economic outlookeconomic outlook · sector while local government debt and shadow bank lending are...

TRANSCRIPT

Economic OutlookEconomic Outlook

The Birmingham Estate PlanningThe Birmingham Estate Planning Council

Nathaniel KarpChi f U S E i tChief U.S. EconomistBBVA Research

Birmingham, AL February 7, 2013

US Economic Outlook

Global Outlook

Global GDP growth (%)

We expect global growth to pick up in 2013

g ( )Source: BBVA ResearchGlobal growth will recover

supported by policy makers:

• A three speed world still 2 8

5,13,9

3,2 3,54

5

6

• A three speed world, still dependent on stimulus policies

• Solid growth in emerging markets,

2,8,

1

2

3

4

Solid growth in emerging markets, slow recovery in the US, weakness in Europe -0,6

-2

-1

0

A tail-risk scenario is less likely

• Important challenges remain: fi l t it li t i t

2008 2009 2010 2011 2012 (f) 2013 (f)

Advanced economies Emerging economies

2

fiscal austerity, policy uncertainty, reform fatigue & geopolitical risks

Baseline

US Economic Outlook

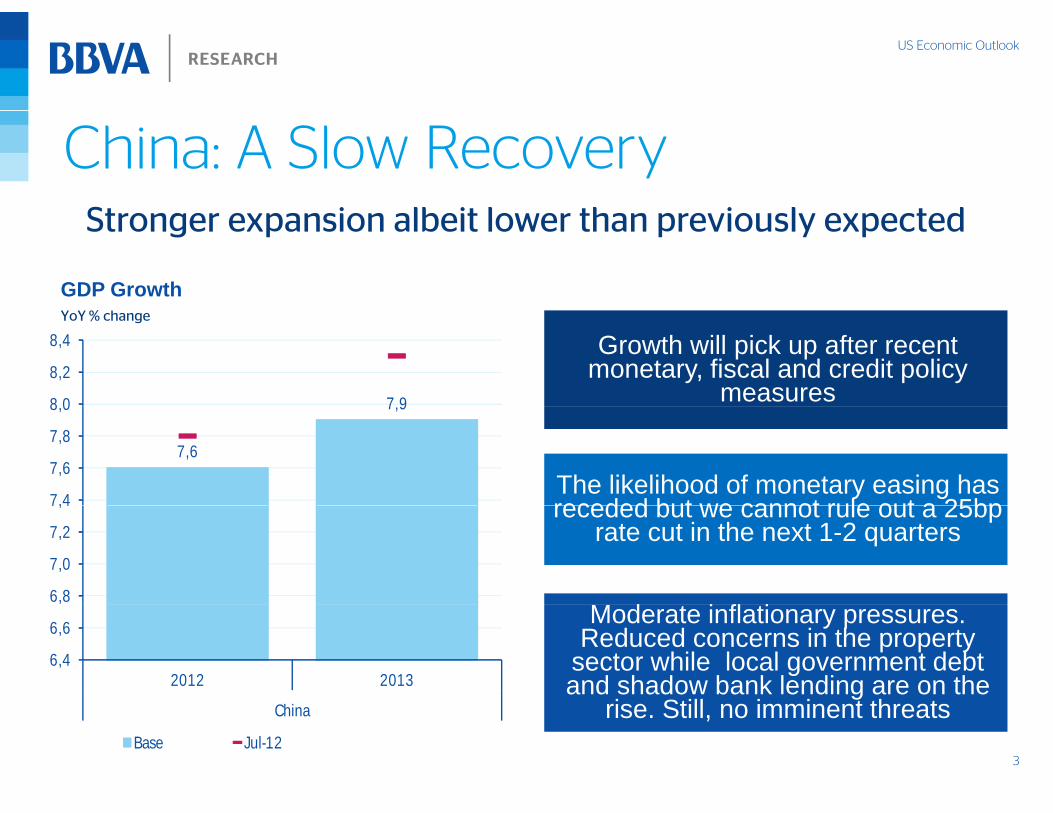

China: A Slow RecoverySt i lb it l th i l t d

GDP Growth

Stronger expansion albeit lower than previously expected

Growth will pick up after recent monetary, fiscal and credit policy

measures

YoY % change

7 98 0

8,2

8,4

The likelihood of monetary easing has receded but we cannot rule out a 25bp

7,6

7,9

7,4

7,6

7,8

8,0

receded but we cannot rule out a 25bp rate cut in the next 1-2 quarters

f6,8

7,0

7,2

7,4

Moderate inflationary pressures.Reduced concerns in the property

sector while local government debt and shadow bank lending are on the

i Still i i t th t

6,4

6,6

2012 2013

3

rise. Still, no imminent threatsChina

Base Jul-12

US Economic Outlook

LATAM: Solid performanceR b t i tl k f t t i St th

GDP Growth

Robust economic outlook for most countries. Stronger than expected data in Brazil and upside risks in Mexico

Stronger-than-expected data signaling solid domestic demand growth

GDP GrowthYoY % change

10

12

Policymakers will respond differently to FX appreciation pressures and

4

6

8

to FX appreciation pressures and higher inflation

‐2

0

2

Solid fundamentals help the region to withstand potential negative shocks

‐8

‐6

‐4 Contribución de la demanda interna

Contribución de la demanda externa

Crecimiento del PIB

Domestic demandExternal demandGDP Growth

4

T1 T2 T3 T4 T1 T2 T3 T4 T1 T2 T3 T4 T1 T2 T3 T4 T1 T2 T3 T4

2009 2010 2011 2012 2013

Source: BBVA Research & Haver

US Economic Outlook

Europe: Lower risk but high uncertaintyRi k ti h d li d i ifi tl idi t t th

EMU: PMI and Leading IndicatorsBBVA European Financial Stress

Risk perception has declined significantly, providing support to the recovery process. However, economic fundamentals remain weak

EMU: PMI and Leading IndicatorsIndex

BBVA European Financial StressIndex

2 0

2.560102

EMU

1.0

1.5

2.0

50

55

99

100

101

-0.5

0.0

0.5

40

45

96

97

98

-1.5

-1.0

07

08

09 10 11 12 13

30

35

94

95

ene-

08

may

-08

sep-

08

ene-

09

may

-09

sep-

09

ene-

10

may

-10

sep-

10

ene-

11

may

-11

sep-

11

ene-

12

may

-12

sep-

12

ene-

13

5

Jan

0

Jan

0

Jan

0

Jan

1

Jan

Jan

1

Jan

e m s e m s e m s e m s e m s e

Lead_EMU (left) PMI_EMU

Source: BBVA Research & Haver

US Economic Outlook

Europe: Financial fragmentationR d i fi i l i j h fi T kli kReducing financial stress is just the first step. Tackling market

fragmentation will allow to rebalance risks and eliminate uncertainty

Change in Interest Rate on New Bank Loans(In basis points, December 2010 to July 2012)Source: ECB, IMF and BBVA Research

Banking imbalances : capital injections and market opennessSource: BBVA Reaerch based on European Commissionand ECB

SP

IT

PT 80

100

120

140

H

IE (43%)

CY11%

13%

15%

GDP)

FR

SP

CYIRE

0

20

40

60

Households loanBE

LU

EL

CY

7%

9%tal Injection

(%G

NTH

GER

FIAU

BE

-60

-40

-20

-80

-60

-40

-20 0 20 40 60 80 00

sES

DE

IT

PT

FI

NL

BE

FR

AU

SK MTSI1%

3%

5%

Public Capit

6

- - - - 1

Corporate loans

FISK MT

‐1%‐80% ‐60% ‐40% ‐20% 0% 20% 40% 60%

Target Position (%GDP)

US Economic Outlook

Europe: A road map

Measures adopted Measures adopted • Fiscal rule (fiscal compact)• Surveillance of all imbalances (European Semester)• Permanent rescue fund (ESM)• ECB: a credible and effective backstop (OMT)

• Road map to a European banking supervisionShort run: credibility and Short run: credibility and

• Periphery countries: deleveraging and reforms

Road map to a European banking supervisionyimbalances

yimbalances

Periphery countries: deleveraging and reforms• European level solutions: implementation of banking

union with a common supervision, direct bank recapitalization & line of credit (ESM)

Medium term: further integration and agreement between core & periphery

Medium term: further integration and agreement between core & periphery

• Complete banking union: single resolution mechanism and deposit guarantee

The final stage:A stable monetary and

i i

The final stage:A stable monetary and

i i

7

• Fiscal union: sovereign debt mutualization & Treasury economic unioneconomic union

