eex at montel nordic energy days 2016

TRANSCRIPT

Copyright 2015 – All rights reserved

The future of financial power trading in a low-

price market - Impact from EU-regulation

Heine Rønningen, Nordic KAM Power & Environmental Markets

European Energy Exchange

Copyright 2014 – All rights reserved

How to make the Nordic market great again?

- It is not about building a Trump style brick wall to stop central European energy flows

- It is not about a Nordic exit from IEM – Nordic Exit = NoExit, so we better stay…

- It is not about how to escape regulations – adapting is an easier pathway

- It is all about increasing liquidity by serving the needs of hedgers and traders:

Page 2

Todays topic rephrased:

Source: Nasdaq OMX

Copyright 2015 – All rights reserved

Nordic market – strong trends and lot of

potential

Page 3

Nordic market needs fresh blood – new participants and instruments to attract them

Total range 2006 - 2016 = 135 €

Range 2009-11 = 55 €

Range YtD =15 €

1. Position Quarter gap adjusted

1. Position Quarter actual price

Range 2015 = 20 €

Copyright 2015 – All rights reserved

Nordic market – structural reasons for the

unattractiveness

Page 4

Why:

- Financial players have lost their interest in the Nordic market due to non-compliant

Instruments and clearing.

- Instruments:

- DS Futures makes no sense when backed by cash

- DS Futures is not attractive to financial players due to locked in profits

- Harmonized Future structure would attract financial players, make spread

trading and exchange competition easier…..

- Clearing:

- Direct membership and non-rated members puts clearing solidity in doubt

- Direct membership is capital intensive for multi exchange participants

- Direct membership induces less competition, higher cost, reduced liquidity…….

Great potential = record low volume (15-year low) ? ? ? ?

Copyright 2014 – All rights reserved Page 5

How to make the Nordic market great again?

Hope is not a strategy - to make something change we need focused action:

Accept the things I cannot change:

- Do not waste time on: G20, ESMA & ACER on the broader accepted regulatory issues….

Change the things I can:

- Focus on:

- Measures to improve liquidity and overall market efficiency – compliant with the regulatory

framework:

- Expanding the total market by facilitating competition

- Product harmonization & development

Grant me the serenity to accept the things I cannot change...

The courage to change the things I can...

&

The wisdom to know the difference...

-based on the Serenity Prayer

Copyright 2014 – All rights reserved Page 6

How to make the Nordic market great again?

The structural reasons for the market unattractiveness

can be sorted out in two simple steps:

Exchange competition in Futures-, Day Ahead- and Intra

Day Markets:

- EPEX Spot: Will launch Nordic Bidding Zone products in

2017

- EEX Nordic Power Futures: Launched already

Product development:

- A solid liquidity base in Baseload Futures & Vanilla

Options

- + Extensions:

- non-MTF (tool for physical delivery)

- Cap Futures (tool for capacity hedging & trading)

- Bidding Zone risk mitigation tools

Copyright 2014 – All rights reserved Page 7

Exchange competition in DAM & IDM:

What:

- EPEX Spot:

- The preferred European spot exchange (566 TWh in 2015)

- Part of EEX Group

- Cleared by ECC (European Commodity Clearing)

- Launch of Nordic Bidding Zone Day Ahead & Intra Day products in 2017

Why:

- Competition is good for pricing and product development

- CACM regulation results in orderbook consolidation and a single price

- EMIR compliant clearing of DAM & IDM opens for:

- Futures, DAM, IDM cross clearing

- Physical delivery of longer term positions (Non-MTF)

- IDM index for hedging and trading capacity (Cap Future)

