deloitte_gfsi 1103 basel iii pov bank capital landscape 2012 03

TRANSCRIPT

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 1/53

Deloitte perspectivesBasel III: Transforming the bank

capital landscape

March 2011

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 2/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.1 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

What is Basel III 2

Basel III overview 9

Financial services industry impacts 23

Implementation considerations 32

Client focus — Preparing for change 40

Why Deloitte?

A leader in bank capital 45

Americas contacts 51

Table of contents

As used in this document, “Deloitte” means Deloitte LLP and its subsidiaries. Please see www.deloitte.com/us/about for a

detailed description of the legal structure of Deloitte LLP and its subsidiaries.

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 3/53

What is Basel III ?

• Evolution of Basel III guidance

• Scope of Basel III

• Timeframe for Basel III implementation

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 4/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.3 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• “Basel III” refers to guidance issued by Basel Committee for BankingSupervision (BCBS) as a comprehensive response to the global credit crisis.Basel II and Basel III, together, replace most elements of Basel I.

• Basel III formalizes the April 2008 recommendations of the Financial StabilityForum (FSF) and the G20's November 2008 action plan.

• Also includes revisions to the market risk rules.

– European Union (EU) Capital Requirements Directive (CRD) implemented the 2005market risk rules, but the revisions were not incorporated in the U.S. rules.

– EU will only have to implement additional changes to the market risk rules.

Evolution of Basel III guidance

Relative to Basel II, international rules for

Basel III have been finalized

over a relatively short period.

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 5/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.4 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• Basel III development – Revisions to Basel framework

– Capital and liquidity consultative papers issued

– Quantitative impact study (QIS) conducted in early 2010

– Revised Basel III guidance issued

– Basel committee agreement announced in Sep.

– Ratification at the G20 meeting in Seoul in Nov.

– Final BCBS rules released mid-December 2010

– Implementation timeframe occurs between2012–2018

Evolution of Basel III guidance (cont.)

QISQIS Result s

Jul’09 Dec’09 Apr’10 Jul’10 Sep’10 Nov’10 Dec’10

• Individual countries can now start the rule-making process

– Several areas in the rules for local regulators/national discretion – Likelihood of divergences from Basel Committee’s final guidance

With international guidance largely finalized,

rule making in individu al jurisdictions is

expected to be in fluenced by local

regulatory and political landscape.

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 6/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.5 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

The core of the Basel III framework is revised capital standards, stronger capitaldefinitions, and systemic risk overlays along with a new international frameworkfor liquidity risk.

Evolution of Basel III guidance (cont.)Basel III final guidance consolidates several BCBS items

Enhancements to the

Basel III framework

Revisions t o Basel III

market ris k f ramework

Guidelines for incremental

risk charge (IRC) calculati on

Principles for

sound liquidity risk

management

International

LRM framework

Strengthening the

resilience of the

banking sector

Regulators’

consensus July 26,

2010

Capital calibration

September 12, 2010

Requirements for liquidity risk, a subject of

debate over the years, makes it appearance

in Basel III, with possibly far-reaching

implications.

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 7/53Copyright © 2011 Deloitte Development LLC. All rights reserved.6 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• Basel III is incremental to Basel II; together, Basel III and Basel II replaceBasel I.

• Basel II implementation continues in the U.S with several core* banks in parallelreporting.

• The scope of Basel III is comprehensive and far reaching

– Capital — Quality and transparency

• Revised capital definitions to improve quality of capital, additional Buffers, andenhanced minimum capital standards.

– Leverage ratio

• An international leverage ratio has been defined.

Scope of Basel III

Capital Leverage ratioCredit & market

riskLiquidity risk

Basel III is no t a replacement for Basel II

* Large U.S. Bank hol ding companies that meet the U.S. regulatory criteria for

the Basel II implementation

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 8/53Copyright © 2011 Deloitte Development LLC. All rights reserved.7 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• The scope of Basel III is comprehensive and far reaching (cont.) – Credit and market risk revisions

• Changes to counterparty credit risk rules, re-securitization exposures, use of externalratings, etc.

• Extensive revisions to market risk rules — incremental risk charge (IRC), stressedvalue at risk (VaR), and trading book securitizations.

– Liquidity risk• A new framework for liquidity risk measurement, standards, and monitoring.

• Several provisions of the Dodd-Frank legislation may shape U.S. regulatorystandards for common Basel III elements.

– Systemic risk (systemicly important financial institution or SIFI) designations

– Orderly liquidation authority (living wills)

– Volcker rule on proprietary trading

– Collins amendment on bank capital

– Credit retention requirements on securitizations

– Credit rating agencies regulation

– Derivatives clearing

Scope of Basel III (cont.)

In the U.S., the Dodd-Frank legislation wi ll

impact implementation of Basel III.

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 9/53Copyright © 2011 Deloitte Development LLC. All rights reserved.8 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

Time frame for Basel III implementation

All dates as of Jan 1 2011 2012 2013 2014 2015 2016 2017 2018 2019

Regulatory adjustments to

common equity20% 40% 60% 80% 100% 100%

Capital instruments that no

longer qualifyPhased out over 10 yrs, beginning 2013

Capital conservation buffer 0.625% 1.25% 1.875% 2.50%

Minimum common equity

capital ratio1

3.5%(3.5%)

4.0%(4.0%)

4.5%

(4.5%)4.5%

(5.125%)4.5%

(5.75%)4.5%

(6.375%)4.5% (7.0%)

Minimum Tier 1 capital14.5%

(4.5%)5.5%

(5.5%)6.0%

(6.0%)6.0%

(6.625%)6.0%

(7.25%)6.0%

(7.875%)6.0% (8.5%)

Minimum total capital18.0%

(8.0%)8.0%

(8.0%)8.0%

(8.0%)8.0%

(8.625%)8.0%

(9.125%)8.0%

(9.875%)8.0% (10.5%)

Leverage ratio Supervisory monitoring3%

(Parallelrun)

3%

3%(Disclosure

starts)3%

3% (re-calibration)

Migration toPillar 1

Liquidity coverage ratioObservation

periodStart

Net stable funding ratioObservation

periodStart

Market risk-weighted assets

(RWA) changesStart

Credit RWA changes Start

1 Amount in bracket includes conservation buffer

Many banks have already announced strategic actions to

mitigate adverse capital impacts from Basel III, and intent to

meet targets in advance of deadlines.Final level of capital ratios including conservation buffer

Initial implementation date for target minimum capital and leverage ratio

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 10/53

Basel III overview

• Capital

• Leverage ratio

• Market and credit risk revisions

• Liquidity framework

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 11/53Copyright © 2011 Deloitte Development LLC. All rights reserved.10 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

Shift in regulatory mindset

• Many banks received public sector support to avoid failure.

• Losses were borne by the common equity holders, and not other Tier 1 and Tier 2 components.

• Basel III is designed to require that common equity is the dominant component of capital, other regulatorycapital instruments are converted into equity, if a bank is deemed non-viable.

Stronger

capital

Buffer for

stress

conditions

Counter

cyclical buffer

SIFI surcharge

Macro

prudentialoverlays for

system risk

• Capital conservation buffer of 2.5% to withstand future periods of stress.

• Regulators can impose restrictions on bank’s ability to distribute earnings, i.e., dividends, sharebuybacks, when capital levels fall below buffer.

• Supervisors may impose time limits on a bank to exit the buffer range.

Addit ional macro-prudent ial overlay to address Systemic r isk: risk of financial system disruptions

that can impact th e broader economy.

• A capital overlay of 0 — 2.5% can be imposed to dampen excessive credit growth.

• Objective is to reduce pro-cyclicality.

• Buffer would build up during periods of excessive credit growth, and can be released during a down cycle.

• Applied to largest financial firms that are interconnected due to common exposures, and posedisproportionate level of systemic risk.

• National supervisors to establish systemic capital surcharge, recommended range 0–3%.

More Capital • More capital, i.e., higher minimum capital standards.• Increases minimum capital ratios for Tier 1 and Tier 1 common, while Tier 2 remains same.

Tier 1 Common equity requirements for the

largest banks in some jurisdict ions could

approach double digits .

Capital

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 12/53Copyright © 2011 Deloitte Development LLC. All rights reserved.11 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• Strengthening the definition of capital, focusing onits overall quality, consistency, and transparency.

• Higher capital standard that promotes long-termstability and sustainable growth.

• Regulatory capital must be simple andharmonised across jurisdictions.

Basel III capital measures focus on quality andtransparency

Components of capital

Tier 1 capital s trengthened

Tier 2 capital simplified

Tier 3 capital abolished

Tier 1 — Going-concern capital

• Predominantly common equity.

• High-quality capital capable of absorbing losses.

• Subordination to all claims in liquidation, no repurchaseobligation or mandatory dividend, etc.

• Noncommon equity criteria: senior and distributionpreference only to common equity; callable only after fiveyears; principal repayment subject to regulatoryapproval, etc.

Tier 2 — Gone-concern capital

• Subordinate to depositors and all creditors; can’t besecured or covered by issuer guarantee; callable afterfive years; no accelerated credit feature.

• Restriction that Tier 2 cannot exceed Tier 1 is eliminated.

Exclusion of several instruments from Tier 1

capital may alter the capital structure

at many banks.

• A full reconciliation of regulatory capitalelements back to the balance sheet in theaudited financial statements is required.

Capital

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 13/53Copyright © 2011 Deloitte Development LLC. All rights reserved.12 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

Tier 1 Capital• Common equity will be the predominant form of Tier 1, with specific minimum

requirements.

• Perpetual preferred stock can remain in Tier 1.

• Tax advantaged hybrid securities mostly excluded.

– Step-up convertibles (due to incentives to redeem, else rates go up). – Cumulative preferred (due to full access to cancelled dividends).

– Trust preferred (due to maturity date, payments are noncancellable and lack of lossabsorption).

Tier 1 capital — What is in and what is out

While Basel II scope in the U.S. is limited to

“ core” banks only, Basel III changes in

capital definition, deductions, and filters

should apply to banks more broadly.

Capital

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 14/53Copyright © 2011 Deloitte Development LLC. All rights reserved.13 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

Tier 1 and Tier 1 common adjustments• A series of adjustments and filters are applied to book equity to determine Tier 1

common equity; Some, of the adjustments are similar to those under Basel I.

Tier 1 capital — What is in and what is out (cont.)

Deferred tax assets

(DTA)

Mortgage servicing

rights (MSR)

Investments in financial

institutions

AFS unrealized gains

and losses

Defined benefit pension

assets

Minority Interest

Allowance for loan and

lease losses

vs. ECL

Goodwill and other

intangibles

Fair value option changes

due to own credit risk

Nonfinancial equity

investments

Insurance subsidiaries

50/50

deductions

Similar to current adjustmentsDeducted from Tier 1 commonLimited to 10% individually

And 15% in aggregate

Capital

Individual and aggregate limits on inclusion

of certain it ems from Tier 1 may have

significant impli cations for U.S. banks

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 15/53Copyright © 2011 Deloitte Development LLC. All rights reserved.14 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• As part of Basel III framework, a nonrisk-based leverage ratio is introduced as asupplementary measure or a “backstop” to the risk-based capital (RBC) ratios.

• The objective of leverage ratio is to constrain the build up of leverage in thesystem, irrespective of risk sensitivity.

• Minimum leverage ratio is set at 3%.

• Gross Exposure includes on balance sheet assets (book value) and off balancesheet times translated to balance sheet equivalent.

– Unused credit card commitments converted at 10%, all other commitments at 100%.

• In contrast to Europe, U.S. banks have traditionally been subject to a leverageratio requirement.

• Credit card banks and trading operations are more adversely affected byleverage measure.

Leverage ratio is introduced as a supplementarymeasure

Leverage ratio

Tier 1 capital

Gross exposure

Leverage ratio requirements h ave been

in place in U.S.; hence this may no tpose issues for U.S. banks, and in light

of high common equity targets.

=

Leverage

ratio

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 16/53Copyright © 2011 Deloitte Development LLC. All rights reserved.15 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

Revisions to Basel II framework were intended to eliminate capital arbitragebetween the banking book and trading book, and signif icantly expand

capital charges for certain products, practices, and activit ies.

Market and credit risk revisions

Market risk revisions

• Inclusion of Stressed VaR in internal models approach.

• Banking book risk weights for securitization exposures in the trading book.

• IRC for credit risk from default and migration.

Credit risk refinements

• Higher asset value correlation multiplier for exposure to large, or unregulated, financialfirms.

• Enhance methodologies to calculate counterparty

credit risk (CCR), and CCR managementpractices.

• Higher risk weights for re-securitization exposures.

• Reduced reliance on external ratings.

Pillar 2 and 3 changes• Enhanced governance of securitization related risks, compensation practices, etc.

• Detailed disclosure of securitization activities.

Market risk capital can possibly

increase by 2–4 X leading to smaller

trading book.

Significant credit risk capital

increases for securitizations andcapital market produ cts are likely to

lead to reduced activity and squeeze

profitability.

Credit and

market r isk

C dit d

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 17/53Copyright © 2011 Deloitte Development LLC. All rights reserved.16 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• In 1996, BCBS published amendment to the 1988 Basel I capital accord toincorporate market risk rules. The Market Risk Amendment finalized in 1997,introduced two key approaches to capture market risk for trading positions:

– Standardized measurement method

– Internal Models Approach (IMA)

• Market risk rules were again revised in 2005 to

incorporate the following changes: – Enhancements to the treatment of specific risks, including the introduction of

incremental default risk

– Specific capital treatment for failed and unsettled transactions

Market risk background and evolution

U.S. rule making on market risk has

been slower relative to Europe.

Credit and

market r isk

C dit d

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 18/53Copyright © 2011 Deloitte Development LLC. All rights reserved.17 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• In 2009, BCBS published revisions to the market risk framework in response tothe financial crisis which have now been incorporated in Basel III forimplementation by 2012. Key changes include:

– Introduction of IRC to capturedefault and migration risk under IMA for unsecuritizedproducts.

– Banking book charges for specific r isk of securitization exposures in the tradingbook.

– Introduction of stressed VaR measure in addition to existing VaR calculations.

– Conservative treatment of correlation trading portfolios.

– Increased frequency of data updates from every three months to monthly.

– More stringent guidance around treatment and valuation of illiquid positions.

• The 2005 changes were implemented in Europe as part of Basel II, but notin the U.S.

– U.S. Regulators issued market risk Notice for Proposed Rulemaking in December 2010,which consolidates the 2005 BCBS rules with the 2009 revisions.

Market risk background and evolution (cont.)

Credit and

market r isk

U.S. rule making on market risk has

been slower relative to Europe.

C dit d

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 19/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.18 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

Stressed VaR and IRC will likely lead to much highercapital for market risk

Incremental risk charge

IRC definition

• Captures potential for loss from an obligor’s defaultand credit migration risk.

IRC scope

• Positions subject to interest rate risk under IMAapproach, excluding securitizations and creditdefault swap.

Requirements Highlights

• Measured at 99.9% confidence level over one yearhorizon considering market liquidity.

• Liquidity horizon has a floor of three months

• Includes correlations in default and migrationsamong borrowers, but excludes diversification withother trading positions.

• Incorporates issuer and market concentration risks.

• Extensive model validation requirements related todesign, testing and maintenance, with emphasis onstress testing, scenario analysis and sensitivityanalysis.

Capital

charge

VaR

Multiplication

factor mb

VaR

Multiplication

factor mb

Stressed VaR

×

Multiplication

factorm

Newly

introduced

capital charge

Current Revised

Add on st ressed VaR

capital chargeCurrent formula

Multiplication

factors may be

different

3 mb

m 3

VaR is measured over a 99% conf idence interval

over a 10-day period.

• The 12-month stress period likely corresponds to2007-08 period with extreme volatility and largelosses.

Stressed VaR

Credit and

market r isk

Credit and

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 20/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.19 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

Significant revisions to Basel II framework for securitizations were finalized in July 2009 impacting all three pillars. The

December 2010 publication finalizes changes to counterparty credit risk rules. All changes are targeted for implementationby December 2011. Key provisions are summarized below:

Credit risk changes impact securit izations andcounterparty risk

Securitizations

• Resecuritizations defined to include collateralized debt obligations (CDOs) and liquidity facilities to asset-backedcommercial paper programs, and higher risk weights established.

• Banks not permitted to use external rating that benefit from self guarantees. Such exposures in the trading book have acapital requirement no less that that when held in the banking book.

• Must perform credit analysis of securitization exposures instead of solely relying on rating agency conclusions.

• Banks must have continuous access to up-to-date performance information for all underlying pools of their securitizationexposures, both in banking or trading book.

• Very conservative treatment for securitization liquidity facilities.

• Eliminates favorable treatment for market disruption liquidity facilities.

Counterparty

credit risk

• Inputs for counterparty credit risk (CCR) capital to be based on stressed inputs, so EPE calculations to include datareflecting periods of stress.

• Improve exposure at default (EAD) calculation to promote more robust collateral management practices.

• Higher asset value correlation for exposures to large (>$100Bn), or unregulated, financial firms.

• Extend margin period of risk for transactions to large netting sets

• Includes capital add-on charge for potential mark-to-market losses, i.e., credit valuation adjustments (CVA).

• Include an explicit capital-charge under Pillar 1 for specific wrong-way risk.

• Increase incentives for firms to use clearinghouse counterparties, which get a nominal RWA.

Other changes cover Pillar II and III and include items such as more rigorous stress testing and validation standards,

more active monitoring of concentration r isks, and inclusion of any incremental securitization risks in Pillar II,

increased disclosure requirements related to sponso rship o f off balance sheet vehicles, and conduit p rograms.

Credit and

market r isk

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 21/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.20 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• The core of the framework consists of two liquidity measures calibrated toaddress stressed conditions.

• These ratios have been developed to achieve two separate but complementaryobjectives.

• Liquidity coverage ratio

– Objective is to promote short-term resiliency with sufficient high-quality liquid

resources.

• Net stable funding ratio

– Objective is to promote medium-and-long term resiliency by creating additionalincentives for funding with more stable sources.

• The framework also proposes four metrics for liquidity monitoring

– Contractual maturity mismatch – Funding concentration

– Available unencumbered assets

– Market-related monitoring tools (not bank specific)

• Public disclosure

Basel III introduces global standards for liquidity for thefirst time

Global liquidity standards that have been

finalized with Basel III have the potential to

alter the cost and structure of bank funding.

Liquidity risk

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 22/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.21 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

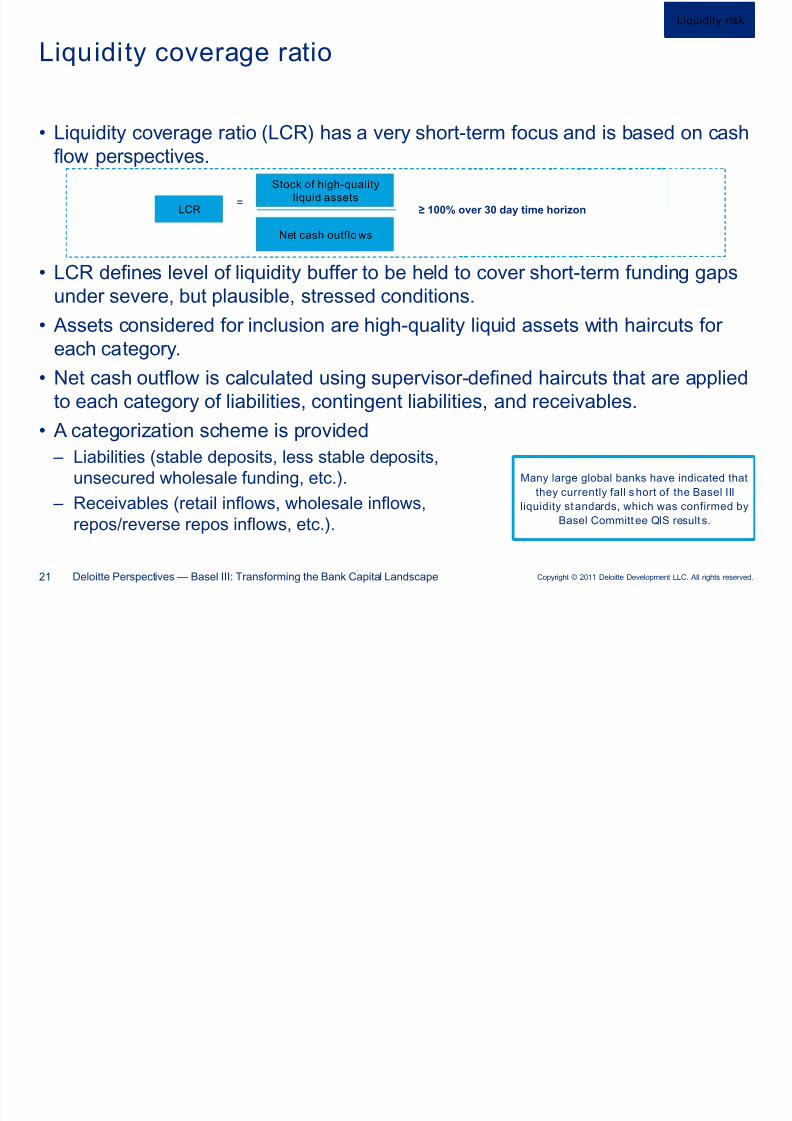

• Liquidity coverage ratio (LCR) has a very short-term focus and is based on cashflow perspectives.

