ferrochrome market overview 2017 - meraferesources.co.za · outlook on global fecr supply source:...

TRANSCRIPT

Ferrochrome Market Overview 2017

Presented by:

Mark BeveridgePrincipal Consultant

CRU Nickel, Chrome, Stainless Steel Group

▪Which factors define the chrome market?

1. Chinese demand and the stainless steel cycle

- Chinese credit creation

- Inventory levels

- Trade

- Real demand

2. Chinese Production costs

3. South African Cr ore supply and price

▪Explaining recent events

▪Outlook global demand and supply

▪Conclusions

Key Themes

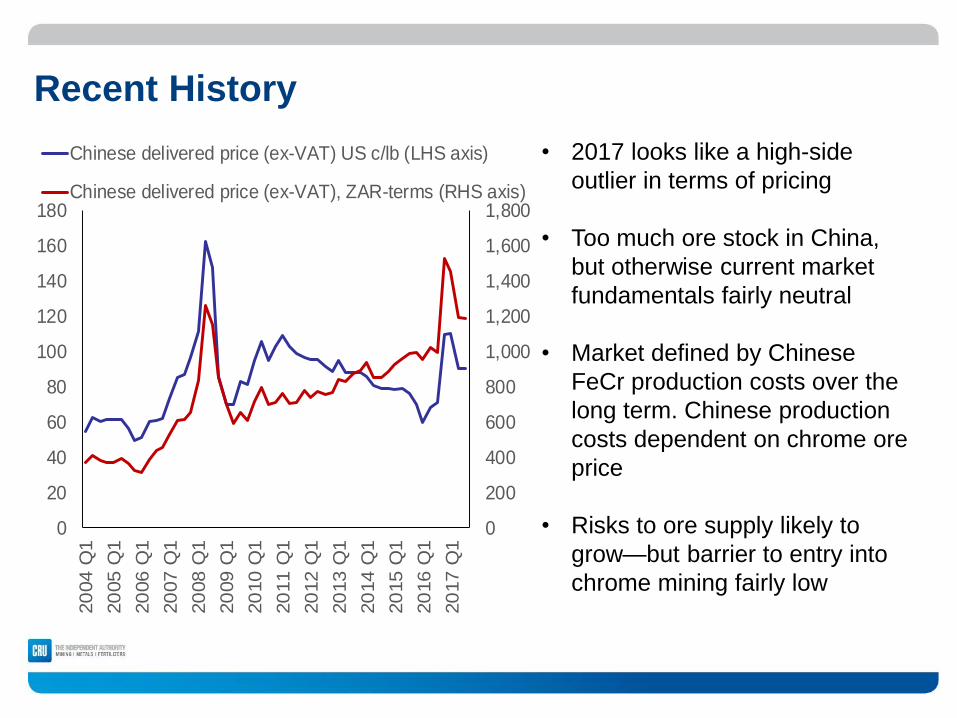

Recent History

• 2017 looks like a high-side

outlier in terms of pricing

• Too much ore stock in China,

but otherwise current market

fundamentals fairly neutral

• Market defined by Chinese

FeCr production costs over the

long term. Chinese production

costs dependent on chrome ore

price

• Risks to ore supply likely to

grow—but barrier to entry into

chrome mining fairly low

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

0

20

40

60

80

100

120

140

160

180

20

04

Q1

20

05

Q1

20

06

Q1

20

07

Q1

20

08

Q1

20

09

Q1

20

10

Q1

20

11

Q1

20

12

Q1

20

13

Q1

20

14

Q1

20

15

Q1

20

16

Q1

20

17

Q1

Chinese delivered price (ex-VAT) US c/lb (LHS axis)

Chinese delivered price (ex-VAT), ZAR-terms (RHS axis)

