expanding microfinance in brazil: credit utilisation and performance of small firms

TRANSCRIPT

This article was downloaded by: [Washington University in St Louis]On: 04 October 2014, At: 13:24Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954 Registeredoffice: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK

The Journal of Development StudiesPublication details, including instructions for authors andsubscription information:http://www.tandfonline.com/loi/fjds20

Expanding Microfinance in Brazil:Credit Utilisation and Performance ofSmall FirmsEmmanuel Skoufias a , Phillippe Leite a & Renata Narita aa Poverty Reduction and Equity Unit, The World Bank ,Washington , DC , USAPublished online: 18 Jun 2013.

To cite this article: Emmanuel Skoufias , Phillippe Leite & Renata Narita (2013) ExpandingMicrofinance in Brazil: Credit Utilisation and Performance of Small Firms, The Journal ofDevelopment Studies, 49:9, 1256-1269, DOI: 10.1080/00220388.2013.790961

To link to this article: http://dx.doi.org/10.1080/00220388.2013.790961

PLEASE SCROLL DOWN FOR ARTICLE

Taylor & Francis makes every effort to ensure the accuracy of all the information (the“Content”) contained in the publications on our platform. However, Taylor & Francis,our agents, and our licensors make no representations or warranties whatsoever as tothe accuracy, completeness, or suitability for any purpose of the Content. Any opinionsand views expressed in this publication are the opinions and views of the authors,and are not the views of or endorsed by Taylor & Francis. The accuracy of the Contentshould not be relied upon and should be independently verified with primary sourcesof information. Taylor and Francis shall not be liable for any losses, actions, claims,proceedings, demands, costs, expenses, damages, and other liabilities whatsoever orhowsoever caused arising directly or indirectly in connection with, in relation to or arisingout of the use of the Content.

This article may be used for research, teaching, and private study purposes. Anysubstantial or systematic reproduction, redistribution, reselling, loan, sub-licensing,systematic supply, or distribution in any form to anyone is expressly forbidden. Terms &Conditions of access and use can be found at http://www.tandfonline.com/page/terms-and-conditions

Expanding Microfinance in Brazil: CreditUtilisation and Performance of Small Firms

EMMANUEL SKOUFIAS, PHILLIPPE LEITE & RENATA NARITAPoverty Reduction and Equity Unit, The World Bank, Washington DC, USA

Final version received February 2013

ABSTRACT We take advantage of the natural experiment generated by the exogenous change in governmentpolicy towards microcredit to evaluate the impact of the increased supply of microcredit on the utilisation of creditby micro-entrepreneurs. Based on micro-entrepreneurs’ survey and administrative data from a microcreditprogramme in Brazil, we show that: the increased supply of microcredit raised formal credit utilisation andthis does not crowd out the use of informal credit sources; formal credit taking improves business performance;and returns are larger for women- than for men-owned firms, but males employ significantly more workers aftertaking formal credit than females.

JEL Classification: O16, G21, L25

Introduction

Although Brazil is now one of the world’s 10 largest economies, high levels of poverty and inequalitycontinue to pose major challenges for the country. The spatially uneven development of the Brazilianeconomy among the five major regions of the county, with the north and north-east regions laggingbehind the south and south-east regions, accompanied by the persistently high level of inequality haveraised many economic and social concerns. Primary among these is the belief that high levels ofinequality may compromise economic efficiency and growth. Credit and insurance market failures, forexample, may prevent poorer households from investing in and contributing to the economy at anoptimal level, thereby undermining efficiency and growth.

As a consequence, many of the efforts of the Brazilian government to date have focused onfostering the availability of financial services and expanding access to microfinance. Directly orindirectly, micro and small enterprises in Brazil are estimated to provide the primary source of incomefor almost 60 million people and generate nearly 20 per cent of GDP (Kumar, 2005). Lack of access tofinance for these micro-entrepreneurs can be a major constraint to their ability to effectively performtheir activities, or to increase their scale of operations. This suggests that microfinance has thepotential to induce significant favorable impacts in the country.

A leading example of such efforts is the Banco do Nordeste do Brasil (BNB) – a state-owneddevelopment bank created in 1952 to promote the development of the north-east region of Brazil –aimed at expanding access to credit in this relatively poor region of Brazil.1 The CrediAmigoprogramme is a flagship programme of BNB that initiated its operations in April 1998 and offers

Correspondence Address: Emmanuel Skoufias, TheWorld Bank (Mail Stop: MC4-415), 1818 H Street NW, Washington, DC,20433, USA. Email: [email protected] Online Appendix is available for this article which can be accessed via the online version of this journal available at http://dx.doi.org/10.1080/00220388.2013.7907961

The Journal of Development Studies, 2013Vol. 49, No. 9, 1256–1269, http://dx.doi.org/10.1080/00220388.2013.790961

© 2013 The World Bank

Dow

nloa

ded

by [

Was

hing

ton

Uni

vers

ity in

St L

ouis

] at

13:

24 0

4 O

ctob

er 2

014

loans to established micro-entrepreneurs for the financing of their working capital and fixed assetneeds.

In this study, we take advantage of the natural experiment generated by the exogenous change ingovernment policy towards microcredit to evaluate the impact of the increased supply of microcrediton the utilisation of credit by micro-entrepreneurs in the north-east region of Brazil. The survey dataavailable do not identify BNB or the CrediAmigo programme explicitly as a source of credit.However, in consideration of the fact that CrediAmigo was by far the largest microcredit programmeoperating in the north-east region of Brazil between 1998 and 2003, our analysis presumes that thecredit from public or private banks reported by micro-entrepreneurs in the national survey, at least inthe north-east region of Brazil, originates from the CrediAmigo programme.

The first question we address is whether the increased supply of credit in the north-east regionresulted in higher utilisation of formal (or bank) credit in the region. Based on administrative data fromthe CrediAmigo programme, we identify all the municipalities in the north-east region of Brazil wherethe programme operated and combine this information with the 1997 and 2003 detailed micro-entrepreneur surveys on the informal urban economy (ECINF), collected by the Brazilian Instituteof Geography and Statistics (IBGE) for firms with five or fewer employees. We employ the difference-in-differences estimator to estimate the ‘intent to treat effect’ of the increased availability of creditbetween 1997 and 2003 on the utilisation of credit by micro-entrepreneurs in the municipalities wherethe CrediAmigo programme operated.

The second question of interest explored is whether the utilisation of formal credit ‘crowds out’credit from other informal sources, such as credit from friends and relatives or product suppliers. Theinterest rate on loans offered by CrediAmigo is substantially lower than that charged by informalmoneylenders and trade credit providers. Thus, it is quite possible that the availability of relativelycheaper credit through the formal banks may simply replace the credit obtained through other sources,with little or no increase in the overall access to credit by micro-entrepreneurs who never had creditbefore (for example, Jain, 1999). This implies that it is also important to investigate whether theutilisation of credit increased, irrespective of whether the source is formal or informal.

By 2003, CrediAmigo had been operating in the north-east region for more than four years, which isa sufficiently long period of time in which to expect changes in the behaviour and performance ofcredit-taking micro-entrepreneurs. For this reason, we also examine whether the use of credit fromformal banks is associated with better performance, such as a higher profitability and size in terms ofnumber of employees. For this purpose, we use data from the 2003 ECINF survey and compare theperformance of firms utilising credit from public or private banks with the performance of acomparison group of firms using credit from informal sources or no credit at all. In this analysis weemploy the propensity score matching (PSM) method to match one or more entrepreneurs to a micro-entrepreneur who used credit from a private or public bank and estimate the ‘average treatment on thetreated’ effect of credit on firm performance.

Our article relates to a broad literature on microfinance and business development in developingcountries; see, for example, Paulson & Townsend (2004), de Mel, McKenzie & Woodruff (2008a),Banerjee, Duflo, Glennerster & Kinnan (2010), Karlan & Zinman (2010), and Dupas & Robinson(2011). For Brazil, there is little evidence on this topic. The closest research to ours is Neri (2008),who uses ECINF data for 1997 and 2003 to compare average credit utilisation for the north-east,where most CrediAmigo loans were applied in relation to the rest of the country. He finds that accessto credit increased by 1.6 per cent. In terms of evidence for the impact of credit on firm performance,Neri uses data from beneficiaries of CrediAmigo and matches it with a control group constructed fromthe longitudinal employment survey of Brazil (PME). Using a one-year window from 2005–2006, hefinds that the average impact of CrediAmigo on profits in relation to similar households sampled inPME is 7.7 per cent, and statistically significant at the 5 per cent level of significance. However, onemajor shortcoming of this approach is that the profit measure across treatment and control groups isdifferent, thus raising concerns about the reliability of the estimated effects of credit on performance.2

Expanding Microfinance in Brazil 1257

Dow

nloa

ded

by [

Was

hing

ton

Uni

vers

ity in

St L

ouis

] at

13:

24 0

4 O

ctob

er 2

014

The article is organised as follows: the following section describes the data; the section followingthat contains the description of the empirical methods employed to address the three questions posedabove, and a discussion of the findings; and the final section concludes.

Data

The Brazilian Survey of Small Firms

Our analysis is based on data from the 1997 and 2003 Economia Informal Urbana (ECINF)3 survey,which gathers socio-economic information from micro-entrepreneurs throughout Brazil. In particular,the ECINF is a repeated cross-section survey that collects data on owners of informal enterprises,identified as self-employed or employers with less than five employees, in urban areas of Brazil. Thesurvey does not include: non-agricultural units in the rural areas; homeless populations in urban areas;people connected to illegal activities; or domestic workers. The dataset is rich in information on firmand entrepreneur characteristics, but also on the entrepreneur’s personal and household characteristics.

The sampling in each year (1997 and 2003) of the ECINF survey is carried out following a two-stage methodology aimed at determining the role and dimension of the informal activities in theBrazilian economy. First, IBGE carries out a listing of all households in different enumeration areas,randomly selected4 from a sample frame, setting each one of 27 Brazilian states as a stratum.5 This sortof census in selected enumeration areas intends to identify target micro-economic units. Then, on thebasis of the listing of micro-economic units, IBGE selects the final sample of units, applying a verydetailed questionnaire. The sample was designed to cover all different types of activities in sectorssuch as: manufacturing, construction, trade, lodging and food services, transportation, renderingservices, technical and auxiliary services, and others services.

The first listing of households in randomly selected enumeration areas contained more than onemillion households, of which 30 per cent had at least one person working as account or micro-entrepreneur, the micro-economic unit. Hence, 49,664 micro-economic units were selected over 27Brazilian states (urban areas only).

Table A1 in the Online Appendix shows by year a summary of the micro-enterprise data used in thearticle. In 2003, the complete dataset has 48,813 respondents, representing 10,526,074 entrepreneursin Brazil. When restricting the attention to the north-east, we have 19,200 respondents representing2,763,987 entrepreneurs.

Whenwe look at whether formal credit has impacts on the performance of small businesses, the ‘treatment’is identified by whether the entrepreneur has been using credit or a loan from a bank (public or private) in theprevious threemonths for his/her activity. Only 6.2 per cent of all entrepreneurs in the north-east did use sometype of credit, with 3.6 per cent using formal credit sources (from a bank) and 2.6 per cent from informalsources (from friends or family, other enterprises, or a supplier). Unfortunately we are unable to determinewhether an entrepreneur has been using both types of sources, since the manner in which the questions areposed allows only the main source of credit to be identified.

The use of credit is slightly more common and statistically different for female entrepreneurs (6.97% ofthem declare to have used credit in the previous three months) than among male entrepreneurs (5.69%). Thisis mainly due to the wider difference in utilisation of informal credit (3.04% of women entrepreneurs usedinformal credit, as opposed to 2.30% of men, which are statistically different at 5%).

Considering business performance, the average profit of small firms in Brazil is 821 Reais (USD355), while in the north-east this is smaller at 596 Reais (USD 258). The average size of small firms is1.48 and 1.42 workers, respectively, in the entire country, and in the north-east region. Although creditis more commonly used among female entrepreneurs, businesses run by females seem to underper-form, at least when we look at profits. On average, men earn 947 Reais while women earn 592 Reais.In the north-east, the gap is even larger, with men earning 706 Reais and women 416 Reais, bothdifferences being significant at 1 per cent. Men also run slightly larger businesses, with 1.50 (1.46)workers on average and women with 1.43 (1.37), respectively, in Brazil and the north-east region.These differences are also found significant at 1 per cent level.

1258 E. Skoufias et al.

Dow

nloa

ded

by [

Was

hing

ton

Uni

vers

ity in

St L

ouis

] at

13:

24 0

4 O

ctob

er 2

014

In terms of the main characteristics of the entrepreneurs, 65 per cent are males, they are on average41 years old and started working at the age of 15; 57 per cent have less than secondary education, 31per cent have secondary, and only 12 per cent beyond secondary. About 85 per cent are self employed,and among the remaining employers, 10 per cent have partners, 29 per cent have their domicile as theirmain workplace, 33 per cent did not need capital to start up, and 50 per cent did not register thebusiness. From 1997 to 2003, significantly, formal credit utilisation increased by 2.4 percentage pointsand profits decreased 1.6 per cent in the north-east region, following a lower economy growth in 2003.

CrediAmigo programme

CrediAmigo is a microcredit programme that is operated by the state-owned Banco do Nordeste doBrasil (BNB). Its operations began in April 1998, aiming to improve the development of the north-eastthrough expanding access to microloans in this relatively poor region of Brazil. The programmeoperates in municipalities from nine states in the poor north-east region and in some poorer munici-palities in the state of Minas Gerais and Espirito Santo in the south-east region. Priority in theimplementation of CrediAmigo was given to those cities where microfinance was non-existent orvery small. Unlike other microfinance programmes focusing on informal micro-enterprises in ruralareas, in Brazil most of the informal micro-enterprises are located in urban areas. The CrediAmigoprogramme remained unrivalled in scale in Brazil at least until 2003 and constitutes a significant partof the microfinance expansion of the past two decades.