US Economic Outlook

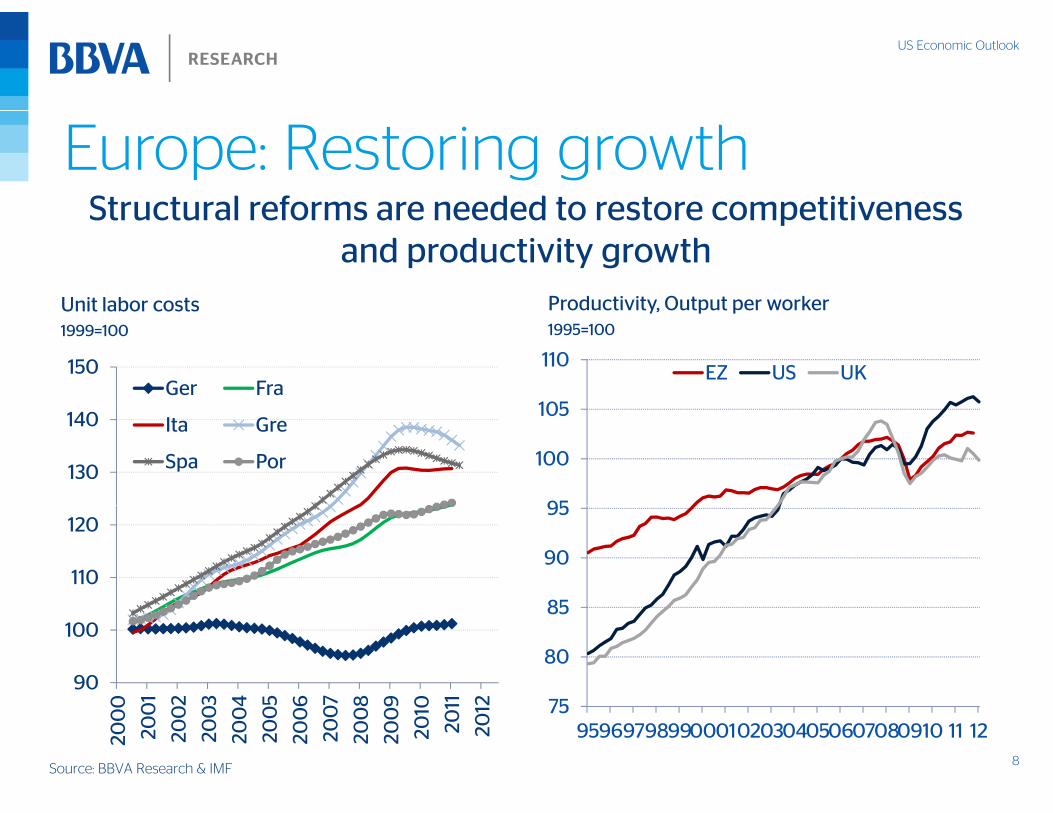

Europe: Restoring growthStructural reforms are needed to restore competitiveness

Productivity, Output per workerUnit labor costs

Structural reforms are needed to restore competitiveness and productivity growth

150Ger Fra

105

110EZ US UK

Productivity, Output per worker1995=100

Unit labor costs1999=100

130

140 Ita Gre

Spa Por

95

100

105

110

120

85

90

95

90

100

0 1 2 3 4 5 6 7 8 9 0 1 2 75

80

85

8

200

0

200

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

2010

201

2012 75

95969798990001020304050607080910 11 12

Source: BBVA Research & IMF

US Economic Outlook

Europe: Structural reforms•Fiscal stability •Wage and labor cost flexibility•Fiscal stability

•Enhance technological change

•Working-time flexibility

•Flexible retirement

•Wage and labor cost flexibility

•Reform security provisions

•Increase skills

•Reform benefit system

Employment Protection, 2008

•Flexible retirement

•Nurture Entrepreneurship

•Reform benefit system

•Align incentives

3 0

3.5Protection of permanent workers against dismissal Requirements for collective dismissal Regulation on temporary employment

Employment Protection, 2008Scale from 0 (least restrictions) to 6 (most restrictions)

1.5

2.0

2.5

3.0

0.0

0.5

1.0

ey ux co in sia ce ce g

al na

nia ay ny

dia m aly

nd

ria

nia ep nd zil

ds

ep ea nd ry en ile rk ael

ed nd an nd lia ca nd

UK da

US

9

Turk

eLu

Mex

icSp

aIn

do

nes

Fran

cG

reec

Po

rtu

gC

hin

Slov

enN

orw

aG

erm

anIn

dB

elg

iu Ita

Po

lan

Au

str

Est

on

Cze

ch R

eFi

nla

nB

raz

Net

her

lan

dSl

ovak

Re

Ko

reIc

elan

Hu

ng

aSw

ede

Ch

iD

enm

aIs

r aR

uss

ian

Fe

Swit

zerl

anJa

pa

Irel

anA

ust

ral

Sou

th A

fric

N Z

eala

n UC

anad U

Source: IMF, OECD & BBVA Research

US Economic Outlook

Political challengesS d d i l d liti l

Socio-economic democracy: EurozoneSocio-economic democracy: U S

Success depends on social and political consensus

0 7

0.8

Other Core0 7

0.8

G F

Socio-economic democracy: Eurozone%

Socio-economic democracy: U.S.%

0.5

0.6

0.7

are 0.5

0.6

0.7

are

Ger+Fra

Periphery

0 2

0.3

0.4

GD

P S

ha

Bubble: Population shareCA+TX

0 2

0.3

0.4

GD

P S

ha

B bbl P l

Periphery

Other Core

0

0.1

0.2

0 0 1 0 2 0 3 0 4 0 5 0 6 0 7 0 8

Periphery

0

0.1

0.2

0 0 1 0 2 0 3 0 4 0 5 0 6 0 7 0 8

Bubble: Population share

10

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8Political Share

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8Political Share

Source: BBVA Research & Haver

Other Core: NY, FL, IL, PA & NJ, Other Core: Neth, Fin, Aus, Bel, Lux

US Economic Outlook

Long-term Global Outlook

Businesses must prepare to changing global dynamics

Percentage of urban population and agglomerations by size classSource: UN Urbanization Prospects, 2011 revision

2011 2025

11

US Economic Outlook

Long-term Global Outlook

C i P i Chi (2000 2020) US Exports as a share of GDP and

Abundant opportunities for US businesses

Consumption Patterns in China (2000-2020)(% of total urban household spending)Source: Mckinsey

16.0160% of NRI % of GDP (rhs)

US Exports as a share of GDP and Nonresidential Investment; 1930-2012

10 0

12.0

14.0

100

120

140% of NRI % of GDP (rhs)

6.0

8.0

10.0

60

80

100

2.0

4.0

20

40

12

0.0030 40 50 60 70 80 90 00 10

US Economic Outlook

US Economic Activity“Th f i ' h i d b ”

U.S. Real GDP per working age populationU.S. Real GDP Growth

“The future ain't what it used to be” (Y. Berra)

Log GDP/Pop 16-65yrsYoY % change

6.011.2

2.0

4.0

10.8

11.0

-2.0

0.0

10.4

10.6

-6.0

-4.0

100

10.2

13

6.093 95 97 99 01 03 05 07 09 11

10.050 60 70 80 90 00 10

Source: BBVA Research & Haver

US Economic Outlook

Economic ActivityD it th h l d i 4Q12 t i di t

BBVAUS Weekly Activity IndexBBVA US MAI

Despite the sharp slowdown in 4Q12, recent indicators suggest stronger growth ahead

BBVAUS Weekly Activity Index3m % change

BBVA US MAILast vs. previous 3M average

H i

Prices

10

15

Confidence

Spending

Banking

Housing

0

5

10

Financial

Composite

Foreign Trade

Confidence

-5

0

Employment

Production

CRE

Financial

-15

-10

14

-2.0 -1.0 0.0 1.0 2.0 3.0

p y-20

2008 2009 2010 2011 2012 2013

Source: BBVA Research & Haver

US Economic Outlook

HouseholdsHousehold Debt Flows

1000

1500Mortgages Consumer+Other*

US$bn, SAARA painful deleverage process was needed to support sustained consumption

-500

0

500

Debt Service RatioD b d fi i l bli i di bl i

sustained consumption growth

-1000

500

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

Liabilities / Disposable Personal Income18

19

20Financial Obligations Ratio Debt Service Ratio

Debt and financial obligations to disposable income

1.2

1.4

Actual

Liabilities / Disposable Personal IncomeHousehold sector, ratio

15

16

17

0.8

1.0

Trend before12

13

14

150.6

90 92 94 96 98 00 02 04 06 08 10 12

Trend beforeboom

10

11

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12Source: BBVA Research & Haver

US Economic Outlook

Business SectorA h lth t b i t t d d t t k th

NRI and capital pending planC t fit

A healthy corporate business sector stands ready to take the lead if expectations edge up

NRI and capital spending plansUS$bn and net index

Corporate profits% of GDP

13

14120040

CEO Confidence

Equipment & Software (rhs)

11

12

13

1050

1100

1150

10

20

30Equipment & Software (rhs)

9

10

900

950

1000

‐10

0

10

7

8

800

850

‐30

‐20

06 06 07 07 08 08 09 09 10 10 11 11 12 12

16

600 01 02 03 04 05 06 07 08 09 10 11 12 13

Source: Haver & BBVA Research

Mar

Sep

Mar

Sep

Mar

Sep

Mar

Sep

Mar

Sep

Mar

Sep

Mar

Sep

US Economic Outlook

Business SectorH ll fi f h ll i b i

Mo t Impo tant P oblemS ll B i O ti i

However, smaller firms face a more challenging business environment

Most Important Problem:% sha of responsesre

Small Business OptimismIndex

15

20Good time to expand

Taxes

5

10

15Increase Employment

Other

Sales

Regulation

-5

0

Labor Quality

Competition

Insurance

-15

-10

07

07

07

08

08

08

09

09

09 10 10 10 n

11 y 11

p 11 12 12 12 Interest rates

Labor cost

Inflation

17Source: Haver & BBVA Research

Jan

0M

ay 0

Sep

0Ja

n 0

May

0Se

p 0

Jan

0M

ay 0

Sep

0Ja

n

May

Se

p

Jan

May

Sep

Jan

M

ay

Sep

0 10 20 30

US Economic Outlook

Residential ActivityA i i iti t ib ti f th d i

Home PricesHousing Starts and Home Sales

An increasing positive contribution from the enduring housing recovery

o e cesIndex

Housing Starts and Home SalesThousands

8000

90002500

200

220

Distressed Sales

5000

6000

7000

1500

2000

180

200 Distressed Sales

Ex. Distressed Sales

2000

3000

4000

500

1000

S

140

160

0

1000

2000

0

500

03

04

05

06 07

08

09 10 11 12

Housing StartsHome sales (rhs)

