld also like tntation of thth us their ex

k City Deparlizabeth Ehrl

Davida Rowle

Community Brian Doran, R

Dawn M. CarrWendy Scarle

k City Finanedro Salazaroseph FrewerAdalberto Jaim

e findings, coons and recom.

SSING FINANC

ed by the Corpment of the Tr

CFED NYC DepaCenter for CFED

ts have been pod from the NNew York Cular). Micharesearch assiance and inpugs and implic

to thank the he AFCO piloperiences wi

rtment of Parlich, Chief, Pey, Superviso

Bank Region Execurillo, Vice Prett , Vice Pres

cial Empower, Phipps Comr, Neighborhmes, Neighbo

onclusions anmmendation

CIAL CAPABILI

poration for Ereasury.

artment of CoFinancial Sec

ossible withoNew York CitCity Parks Oael Batty, andistance. Thanut throughoucations.

following reot for their cith the pilot.

rks & RecreaParks Opportor of Client S

utive, New Yesident, NY Msident, forme

erment Centemmunity Devhood Trust Fiorhood Trust

nd recommenns contained

ITY OUTCOME

Enterprise Dev

onsumer Affacurity, Unive

out the contrity DepartmenOpportunity d Karen Wank you also ut the design

epresentativecooperation i

tion, Parks Ounity PrograServices, Divi

York Metro RMetro Markeer Branch Ma

er Counselorvelopment Cinancial Partnt Financial P

ndations are in this repor

ES (AFCO) ADU

velopment (CF

airs Office ofersity of Wis

ibutions andnt of ConsumProgram an

alsh from UWto Ida Rademn and implem

es from the in this resear

Opportunity Pam ision of Educ

Region & Direeting Managanager

rs Corporationners

Partners

those of the rt are those o

ULT PILOT

FINANCI FOR T

FED) under c

f Financial Emconsin‐Madi

d cooperationmer Affairs Ond Popular CW‐Madison amacher and mentation of

organizationrch and for t

Program

cation and Tr

ector of Goveger

authors. Nonof the U.S. D

IAL COUNSELINTHE FINANCIAL

contract TOS‐

mpowermenison

n of Amelia EOffice of FinaCommunity and Kerry GLeigh Tivol f the pilot an

ns involved itaking the tim

raining

ernmental A

ne of the findDepartment o

NG AND ACCELLY VULNERAB

‐11‐F‐

nt

Erwitt ancial Bank

Griffin from

nd the

in the me to

Affairs

dings, of the

ESS BLE

2

FINDINGS FRO

DEPARTWASHIN April X, 2 Dear Coll The Depfinancial assesses taged chilstudents’actions. The findigovernmfinancial economy We are vWisconsinIndepend(TCEE), aparticipat As the Dability toWisconsinpractices Presidentagencies across othsimilarly

DEPARTMEWASHINGT April, 2014 Dear Colleag The Departmcounseling conducted oand financiamanage thei

These imporwell as the Americans s

We are veryWisconsin‐MParks Oppocontribution

These findinworking peoladder. We wAmericans, we encouraorganizationevaluation o

Best regards

Melissa KoidDeputy AssiU.S. Departm

OM THE ASSES

MENT OF TNGTON, D.C

2014

leagues:

artment of tknowledge the interplaydren. The re financial kn

ings in this ent, as well capability o.

very pleased n‐Madison, dent School and financialted in the pro

epartment coo make sounn‐Madison’sin this are

t’s Advisory in the Finanher levels of use the asses

ENT OF THE TON, D.C. 20

gues:

ment of the and financiaover two yearal counseling ir financial res

rtant findingsefforts of theso they are be

y pleased to Madison, the ortunity Progns of everyone

ngs will expaople manage will share theand our partge policy mans and social sof similar proj

s,

de istant Secretament of the Tr

SSING FINANC

HE TREASUC. 20220

the Treasuryand capabil

y of classroomsearch examnowledge, sa

report will as the effortsof young peo

to have wothe Eau CDistrict, Op institution poject.

onsiders polnd financial Center for Fea. MoreovCouncil on Fcial Literacy governmentssment, and

TREASURY 0220

Treasury is al access to rs, takes a rigo– that hold prsources and m

s will inform e private andtter prepared

have workedCity of New ram in the de involved in

and understatheir money, e findings wittner federal aakers across service providjects.

ry for Consumreasury

CIAL CAPABILI

URY

y is pleasedlity of younm financial e

mines how theavings pract

inform Treas of the privople and bet

rked with CClaire (Wiscopportunity Tpartners, and

icies that hedecisions, tFinancial Secver, the DepFinancial Capand Educatit, employersconsider furt

pleased to improve unorous look atromise to helpmove up the e

Treasury’s wd non‐profit sd to fully parti

d with CFEDYork’s Office

design and imthe project, in

anding of bestransition bath the Presideagencies in thall levels of ders to simila

mer Policy

ITY OUTCOME

to have cong people. Teducation anese two impotices, and at

asury’s workvate and nontter prepare

CFED, the Ceonsin) AreaTexas, the Td are grateful

lp young pethe findings curity shouldpartment wipability for Yion Commisss, financial inther research

have comminbanked Amtwo importap a populatioeconomic ladd

work and the wsectors, as weicipate in our

D, the Centere of Financialmplementationcluding the

st practices ack into the went’s Advisorhe Financial Lgovernment,arly use this a

ES (AFCO) ADU

ommissionedThe researchnd access to aortant strategttitudes and

k and the wn‐profit sectothem to ful

enter for Fina School DiTexas Councl to the teach

eople manageissued by Cd help expanll share theYoung Amersion. Finally,nstitutions, ah and evaluat

issioned this mericans’ finaant strategies on of particulader.

work of othere all seek to r nation’s econ

r for Financial Empowermon of the studstudy particip

as the Departworkforce, andry Council onLiteracy and , employers,assessment, an

ULT PILOT

FINANCI FOR T

d this reporth, conducteda savings accgies can affeconfidence

work of others, as we all lly participat

nancial Securistrict, the cil on Econohers, parents a

e their moneCFED and tnd our undee authors’ firicans, and ou, we encouraand social sertion of simila

report on lancial capabi– access to a arly vulnerab

r agencies acrbuild the finnomy.

al Security oment, and the dy, and we apants.

tment considd strive to mon Financial CEducation Cofinancial insnd consider f

IAL COUNSELINTHE FINANCIAL

t on buildind over two ycount for schct elementarin their fina

er agencies aseek to builte in our na

rity, UniversAmarillo (Tomic Educaand students

ey and growthe Universierstanding oindings withur partner feage policy mrvice providear projects.

everaging finility. The retransaction able Americans

ross governmnancial capab

of the UniverCity of New are grateful f

ers policies tove up the ecoapability for ommission. Fstitutions, adfurther resear

NG AND ACCELLY VULNERAB

ng the years, hool ‐ry‐age ancial

across ld the ation’s

ity of Texas) tion’s s who

w their ity of f best h the ederal makers ers to

nancial search, account s better

ment, as ility of

rsity of York’s for the

to help onomic Young Finally, vocacy rch and

ESS BLE

3

FINDINGS FRO

Conte

Introduct

Prior Stud

Pilot Desi

Bankin

Financ

Data ........

Analysis

Credit

Bankin

Financ

Summa

Insights f

Accoun

Accoun

Counse

Insights f

Reference

Appendix

Appendix

Appendix

Appendix

Appendix

Appendix

Appendix

OM THE ASSES

ents

tion ...............

dies ..............

ign and Impl

ng Access ......

ial Counselin

......................

and Results

Outcomes ...

ng Outcomes

ial Planning

ary of Findin

from Implem

nt Take‐up ...

nt Use and M

eling Take‐U

for Practice a

es ..................

x A: Full Sum

x A‐2: Indice

x A‐3: First S

x A‐4: Percen

x B: Compari

x C: Popular

x D: Survey I

SSING FINANC

......................

......................

lementation .

......................

ng ..................

......................

......................

......................

......................

Outcomes ...

ngs .................

mentation ......

......................

Maintenance .

Up ...................

and Policy .....

......................

mmary Table

es Created .....

Stage IV Estim

nt Missing D

ison of Samp

Community

Instruments .

CIAL CAPABILI

.......................

.......................

.......................

.......................

.......................

.......................

.......................

.......................

.......................

.......................

.......................

.......................

.......................

.......................

.......................

.......................

.......................

es ....................

.......................

mates .............

ata by Period

ple Demograp

y Bank Check

.......................

ITY OUTCOME

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

d ....................

phics to US P

king Account

......................

ES (AFCO) ADU

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

Population a

t and ID Req

......................

ULT PILOT

FINANCI FOR T

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

nd Populatio

quirements ...

......................

IAL COUNSELINTHE FINANCIAL

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

on in Poverty

......................

......................

