emirati arabi uniti diritto societario - orotech · a cura di: avv. najdatal najjari...

TRANSCRIPT

A cura di:

avv. avv. NajdatNajdat Al Al NajjariNajjari

AAll NNajjariajjari && PPartnersartnersL a w F i r m

EMIRATI ARABI UNITIEMIRATI ARABI UNITI

DIRITTO SOCIETARIODIRITTO SOCIETARIO

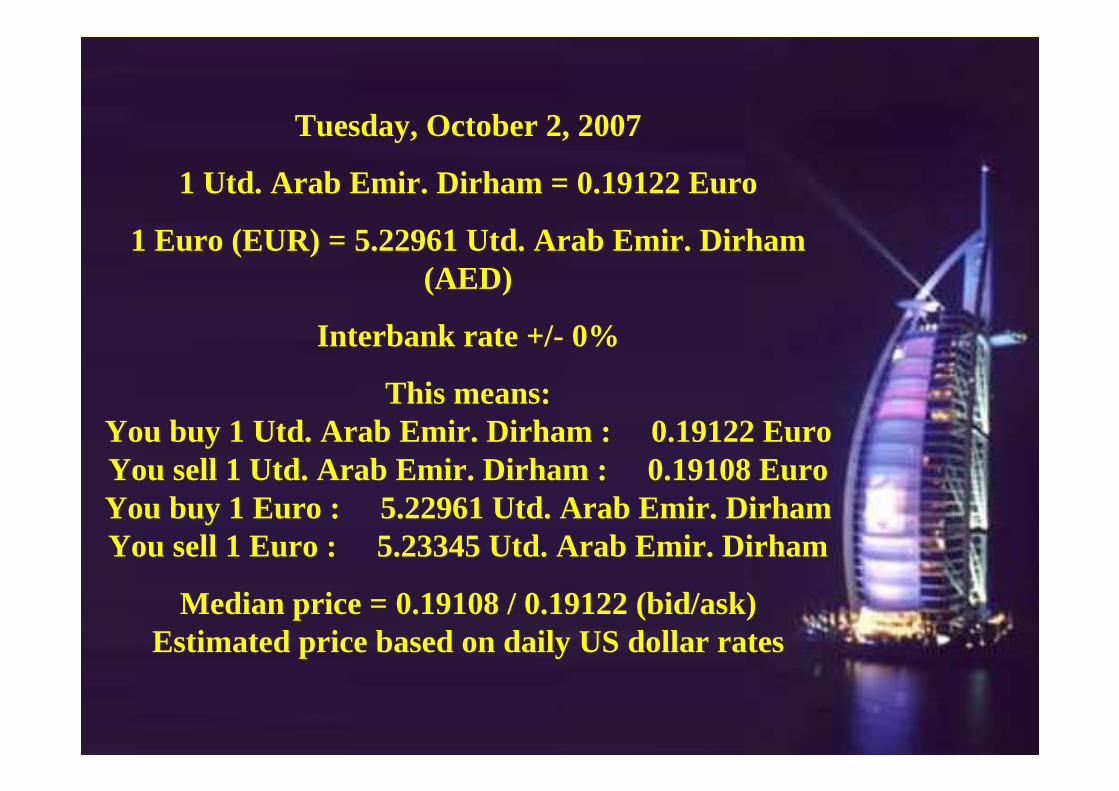

Tuesday, October 2, 2007

1 Utd. Arab Emir. Dirham = 0.19122 Euro

1 Euro (EUR) = 5.22961 Utd. Arab Emir. Dirham(AED)

Interbank rate +/- 0%

This means:You buy 1 Utd. Arab Emir. Dirham : 0.19122 EuroYou sell 1 Utd. Arab Emir. Dirham : 0.19108 EuroYou buy 1 Euro : 5.22961 Utd. Arab Emir. DirhamYou sell 1 Euro : 5.23345 Utd. Arab Emir. Dirham

Median price = 0.19108 / 0.19122 (bid/ask)Estimated price based on daily US dollar rates

Apertura di un business localeSTANDARDIZED COMPANYLegal Form: Limited Liability CompanyMinimum Capital Requirement: 300,000City: Dubai

Procedure 1.

Submit an application and proposed company name to the Department of Economic Development for an initial approval

Time to complete: 1 dayCost to complete: AED 200 for an Arabic name, AED 2,000 for a foreign name + AED 110 for preliminary approval

Comment:

The first step in the registration process is to obtain preliminary approvals from the Licensing Section of the Dubai Department of Economic Development (the "DED") of the classification of the LLC's business activities, trade name, identity of its partners and its capitalization.The application can be made either by a personal visit to the Department Offices or through the Internet, a document clearing service or a legal consultant's office.

Procedure 2.

Draw up the company's Memorandum of Association and have it notarized by a Notary Public in the Dubai courts

Time to complete:

1 dayCost to complete:

0.25% of the capital (for 3 copies of the Memorandum of Association), AED 50 for each page of the additional copy

Comment:

The DED provides a standard MOA. Maximum notary fee is Dhs. 10,000.

Procedure 3.

Deposit the required initial capital in a bank and obtain a bank certificate

Time to complete:

2-3 daysCost to complete:

no charge or bank commission, depends on bank

Comment:

The certificate must provide the following: (i) that the total amount has been deposited by each partner; and (ii) an undertaking from the bank to the effect that the deposited amount will only be released to the managers upon proof of registration of the company.

Procedure 4.

Submit the documents to the DED for approval

Time to complete:

4-6 daysCost to complete:

AED 100

Comment:

The following original documents are to be filed:• The notarized Memorandum; • A signed prescribed application form; and • A bank certificate. The MOA will be scrutinized by the DED to ensure compliance with the Commercial Companies Law as well as with the DED's economic policy and guidelines.

Procedure 5.

Seek approval of use of the premises from the Planning Department of Dubai Municipality

Time to complete:1 day

Cost to complete: no charge

Comment:

The lease for the proposed business premises of the LLC must be approved and the premises must be inspected by the Planning Section of the Dubai Municipality and the Dubai Civil Defense.

Procedure 6.

Make a name board

Time to complete: 2 daysCost to complete: AED 1000

Comment:

Once the Planning Department clearance has been obtained for the office premises, a name board must be prepared both in English and Arabic. The office premises will then be inspected by the fire and civil defense authorities, and by the Licensing Department of the DED.

Procedure 7.

File company documents with the Department for Economic Development (DED) and obtain copies of Trade License and Commercial Registration Certificates

Time to complete:

3 days for commercial registration, 3 days for trade license

Cost to complete:

AED 230+ AED 15,000 license fee for general trading companies and contracting companies + AED 3000 publication fee

Comment:

It is necessary to submit the following original documents to the Commercial Registry at the Trade License and Commercial Registration Department of the DED in order to register the company.(1) The prescribed application form signed by the manager(s) or their legal representative(s);(2) The MOA together with a copy;(3) A certificate issued by the managers(s) and signed by the company's auditor(s); (4) A certificate issued by the bank showing the total amount deposited by each partner and an undertaking from the bank to the effect that the deposited amount will only be released to the managers upon proof of registration of the company ;(5) Letter of approval of the company's name issued by the DED;

(6) The original letter of approval of the company by the Committee of LLCs at the DED; and(7) Letter from the company's auditors stating that they are willing to act as auditors for the company.If officials at the Commercial Registry consider that the documentation is in order, the name of the company will be entered into the Commercial Register and the following documents will be released at no cost to a representative of the company in a sealed envelope within three days from the date the company is entered in the Commercial Register.Before the newly formed company can begin its operations, it must apply to the DED for a trade license. After notarization of the MOA by the Dubai Notary Public, a completed license application is filed with the DED in duplicate. One copy remains with the DED and the other is forwarded by the DED to the Federal Ministry of Economy and Commerce.

Application for a trade license is made on the prescribed form which must be completed in Arabic and signed by the authorized signatory of the company. The following documents should be filed with the application along with the applicable fees:• A prescribed form setting out the proposed name of the company in Arabic and English;• The original lease of the company's office premises; and• The prescribed form for obtaining the Dubai Municipality Building Department's clearance on the suitability of office premises.Licensing fee for general trading companies and contracting companies is AED 15,000. The duration for this procedure is between 2 - 3 days. All business activities fall into three categories of licenses:

(1)Commercial licenses covering all kinds of trading activity;(2)Professional licenses covering professions, services, craftsmen and artisans;(3)Industrial licenses for establishing industrial or manufacturing activity.Upon the conclusion of this procedure the Department of Economic Development issues the original Trade License and Commercial Registration Certificate. Upon presentation of receipts showing payment of the Ministry publication fee and the Chamber of Commerce membership fee, the DED will issue the originals of the trade license and certificate of commercial registration for the LLC.

Procedure 8.