The design of CrediAmigo incorporates key features of successful microfinance interventionsaround the world.6 Loans are collateral-free, but are extended using the solidarity group techniqueto small groups of three to five borrowers who cross-guarantee each other’s loan. The average size of aCrediAmigo loan was 590 Reais (or USD 256 at the prevailing exchange rate). Loans usually last forthree months. First loans are limited to 300–1,000 Reais (about USD 130–433), but repeat loans canbe up to 4,000 Reais (USD 1,733). The programme initiated with a 5 per cent flat monthly rate, but theinterest rate has since decreased to 2 per cent.7 As mentioned earlier, interest rates are substantiallylower than those charged by informal moneylenders and trade credit providers. After a borrower hassuccessfully paid back two loans under the solidarity programme, the borrower becomes eligible forindividual credit, with a loan maturity of up to six months. Fixed investment credit is also offered, witha maturity of up to 18 months.8

CrediAmigo is the largest microfinance institution in Brazil and is among the top microfinance institutionsin Latin America in terms of geographical penetration, numbers of clients and depth of outreach. In 2002,CrediAmigo served nearly 60 per cent of microfinance clients and held about 45 per cent of their outstandingloans (Kumar, 2005). According to the administrative data of the programme, as of the end of 2002 roughly50 per cent of clients were women, 40 per cent were 35 years old or younger, 57 per cent had reached theprimary school level, and 41 per cent were poor, earning between USD 1-2 per day.

Empirical Analysis

This section is composed of two parts. First, we show the impacts of the availability of the CrediAmigoprogramme on total credit utilisation and on credit from formal sources. Second, we analyse the extent towhich higher formal credit utilisation led to impacts on the performance of small firms.

Supply of Formal Credit and Credit Utilisation

The empirical literature provides evidence of high marginal productivity of capital from formalsources. This seems to be the case for small Sri Lankan (de Mel, McKenzie & Woodruff, 2008b),small Mexican (McKenzie & Woodruff, 2008) and medium-sized Indian firms (Banerjee & Duflo,2008). These studies find that returns to capital are higher than the interest rates charged by banks, soentrepreneurs would be happier to borrow even more than they are offered. These suggest that creditmatters, at least for smaller entrepreneurs in developing countries.

Expanding Microfinance in Brazil 1259

Dow

nloa

ded

by [

Was

hing

ton

Uni

vers

ity in

St L

ouis

] at

13:

24 0

4 O

ctob

er 2

014

Here we examine whether in Brazil the utilisation of credit has increased after the start of theCrediAmigo programme in 1998. Increased access to credit does not necessarily imply increasedutilisation of credit. The utilisation of credit is the end result of an interaction between the supply ofcredit by formal entities and the demand for credit by micro-entrepreneurs. To the extent that theconditions for loans are not attractive, it is possible that a greater supply of credit may not beassociated with an increased utilisation of credit.

One potential constraint associated with the estimation of the impact of the increased access tomicrocredit through CrediAmigo on credit utilisation by micro-entrepreneurs in Brazil is that theECINF survey does not contain a specific question about the source of credit from formal bankinginstitutions. Thus, while one can identify whether the source of credit was from a private or publicbank, one cannot attribute the source of credit only to CrediAmigo with any certainty. However, asmentioned above, by 2003 this programme was still the largest microfinance institution in the country,and in the north-east in particular, having been implemented in cities with very little or no sources ofmicrocredit. To our knowledge, there were no other important sources of microcredit in the north-eastregion of Brazil other than CrediAmigo in 2003 or earlier. In September 2003, the Federal Law No.10735 established that banks must earmark 2 per cent of cash deposits to microcredit transactions(Soares & Sobrinho, 2008). Given that the ECINF survey took place in October 2003, we believe thatit is practically impossible for other potentially important credit sources from banks other than BNB tobe reflected in the survey data.9

The ECINF survey of micro-entrepreneurs collects information on whether the entrepreneur hadused any credit in the previous three months10 and, conditional on the answer being positive, theprimary source of credit is identified, based on five alternative sources.11 The sources of creditidentified in the survey include friends and relatives, private or public banks, suppliers, and otherpersons/firms.12

Bearing in mind these caveats about the survey instrument, it is important to identify asclosely as possible the municipalities where CrediAmigo operated in 2003. Based on admin-istrative data from the programme, CrediAmigo, as of December 2003, was active in 1,172municipalities (out of a total of about 5,500 municipalities in the country as of 2003) in thenorth-east region and in the north of the states of Minas Gerais and Espirito Santo. Of the1,172 municipalities covered by CrediAmigo, 850 municipalities had more than 20 activeclients in 2003. Service is provided through a logistics structure comprised of 166 branches,44 service centres and 857 loan officers.

The publicly released versions of the ECINF surveys in 1997 and 2003 contain the state code butnot the municipality code for the residence of the micro-enterprise. The state code, however, providesa rather crude approximation of the areas of operation of the CrediAmigo programme that might inturn lead to a biased estimate on the utilisation of credit from CrediAmigo.13 In order to generate amore precise identification of the areas where access to credit was expanded as a result of theCrediAmigo programme, we utilised the complete list of municipalities in the north-east and south-east regions covered by the CrediAmigo programme, made available to us by the programmeadministration. We then managed to obtain permission from the Brazilian Institute of Geographyand Statistics (IBGE) to access the confidential municipality codes for the location of the micro-enterprises by working with the ECINF surveys within the premises of IBGE in Rio de Janeiro.14

In our analysis we employ the difference-in-differences (DD) estimator. This estimator comparesdifferences in the utilisation of credit between the treatment group (micro-entrepreneurs in themunicipalities of Brazil where CrediAmigo operated) and the control group (micro-entrepreneurs inareas where CrediAmigo did not operate) before and after the start of the CrediAmigo programme (in1998). The DD estimator offers the advantage that any time invariant pre-programme unobservedheterogeneity between the treatment and control groups is eliminated in the estimation of impacts. Theuntested maintained assumption behind the application of the DD estimator is that the time or trendeffect is identical across the treatment and control groups (see, for example, Blundell and Costa Dias,2000). We also include a number of control variables that may be useful for reducing any remainingstatistical bias.15

1260 E. Skoufias et al.

Dow

nloa

ded

by [

Was

hing

ton

Uni

vers

ity in

St L

ouis

] at

13:

24 0

4 O

ctob

er 2

014

The following regression equation defines a model that can nest various ‘difference’ estimatorscontrolling for individual, household and other observed characteristics:

Y i; tð Þ ¼ β0 þ βTT þ βRD2003þ βTR T�D2003ð Þ þXK

k¼1

θkXk i; tð Þ þ η i; tð Þ; (1)

where Y(i,t) denotes that the outcome of interest equals one if the household i in period/round t reportsusing credit in the previous three months prior to the month of the survey and equals zero otherwise; βand θ are fixed parameters to be estimated; T is a binary variable taking the value of one if thehousehold resides in a municipality where CrediAmigo operates (the treatment region), and zerootherwise. The binary variable D2003 is equal to one for the 2003 round of the ECINF survey, andequal to zero for the baseline (1997 round) observations. The vector X summarises observed individualand micro-enterprise characteristics. The last term in Equation (1), η, denotes the influence ofunobserved factors (it is a pure random error term with the usual properties).

