Download - Sales force effectiveness in pharmaceutical

Moch Kurniawan property all rights reserved.

Sales Force Effectiveness in Pharmaceutical

Moch Kurniawan

Moch Kurniawan property all rights reserved.

Globalization, consumerism and prosperity are the major trends that will impact healthcare in SEA

Globalization

ConsumerismProsperity

Globalization: • World is becoming smaller: cheap air- travel, connectivity, internet, medical tourism• Increased healthcare awareness because of multiple media

Consumerism: • Increased self medicating behaviour; ease of access (online)• Increased expression of consumer individuality through brand choices

Prosperity: • Increasing disposable income, financial independence leading to exploring more choices• Increased health awareness has led to consumers spending more on health prevention and OTC

2 3

1

Source: Frost & Sullivan

INFRASTRUCTURE

Moch Kurniawan property all rights reserved.

APAC among the fastest growing economies over the next 5 years

31.1

20.0

4.91.7 0.9 0.3

40.5

21.0

6.22.3 1.1

0.3

50.9

23.3

7.93.0

1.5

0.4

CAGR5.1%

CAGR1.5%

CAGR5.0%

CAGR5.7%

CAGR5.1%

CAGR2.5%

0

10

20

30

40

50

60

Singapore Brunei Malaysia Thailand Indonesia Vietnam

GD

P p

er c

ap

ita

(U

S$ t

ho

usa

nd

)

Southeast Asia

2006 2010 2016

CAGR3.3%

CAGR12.0%

CAGR5.5%

0

10

20

30

40

50

Hong Kong China India

GD

P p

er c

ap

ita

(U

S$ t

ho

usa

nd

)

Asia

2006 2010 2016

CAGR4.8%

CAGR0.7%

CAGR1.9%

CAGR-1.2%

CAGR1.7%

0

10

20

30

40

50

60

GD

P p

er c

ap

ita

(U

S$ t

ho

usa

nd

)

Developed Economies

2006 2010 2016

Source: Data in the above charts were based on GDP per capita data in the respective country’s national currency as sourced from the WEO online database. The data above was converted to US dollar based on the currency conversion rate for the respective years. Analysis by Frost & Sullivan

CAGR

2.9%

Moch Kurniawan property all rights reserved.

Diverse population structures with varying levels of purchasing power

1.3%

0.5%

1.2%

1.5%

2.7%

2.3%

0.5%1.6%

0.9%

-0.5%

1.0%

2.1%

-0.2%

2.6%

0.2%

3.9%

0.9%

-0.1%

-0.2%

0.7%

0.4%

0

200

400

600

800

1,000

1,200

1,400

Po

pu

lati

on

(m

illio

n)

2006 2010 2016

Asia Pacific Mature markets

CAGR (2006-2016F)

Sources: World Economic Outlook (WEO), World Bank and countries data. CAGR data is for 2006 to 2016

Increasing consumer power

•Rural population, low income, relies on government support. •Upwardly growing middle class, living in tier 2 cities, educated, can pay for some level of healthcare• High income category, first adopters of new technology, services, private HC

Moch Kurniawan property all rights reserved.

Patient Protection and Affordable Care Act (PPACA) Highlights

Source: Ernst & Young LLP

Moch Kurniawan property all rights reserved.

NEW GLOBAL CENTER IN ASIA-PAC

DOCTORS LESS CENTRAL IN HEALTH

GLOBAL SYSTEMS IN CRISIS

PAYERSFIRMLY

IN CONTROL

1 2 3 4

CUSTOMER

NEARUNIVERSAL IPAD ACCESS

HIRING THE

COMPETITION

FEAROF THE

CLOSING DOOR

5 6 7

TRENDS OVERVIEW

TALENT

STRATEGY

THE NEW REP-RELIANT BLOCKBUSTER

DISCONNECTED DIGITAL TOOL SET

DETAILING FOR THE

DOUBLE YES

WORKING WITH NEW PREFERENCES

8 9 10 11

Moch Kurniawan property all rights reserved.

Relevant Trends in Indonesia

• Middle class to rise from 19% of Asian population in 2009 to 30% by 2014

• Indonesia has a young population, where 44% are below 24 years old

Growing wealth of middle class to drive demand

Source: CLSA Mr & Mrs Asia Moving up the J-curves – Spring 2010

Moch Kurniawan property all rights reserved.

Toddler10%

Kids10%

Teens9%

Teens adult9%

Young adult8%

Early jobber

9%Young Parent

8%

Parenthood

8%

Mature18%

Ageing well11%

Age Group Population

Source: sp2010.bps.go.id

Indonesian population per 2010 national census grew at 1.1% YoY. The population pyramid has shown a shift to a bigger young to middle age group – which resulted to the increasing productive age group between 24 to 54 y.o. The split between Male:Female is almost equal, except a slightly higher in Female Ageing Well group

Population % based on total age group % based on Gender

Grouping Age Range # of Population Male Female ALL Male Female ALL

Toddler 0-4 22,678,702 10% 9% 10% 51% 49% 100%

Kids 5-9 23,253,480 10% 10% 10% 51% 49% 100%

Teens 10-14 22,671,081 10% 9% 10% 51% 49% 100%

Teens adult 15-19 20,880,734 9% 9% 9% 51% 49% 100%

Young adult 20-24 19,891,633 8% 8% 8% 50% 50% 100%

Early jobber 25-29 21,310,443 9% 9% 9% 50% 50% 100%

Young Parent 30-34 19,830,685 8% 8% 8% 50% 50% 100%

Parenthood 35-39 18,505,131 8% 8% 8% 50% 50% 100%

Mature 40-54 42,127,155 18% 18% 18% 50% 50% 100%

Ageing well 55+ 26,492,282 11% 12% 11% 48% 52% 100%

Total 237,641,326 100% 100% 100% 50% 50% 100%

Moch Kurniawan property all rights reserved.

Relevant Trends in Indonesia

Demographic

Indonesian population by Generation Group 2010-2016 (in ‘000)

40,988 41,118 41,247 41,377 41,498 41,595 41,673

103,127 103,233 103,317 103,369 103,353 103,271 103,311

49,305 50,294 51,251 52,192 53,103 53,997 54,893

40,058 41,686 43,360 45,076 46,862 48,708 50,461

-

50,000

100,000

150,000

200,000

250,000

300,000

2010 2011 2012 2013 2014 2015 2016

Gen Z (age 0 - 9) Gen Y (age 10 - 34) Gen X (age 35 - 49) Baby Boomers (age 50 - 75+)

2010 vs 2016 Growth

26.0%

11.3%

0.2%

1.7%

• From the chart above, baby boomers and retire (>54) population have the biggest growth until 2016 people’s life expectancy longer people’s health awareness higher

• Productive people (25 – 54) (gen X and partial gen Y) also growing around 11.3%

Source: Data Statistik Indonesia

Moch Kurniawan property all rights reserved.

Indonesia Socio Economic Class - Nielsen & BCG report

Nielsen, the leading global market data provider company, publishes yearly consumer segmentations, called Socio Economic Class (SEC) and the single measure/ criteria is heavily based on routine Monthly Household Expenditure (MHE). It’s widely used by consumer goods company or any marketer

which targeting consumer/ patient base. It shows the level of economic buying power, from the lowest E class (those who spends MHE below IDR 700K per month to the highest A class (> IDR 3mio per month). From the past 3 years consecutive data below, it tells us that Indonesian middle economic classes (AtoC1) are increasing at +6% average, correlates to the economic growth at +6% yoy. This is also aligned with the latest Boston Consulting

Group’s (BCG) report and World Bank’s report on Indonesian middle class

8% 8% 14%

18% 16%

25%

23% 23%

28%25% 27%

22%17% 14%

8%9% 12%3%

2010 2011 2012

Year

E IDR < 700.000

D IDR 700.001 -1.000.000

C2 IDR 1.000.001 -1.500.000

C1 IDR 1.500.001 -2.000.000

B IDR 2.000.001 -3.000.000

A IDR > 3.000.000

+6%

+9%

+5%

Nielsen’s SESBCG’s Report

World Bank’s Report –from the economist.com

Moch Kurniawan property all rights reserved.

Population in Indonesia, income demographics 2012 vs 2020

Source: Statistics Indonesia

Moch Kurniawan property all rights reserved.

Pharmaceutical and medical technology firms are not alone in the race

Moch Kurniawan property all rights reserved.

• Per capita healthcare expenditure is far below global average (lowest is Vietnam and Indonesia).

• Shortage of healthcare professionals in both countries.

• Efflux of medical tourists seeking treatment in other countries; 400,000 Indonesians patients travel annually.

Market Restraints

• Growing middle-class population in Indonesia;per capita income expected to grow from$2,580 in 2011 to $3,500 by 2015.

• Rise in non-communicable disease incidence,cardiovascular disease will account for 31percent of total number of deaths in Indonesiaby 2030, followed by other chronic diseases at28 percent.

• Vietnamese government intervention toenhance healthcare workforce by 2020.

Market Drivers

Total Indonesia Healthcare Market Size

Healthcare Industry: Revenue Forecast Indonesia 2011–2015

Source: Frost & Sullivan analysis.

0.0

2000.0

4000.0

6000.0

8000.0

10000.0

12000.0

2011 2012 2013 2014 2015

Indonesian Healthcare Market Size

Year

Indonesia 5549.30 6016.30 6515.90 7072.10 7742.50

$ (Billion)

CAGR8.7%

Moch Kurniawan property all rights reserved.

3,119

3,453

3,816

4,187

4,755

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2009 2010 2011 2012 2013

Sale

s V

alu

e Tr

ade

OK

U Y

EN (

IDR

10

,58

3,3

33

,33

3/O

KU

YEN

)

Nutrition

OTC

ETHICAL

TOTAL MARKET42%

58% 61%

39%39%

61%

40%

+4%

+9%

+15%

+15% +11%

+13%

+11%

+11%

+14%

39%

61%

+15%

+11%

+12%

60%

Exchange rate: Constant IDR10,583,333,333/OKU YENSource: IMS Plus 2013-Q2

Indonesia Pharmaceutical Market – MAT 2013Q2• Indonesia is a big potential market for pharmaceutical industry, with total market size at OKU YEN 4,755 in MAT 2013Q2

• And the pharmaceutical market in Indonesia has grown rapidly at growth +12% in last year, driven by OTC sector growing +15% in 2013Q2 .

• In overall the pharmaceutical market growth is outperforming economic growth (6%). • The market growth is expected to continue at the same rate for 2012-2015.

Moch Kurniawan property all rights reserved.

Decrease new product launch in Indonesia

Source: IMS: ITMA-Ethical Only MAT 4Q10

0

50

100

150

200

250

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Number of Products Launch per Year

Foreign Ethical Foreign OTC Local Ethical Local OTC

Avg : 150

Avg : 63

Avg : 33

Avg : 9

Moch Kurniawan property all rights reserved.

Most companies have ambitious growth targets - combined with and increasing complexity in their business model

2013 – Commercial Excellence Forum

Moch Kurniawan property all rights reserved.

Indonesia—Healthcare System

Moch Kurniawan property all rights reserved.

Indonesia—Healthcare Indicators

Healthcare Indicators: Indonesia, 2007–2011

Key Features

• The population of the country as of 2010 stands at 238.0 million people. It is recorded as the fourth most

populous country in the world.

• The population of the country is expected to grow at a consolidated pace of 1.0 percent for the 2010‒2015

period.

• Life expectancy at birth has increased by 16 months per person from 2007 to 2011, and decreasing mortality

rates are a result of improving healthcare services.

Healthcare Indicators 2007 2008 2009 2010 2011

Population (Million) 226 229 232 238 245

Population Growth Rate (%) 1.3 1.3 1.3 1.07 1.04

Birth Rate (per 1,000) 19.65 19.24 18.84 18.10 17.76

Mortality Rate (per 1,000) 6.90 6.85 6.80 6.28 6.26

Life Expectancy (Female) (years) 72.7 73.1 73.4 74.0 74.3

Life Expectancy (Male) (years) 67.6 68.0 68.3 68.8 69.1

Source: IMF, CIA World Fact Book, Indonesian Department of Health, Frost & Sullivan analysis.

Moch Kurniawan property all rights reserved.

Disease Information – Major Causes of Death

Cardiovascular

31.0%

Cummunic

able13.0%Other

Chronic28.0%

Cancer

18.0%

Others10.0%

Major Causes of Death, 2030

Cardiovascular

30.0%

Cummunic

able25.0%

Other

Chronic21.0%

Cancer

13.0%

Others

11.0%

Major Causes of Death, 2010

Source: Indonesian Association of Medical Doctors (Ikatan Dokter Indonesia, or IDI)

Moch Kurniawan property all rights reserved.

Three dimensions of coverage

Increasing coverage of 41.7% (2005) to 63.2% (2012)

Comprehensive benefit package (2012)

No cost sharing (Jamkesmas)

Ahmad Fuady Health Economics, Policy and Law Erasmus University Rotterdam The Netherlands 2013

Moch Kurniawan property all rights reserved.

Three dimensions of coverage

• Less coverage, compared to neighboring countries

• A low coverage to formal workers group

3%

Ahmad Fuady Health Economics, Policy and Law Erasmus University Rotterdam The Netherlands 2013

Moch Kurniawan property all rights reserved.

Indonesia Social Security and Healthcare Programs Up Date

Member

• 142.711.701 (24/4/15)

Healthy Facilities

• Central of Healthy People 9798

• Army Clinic 750

• Police Clinic 570

• Basic Clinic 2712

• Hospital D Class 1675

• Primary Clinic 79

• Pharmacy 1679

• Optic 870

Doctor

• Dentist 1050

• Private Practice 4222

Moch Kurniawan property all rights reserved.

Indonesia—Health Care Delivery System

Healthcare System

Public Private

MOH Hospital

Provincial Hospital

District Hospital

Puskesmas Pustus and

Mobile Clinics

Specialty Private

Hospital

General Private

Hospital

Private Clinics

Source: Ministry of Health and Frost & Sullivan analysis

Moch Kurniawan property all rights reserved.

Indonesia—Hospital Categorization

Hospitals (General and Specialty)

Public Hospital

Private Hospital

Class A (>400 beds) = 10

Class B (100-400 beds) = 120

Class C (50-100 beds) = 250

Class D (<50 beds) = 126

Extensive specialist medical services + extensive sub specialists

Extensive specialist medical services + limited sub specialists

Has minimum of four basic specialist medical

services

Provides basic medical facilities

Priority

General medical services + specialists and sub-specialists

Madya

Pratama

Minimum four specialists medical services

General medical service

Source: Indonesian Department of Health, Frost & Sullivan analysis

Moch Kurniawan property all rights reserved.

Indonesia—Hospital Classification

Public (Ministry of

Health)

36%

Public (Military)

8%

Public (State or other govt dept-owned)

5%

Private51%

Percent of Hospitals by Type and Sector, Indonesia, 2010

Mental 15.3% Leprosy

6.6%Pulmonary

TB3.0%

Eye3.9%

Maternity 19.5%

Pediatric32.1%

Others19.5%

Percent of Specialist Hospitals Split by Specialty, Indonesia, 2010

Source: Indonesian Department of Health, Frost & Sullivan analysis

Hospital Classification by Type Hospital Classification by Specialty

Moch Kurniawan property all rights reserved.

Number of Hospitals: Regional Spread

Source: Ministry of Health, Indonesia

BaliNo. of hospitals:

34

Sumatra SelatanNo. of hospitals:

34

DKI JakartaNo. of hospitals:

124

Sumatra UtaraNo. of hospitals:

130

Sumatra BaratNo. of hospitals:

41

Sulawesi SelatanNo. of hospitals:

62

Jawa BaratNo. of hospitals:

144

Jawa TengahNo. of hospitals:

162

AcehNo. of hospitals:

35

Jawa TimurNo. of hospitals:

171

Hospitals are concentrated in major cities in the Sumatra and Java province, such as Jakarta, Surabaya, Medan.

Moch Kurniawan property all rights reserved.

Why look at hospital channel today

Know thy customer: Winning in the hospital channel, Copyright © April 2015 McKinsey & Company

Moch Kurniawan property all rights reserved.

three key actions a company must take to drive growth in this channel today

Develop a deeper understanding of the

changing hospital customer segments,

including their unique needs and willingness to

engage with pharmaceutical companies

Expand team/account-based sales model and

build new capabilities and supporting processes and tools to better meet the needs of select hospital

customers

Broaden and tailor your value propositions to

address hospitals’ evolving cost, quality/outcomes and patient satisfaction

priorities

Know thy customer: Winning in the hospital channel, Copyright © April 2015 McKinsey & Company

Moch Kurniawan property all rights reserved.

Pharmaceutical companies focus

Source: PricewaterhouseCoopers, Pharma Vision 2020

Moch Kurniawan property all rights reserved.

Availability

Availability of trained health care professionals and their salaries.

• Problem of data validity and reliability• Lack of health care professionals• Problem of deployment policy and unclear

decentralization policy• Without domestically competitive salary

Ahmad Fuady Health Economics, Policy and Law Erasmus University Rotterdam The Netherlands 2013

Moch Kurniawan property all rights reserved.

National Health Strategic Plan: Infrastructure Targets

• Aim to increase the number of community health centers from 9,133 in 2010 to 10,856 in 2014

• Develop hospitals to achieve a ratio of 1 bed per 1,000 population in 2014

• Indonesia also aims to achieve sufficient numbers of medical professionals:

Source: Indonesia Human Resource for Health; Development Plan, 2010 Regional Health Forum, 2006

Moch Kurniawan property all rights reserved.

Key mega trends impacting Indonesia

Low Probability of Success

De

gree

of

Imp

act

Low

Hig

h

High

Urbanization

Generation Y

Increase in Working Age Population

“She-conomy”

The Middle Bulge

Wealth Watchers

Future Economic Growth

Space Jam

Connectivity

Innovating to Zero

E-Mobility

Future Infrastructure

Top Industries of the Future

“Value for Many” Business Model

Health, Wellness and Well Being

Future Energy Power Generation

Private public partnerships

E-Governance

“Click-n-Connect”Mobile users

Moch Kurniawan property all rights reserved.

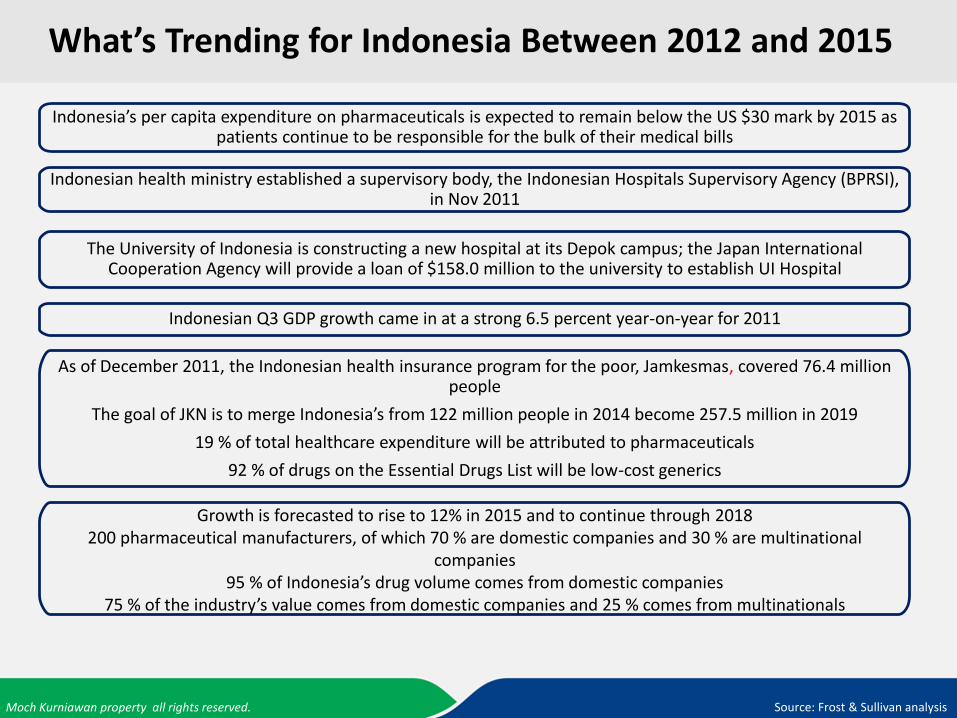

What’s Trending for Indonesia Between 2012 and 2015

Indonesia’s per capita expenditure on pharmaceuticals is expected to remain below the US $30 mark by 2015 as patients continue to be responsible for the bulk of their medical bills

Indonesian health ministry established a supervisory body, the Indonesian Hospitals Supervisory Agency (BPRSI), in Nov 2011

The University of Indonesia is constructing a new hospital at its Depok campus; the Japan International Cooperation Agency will provide a loan of $158.0 million to the university to establish UI Hospital

Indonesian Q3 GDP growth came in at a strong 6.5 percent year-on-year for 2011

As of December 2011, the Indonesian health insurance program for the poor, Jamkesmas, covered 76.4 million people

The goal of JKN is to merge Indonesia’s from 122 million people in 2014 become 257.5 million in 2019

19 % of total healthcare expenditure will be attributed to pharmaceuticals

92 % of drugs on the Essential Drugs List will be low-cost generics

Growth is forecasted to rise to 12% in 2015 and to continue through 2018200 pharmaceutical manufacturers, of which 70 % are domestic companies and 30 % are multinational

companies95 % of Indonesia’s drug volume comes from domestic companies

75 % of the industry’s value comes from domestic companies and 25 % comes from multinationals

Source: Frost & Sullivan analysis

Moch Kurniawan property all rights reserved.

Examples of investments into Indonesia

Philips supplied most of $140m in medical equipment for the first dedicated cancer research centre and the biggest hospital in Indonesia. Philips, which has group sales of $32bn and 120,000 employees, has set up a regional headquarters in Singapore with almost 300 staff with a view to increasing its share of the medical and home healthcare products in Indonesia, the Philippines and Vietnam.

Singapore-based Invida Group, a specialty biopharmaceutical company announced a joint venture with the local Indonesian drug manufacturer PT MUGI Laboratories. Under the terms of the agreement, Invida will seek to expand its operations in Indonesia to include the importation of raw materials and auxiliaries and the manufacture of pharmaceutical products.

A state pharmaceutical company PT Bio Farma announced that it is to spend USD 60 million on a facility to produce blood plasma products, including albumin and Factor IX. The plant will be the first of its kind in Indonesia and will be built using assistance from South Korean and Australian pharmaceutical companies, based on guidelines stipulated by the WHO.

Sources: Company websites, Frost & Sullivan

Siemens in Indonesia has provided support to public and private hospitals by installing computed tomography, magnetic resonance imaging systems, and angiographic systems, as well as conventional x-ray units and life support systems. Siemens supplied the first 128-slice computed tomography (CT) Somatom Definition AS+ in Indonesia.

Moch Kurniawan property all rights reserved.

Pharma 3.0 From drugs to healthy outcomes

Ernst & Young – Global Life Sciences Center, Pharma 3.0 Life Sciences Network Basel, 20 May 2010

Moch Kurniawan property all rights reserved.

We need to look at the situation from different perspectives…

Moch Kurniawan property all rights reserved.

…but at the same time make sure that we have a common focus

Moch Kurniawan property all rights reserved.

Our sales teams are faced with

Less physician face-to-face

time

Older products

Fewer new ‘blockbuster’

brands

Increasing competition –both generic and branded

Managed care and

market access challenges

Less ‘new’ clinical data

being provided by

their companies

Customers’ increasing

use of digital media to

source product

information

The 2014 Guide to Improving Your Field Force Coaching Process, www.acoach.net

Moch Kurniawan property all rights reserved.

Moch Kurniawan property all rights reserved.

Moch Kurniawan property all rights reserved.

Moch Kurniawan property all rights reserved.

The consumerization of business buying

More social

More real-time

More modular

Do you really understand how your business customers buy? Copyright © 2015 McKinsey & Company. All rights reserved

Moch Kurniawan property all rights reserved.

Three priorities for reshaping the sales organization

Charting decision journeys by customer segment and drilling down on customer

expectations and needs at each stage of the

journey

Tackling the difficult process of reallocating

sales and marketing resources to the

activities most likely to influence decisions

Changing organizational structures to ramp up collaboration between

marketing and sales

Do you really understand how your business customers buy? Copyright © 2015 McKinsey & Company. All rights reserved

Moch Kurniawan property all rights reserved.

Moch Kurniawan property all rights reserved.

Moch Kurniawan property all rights reserved.

Moch Kurniawan property all rights reserved.