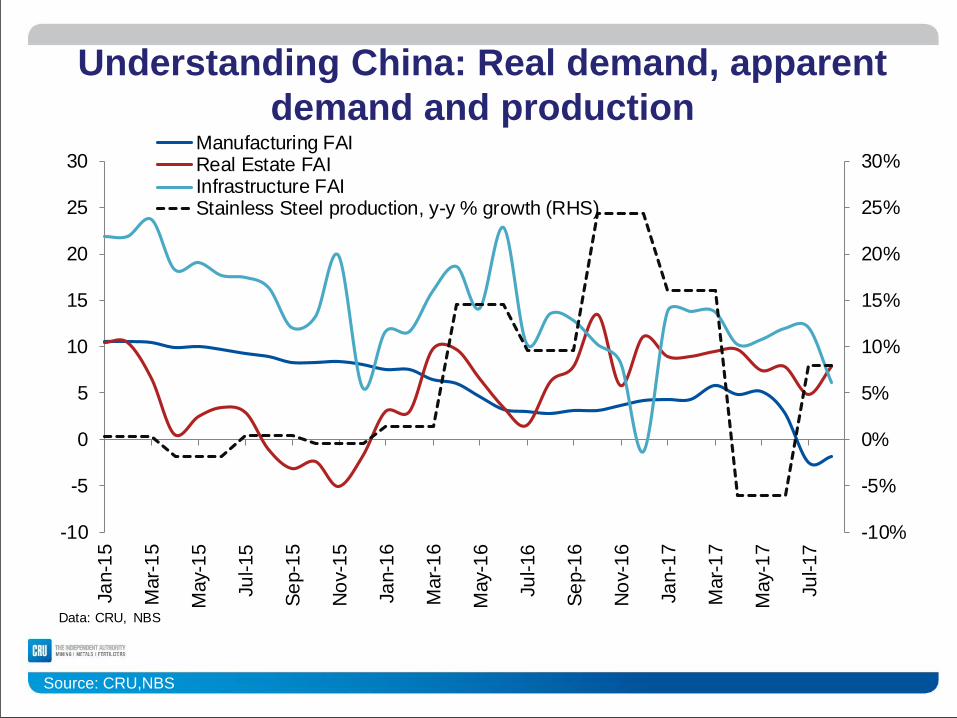

Understanding China: Real demand, apparent

demand and production

Source: CRU,NBS

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

-10

-5

0

5

10

15

20

25

30

Ja

n-1

5

Mar-

15

May-1

5

Ju

l-15

Se

p-1

5

No

v-1

5

Ja

n-1

6

Mar-

16

May-1

6

Ju

l-16

Se

p-1

6

No

v-1

6

Ja

n-1

7

Mar-

17

May-1

7

Ju

l-17

Manufacturing FAIReal Estate FAIInfrastructure FAIStainless Steel production, y-y % growth (RHS)

Data: CRU, NBS

Chinese apparent stainless steel demand and the

credit cycle

Source: CRU

-20

-10

0

10

20

30

40

10

12

14

16

18

20

22

Jan-1

2

Ap

r-1

2

Jul-12

Oct

-12

Jan-1

3

Ap

r-1

3

Jul-13

Oct

-13

Jan-1

4

Ap

r-1

4

Jul-14

Oct

-14

Jan-1

5

Ap

r-1

5

Jul-15

Oct

-15

Jan-1

6

Ap

r-1

6

Jul-16

Oct

-16

Jan-1

7

Ap

r-1

7

Jul-17

Stock of TSF + Local govt bonds (LHS)

Qtrly Crude SS Apparent Consumption (RHS)

Allowing for some lag, there is correlation between credit creation growth and

apparent consumption of stainless steel in China y/y % change

Understanding China: real vs. apparent demand

Source: CRU

0

2

4

6

8

10

12

14

16

20

10

Q1

20

10

Q3

20

11

Q1

20

11

Q3

20

12

Q1

20

12

Q3

20

13

Q1

20

13

Q3

20

14

Q1

20

14

Q3

20

15

Q1

20

15

Q3

20

16

Q1

20

16

Q3

20

17

Q1

20

17

Q3

China’s stainless steel inventory cycle—not yet carrying excessively high stock

Stainless steel stocks, crude steel basis, week's supply in hand

Long-term average stock levels

Understanding China: stainless steel production

and the stocking cycle

Source: CRU

Q-Q volatility in Chinese stainless steel production well reflected in the changing stock levels

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

0

2

4

6

8

10

12

14

16

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

2016Q2

2016Q3

2016Q4

2017Q1

2017Q2

2017Q3

China, stainless steel stocks, wks supply on hand (LHS axis)

China, quarterly crude SS apparent consumption, y-y % change (RHS)