100

1200

7

08

09 0 11 12

18Source: BBVA Research & Haver Source: BBVA Research, CoreLogic, Haver

Jan

0

Jan

0

Jan

0

Jan

0

Jan

0

Jan

0

Jan

0

Jan

1

Jan

Jan

Jan

0

Jan

0

Jan

0

Jan

1

Jan

1

Jan

1

US Economic Outlook

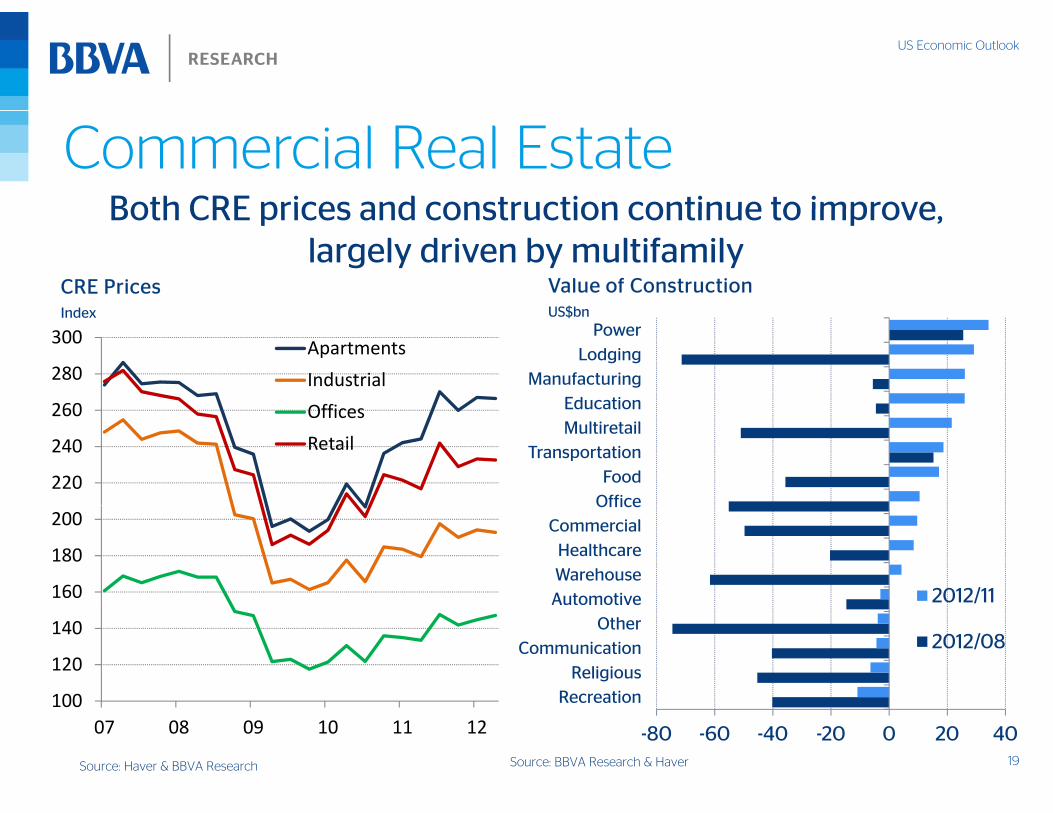

Commercial Real EstateBoth CRE prices and construction continue to improve

Value of ConstructionUS$b

CRE PricesI d

Both CRE prices and construction continue to improve, largely driven by multifamily

US$bnIndex

260

280

300 Apartments

Industrial

Offi Education

ManufacturingLodging

Power

220

240

260 Offices

Retail

Office

Food

TransportationMultiretail

Education

160

180

200

AutomotiveWarehouse

Healthcare

CommercialOffice

2012/11

100

120

140

RecreationReligious

Communication

Other

Automotive

2012/08

19Source: BBVA Research & HaverSource: Haver & BBVA Research

10007 08 09 10 11 12 -80 -60 -40 -20 0 20 40

ec eat o

US Economic Outlook

Labor MarketsL b k t k tit t j h d i dLabor market weakness constitutes a major headwind

N f P i t P llNonfarm payrollYoY % change

Nonfarm Private PayrollT= start of the recession

120

1973 741

16

110

1151973-74

1981-821

1

1

2

4

100

1051990-91

1981 82

0

0

1

1

-2

0

90

95

2007-12

2001-02

0

0

0

6

-41954-86: 2.1%

1987-01: 1.9%

2002-12: 0.1%

20Source: BLS & BBVA Research

90T 4 8 12 16 20 24

0-654 58 62 66 71 75 79 83 88 92 96 00 05 09

US Economic Outlook

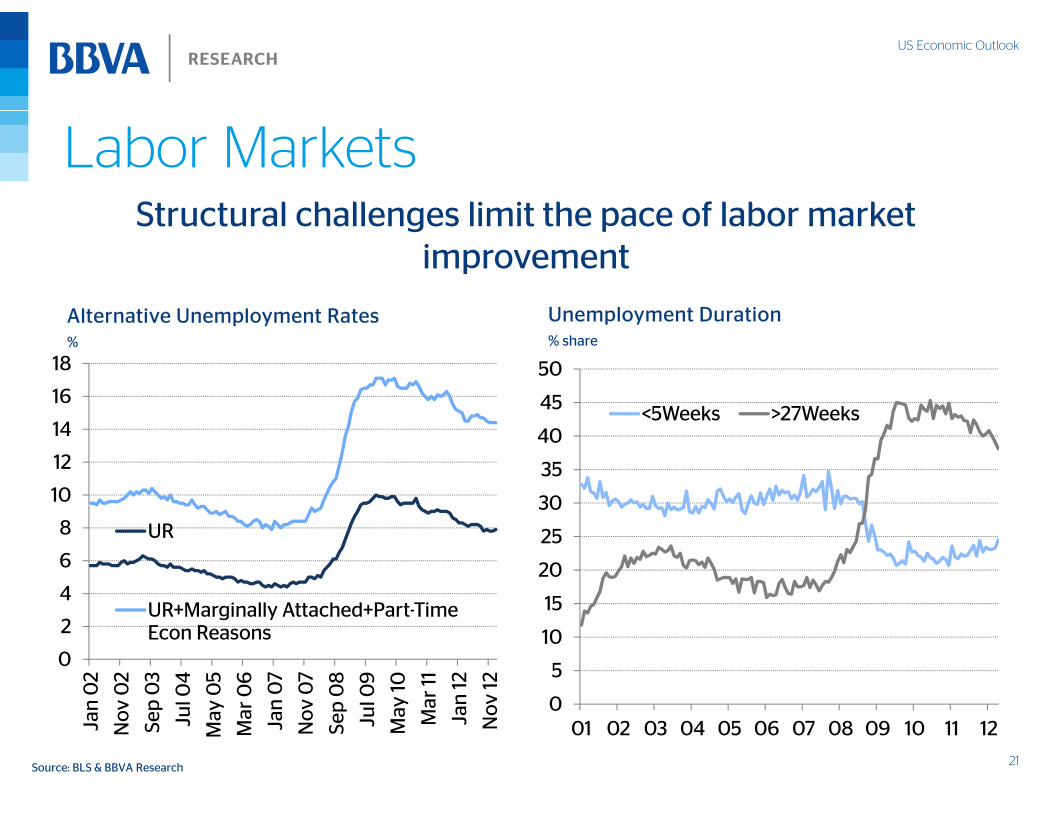

Labor MarketsStructural challenges limit the pace of labor marketStructural challenges limit the pace of labor market

improvement

U l t D tiAlternative Unemployment Rates%

Unemployment Duration% share

16

18

45

50

5W k 27W k

10

12

14

30

35

40

45 <5Weeks >27Weeks

4

6

8 UR

UR M i ll Att h d P t Ti 15

20

25

30

0

2

n 0

2

v 0

2

p 0

3

l 04

y 0

5

r 0

6

n 0

7

v 0

7

p 0

8

l 09

y 10

ar 11

n 12 v 12

UR+Marginally Attached+Part-Time Econ Reasons

0

5

10

15

21Source: BLS & BBVA Research

Jan

Nov Se

p

Jul

May

Mar Ja

n

Nov

Sep

Jul

May M

a

Jan

Nov 0

01 02 03 04 05 06 07 08 09 10 11 12

US Economic Outlook

Banking SectorA h lth b ki t i d d t t

Bank Profitability and CapitalDelinquency rates

A healthy banking sector is needed to support a private-led recovery

Bank Profitability and Capital%

Delinquency rates% of total loans

2.09.5Core CapitalROA (rhs)16

18Real estate

0 5

1.0

1.5

8 5

9.0ROA (rhs)

