enabling any mobile app to be a wallet - · pdf filethe wallet - expanding mcommerce to the...

TRANSCRIPT

Open Wallet PlatformEnabling Any Mobile App to Be a Wallet

WHITE PAPER

The Wallet - Expanding mCommerce to the Real WorldIn spite of the rapid growth of mobile commerce, payments made via mobile devices still only represent around 1% of all commerce in the United States1. Even e-commerce, around for over 15 years, still represents only close to 4% of all commerce in the US2. These percentages are even lower internationally. Mobile wallets have the potential to break mobile and e-commerce transactions out of these low adoption rates. Mobile wallets allow mobile phone users to make payments where 95% of transactions happen; in the real world of their daily lives.

The potential of mobile wallets has attracted some of the world’s largest corporations. The level of buzz surrounding mobile wallets shows it’s one of today’s hottest payment technologies but chances are you don’t use one today. While mobile wallets promise to revolutionize how we pay for daily necessities, implementation has been awkward or so complex and full of hurdles that most stakeholders, let alone consumers, become cool to it very fast.

1 eMarketer - Mobile Devices to Boost US Holiday Ecommerce Sales Growth2 US Census Bureau

2

A single wallet doesn’t fit the needs of all stakeholders

• Banks, merchants and MNOs don’t want to give up control

over customer engagement and data.

• Banks, merchants and MNOs don’t want to give up control

over brand and brand differentiation.

• And consumers want choice!

The fact is first generation wallet concepts were born before the iPhone and the app revolution and are outdated. Today thousands of apps are available from all major stakeholders and consumers are used to this choice. The key for mobile wallet success is not the do-it-all wallet app but enabling existing apps for payments.

Why Do Closed Wallets Fail?First generation mobile wallets try to be a single solution for all stakeholders. The problem is a single, closed wallet can’t be all things to everyone. Banks, mobile operators, merchants, and the consumers all have very different needs and expectations from a mobile wallet. The imposition of a do-it-all wallet app creates a cascade of unintended consequences that have led to many unsuccessful wallet deployments around the world.

MNO Wallet Banking App

Retailer App Access Control App(Non-Payment Issuers)