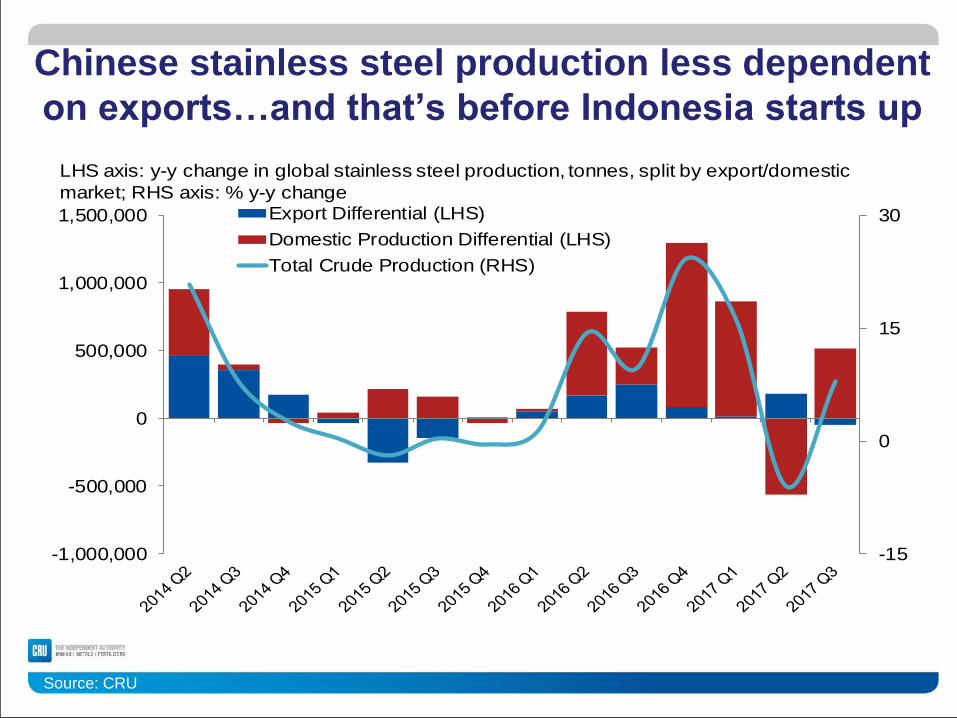

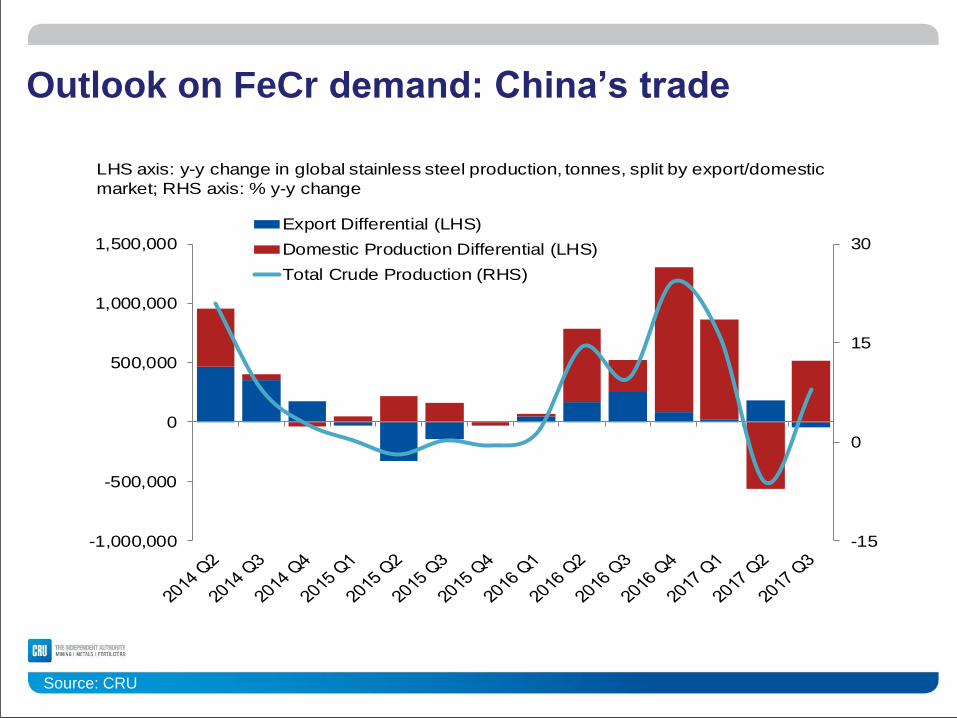

Chinese stainless steel production less dependent

on exports…and that’s before Indonesia starts up

Source: CRU

-15

0

15

30

-1,000,000

-500,000

0

500,000

1,000,000

1,500,000 Export Differential (LHS)

Domestic Production Differential (LHS)

Total Crude Production (RHS)

LHS axis: y-y change in global stainless steel production, tonnes, split by export/domestic

market; RHS axis: % y-y change

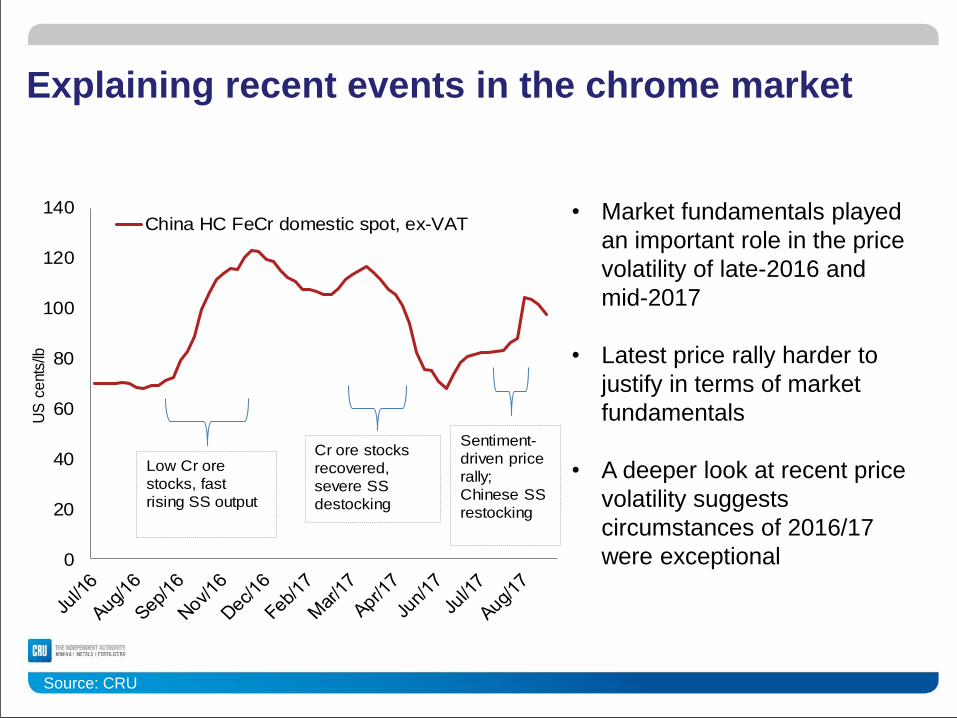

Explaining recent events in the chrome market

Source: CRU

• Market fundamentals played

an important role in the price

volatility of late-2016 and

mid-2017

• Latest price rally harder to

justify in terms of market

fundamentals

• A deeper look at recent price

volatility suggests

circumstances of 2016/17

were exceptional 0

20

40

60

80

100

120

140

US

ce

nts

/lb

China HC FeCr domestic spot, ex-VAT

Cr ore stocks

recovered,

severe SS

destocking

Sentiment-

driven price

rally;

Chinese SS

restocking

Low Cr ore

stocks, fast

rising SS output

Explaining recent events: Chrome ore stocks

Source: CRU

• Late 2016/early 2017 prices defined by critically-low ore stocks in China

and surge in demand (liquidity-driven)

• Pull back in prices in Q2 2017 coincided with collapse in demand, credit

creation slowdown

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

0

2

4

6

8

10

12

Jan-1

6

Mar-

16

May-

16

Jul-16

Se

p-1

6

No

v-1

6

Jan-1

7

Mar-

17

May-

17

Jul-17

Se

p-1

7

Cr Ore Stocks: Weeks consumptionin handChinese Monthly Cr Ore Imports

LHS: Weeks Consumption in Hand,

RHS: '000 tonnes Chrome Ore (Gross Weight)