NG AND ACCELLY VULNERAB

....... 4

....... 6

....... 8

....... 8

..... 10

..... 12

..... 15

..... 16

..... 18

..... 20

..... 21

..... 22

..... 23

..... 23

..... 24

..... 25

..... 29

..... 31

..... 34

..... 34

..... 34

y .... 35

..... 36

..... 37

ESS BLE

4

FINDINGS FRO

Introd

Approximamong vfour.1 Nobuild themanagemEnterprisMadison Empoweran averagtransition(AFCO) ppublic pr

Research financial these stufinancial strategiescounselinwhich ofunbanked

The AFCworkforcemploymservices Programsemploymtheir clienfinancial

1 Federal Dhttp://www2 For more Integrated Working FE25E‐4B20Domestic Vhttp://drup

OM THE ASSES

duction

mately one inery low‐incot only do theeir financialment of monese Developm(CFS), and rment (OFE)ge of one to ning off of pupilot study pogram.

suggests thknowledge, dies). Howeaccess as a

s. The AFCOng on the finfers personad population

CO pilot wae program:

ment programto a programs working ment, domestnts are givenfutures. Sim

Deposit Insuranw.fdic.gov/houon the potentiaApproach to Families Appro‐A005‐0DE98CViolence Advocpaldev.poverty

SSING FINANC

n twelve Amome househoese low‐incoml capability—ey. With sup

ment (CFED), the New Y partnered otwo hours oublic benefitsrovides uniq

hat the combbehavior, anver, researcha single treaO pilot assesnancial capaalized assistan.

as an effort the New

m for adults m already inwith clientstic violence an tools to bettmilarly, progr

nce Corporatiouseholdsurvey/2al impact of anFostering Familach.” http://ww

C2FA82C%7D., cacy.” Clearingylaw.org/sites/d

CIAL CAPABILI

merican houseolds the propme househol—the abilitypport from tthe Center f

York City Dn a pilot proof financial cs in New Yoque evidence

bination of find outcomesh to‐date largatment, withsses the comability and wance, seemed

to integratYork City moving off n place mays in financiand prisoner ter manage trams offerin

on. (2012). 20112012_unbanken integrated serly Economic Suww.aecf.org/Knand Kovach, Aghouse Review 43default/files/file

ITY OUTCOME

eholds do noportion that lds lack basicy to make the U.S. Depfor Financial

Department oogram to test counseling ork City. The of the causa

inancial edus (see Baker gely examinehout attemptmbined and well‐being ofd an appropr

e financial Parks Oppoof public asy improve tial transitionre‐entry pro

their money, ng financial c

1 FDIC Nationadreport.pdf rvices model seuccess: How ThnowledgeCenteAndrea. 2009. “3 (148). es/webinars/ass

ES (AFCO) ADU

ot have a cheis unbanked

c financial toinformed dpartment of tl Security at of Consumethe effect of

on the financAssessing F

al effects of co

cation and fand Dylla [2es the impacts to untangseparate imf unbanked riate interven

empowermeortunity Prossistance. Adthe odds of n such as ograms may improve thecounseling a

al Survey of Un

ee: The Annie Ehree Model Siteer/Publications“Integrating As

sets‐dv/kovach

ULT PILOT

FINANCI FOR T

ecking or savd jumps to mools, but theyecisions abothe Treasurythe Univers

er Affairs Oparing of fincial capabilityFinancial Capounseling pr

financial acc2007] for a rcts of financgle interactiompacts of fina

adults. Finantion for a h

ent services ogram (POPdding financiboth intervwelfare‐to‐wachieve stro

eir credit scoand bank acc

banked and Und

E. Casey Foundes are Implemes.aspx?pubguidsset‐Building S

h.pdf.

IAL COUNSELINTHE FINANCIAL

vings accountmore than oy may also neout the usey, Corporatiosity of Wiscoffice of Finanancial accesy of a populpability Outcrovided throu

cess may impreview of somial educationons or ‘bundancial accessancial counshistorically h

into an exP), a transitial empowerentions’ sucwork, transitonger outcomres and plancount access

derbanked Hous

dation. 2010. “Aenting the Centd=%7BF0C4C2Strategies into

NG AND ACCELLY VULNERAB

t, and one in eed to e and on for onsin‐ancial ss and lation comes ugh a

prove me of n and dling’ s and eling, highly

isting tional rment ccess.2 tional mes if n their s may

seholds.

An ter for 227‐

ESS BLE

5

FINDINGS FRO

also be msystems o

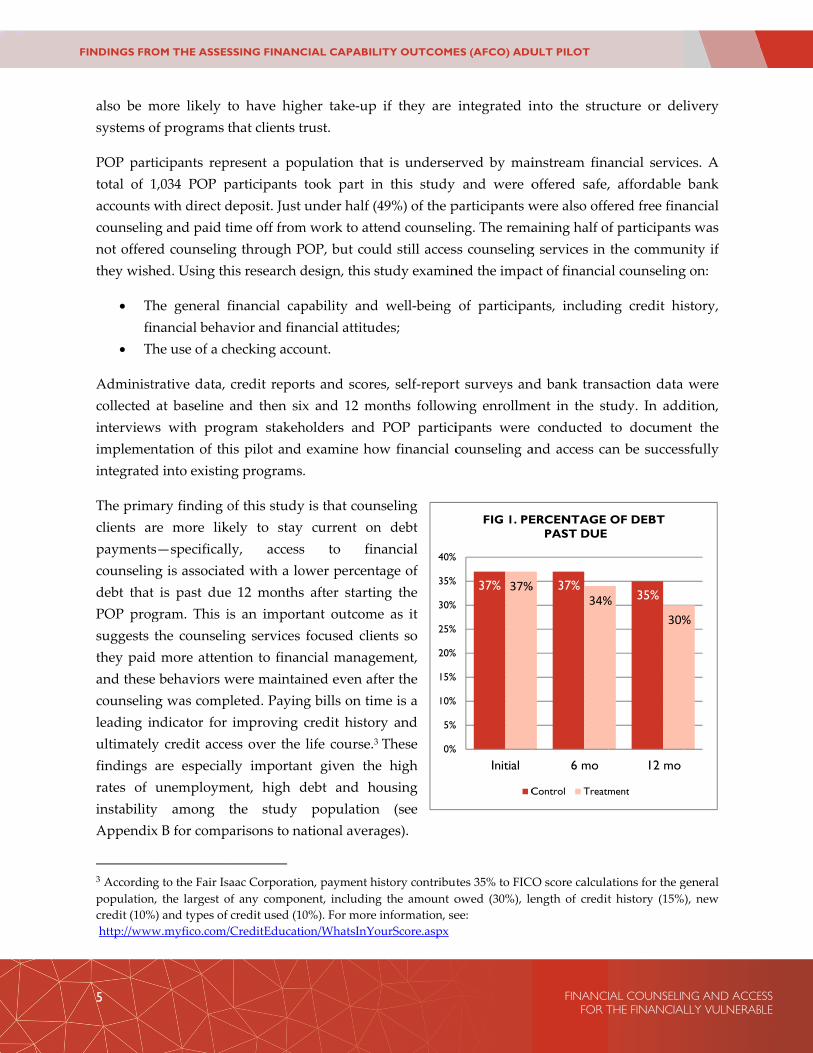

POP parttotal of 1accounts counselinnot offerethey wish

• Tfi

• T

Administcollected interviewimplemenintegrated

The primclients arpaymentscounselindebt thatPOP progsuggests they paidand thesecounselinleading inultimatelyfindings rates of instabilityAppendix

3 Accordinpopulationcredit (10% http://www

OM THE ASSES

more likely tof programs t

ticipants rep1,034 POP pwith direct dng and paid ted counselinhed. Using th

he general fnancial behahe use of a ch

trative data, at baseline

ws with progntation of thd into existin

mary finding ore more liks—specificallng is associatt is past duegram. This ithe counselid more attene behaviors wng was compndicator for y credit acceare especialunemploymy among x B for comp

ng to the Fair Isn, the largest o%) and types of w.myfico.com/

SSING FINANC

to have highthat clients tr

present a popparticipants deposit. Just time off fromng through Phis research d

financial capavior and finahecking acco

credit reporand then sixgram stakehhis pilot and ng programs.

of this studykely to stay ly, accessted with a loe 12 monthsis an importing services ntion to finanwere maintaipleted. Payingimproving

ess over the lly importan

ment, high dthe study

parisons to na

saac Corporatioof any componcredit used (10/CreditEducati

CIAL CAPABILI

her take‐up rust.

pulation thattook part inunder half (4

m work to attePOP, but couldesign, this st

pability and ancial attitudount.

rts and scorex and 12 moholders and examine how.

y is that councurrent on

s to finower percentaafter startin

tant outcomefocused cliencial manageined even aftg bills on timcredit historlife course.3

nt given thedebt and hopopulation

ational avera

on, payment hinent, including0%). For more ion/WhatsInYo

ITY OUTCOME

if they are

t is undersern this study 49%) of the pend counselinld still accestudy examin

well‐being des;

s, self‐reportonths followPOP particiw financial c

nseling n debt nancial age of ng the e as it nts so ement, ter the me is a ry and These e high ousing

(see ges).

istory contributg the amount oinformation, seourScore.aspx

0%

5%

10%

15%

20%

25%

30%

35%

40%

ES (AFCO) ADU

integrated i

rved by maiand were o

participants wng. The remass counselingned the impac

of participa

t surveys anwing enrollmeipants were counseling a

tes 35% to FICOowed (30%), leee:

37% 37%

%

%

%

%

%

%

%

%

%

Initial

FIG 1. PE

C

ULT PILOT

FINANCI FOR T

nto the stru

instream finaoffered safe,were also offeaining half og services in ct of financia

ants, includin

nd bank transent in the stconducted

and access ca

O score calculaength of credit

37%%34%

6 mo

ERCENTAGE PAST DUE

Control Treatm

IAL COUNSELINTHE FINANCIAL

ucture or del

ancial servic, affordable ered free finaf participantthe communal counseling

ng credit hi

saction data tudy. In addto documenan be succes

ations for the gt history (15%

35%%30%

12 mo

OF DEBT

ment

NG AND ACCELLY VULNERAB

livery

ces. A bank ancial ts was nity if g on:

story,

were dition, nt the sfully

general ), new

%

ESS BLE

6

FINDINGS FRO

The data significanthat can counselinparticipanfrom abohelped tobarriers tbe instrucprograms

This studbenefits aEducation

• Idof

• Eefkn

• Idin

• Idp

The remaof the prprogram analyzed documen

Prior

In the Un1970s, mureview). Mnon‐randcounselinnot partic

OM THE ASSES

in this studnt improvembe causally

ng, althoughnts being baout a third to document ato enrolling ctive to others.

dy offers a uand addressn Commissio

dentify and ef high qualityvaluate the ffective appnowledge, pdentify, evaluncluding meadentify oppolatforms for

ainder of thisior research and study din this rep

ntation of the

Studies

nited States, uch of whicMany evaluadom comparing, comparincipate in cou

SSING FINANC

dy do not suments in bank

linked to ah the overallanked increato over half.a range of perin bank accor public and

unique look es several oon in 2012:

evaluate the y financial prdelivery of roaches, delroducts, anduate, and buasures of knoortunities anfinancial cap

s paper is orgon financial

design, Sectioport, Sectionimplementa

s

there is genh focuses onations are desson group. Fng clients whunseling. Whi

CIAL CAPABILI

upport statistking access oaccess to finl rate of allased dramat This projecrceived and aounts, whichcommunity‐

at the finanf the researc

relationship roducts. financial ed

livery channd behaviors) tuild consensuowledge, behnd roles forpability.

ganized into l counseling on 4 describn 5 describeation, and Sec

eral literaturn mortgage scriptive andFor example, o received coile the initial

ITY OUTCOME

tically or use ancial l POP tically ct also actual h may ‐based

ncial lives ofch priorities

between fin

ducation fornels, and otthat enhance us on “key mhavior, and wr local, state

the followingand use of es the data ces the researction 7 offers

re on financipayment issd lack a compElliehausen ounseling to l analysis ind

0%

15%

30%

45%

60%

75%

ES (AFCO) ADU

f a populatioidentified b

nancial educa

r youth andther factors effectivenesmetrics” for fwell‐being. e, and fede

g sections: Sefinancial sercollected durrch findingss insights for

ial counselinsues (see Colparison groupet al. (2007) a non‐randodicated that c

40%

36%

Initial

FIG 2

ULT PILOT

FINANCI FOR T

on transitionby the Finan

ation and acc

d adults in (such as th

ss. financial edu

eral governm

ection 2 provrvices, Sectioring the pilos, Section 6 practice and

ng that dates llins & O’Rop, or they coevaluated th

om compariscounseling le

67%

57%

6 mo

. PERCENTA

C

T

IAL COUNSELINTHE FINANCIAL

ning off of pncial Literacy

cess to and d

order to idehe interactio

ucation/capab

ments as sca

vides an overon 3 describeot and the sasummarize

d policy.

back to the ourke, 2010, ompare clienthe effects of con group thaed to conside

57%

56%

12 mo

GE BANKED

Control

Treatment

NG AND ACCELLY VULNERAB

public y and

design

entify on of

bility,

alable

rview es the ample es the

early for a ts to a credit at did erable

ESS BLE

7

FINDINGS FRO

improvemafter conta random

Studies oplanning 2008). Thhigher rastudies ofinancial

No prior a checkinoverdraftidentificaor have ninvolved,eligibility(Prescott concerns Unbankebanked h(Agarwalunexpect

Direct derecurring(Beverly spend “cpersonallawarenes

Overall, focused) direct deemployeenone inclquasi‐expprovides foundatiovulnerabl

OM THE ASSES

ments in credtrolling for wmized design

of workplaceand saving

hese studies ates of particif workplace‐managemen

studies haveng or savingts or unauthoation (Fine, Lnot gotten aro, while othey for public & Tatar, 199contribute td householdhouseholds, l et al., 2011)ed negative i

eposit has bg, potentiallyet al., 2003; cash in handly (Bertrandss, understan

the financiacounseling aeposit functioes. But few slude a combiperimental frseveral uni

on of new resle population

SSING FINANC

dit scores thrwhich clients that allows f

e‐based finans education are suggestipation and c‐based financnt outside of r

e examined tgs account). Porized use (BLeimbach, & ound to openrs are hampassistance p99; O’Brien, to the indivds may find as lenders . Without acincome or ex

been describy difficult decBeverly et ad,” it also r et al., 2006nding, and tru

al capabilityand access toon—are disctudies examination of coramework toique potentisearch on intns.

CIAL CAPABILI

ree years aftesought helpfor estimating

ncial capabilseminars (Btive that emcontribution cial counselinretirement sa

the effects of People may Barr, 2004; RJacob, 2006) ning an accoupered by theprograms (O2012). Addi

vidual’s deciit more diffhave limite

ccess to finanxpenditure sh

ed as a “prcisions into aal., 2008). Neduces the 6). Offering ust of direct

strategies io low‐fee trancussed in priine a populaounseling ano facilitate aial contributtegrated fina

ITY OUTCOME

er counselinp. Other studg causal effec

lity interventernheim & G

mployer‐baserates for retng on lower‐avings.

counseling obe unbankeomich et al.,or because tunt. Some pee perception O’Brien, 2006tionally, distsion to remficult to acceed means bncial liquidityhocks.

re‐commitmea single, perhot only mayfinancial andirect depodeposit by p

included in nsactional acior studies aation as finand banking aca causal anations to the ancial capabil

ES (AFCO) ADU

g, the estimaies follow a cts of counse

tions have mGarrett, 2003d financial tirement acco‐income peop

on being unbed due to re, 2010), lack they either ceople do not hn that having6) or could ttrust of finanain unbankeess or receivby which toy, people ma

ent” constrahaps easier, y direct depond time‐relatosit to partiroviding exp

this study—ccounts, incluas potentiallncially distreccess. Prior salysis of finaliterature ality and acce

ULT PILOT

FINANCI FOR T

ated effects dsimilar patteeling.

mainly focus3; Bayer, Bereducation isounts. But thple related to

banked (definestrictions suof accepted fchoose not tohave accoung formal savtrigger collencial instituted (Barr & ve a line of o determine ay become m

aint that condecision to uosit reduce tted costs of icipants couperience with

—financial (uding an emy being appessed as POPstudies also ancial counsand ideally ess focused in

IAL COUNSELINTHE FINANCIAL

decreased shern, largely d

sed on retirernheim & Scs associated here have beeo basic house

ned as not huch as unresoforms of pero open an accnts due to thevings could ections judgmtions and prSharraden, 2credit relaticreditworth

more vulnerab

nverts a seriuse direct dethe temptatimaking dep

uld increase h its use.

(primarily cmployer‐supppropriate forP participantslack a formaeling. This scan serve an low‐incom

NG AND ACCELLY VULNERAB

harply due to

ement cholz, with en no ehold

aving olved rsonal count e costs harm ments rivacy 2005). ive to hiness ble to

ies of eposit ion to posits their

credit‐ported r POP s, and alized study as the e and

ESS BLE

8

FINDINGS FRO

Pilot D

POP is onCity’s Decoupled w6,000 aduplaygrouThroughohorticultuservices a11,000 tra

POP partFamilies AdministPOP proghealth anDuring themployeesecure emParticipanjob‐readinand comp

The Newmanagedspecialistformer POscript usethe studysite at POand impl

BANKING

All particCommun

4 One borohave brancfor the pur

OM THE ASSES

Design a

ne of the naepartment ofwith job searults receivingnds and recout the progure, adminisand career cainees into fu

ticipants are (TANF) at

tration, the agram who hnd substancehe six‐ mones of the Parmployment dnts cycle thrness trainingputer classes

w York City d the implemts” to assist wOP participaed in the offey to POP empOP locations ement the pi

G ACCESS

cipants enronity Bank (fo

ough – Staten Iches in that borposes of the stu

SSING FINANC

and Imp

tion’s largesf Parks and rch counseling public assisreation centegram, POP stration, macounseling. Sull‐time posit

heads of houthe time

agency that aave been scre abuse issueth program,rks Departmduring the prough the prg. Participantin preparati

Departmententation of thwith the enronts on what er of bank acployees. Betwacross four ilot.

olled in the ormerly Banc

Island – was exrough; this is audy.

CIAL CAPABILI

plement

t transitionaRecreation,

ng and other stance annuaers, with theparticipants

aintenance aSince its incetions.

usehold whoof POP enadministers treened for “wes, physical c participants

ment. The parprogram, androgram buildts may also eon for privat

t of Consumhe research pollment in anmessages anccounts, finaween JanuaryNew York C

study were co Popular).

xcluded from also the smalle

ITY OUTCOME

tation

l employmenPOP providhuman capi

ally. POP pare goal of tras gain transfand customeeption in 199

o have been rnrollment. Ththe City’s TAwork‐readinecapability ans work 35 hrticipants’ god transition ding their skenroll in edute sector emp

mer Affairs Opilot and hirend implemennd real‐life exancial counsey and early MCity borough

offered checThe account

this study in pest POP site an

ES (AFCO) ADU

nt programsdes six monital enrichmerticipants woansitioning toferable skiller service w94, the traini

receiving Temhe New YoANF programess,” which ind the abilityhours per weoal is to prefrom public kills in weekucation (GEDployment.