Copyright 2014 – All rights reserved Page 8

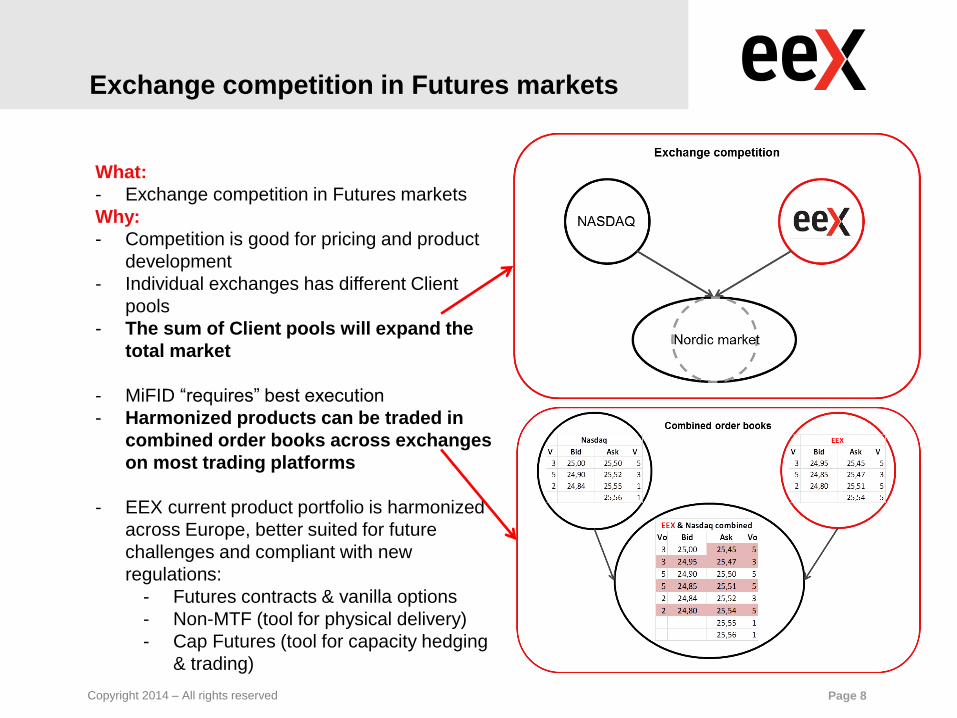

Exchange competition in Futures markets

What:

- Exchange competition in Futures markets

Why:

- Competition is good for pricing and product

development

- Individual exchanges has different Client

pools

- The sum of Client pools will expand the

total market

- MiFID “requires” best execution

- Harmonized products can be traded in

combined order books across exchanges

on most trading platforms

- EEX current product portfolio is harmonized

across Europe, better suited for future

challenges and compliant with new

regulations:

- Futures contracts & vanilla options

- Non-MTF (tool for physical delivery)

- Cap Futures (tool for capacity hedging

& trading)

Copyright 2014 – All rights reserved Page 9

Product development

Non-MTF (contract with physical delivery) :

What:

- Non-MTF is a Physical contract regulated by REMIT (not MiFID)

- EEX Link provides a “slewing service” and ensures same spreads in the two contracts

- Currently introduced on Phelix & French power & gas

Why:

- Makes the Clients free to trade contracts regulated by the regime of choice (MiFID or REMIT)

Prerequisite:

- EPEX Spot in the Nordics (2017)

A full presentation on Non - MTF enclosed

EEX financial futures (MiFID regulated) EEX physical Non-MTF (REMIT regulated)

EEX Link GmbH mirrors best bid - ask between the books to avoid liquidity splitting

Copyright 2014 – All rights reserved Page 10

Product development

Cap Future (capacity hedging & trading):

What:

- Average option

- Intraday Market as underlying

- The Call option structure caps the marked

- Could also be implemented as Put options

(as a floor)

Why:

- Capacity hedging and trading product

- Suitable for:

- Forecast error hedging:

- Intermittent renewable generation

- Retail load hedging

- Revealing the value of capacity:

- Flexible and controllable generation

- Demand response

- Trading

Prerequisite:

- EPEX Spot in the Nordics (2017)

A full presentation on Phelix Cap Futures enclosed

60 € Cap

60 € Cap

Copyright 2014 – All rights reserved Page 11

Product development

Bidding Zone risk mitigation:

What:

- Regulation on Forward Capacity allocation (FCA) is soon to

enter into force…

- Hedging opportunities in some Nordic bidding Zones are rather

poor (e.g. SE4, NO3, NO5)

- 12 Nordic Bidding Zones with a sufficient market efficiency are

deemed to be unsuccessful (we have tried for 20 years…)

How:

- The short term quick fix would be to introduce Volume Weighted

Average Price Indexes consisting of correlated Bidding Zones

Prerequisite:

- A commitment from the TSOs to keep some of the borders fixed

(in addition to national borders).

- TSO will face the same degree of freedom to change Bidding

Zones. No reality change from current solution.

Why:

- If you do not fix it - the regulators will fix it for you…by

introducing non firm Long Term Transmission Rights…..be

careful what you wish for…

A full proposal on Bidding Zone risk mitigation structure enclosed

Copyright 2014 – All rights reserved Page 12

How to make the Nordic market great again?

Nord Pool Spot & Forward heydays are gone (3100 TWh in

2002).

The situation will not change unless we change something:

We cannot blame it on:

- Regulations

- Financial crisis (it is 8 years ago)

It is due time to change the things we can change:

- Last decades products and exchange structure was

great…last decade

My best advice:

- Expand the total market and its client pool by introducing

competition

- Encourage product development of attractive trading and risk

mitigation tools – both fit for purpose & compliant with the

regulatory regime.

- Remember: DS Futures makes no sense when backed by

cash

- A full conversion from DS Futures to Futures is the

single most important first step to attract liquidity…

Copyright 2014 – All rights reserved

Thank you for your attention.

Heine Rønningen

Key Account Manager, Sales Power & Environmental Markets - Nordics

P: +47 90 60 87 74 | E: [email protected] | Eikon ID: