digital: developing insurance in emerging markets · digital: developing insurance in emerging...

TRANSCRIPT

Digital:

Developing insurance

in emerging markets

Recaredo Arias

CEO AMIS

2

Index

Innovation Concepts

Macro-trends

Challenges

Innovation in Insurance

AMIS Hackathon

Conclusions

3

Small activities that until recently cost us

time in travel and paperwork, today are resolved through the

use of ICT’s.

The hasty development that ICTs have had over

the last 20 years has altered our

understanding of the world.

ICTs are the backbone on which the operations of a public and private organization are held.

Information and Communication Technologies (ICT) in the new business environment

Difficult to conceive our life without technology

4

Snapchat

Facebook Twilio

Uber

Netflix

Amazon AppleGoogle

Chobani Spotify

Alibaba Tencent

Source: Fast Company Website, 2017

Most innovative companies of 2017

5

New technologies

Genomics

Blockchain

Robotics

Autonomous vehicles

Cognitive systems

Telemedicine

Cyber risk

Telematics

Source: AMIS / CAM 2016

Food

Drones

IoT

6

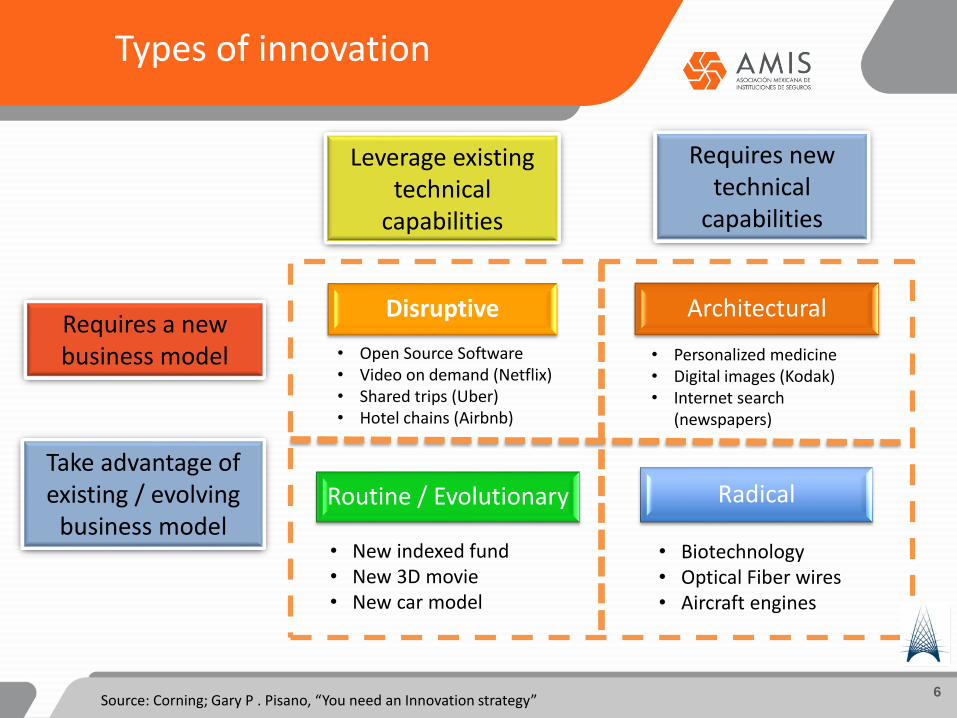

Types of innovation

Source: Corning; Gary P . Pisano, “You need an Innovation strategy”

Requires a new business model

Take advantage of existing / evolving

business model

Leverage existing technical

capabilities

Requires new technical

capabilities

• Open Source Software• Video on demand (Netflix)• Shared trips (Uber)• Hotel chains (Airbnb)

• Personalized medicine• Digital images (Kodak)• Internet search

(newspapers)

• New indexed fund• New 3D movie• New car model

• Biotechnology• Optical Fiber wires• Aircraft engines

Routine / Evolutionary Radical

ArchitecturalDisruptive

7

Stop thinking about limitations and start thinking about possibilities.

8

Macrotrends

6 tendencies which define the business world

• Companies should compete in the analyzes

(Data Science) to differentiate themselves.

• Intelligent mobility will change the way

people interact.

• Technology blurs borders.

• Cloud computing finally takes off.

• The power of individuals will stimulate

innovation.

• The government's role in innovation is

growing.

Source: EY, “La innovación rápida en tecnología crea un mundo inteligente y móvil”

9

• Consumer oriented

• Simplicity

Strategies

• Asking ourselves: which is our strategy in the digital world?

Not: which is your digital strategy?

10Source: Insurance Thought Leadership

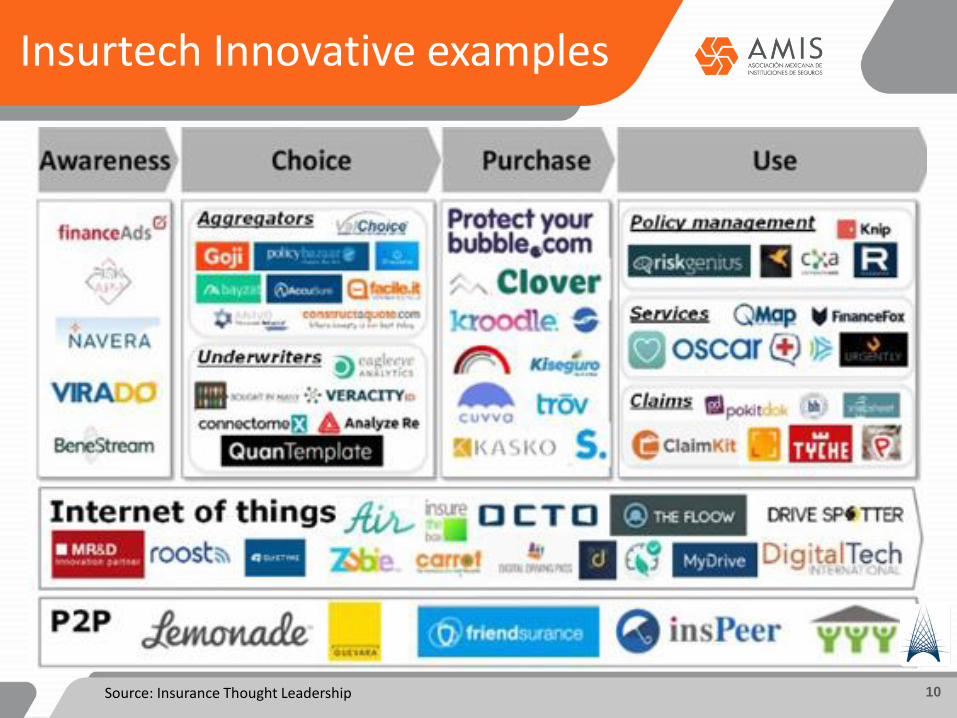

Insurtech Innovative examples

11

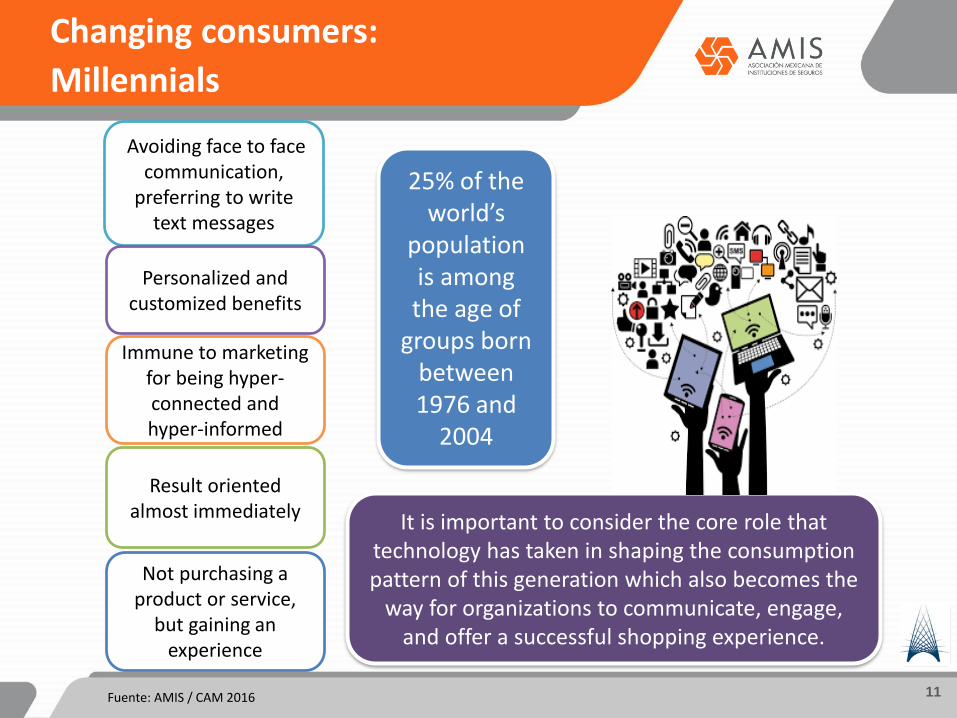

Changing consumers:

Millennials

25% of the world’s

population is among the age of

groups born between 1976 and

2004

Avoiding face to face communication,

preferring to write text messages

Immune to marketing for being hyper-connected and hyper-informed

Result oriented almost immediately

Personalized and customized benefits

Not purchasing a product or service,

but gaining an experience

It is important to consider the core role that technology has taken in shaping the consumption pattern of this generation which also becomes the

way for organizations to communicate, engage, and offer a successful shopping experience.

Fuente: AMIS / CAM 2016

12Source: OCDE, “Startup América Latina 2016”

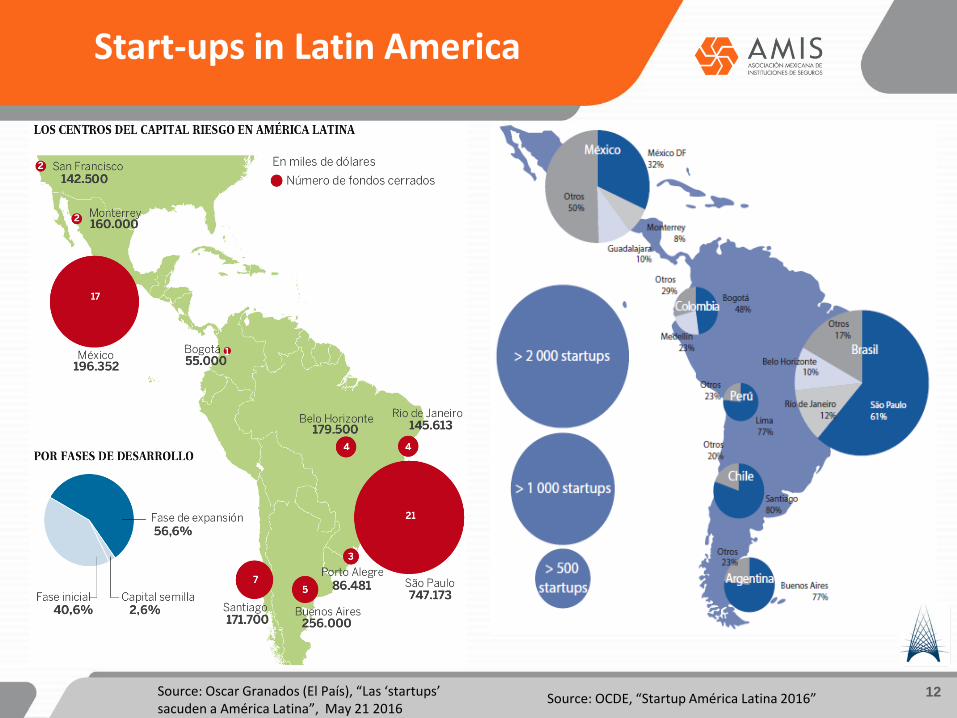

Start-ups in Latin America

Source: Oscar Granados (El País), “Las ‘startups’ sacuden a América Latina”, May 21 2016

13

Only that which is not tried is impossible

We must always look for an opportunity in every challenge, so we do not paralyze when thinking of the challenge of each opportunity.

14

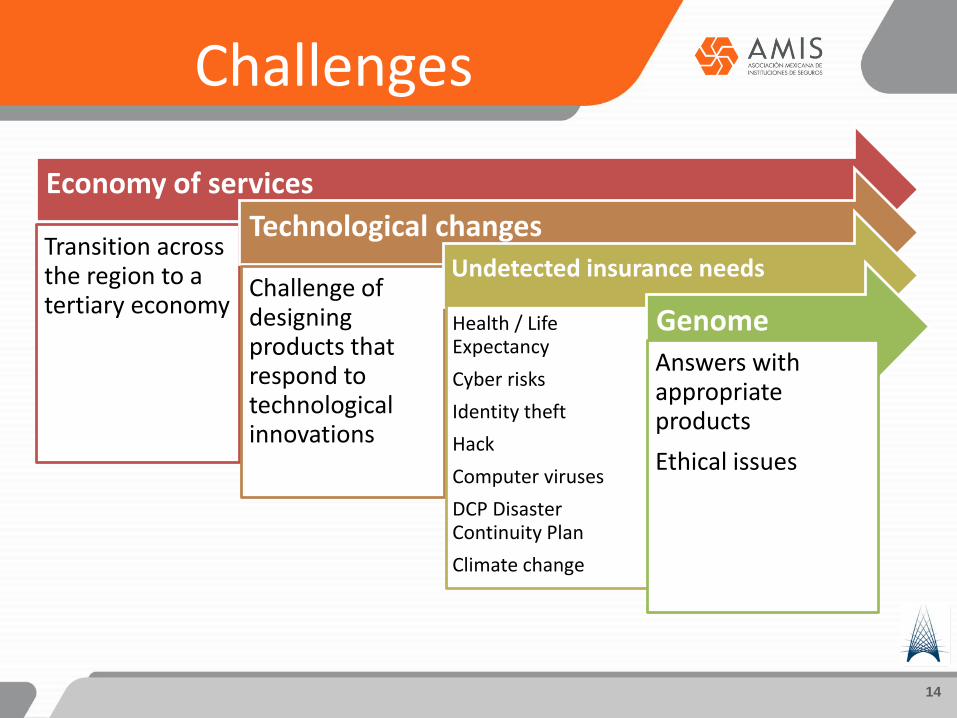

Challenges

Economy of services

Transition across the region to a tertiary economy

Technological changes

Challenge of designing products that respond to technological innovations

Undetected insurance needs

Health / Life Expectancy

Cyber risks

Identity theft

Hack

Computer viruses

DCP Disaster Continuity Plan

Climate change

Genome

Answers with appropriate products

Ethical issues

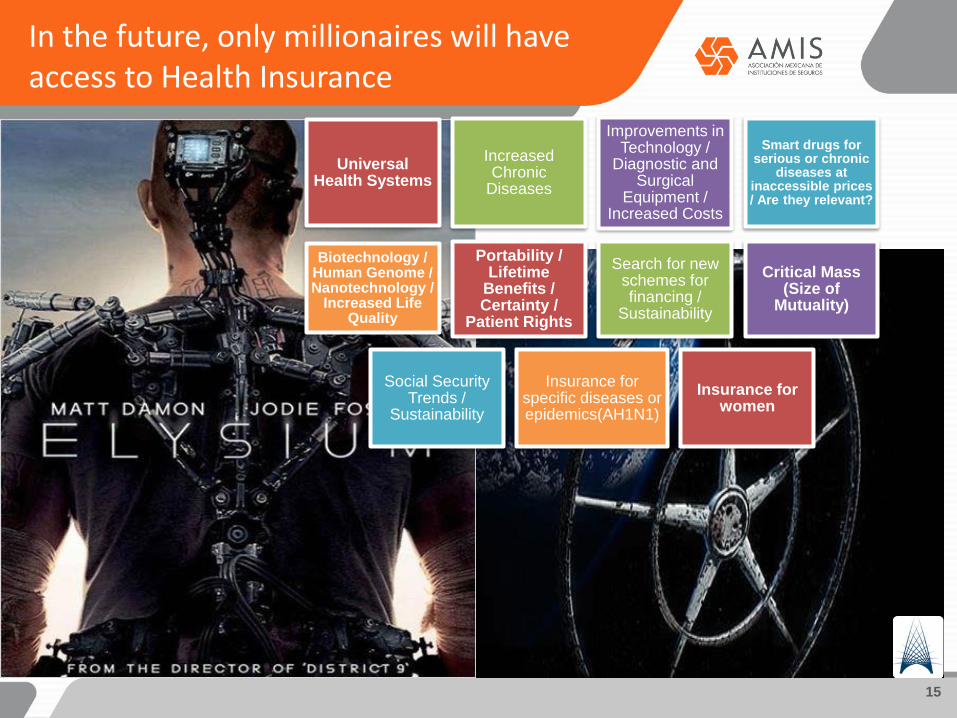

15

In the future, only millionaires will have access to Health Insurance

Universal Health Systems

Increased Chronic

Diseases

Improvements in Technology /

Diagnostic and Surgical

Equipment / Increased Costs

Smart drugs for serious or chronic

diseases at inaccessible prices / Are they relevant?

Biotechnology / Human Genome / Nanotechnology /

Increased Life Quality

Portability / Lifetime

Benefits / Certainty /

Patient Rights

Search for new schemes for financing /

Sustainability

Critical Mass (Size of

Mutuality)

Social Security Trends /

Sustainability

Insurance for specific diseases or epidemics(AH1N1)

Insurance for women

16

Always set the trail, never follow the path

Innovation in Insurance

The Insurance Sector will be transformed

in the next 7 years as never before.

17

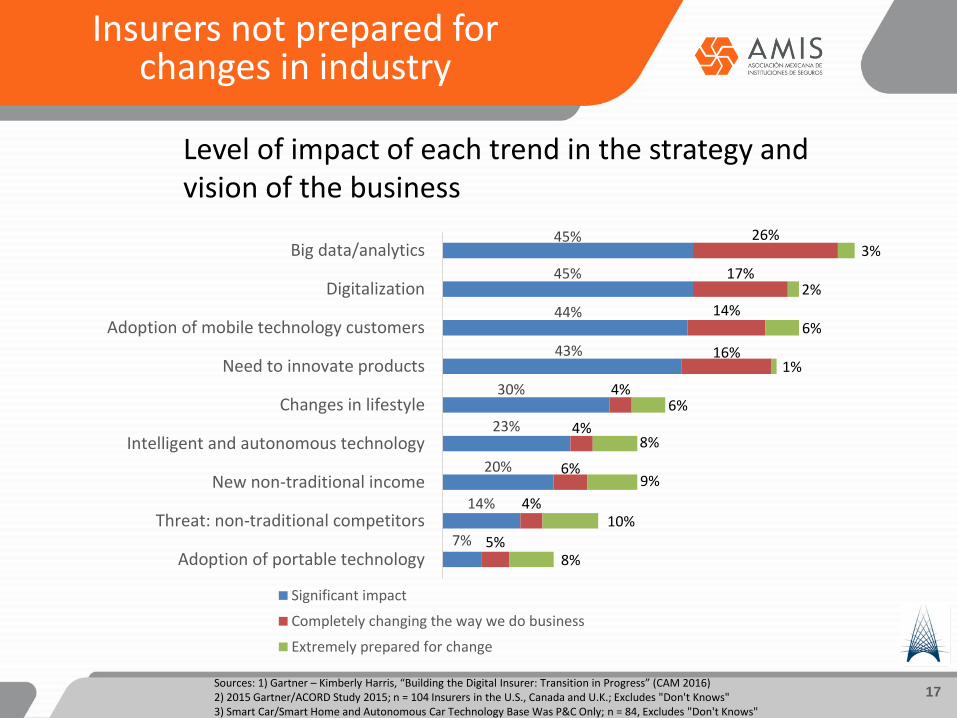

Level of impact of each trend in the strategy and vision of the business

Sources: 1) Gartner – Kimberly Harris, “Building the Digital Insurer: Transition in Progress” (CAM 2016)2) 2015 Gartner/ACORD Study 2015; n = 104 Insurers in the U.S., Canada and U.K.; Excludes "Don't Knows"3) Smart Car/Smart Home and Autonomous Car Technology Base Was P&C Only; n = 84, Excludes "Don't Knows"

Insurers not prepared for changes in industry

7%

14%

20%

23%

30%

43%

44%

45%

45%

5%

4%

6%

4%

4%

16%

14%

17%

26%

8%

10%

9%

8%

6%

1%

6%

2%

3%

Adoption of portable technology

Threat: non-traditional competitors

New non-traditional income

Intelligent and autonomous technology

Changes in lifestyle

Need to innovate products

Adoption of mobile technology customers

Digitalization

Big data/analytics

Significant impact

Completely changing the way we do business

Extremely prepared for change

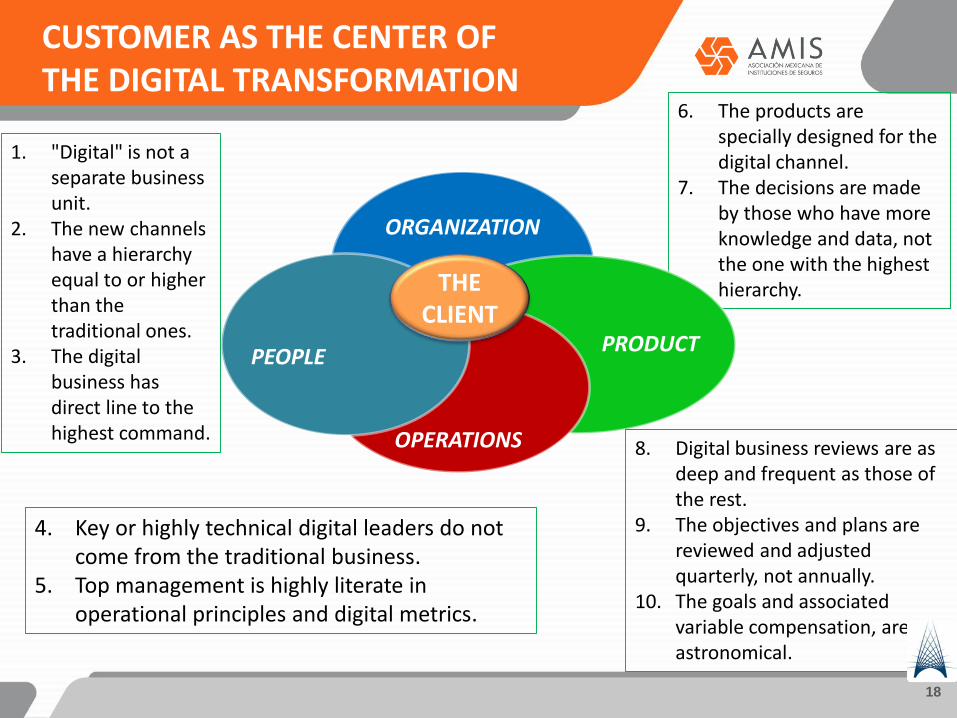

6. The products are specially designed for the digital channel.

7. The decisions are made by those who have more knowledge and data, not the one with the highest hierarchy.

18

ORGANIZATION

PRODUCT

OPERATIONS

PEOPLE

1. "Digital" is not a separate business unit.

2. The new channels have a hierarchy equal to or higher than the traditional ones.

3. The digital business has direct line to the highest command.

4. Key or highly technical digital leaders do not come from the traditional business.

5. Top management is highly literate in operational principles and digital metrics.

8. Digital business reviews are as deep and frequent as those of the rest.

9. The objectives and plans are reviewed and adjusted quarterly, not annually.

10. The goals and associated variable compensation, are astronomical.

CUSTOMER AS THE CENTER OF THE DIGITAL TRANSFORMATION

THE CLIENT

19

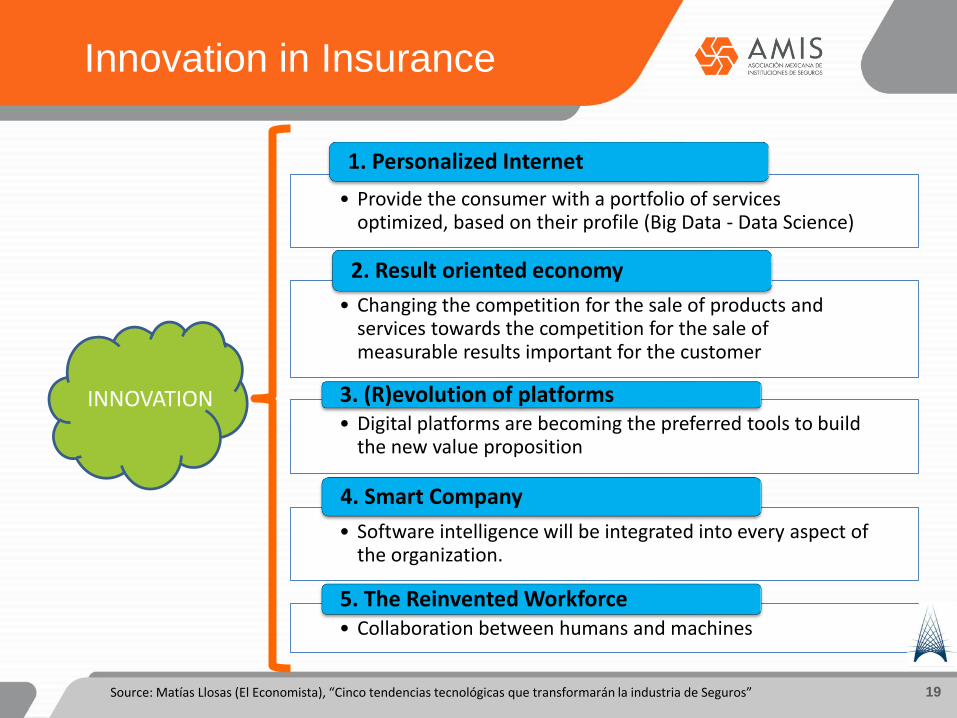

• Provide the consumer with a portfolio of services optimized, based on their profile (Big Data - Data Science)

1. Personalized Internet

• Changing the competition for the sale of products and services towards the competition for the sale of measurable results important for the customer

2. Result oriented economy

• Digital platforms are becoming the preferred tools to build the new value proposition

3. (R)evolution of platforms

• Software intelligence will be integrated into every aspect of the organization.

4. Smart Company

• Collaboration between humans and machines

5. The Reinvented Workforce

Source: Matías Llosas (El Economista), “Cinco tendencias tecnológicas que transformarán la industria de Seguros”

Innovation in Insurance

INNOVATION

20

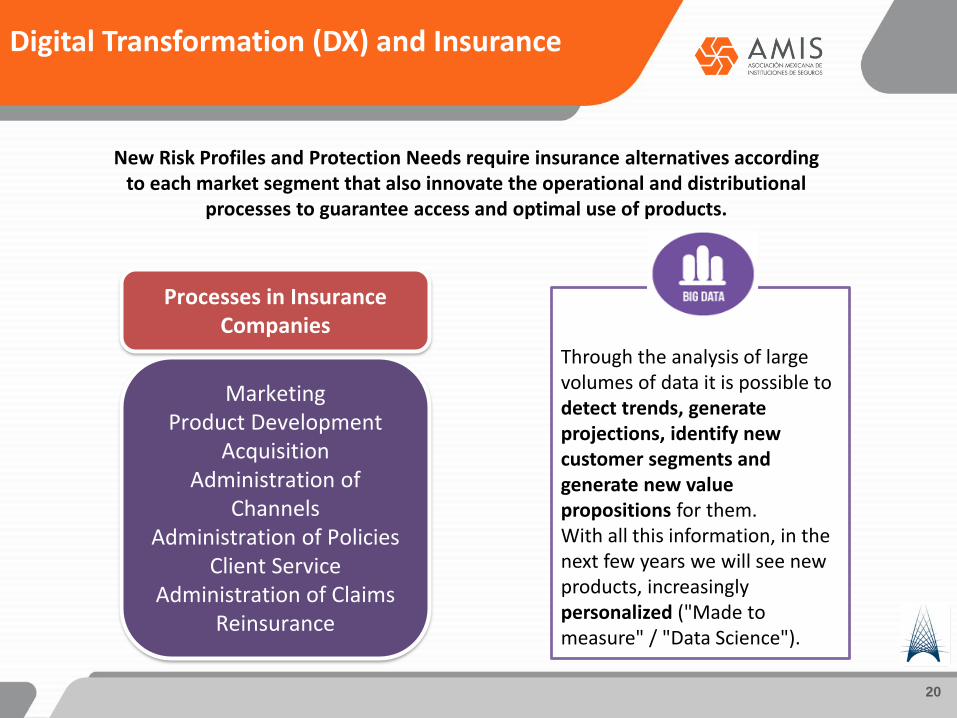

Digital Transformation (DX) and Insurance

New Risk Profiles and Protection Needs require insurance alternatives according to each market segment that also innovate the operational and distributional

processes to guarantee access and optimal use of products.

MarketingProduct Development

AcquisitionAdministration of

ChannelsAdministration of Policies

Client ServiceAdministration of Claims

Reinsurance

Processes in Insurance Companies

Through the analysis of large volumes of data it is possible to detect trends, generate projections, identify new customer segments and generate new value propositions for them.With all this information, in the next few years we will see new products, increasingly personalized ("Made to measure" / "Data Science").

21

Customized offersTr

adit

ion

al o

ffer

s

• Insured decides product type and coverages

• Insurer calculates premiums

Inn

ova

tive

off

ers • Insured decides needs,

product type and premiums

• Insurer offers different alternatives (products and coverages) within the maximum price (budget) established by the client

22

Industry Trends

Source: SAP, “Insurance: Preparing insurers for the digital century”

23

Life Events ("Lifestyle")Product Design for those needs

Life

Buying a carChanging

work

Wedding

Buying a house

Birth

Vacations

DivorceUniversity

Disability

Loss

Unemployment

Natural catastrophe

Retirement

24

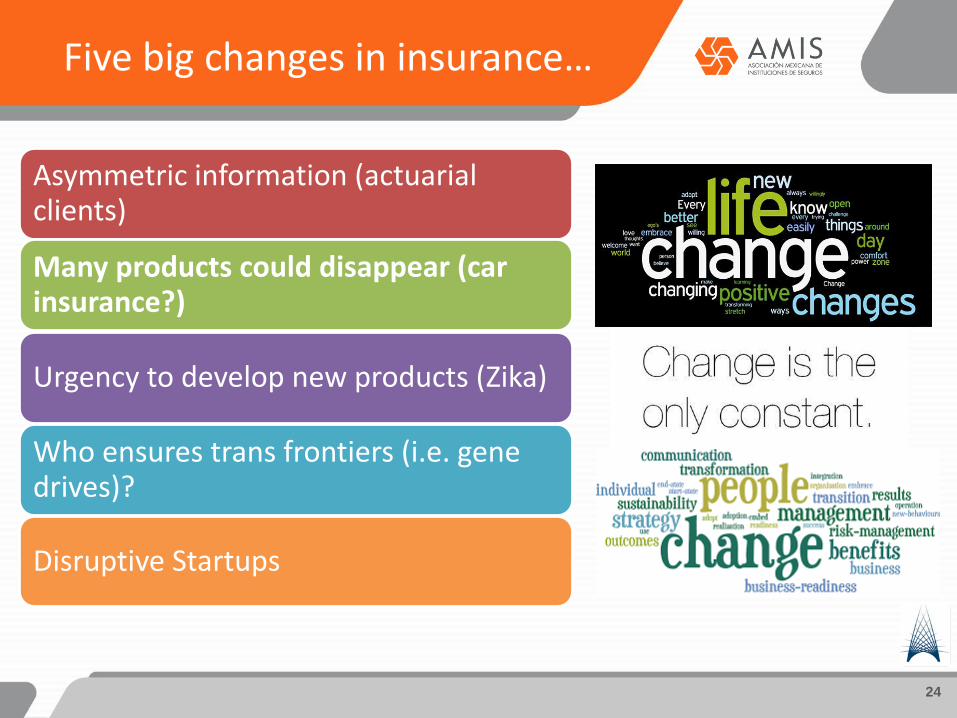

Five big changes in insurance…

Asymmetric information (actuarial clients)

Many products could disappear (car insurance?)

Urgency to develop new products (Zika)

Who ensures trans frontiers (i.e. gene drives)?

Disruptive Startups

25

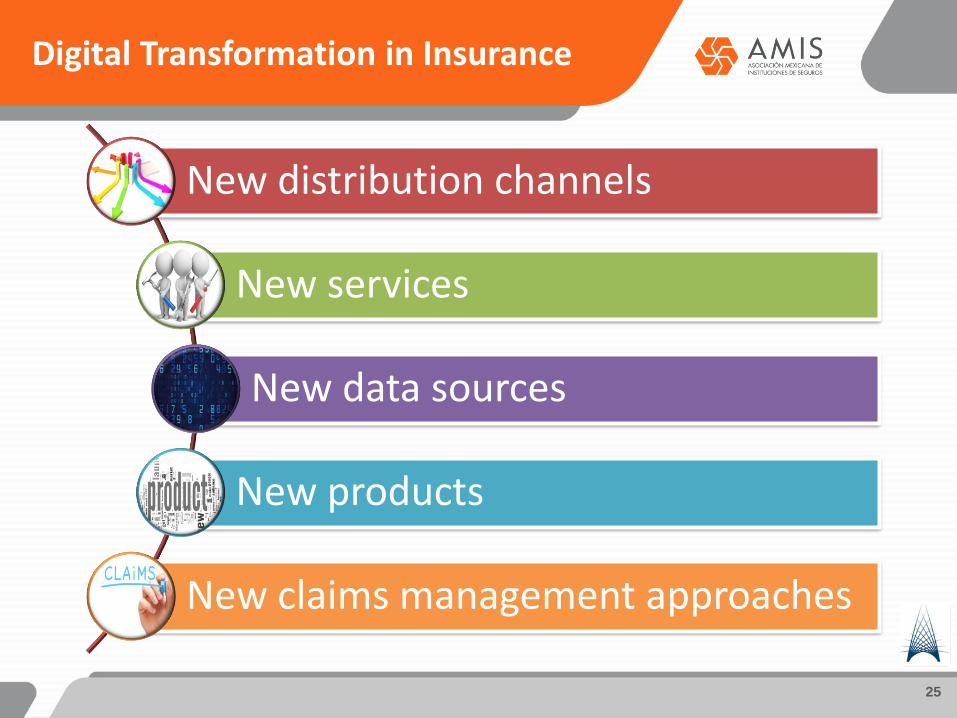

Digital Transformation in Insurance

New distribution channels

New services

New data sources

New products

New claims management approaches

26

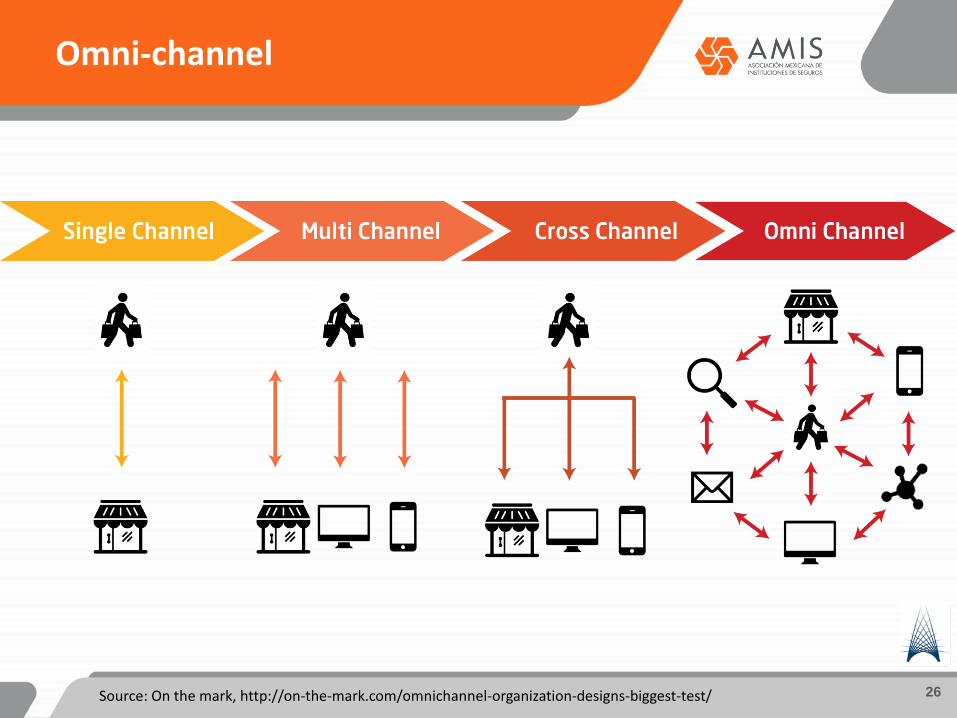

Omni-channel

Source: On the mark, http://on-the-mark.com/omnichannel-organization-designs-biggest-test/

27

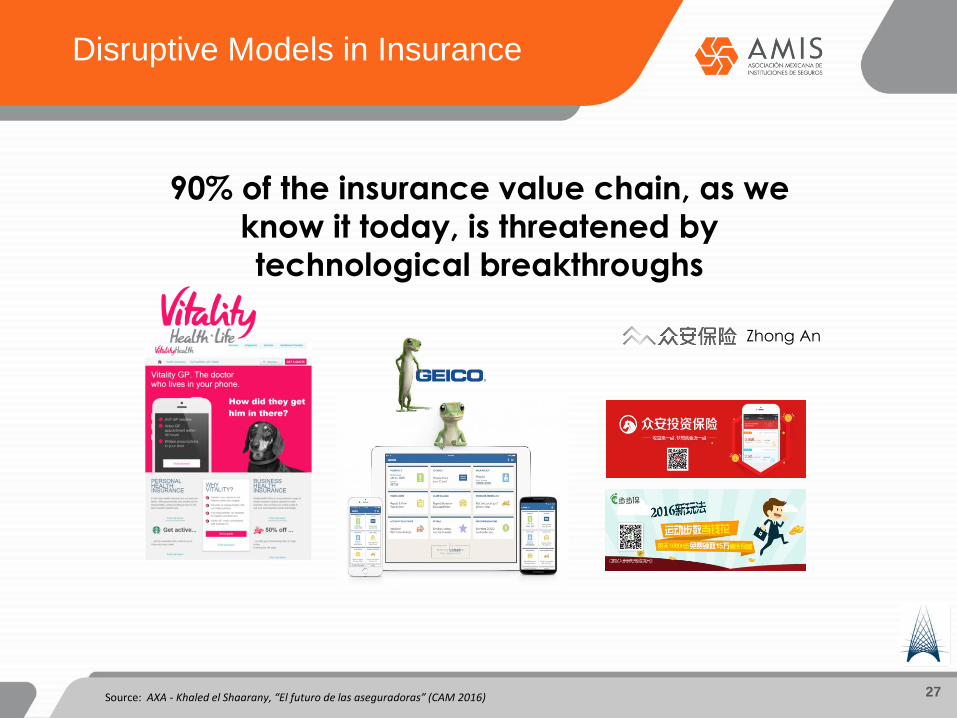

Zhong An

90% of the insurance value chain, as we

know it today, is threatened by

technological breakthroughs

Source: AXA - Khaled el Shaarany, “El futuro de las aseguradoras” (CAM 2016)

Disruptive Models in Insurance

28

Wibe Flexible Car Insurance

Coverage in 5 minutes

Source: Wibe, “Seguro de autos Wibe”, https://www.wibe.com/seguros-auto/

29

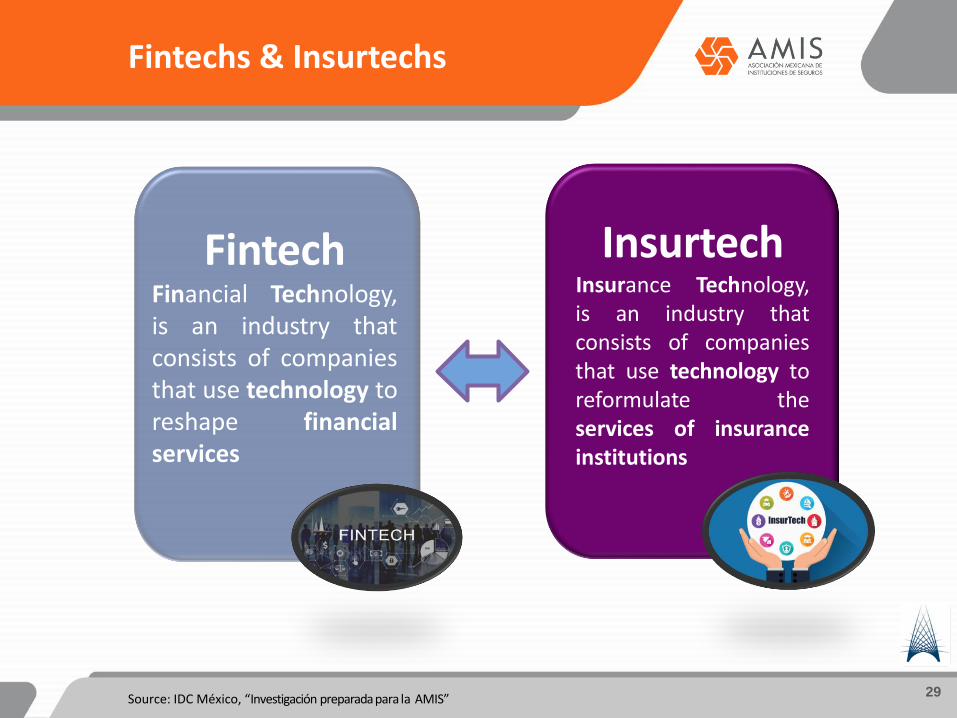

FintechFinancial Technology,is an industry thatconsists of companiesthat use technology toreshape financialservices

InsurtechInsurance Technology,is an industry thatconsists of companiesthat use technology toreformulate theservices of insuranceinstitutions

Source: IDC México, “Investigación preparada para la AMIS”

Fintechs & Insurtechs

30Source: PwC 2016GenRe, Future of Insurance

Impact of Fintechs

31Source: Hayman, Alexander, Swiss Finance and Technology Association

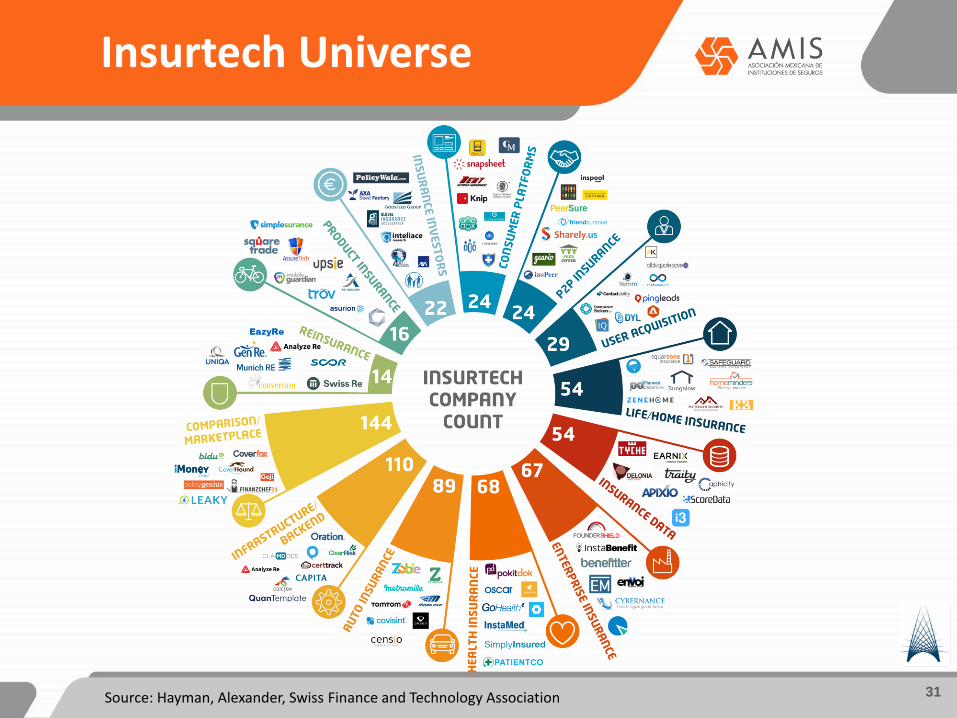

Insurtech Universe

32

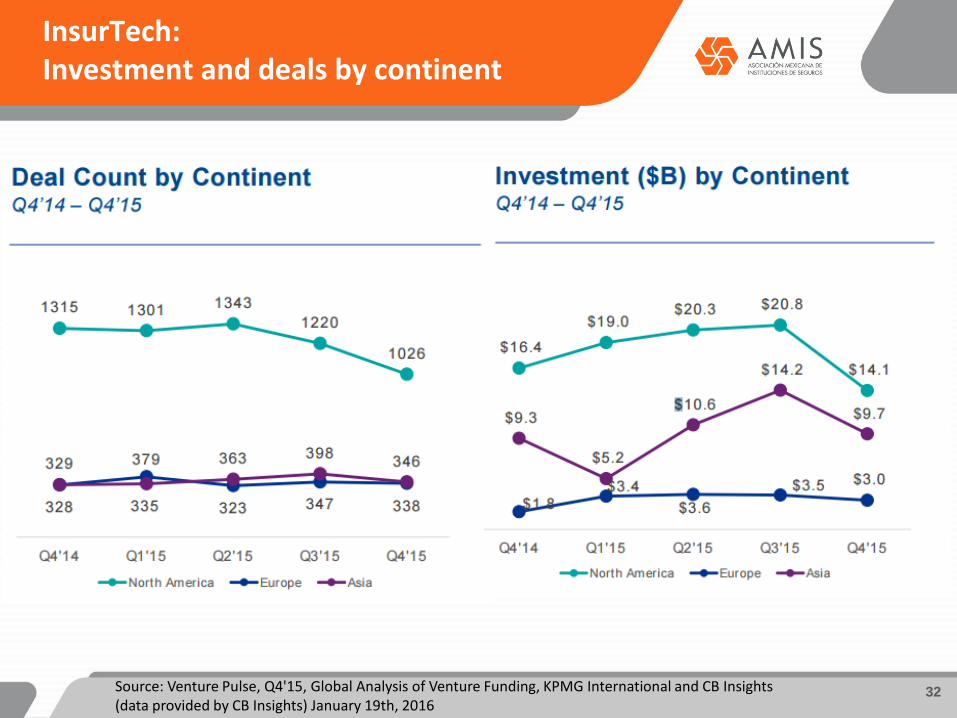

InsurTech:Investment and deals by continent

Source: Venture Pulse, Q4'15, Global Analysis of Venture Funding, KPMG International and CB Insights (data provided by CB Insights) January 19th, 2016

33

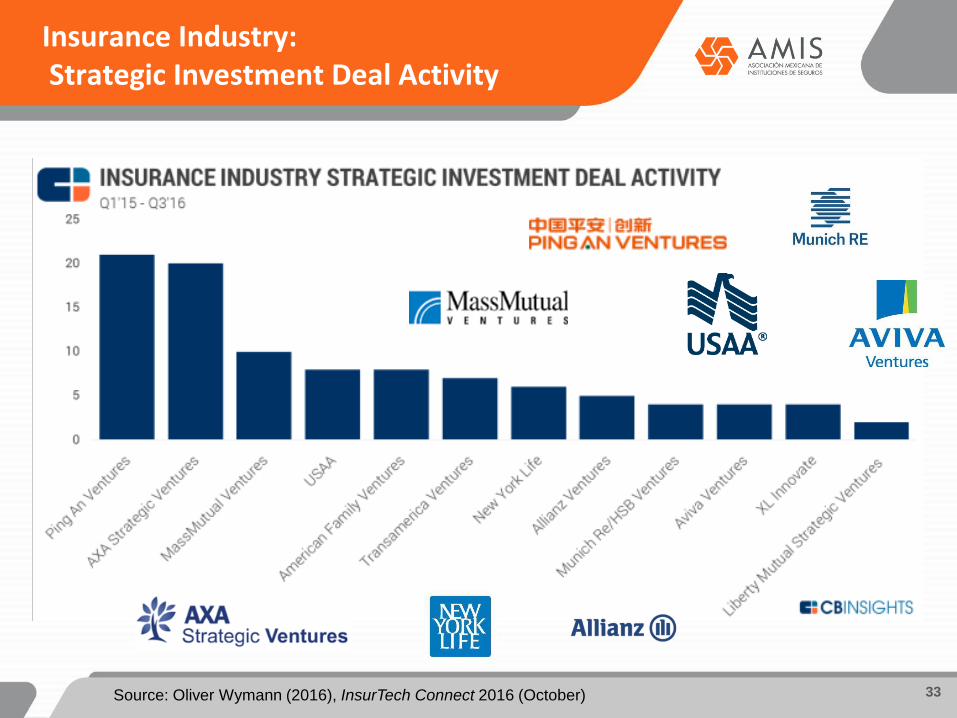

Insurance Industry:Strategic Investment Deal Activity

Source: Oliver Wymann (2016), InsurTech Connect 2016 (October)

34

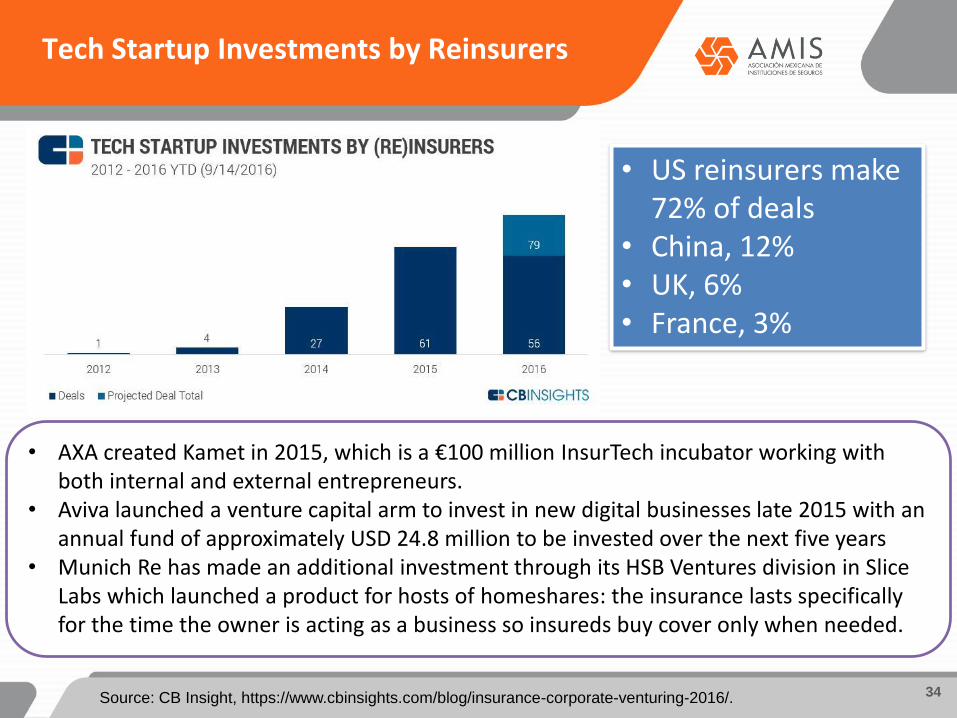

Tech Startup Investments by Reinsurers

Source: CB Insight, https://www.cbinsights.com/blog/insurance-corporate-venturing-2016/.