The coefficient βT allows the conditional mean of the outcome indicator to differ between house-holds in treatment and control municipalities before the initiation of the CrediAmigo programme. Astatistically significant value of βT suggests that in 1997 there are pre-existing differences in the use ofcredit between the treatment municipalities (mostly in the north-east) and the control municipalities.Along similar lines, the coefficient βR allows the conditional mean of the outcome indicator to differbetween households across the 1997 and the 2003 rounds. The coefficient of primary interest in ouranalysis is βTR, the difference-in-differences estimate, which summarises the difference in the outcomemeans over time between the treatment and control municipalities, that is:

βTR ¼ E Y jT ¼ 1;D2003 ¼ 1;X ¼ �Xð Þ � E Y jT ¼ 1;D2003 ¼ 0;X ¼ �Xð Þ½ � � E Y jT ¼ 0;ð½D2003 ¼ 1;X ¼ �X Þ � E Y jT ¼ 0;D2003 ¼ 0;X ¼ �Xð Þ�:

Put differently, the parameter βTR provides an estimate of the ‘intent or offer to treat effect’ (ITE),which summarises the effect of the opportunity to access credit in municipalities in which CrediAmigooperates on the use of credit from formal banks (public or private; see Heckman, La Londe & Smith,1999).16 The ITE is an estimate of the impact of making the credit available in specific municipalities,regardless of whether micro-enterprises actually take advantage of the opportunity (by choice or not)to get the credit. The ITE is of particular interest to policy makers since it captures the operationalefficiency in the implementation of the CrediAmigo programme, as well as any potential generalequilibrium effects of the credit availability on non-borrowing micro-enterprises in the municipalitieswhere CrediAmigo operated.

With this background in mind, regression Equation (1) is estimated for each of the four sources ofcredit for two different samples from the 1997 and 2003 ECINF. Sample A consists of the full sampleof micro-entrepreneurs in the ECINF surveys. In this sample, the treatment variable T equals one if themicro-enterprise is located in a municipality in the north-east region of Brazil or in a municipality inthe states of Minas Gerais and Espirito Santo, where CrediAmigo operates/has clients, and equals zerootherwise. In this case, the comparison group consists of all other municipalities in the ECINF surveynot covered by CrediAmigo in the north and north-east, as well as in the centre, south, and south-eastregions.17 Given potential concerns that the trend in the comparison group may not be an adequaterepresentation of the trend that would have prevailed in the municipalities covered by CrediAmigo inthe north-east region, we also employ an alternative comparison group.

Sample B consists of micro-entrepreneurs from municipalities in the north-east region of Brazilcovered by CrediAmigo. In this sample, the treatment variable T equals one if the micro-enterprise islocated in a municipality of the north-east region in which CrediAmigo operates, and equals zero

Expanding Microfinance in Brazil 1261

Dow

nloa

ded

by [

Was

hing

ton

Uni

vers

ity in

St L

ouis

] at

13:

24 0

4 O

ctob

er 2

014

otherwise. In this case, the comparison group consists of all other municipalities in the north-east notcovered by CrediAmigo.

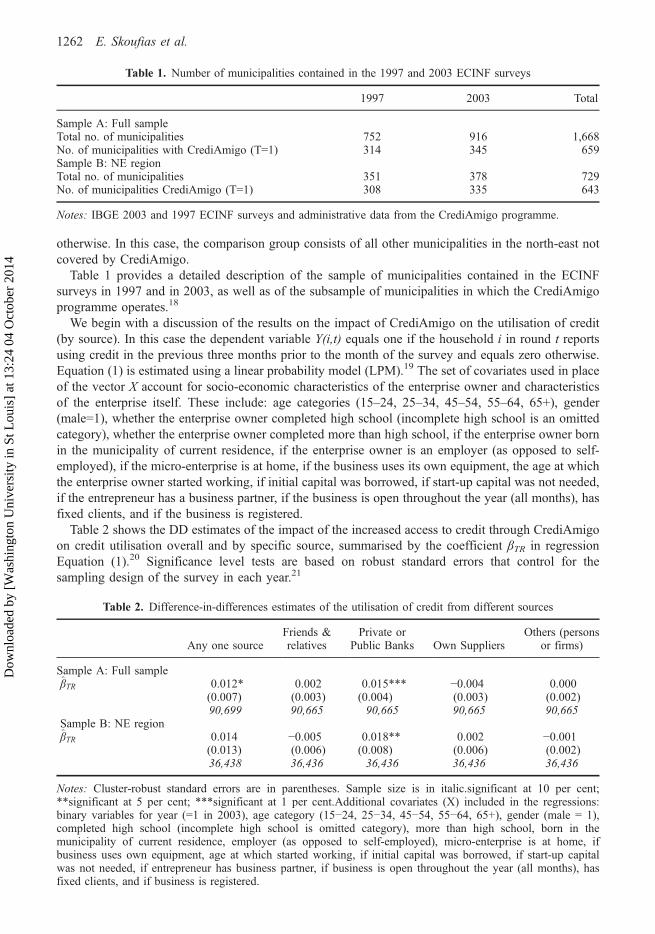

Table 1 provides a detailed description of the sample of municipalities contained in the ECINFsurveys in 1997 and in 2003, as well as of the subsample of municipalities in which the CrediAmigoprogramme operates.18

We begin with a discussion of the results on the impact of CrediAmigo on the utilisation of credit(by source). In this case the dependent variable Y(i,t) equals one if the household i in round t reportsusing credit in the previous three months prior to the month of the survey and equals zero otherwise.Equation (1) is estimated using a linear probability model (LPM).19 The set of covariates used in placeof the vector X account for socio-economic characteristics of the enterprise owner and characteristicsof the enterprise itself. These include: age categories (15–24, 25–34, 45–54, 55–64, 65+), gender(male=1), whether the enterprise owner completed high school (incomplete high school is an omittedcategory), whether the enterprise owner completed more than high school, if the enterprise owner bornin the municipality of current residence, if the enterprise owner is an employer (as opposed to self-employed), if the micro-enterprise is at home, if the business uses its own equipment, the age at whichthe enterprise owner started working, if initial capital was borrowed, if start-up capital was not needed,if the entrepreneur has a business partner, if the business is open throughout the year (all months), hasfixed clients, and if the business is registered.

Table 2 shows the DD estimates of the impact of the increased access to credit through CrediAmigoon credit utilisation overall and by specific source, summarised by the coefficient βTR in regressionEquation (1).20 Significance level tests are based on robust standard errors that control for thesampling design of the survey in each year.21

Table 1. Number of municipalities contained in the 1997 and 2003 ECINF surveys

1997 2003 Total

Sample A: Full sampleTotal no. of municipalities 752 916 1,668No. of municipalities with CrediAmigo (T=1) 314 345 659Sample B: NE regionTotal no. of municipalities 351 378 729No. of municipalities CrediAmigo (T=1) 308 335 643

Notes: IBGE 2003 and 1997 ECINF surveys and administrative data from the CrediAmigo programme.

Table 2. Difference-in-differences estimates of the utilisation of credit from different sources

Any one sourceFriends &relatives

Private orPublic Banks Own Suppliers

Others (personsor firms)

Sample A: Full sampleβ̂TR 0.012* 0.002 0.015*** −0.004 0.000

(0.007) (0.003) (0.004) (0.003) (0.002)90,699 90,665 90,665 90,665 90,665

Sample B: NE regionβ̂TR 0.014 −0.005 0.018** 0.002 −0.001

(0.013) (0.006) (0.008) (0.006) (0.002)36,438 36,436 36,436 36,436 36,436

Notes: Cluster-robust standard errors are in parentheses. Sample size is in italic.significant at 10 per cent;**significant at 5 per cent; ***significant at 1 per cent.Additional covariates (X) included in the regressions:binary variables for year (=1 in 2003), age category (15−24, 25−34, 45−54, 55−64, 65+), gender (male = 1),completed high school (incomplete high school is omitted category), more than high school, born in themunicipality of current residence, employer (as opposed to self-employed), micro-enterprise is at home, ifbusiness uses own equipment, age at which started working, if initial capital was borrowed, if start-up capitalwas not needed, if entrepreneur has business partner, if business is open throughout the year (all months), hasfixed clients, and if business is registered.

1262 E. Skoufias et al.

Dow

nloa

ded

by [

Was

hing

ton

Uni

vers

ity in

St L

ouis

] at

13:

24 0

4 O

ctob

er 2

014

The DD estimates reported in Table 2 reveal that overall the utilisation of credit (independently ofsource) increased by 1.2 percentage points in the full sample or 48 per cent of growth in creditutilisation between 1997 and 2003. Moreover, the utilisation of formal credit from private or publicbanks as a primary source of credit increased by 1.5 percentage points without any indication that theutilisation of credit from other sources declined in a statistically significant sense. Thus, the increasedaccess to credit offered through CrediAmigo not only increases the utilisation of credit from the privateor public sector, but it also appears to be associated with an overall increase in the utilisation of credit,without replacing pre-existing sources of credit, such as suppliers or friends and relatives. Thesefindings are consistent with the presence of binding constraints in accessing credit prior to theinitiation of loans by CrediAmigo.

The results obtained for the full sample are mostly driven by the results found using only the north-east region (Sample B). The DD analysis in this sample shows that the utilisation of formal credit fromprivate or public banks increased by 1.8 percentage points, that is 72 per cent of the observedincrement in formal credit taking between 1997 and 2003.

While there is a significant increase in the use of credit from any source in the full sample, there isno apparent (statistically significant) increase on the overall utilisation of credit in the north-eastregion. To a large extent, this rather peculiar result can be attributed to the fact that the comparisongroup is different in each of the samples.

Is Credit Take-up Higher among Women?

Unlike most commercial banks, which tend to offer credit to men mainly because they run largerbusinesses, microfinance is a different business (Armendáriz & Morduch, 2010). Pioneer programmessuch as the Grameen Bank were built around serving women. Essentially, women are mostly involved insmall businesses, contributing to the large informal sector in developing economies. Women also tend to bemore credit-constrained than men. They are reported to be more conservative in their investment strategies,thus are better than men at repaying loans. Finally, women are overrepresented among the poorest.

For these many reasons, given that overall formal credit utilisation increased as a result of morecredit supply in municipalities, one wonders if the formal credit take-up is higher among women thanmen in Brazil.22 Table 3 confirms this prediction, showing that females take significantly more credit

Table 3. Difference-in-differences estimates of the utilisation of credit from formal or any sources, males and females

Any one source Private or Public Banks

Males Females Males Females

Sample A: Full sampleβ̂TR 0.007 0.021* 0.009* 0.025***

(0.008) (0.011) (0.005) (0.007)59,137 31,562 59,109 31,556

Sample B: Northeast regionβ̂TR −0.005 0.051** 0.007 0.038***

(0.015) (0.022) (0.011) (0.013)22,993 13,445 22,991 13,445

Notes: Cluster-robust standard errors are in parentheses. Sample size is in italic. *significant at 10 per cent;**significant at 5 per cent; ***significant at 1 per cent. Additional covariates (X) included in the regressions:binary variables for year (=1 in 2003), age category (15–24, 25–34, 45–54, 55–64, 65+), completed high school(incomplete high school is omitted category), more than high school, born in the municipality of current residence,employer (as opposed to self-employed), micro-enterprise is at home, if business uses own equipment, age atwhich started working, if initial capital was borrowed, if start-up capital was not needed, if entrepreneur hasbusiness partner, if business is open throughout the year (all months), has fixed clients, and if business isregistered.

Expanding Microfinance in Brazil 1263

Dow

nloa

ded

by [

Was

hing

ton

Uni

vers

ity in

St L

ouis

] at

13:

24 0

4 O

ctob

er 2

014

than males, regardless of the sample used. The overall credit utilisation (independently of source)increased by 2.1 percentage points among women but did not increase among males. The utilisation offormal credit increased by 2.5 percentage points for women and less than 1 percentage point for men,in both cases statistically significant. Focusing exclusively in the north-east (Sample B), this gap iseven higher, with utilisation of credit from private or public banks increasing by 3.8 percentage pointsamong women and showing no statistically significant increase among males. Thus, in principle, thisanalysis suggests that there are large differences in credit usage by gender. In view of these findings,the analysis of how credit usage reflects on firm performance allows for heterogeneous impacts acrossmale and female micro-entrepreneurs.

Formal Credit Utilisation and Performance of Small Firms

The preceding analysis provided evidence that the increased access to microcredit in the municipalitieswhere CrediAmigo operated was associated with increased use of credit from formal sources, fromeither private or public banks. In this section we investigate whether the profits of micro-enterprisesincrease with the utilisation of formal sources of credit. Given that micro-enterprise profits are animportant component of household welfare we can infer indirectly the impacts of the increasedavailability of credit on household welfare.

Our analysis of the impact of credit on small business performance is carried out using data from the 2003ECINF survey, by comparing the performance of firms utilising credit from public or private banks with theperformance of a comparison group of firms using credit from informal sources or no credit at all. We use twomeasures of performance: business profit and number of employees. The profit variable is constructed by thedifference between revenues and expenditures per month (in October).23

We take into account substantial differences in living costs across areas in Brazil by adjusting ourmeasure of profits using spatial price indices (World Bank, 2007a). In the ECINF 2003, there is alsodetailed information on entrepreneur characteristics, which we use as control variables.

Specifically, our estimate of the impact of credit on business performance is based on two differentsamples using the 2003 ECINF survey and focusing on cities with the CrediAmigo programme.Sample C consists of the sample of micro-entrepreneurs in the north-east region and in the states ofMinas Gerais & Espirito Santo of the south-east region. Sample D consists of the sample of micro-entrepreneurs in the north-east region exclusively.

In each of these samples some micro-entrepreneurs have credit from public or private banks andsome (or the majority) do not have any credit at all. We use the propensity score matching (PSM)method to match one or more entrepreneurs with no credit or credit from informal sources to a micro-entrepreneur who used credit from a private or public bank and thus estimate the ‘average treatmenteffect on the treated’ (ATT):

ATT ; E Y1 � Y0jT ¼ 1f g ¼ E Y1 � Y0jT ¼ 1; p Xð Þf g ¼ E E Y1jT ¼ 1; p Xð Þ½ �f�E Y0jT ¼ 0; p Xð Þ½ �jT ¼ 1g;

where Y1 and Y0 are the outcomes of interest (profits or number of employees), under treatment andnon-treatment; T is the indicator for exposure to treatment (=1 if the individual has credit from a publicor private bank, and equal to zero if not); p(X)≡Pr(T=1|X)=E(T|X) is the conditional probability ofusing credit, given pre-treatment characteristics X (see, for example, Rosenbaum (2002), Sianesi(2001) and Leuven and Sianesi (2003). The set of pre-treatment characteristics used in the logitspecification of whether a micro-entrepreneur has credit from public or private banks includes: binaryvariables for age category (15–24, 25–34, 45–54, 55–64, 65+), gender (male = 1), if the micro-entrepreneur completed high school (incomplete high school is an omitted category), if the micro-entrepreneur completed more than high school, whether the micro-entrepreneur was born in themunicipality of current residence, whether the micro-entrepreneur is an employer (as opposed to

1264 E. Skoufias et al.

Dow

nloa

ded

by [

Was

hing

ton

Uni

vers

ity in

St L

ouis

] at

13:

24 0

4 O

ctob

er 2

014

self-employed), if the micro-enterprise is at home, if the business uses its own equipment, the age atwhich the micro-entrepreneur started working, if initial capital was borrowed, if start-up capital wasnot needed, if the entrepreneur has a business partner, if the business is open throughout the year (allmonths), if the business has fixed clients, if the business is registered, and municipality dummies.24

Online Appendix Table A4 shows the means of covariates by treatment status and relevant statistics,before and after the matching.

The first column of Tables 4 and 5 show the impact on profits and the number of employees,respectively. The second column of these tables shows the impact on indicators of high (aboveaverage) profits and number of employees. This is useful because measured profits are very dispersed,including negative values. In addition, we use the results for binary outcomes to later perform somesensitivity analysis.

In terms of profits, the results show that the use of formal sources of credit is associated withsignificantly higher profits. In Sample C, results suggest that using formal credit versus having nocredit or other sources, such as family, leads to an increase of 281 Reais in profit (46% of averageprofit in 1997). In Sample D, returns are smaller but not dissimilar: 247 Reais, representing 41 per centof the average profits in this region.

The results using binary outcomes also confirm a significant and sizable effect of formal credittaking on the probability of having high profits (that is, profits that are greater than the sample mean).This effect is 0.11 percentage points or a 63 per cent increase in the probability for the north-eastsample and 0.12 or a 49 per cent increase for the full sample.

In terms of firm size, the use of formal sources of credit does lead to a significant increase of 0.18employees (about 42% of sample average) in the north-east sample and a similar increase in thenumber of employees in the full sample (about 43% of sample mean). The probability that a business

Table 5. The impacts of credit on the number of employees in the micro-enterprise

# of Employees 1 (if # Employees>mean)

Sample C: NE region + Minas Gerais and Espirito Santo states 0.183*** 0.086***(0.055) (0.020)14,221 14,22143% 37%

Sample D: NE 0.179*** 0.084***(0.055) (0.020)14,084 14,08442% 35%

Notes: Method used: PSM (kernel matching). Standard errors are in parentheses. Sample size is in italic.Percentages of sample mean are indicated in third line of each set of results. *significant at 10 per cent;**significant at 5 per cent; ***significant at 1 per cent.

Table 4. The impacts of formal source of credit on the profits of micro-enterprises

Profits in Reais 1 (if Profits>mean)

Sample C: NE region + Minas Gerais and Espirito Santo states 281.492*** 0.115***(108.471) (0.020)14,221 14,22146% 49%

Sample D: NE region 246.808*** 0.112***(107.731) (0.020)14,084 14,08441% 63%

Notes: Method used: PSM (kernel matching). Standard errors are in parentheses. Sample size is in italic.Percentages of sample mean are indicated in third line of each set of results. *significant at 10 per cent;**significant at 5 per cent; ***significant at 1 per cent.

Expanding Microfinance in Brazil 1265

Dow

nloa

ded

by [

Was

hing

ton

Uni

vers

ity in

St L

ouis

] at

13:

24 0

4 O

ctob

er 2

014

is large also increases significantly in the north-east by 8.4 percentage points and in the whole sampleby 8.6 percentage points, which stands for 35 and 37 per cent, respectively, of the proportion of largebusinesses in each sample.

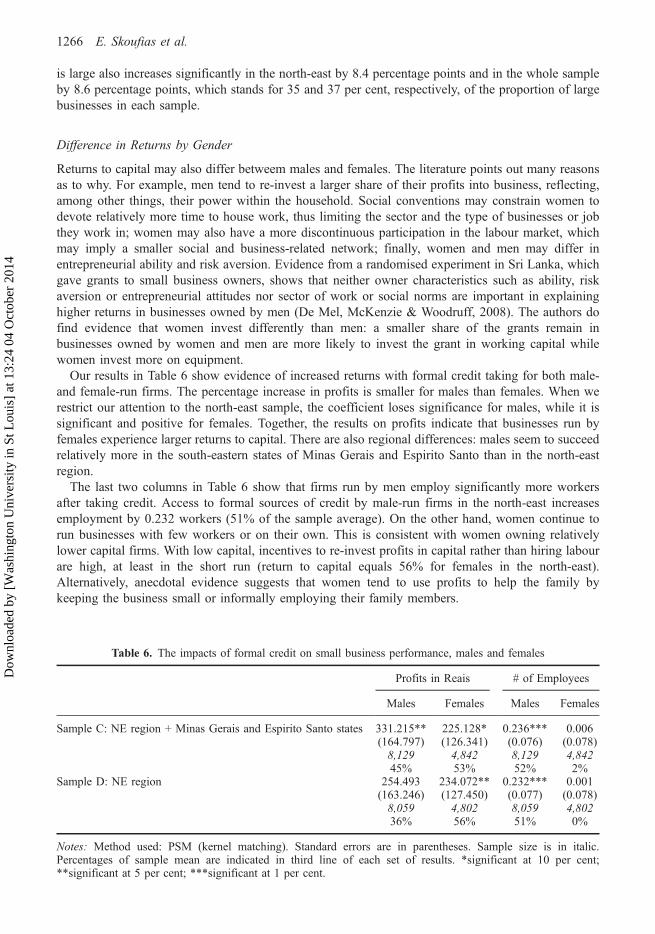

Difference in Returns by Gender

Returns to capital may also differ betweem males and females. The literature points out many reasonsas to why. For example, men tend to re-invest a larger share of their profits into business, reflecting,among other things, their power within the household. Social conventions may constrain women todevote relatively more time to house work, thus limiting the sector and the type of businesses or jobthey work in; women may also have a more discontinuous participation in the labour market, whichmay imply a smaller social and business-related network; finally, women and men may differ inentrepreneurial ability and risk aversion. Evidence from a randomised experiment in Sri Lanka, whichgave grants to small business owners, shows that neither owner characteristics such as ability, riskaversion or entrepreneurial attitudes nor sector of work or social norms are important in explaininghigher returns in businesses owned by men (De Mel, McKenzie & Woodruff, 2008). The authors dofind evidence that women invest differently than men: a smaller share of the grants remain inbusinesses owned by women and men are more likely to invest the grant in working capital whilewomen invest more on equipment.

Our results in Table 6 show evidence of increased returns with formal credit taking for both male-and female-run firms. The percentage increase in profits is smaller for males than females. When werestrict our attention to the north-east sample, the coefficient loses significance for males, while it issignificant and positive for females. Together, the results on profits indicate that businesses run byfemales experience larger returns to capital. There are also regional differences: males seem to succeedrelatively more in the south-eastern states of Minas Gerais and Espirito Santo than in the north-eastregion.

The last two columns in Table 6 show that firms run by men employ significantly more workersafter taking credit. Access to formal sources of credit by male-run firms in the north-east increasesemployment by 0.232 workers (51% of the sample average). On the other hand, women continue torun businesses with few workers or on their own. This is consistent with women owning relativelylower capital firms. With low capital, incentives to re-invest profits in capital rather than hiring labourare high, at least in the short run (return to capital equals 56% for females in the north-east).Alternatively, anecdotal evidence suggests that women tend to use profits to help the family bykeeping the business small or informally employing their family members.

Table 6. The impacts of formal credit on small business performance, males and females

Profits in Reais # of Employees

Males Females Males Females

Sample C: NE region + Minas Gerais and Espirito Santo states 331.215** 225.128* 0.236*** 0.006(164.797) (126.341) (0.076) (0.078)8,129 4,842 8,129 4,84245% 53% 52% 2%

Sample D: NE region 254.493 234.072** 0.232*** 0.001(163.246) (127.450) (0.077) (0.078)8,059 4,802 8,059 4,80236% 56% 51% 0%

Notes: Method used: PSM (kernel matching). Standard errors are in parentheses. Sample size is in italic.Percentages of sample mean are indicated in third line of each set of results. *significant at 10 per cent;**significant at 5 per cent; ***significant at 1 per cent.

1266 E. Skoufias et al.

Dow

nloa

ded

by [

Was

hing

ton

Uni

vers

ity in

St L

ouis

] at

13:

24 0

4 O

ctob

er 2

014

We also carried out sensitivity tests for the propensity score estimates following Becker & Caliendo(2007) to test for several deviations from the conditional independence assumption (the procedure andmain results are in the Online Appendix). We find that our estimates are robust, considering bothperformance outcomes and different subsamples.

Concluding Remarks and Policy Considerations

Our main findings suggest that an exogenous increase in the supply of credit through the CrediAmigoprogramme raised formal credit utilisation and that the use of formal credit did not crowd out creditfrom informal sources such as family and friends. Overall, the utilisation of credit independently ofsource increased by 1.2 percentage points, while formal credit utilisation increased by 1.5 percentagepoints. Moreover, these effects differ across male and female owners. Females take more credit frombanks or formal institutions than males. This is consistent with the focus of microfinance on women,reinforcing the argument that, amongst other factors, women are more credit-constrained than men,they are overrepresented among the poorest, and they are better at repaying their loans. We also showthat the use of credit from formal sources is associated with better business performance, meaninglarger business profits and number of employees. Individuals who use formal sources of credit seem tore-invest it towards higher returns and larger businesses.

The results for males and females are twofold: on the one hand, returns are large and higher forfemale- than male-owned firms; on the other hand, existing businesses run by males employ sig-nificantly more workers after taking formal credit, while firms owned by women do not. This meansthat if microcredit policies were to focus on women, they would achieve relatively more credit takingand profits but less employment, at least in the short run, with high returns to capital. The availabilityof formal credit targeted to women is likely to be an effective way to encourage women to establishand develop small businesses, increase their participation in the labour market and their economicempowerment.

Acknowledgements

The authors are grateful to the CrediAmigo administration (Stelio, Iracema and Marcelo) that madepossible this analysis, and to Susana Sanchez, Pedro Olinto, Edinaldo Tebaldi, Alinne Veiga, FranciscoHaimovich, and two anonymous referees for valuable comments and inputs throughout the longgestation of this project. The findings, interpretations, and conclusions in this article are entirelythose of the authors and they do not necessarily reflect the view of the World Bank.

Notes

1. In 1998, the per capita GDP in 2000 prices for the north-eastern states was from 1.51 to 3.65 thousand dollars, whereas forthe relatively richer south-eastern states the figure was about three times as much or more: 5.89 to 10.35 thousand dollars.Source: IPEADATA, IPEA, Brazil.

2. In fact, the PME contains information on the labour incomes of the self employed and employers. Neri (2008) uses thesedata as a measure of profit.

3. The reference month is October. It is also important to note that the ECINF surveys took place during the same calendarmonths in 1997 and 2003, thus minimising problems due to seasonal variation in the need for credit.

4. Enumeration areas (EA) were selected using a probabilistic sample proportional to size on the basis of the urban censusenumeration areas. Each EA contains on average 300 households.

5. Actually each state was segmented into three strata: the municipalities of the capital city; urban areas of the municipalities ofthe metropolitan area; and urban areas of the remaining municipalities of the state.

6. These key design features included solidarity group lending, targeting the informal sector, charging interest rates highenough to provide a return on assets, and to permit financial sustainability with gradually increased loans, amortising loansregularly, offering incentives for regular repayment through discounts on the last instalment, and penalising borrowers ifrepayment falls behind schedule.

7. This rate only applies to loans under 1,000 Reais. Clients are also required to pay a few other fees when obtaining a loan.

Expanding Microfinance in Brazil 1267

Dow

nloa

ded

by [

Was

hing

ton

Uni

vers

ity in

St L

ouis

] at

13:

24 0

4 O

ctob

er 2

014

8. Loan overdue rates were initially 4.2 per cent in the first year of the programme, but by writing off bad loans and modifyingthe performance-based incentive scheme for staff, by 2003 only 1.8 per cent of programme loans were overdue more thanone day (Banco do Nordeste, 2003).

9. The fraction of credit that is not from CrediAmigo can be interpreted as measurement error in the dependent variable.Therefore, coefficients remain unbiased. This only decreases efficiency. Yet, our coefficients are significant and most at 1 or5 per cent level, as we will show later.

10. We use variable V4331, which equals three for occasional or five for frequent access to credit.11. The emphasis on the primary source of credit implies that we cannot distinguish whether micro-entrepreneurs used more

than one source of credit.12. We use variable V4332, which equals one if credit is from friends or relatives, two if from private or public banks, three if

from suppliers, and four or five if from other firms, people or other sources.13. For example, Neri (2008) reports difference-in-differences estimates of the increased access to credit through CrediAmigo

using the same surveys by simply comparing the utilisation of credit in the nine states comprising the north-east region ofBrazil with all other states outside the north-east region.

14. The ECINF surveys can be obtained directly from IBGE (http://loja.ibge.gov.br). Please note that the municipality codescannot be made available due to a confidentiality agreement.

15. Table A1 shows means by treatment status. As the simple t-test suggests, there are significant differences between treatmentand control groups for most control variables in 1997. Thus, these factors need to be accounted for. In any case, later we alsopresent estimates of the treatment effects with and without the control variables.

16. Treatment in this case is ‘exposure to credit’ from CrediAmigo. Because exposure is involuntary, βTR provides the intent-to-treat rather than the treatment-on-treated effect.