• LCR defines level of liquidity buffer to be held to cover short-term funding gapsunder severe, but plausible, stressed conditions.

• Assets considered for inclusion are high-quality liquid assets with haircuts foreach category.

• Net cash outflow is calculated using supervisor-defined haircuts that are appliedto each category of liabilities, contingent liabilities, and receivables.

• A categorization scheme is provided

– Liabilities (stable deposits, less stable deposits,unsecured wholesale funding, etc.).

– Receivables (retail inflows, wholesale inflows,repos/reverse repos inflows, etc.).

Liquidity coverage ratio

LCR

Stock of high-quality

liquid assets

Net cash outflo ws

=≥ 100% over 30 day time horizon

Many large global banks have indicated that

they currently fall short of the Basel III

liquidity st andards, which was confirmed by

Basel Committ ee QIS results.

Liquidity risk

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 23/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.22 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• Net stable funding ratio (NSFR) is a medium-to-long term measure and has abalance sheet focus.

• NSFR defines minimum acceptable amount of stable funding in an extendedfirm-specific stress scenario.

• Amount of stable funding is defined as various categories of funding sources,and their applicable haircuts.

– e.g. capital, stable retail deposits, less stable retail deposits, etc.

• Required stable funding is calculated by applying fixed factors to various definedcategories of assets and contingent liabilities.

• NSFR was recalibrated in the BCBS final rules.

– e.g., cash, loans and securities with maturities < 1 year,marketable securities, etc.

Net stable funding ratio

Many European banks with large retail

deposit franchises, may be slightly better

positioned than U.S. counterparts.

Liquidity risk

NSFR

Available amount o f

stable funding

Required amount of

stable funding

=≥ 100% over 1 year

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 24/53

Financial services

industry impacts

• Key areas of impact

• BCBS QIS summary

• Basel III international comparisons

• Expected industry trends inresponse to Basel III

Basel II

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 25/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.24 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• Due to its broad scope and reach, Basel III is expected to have a transformativeeffect on the banking industry landscape, especially the large, global institutions.For these firms, Basel III will likely impact:

– Strategic decisioning

– Tactical near-term choices

– Infrastructure and operations

• Some potential implications from the evolving bank capital regulatory standardsare shown below:

• The extended implementation timeframe allows for an orderly approach totransition to target state.

Basel III has significant potential implications for banks

Return on equity

cost of capitalSimpler capital

structure

Financial crossholdings/ownership

Largebankingmergers

OTC, CDOs,repos, PB, and

correlation trading

Pricing for tradefinance products

Competition for retaildemand and term

deposits

Fee-based businesses

Off balance sheetproducts such asguarantees and

contingent credit lines

TB and BBsecuritizations

Wholesale short-termfunding costs

Credit card limits,home equity lines and

personal LOCs

Clearinghousesettlement volumes

Mortgage servicingrights

Rating agency roleand influence

Inter-banktransactions

Collateral andmargin

Basel II

impacts

Basel III

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 26/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.25 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• BCBS conducted a comprehensive study to understand the impact of the BaselIII guidance, including changes to RWA from market risk and creditrisk revisions.

• Results summarized for Group 1 (i.e., international banks with greater than 3billion euros in Tier 1 capital as of Q4 2009) and Group 2 banks (all otherparticipating banks).

– 13 U.S. banks were included in the study, all Group 1

• Basel III rules applied on a pro-forma basis assuming full implementation basedon December 31, 2009, data.

Results of Basel Committee Quantitative Impact Study

Large, internationally active banks w ith

sizeable capital markets portfolios have the

potential to be adversely affected by Basel

III, according to the BCBS QIS.

Basel III

impacts

Basel III

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 27/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.26 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• Highlights of QIS study and key findings – Large global banks far more adversely effected than smaller banks; this result isconsistent for capital ratios, leverage ratio, liquidity ratios and RWA changes.

– For Group 1 banks, Common equity Tier 1 (CET1) ratio drops from 11.1% to 5.7% whenBasel III definition of capital used, and filters and deductions applied, to common equity,along with RWA changes due to market risk and credit risk revisions.

– Relative to 7% CET1 standard, banks have a shortfall of $577 billion to be addressedthrough 2019. BCBS noted that net income after taxes at Group 1 banks for 2009 was209 billion euros.

– Average leverage ratio for large banks was 2.8% while smaller banks, at 3.8%, werewell above minimum requirement of 3%.

– Liquidity ratio requirements create a significant funding shortfall for large banks.

– RWA goes up significantly for Group 1 banks with large trading operations andsecuritization exposures.

Results of Basel Committee Quantitative Impact Study(cont.)

Basel III

impacts

Capital ratios are adversely impacted under

Basel III due to changes in capital definition

along with increases in risk weighted assets.

Basel III

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 28/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.27 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

Basel III item Current*

Sample

average (as of

Dec 31, 2009)

Minimumrequirement

Estimated

shortfall

(Euros)

Key drivers

Common equityTier 1

11.1% 5.7% 7.0%

577bln^

Goodwill, intangibles, financial cross holdings, and15% limit on DTA/MSR/Investments

Tier 1 capital 10.5% 6.3% 8.5%

Total capital 14.0% 8.4% 10.5%

Leverage ratio* 2.8% 3.0% Cancellable lines, potential exposure

Liquidity**-LCR 83% 100% 1.73 tln Outflows to unsecured Fis, collateral,securitizations, etc.

Liquidity**-NSFR 93% 100% 2.08 tln

RWA +23% CCR, sVaR, IRC securitization

Group 1 banks results summary

Breakdown of increase in RWA (+23%)^ Tier 1 and total capital shortfall shouldbe less than CET1, and easily addressed

by meeting CET1.* Leverage ratio requirement can beexceeded easily by meeting CET1standard.

** Liquidity shortfall for LCR and NSFRnot additive.

impacts

0%

1%

2%

3%

4%

5%6%

7%

8%

Definition ofCapital

CounterpartyCredit Risk

SecuritizationBanking Book

Stressed VaR Equity StdMeasuremet

Method

IRC & TradingBook Securzn

Basel III

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 29/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.28 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• Credit Lyonais Securities Asia (CLSA) analyzed the Basel II impact using morerecent financials, and included the effects from mitigation actions alreadyannounced by several banks.

• The study compared Basel III impacts across a set of 44 banks (16 global, 24regional) across U.S., Europe, and Asia.

• Results are directionally consistent with Bank for International Settlements study.

• While global institutions have higher capital ratios than regional banks, theirdecline in CET1 ratio is much higher than that for regional banks(240 bps vs. 150 bps).

Basel III international comparisons

Large global banks Regional banks

Current Basel impact* Current Basel impact*

U.S. 10.3% 7.4% 9.6% 7.8%

Europe 9.2% 7.1% 8.3% 8.0%

Asia 12.5% 10.5% 11.0% -

-

Total 10.0% 7.6% 9.4% 7.9%

Source: CLSA (Credit Lyonais Securities Asia) U.S. banks sector outlook, Nov 5, 2010,“Basel III – International comparisons” used with permission

impacts

Basel III

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 30/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.29 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• Asian banks appear to be better positioned from capital standpoint to absorbBasel III changes.

• U.S.-based global banks are more impacted (290 bps) than their Asian or EUcounterparts (200 bps and 210 bps decline, respectively).

– Current common equity capital at U.S. banks are higher than European banks, likelydue to capital raised in 2009 following Fed’s SCAP/stress testing initiative results.

Basel III international comparisons (cont.)impacts

Source: CLSA (Credit Lyonais Securities Asia) U.S. banks sector outlook, Nov 5, 2010,“Basel III – International comparisons” used with permission

Basel III

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 31/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.30 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• As a result of Basel III and other regulations (e.g., Dodd-Frank in U.S), bankingwill be more heavily regulated.

• We can expect a trend towards simplicity in balance sheet composition andsimpler capital structure.

• Due to significantly higher capital requirements, capital markets trading andstructured finance transactions may see reduced levels of activity and a squeeze

on profitability. – With greater volumes of over-the-counter derivatives cleared through centralized

counterparties such as exchanges (given favorable capital charges) will continue to addpressure on profitability.

• Banks will likely be less inclined to use various forms of off balance sheetfinancing and investment vehicles due to implications for capital, leverage, andliquidity.

– It is conceivable that some of these volumes are directed to unregulated segments ofthe financial services industry.

Expected industry trends in response to Basel III

With stronger capital and liquidity measures,

large global banks can be expected to have

more stable and predictable earnings

stream, and may be less prone to

boom and bust cycles.

impacts

Basel III

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 32/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.31 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• Retail deposits as a share of overall funding for large global banks will likelyneed to increase to meet liquidity standards.

– Competition for retail deposits may be spurred, and may lead to acquisitions of small,niche banks with local deposit share.

– The low-interest rate environment may encourage banks to lock in longer-term fundingthrough debt markets.

– Short-term wholesale funding markets such as brokered CDs and commercial papermay be adversely impacted with lower liquidity and higher spreads.

• An acceleration in trends is likely towards fee based businesses such as wealthmanagement and private banking due to lower capital charges

• Various forms of mortgage credit may see tighter lending standards and a returnto traditional products and collateral requirements. Fees and pricing for home

equity lines and credit cards is likely to increase.

• Dividend payout ratios should stabilize, but at levels below the pre-crisis levels.

Expected industry trends in response to Basel III (cont.)

Basel III greatly increases the

attractiveness of retail deposits as th e

preferred form o f bank funding.

impacts

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 33/53

Implementation

considerations

• Program management

• Risk management

• Corporate treasury

• External reporting

Change toProgram

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 34/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.33 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

Our perspective on Basel III applicabili ty

• Critical to consider establishing a top down, end-to-end view of the program for all

stakeholders (business, risk, treasury, reporting).• Program management

– PMO should serve as the “Requirements Clearinghouse” balancingconsiderations of business/risk, technology, regulatory expectations, andexecutive management.

– Basel II domain expertise, understanding of industry/peer bank approaches, andregulatory trends in the PMO can be important.

– PMO should manage scope aggressively in face of rationalization from businessand information technology.

• Communication strategy must again address the “core” and “extended”stakeholders.

– Front office, middle office and back office

– Training and education is core part of communications

• A structured approach to planning and governance

– Early focus on data definitions, data governance and data quality.

– Clear definition of ownership and accountability.

– Detailed upfront project planning.

– Establish and enforce standards.

• Basel III implementation may impact several aspects of a bank’s infrastructure and operations, especially:

– Risk management (especially risk functions supporting capital markets and structured finance) – Corporate treasury

– External reporting

• Institutions may be well served to remember the lessons from Basel II implementation, where costs and complexitysignificantly exceeded expectations resulting in huge budget over-runs and above-plan spend.

Basel III may impact bank infrastructure in severaldimensions

Our Basel II observations

• Lack of end-to-end implementation perspective covering business, data,

technology, process, analytics, and reporting.• Program management

– Design, structure, and role of project management office (PMO) underwentseveral iterations.

– Traditional “operations” centric PMO were not very effective.

– Excessive reliance on subject-matter experts to influenceprogram direction.

– Inability of PMO to manage and contain scope.

• Basel II also exposed limitations of large complex organizations in many respects

– Limitations to cross functional collaboration

– Misalignment of objectives between business and technology

– Ownership and accountability for “requirements”

• Excessive focus on some narrow areas left large components without focus andplans till late in the game

– Data quality

– Traceability of requirements

– Risk exposure to general ledger reconciliation

– Sustainability model

Program

management

Risk

t

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 35/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.34 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• Regulations, such as Basel II, Dodd-Frank (Volcker rule, Collins Amendment,etc), stress testing, etc.

– Regulatory information requests, horizontal and targeted exams.

– Technology integration from mergers and acquisitions activity that occurred during creditcrisis and impacted several large financial firms.

– In the U.S., newly formed bank holding companies are transitioning to a very different

regulatory landscape. – Core investments in risk infrastructure/technology/reporting that were deferred.

Risk management infrastructure at the largest banks isresponding to change

Given the myriad of regulatory initiatives,

flexibility, and adaptability may be key from

a risk management infrastructure

standpoint. .

management

Risk

management

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 36/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.35 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• Basel III rules introduces a variety of new data, analytical, and technologyrequirements.

– Guidance disproportionately impacts areas already undergoing significant changes suchas derivatives and securitizations.

– Significant requirements around collateral, risk management, stress testing, and modelvalidation that are difficult to implement and maintain.

– Requirements for IRC are both analytically and operationally intensive, although currentprocesses and systems may be extended for sVaR calculations.

– Requirements to produce an additional set of effective expected positive exposure(EEPE) based on stressed conditions is likely to be both systems and human resourceintensive.

• Computation of leverage ratio based on varying local accounting rules at the

legal-entity level and harmonization at parent level for large internationally activebanks could be operationally challenging.

Risk management data and operational challenges

Implementation of credit and market risk

RWA rules by 2012 will likely impose

significant costs , and be associated with

implementation and compliance risks.

management

Corporate

treasury

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 37/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.36 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• A number of Basel III requirements — capital, liquidity standards (LCR andNSFR), leverage ratio — are core to corporate treasury’s strategic and functionalrole in a bank.

• Strategic considerations

– Active role in capital management including capital structure, cost of capital,distributions, etc.

– Long-term funding and liquidity management strategies, with flexibility to refine andreact to market.

– Much tighter integration of treasury with business strategy and plans, with capitalimplications addressed proactively.

– Alignment with risk management due to dependencies such as limit management,collateral, and exposure management, etc.

Considerations for corporate treasury

While capital- and liquidity-related changes

are significant, the level of investment for

infrastructure enhancements should be

lower than costs associated wit h Basel II.

treasury

Corporate

treasury

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 38/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.37 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• Operational considerations

– Treasury data, systems, processes, analytics, and reporting will likely require significantenhancements.

– Stressed liquidity ratios will likely require new data and system feeds, mapping andcategorization efforts, reconciliation to accounting books, and harmonization across

jurisdictional requirements.

• Sustainable operational processes to support external disclosure and regulatoryreporting requirements around liquidity and capital will likely require a change inmindset.

– Treasury processes and reporting serve internal management (and board) needs suchas interest rate risk management, liquidity, and capital planning/management.

– Recent regulatory requests relating to capital adequacy assessment, stress testing, etc.,

have been addressed largely through ad hoc and one-time efforts. – ALM systems may be subject to higher level of change management and controls.

– Formal monitoring and reporting requirementsrelating to maturity.

Considerations for corporate treasury (cont.)

treasury

Addressing data quali ty and operational

requirements for treasury are expected to be

substantive.

External

reporting

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 39/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.38 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• Basel III increases reporting and disclosure requirements, which may continue topressure bank functions involved in regulatory reporting/external reporting.

– However, some reporting requirements (leverage ratio, capital, funding mismatch, etc.)could be able to leverage existing processes and infrastructure.

• External reporting is typically downstream of most applications where thedisclosure information is derived, aggregated and assimilated.

– Basel II reporting and disclosure required close coordination between risk managementand regulatory reporting.

– Basel III could enhance coordination and collaboration of Regulatory Reporting withtreasury.

• Significant disclosure requirements relating to counterparty exposures andsecuritizations will rely on risk management to provide the data and analytics;

the existing Basel II reporting processes may be enhanced to address theserequirements.

Changes in external reporting are evolutionary

Meeting enhanced disclosure and reporting

requirements is expected to be less

challenging than other aspects of Basel III.

reporting

External

reporting

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 40/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.39 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• Reporting of newly defined capital components may not pose additionalcomplexities, as it will likely continue to be general ledger-based, and tightlyintegrated with financial reporting.

– The elimination of 50/50 deductions from Tier 2, and change in approach to incorporatedeductions related to risk exposures in the RWA computations, in effect simplifies someaspects of calculation of regulatory capital measures.

• Existing bank processes relating to interest rate risk management and liquiditymanagement may be able to support Basel III reporting and disclosurerequirements, with some enhancements.

• While the BCBS leverage ratio requirement has some differences to the currentU.S. definition, information on incremental items (such as credit card lines, EPE,etc.) can be obtained from Basel II sources.

Changes in external reporting are evolutionary (cont.)

For Basel III reporting , synergies wit h Basel

II data, and reporting infrastructure must be

actively explored.

reporting

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 41/53

Client focus — Preparing

for change

• Assessment and analysis

• Planning and design

• Strategic implications

Ass essment

and analysis

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 42/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.41 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• The long timetable for Basel III implementation allows for methodical planningand preparation for the Basel III target state.

– 13 U.S. banks participated in BCBS QIS in early 2010, and others have assessedimpacts of Basel III.

– Several large banks have already announced plans to mitigate an adverse impact oncapital and liquidity from Basel III.

– Practically, we expect investors and regulators to influence banks to adopt revisedcapital standards well in advance of the Basel III timelines.

– However, the extended timeframe could also induce complacency for some institutionswhich may chose to push out implementation efforts.

• Interdependencies and linkages across capital markets, risk management,corporate treasury, and external reporting make Basel III implementation

complex, though less invasive as Basel II. – Individual requirements for calculations (excluding credit and market risk RWA) on the

surface likely be manageable

– Early focus on dependencies can help mitigateexecution risk

Preparing for change

Delay in f inal rules and inadequate

planning adversely affected Basel II

programs. Basel committee final rules

provide a reasonable foundation to

initiate program design and

programming for Basel III.

and analysis

Ass essment

and analysis

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 43/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.42 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• Preparations for Basel III should be considered in different stages.

– Strategic actions for balance sheet composition, funding, capital management, andbusiness planning necessitate a solid understanding of issues and robust action plan.

• Execution of business strategies and changes to funding mix, liquidity profile, orcapital structure can also depend on macro variables, competitive environment,market conditions, and business opportunities; as such, some may take several yearsto accomplish.

– Initial planning, PMO set up and design activities in preparation of U.S. rule making.

– Detailed planning and requirements, execution and testing.

Preparing for change (cont.)

a d a a ys s

Advanced p lanning, program management,

and end to end requirement definitions are

critical for a successful and cost effective

implementation.

Ass essment

and analysis

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 44/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.43 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

With BCBS rules finalized, clients should consider avariety of activit ies in preparation for U.S. Basel III rules

Pro-formaassessment and

scenario

analysis

• Detailed pro-forma assessment of capital, liquidity, and leverage ratio impacts from BCBS rules(December 16, 2010) [Update BCBS QIS from 2009 may be used].

• Projections of capital and liquidity measures, along with market-based scenario analysis.

• Identification of significant issues and “shortfall” drivers for Basel III items.

Basel III

business and

capital strategy

• Results analysis, issue identification, and strategic assessment of choices/options.

• Catalog and prioritization of actions for the short, medium and long term.

• Senior management buy in, endorsement and sponsorship.

• Mitigation action plan with agreement of timeframe and assignment of accountability.• Analysis of various capital and liquidity levers, and sensitivities, simultaneously leading to optimal

balance sheet composition and capital structure

PMO design and

set up

• Establish PMO and associated governance structure for Basel III execution.

• Define protocols for interactions with key stakeholders (e.g., board, steering committee, businessexecutives, internal audit, regulators, etc.).

• Establish work threads with clear accountability, and define approach to manage requirements with

coverage across data, process, technology and business.

Program road

map and high-

level design

• Develop a high-level program roadmap and develop materials for stakeholder/senior managementeducation, support, and buy-in.

• Data requirements and source map — Assessment and analysis of potential sources for broadsets of data requirements.