12

141-4 family

Construction

C&I

0 5

0.0

0.5

8.0

8.5

6

8

10 Credit cards

Other consumer

-1 5

-1.0

-0.5

70

7.5

0

2

4

22

1.57.004 05 06 07 08 09 10 11 12

007 08 09 10 11 12

Source: BBVA Research & Haver

US Economic Outlook

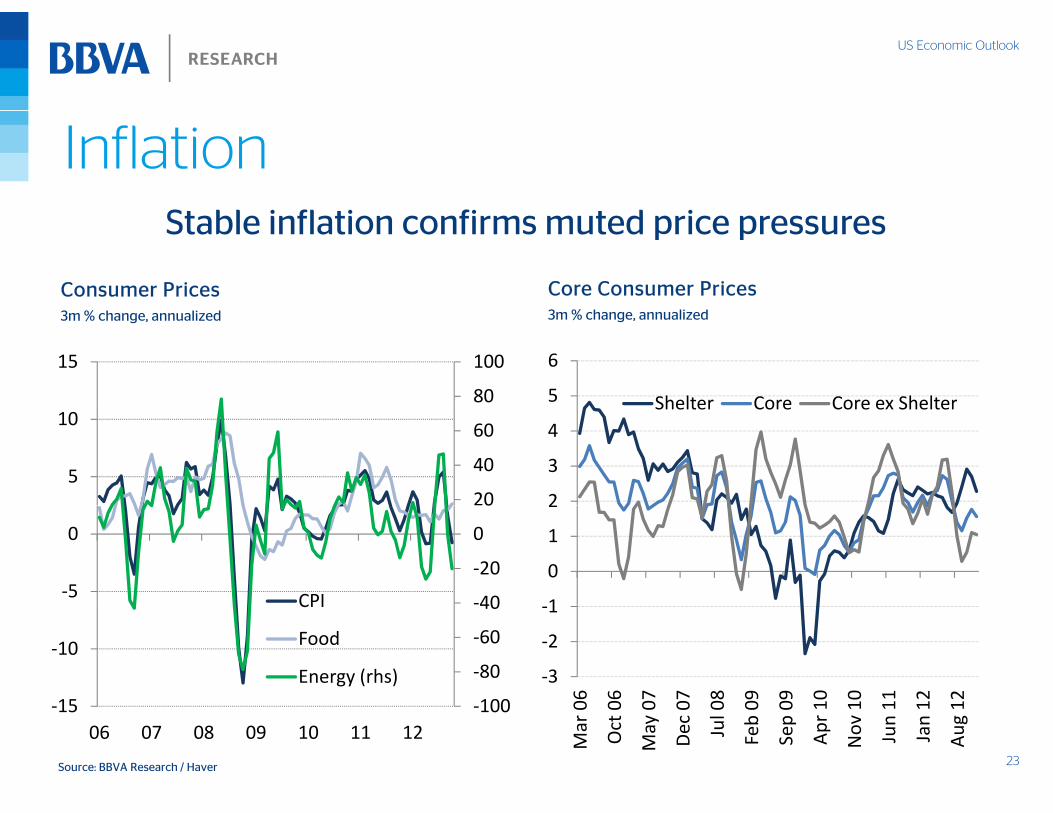

Inflation

Core Consumer PricesConsumer Prices

Stable inflation confirms muted price pressures

3m % change, annualized3m % change, annualized

5

6

Shelter Core Core ex Shelter80

10015

2

3

4Shelter Core Core ex Shelter

20

40

60

5

10

1

0

1

2

‐40

‐20

0

0

‐5

0

CPI

‐3

‐2

‐106 06 07 07 08 09 09 10 10 11 12 12100

‐80

‐60

‐40

15

‐10

CPI

Food

Energy (rhs)

23Source: BBVA Research / Haver

Mar 0

Oct 0

May 0

Dec 0

Jul 0

Feb 0

Sep 0

Apr 1

Nov

1

Jun 1

Jan 1

Aug

1‐100‐1506 07 08 09 10 11 12

US Economic Outlook

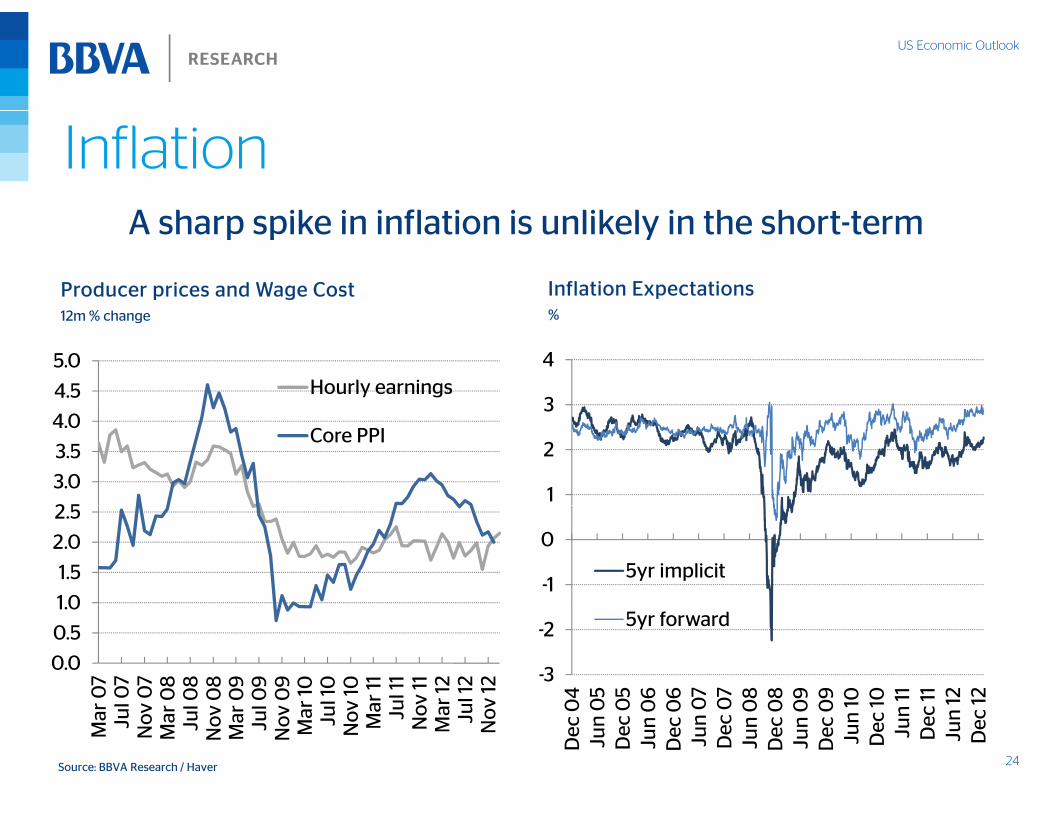

Inflation

Inflation ExpectationsProducer prices and Wage Cost

A sharp spike in inflation is unlikely in the short-term

%12m % change

3

4

4.5

5.0Hourly earnings

1

2

3

2 5

3.0

3.5

4.0Core PPI

-1

0

5yr implicit

1 0

1.5

2.0

2.5

-3

-2

04

05

05

06

06 07

07

08

08

09

09 10 10 11 11 12 12

5yr forward

0.0

0.5

1.0

07

07

07

08

08

08

09

09

09

r 10 l 10

v 10 r 11

ul 1

1v

11r

12 l 12

v 12

24Source: BBVA Research / Haver

Dec

0Ju

n 0

Dec

0Ju

n 0

Dec

0Ju

n 0

Dec

0Ju

n 0

Dec

0Ju

n 0

Dec

0Ju

n 1

Dec

1Ju

n

Dec

Ju

n 1

Dec

1

Mar Ju

lN

ovM

ar

Jul

Nov

M

ar

Jul

Nov

M

ar Jul

Nov M

a J u Nov

Mar Ju No v

US Economic Outlook

Fiscal PolicyTh fi l liff d l h l d t id th i

Size of the cliff

The fiscal cliff deal helped to avoid another recession

• The deal represents a wasted % of GDP, CY 2013

4.0

4.5Doc fix

popportunity to improve fiscal conditions

2.5

3.0

3.5 ACA

Tax extendersUI benefits

• Positive: Avoids an abrupt economic impact; increases revenues; extension of the sequester and doc

1.5

2.0

2.5

Payroll tax

Tax cuts

fix with offsetting provisions; and leaves open the option to discuss a more meaningful agreement

0.0

0.5

1.0 AMT Patch

BCA cuts • Negative: No entitlement reform; no

pro-growth policy measures; no debt sustainability triggers; missed

25

Fiscal Cliff Left out ATRAdebt sustainability triggers; missed opportunity for a grand-bargain

*American Taxpayer Relief Act of 2012

Source: BBVA Research

US Economic Outlook

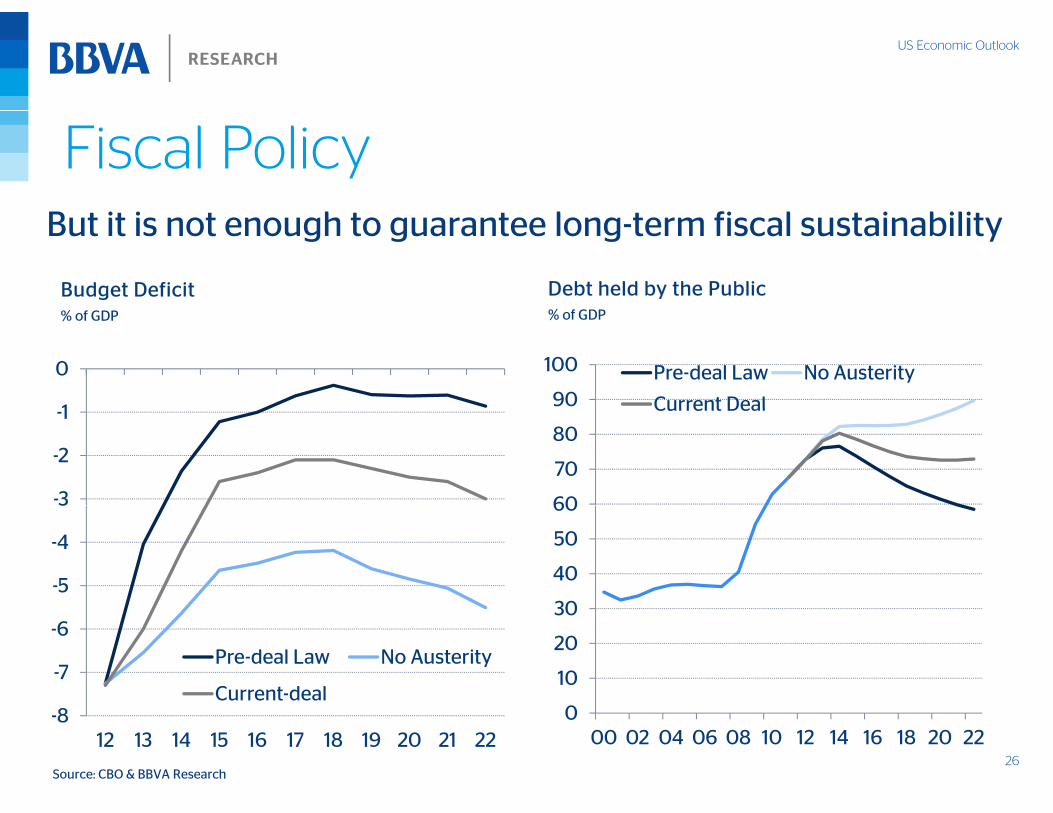

Fiscal Policy

Debt held by the PublicBudget Deficit

But it is not enough to guarantee long-term fiscal sustainability

% of GDP% of GDP

1

0

90

100 Pre-deal Law No Austerity

Current Deal

-3

-2

-1

60

70

80

Current Deal

-5

-4

3

30

40

50

60

-7

-6Pre-deal Law No Austerity

Current-deal10

20

30

26

-812 13 14 15 16 17 18 19 20 21 22

000 02 04 06 08 10 12 14 16 18 20 22

Source: CBO & BBVA Research

US Economic Outlook

Monetary PolicyTh FOMC i i d th t th d

Fed Balance Sheet

The FOMC remains worried on the strength and sustainability of the recovery

Fed Balance SheetUS$bn

FOMC Strategy

Objecti e 3000

3500

Banks' Reserves• Objective• Improve labor market conditions and

maintain price stability

• Quantitative Easing 2000

2500

3000Assets

Q g– $40bn monthly purchases of MBS

– $45bn monthly purchases of Treasury Securities

R i ti i i l t f it 1000

1500

2000

– Reinvesting principal payments from its holdings rolling over maturing Treasuries

• Policy Guidance– Thresholds: unemployment rate at 6.5% and 0

500

1000

27

Thresholds: unemployment rate at 6.5% and one-two year inflation expectation at 2.5%

007 08 09 10 11 12

Source: BBVA Research & Haver

US Economic Outlook

Financial MarketsThe positive reaction to QE3 and the fiscal deal could

Asset Prices & Personal ConsumptionEquity Prices and Risk Perception

The positive reaction to QE3 and the fiscal deal could generate a positive feedback loop

pYoY % change

q y pS&P 500 & VIX

26

28

1 500

1,550SP500 VIX (rhs)

6

8

40

60S&P500 Real PCE (rhs)

20

22

24

1,450

1,500

4

6

20

40

14

16

18

20

1,350

1,400

0

2

-20

0

10

12

14

1,250

1,300

2 2 2 2 2 2 3

-4

-2

-60

-40

82

84

86

89 91

94

96

99 01

03

06

08 -11

28Source: BBVA Research / Haver

Jan

-1

Mar

-1

May

-1

Jul-1

Sep

-1

Nov

-1

Jan

-1

Feb

-8

Jul-8

Dec

-8

May

-8

Oct

-9

Mar

-9

Au

g-9

Jan

-9

Jun

-0

Nov

-0

Ap

r-0

Sep

-0

Feb

-

US Economic Outlook

QE3 ImpactImpact on the unemployment rate

Th f ll i t f QE3 d d thp p y

Pp, accumulated

-0.20

0.00The full impact of QE3 depends on the

size and duration of the program, which are inversely dependent on the self-

i bili f h

Impact of QE3 on Real GDP growth% l d

-0.60

-0.40

3Qtrs 5Qtrs 11Qtrs

sustainability of the recovery

Impact on 5yr forward inflation expectations

%, accumulated -0.80

1.4

1.6

1.83Qtrs

5QtrsImpact on 5yr forward inflation expectationsPp, accumulated

0.15

0.203Qtrs 5Qtrs 11Qtrs

0.8

1.0

1.2 11Qtrs

0 00

0.05

0.10

0 0

0.2

0.4

0.6

29

0.000.0

US Economic Outlook

Interest RatesThe low interest rate environment is likely to continue for a

Mortgage Interest RatesYield Curve

The low interest rate environment is likely to continue for a prolonged period

Mortgage Interest Rates%

Yield Curve%

3 00

3.50

6.5

7.0

2 00

2.50

3.00 10/12/12

12/07/125.0

5.5

6.0

1.00

1.50

2.00

02/01/13

3 5

4.0

4.5

0.00

0.50

1.00

2 0

2.5

3.0

3.55/1 ARM 30Y-fixed

30Source: Bloomberg & BBVA Research Source: Haver & BBVA Research

1m 3m 6m 1y

r

2yr

3yr

5yr

7yr

10yr

20yr

30yr

2.005 06 07 08 09 10 11 12 13

US Economic Outlook

Policy UncertaintyResponse to Uncertainty: Unemployment RatePercentage pointsPolicy uncertainty is the most

important domestic risk to our outlook 0.15

0.20

BBVA US Uncertainty IndexIndex (0=normalized average)

our outlook

0.05

0.10

Response to Uncertainty: U.S. Treasuries

LehmannDebt ceiling

0.000 6 12 18 24

8.0

10.0

Response to Uncertainty: U.S. Treasuries bp

0

530YR 10YR 3MONTH

Fiscal

Cliff

2 0

4.0

6.0

-10

-5

-2.0

0.0

2.0

31

Index weights: Policy(60%), Financial(30%), Geopolitical(10%)

-150 2 4 6 8 10 12 14 16 18 20 22 24

-4.0J-06 J-07 J-08 J-09 J-10 J-11 J-12

US Economic Outlook

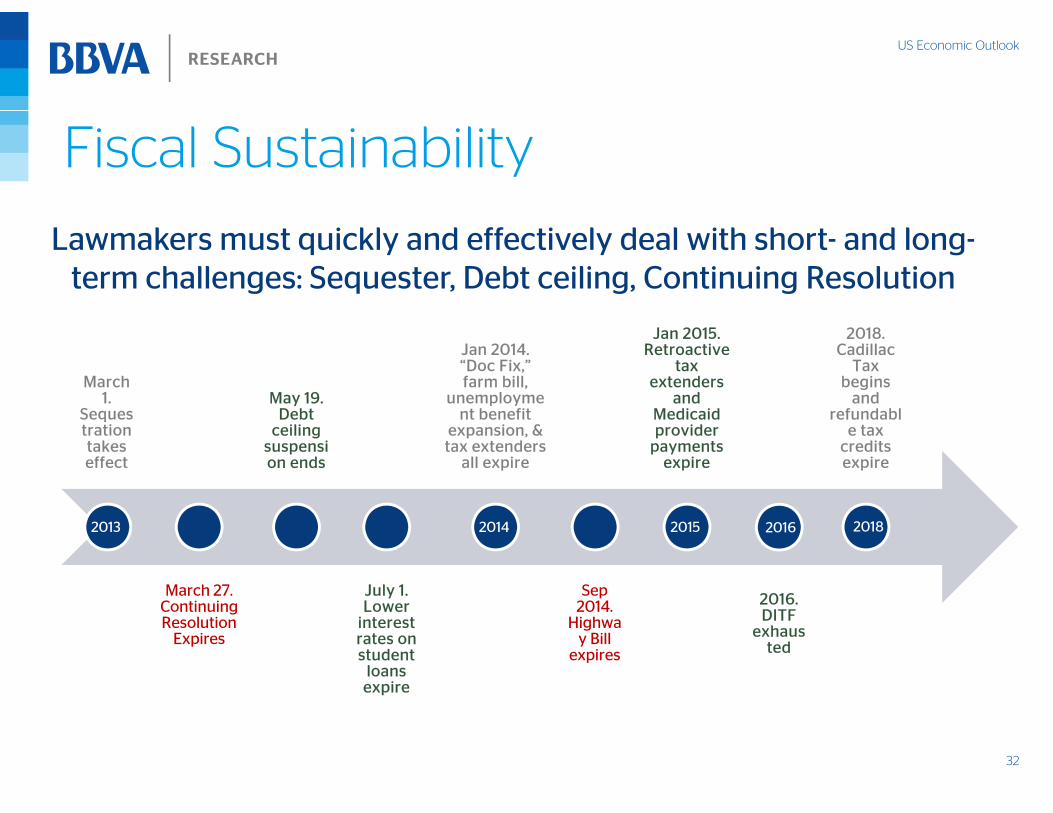

Fiscal Sustainability

Lawmakers must quickly and effectively deal with short- and long-term challenges: Sequester, Debt ceiling, Continuing Resolution

March 1. May 19.

Jan 2014. “Doc Fix,” farm bill,

unemployme

Jan 2015. Retroactive

tax extenders

and

2018. Cadillac

Tax begins

and Sequestration takes effect

Debt ceiling

suspension ends

nt benefit expansion, & tax extenders

all expire

Medicaid provider

payments expire

refundable tax

credits expire

March 27. Continuing

July 1. Lower

Sep 2014 2016.

2014 2015 20162013 2018

Continuing Resolution

Expires

Lower interest rates on student

loans expire

2014. Highwa

y Bill expires

2016. DITF

exhausted

32

US Economic Outlook

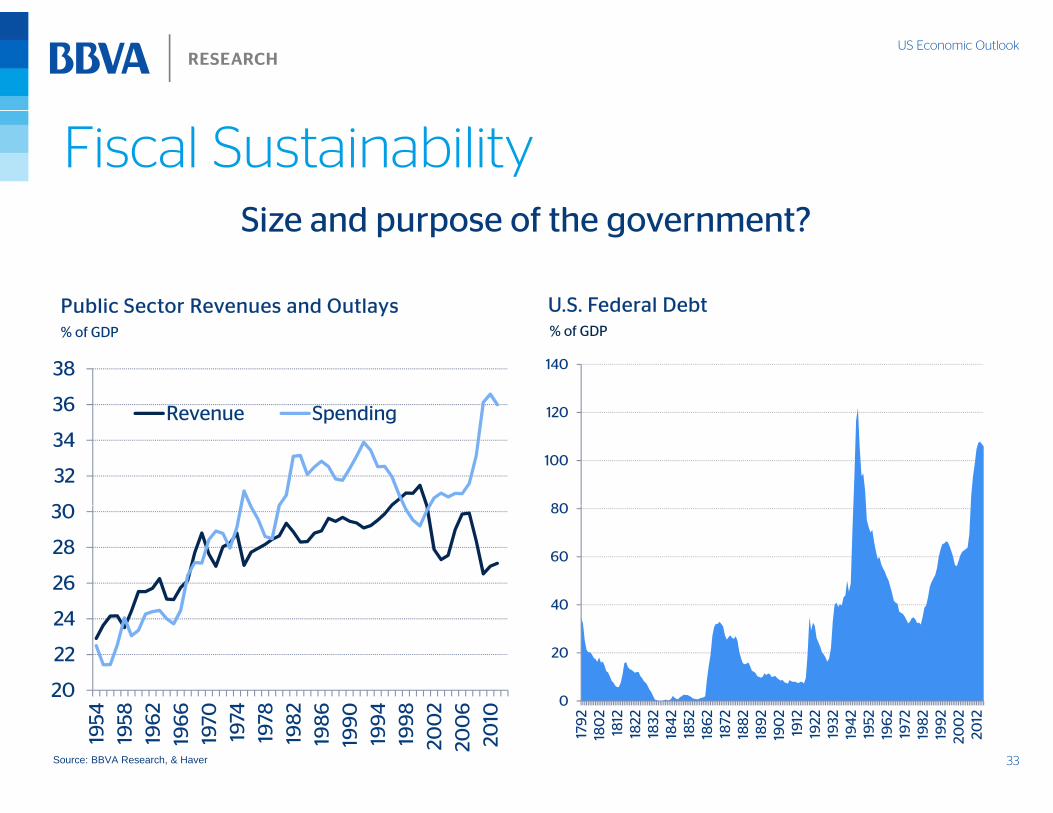

Fiscal SustainabilitySi d f th t?

U S Federal DebtPublic Sector Revenues and Outlays

Size and purpose of the government?

U.S. Federal Debt% of GDP

Public Sector Revenues and Outlays% of GDP

36

38

R S di

140

30

32

34

36 Revenue Spending

80

100

120

26

28

30

40

60

80

20

22

24

0

20

40

33Source: BBVA Research, & Haver

1954

1958

196

219

66

1970

1974

1978

198

219

86

199

019

94

199

820

02

200

620

10

0

179

218

02

1812

1822

1832

184

218

5218

62

1872

188

218

92

190

219

1219

2219

3219

42

1952

196

219

7219

82

199

220

02

2012

US Economic Outlook

Fiscal SustainabilitySi d f th t?

State DebtGovernment Outlays

Size and purpose of the government?

State Debt% of GDP, ranking

Government Outlays% of GDP, CBO

35

Medicare/25

30

S. Security

aid

15

20

Other5

10

WorseBetter

34Source: BBVA Research, & Haver

012 22 32 42 52 62 72 82

WorseBetter

US Economic Outlook

Long-term growthWashington needs to focus on the basicsWashington needs to focus on the basics

Declining competitiveness: 2009: 2nd 2010: 4th 2011: 5th 2012: 7th

The Twelve Pillars of Global Competitiveness (US ranked 7th)• Investor protection vs. legal burden, cost of crime & violenceInstitutions (41)

• Airline supply vs. mobile phone penetrationInfrastructure (14)

• Excessive budget deficits, and high public debtMacro Environment (111)

• Low enrollment rates and expensive healthcare systemHealth and Primary Education (34)

• Tertiary enrollment high, and strong R&DHigher Education and Training (8)

• High tax rates and tariffs vs. strong competitionGoods Market Efficiency (23)

• Labor Markets fluid, and highly productiveLabor Market Efficiency (6)

• Soundness of banks vs. abundant venture capitalFinancial Market Development (16) pp

• Technology adoption vs. FDI and tech transferTechnological Readiness (11)

• Size dominant feature of U.S. economyMarket Size (1)

35

• Strong business management and high value added process Business Sophistication (10)

• Patent production and university-business collaborationInnovation (6)

*Source: World Economic Forum

US Economic Outlook

Long-term growthAdd i k b ttl k ill b t t ti l GDP

GDP per capita

Addressing key bottlenecks will boost potential GDP

Potential GDP GrowthGDP per capita2010 US$

Potential GDP GrowthYoy % change

70,0004.0

Population TFP Part RateCapital Hours NAIRUPotential

65,000

NoCrowdingOut

With Crowding Out2.5

3.0

3.5Potential

55,000

60,000

1.0

1.5

2.0

50,000

-0.5

0.0

0.5

36Source: BBVA Research & Haver

45,0002010 2016 2022 2028 2034

-1.080 84 88 92 96 00 04 08 12 16

US Economic Outlook

Polarization Political Polarization: House and Senate Polarization and Income Inequality% % & Index 0 to 1

0 90

1.00House Senate

0.44

0.49

0.90

1.00House SenateGini (rhs)

0.80

0.90

0 34

0.39

0.44

0 70

0.80

0.90

Polarization and Median AgePolarization and Foreign Born Population

0.70

1879

1887

189

519

03

1911

1919

1927

1935

194

319

5119

5919

67

1975

198

319

91

199

920

07

0.340.70

1947

1951

1955

1959

196

319

67

1971

1975

1979

198

319

8719

91

199

519

99

200

320

07

Polarization and Median Age% & years

Polarization and Foreign Born Population% & % of total Population

10

12

0 90

1.00HouseSenateForeign Born (rhs) 33

35

37

0 90

1.00House Senate Age (rhs)

4

6

8

0 70

0.80

0.90 Foreign Born (rhs)

27

29

31

33

0 70

0.80

0.90

37

40.70

1947

1951

1955

1959

196

319

67

1971

1975

1979

198

319

8719

91

199

519

99

200

320

07

270.70

1947

1951

1955

1959

196

319

67

1971

1975

1979

198

319

8719

91

199

519

99

200

320

07

US Economic Outlook

Opportunities: Energy RevolutionGeopolitical rebalancing higher employment CO emissions

Energy Trade BalanceEnergy Consumption

Geopolitical rebalancing, higher employment, CO emissions reduction & stronger economic growth

Energy Trade BalanceQuadrillion Btu

Energy Consumption Quadrillion Btu

120 5

C l 20Coal, 21

Other, 15Other, 21

80

100

-5

0

NaturalGas, 23

NaturalGas, 27

Coal, 20Coal, 21

40

60

-15

-10

Petroleum, 37

Petroleum, 36

0

20

-25

-20 Crude Oil OtherNatural Gas Liquid FuelsTotal

38

02009 2035

-25

200

9

2011

2013

2015

2017

2019

2021

2023

2025

2027

2029

2031

2033

2035

Source: BBVA Research , & EIA

US Economic Outlook

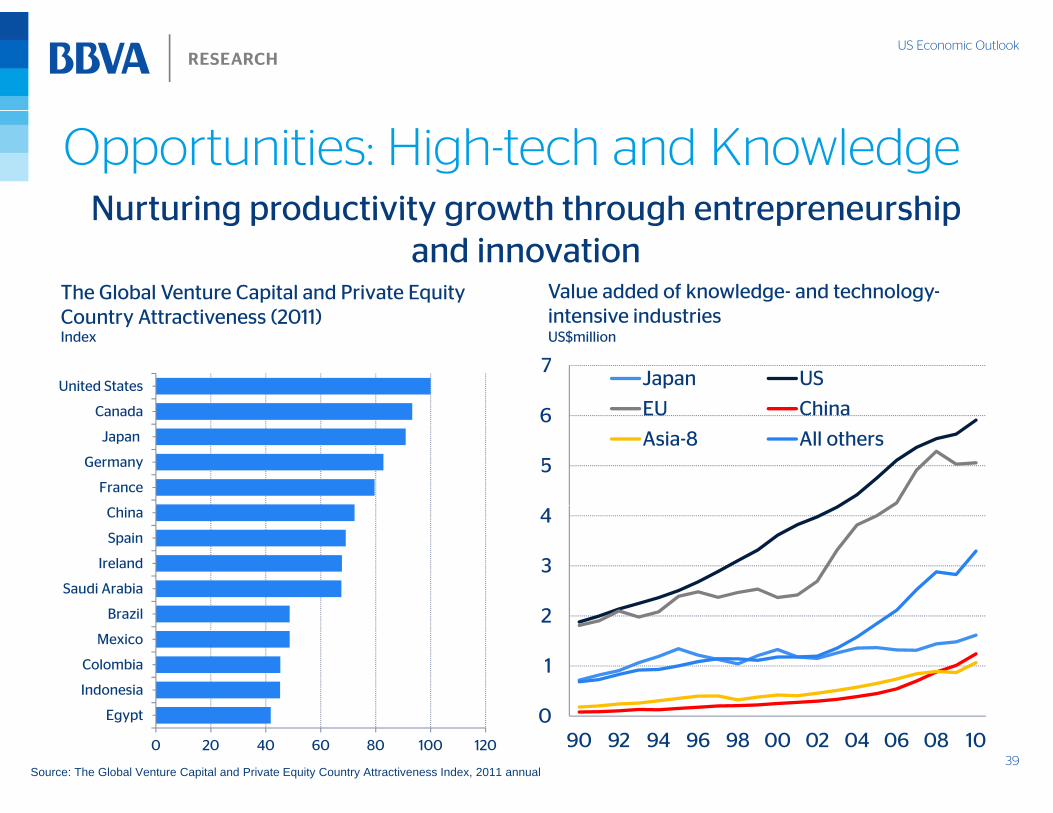

Opportunities: High-tech and KnowledgeNurturing productivity growth through entrepreneurship

Value added of knowledge- and technology-The Global Venture Capital and Private Equity

Nurturing productivity growth through entrepreneurship and innovation

intensive industriesUS$million

Country Attractiveness (2011)Index

C d

United States7

Japan US

EU China

France

Germany

Japan

Canada

5

6 EU China

Asia-8 All others

Saudi Arabia

Ireland

Spain

China

3

4

Indonesia

Colombia

Mexico

Brazil

1

2

390 20 40 60 80 100 120

Egypt

Source: The Global Venture Capital and Private Equity Country Attractiveness Index, 2011 annual

090 92 94 96 98 00 02 04 06 08 10

US Economic Outlook

Opportunities: The Green EconomyRenewable resources and the clean economy

Employment Growth in Selected Clean Industries

Renewable resources and the clean economy offer huge upsides

Employment Growth in Selected Clean IndustriesAnnual average % growth 2003-2010

6 +39,668Absolute change

4

5

+754+79,401 +565,337

g

2

3

0

1+3,237

+87,000

40-1

US Average Recycled-Content Products

Recycling and Reuse

Waste-to-Energy Waste Management and

Treatment

Aggregate Clean Economy

Source: Brookings Institute and BLS

US Economic Outlook

Regional OutlookThe energy boom is boosting economic performance in

Home PricesUnemployment Rate

The energy boom is boosting economic performance in central states

% change 2007-12

p y%, Last

41

WorseBetterSource: BBVA Research & Haver

US Economic Outlook

Regional OutlookRegional risks automatic spending cuts could have

GDP Impact as % of State GDPEmployment losses as % of State Total

Regional risks: automatic spending cuts could have heterogeneous effects

pImpact from sequestration

p yImpact from sequestration

42

LowerHigherSource: BBVA Research & Haver

US Economic Outlook

AlabamaState Monthly Activity Index Housing Price Index (Purchase Only)3-Month Moving Average Year over Year % Change

0.20.40.6

5

10

15

-0 6-0.4-0.20.0

USAlabama -10

-5

0

5

USAlabama

Unemployment RateTotal Exports

-0.80.6

01 02 03 04 05 06 07 08 09 10 11Source: BLS / Haver Analytics

-15

10

01 02 03 04 05 06 07 08 09 10 11 12Source: BLS / Haver Analytics

Unemployment Rate%

Total ExportsYear over Year % Change, Moving Average

40

60

8 0

10.0

12.0

USAlabama

-20

0

20

US 2 0

4.0

6.0

8.0 Alabama

43

-40

20

01 02 03 04 05 06 07 08 09 10 11

USAlabama

Source: BLS / Haver Analytics

0.0

2.0

02 03 04 05 06 07 08 09 10 11 12Source: BLS / Haver Analytics

US Economic Outlook

AlabamaSolid growth in North America and strong demand for commodities

Alabama Value of ExportsAlabama Exports by Country

Solid growth in North America and strong demand for commodities will support exports and the local economy

Alabama Value of ExportsAnnual average, US$bn

Alabama Exports by CountryYoY % change, 4QMA

70

8.0 Transportation Chemicals

Minerals Metals125

150Canada

5.0

6.0

7.0 Minerals Metals

Machinery

75

100

125China

Germany

Mexico

3.0

4.0

25

50Other

0 0

1.0

2.0

-50

-25

0

44

0.02006-07 2010-11 2012

5007 08 09 10 11 12

Source: BBVA Research & Haver

US Economic Outlook

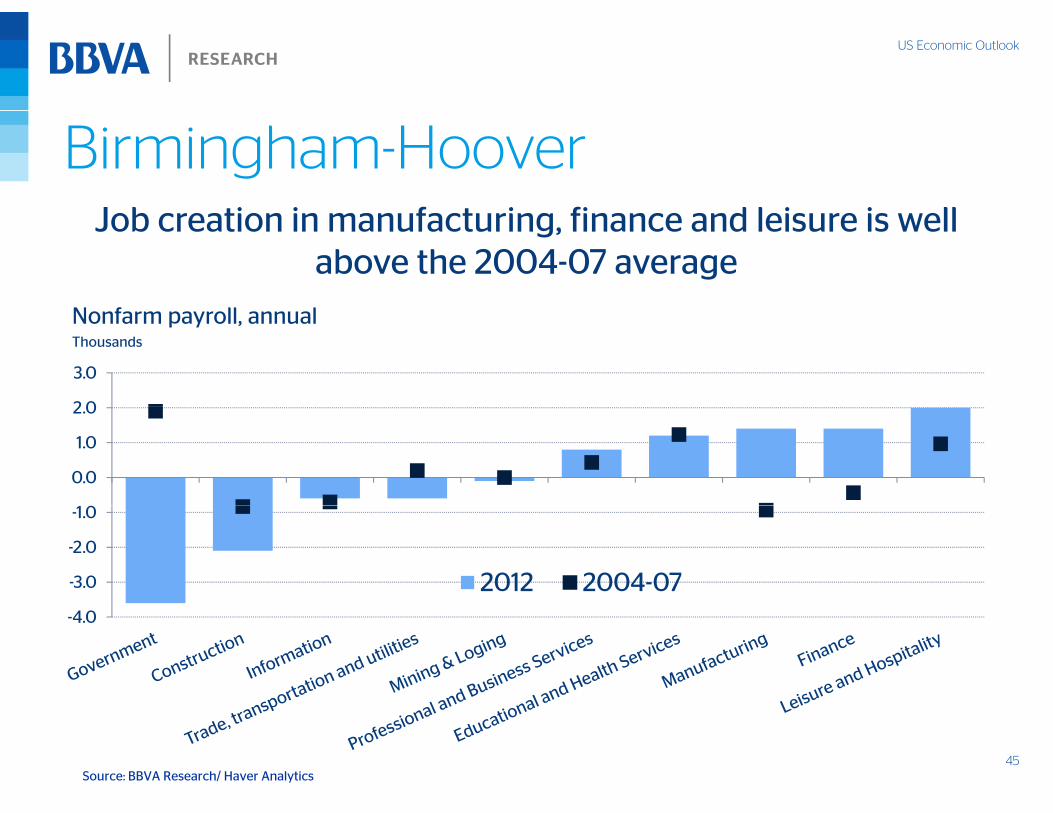

Birmingham-HooverJ b ti i f t i fi d l i i llJob creation in manufacturing, finance and leisure is well