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

2016Q1

2016Q2

2016Q3

2016Q4

2017Q1

2017Q2

2017Q3

China HC FeCr consumption y-y % change

Explaining recent events: Stainless steel stocks

Source: CRU

• China’s stainless steel

inventories also had a role to

play—they grew rapidly in Q4

2016/Q1 2017; then fell in Q2

2017

• CRU doesn’t believe that

stocks are currently close to

problematic levels—even with

large SS output in Q3,

stainless steel stock only

slightly higher than the long-

term average0

2

4

6

8

10

12

14

16

20

10

Q1

20

10

Q3

20

11

Q1

20

11

Q3

20

12

Q1

20

12

Q3

20

13

Q1

20

13

Q3

20

14

Q1

20

14

Q3

20

15

Q1

20

15

Q3

20

16

Q1

20

16

Q3

20

17

Q1

20

17

Q3

Stainless steel stocks, crude steel basis, week's supply

in hand

Long-term average

stock levels

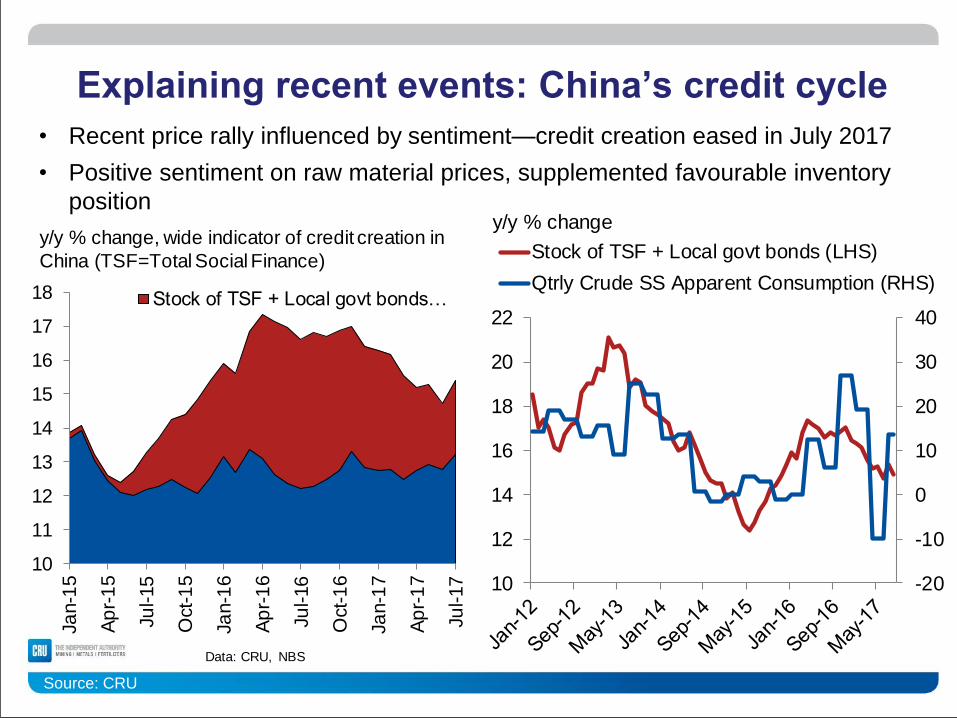

Explaining recent events: China’s credit cycle

Source: CRU

• Recent price rally influenced by sentiment—credit creation eased in July 2017

• Positive sentiment on raw material prices, supplemented favourable inventory

position

10

11

12

13

14

15

16

17

18

Ja

n-1

5

Ap

r-1

5

Ju

l-15

Oct-

15

Ja

n-1

6

Ap

r-1

6

Ju

l-16

Oct-

16

Ja

n-1

7

Ap

r-1

7

Ju

l-17

Stock of TSF + Local govt bonds…

Data: CRU, NBS

y/y % change, wide indicator of credit creation in

China (TSF=Total Social Finance)

-20

-10

0

10

20

30

40

10

12

14

16

18

20

22

Stock of TSF + Local govt bonds (LHS)

Qtrly Crude SS Apparent Consumption (RHS)

y/y % change

Explaining recent events: BM price moves

Source: CRU

EU charge chrome benchmark has stuck to established trend

40

60

80

100

120

140

160

180

Ja

n/1

6

Fe

b/1

6

Ma

r/1

6

Ma

r/1

6

Ap

r/1

6

Ma

y/1

6

Ju

n/1

6

Ju

l/1

6

Au

g/1

6

Se

p/1

6

Oct/

16

No

v/1

6

De

c/1

6

Ja

n/1

7

Fe

b/1

7

Ma

r/1

7

Ma

r/1

7

Ap

r/1

7

Ma

y/1

7

Ju

n/1

7

Ju

l/1

7

Au

g/1

7

Se

p/1

7

Oct/

17

EU BM (gross)

China HC FeCr domestic spot, ex-VAT

Outlook on FeCr demand: China

Source: CRU

• Credit tightening, FAI slowdown contribute to slowing stainless steel demand growth

• Output growth to move in range between 3-5% y-y, 2018-21

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

20

16

Q1

20

16

Q2

20

16

Q3

20

16

Q4

20

17

Q1

20

17

Q2

20

17

Q3

20

17

Q4

20

18

Q1

20

18

Q2

20

18

Q3

20

18

Q4

y-y

% c

hang

e

Chinese IP

0

2

4

6

8

10

12

14

16

18

Y-y

% c

hang

e

Chinese IP

Outlook on FeCr demand: China’s trade

Source: CRU

-15

0

15

30

-1,000,000

-500,000

0

500,000

1,000,000

1,500,000

Export Differential (LHS)