Deliver the copies of the documents to the Federal Ministry of Economic and Commerce; Publish the company documents in the Ministry's Bulletin

Time to complete: 1 day

Cost to complete:

AED 3,000, included in the procedure above

Comment:

The representative of the company deliver the following documents to the Federal Ministry of Economy & Commerce:• Copy of the notarized MOA; • Copy of the certificate of the managers referred to above marked with the number and date of the commercial registration;

• Copy of the certificate issued by the bank and auditors certificate;• Copy of the application for entry of the company's name in the Commercial Register; and• Extract of the entry of the company's name in the Commercial Register. Publication takes several months. However, time frame is of no significance because authorities will act on a copy of the Ministry's receipt which evidences payment of fee for publication. After the publication, the Ministry of Economy and Commerce issues its approval letter.

Procedure 9.

Register with the Dubai Chamber of Commerce and Industry

Time to complete: 2 days

Cost to complete: AED 1,200-3,000 (annual fee), included in the procedure above

Comment:

Membership in the Chamber is mandatory.

Procedure 10.

Register employees with the Dubai Naturalization & Residency Department

Time to complete: 30 days

Cost to complete: AED 700

Comment:

Application must be made at the Dubai Naturalization & Residency Department for the issuance of an Establishment card, this requires the following:. New Establishment form to be filled;. A passport copy of the establishment owner;. A copy of the valid commercial license;. A location map drawing of the establishment;

Procedure 11.

Register employees with the Ministry of Labor

Time to complete:7-14 days

Cost to complete: AED 1,000 per worker, assume 10 workers. Time can take up to 3 months.

Procedure 12*.

Register native workers with the General Authority for Pension and social security

Time to complete: 1 day (simultaneous with previous procedure)

Cost to complete:no charge

Comment: None

INVESTIRE NEGLI E.A.U.

• Gestione pratica delle implicazioni fiscali.

• Cenni sulla Convenzione in vigore con l’Italia

La Convenzione Italia La Convenzione Italia –– U.A.E. U.A.E. contro le Doppie Imposizionicontro le Doppie Imposizioni

• Firmata ad Abu Dhabi in data 22 gennaio 1995, ratificata e resa esecutiva con Legge 28 agosto 1997 n. 309, oggi i vigore

• Redatta su modello O.C.S.E., quindi soggetta ai canoni di interpretazione di quel modello

•• Struttura:Struttura:

I Campo di applicazione

II Definizioni

III Imposizione dei redditi

IV Metodo per eliminare la doppia imposizione

V Disposizioni particolari

VI Disposizioni finali

• La Convenzione si applica alle persone residentiin uno o entrambi gli Stati contraenti.

• Le imposte considerate sono – per quanto riguarda l’Italia – l’I.RE.S e – per quanto riguarda gli Emirati – la locale Imposta sul Reddito delle Persone Giuridiche e l’Imposta sul reddito delle Società, ancorché riscosse tramite il meccanismo della ritenuta alla fonte.

• Essa troverà applicazione anche a future imposte di natura analoga o identica, in aggiunta o in sostituzione a quelle oggi esistenti.

• Essa si applica anche alle plusvalenze.

• La residenza ai fini dell’applicazione della Convenzione è determinata ai sensi delle leggi fiscali di ciascuno Stato è ivi assoggettata ad imposta in virtù della propria residenza, sede di direzione o altro criterio di analoga natura.

• In ipotesi di persone giuridiche residenti in entrambi gli Stati contraenti, si ritiene che esse siano residenti nello Stato ove è collocata la sede della direzione effettiva.

• Collegamento con l’Art. 73 III comma T.U.I.R.

S.O. si o no? (Art. 5)

• Sede di direzione

• Succursale

• Ufficio

• Officina

• Laboratorio

• Miniere o cave

• Cantieri di durata superiore a nove mesi

• Deposito, esposizioni, attività logistica

• Immagazzinamento ai fini di trasformazione da parte di terzi

• Sedi utilizzate per raccolta informazioni o acquisto merci

• Sedi utilizzate per pubblicità, raccolta informazioni, ricerche scientifiche o attività preparatorie o ausiliarie.

S.O. “personale”: si o no?

• Poteri abitualmente esercitati di concludere contratti a nome dell’impresa, salvo il caso del commissionario di solo acquisto

• Presenza tramite commissionario generale o mediatore ovvero di altro intermediario indipendente che agisca nell’ambito della propria ordinaria attività

Norma di esclusione

• Il controllo esercitato da una società di uno Stato contraente rispetto ad un’altra ovvero l’esercizio di attività nell’altro Stato contraente da parte di Società residente in uno Stato contraente non è sufficiente a far considerare le Società come stabile organizzazione l’una dell’altra.

Utili delle imprese – Art. 7

• Imponibilità nello stato di residenza salva la presenza di S.O.

• In presenza di S.O. imputazione pro quota

• Deduzione dei costi di funzionamento della S.O. sostenuti nello Stato della stessa, ed altrove se inerenti al suo funzionamento (es. trasferte)

• Nessun utile può essere attribuito alla S.O. per il solo fatto di avere acquistato merci per l’impresa.

Imprese associate – Regola contro il transfer pricing

(Art. 9) - Condizioni• Un’impresa di

uno Stato partecipa direttamente alla direzione o al controllo di un’impresa dell’altro Stato

• Le stesse persone partecipano direttamente o indirettamente alla direzione, al controllo o al capital di un’impresa di uno Stato contraente e di un’impresa dell’altro Stato contraente

- Regola -

• Le condizioni di scambio tra le imprese devono essere pari a quelle esistenti – a parità di altre condizioni – tra imprese indipendenti.

• In assenza di questa condizione gli utili non realizzati e riconducibili a condizioni di transazione non eque possono essere ripresi a tassazione.

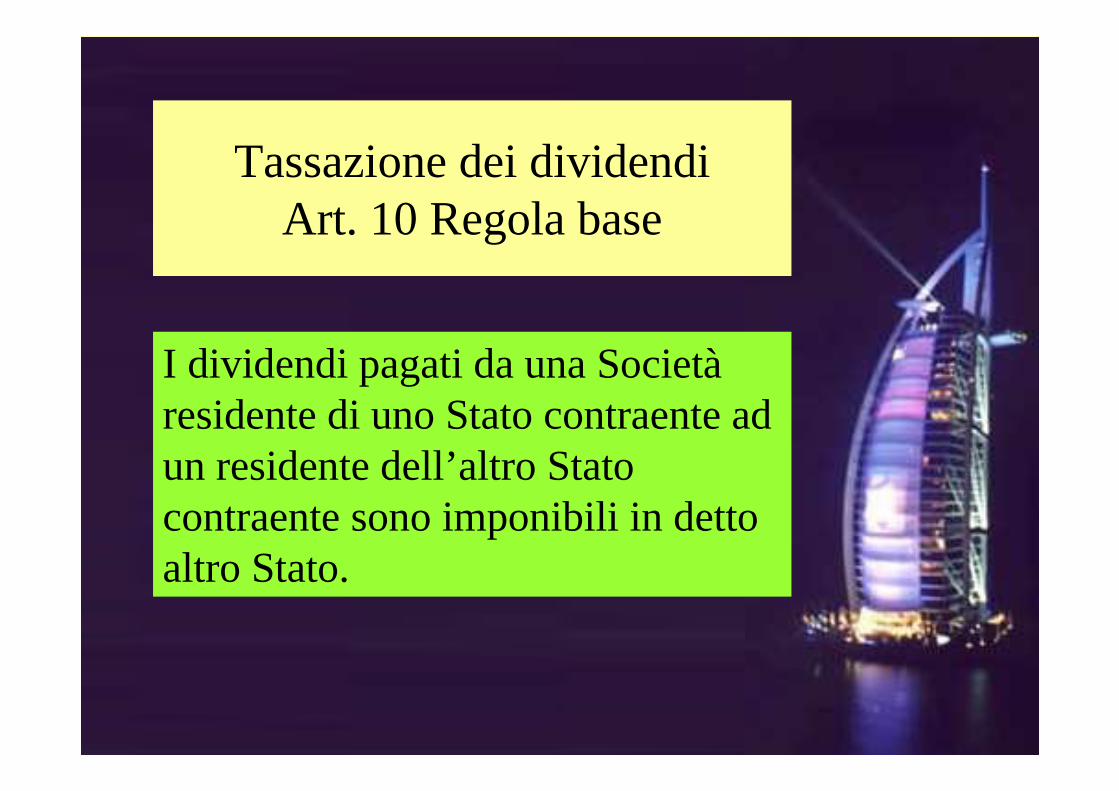

Tassazione dei dividendi Art. 10 Regola base

I dividendi pagati da una Società residente di uno Stato contraente ad un residente dell’altro Stato contraente sono imponibili in detto altro Stato.

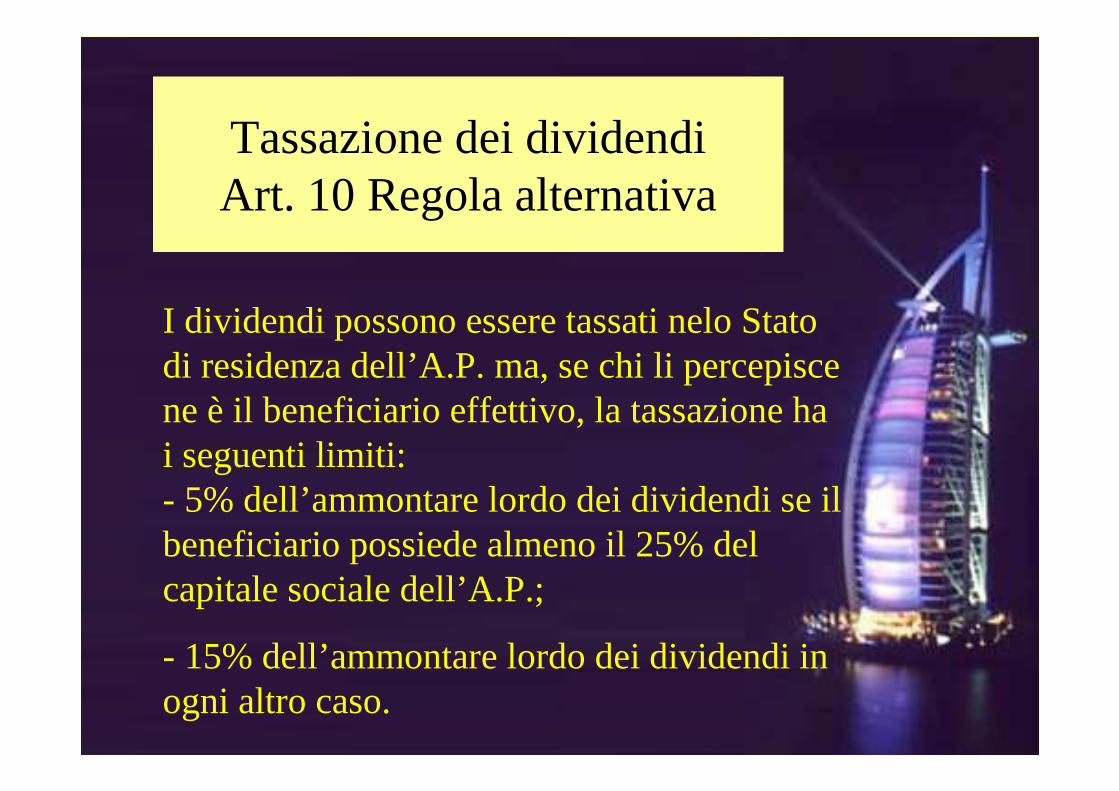

Tassazione dei dividendi Art. 10 Regola alternativa

I dividendi possono essere tassati nelo Stato di residenza dell’A.P. ma, se chi li percepisce ne è il beneficiario effettivo, la tassazione ha i seguenti limiti:- 5% dell’ammontare lordo dei dividendi se il beneficiario possiede almeno il 25% del capitale sociale dell’A.P.;

- 15% dell’ammontare lordo dei dividendi in ogni altro caso.

Tassazione dei dividendi Art. 10 Esclusione

La regola alternativa non trova applicazione nel caso in cui il beneficiario – residente nell’altro Stato contraente – eserciti nello Stato dell’A.P. attività tramite S.O. ivi situata e la partecipazione generatrice dei dividendi si ricolleghi direttamente ad esse. In tal caso i dividendi sono imponibili nello Stato dell’A.P.

Tassazione degli interessi Art. 11

• Gli interessi sono imponibili nello Stato del precettore che ne sia l’effettivo beneficiario;

• Gli interessi si considerano pagati da uno Stato contraente se ivi ha sede l’A.P.

• Si applica la medesima restrizione prevista per i dividendi qualora il beneficiario eserciti tramite S.O., nello Stato di residenza dell’A.P., attività riconducibili al pagamento degli interessi di cui si tratta.

Tassazione dei canoni Art. 12

• La tassazione dei canoni avviene nello Stato di residenza dell’effettivo beneficiario.

• Possono essere tassati nello Stato di residenza dell’A.P. ma e la persona che li percepisce ne è il beneficiario effettivo l’imposta applicata sarà pari sino al 10% dell’ammontare lordo dei canoni stessi.

• Se il beneficiario effettivo svolge nello Stato dell’A.P. un’attività tramite S.O. riconducibile al diritto o al bene generatore dei canoni, gli stessi divengono imponibili all’interno dello Stato stesso.

Lavoro subordinato Art. 15

• La regola generale è l’imposizione nel Paese di residenza, salvo che il lavoro venga prestato nell’altro Stato contraente;

• In questo caso può essere tassato nello Stato di residenza a condizione che:- la permanenza sia inferiore a 183 giorni in ogni 12 mesi;- lo stipendio sia pagato da un datore di lavoro non residente nell’altro Stato;

• - la remunerazione non è sostenuta da S.O. che il datore di lavoro ha nell’altro Stato.

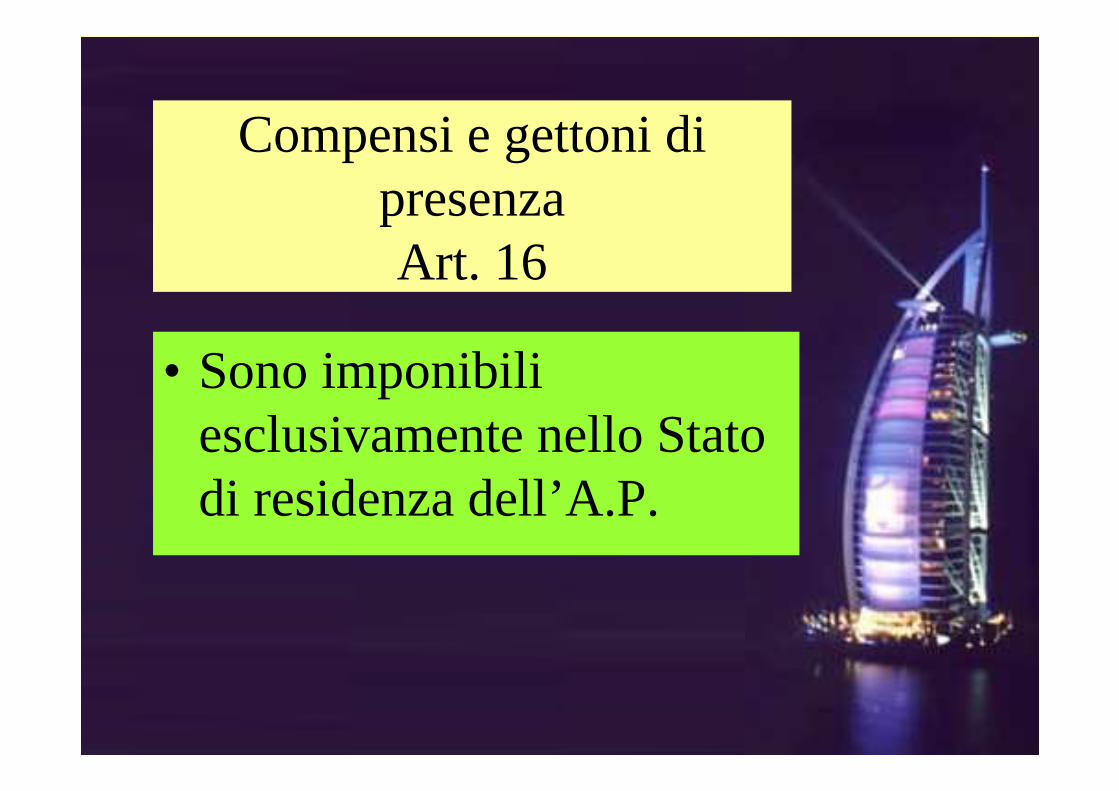

Compensi e gettoni di presenza Art. 16

• Sono imponibili esclusivamente nello Stato di residenza dell’A.P.

Metodo per eliminare la doppia imposizione

Art. 23• Calcolo del reddito complessivo con inclusione

del reddito prodotto in E.A.U.• Deduzione dalle imposte calcolate sul suddetto

reddito delle imposte pagate negli E.A.U. sino al raggiungimento della quota di imposta italiana attribuibile ai predetti elementi di reddito nella proporzione in cui gli stessi concorrono alla formazione del reddito complessivo.

• La detrazione non sarà concessa ove l’elemento di reddito sia assoggettato a tassazione in Italia su richiesta del beneficiario.