Office of Fined three formntation of thixamples resoeling and theMay 2012, thhs4 to enroll P

cking account offered to p

part because Pnd was unlikely

ULT PILOT

FINANCI FOR T

s. Administernths of full‐tent activities ork in New Yo private secs in fields while receiving program

mporary Assork City Hm, refers eligincludes screy to take direek earning epare for, seaassistance t

kly specializeD, adult basi

nancial Empmer POP paris study. Feenated with the opportunityhe POP speciPOP particip

nts by a locparticipants i

Popular Commy to provide en

IAL COUNSELINTHE FINANCIAL

red by New time employto approximYork City’s pctor employmsuch as secving employm has placed

sistance for NHuman Resogible clients teening for mrection in En$9.21 an hoarch for andto self‐sufficied vocationaic education,

powerment (rticipants as edback from hem informey to participaialists workepants in the s

cal bank, Pois a ‘safe’ acc

munity Bank donough client v

NG AND ACCELLY VULNERAB

York yment mately parks, ment. curity, yment d over

Needy ources to the mental nglish. our as d find iency. al and ESL)

(OFE) “POP these ed the ate in ed on‐study

opular count

oes not volume

ESS BLE

9

FINDINGS FRO

with no dunintentirequiremCommunpast probanother employeeflexibilitiethe POP p

During thaccounts participanopening atheir accoaccounts.individuaaccount oparticipan

Study paopportunprofessiotouch” finthe termsaccounts.deposit, i

The respoParks Depup for dimplemendeposit. Tbanked w 5 Without insufficientinsufficient6 Take‐up obanked sigone‐third othe month

OM THE ASSES

direct markeionally incur

ment, and fenity Bank alsblems with ainstitution be addresses tes are an impopulation.

heir POP oriand direct dnt already haand answer qount number. At the bankal’s ability toopening wasnts received

rticipants whnity to open anal developmnancial educs of the Pop. At this secoin to any type

onse to the bpartment expdirect depositntation of thThe high takewhen given a overdraft prott funds in thet funds fees weof direct deposgned up for dirof the study saprior to POP.

SSING FINANC

eting of an orring overdrw other reqso agreed to a transactionbelow $100 to suffice as “

mportant featu

entation daydeposit of thead a card). Aquestions abr that day ank branch follo open the as not possiblbasic inform

ho did not oan account anment day. Acation focusepular accounond offer, ale of account

bank accountpected. A tott and 49% ahe AFCO pe up of accouaccess to an tection, point‐oe account, limere applied. sit is higher tharect deposit tomple had a ba

CIAL CAPABILI

overdraft proraft fees.5 Thquirements provide flex

n account. Inwere forgiv“proof of addure of this p

y, the POP speir City paycA Popular staout the accound were abllowing the oaccount and le (for examp

mation about d

open an accound enroll in dAt this second on short tet. Popular stll participantat any financ

t and direct dtal of 55% of applied for ilot, approxiunts suggestsaccount with

of‐sale purchasmiting the accr

an take‐up of to their existingank account in

ITY OUTCOME

otection optihe accounts (see Appenxibility in opn most casesven. The badress,” a requrogram give

pecialists offechecks to eithaff member wunt and banke to fill out pening on‐sinotified theple, due to adirect deposi

unt with Popdirect deposind presentatierm and longtaff was agats were offercial institutio

deposit offersthe total POPa new checkimately 15%s unbanked ph agreeable

ses or ATM wrual of overdr

the Popular accaccount (checthe month prio

ES (AFCO) ADU

ion, intendedalso had no

ndix C for tpening accous, those withank also alluirement when the histori

ered all POPher a bank awas present oking more gedirect deposite, the banke client by pha negative Cit and accoun

pular at orienit approximaion, the POPg term financain on‐site tored a $25 incon, not just th

s was more eP participantking accoun% of POP paparticipants terms. Howe

withdrawal reqraft fees. How

counts as somecking account oor to joining P

ULT PILOT

FINANCI FOR T

d to protect o minimum the account unts for POPh outstandinowed emplohen opening ically under‐

P employees account or pron‐site to facenerally. Parsit forms whk representatihone or letteChexSystemsnt benefits an

ntation wereately two weP specialistscial goals, ano answer qucentive for ehe Popular ac

enthusiastic ts enrolled innt with Popuarticipants ehad a strongever, even w

quests were dewever, there w

e participants tor a prepaid cOP and 31% h

IAL COUNSELINTHE FINANCIAL

participants monthly baterms). Po

P employeesng funds owoyer letters an account. T‐banked natu

Popular cherepaid card (ilitate the accrticipants rechile opening ive confirmeer in cases w report). Allnd use.

e offered a seeeks later at a provided “nd again reviuestions and enrolling in dccounts.

than OFE ann the study siular.6 Prior tenrolled in dg desire to bewith the flexi

enied in the cwere instances

that were prevard). Approximhad a prepaid c

NG AND ACCELLY VULNERAB

from alance opular s with wed to

with These ure of

cking (if the count ceived their ed the where l POP

econd a POP “light‐iewed open direct

nd the igned to the direct ecome ibility

case of when

viously mately card in

ESS BLE

10

FINDINGS FRO

Popular third of tmany casBank conparticipansome prinegative $38 to $6,

FINANC

As part oto attendprovidedoffer finaparticipanmoney mdebt manthis clientmight adnegotiateclients’ emfull finanplan of arepair, reand partisession. Psessions m

At the POfacilitatedfinancial randomizuse indivconcerns comparisrandomlycorrelatedapproximoffer counof site‐sp

OM THE ASSES

Community the participanses, due to nenducted on tnts or 46% hor misuse obalances ow,423. Only 33

CIAL COUN

of the field ex one‐on‐one

d by New Yorancial counsents. Center cmanagement,nagement. Fot group withddress transie problems wmployment sncial health action for addeducing debt icipants offerParticipants may also hav

OP professiod the scheducounseling

zed by monthvidual randothat co‐work

sons. During y assigned tod with diffmately half thnseling becaecific effects,

SSING FINANC

Bank provints who appegative Chexhe 175 partichad ChexSystf an account

wed on previo3 profiles in C

SELING

xperiment, afinancial courk City’s Fineling at over counselors a budgeting, or the purpoh reference toitioning fromwith prior basituations chassessment thdressing a raand planninred counselinalso had theve been comp

nal developmuling of appotreatment ih of hire andom assignmekers would cthe first halo offer finanferences bethe participanme the sites , as well as ʺt

CIAL CAPABILI

ding in openplied for a chxSystems repcipants whotems profilest, e.g., owingous accountsChexSystem r

bout one‐halunseling durnancial Empo20 locations

are trained toselecting sases of this pio direct depom the use oanks, or thehange. Howehat looked atange of needsng for future ng were crede option to rpensated at th

ment day, thintments forin this studd by boroughent for severcommunicatf of the studncial counselitween sites,nts were recroffering coutreatmentʺ ef

ITY OUTCOME

ning accounhecking accouports. Accord there was ns. Most of thg a balance s were less threported frau

lf of the POPring their prowerment Ce citywide to o help clientafe and afforilot, counseloosit and the Pf alternativee maintenancever, the count their financs such as: buneeds. Sessiodited a full dreturn for a he counselor

he POP specir those particdy was not h in which thal reasons, ie about whady period, POing to partic, the counruited. At thunseling as shffects, in isola

ES (AFCO) ADU

nts through tunt on‐site ading to an anano record of he negative Con a previohan $500, buudulent activ

P employees escribed worenters, whichall New Yorts on a rangrdable financors were infoPopular accoue financial sce of accounnselors also ces overall anudgeting for ons lasted beay of work wsecond sessir’s recommen

ialists introducipants who offered to

he POP site wincluding logat they learneOP sites in twcipants. Becaseling assighis point, thehown in Tabation.

ULT PILOT

FINANCI FOR T

the pilot, apat POP couldalysis by Popan account

ChexSystem ous account. ut the range ovity on a prev

were offeredrk hours. Thh were establrk City residge of financiacial productsormed of theunts. For exaervices, hownts and direcengaged witnd helped thtransitions, etween 30 mwith pay to aion on workndation.

uced financisigned up foevery part

was located. Tgistical comped in counsewo of the fouause treatmegnment wase sites that dble 1. This pe

IAL COUNSELINTHE FINANCIAL

pproximatelyd not open onpular Commbeing openeprofiles indiOver 60% oowed varied vious accoun

d the opporthe counselinglished in 200dents at no coal issues, sus, and credie unique neeample, counsw to addressct deposit shth each clienhem to estabcredit review

minutes to an attend their ik time. Addit

al counselingor counselingticipant, butThe study diplexity as weling and biaur boroughs nt effects ms switched did not previermits an an

NG AND ACCELLY VULNERAB

y one‐ne, in

munity ed, 81 icated of the from

nt.

tunity g was 8 and ost to uch as t and eds of seling s and hould nt in a blish a w and hour, initial tional

g and g. The t was id not

well as as the were ay be after

iously alysis

ESS BLE

11

FINDINGS FRO

TABLE 1.

Borough

Bronx

Brooklyn

Manhatta

Queens

Accordincounselinparticipancounselinfour and the compacross thepart. Becathat woucounselinpresentatbeing offe

TABLE 2.