Insight in customer needs makes it possible for us to identify the right actions and target the execution

2013 – Commercial Excellence Forum

Moch Kurniawan property all rights reserved.

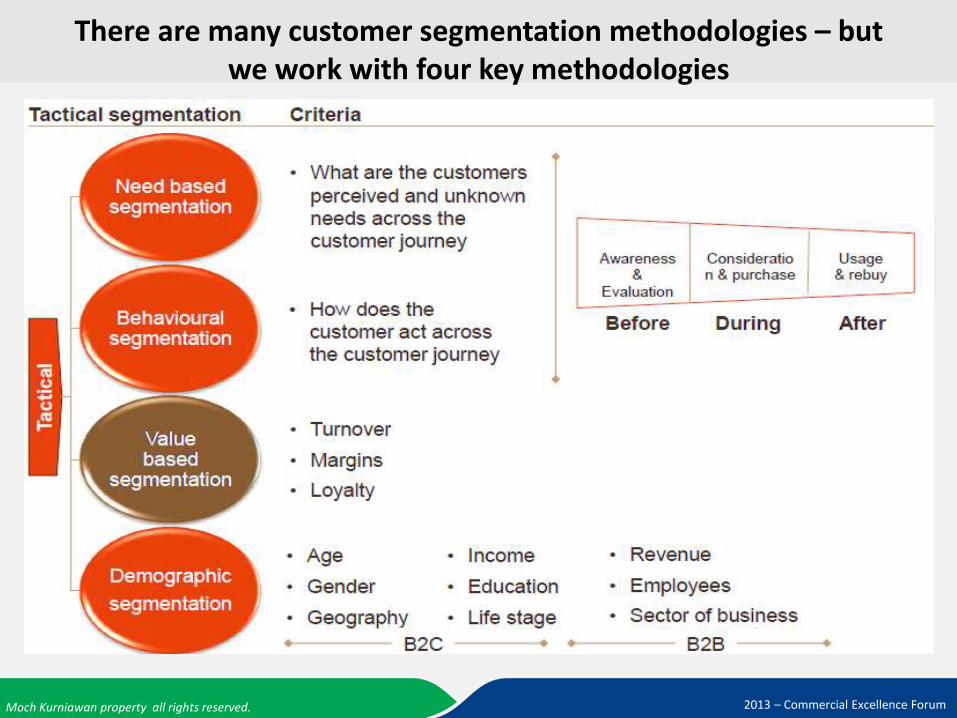

There are many customer segmentation methodologies – but we work with four key methodologies

2013 – Commercial Excellence Forum

Moch Kurniawan property all rights reserved.

There are many customer segmentation methodologies – but we work with four key methodologies

2013 – Commercial Excellence Forum

Moch Kurniawan property all rights reserved.

Customer insight is the driver for both customer segmentation and building your value proposition

2013 – Commercial Excellence Forum

Moch Kurniawan property all rights reserved.

Segmentation is needed to drive higher profitability through understanding customer needs and delivering on those needs

Meet Exceed

Relationship Development

Retain anddevelop

Manage

Customer Expectations

Cherish and tailor

Nu

mb

er o

f in

div

idu

als

Few

Many

Low HighValue per individual

Unprofitable Marginally profitable

More profitable

Very profitable

Segmentation is an important tool in becoming customer-centric. It is a key enabler of CRM.

“Recognise me, remember me, value me.”

Typically customers are not created equal ..and different “segments” need different customer strategies to exploit their value

20-30%

40-50%

20-30%

Moch Kurniawan property all rights reserved.

The operational segmentation help prioritization of time and resourcesand understand what to offer to who at what price/discount level

2013 – Commercial Excellence Forum

Moch Kurniawan property all rights reserved.

Yesterday: Today & Tomorrow:

Targeting Mass customisation Differentiation

Focus Acquisition Retention

Approach How big is my list? Test and learn

Company KPIs Volume targets Value targets

Marketing KPIs Sales volumes Segment objectives (KPIs)

Propositions Sell to all Customer-needs driven

Using segmentation for a ‘Customer Driven Organization’

Moch Kurniawan property all rights reserved.

Criteria for ABC Classification

The accumulated revenue of the customer within a defined period of time. By default, the period of time begins with the beginning of the previous year and

ends at the current date.