above the 2004-07 average

N f ll lNonfarm payroll, annualThousands

2 0

3.0

0.0

1.0

2.0

-3.0

-2.0

-1.0

2012 2004-07-4.0

45Source: BBVA Research/ Haver Analytics

US Economic Outlook

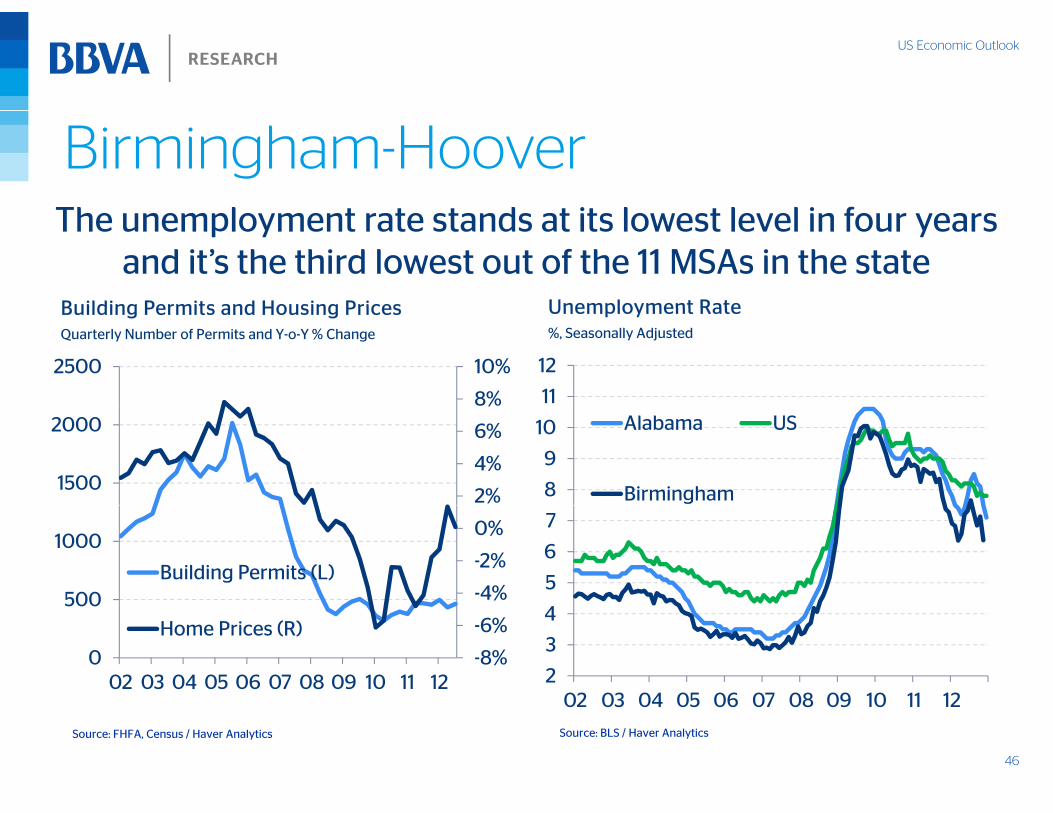

Birmingham-HooverTh l t t t d t it l t l l i f

Unemployment RateBuilding Permits and Housing Prices

The unemployment rate stands at its lowest level in four years and it’s the third lowest out of the 11 MSAs in the state

Unemployment Rate%, Seasonally Adjusted

Building Permits and Housing PricesQuarterly Number of Permits and Y-o-Y % Change

8%

10%2500

11

12

2%

4%

6%

1500

2000

8

9

10 Alabama US

Birmingham

-4%

-2%

0%

500

1000

Building Permits (L) 5

6

7

-8%

-6%

0

500

02 03 04 05 06 07 08 09 10 11 12

Home Prices (R)

2

3

4

02 03 04 05 06 07 08 09 10 11 12

46

Source: FHFA, Census / Haver Analytics

02 03 04 05 06 07 08 09 10 11 12

Source: BLS / Haver Analytics

US Economic Outlook

Key Messages

• Slow global recovery but with a lower probability of a tail risk scenario

•• The U.S. economy is closer to a selfThe U.S. economy is closer to a self--sustainable sustainable privateprivate--led expansion cycleled expansion cyclepp p yp y

•• Elevated policy uncertainty is limiting the pace of Elevated policy uncertainty is limiting the pace of the recoverythe recoverythe recoverythe recovery

•• Implementing structural reforms will boost longImplementing structural reforms will boost long--term potential growthterm potential growth

•• Economic conditions in Alabama and Economic conditions in Alabama and

47Birmingham will continue to improveBirmingham will continue to improve

US Economic Outlook

Thank you!Thank you!Let us know your opinion!

To receive our publications send us an email:

Follow us on Twitter: @BBVAresearchUSA

48

More information on the Web: www.bbvaresearch.com

US Economic Outlook

This document and the information integrity or correctness BBVA accepts the aforementioned securities or financial promotion order or (iii) are

DisclaimerThis document and the information,opinions, estimates and recommendationsexpressed herein, have been prepared byBanco Bilbao Vizcaya Argentaria, S.A.

(hereinafter called “BBVA”) to provide itscustomers with general informationregarding the date of issue of the report

integrity or correctness. BBVA acceptsno liability of any type for any direct orindirect losses arising from the use of thedocument or its contents. Investors shouldnote that the past performance ofsecurities or instruments or the historicalresults of investments do not guaranteefuture performance.

the aforementioned securities orinstruments or to companies relatedthereto or to their shareholders, executivesor employees, or may have interests orperform transactions in those securities orinstruments or related investments beforeor after the publication of this report, to theextent

financial promotion order, or (iii) arepersons to whom an invitation orinducement to engage in investmentactivity (within the meaning of section 21of the financial services and markets act2000) may otherwise lawfully becommunicated (all such persons togetherbeing referred to as “relevant persons”).

and are subject to changes without priornotice. BBVA is not liable for giving noticeof such changes or for updating thecontents hereof

This document and its contents do notconstitute an offer, invitation or solicitationto purchase or subscribe to any securities

The market prices of securities orinstruments or the results of investmentscould fluctuate against the interests ofinvestors. Investors should be aware thatthey could even face a loss of theirinvestment. Transactions in futures,options and securities or high-yield

permitted by the applicable law.

BBVA or any of its affiliates´ salespeople,traders, and other professionals mayprovide oral or written market commentaryor trading strategies to its clients thatreflect opinions that are contrary to theopinions expressed herein Furthermore

This document is directed only at relevantpersons and must not be acted on or reliedon by persons who are not relevantpersons. Any investment or investmentactivity to which this document relates isavailable only to relevant personsand will be engaged in only with relevantpersons The remuneration systemto purchase or subscribe to any securities

or other instruments, or to undertakeor divest investments. Neither shall thisdocument nor its contents form the basisof any contract, commitment or decision ofany kind.

Investors who have access to this

options and securities or high yieldsecurities can involve high risks and arenot appropriate for every investor. Indeed,in the case of some investments, thepotential losses may exceed the amount ofinitial investment and, in suchcircumstances, investors may be requiredto pay more money to support those

opinions expressed herein. Furthermore,BBVA or any of its affiliates’ proprietarytrading and investing businesses maymake investment decisions that areinconsistent with the recommendationsexpressed herein. No part of thisdocument may be (i) copied, photocopiedor duplicated by any other form or means

persons. The remuneration systemconcerning the analyst/s author/s of thisreport is based on multiple criteria,includingthe revenues obtained by BBVA and,indirectly, the results of BBVA Group in thefiscal year, which, in turn, include theresults generated by the investment

document should be aware that thesecurities, instruments or investments towhich it refers may not be appropriate forthemdue to their specific investment goals,financial positions or risk profiles, as thesehave not been taken into account toprepare this report Therefore investors

losses. Thus, before undertaking anytransaction with these instruments,

investors should be aware of theiroperation, as well as the rights, liabilitiesand risks implied by the same and theunderlying stocks. Investors should alsobe aware that secondary markets for the

(ii) redistributed or (iii) quoted, without theprior written consent of BBVA. No part ofthis report may be copied, conveyed,distributed or furnished to any person orentity in any country (or persons or entitiesin the same) in which its distribution isprohibited by law. Failure to comply withthese restrictions may breach the laws of

bankingbusiness; nevertheless, they do notreceive any remuneration based onrevenues from any specific transaction ininvestment banking.

BBVA is not a member of the FINRA andis not subject to the rules of disclosureprepare this report. Therefore, investors

should make their own investmentdecisions considering the saidcircumstances and obtaining suchspecialized advice as may be necessary.The contents of this document is basedupon information available to the publicthat has been obtained from sources

be aware that secondary markets for thesaid instruments may be limited or evennot exist.

BBVA or any of its affiliates, as well astheir respective executives andemployees, may have a position in any ofthe securities or instruments referred to,

these restrictions may breach the laws ofthe relevant jurisdiction.

In the United Kingdom, this document isdirected only at persons who (i) haveprofessional experience in matters relatingto investments falling within article 19(5) ofthe financial services and markets act

is not subject to the rules of disclosureaffecting such members.

“BBVA is subject to the BBVA Group Codeof Conduct for Security Market Operationswhich, among other regulations, includesrules to prevent and avoid conflicts ofinterests with the ratings given, including

49

considered to be reliable. However, suchinformation has notbeen independently verified by BBVA andtherefore no warranty, either express orimplicit, is given regarding its accuracy,

directly or indirectly, in this document, or inany other related thereto; they may tradefor their own account or for third-partyaccount in those securities, provideconsulting or other services to the issuer of

2000 (financial promotion) order 2005 (asamended, the “financial promotion order”),(ii) are persons falling within article 49(2)(a) to (d) (“high net worth companies,unincorporated associations, etc.”) Of the

information barriers. The BBVA GroupCode of Conduct for Security MarketOperations is available for reference at thefollowing web site:www.bbva.com / Corporate Governance”.

Economic OutlookEconomic Outlook

The Birmingham Estate PlanningThe Birmingham Estate Planning Council

Nathaniel KarpChi f U S E i tChief U.S. EconomistBBVA Research

Birmingham, AL February 7, 2013