AttendedNo CounTotal

The unbiaccount aemployeetime periinherent i

7 This estimwho were month of sprior knowpredict if ait is the est

OM THE ASSES

FINANCIAL

Janua

an

ng to adminng actually ants in the cng session, 3213 sessions. parison (or ce counselingause the choiuld bias the ng using a twtion of averagered counsel

TAKE UP OF

d FEC seling

iased effects access cannoes and there od. There is in which clie

mate is more pmost likely to starting in POPwledge of the all clients particimated effects

SSING FINANC

EDUCATION

R

ary-February

FEC offer

FEC offer

No FEC offer

No FEC offer

nistrative daattended coucomparison 2% attendedTable 2 showcontrol) groug group are dice to seek coresults, we iwo‐stage leage ʺintent to ing and actu

F COUNSELIN

Counseling G

186 319 505

of counselint be estimatewas no varianot a way toents selected

precisely the Lobe induced intP. It is valid asoffer of counscipated in counof for the marg

CIAL CAPABILI

N CENTER CO

ecruitment Pe

y 2012

r

r

ata, approxiunseling at agroup. Just

d two or threws the numbeup by counsdiffused by tounseling is ninstead use st square instreatʺ as we

ually receivin

NG AT NYC F

roup C

ng can be esed in a similation in acceo identify theto open and

ocal Average Tto counseling b long as peoplseling‐‐which snseling, nor theginal client ind

ITY OUTCOME

OUNSELING O

eriod

March-May

No FEC o

No FEC o

FEC offe

FEC offe

imately 186 Financial Eover half

ee sessions, aer of clients iseling attendthe nearly twnonrandom acounseling gstrumental vll as estimate

ng counseling

FINANCIAL E

Comparison

2527529

stimated usinar way. Accoess to accoune effects of acuse accounts

Treatment Effecby assignment be did not seekseems highly pe effect just amuced into coun

ES (AFCO) ADU

OFFER TREAT

y 2012

offer

offer

er

er

(37%) parEmpowermenof participaand the remain the counsedance. The awo‐thirds of cand correlategroup membvariable appred ʺtreatmeng.7

MPOWERME

To

188410

ng this reseaounts were onts or the proccount accesss.

ct (LATE). It rebased on the r

k out POP serviplausible. It is

mong clients monseling by assig

ULT PILOT

FINANCI FOR T

TMENT ASSI

rticipants whnt Center, asnts (53%) aaining 15% aeling (or treaaverage effeclients (63%)ed financial obership to proach (2SLS‐nt on treatedʺ

ENT CENTERS

otal

8846034

arch design, offered univomotion of as that can ov

epresents the erandom nature ices and locatis not the sameost interested ingnment (hence

IAL COUNSELINTHE FINANCIAL

GNMENT

ho were ofs well as jusattended justattended betatment) groupects of couns) who do notoutcomes in predict take u‐IV). This peʺ effects relat

S

but the effeersally to allaccounts by svercome the b

effects among of POP locatioons because ofe estimate we n counseling. R the ʺlocalʺ labe

NG AND ACCELLY VULNERAB

ffered t two t one tween p and seling t take ways up of ermits ted to

cts of l POP site or biases

clients on and f some might

Rather, el).

ESS BLE

12

FINDINGS FRO

Data

The data baseline ajuncture participanis summparticipatadministrbanking characterparticipanparticipatdata collenrollmenparticipansurvey byremaininsurveys wrate was 4pre‐incenbasis andthrough J

Data regathen at siwere accebaseline pparticipan

Credit restatus, avThese repon negatiof study Appendixaddition, those wit 8 The repor

OM THE ASSES

for this studand six and 1as it coincidnts it marks

marized in Ttion, demogrrative data status and firistics was ants between te. These clielection. A font at POP ents’ employmy mail. Apprg 61% admiwas 58%. All48%. Mailed ntives and $1d the last clJuly 2013.

arding debt ix and 12 moessed througparticipant sntʹs Social Se

eport recordsvailable crediports represeive items sucparticipantsx A‐4), but ojust over hath a credit r rts were condu

SSING FINANC

y consists of 12 months frodes with thetheir entry in

Table 3. Theraphic charaon counselininancial situadministeredJanuary an

ents also receollow‐up suexit seminarment with Proximately 3nistered thro 12‐month fo12‐month su

10 metro cardlient was rec

levels, delinonths after engh TransUniosurvey data uecurity numb

s used in thiit, as well as ent a snapshoch as delinqu at baseline.only 80% of alf (55%) of streport availa

ucted as “soft pu

CIAL CAPABILI

a combinatioom enrollmee end of parnto unemploe Parks Depcteristics andng attendancation, behavd on‐site dud May 2012eived a $25 grvey was ars, as the siPOP. Partici39% of the siough the maollow up survurveys used d post‐incentcruited in ea

quencies, annrollment usion, read intousing a combber.8

is project conpublic recordot of credit auency and ban The rate ofparticipantstudy participable, as man

ulls” and were

ITY OUTCOME

on of self‐repnt in the studrticipants’ enoyment. The partment prod post‐progrce. In additiviors, and atturing study were recruigift card to codministered ix‐month dapants not atix‐month surail, and the cveys were ala three‐wavetives. Becausarly May 20

nd credit utiling extracts fo a machine bination of d

ntain data ond informatioat a point in tnkruptcy. Crf missing reps have credipants do not ny as 40% d

e not recorded a

ES (AFCO) ADU

ported and addy. Six montnrollment innumber of rovided admram employmtion, a baseltitudes as wrecruitmentited, and 1,0ompensate that all POP

ata collectionttending therveys were acombined rell completed e design withse participan012, follow‐u

lization ratesfrom printedreadable fordate of birth

n outstandinon such as batime, but alsredit reports ports overallt report datahave a credi

do not have

as an inquiry th

ULT PILOT

FINANCI FOR T

dministrativths post‐enron POP and frecords from

ministrative dment data, anline survey

well as collectt. Approxim034 participahem for theirP sites six mn coincided e exit seminadministeredesponse rate via the mailh two remindnts were recrup data colle

s were collecd credit reporrmat and theand the last

ng debt, payankruptcy filiso contain hisare unavailal declines ova in all perioit score repora credit sco

hat could harm

IAL COUNSELINTHE FINANCIAL

e data collectollment is a crfor two thir

m each data sdata on prond OFE provassessing cuting demogrmately 1,300 ants consentr time involvmonths followith the en

nar were send on‐site, witfor all six‐ml and the respder postcarduited on a roection took

cted at intakerts. Credit reen matched tfour digits i

yment historyings and tax storic informable for abouver the studyods examinerted. Even amore reported

m credit history

NG AND ACCELLY VULNERAB

ted at ritical rds of ource ogram vided urrent raphic POP

ted to ved in owing nd of nt the th the month ponse s, $10 olling place

e and eports to the in the

y and liens.

mation ut 15% y (see ed. In mong from

y.

ESS BLE

13

FINDINGS FRO

TransUniaccounts.

For particprovidedaccount dto the 49%is due topreviousl

TABLE 3.

Credit Re

Credit Sc

Survey

Bank Rec

Table 4 scomparisvery finaexpected and one‐ithe montmoney orconsider report did

TABLE 4:

AttendedMale Age Married Have ChiPublic HoHomelesBanked Use AlterSelf-RepoIn ControSavings ($Debt (excCredit Sc

OM THE ASSES

ion. This is l.

cipants who d data on modata is availa% of clients wo several factly reported b

SAMPLE SIZE

eport

core

cord

summarizes son groups. Bncially vulnefor a populain‐five live inth prior to enrders and cha good credid not have en

BASELINE C

d FEC

ildren ousing/Stayins

rnative Finanorted Financiol of Finance$) cluding mortcore

SSING FINANC

largely due t

opened a Ponthly accouable for apprwho applied tors: the numbut also the in

E BY DATA S

selected aspeBaseline dataerable population transitin a homelessnrolling in Pheck cashers. it score, althnough credit

HARACTERIS

ng with Frien

ncial Servicesial Literacy (s (5pt)

tgage) ($)

CIAL CAPABILI

to people ha

opular checkunt balances roximately 32to open accomber of POPnability to m

SOURCE

Baseline

884

415

1034

ects of the oa on the POPlation from toning off of s shelter. AppOP, and 74%The averageough as statt history or ac

STICS OF STU

nds

s 5pt)

ITY OUTCOME

aving little fo

king accountand fees fro2% of study ounts with PoP participantatch records

6-Mo

99

44

59

334

overall study participantsraditionally public benefproximately % report usine credit scoreed above, almctivity to hav

UDY PARTIC

Total18.2%22%35.58.5%76%24%20%34%74%3.32.8122

5,316558

ES (AFCO) ADU

ormal credit

t and signedom January 2participantsopular Commts who weredue to missi

onth

98

49

99

y population s enrolled in disadvantagfits. Most areone‐third repng alternative of 558 is wemost half of ve a credit sc

IPANTS

Counseling 36.8%27%35.68.3%73%25%19%33%72%3.32.888

4,817561

ULT PILOT

FINANCI FOR T

activity or h

d a data relea2012 throughs, a relativelymunity Banke unable to ing data field

12-Month

997

449

499

and then ththe study pa

ged commune single womport having ve financial sell below whthe particip

core.