Domestic Production Differential (LHS)

Total Crude Production (RHS)

LHS axis: y-y change in global stainless steel production, tonnes, split by export/domestic

market; RHS axis: % y-y change

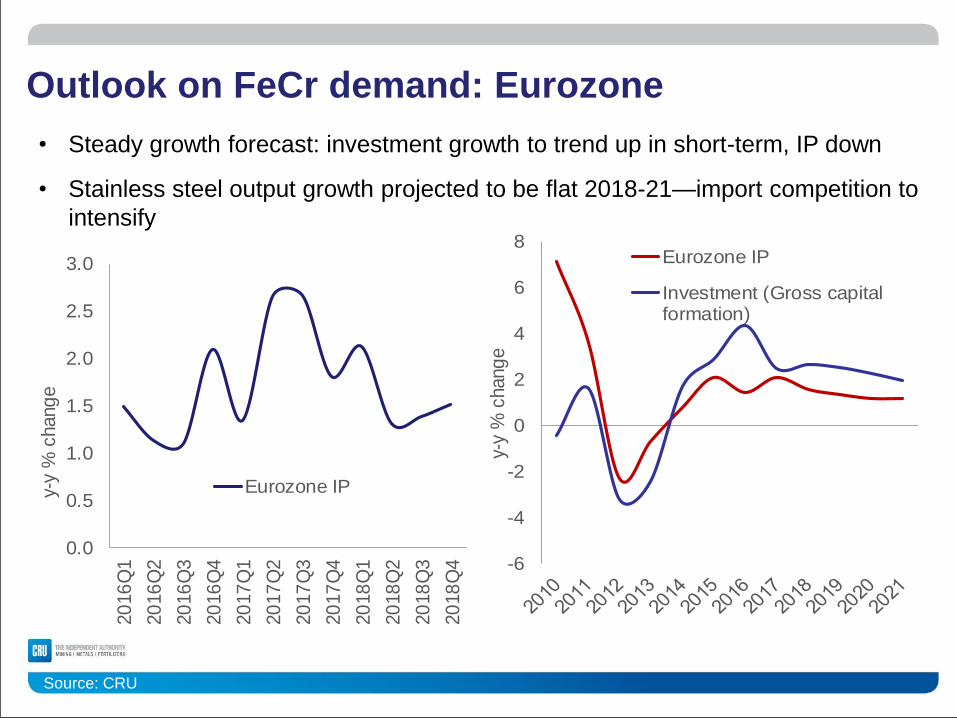

Outlook on FeCr demand: Eurozone

Source: CRU

• Steady growth forecast: investment growth to trend up in short-term, IP down

• Stainless steel output growth projected to be flat 2018-21—import competition to

intensify

0.0

0.5

1.0

1.5

2.0

2.5

3.0

20

16

Q1

20

16

Q2

20

16

Q3

20

16

Q4

20

17

Q1

20

17

Q2

20

17

Q3

20

17

Q4

20

18

Q1

20

18

Q2

20

18

Q3

20

18

Q4

y-y

% c

hang

e

Eurozone IP

-6

-4

-2

0

2

4

6

8

y-y

% c

hang

e

Eurozone IP

Investment (Gross capitalformation)

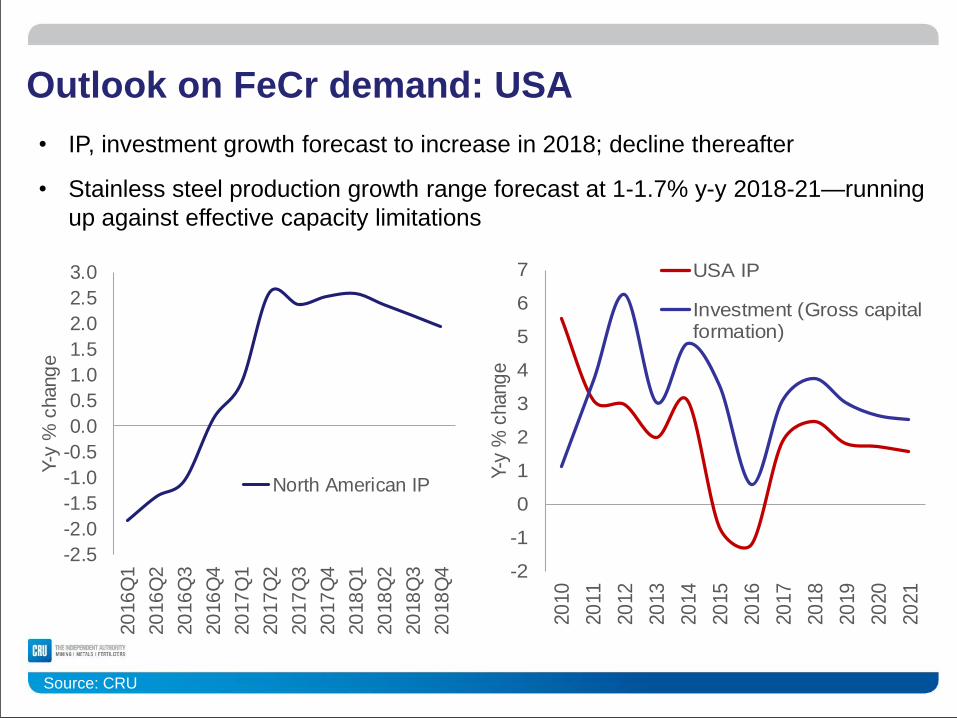

Outlook on FeCr demand: USA

Source: CRU

• IP, investment growth forecast to increase in 2018; decline thereafter

• Stainless steel production growth range forecast at 1-1.7% y-y 2018-21—running

up against effective capacity limitations

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

20

16

Q1

20

16

Q2

20

16

Q3

20

16

Q4

20

17

Q1

20

17

Q2

20

17

Q3

20

17

Q4

20

18

Q1

20

18

Q2

20

18

Q3

20

18

Q4

Y-y

% c

hang

e

North American IP

-2

-1

0

1

2

3

4

5

6

7

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

Y-y

% c

hang

e

USA IP

Investment (Gross capitalformation)