The total revenue of all customers within the same period of time

Defined percentages of the total revenue, which are used as thresholds

for the classification. By default, the thresholds

are defined as 80%, 15%, and 5%.

The classification is based to the following criteria:

PUBLIC © 2014 SAP SE or an SAP affiliate company. All rights reserved

Moch Kurniawan property all rights reserved.

Moch Kurniawan property all rights reserved.

Moch Kurniawan property all rights reserved.

Moch Kurniawan property all rights reserved.

Customer Behavior In Indonesia – 9 Trends

Marketeers Dinner Seminar|Customer Insight Tools | Feb 27-29 2012

Moch Kurniawan property all rights reserved.

The foundation for organic growth, is a strong value differentiation which is perceived valuable by the customers

2013 – Commercial Excellence Forum

Moch Kurniawan property all rights reserved.

The value curve can be used to design the customer experience

Finding the Consumer value Curve

Moch Kurniawan property all rights reserved.

Moch Kurniawan property all rights reserved.

Moch Kurniawan property all rights reserved.

Moch Kurniawan property all rights reserved.

Moch Kurniawan property all rights reserved.

Moch Kurniawan property all rights reserved.

The key metrics for measuring FFE effectively

understand demand

master product knowledge

communicate business benefits

use account plans

use differentiated metrics

www.mentorgroup.co.uk

Moch Kurniawan property all rights reserved.

Business Challenges: The Selling Environment

Competition is intense

Customers are more sophisticated, knowledgeable and demanding

Acquiring new customers and opening new channels were reported as increasingly important to growth strategies

Profitability has replaced revenue growth as a critical focus of sales organizations

Commoditization/shrinking markets was a theme in most industries

The roles of sales representative and sales manager are described as more complex and demanding

How Sales Forces Sustain Competitive Advantage Research Report© 2008 IIR Holdings, Ltd

Moch Kurniawan property all rights reserved.

3 sales skills correlated significantly with performance

Sales Skills

How Sales Forces Sustain Competitive Advantage Research Report© 2008 IIR Holdings, Ltd

Moch Kurniawan property all rights reserved.

The correlations of the three sales management skills with performance

Sales Management Skills

How Sales Forces Sustain Competitive Advantage Research Report© 2008 IIR Holdings, Ltd

Moch Kurniawan property all rights reserved.

Sales Effectiveness Landscape

How Sales Forces Sustain Competitive Advantage Research Report© 2008 IIR Holdings, Ltd

Moch Kurniawan property all rights reserved.

Sales Force Effectiveness Metrics

Moch Kurniawan property all rights reserved.

5 Steps to Pharmaceutical Sales Force Effectiveness

Performance Measurement & Management

Moch Kurniawan property all rights reserved.

Sales Performance Metrics – Current and Future State Example

Source: L.E.K. Consulting

Moch Kurniawan property all rights reserved.

Moch Kurniawan property all rights reserved.

Package sale

Dynamic calls

Affiliate “labs”

20

13

/14

20

15

/bey

on

d

On-the-go learning

Navigators of new data

NEW OPPORTUNITIES FOR REP EXPERIENCE

The new, compelling experiences we can build position reps as quick-access experts and leverage our individual affiliates to improve global strategy.

Moch Kurniawan property all rights reserved.

All the

answers (in best-fit

media)

Influencer

call plans

and content

Flexible

contact

model

Reconnect

marketing

and sales

Feature-rich

engagement

s

REP EXPERIENCE 2015 BEST PRACTICES

Tools, experiences, and expectations designed to stand out in a crowded marketplace—or even just a crowded waiting room

Moch Kurniawan property all rights reserved.

Summary and Conclusions

It takes an organization, not just skilled individuals

How Sales Forces Sustain Competitive Advantage Research Report© 2008 IIR Holdings, Ltd

Moch Kurniawan property all rights reserved.

How loyal are your customers?

Moch Kurniawan property all rights reserved.

Moch Kurniawan property all rights reserved.

Moch Kurniawan property all rights reserved.

Moch Kurniawan property all rights reserved.

Roles & responsibilities

Know thy customer: Winning in the hospital channel, Copyright © April 2015 McKinsey & Company

Moch Kurniawan property all rights reserved.