• Develop top down end -o-end logical design for Basel III liquidity framework solution, and identifyleverage points of integration with Basel II infrastructure.

y

Strategic

implications

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 45/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.44 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

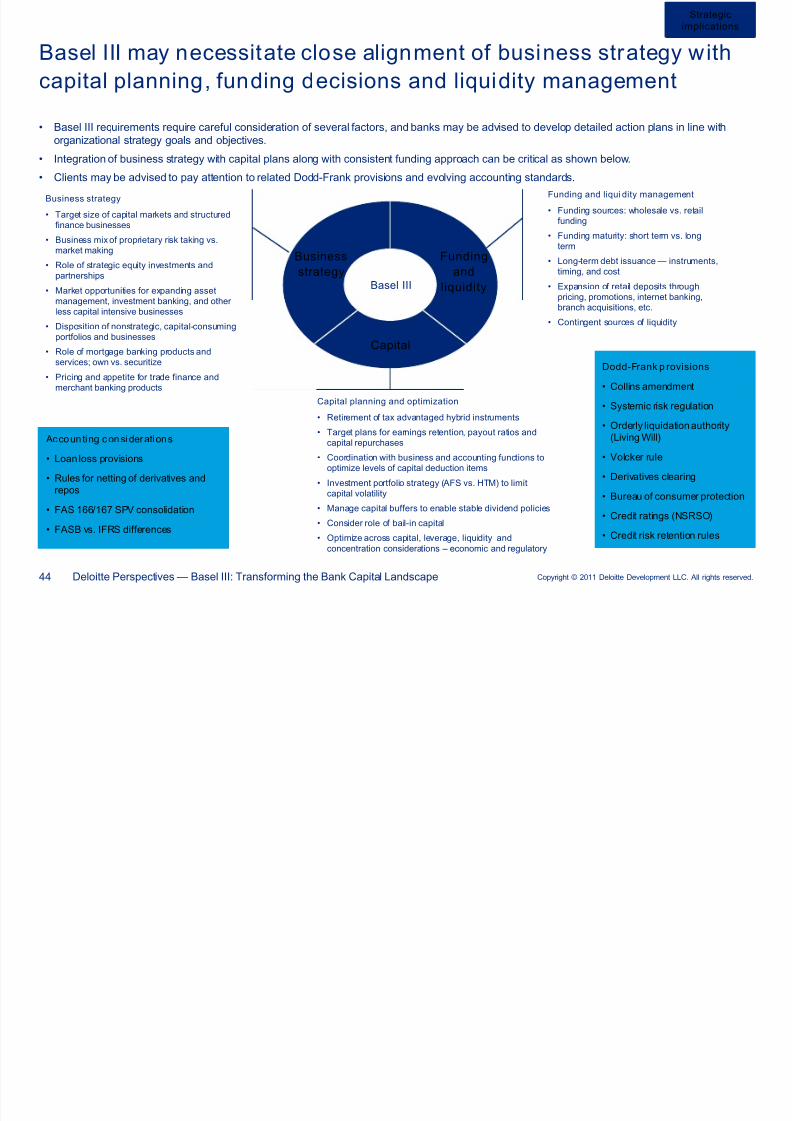

• Basel III requirements require careful consideration of several factors, and banks may be advised to develop detailed action plans in line with

organizational strategy goals and objectives.• Integration of business strategy with capital plans along with consistent funding approach can be critical as shown below.

• Clients may be advised to pay attention to related Dodd-Frank provisions and evolving accounting standards.

Basel III may necessitate close alignment of business strategy with

capital planning, funding decisions and liquidity management

Basel III

Business strategy

• Target size of capital markets and structuredfinance businesses

• Business mix of proprietary risk taking vs.market making

• Role of strategic equity investments andpartnerships

• Market opportunities for expanding assetmanagement, investment banking, and otherless capital intensive businesses

• Disposition of nonstrategic, capital-consumingportfolios and businesses

• Role of mortgage banking products andservices; own vs. securitize

• Pricing and appetite for trade finance andmerchant banking products

Funding and liqui dity management

• Funding sources: wholesale vs. retailfunding

• Funding maturity: short term vs. longterm

• Long-term debt issuance — instruments,timing, and cost

• Expansion of retail deposits throughpricing, promotions, internet banking,branch acquisitions, etc.

• Contingent sources of liquidity

Capital planning and optimization

• Retirement of tax advantaged hybrid instruments• Target plans for earnings retention, payout ratios and

capital repurchases

• Coordination with business and accounting functions tooptimize levels of capital deduction items

• Investment portfolio strategy (AFS vs. HTM) to limitcapital volatility

• Manage capital buffers to enable stable dividend policies

• Consider role of bail-in capital

• Optimize across capital, leverage, liquidity andconcentration considerations – economic and regulatory

Accounting considerations

• Loan loss provisions

• Rules for netting of derivatives andrepos

• FAS 166/167 SPV consolidation

• FASB vs. IFRS differences

Dodd-Frank p rovisions

• Collins amendment

• Systemic risk regulation

• Orderly liquidation authority(Living Will)

• Volcker rule

• Derivatives clearing

• Bureau of consumer protection

• Credit ratings (NSRSO)

• Credit risk retention rules

p

Funding

and

liquidity

Business

strategy

Capital

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 46/53

Why Deloitte?

A leader in bank capital

• Global footprint

• End-to-end service capabilities

• Marketplace eminence andthought leadership

Globalfootprint

heading

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 47/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.46 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

Deloit te in financial services

Deloit te’s global breadth and depth

• A global network of more than 21,000 dedicated professionals,including 2,880 partners in 40 countries, combining assurance,tax consulting, and financial advisory experience.

• Serve 88% of financial services companies in the Fortune Global500.

• Deloitte member firms serve:

– All of the top 20 global banks

– 18 of the top 20 global insurance companies

– 17 of the top 20 global asset management firms

• Contributes more than 25% of our organization’s global revenues

• Representative financial services clients:

Global Financial Services Industry organization

Fifth Third Bancorp

Huntington Bancshares

Lazard Frères

ING

Morgan Stanley

Northern TrustRBC Bancorp

UBS

AXA

Banco Santander

Bank of Tokyo

Mitsubishi, UFJ

BB&T

BNP ParibasGoldman Sachs

E*Trade Financial

Source: Kennedy; Public Sector Consulting Marketplace 2009-2012; © BNA Subsidiaries, LLC; used with permission

• One of the largest professional services organization in the world,with 169,000 people in 140 countries.

• A professional services organization that offers a complete rangeof audit, tax, consulting and financial advisory services.

• One of the largest global financial services consultancy, with $26billion in global revenues in FY2009.

• U.S. practice with 90 offices, 42,000 professionals, and fiscal2009 revenues of approximately US$10.7 B.

People: 56,000

Europe, Middle East, Africa

People: 26,000

Asia Paci fic

People: 53,000

Amer icas

heading

End-to-endservice

capabilities

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 48/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.47 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• Successful transition to Basel III may require robust business and capital st rategies supported by strong execution and

technology implementation capabilities anchored in domain knowledge of credit and market risk, capital markets, assetliability management, accounting, and regulatory reporting.