Outlook on Global HC FeCr demand

Source: CRU

• The combination of Chinese, Indonesian and Indian demand will define HC

FeCr market in coming years

• HC FeCr demand growth forecast to be relatively flat over forecast period

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2010 2012 2014 2016 2018 2020

China India

RoW Indonesia

HC FeCr consumption, '000 tonnes gross weight

-10%

-5%

0%

5%

10%

15%

20%

25%

30%China

India

RoW (ex-Indonesia)

RoW including Indonesia

HC FeCr consumption, y-y % change

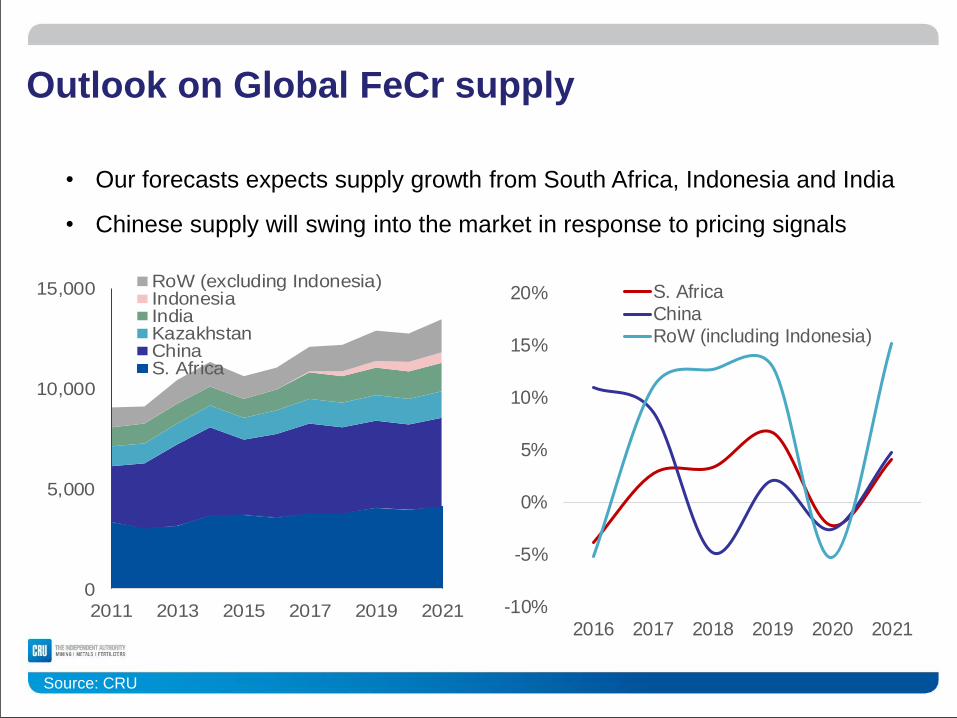

Outlook on Global FeCr supply

Source: CRU

• Our forecasts expects supply growth from South Africa, Indonesia and India

• Chinese supply will swing into the market in response to pricing signals

0

5,000

10,000

15,000

2011 2013 2015 2017 2019 2021

RoW (excluding Indonesia)IndonesiaIndiaKazakhstanChinaS. Africa

-10%

-5%

0%

5%

10%

15%

20%

2016 2017 2018 2019 2020 2021

S. AfricaChinaRoW (including Indonesia)

Global HC FeCr supply/demand balance

Source: CRU

• Global HC FeCr will tend

towards oversupply over

the forecast period

• However, deficits will be

required in order to

prevent excessive stock

accumulation

• Chinese supply will swing

in and out of the market

depending on pricing

signals-500

-400

-300

-200

-100

0

100

200

300

400

500

600

2010 2012 2014 2016 2018 2020

Market balance

Production costs

Source: CRU

• Rising power costs in South Africa (ZAR-terms) will push up

production costs; effect will be offset by depreciating currency

• But South African marginal production costs will not be as important

for global prices as Chinese production costs

12.00

12.50

13.00

13.50

14.00

14.50

15.00

15.50

16.00

-8%-6%-4%-2%0%2%4%6%8%

10%12%14%

2016 2017 2018 2019 2020 2021

ZA power price increase in US$ terms (15%LC y-y increase post-2017)

ZAR nominal ex-rate vs US$ (RHS)

0

10

20

30

40

50

60

70

80

90

100

0 1,000 2,000 3,000 4,000

Thousands

ZA FeCr producers, delivered costs, US c/lb

(ex-VAT), 2021 projection

Data: CRU

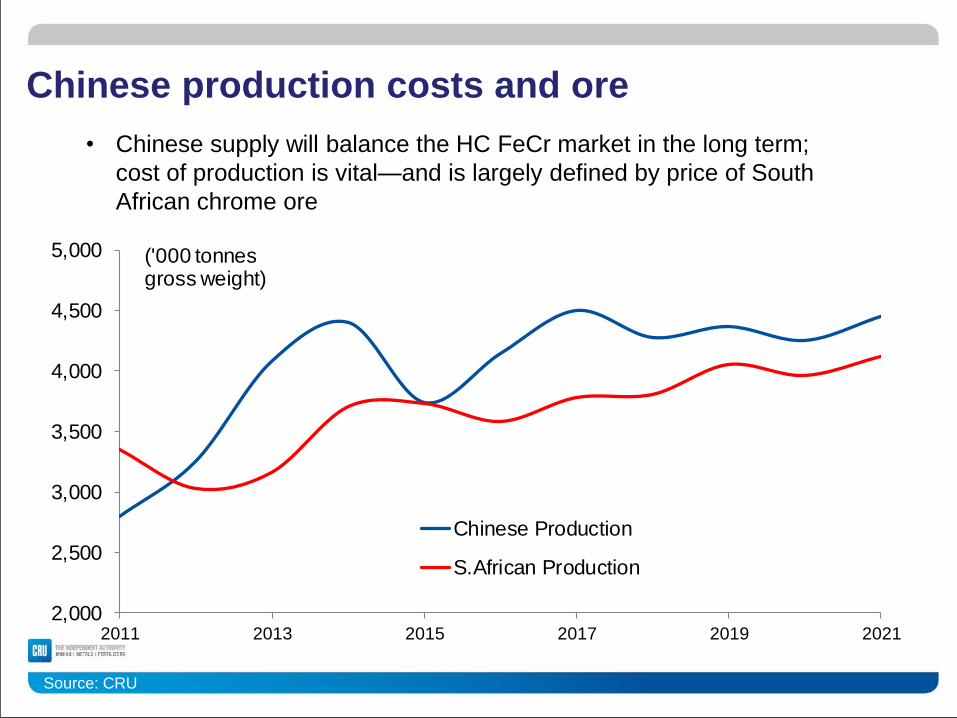

Chinese production costs and ore

Source: CRU

• Chinese supply will balance the HC FeCr market in the long term;

cost of production is vital—and is largely defined by price of South

African chrome ore

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2011 2013 2015 2017 2019 2021

('000 tonnes gross weight)