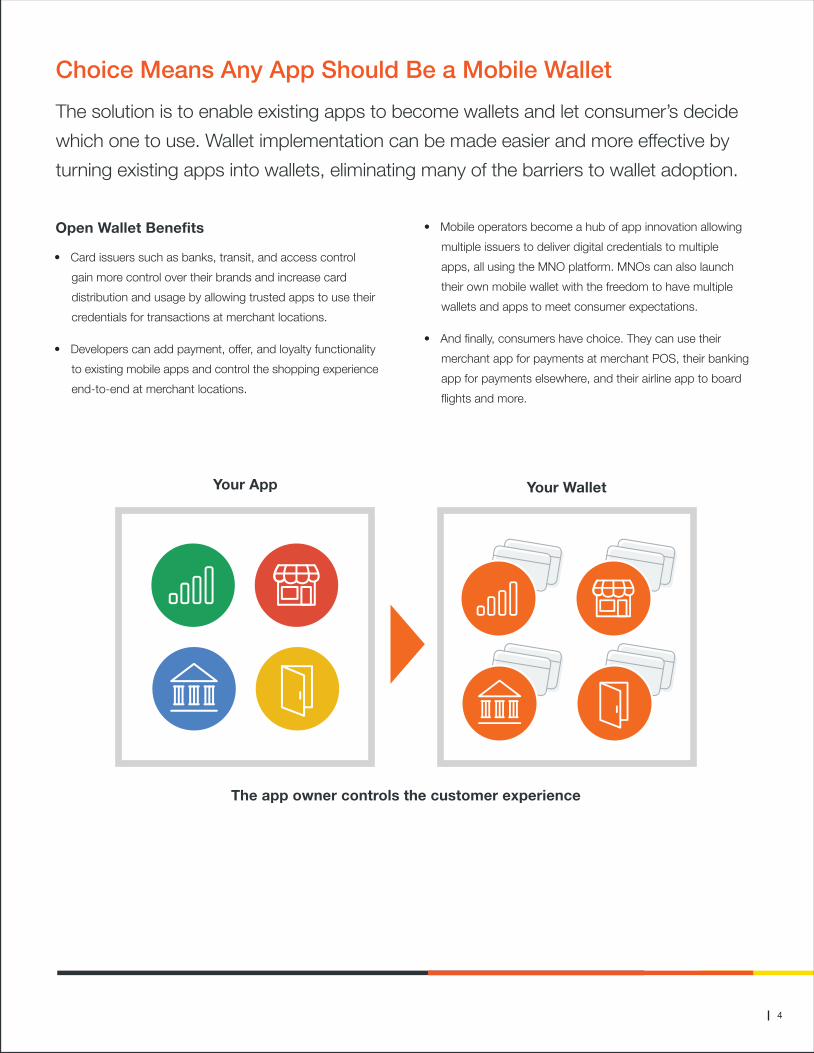

Choice Means Any App Should Be a Mobile WalletThe solution is to enable existing apps to become wallets and let consumer’s decide which one to use. Wallet implementation can be made easier and more effective by turning existing apps into wallets, eliminating many of the barriers to wallet adoption.

Open Wallet Benefits

• Card issuers such as banks, transit, and access control gain more control over their brands and increase card distribution and usage by allowing trusted apps to use their credentials for transactions at merchant locations.

• Developers can add payment, offer, and loyalty functionality to existing mobile apps and control the shopping experience end-to-end at merchant locations.

• Mobile operators become a hub of app innovation allowing multiple issuers to deliver digital credentials to multiple apps, all using the MNO platform. MNOs can also launch their own mobile wallet with the freedom to have multiple wallets and apps to meet consumer expectations.

• And finally, consumers have choice. They can use their merchant app for payments at merchant POS, their banking app for payments elsewhere, and their airline app to board flights and more.

The app owner controls the customer experience

Your App Your Wallet

4

The API-based open wallet approach allows for increased adoption by phone users while breaking down barriers between MNOs, banks, and other service providers. By retaining complete control of branding and user experience, issuers and service providers are enabled to extend existing relationships with customers while forging new ones with improved user experiences. Already existing or new apps are enriched with mobile payments, along with other value added services, like offers, gift cards, and loyalty programs. The increase in transaction volume and usage data benefits all players in the ecosystem by providing new revenue streams and greater marketing opportunities.

Sequent Open Wallet Platform is a comprehensive solution responsible for: • Lifecycle management of the wallet and mobile applications,

the service being offered, and end-user changes with respect to the device

• Service aggregation for delivery of rich services to the user

• Filtering and delivery of the service to the user.

The components of the Sequent Open Wallet Platform are:• Sequent on-device middleware (CCS) and SDK

• Robust and configurable backend system

• Reference white label wallet mobile app.

Sequent Open Wallet Platform SolutionSequent opens the mobile wallet concept and turns it inside out by allowing cards to be used by any authorized app. Whether a consumer prefers to pay with a card in their banking app or from their favorite coffee shop app, Sequent makes it possible. With the Sequent SDK and on-device middleware, Sequent Open Wallet Platform allows authorized app developers to access secure cards and make them available through any mobile app.

5

Core Card Services

Core Card Services (CCS) is the on-device middleware that provides mobile apps with the resources they need. By abstracting and isolating communications with the secure element or managing HCE tokens, multiple apps can securely share access to credentials. CCS manages the complexities of payment, compliance, and smartcards so that developers don’t have to worry about it. Developers can build NFC mobile payment and other services into their apps using the Sequent SDK with simplified APIs, such as Download Card, Link Card, Manage Card, and Start Card Emulation. Enabling apps for secure transactions has never been easier.