Group C%

%6%%%%%%

7

IAL COUNSELINTHE FINANCIAL

having few a

ase form, Poh June 2013. y low rate rek. The lack ofopen accounds.

he counselingaint a portrainities, as woumen with chila bank accouervices, incluhat lenders wants with a c

Comparison G0.4%16%35.48.7%79%23%21%35%75%3.42.8156

5,901555

NG AND ACCELLY VULNERAB

active

opular Bank lative f data nts as

g and it of a uld be ldren, unt in uding would credit

roup

ESS BLE

14

FINDINGS FRO

Looking comparishousing, gender, smore savhold up effects wo

Table 5 ssources. Tpercent mnon‐respocomparabpeople wthese oth

TABLE 5.

CounselinAttendedMale Age Married Have ChiPublic HoFriends HomelesBanked Use AlterServices In ControSelf-RepoSavings ($Debt (excCredit ScOBSERVA* = baseline

The final trajectoryinstitutionparticipanmonths aprogram:assistance

OM THE ASSES

at the characson group arbeing bank

savings and vings and deto common ould be appr

summarizes The last linemissing in Aonse bias. Thble in most r

who indicate ter factors are

BASELINE C

ng Group d Counseling

ildren ousing/Stayin

s

rnative Finan

ol of Financeorted Fin. Lit$) cluding mortcore ATIONS e data

aspect of they in terms of ns (See Tabnts who repand still ove: employmene with the g

SSING FINANC

cteristics of tre comparablked and selfdebt levels, ebt (and perhstatistical teropriate.

these same e shows the tppendix A‐4his table shoespects. The they are home statistically

HARACTERIS

ng w/

ncial

s (5pt) teracy (5pt)

tgage) ($)

e data worth improving c

ble 6). The mport being ber half at 12 nt. POP is a tgoal of movin

CIAL CAPABILI

the participanle on some vf‐reported finappear skewhaps more fiests, but do

variables batotal numbe4). One conceows that that12‐month fo

meless. Surpr different.

STICS BY SUB

Total

48.8% 18.2% 22% 35.5 8.5% 76%

24%

20% 34%

74%

3.3 2.8 122

5,316 558

1,034

noting is thacredit scores, most dramatanked, movmonths. Tabtransitional eng people in

ITY OUTCOME

nts by treatmvariables, sunancial literawed such thainancial activsuggest that

ased on whicr of participern with higt selected asollow up wasrisingly, give

BPOPULATIO

Credit Report*

49.4% 18.3% 22% 35.6 8.5% 76%

24%

20% 34%

73%

3.3 2.8 119

5,316 558 879

at all POP embeing banketic change oing from onble 6 also deemploymentnto unsubsid

ES (AFCO) ADU

ment group, uch as age, macy and attiat the compavity in genert including c

ch participanpants in eachgh rates of mspects of the s (predictablyen the magni

ON WITH EA

Credit Score*

6

44.6% 19% 17% 35.7 9.8% 76%

23%

16% 45%

75%

3.3 2.7 105

9,761 558 415

mployees seeed and reducover the stune‐third at bemonstrates t program fodized employ

ULT PILOT

FINANCI FOR T

the counselimarital statusitudes. Othearison groupral). These dcontrol varia

nts are incluh form of datmissing data ioverall study) less likely itude of miss

ACH DATA SO

6-Month Survey

12S

45.7% 17.5% 22% 37.5 7.2% 73%

24%

15% 37%

73%

3.3 2.7 87

6,496 562 599

m to be on aced use of altudy period ibaseline to athe key pur

or people comyment. The

IAL COUNSELINTHE FINANCIAL

ng group ans, living in per items, sup appears to differences dables in estim

uded in eachta (also showis the potentdy populatioto be reportsing data, no

OURCE

2-Month Survey

BD

48.5% 418.6% 125% 38.5 8.0% 870%

25%

12% 37%

77%

3.3 2.8 124

5,977 4562 499

a positive finaternative finais the percealmost 60% arpose of theming off of psix‐month su

NG AND ACCELLY VULNERAB

nd the public ch as have

do not mated

h data wn as tial of on are ed by one of

Bank Data

45.8% 7.4% 15% 34.2 8.4% 81%

25%

20% 28%

76%

3.3 2.7 81

4,960 555 334

ancial ancial ent of at six e POP public urvey

ESS BLE

15

FINDINGS FRO

was colleseminar fAbout onThis selfparticipanother tran2012 for lin this stustill beneexpectatiocheck.11

TABLE 6.

Credit ScBanked Uses alteEmployedEmployed

Analy

This analworked inof financunbiasedadjusted Our estimthe two‐tOur estim

9 Through temploymenumber ofwas includ10 See: GretUnsubsidiz http://www11 We do nhave not at

OM THE ASSES

ected just asfrom the prone‐third repof‐reported emnts entering nsitional jobslow‐wage woudy. Populatfit from finanons about th

CHANGES IN

core

rnative finand full time d part time

ysis and

lysis uses a n POP) to thcial counseli impacts of or estimatedmates of overthirds of POmates of just

the Parks Depant outside of f days worked ded in the analytchen Kirby, Hzed Employmew.mathematicanot find statisticttended financi

SSING FINANC

s employmenogram), and ort being emmployment unemployms programs,10

orkers. Nevetions who lacncial counsehe degree to

N POP POPUL

nce

Results

POP employhe counselingng. This practually atted treatment‐orall average P participanthose clients

artment, we wePOP. The aveduring the stuysis, there was Heather Hill, Laent.ʺ Mathmatica‐mpr.com/PDcal differences ial counseling,

CIAL CAPABILI

nt through Ponly 18% re

mployed at 12rate is in

ment after the0 especially gertheless, it isck employmeling and accewhich these

LATION OVE

Baseline558 34% 74% 100% 0%

yeeʹs ʺassignmg group as a rovides a vaending a finaon ‐treated (Teffects of ass

nts who weres who took p

ere able to collrage hourly wudy period wano significant aDonnaPavetti ca Policy Resea

DFs/transitionalin the likelihoonor assignmen

ITY OUTCOME

POP was eneported havin2 months, sixline with Pe program. Itgiven the extrs critical to keent and face ess to mainste services can

ER THE 12-MO

6 M55761

mentʺ (definrandom evenalid instrumeancial counseTOT) impactsignment to e offered coupart in couns

lect additional wage was $11.1as 229 days. Wdifference in thand Jon Jacobsarch. lreport.pdf od of finding wnt to sites wher

ES (AFCO) ADU

nding (and fng found othx months aftPOP’s overalt is also a reremely pooreep the conteextreme levetream financn resolve lar

ONTH STUDY

Months561 59% 70% 6.9% 1.5%

ned here simnt that can beent to identeling sessiont. Other app(intent to treunseling but seling were b

hourly wage d10 with a max

When a control he estimated trson. (2002). ʺTr

work outside ofre/when counse

ULT PILOT

FINANCI FOR T

for many ather employmter exiting thll statistics easonably higr job market bext of unempels of financicial productsrger issues n

Y

12 Mont570 54% 64%

12.1% 23.1%

mply as whene then used ttify counselin. This is somproaches proveat, or ITT) wdeclined to

biased since t

data on 244 parximum of $28.for income earreatment effectsransitional Job

f POP betweeneling is offered

IAL COUNSELINTHE FINANCIAL

t their actuament at that he POP progof two‐thirdgh rate relatibetween 201ployment in ial instabilitys and serviceneed to be he

hs

n and whereto predict taking and estmetimes calleved less effewere swampetake up serthese clients

rticipants who .90, and the avrned outside os. s: Stepping Sto

n those who havd.

NG AND ACCELLY VULNERAB

al exit time.

gram.9 ds of ive to 0 and mind y may s, but eld in

e they ke‐up imate ed an ective. ed by vices. were

found verage of POP

ones to

ve and

ESS BLE

16

FINDINGS FRO

motivatedcrisis atte

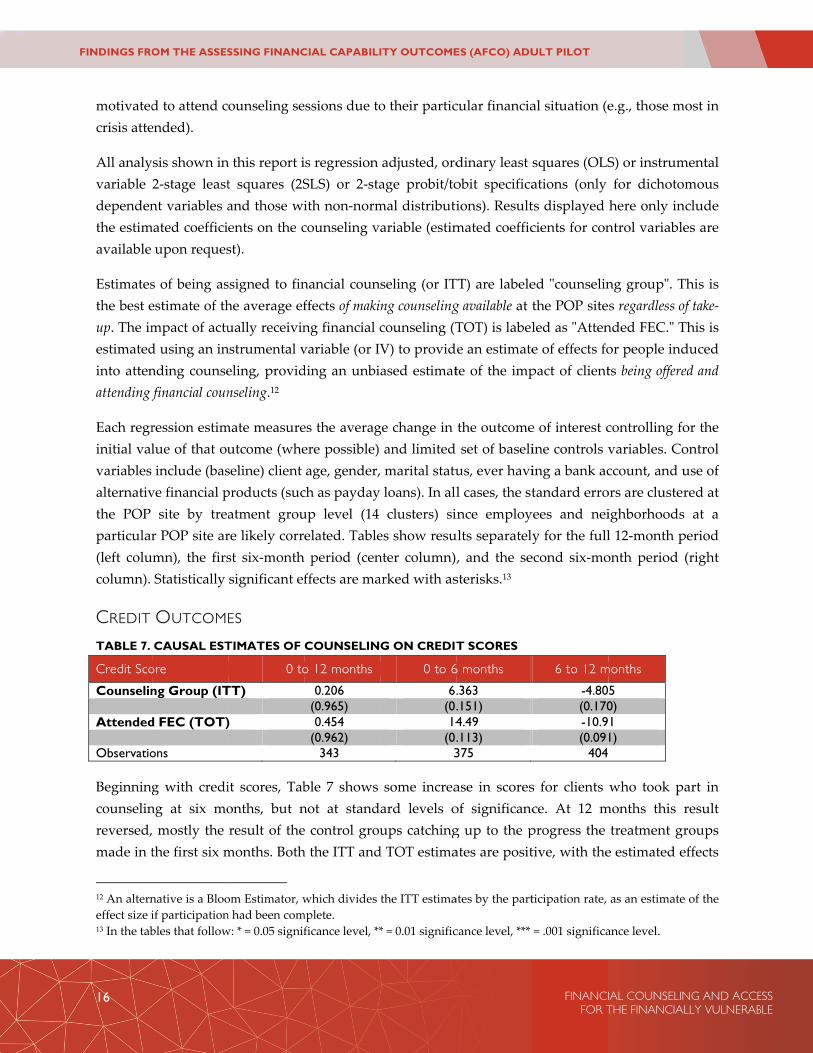

All analyvariable dependenthe estimavailable

Estimatesthe best eup. The imestimatedinto attenattending f

Each regrinitial valvariables alternativthe POP particular(left colucolumn).

CREDIT

TABLE 7.

Credit Sco

Counselin Attended Observatio Beginningcounselinreversed,made in t

12 An alterneffect size i13 In the tab

OM THE ASSES

d to attend cended).

sis shown in2‐stage leastnt variables a

mated coefficiupon reques

s of being asestimate of thmpact of actud using an innding counsefinancial coun

ression estimlue of that ouinclude (bas

ve financial psite by trea

r POP site armn), the firsStatistically

OUTCOM

CAUSAL EST

ore

ng Group (IT

d FEC (TOT)

ons

g with creding at six mo mostly the the first six m

native is a Blooif participationbles that follow

SSING FINANC

ounseling se

n this report it squares (2Sand those wients on the cst).

ssigned to finhe average efually receivinnstrumental veling, providnseling.12

mate measureutcome (wheseline) client products (sucatment groure likely corrst six‐monthsignificant ef

ES

TIMATES OF

0 to

TT)

)

it scores, Tabonths, but nresult of themonths. Both

om Estimator, wn had been comw: * = 0.05 signif

CIAL CAPABILI

essions due to

is regression SLS) or 2‐staith non‐normcounseling v

nancial counffects of making financial cvariable (or IVding an unbi

es the averagere possible) age, gender,ch as paydayup level (14 elated. Table

h period (cenffects are ma

COUNSELIN

o 12 months

0.206(0.965)0.454

(0.962)343

ble 7 shows not at stande control grouh the ITT and

which divides mplete. ficance level, **

ITY OUTCOME

o their partic

adjusted, ordage probit/tomal distributiariable (estim

seling (or ITng counselingcounseling (TV) to providased estimat

ge change in and limited marital statu loans). In allclusters) si

es show resunter column),arked with as

G ON CREDIT

0 to 6

6.(0.14

(0.3

some increaard levels oups catchingd TOT estima

the ITT estima

* = 0.01 signific

ES (AFCO) ADU

cular financia

dinary least sobit specificaions). Resultmated coeffic

TT) are labeleg available at tTOT) is labele an estimatete of the imp

the outcome set of baselius, ever havil cases, the stince employults separately, and the sesterisks.13

T SCORES

6 months

.363

.151)4.49.113)375

ase in scoresof significancg up to the pates are posit

ates by the part

cance level, ***

ULT PILOT

FINANCI FOR T

al situation (e

squares (OLSations (only ts displayed cients for con

ed ʺcounselinthe POP siteled as ʺAttene of effects fopact of client

e of interest cine controls ving a bank actandard erroyees and neiy for the fullecond six‐mo

6 to 12 m

-4.80(0.170-10.9(0.09

404

s for clients ce. At 12 mprogress the tive, with the

ticipation rate,

= .001 significa

IAL COUNSELINTHE FINANCIAL

e.g., those m

S) or instrumfor dichotohere only inntrol variable

ng groupʺ. Ts regardless ofnded FEC.ʺ Tor people indts being offere

controlling fovariables. Coccount, and uors are clusterighborhoodsl 12‐month ponth period

months

5 0) 1 1)

who took pamonths this rtreatment gre estimated e

as an estimate

ance level.

NG AND ACCELLY VULNERAB

most in

mental mous

nclude es are

This is f take‐This is duced ed and

or the ontrol use of red at at a period (right

art in result roups effects

e of the

ESS BLE

17

FINDINGS FRO

of attendPOP part343 studyof these e

TABLE 8.

Pct Past D

Counselin Attended Observatio

The estimreports (nproducesattendingcould be specificatstatisticalindividuais past duconfidenc

OM THE ASSES

ing counselinticipants tooky participantestimates. No

CAUSAL EST

Due

ng Group (IT

d FEC (TOT)

ons

mates in Tabln=879 for alls a 5% reducg counselinga result of ttions such aslly significanals stay curreue. Figure 3 ce intervals o

SSING FINANC

ng about thrk part in cous had credit one of these f

TIMATES OF

0 to

TT)

)

e 8 on percen three periodction in fallin. Because ththe distributis a Tobit modnt. The resultent with theifurther displof the results.

FIGURE 3: I

10%

15%

20%

25%

30%

35%

40%

CIAL CAPABILI

ree times theunseling, conscores reporfindings mee

COUNSELIN

o 12 months

-0.0518**

(0.004)-0.140**

(0.002)879

ntage of debds). These esng behind onhis outcome iion of this vadel. The resus overall shoir debt paymlays these es.

INTENT TO T

31%

31%

Baseline

Contr

Treat

ITY OUTCOME

e level of thensistent withrted in all thrts standard s

G ON THE PE

0 to 6

-0.(0.-0.(0.

8

t past due usstimates indin debt paymis constraineariable. Howults at six monow a consistements, at leasttimates as a

TREAT PERCE

31%

29%

6 Months

rol (405 memb

ment (474 me

ES (AFCO) ADU

e overall averh Bloom estimree periods, statistical ben

ERCENTAGE

6 months

.0183.340).0494.305)879

ses the largeicate that, onments over 1ed to 0% to wever, the renths are direent pattern oft measured bline graph, i

ENTAGE PAS

29%

24%

12 Months

bers)

mbers)

ULT PILOT

FINANCI FOR T

rage effect (rmator resultsreducing thenchmarks for

E OF DEBT TH

6 to 12 m

-0.031(0.04-0.087(0.030

995

r sample of cn average, of12 months, a100%, we w

esults are robectionally apf financial coby the percenincluding da

ST DUE

IAL COUNSELINTHE FINANCIAL

recall about 1s). However,e statistical pr significance

HAT IS PAST

months

8* 1) 78* 0)

clients with cffering counsand 14% for worry this finbust to alternpropriate, buounseling, hentage of debashed lines fo

NG AND ACCELLY VULNERAB

1/3 of , only power e.

DUE

credit seling those nding native ut not elping bt that or the

ESS BLE

18

FINDINGS FRO

Past due significanThis appthan halfbelow in people wwithout cLarge chendpoint 100%, or

TABLE 9. BY CREDI

Pct Past D Attended Observatio Attended Observatio

BANKIN

One objeunderstanshown inOne potehaving a

TABLE 10

Banked Counselin Attended ObservatioNote: marg

Table 10 savings aassociatedrelated tothe 6‐12 m

OM THE ASSES

debt is an int reductionsarent discrepf of this popuTable 9, the

who do have credit scores anges in perand positivvice versa).

CAUSAL ESTIT SCORE RE

Due

d FEC (TOT)

ons

d FEC (TOT)

ons

G OUTCO

ective of the nd how counn Table 6 aboential outcombank accoun

0. CAUSAL ES

ng Group (IT

d FEC (TOT)

ons ginal effects.

shows estimaccount) usid with a largo financial comonth period

SSING FINANC

important des in the percepancy stems ulation has sre are no sigcredit scores(without scorcentage pasve, but comp

TIMATES OF PORTING

0 to

)

)

MES

design of cnselors mighove, POP parme of counsent in follow‐u

STIMATES OF

0 to 12TT) -0.0

(0.) 0.0

(0.4

mated rates ing a Probitge increase iounseling. Cod (likely due

CIAL CAPABILI

eterminant oentage past dfrom the di

sufficient cregnificant redus. The reducores as of at st due are apletely past d

COUNSELIN

o 12 months

-0.0359(0.433)

343

-0.193**(0.006)

536

counseling anht aid clients rticipants shoeling wouldup surveys.

F COUNSELIN

2 months 00002.996)0004.997)495

of reportingt 2‐stage IVin being banounseling is ae to the persi

ITY OUTCOME

of credit scorue debt withifferent sampedit history ouctions in thctions in debleast one enlso dominatdue debt at t

NG ON THE P

0 to 6With Sco

-0.(0.

3Without Sc

-0.(0.

5

nd the offerin better maowed a dram be that cou

NG ON BANK

0 to 6 months-0.0370(0.166)-0.0948(0.214)

593

being bankV model. Alnked, there isassociated wstence of acc

ES (AFCO) ADU

re. Thereforehout similar mples availablon file to reche percentagebt past due andpoint necested by peoplthe other (e.