• US reinsurers make72% of deals

• China, 12%• UK, 6%• France, 3%

• AXA created Kamet in 2015, which is a €100 million InsurTech incubator working with both internal and external entrepreneurs.

• Aviva launched a venture capital arm to invest in new digital businesses late 2015 with an annual fund of approximately USD 24.8 million to be invested over the next five years

• Munich Re has made an additional investment through its HSB Ventures division in Slice Labs which launched a product for hosts of homeshares: the insurance lasts specifically for the time the owner is acting as a business so insureds buy cover only when needed.

35

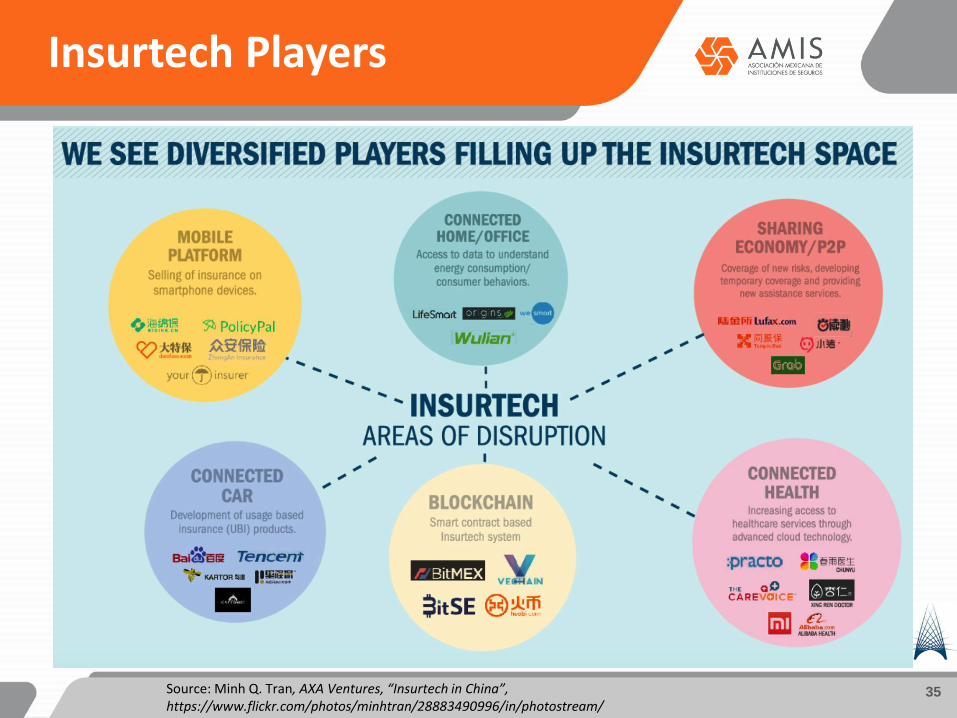

Insurtech Players

Source: Minh Q. Tran, AXA Ventures, “Insurtech in China”, https://www.flickr.com/photos/minhtran/28883490996/in/photostream/

36

Insurtechs

Insurtechs Distributors

• They are allies and very powerful tools for the distribution of insurance products.

• Traditional insurers should have a digital strategy and develop their Insurtech for digital distribution, or partner with new or existing Insurtechs.

• They are also technological platforms for "Data Science" and for providing additional services such as health care.

Insurtechs “Carriers”

• Disruptive models can be the "Uber of insurance", if they are carriers, regardless of regulation, without solvency or reserve requirements, and without supervision and surveillance.

• Acting in a multinationalenvironment and the cloud.

• A regulation for these models is indispensable, from IAIS, IMF, and FSB. Request from GFIA and FIDES.

• “Same rules for same activities” principle.

37

Acknowledging that technological advances are having a significant effect on the insurance industry, current insurance legislation and regulations could limit the capabilities of insurers in some jurisdictions to fulfill their potential.

The pace of policy and regulations should match the speed of technological changes.

We also warned against government responses that create a two-tier system of regulations, whereby established insurers are at a disadvantage relative to start-ups.

Some insurers have expressed interest in the development of a regulatory “sandbox,” whereby regulatory standards are relaxed to encourage the development of innovative products that benefit both insurers and consumers. However, for this sandbox to work, it would be vital to maintain a level playing field between incumbents and new entrants.

Source: GFIA President’s Newsletter, February 2017, and GFIA position paper to OCDE

Insurtechs Regulation GFIA Position to OECD

38

Financial technology law:Regulate financial activities that are operatedthrough the following platforms:

1. Crowdfunding.

2. Electronic money.

3. Virtual Assets and Experimental Platforms.

4. Insurtechs

Mexican Fintech Project Bill

AMIS Hackathon

40

Objectives and Challenges

Bring the start uppers closer to our industry.

Promote a community of technological

start uppers (entrepreneurs) specialized

in insurance.

Educate the industry about the importance of innovation to reach new customers and face the technological revolution

Permanent and innovative contact with client when issuing policies and claim processing.

Simplify the processes of underwriting and issuing policies.

Improve loss indicators and client services (apps, Big Data, A.I., etc.)

Access to policy information at any time and any place with the digital signature

Improve the claims management process (issue, registration, compensation)

Homogenization of all distribution channels and generate financial inclusion with microinsurance.

Prevent risks through the IoT (apps, health wristbands, etc.)

41

Technological revolution changes paradigms

Rate of change accelerating

Need to focus on the customer

Use technologies to ensure survival and generate value and growth

Conclusions

42

“Neither the technology nor the disruption associated with it is anexogenous force over which humans have no control. We are allresponsible for guiding its evolution in the decisions we make every dayas citizens, consumers and investors. We must seize the opportunity andpower we have to shape the Fourth Industrial Revolution and direct ittowards a future that reflects our goals and values [...] In the end,everything is reduced to people and values. We need to shape a futurethat works for all by putting people first and empowering them. In itsmost pessimistic and dehumanized form, the Fourth IndustrialRevolution has the power to "robotize" humanity and deprive it of itssoul and heart. But as a complement to the best part of human nature -creativity, empathy, and manageability - it can lift humanity toward anew collective moral consciousness based on a shared sense of ourdestiny.”

Klaus Schwab, President and Founder of the World Economic Forum

Reflection

43

The biggest danger is not that our goal is too high or we do not achieve it, but that it is too low and we achieve it.

Michelangelo Buonarroti