17. As a means of testing the sensitivity of the results, we have also estimated Equation (1) using the treatment variable T=1 ifthe micro-enterprise is located in any of the nine states (instead of the specific municipality) in the north-east region and inthe Minas Gerais and Espirito Santo states in the south-east region, and equal to zero otherwise. In this case the comparisongroup consists of all other states not covered by CrediAmigo. The DD estimates in this case were slightly lower overall (forexample, the utilisation of formal credit as a primary source increased by 1.3% instead of 1.5%).

18. Given the sampling design of the ECINF surveys, not every municipality sampled in the 1997 ECINF necessarily appears inthe 2003 survey. However, when we use the DD estimator we do not have to limit our analysis to the set of municipalitiesthat appears in both survey rounds. We run the DD regressions using the sampling weights in each year to account for thestratification procedure explained in Note 5.

19. Given that very similar estimates were obtained using a probit and logit model we chose to report the LPM estimates, sincethe coefficients of the LPM provide direct estimates of the marginal effect on the probability of utilising credit.

20. The full set of estimates of Equation (1) based on Samples A and B are presented in Tables A2 and A3. In particular, theseshow the bias correction by including the covariates. In the full sample, it accounts for the treatment group being worse thanthe control group in terms of human capital and business capacity in 1997, thus with more need of capital. In the north-eastsample, it accounts for the treatment group being relatively better in 1997.

21. Specifically, we cluster our standard errors by enumeration area in each municipality and each year of the survey. As pointedout by Bertrand, Duflo,& Mullainathan (2004), the DD estimator has potentially serious limitations, especially if there isserial correlation in the error term of the regression. We have also investigated the sensitivity of our results, taking intoaccount the potential for serial correlation within municipalities (and states). We found that the correction for serialcorrelation did not have any substantial change in the results reported here.

22. The CrediAmigo programme focused on established entrepreneurs who are found among likely vulnerable groups, such asthe self employed and small businesses, in which women tend to be overrepresented.

23. Revenues are defined as the sum of the value of sales of own product, resale of merchandise, provision of services and otherreceipts. Expenditures are the sum of expenditures on inventories (primary material and items for resale), labour costs,contributions to social security (INSS), severance pay (FGTS), electricity, water, telephone, rental, machines, equipment,vehicles, gasoline, repair and maintenance, taxes, financial and other expenditures.

24. The inclusion of a set of binary variables for municipality implies that micro-entrepreneurs with credit in any givenmunicipality are matched with micro-entrepreneurs without credit in the same municipality.

References

Armendáriz, Beatriz, & Morduch, Jonathan. (2010). The economics of microfinance (2nd ed.). Cambridge, MA: MIT Press.Banco do Nordeste. (2003). CrediAmigo: The experience of the Bank of Northeast of Brazil with microcredit. In Stelio Gama

Lyra Junior (Ed.), Fostering the sustainable development of microcredit in Brazil. Fortaleza. Retrieved from http://www.bnb.gov.br/content/aplicacao/produtos_e_servicos/crediamigo/docs/resultado_2003_eng.pdf

Banerjee, Abhijit, & Duflo, Esther. (2008). Do firms want to borrow more: Testing credit constraints using a targeted lendingprogram. BREAD Working Paper No. 005, 2004, revised 2008, Duke University.

Banerjee, Abhijit, Duflo, Esther, Glennerster, Rachel, & Kinnan, Cynthia. (2010). The miracle of microfinance? Evidence from arandomized evaluation. BREAD Working Paper No. 278, Duke University.

1268 E. Skoufias et al.

Dow

nloa

ded

by [

Was

hing

ton

Uni

vers

ity in

St L

ouis

] at

13:

24 0

4 O

ctob

er 2

014

Becker, Sacha O., & Caliendo, Marco. (2007). Sensitivity analysis for average treatment effects. The Stata Journal, 7, 71–83.Bertrand, Marianne, Duflo, Esther, & Mullainathan, Sendhil. (2004). How much should we trust differences-in-differences

estimates? The Quarterly Journal of Economics, 119, 249–275.Blundell, Richard, & Costa Dias, Monica. (2000). Evaluation methods for non-experimental data. Fiscal Studies, 21, 427–468.de Mel, Suresh, McKenzie, David, & Woodruff, Christopher. (2008a). Who are the microenterprise owners?: Evidence from Sri

Lanka on Tokman v. de Soto. World Bank Policy Research Working Paper 4635.de Mel, Suresh, McKenzie, David, & Woodruff, Christopher. (2008b). Returns to capital in microenterprises: Evidence from a

field experiment. The Quarterly Journal of Economics, 123, 1329–1372.Dupas, Pascaline, & Robinson, Jonathan. (2011). Savings constraints and microenterprise development: Evidence from a field

experiment in Kenya. Cambridge, MA: NBER Working Paper # 14693.Heckman, James, LaLonde, Robert, & Smith, Jeffrey. (1999). The economics and econometrics of active labor market programs.

In Orley Ashenfelter & David Card (Eds.), Handbook of labor economics Vol. III (pp. 1865–2097). Amsterdam: Elsevier.Jain, Sanjay. (1999). Symbiosis vs. crowding-out: The interaction of formal and informal credit markets in developing countries.

Journal of Development Economics, 59, 419–444.Karlan, Dean, & Zinman, Jonathan. (2010). Expanding credit access: Using randomized supply decisions to estimate the

impacts. Review of Financial Studies, 23, 433–446.Kumar, Anjali. (2005). Access to financial services in Brazil. Washington, DC: World Bank.Leuven, E., & Sianesi, Barbara. (2003). PSMATCH2: Stata module to perform full Mahalanobis and propensity score matching,

common support graphing, and covariate imbalance testing. Retrieved from http://ideas.repec.org/c/boc/bocode/s432001.html

Mantel, N., & Haenszel, W. (1959). Statistical aspects of the analysis of data from retrospective studies of disease. Journal of theNational Cancer Institute, 22, 719–748.

McKenzie, David, & Woodruff, Christopher. (2008). Experimental evidence on returns to capital and access to finance inMexico. The World Bank Economic Review, 22, 457–482.

Neri, Marcelo. (2008). Microcredito: O Misterio Nordestino e o Grameen Brasileiro. Rio de Janeiro: Editoria FGV.Paulson, Anna L., & Townsend, Robert. (2004). Entrepreneurship and financial constraints in Thailand. Journal of Corporate

Finance, 10, 229–262.Rosenbaum, P. R. (2002). Observational studies (2nd ed.). New York: Springer.Rosenbaum, P.R., & Rubin, D.B. (1985). The bias due to incomplete matching. Biometrics, 41, 103–116.Sianesi, Barbara. (2001). Implementing propensity score matching estimators with STATA. UK Stata Users Group, VII Meeting

London. Retrieved from http://www.stata.com/meeting/7uk/sianesi.pdfSoares, Marden M., & Sobrinho, Abelardo D. M. (2008). Microfinancas: O Papel do Banco Central do Brasil e a Importancia

do Cooperativismo de Credito. Brasilia: Banco Central do Brasil.World Bank. (2007a). Brazil: Measuring poverty using household consumption. Washington, DC: The World Bank (Report #

36358-BR).

Expanding Microfinance in Brazil 1269

Dow

nloa

ded

by [

Was

hing

ton

Uni

vers

ity in

St L

ouis

] at

13:

24 0

4 O

ctob

er 2

014