• Deloitte is a professional services organization w ith an integrated strategy that has been key to our marketplacesuccesses in delivering large scale, complex programs such as Basel II.

• Our competitive Basel II marketplace footprint provides a strong foundation for assisting clients to successfullyimplement and comply with Basel III.

Basel III requires a broad array of services andcompetencies

Risk

management

Treasury and

capital markets

Regulatory PMO

Implementation

and testing

Accountin g

Tax

Corporate

finance

advisory

Strategy &

operations

Technology

• We have a prestigious portfolio of referenceable “ core”

Basel II bank clients, and one of the largest dedicated

Basel and bank capital team of any professional services

organization.• Our implementation approach incorporates bank’s business

strategy and an end-to-end view of requirements.

• We have deep subject-matter knowledge in bank capital rules,credit risk, treasury, traded and structured products, andregulatory reporting.

• Our accounting and infrastructure capabilities supportsregulatory reporting and disclosure at legal entity andconsolidated levels.

• Data management, data governance, and data qualit y areintegral to our practice.

• We utilize proprietary tool kits for gap assessment,requirements traceability, project planning, and end-to-endtesting.

• Our standardized PMO techniques and tools enablestakeholder involvement, project execution, communication,knowledge transfer, and education.

• With several former regulators in our practice, we have strongregulatory relationships and deep insights into regulatory

expectations.

Deloitte remains as the only

professional services organization

with service capabilities spanning

risk, treasury, accounting, tax,

corporate finance, and technology.

capabilities

Marketplace

eminence and

thought leadership

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 49/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.48 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

Deloit te’s visibil ity, eminence, and thought leadershipon Basel III

• Knowledge Congress Webinar “ Tougher Laws Woven into Basel” , February 18, 2010

– Michael Bleier, Partner, Reed Smith LLP;

– Alok Sinha, Principal, Deloitte & Touche LLP;

– Nancy Hunt, Acting Associate Director of the Capital Markets Branch, Policy Section, Division of Supervision and

Consumer Protection, Federal Deposit Insurance Corp (FDIC)

– Michael Stevens, Conference of State Bank Supervisors

• 11th Annual Risk Conference New York (February 9, 2010); Keynote panel discussion “ Global Regulatory Reform”

– Greg Hands, MP; Shadow Treasury Minister, U.K;

– Martha Cummings, Chief Risk Officer, Banco Santander;

– Til Schuerman, Vice President, Federal Reserve Bank of New York

– Alok Sinha, Principal, Deloitte & Touche LLP;

• 2nd European Risk Congress, London, June 9, 2010

– Presentation, “ Basel III Guidance,: Overview and Implications” , Alok Sinha, Principal, Deloitte & Touche LLP

• Freddie Mac 2010 Executive Forum ” Future State of Mortgage Industry” : Panel Discussion, September 1, 2010

– Laurie Goodman, Senior M.D., Amherst Securities

– Alok Sinha, Principal, Deloitte & Touche LLP ( Basel III Implications for Mortgage Industry)

– Mark Willis, Furman Center for Real Estate & Urban Policy

• CLSA Luncheon Speaker Series Topic, New York, (October 13, 2010), ” Capital at U.S. Banks — How high is

enough?”

Marketplace

eminence and

thought leadership

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 50/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.49 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

Deloit te’s visibil ity, eminence, and thought leadershipon Basel III (cont.)

Basel III: Bank Regulatory Capital Landscape Continues to Evolve

• Robert Maxant, Partner, Deloitte & Touche LLP

• Alok Sinha, Principal, Deloitte & Touche LLP

• Andrea di Giovanni, Director, Deloitte & Touche LLP

• Knowledge Congress Live Webcast “ Basel 3: Important Updates” , January 25, 2011

– Nancy Hunt, Acting Associate Director of the Capital Markets Branch, Policy Section, Division of Supervision and

Consumer Protection, Federal Deposit Insurance Corp (FDIC)

– Bobby Bean, Chief, Capital Markets Policy Section, Federal Deposit Insurance Corp (FDIC)

– Michael Stevens, SVP & Director of Regulatory Affairs, Conference of State Bank Supervisors (CSBS)

– Michael Bleier, Partner, Reed Smith LLP;

– Alok Sinha, Principal, Deloitte & Touche LLP

Banking & Securities Dbriefs

Tuesday, January 11, 2:00 PM EST

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 51/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.50 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

• Basel III rules have been recently finalized by the BCBS Supervision, andimplementation timeframe extends through 2019.

– Bank capital landscape will evolve with the largest, global banks holding more capital,stronger capital instruments, and capital buffers to protect from systemic risk.

– Basel III introduces a global framework for liquidity for the first time and a leverage ratiomeasure.

• Banks will likely need to have much closer alignment between business strategy,capital, and liquidity planning and funding decisions.

• Enhancements will be necessary for infrastructure supporting corporate treasury,risk management, capital markets, and external reporting functions.

• U.S. rule-making process for Basel III should incorporate related Dodd-Frankprovisions.

• Costs of implementation may be be significant, but likely not as high as Basel IIfor well structured and executed programs.

In summary

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 52/53

Copyright © 2011 Deloitte Development LLC. All rights reserved.51 Deloitte Perspectives — Basel III: Transforming the Bank Capital Landscape

Lakshmanan Balachander (Bala)

Director, Deloitte & Touche LLP

Governance, Regulatory & Risk Services

New York, NY

Phone: +1 212 436 5340

E-mail: [email protected]

Americas contacts

Alok Sinh a

Principal, Deloitte & Touche LLPLeader — Banking & Securities Sector

San Francisco, CA

Phone: +1 415 783 5203

E-mail: [email protected]

Carrie Cheadle

Director, Deloitte & Touche LLP

Governance, Regulatory & Risk Services

Chicago, IL

Phone: +1 312 486 4095

E-mail: [email protected]

Andrea d i Giovanni

Director, Deloitte & Touche LLP

Governance, Regulatory & Risk Services

New York, NY

Phone: +1 212 436 7094

E-mail: [email protected]

Edward T. Hida, CFAPartner, Deloitte & Touche LLP

Global Leader — Risk & Capital Management

New York, NY

Phone: +1 212 436 4854

E-mail: [email protected]

Robert Maxant

Partner, Deloitte & Touche LLP

Leader – FSI Treasury Services

New York, NY

Phone: +1 212 436 7046

E-mail: [email protected]

8/16/2019 Deloitte_gfsi 1103 Basel III Pov Bank Capital Landscape 2012 03

http://slidepdf.com/reader/full/deloittegfsi-1103-basel-iii-pov-bank-capital-landscape-2012-03 53/53

C © C

This presentation contains general information only and Deloitte is not, by means of this presentation, rendering accounting, business, financial,investment, legal, tax, or other professional advice or services. This presentation is not a substitute for such professional advice or services, norshould it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affectyour business, you should consult a qualified professional advisor.

Deloitte, its affiliates, and related entities shall not be responsible for any loss sustained by any person who relies on this presentation.