Chinese Production

S.African Production

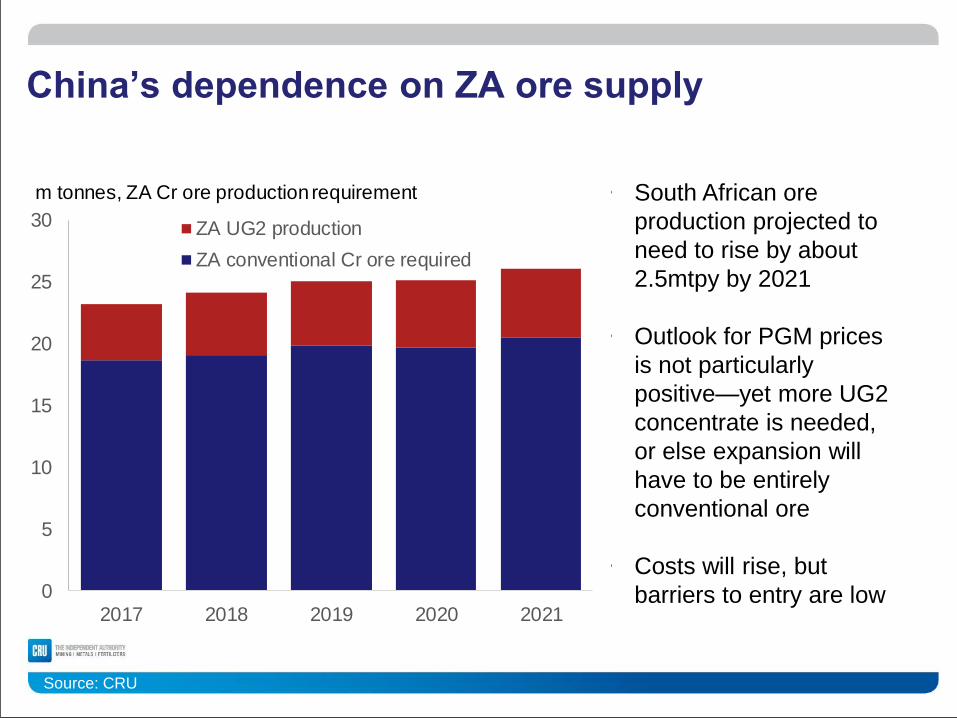

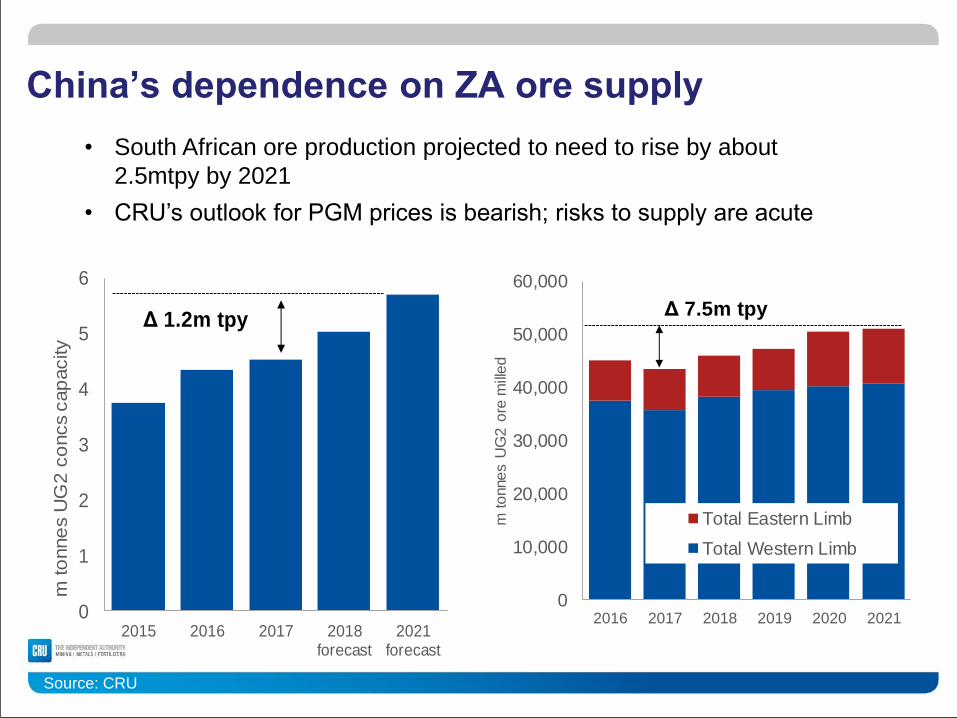

China’s dependence on ZA ore supply

Source: CRU

• South African ore

production projected to

need to rise by about

2.5mtpy by 2021

• Outlook for PGM prices

is not particularly

positive—yet more UG2

concentrate is needed,

or else expansion will

have to be entirely

conventional ore

• Costs will rise, but

barriers to entry are low 0

5

10

15

20

25

30

2017 2018 2019 2020 2021

ZA UG2 production

ZA conventional Cr ore required

m tonnes, ZA Cr ore production requirement

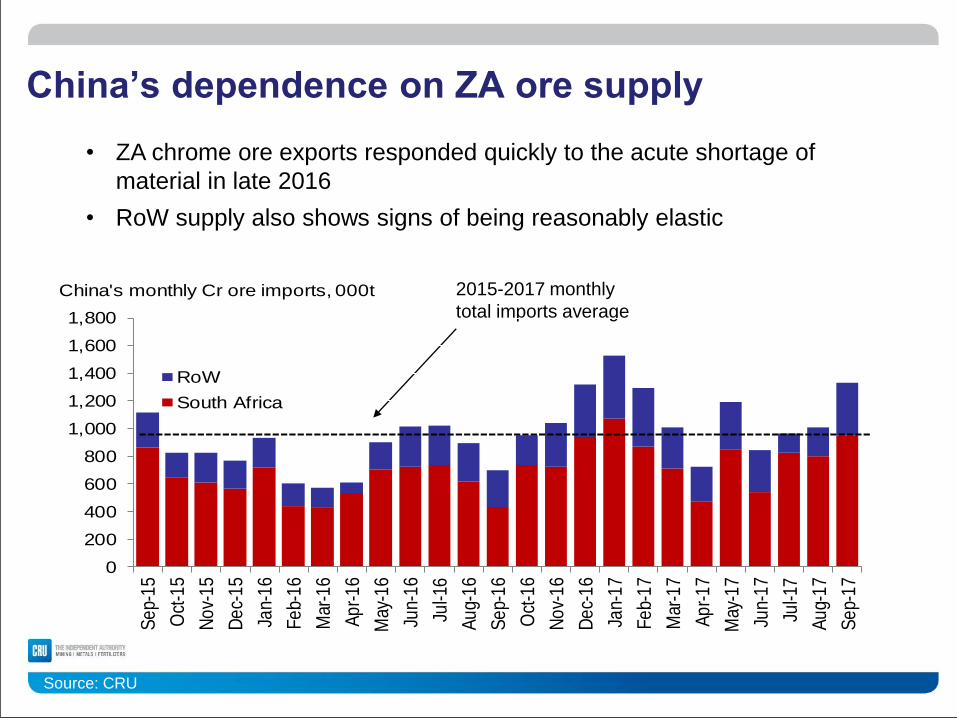

China’s dependence on ZA ore supply

Source: CRU

• ZA chrome ore exports responded quickly to the acute shortage of

material in late 2016

• RoW supply also shows signs of being reasonably elastic

2015-2017 monthly

total imports average

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Se

p-1

5

Oct

-15

No

v-1

5

De

c-1

5

Jan-

16

Fe

b-1

6

Mar

-16

Ap

r-1

6

May

-16

Jun-

16

Jul-1

6

Au

g-1

6

Se

p-1

6

Oct

-16

No

v-1

6

De

c-1

6

Jan-

17

Fe

b-1

7

Mar

-17

Ap

r-1

7

May

-17

Jun-

17

Jul-1

7

Au

g-1

7

Se

p-1

7

RoW

South Africa

China's monthly Cr ore imports, 000t

China’s dependence on ZA ore supply

Source: CRU

• South African ore production projected to need to rise by about

2.5mtpy by 2021

• CRU’s outlook for PGM prices is bearish; risks to supply are acute

0

1

2

3

4

5

6

2015 2016 2017 2018forecast

2021forecast

m to

nne

s U

G2

co

ncs c

ap

acity

Δ 1.2m tpy

0

10,000

20,000

30,000

40,000

50,000

60,000

2016 2017 2018 2019 2020 2021

m t

onne

s U

G2

ore

mill

ed

Total Eastern Limb

Total Western Limb

Δ 7.5m tpy

Conclusions:

26

• Short-term outlook dominated by chrome ore stocks in China

• Chinese stainless steel stock levels not overly worrying at the

moment—but there is the twin threat posed by bullish nickel market and

Indonesian imports

• Long-term trend towards lower global stainless steel production growth,

but it retains late-cycle commodity characteristics

• Chinese stainless steel cycle will determine when domestic Chinese HC

FeCr production is required to swing into the market.

• HC FeCr production cost in China will be key—and that will be

determined by ore availability and price

• South African chrome ore is the key variable in the Chinese production

cost calculation