PERCENTAGE

6 monthsre Reported.0493.381)375core Reported.0426.411)504

r of a bank anaging bankmatic increaseunseling clie

KING STATUS

6 to 12 m0.035(0.190.097(0.218

362

ked (that is hlthough POPs no differen

with a positivcounts open

ULT PILOT

FINANCI FOR T

e, it may be movement inle for the twceive a credite of debt paare concentrassary to calcule who had g. went from

E OF DEBT T

6 to 12 m

-0.003(0.895

404 d

-0.126(0.016

591

account in tking services e in reportinnts are mor

S

months581)738)

having an aP participatintial increaseve increase inwhile emplo

IAL COUNSELINTHE FINANCIAL

surprising tn the credit scwo outcomes.t score. As shst due amonated in the pulate the chazero debt a

m 0% past d

HAT IS PAST

months

79 5)

6* 6)

this study wand product

ng a bank acce likely to r

active checkinion in genere in being ban bank accounoyed by POP

NG AND ACCELLY VULNERAB

to see cores. . Less hown ng the people ange). at one due to

T DUE

was to ts. As count. report

ng or ral is anked nts in P), but

ESS BLE

19

FINDINGS FRO

the estimthe averahere maysurveys.

Monthly POP partand afterusing thedelayed oparticipanwhich we

Account bdistributialso calcustatementʺcorrectʺ sound finsound of

14 Althoughevidence thare open.

OM THE ASSES

mates are not age rate of rey not be signi

statements pticipants, offer taking parteir bank accoopening accont for whome had accoun

balances in tions are highulated as tht. Any negatoutcome fornancial manaa financial d

h not shown, what counseling

SSING FINANC

significant steporting beinificant due to

FIGURE 4: AV

provided by er more detat in POP. Thounts. Not evounts or closm bank data nt data still ha

this analysis hly skewed whe average otive values ar participantagement, but decision.

we did test for significantly in

30%

35%

40%

45%

50%

55%

60%

65%

70%

75%

B

CIAL CAPABILI

tatistically. Fng banked ino the smaller

VERAGE RAT

Popular Comail in how thhis analysis pvery client hased them). Owas able toad open acco

are measurewith many nof the withinare recorded s might be. if a client pa

the effects of cncreased the ra

38%

38%

aseline

Contr

Treat

ITY OUTCOME

igure 4 showncreased starr number of r

E OF REPORT

mmunity Banhose people wprovides an ad a full yea

On average, w be matchedounts as of Ju

d in log dollnear zero andn‐month aveas zero. It shCarrying a lays down hig

counseling on aate of opening a

66%

58%

6 Months

rol (187 memb

tment (174 me

ES (AFCO) ADU

ws these resurkly for all Prespondents

TING BEING

nk, althoughwho have accindication o

ar of accountwe observe 7d, and only une 2013.14

lars (we use d a few veryerage balanchould be notlarger bank gh cost debt,

account openinaccounts or the

57

56%

12 Mon

bers)

embers)

ULT PILOT

FINANCI FOR T

ults graphicalPOP participawho comple

BANKED

h only availabcounts are uof how studyt statements 7.7 bank stat78 of the 33

the log of bay large valuece recorded ted that it is balance is olower balan

ng and terminae amount of tim

7%

%

nths

IAL COUNSELINTHE FINANCIAL

lly: the increaants. Effects eted the follo

ble for a subusing them dy participant(clients maytements per s4 participan

alance becauses). The balanin each mounclear wha

often attributnces may be ju

ation. We do nome the bank acc

NG AND ACCELLY VULNERAB

ase in again ow‐up

bset of uring ts are have study nts for

se the nce is onthly at the ted to ust as

ot find counts

ESS BLE

20

FINDINGS FRO

TABLE 11

Average BCounselin Attended Observatio

Table 11 significanbalances translatesto be a reanalyses,

The averastudy, anpaid at leabout $47fees, and

TABLE 12

Account FCounselin Attended Observatio

The resulincrease fcounterinfor bill pa

FINANC

Six surveItems in establishisavings, awho inten

OM THE ASSES

. CAUSAL ES

Balance ng Group (IT

d FEC (TOT)

ons

shows the efnt differencein the 6‐12s into about aelationship bhowever.

age person innd $91 in 6‐12east one bank7 over the lifTable 12 sho

2. CAUSAL ES

Fees ng Group (IT

d FEC (TOT)

ons

lts in Table 1fees incurredntuitive resulayments.

CIAL PLANN

ey questions this index iing a new soand (6) incrend to make f

SSING FINANC

STIMATES OF

Full StTT)

()

(

ffects of finanes, but there2 month pera $41 decreabetween an i

n the bank d2 month perik fee: typicalfetime of theows the effect

STIMATES OF

0 to 12 TT) 0.4

(0.2) 1.0

(0.233

12 are not stad for insufficlt is counselo

NING OUTC

related to tainclude (1) rource of credeasing amounorward‐look

CIAL CAPABILI

F COUNSELIN

tudy Period0.117

(0.642)0.316

(0.609)334

ncial counsele is directionriod (post Pse in averagendividual pa

ata has an acod (post POPlly insufficiee account. Cots of counseli

F COUNSELIN

months 0 to400 243) 079 246) 34

atistically sigcient funds aors could pr

COMES

aking steps toreviewing a dit, (4) usingnts put into pking changes

ITY OUTCOME

NG ON AVER

0 to 6 mon0.118

(0.678)0.318

(0.650)334

ling on log anal evidencePOP). Lookine balance foraying down

ccount balanP). About 28%nt funds or rounseling coing on avera

NG ON AVER

o 6 months 60.379

(0.269)1.023

(0.274)334

gnificant, buand returnedomote the u

o managing credit repor

g a savings ppaying off dein their finan

ES (AFCO) ADU

RAGE BALAN

nths 6 mo

average balane that counsng at the acr counseled cdebt and ba

nce of $107 du% of the POPreturned itemould potentiaage fees.

RAGE BANK F

6 to 12 month0.364

(0.126)0.908

(0.112)216

ut suggestive d items. One use of autom

personal finart, (2) creatiprogram, (5)ebt. These quncial behavio

ULT PILOT

FINANCI FOR T

CE

onths to End -0.447(0.063) -1.115(0.053)

216

nces. There aseling actuactual (non‐loclients. Thereank balances

uring the firsP participantm fees. On aally help clie

FEES

hs

that counsepotential exatic electron

ances ʺin theing a debt p) increasing uestions couor.

IAL COUNSELINTHE FINANCIAL

are no statistally reduces og) balancese does not aps based on fu

st 6 months ots in the bankaverage, fees ents to avoid

eling may actxplanation fonic funds tran

e last six monpayment planamounts pu

uld capture p

NG AND ACCELLY VULNERAB

tically bank s this ppear urther

of the k data were

d such

tually or this nsfers

nths.ʺ n, (3) t into people

ESS BLE

21

FINDINGS FRO

TABLE 13

Financial Counselin Attended Observatio

Table 13 Additioncredit repbaseline. employeetheir credmuch sm

The quessigning uonce, assuthat the ccompleteand this iplanning,clients are

SUMMA

Financial• A

esscd10

• Aemmsu

• Ath

• Ais

OM THE ASSES

3. CAUSAL ES

Plan Index ng Group (IT

d FEC (TOT)

ons

shows that cal analysis inport. Most suCredit repores in POP todit reports. C

maller, less sta

stions in thisup for a saviuming the pcredit report rd and the cliindex do not, or even chee reducing th

RY OF FIND

counseling iA decrease in stimated effecores and boriven by the00%). An increase mployment measurable efubset of studAn increase inhe six month A decrease ins significant.

SSING FINANC

STIMATES OF

0 to 12 TT) 0.0

(0.5) 0.0

(0.54

counseling isnto the compurvey responrts were como also be seeCreating a 5‐iatistically sign

s index ask aings programparticipant streview that iient exits POt reveal any ecking a crehe percentag

DINGS

is associated the percenta

ect is quite laorrow less the 10% of the

in credit scothrough POffect by the dy participann financial plpoint of the account bal

CIAL CAPABILI

F COUNSELIN

months 0 t0298 563) 0817 548) 94

associated wponents of thndents did nommonly usedeking credit item index enificant effec

about steps m or creatingicks with theis part of the OP. Further ainsights intodit report spe of debt pas

with: age of debt thrge and seeman the typicasample who

ores at the OP and a ret12 month fots, however.lanning behastudy. ances held a

ITY OUTCOME

NG ON FINAN

to 6 months0.0970*

(0.040)0.256**

(0.006)590

with positivehe index sugot report revd as part of cwhile emploexcluding revcts.

taken over tg a debt repem. The 6‐12counseling s

analysis of tho causal pathpecifically, asst due.

hat is past dums to be concal person in o experienced

six month mturn to unemollow‐up cred

aviors, especi

nd an increa

ES (AFCO) ADU

NCIAL PLAN

6 to 12 mo-0.0842(0.187)-0.234(0.124)

354

e changes forggest this is lviewing a repcounseling soyed and thviewing a cre

the past six payment plan2 month resusession but nhe relationshihways—that s contributin

ue for both scentrated in pthis populatd the maxim

mark, whichmployment fdit report. S

ially reviewi

ase in bank fe

ULT PILOT

FINANCI FOR T

NING onths2)

4)

r the zero to largely driveport in the pressions, and