CCS abstracts all communication to backend system. As new services are onboarded (e.g., interactive marketing and location-based offers), they are made available to the applica-tions through APIs. This ensures that app developers can focus on application development and leave the complexities of the mobile payments ecosystem to Sequent Open Wallet Platform.

The innovation on-device middleware introduces is the unique ability to allow other mobile applications to be linked to cards that have already been downloaded. With CCS and the SDK, any app can use any card with permission of the secure element owner (program manager) and the issuer. The permission to access credentials is managed by the Sequent Open Wallet Platform server through its administrative console. Once the permissions have been defined, users can link credentials to their favorite mobile apps through the link card interface on the mobile wallet.

Figure 1 - Sequent’s open wallet architecture

SE Cloud FileSystems

LinkageRules

SmartPosterNFC BarcodeQR

Codes

APIsWallet Platform Abstraction Layer

AggregatorWallet

MNOWallet

mBankingWallet

MerchantWallet

Device

Redemption Storage

6

Wallet Management ServerSequent Open Wallet Platform Wallet Management Server acts as a single point of aggregation for all issuers, service providers, and service types that are streamed to wallets participating in mobile payment services. The following services are provided and configured in the Wallet Management Server administrative console.

Manage Wallet Configuration

The Wallet Management Server allows dynamic management and configuration of the wallet based on backend settings. Configurable settings include the display sequence of cards, categories of supported cards, security settings, and more. MNOs can rollout services that support branding and configu-ration by sub-brands, with each brand having their own terms and conditions, images, supported services, and associated use cases.

Onboarding Issuers, Service Providers, and Credential Metadata

The Wallet Management Server facilitates onboarding of issuers of secure credentials as well as other service providers. This includes but is not limited to credit, prepaid, stored value, access control, and identity management using NFC, QR codes, and barcodes. In addition, the platform aggregates value added services including offers, loyalty, and gift cards. Metadata for secure and non-secure credentials are maintained via the Wallet Management Server and subse-quently synced with CCS on-device middleware.

Access rules are managed in the Wallet Management Server. When an issuer is onboarded, the issuer chooses the access rules it wants to enforce; in other words, which apps it will allow to access its credentials. When an application is onboarded, the issuer chooses which credentials it wants to support in its app. The intersection of business rules deter-mines which credentials are available to an authorized mobile application. The Wallet Management Server serves the rules to CCS, which in turn manages the security and the execution of the rules on-device. The rules are stored encrypted in the phone database and CCS decrypts the rules at runtime.

Manage Business Rules and Permissions between Apps and Secure Credentials

All apps onboarded to the platform must be configured to access selected APIs. While app developers can specify which credentials they want to enable in their app, issuers can specify which app has access to select credentials. These linkage rules insure that all parties remain in control of their own brand and relationships with customers. The level of access to the secure element or HCE tokens is managed with configurable access to the APIs. Apps are also limited in terms of what APIs they have access to. During app onboarding, each app is given access to a set of APIs based on the profile of the app. For example, a banking app can add and delete a card. A merchant app can only view a list of cards and select/deselect a card for emulation

Manage All Lifecycle EventsNFC Service Lifecycle

• Service activation and termination• Lock/unlock of wallet• Reset passcode by Care

Device Lifecycle • Lost/stolen device• Recover device• Port wallet on device swap• Update system on phone number change• New registration with new SIM card

Wallet and Mobile Application • Register wallet/application• Optional and mandatory update of wallet application • Block/unblock of application• Lock/unlock of wallet• Reinstall service on delete of wallet• Wipe of wallet application on service termination

The Wallet Management Server provides an administrative console for customer care professionals to manage common NFC service use cases such as lock/unlock of NFC service, block/unblock of mobile application, passcode reset, and terminate service. The features are exposed as APIs for easy integration with existing customer care portal.

7

Diagnostics

CCS on-device middleware monitors the use of the secure element, HCE tokens, the NFC baseband, TSM services, and credential requests by their associated mobiles apps. If the consumer is having a problem with the wallet, diagnostics data is provided in real-time to the Wallet Management Server so that customer care professionals can easily diagnose issues.

Reports and Analytics

The Open Wallet Platform persists all on-device and backend data and categorizes them into appropriate reports. Out of the box reports include Wallet Usage report, App Linkage and Access report, System Access report, Activity report and Activity Failure report. In addition, data is aggregated into insightful reports and categories that measure success of the wallet program.

VAS and Service AggregationOne of the core functions of the Open Wallet Platform is service aggregation and delivery of rich services to the phone user. These services include offers, loyalty, and stored value cards such as prepaid and gift via all proximity technologies including NFC, QR codes, and barcodes. Open Wallet Platform is a single aggregation point for provisioning diverse services from service providers. Value added services, including loyalty, offers, gift card, and prepaid can be accessed using selected APIs in the platform. Open Wallet Platform services make possible the rich in-app consumer experiences exemplified in the use cases illustrated in Figure 2.

The Open Wallet Platform supports offers, gift, and prepaid programs and is provisioned to support loyalty programs from any service provider. The offers module of the platform allows administrators to create offers and target users based on phone numbers and regions. The platform also provides APIs for merchants to push offers to the phone user. From the wallet, users can buy prepaid and gift cards or add existing cards. Users can check balances, view transaction history, perform top-up and auto top-up for prepaid cards and buy and send a gift card to friends and families.

Wallet ManagementPlatform Server &

Service Aggregation

VAS Offers

Loyalty Gift

Prepaid Transit

Event Tickets

Aggregator Wallet

VAS

Offers Gift Transit

Loyalty Prepaid Ticket

Service Bus

Figure 2 - Value-added Services on Sequent Open Wallet Platform

8

Secure mCommerce Services

Sequent Open Wallet Platform provides all the essential services needed today to rollout rich mCommerce user experience. This includes payment and non-payment cards such as access control and transit cards and support of VAS features such as offers, prepaid, and gift. Sequent has standalone interactive marketing applications that deliver smart-poster triggered offers and manage loyalty programs for merchants. For secure element owners, Sequent’s key-ring application allows their enterprise customers to secure their mobile apps using keys saved in the secure element.

Sequent has identified a rich set of services that it would like to provide its customers and their end users. The Open Wallet Platform exposes all these services through the SDK to participating mobile applications. The flexibility of this open platform enables Sequent customers to lead the way in delivering superior mCommerce experiences to their users.

Reference White Label Wallet Application

Utilizing the Sequent SDK, the Sequent Wallet is a white label wallet designed to be a turnkey solution for MNOs, banks, and others to provide a quick time-to-market wallet to their consumers. The wallet provides a feature-rich and elegant solution that is intuitive, secure, and easy to use. It is designed to take full advantage of the configurable Open Wallet Platform server and CCS, making it easy to integrate to value added services offered in the Open Wallet Platform.

Figure 3 - Roadmap to Expanded mCommerce through NFC Services

Wallet Management Server &Service Aggregation Acquiring Network

Your App Merchant App Transit App Hotel App Corporate App Other Apps

SDK for Apps

Payment Non Payment VAS Key-ring mPOS ePOS Future

VAS ServiceProviders

9

The Sequent Wallet can be branded and customized as needed to suit the wallet provider. Built using XML frames, MNOs and service providers can easily create content used in the wallet without the need of special ‘widget’ tools. The service provider experiences allow consumers to see the issued credentials as well as value added services while still in the same application. MNOs can also have their own experi-ence for their own value added services, and the ability to manage legacy MNO telecom accounts.

Key Features Supported by the Wallet

• Support for payment and non-payment cards such as access control and transit.

• Support for prepaid, gift, loyalty, and offers.

• Default card

• Security settings including passcode, security questions, and offline counter.

• Configurable setting for security options, notifications, and display options

• Help and quick tips

My Wallet

Aggregator Wallet

Bank App

Pay Now

mBanking App

Transit App

Tap Now

3rd Party App

Store App

Pay Now

3rd Party App

Figure 4 - Many-to-many credential and app relationships

10

All Parties Win

• MNOS and other secure element owners can increase ROI in mobile commerce by enabling multiple apps to utilize credentials in the secure element or the cloud for proximity transactions and thereby increasing adoption from consumers.

• Banks and other issuers are able to control exactly which app can access their own secure credentials stored in the secure element or the cloud. Increased distribution of these secure credentials further improves ROI.

• Banks, merchants, and others can maintain relationships with their consumers with enriched in-app experiences (without leaving the app). A wealth of consumer behavioral data is unlocked for further personalization of services.

• “Any App Can Be A Wallet” – App developers can open up new monetization opportunities and provide enriched experiences by enabling their apps for payments at physical stores and much more. Via an SDK and CCS on-device middleware, the complexities of payment, compliance, and smart cards are abstracted.

Offers, Coupons, Loyalty

The richness of the service and the user experience is achieved through delivery of rich value added services. Sequent Open Wallet Platform delivers offers, gift, and prepaid services today and seeks to add richer set of value added services over time including loyalty, interactive marketing, peer-to-peer transactions and more.

One-Stop Shop mCommerce Services

With Sequent Open Wallet Platform, customers can bank on one system to rollout a rich set of mCommerce services for the foreseeable future. Sequent is solely focused on delivering secure and trusted services to mobile apps. Customers simply leverage the Sequent SDK to extend features to their wallet and mobile applications without having to worry about integrating new systems to deliver new features.

Make it Simple

Sequent CCS on-device middleware ensures that app developers can focus on application development and not worry about all the variability involved in rolling out mCommerce services. CCS handles the complexities of secure element access and variability in redemption mode, devices, and OS types. The Wallet Management Server handles all the integration variability in sourcing diverse services from disparate systems.

Quick Integration, Easy Scaling

Sequent has made technology choices to facilitate fast scaling. For example, Sequent has chosen NoSQL database over a relational database for its Open Wallet Platform. The process-ing architecture is non-blocking – event capture and event processing are separate. Scale can be achieved with service providers through usage of standard APIs. Where standards exist (e.g., GlobalPlatform) Sequent has implemented Global-Platform standards to enable onboarding of secure credential service providers. Where standards are yet to evolve, especially for non-secure credentials, Sequent has worked with large customers to use Sequent’s APIs to onboard such non-secure service providers. Sequent Open Wallet Platform is already integrated with some of the large prepaid and gift card providers. Sequent's Loyalty Platform exposes APIs to easily onboard offer and loyalty service providers.

Sequent has brought to bear its many years of mobile payment pilot rollout experience in designing its platform in a modular manner. The Open Wallet Platform is designed to integrate with MNO systems (to perform subscriber eligibility check), service provider systems (to receive secure and non-secure creden-tials), and with NFC program manager systems (e.g., data systems and user profile systems).

Benefits of Sequent Open Wallet Platform

The Open Wallet Platform supports any number of wallet and mobile applications and allows them to share credentials in the secure element.

11

Why Sequent?Sequent is the world’s leading provider of digital issuance and open wallet platform-as-a-service that delivers secure mobile payments and value-added services to banks, mobile operators, merchants and access control providers. With Sequent, customers can offer wallet services open to an ecosystem of partners and developers, while meeting the requirements of highly secure and regulated industries. Sequent products include: Sequent Open Wallet Platform, Digital Issuance and Trust Authority. Sequent is endorsed and used by major customers on four continents.

Sequent Software Inc.www.sequent.com

[email protected]+1 650-419-2713

12