december 2016 | ey.com/ccb | 15th edition capital confi ... perfect storm of sector convergence,...

TRANSCRIPT

December 2016 | ey.com/ccb | 15th edition

Media & Entertainment

CapitalConfi denceBarometerM&A takes center stage, driven by increasing disruption and sector convergence

Key fi ndings

31%see the impact of digital technology on the business model elevated on the boardroom agenda

43%say inorganic strategies are driving growth

31%cite sector convergence as the most disruptive factorto business

Macroeconomic environment

56%expect to actively pursue acquisitions in the next 12 months

Corporate strategy

80%see corporate earnings as either stable or positive

27%cite political instability in their home market as an emerging risk to their core business

M&A outlook

73%see the global economy as either stable or improving

93%are using big data and analytics as part of their deal process

The need to respond to challenges while navigating a complex and fast-changing environment is elevating dealmaking as a strategic priority. Executives are evaluating more targets, and deals will tend to be smaller. However, as boards consider innovative acquisitions outside their own industry, they are using analytics to make better decisions.

Most executives see the global economy as stable and say corporate earnings are back on track. But there are uncertainties ahead, both in the near- and longer-term, including the political backdrop in many geographies and credit markets that may be set to tighten in 2017. Despite these risks, as low growth and disruption continue, boards are focusing on mergers, acquisitions and alliances to create value.

Innovation, new technology and changing customer demands are challenging businesses to reinvent their products and operations. At the same time, uncertainty around regulation is impacting corporate strategy. Companies are responding by reimagining their value proposition and reorganizing their portfolios for future success, executing on a range of acquisition, divestment and partnership transaction options.

48%of companies have more than fi ve deals in their pipeline

1Capital Confi dence Barometer |

M&E companies focus on dealmaking in response to the rapidly evolving industry landscape

Nearly every media and entertainment (M&E) company is exploring a variety of potential strategic moves: international expansion, portfolio optimization, traditional scale mergers or cross-sector investments into emerging – and less familiar – business models or markets. They are considering these steps, alongside organic initiatives, in order to maximize growth within a rapidly-evolving industry landscape.

Unprecedented, unrelenting advances in technology and the swift emergence of new platforms and services are driving change in consumer behaviors, upending long-standing media ecosystems and blurring sector lines. Companies are aggressively seeking the innovation needed to position for future success and are looking to acquisitions, alliances and joint ventures to catalyze transformation.

The EY 15th Media & Entertainment Capital Confi dence Barometer fi nds 56% of industry executives expect to pursue acquisitions in the next 12 months, pointing to a healthy M&A marketplace in 2017. M&E leaders are pushing through a sluggish global economy and increased political uncertainty to chase growth-enhancing transactions.

Four key transaction areas:

• Cross-sector: companies are reaching outside their core business to acquire the products and services necessary to thrive in an increasingly converged world. Vertical integration across the content and distribution supply chain is re-emerging as a strategic theme.

• Horizontal scale: a focus on traditional market share growth is leading companies to consolidate within their own sector, achieving operational effi ciencies to boost earnings growth.

• International: despite the economic challenges around the globe, companies continue to target expansion into new geographies with favorable long-term growth fundamentals.

• Portfolio optimization: streamlining diversifi ed asset bases via divestitures, spins and carve-out IPOs is allowing companies to focus on core operations, allocate capital to the most promising opportunities and unlock sum-of-the-parts value.

While blockbuster mega-mergers grab headlines, companies are also focused on smaller deals to augment existing platforms, making targeted strategic bets in emerging areas to bolster long-term growth plans.

Execution is critical. M&E leaders are deploying sophisticated data and analytics throughout the transaction process to drive more speed and precision than ever before. The real work begins after closing as companies seek to integrate acquisitions seamlessly, leading to value creation over time.

John HarrisonEY Global Media & Entertainment LeaderTransaction Advisory Services

M&E executives view the global economy as stable but recognize an increase in downside risks

2 | Capital Confi dence Barometer

Macroeconomic environment

The majority of executives surveyed see the global economy as stable or positive. Companies are challenged by the ongoing uncertainty over where faster growth will come from. Add to this frustration the impact of events, such as the United Kingdom’s decision to leave the European Union (Brexit), the heightened market volatility caused by potential changes to US interest rates and elections in several countries.

This environment creates a backdrop where strategically focused, growth-oriented inorganic moves, including M&A, joint ventures (JV) and alliances, are necessary to grow revenue and earnings. Companies are using deals and alliances to improve their competitive positioning, extend product offerings, or move into new markets or industries.

53%stable

20%improving

27%declining

What is your perspective on the state of the economy today at the global level?Q:

Without question, politics is now fi rmly back on the agenda for executives. The rise of populist parties across the globe has become a rising concern for executives. Twenty-seven percent regard political instability as the most important risk to their business in the next year.

3Capital Confi dence Barometer |

Responses are generally upbeat on the capital market outlook, but instability may increaseExecutives are moderately upbeat about the overall outlook for capital markets, despite 2016’s sporadic periods of market turmoil. A majority of executives see conditions over the next 12 months as either stable or positive.

The most notable responses show declining sentiment in the outlooks for credit availability and short-term market stability.

These views may be infl uenced by concerns over tapering of quantitative easing policies (especially at the central banks in Europe and Japan) potentially rising rates in the US and global political uncertainty. Such shifts may increase volatility and also impact credit markets, especially for lower-rated segments of the economy and emerging markets.

Macroeconomic environment

Oct 15 Apr 16 Oct 16 Oct 15 Apr 16 Oct 16 Oct 15 Apr 16 Oct 16 Oct 15 Apr 16 Oct 16

Corporate earningsPercent

Short-term market stabilityPercent

Equity valuationsPercent

Credit availabilityPercent

Improving Stable Declining

64

27

9

42

517

41

39

20

83

161

57

349

51

30

19

56

368

41

44

15

39

43

18

77

194

54

388

46

36

18

Please indicate your level of confi dence in the following at the global level:Q:

Having experienced almost a decade of macroeconomic uncertainty, executives have become accustomed to ambiguity about global economic growth, highly volatile capital markets and confusion about the effects of monetary policy on currencies.

Sector convergence and digital remain at the core of M&E strategyA perfect storm of sector convergence, digital innovation and changing customer behavior is disrupting M&E business models. At the same time, greater uncertainty about the path ahead for industry regulation is adding a layer of complexity to corporate strategy.

Companies are responding by reimagining their value proposition and reorganizing themselves to take advantage. Executives are maintaining a healthy outlook for JVs and alliances. These alternative deal structures may be the fastest way to capture growth opportunities arising from the rapid transformation of the M&E sector.

31 M 23 M31 M 34 M43 57 M 45 55 M

4 | Capital Confi dence Barometer

sector convergence is the most disruptive factor to business in the next 12 months31% 23%

see the impact of digital technology on the business model elevated on the boardroom agenda over the past six months

31% 34%

plan to enter into alliances, M&A activities or joint ventures with other companies or competitors to create value from underutilized assets

43% 45%

Corporatestrategy

Media & Entertainment sector Global

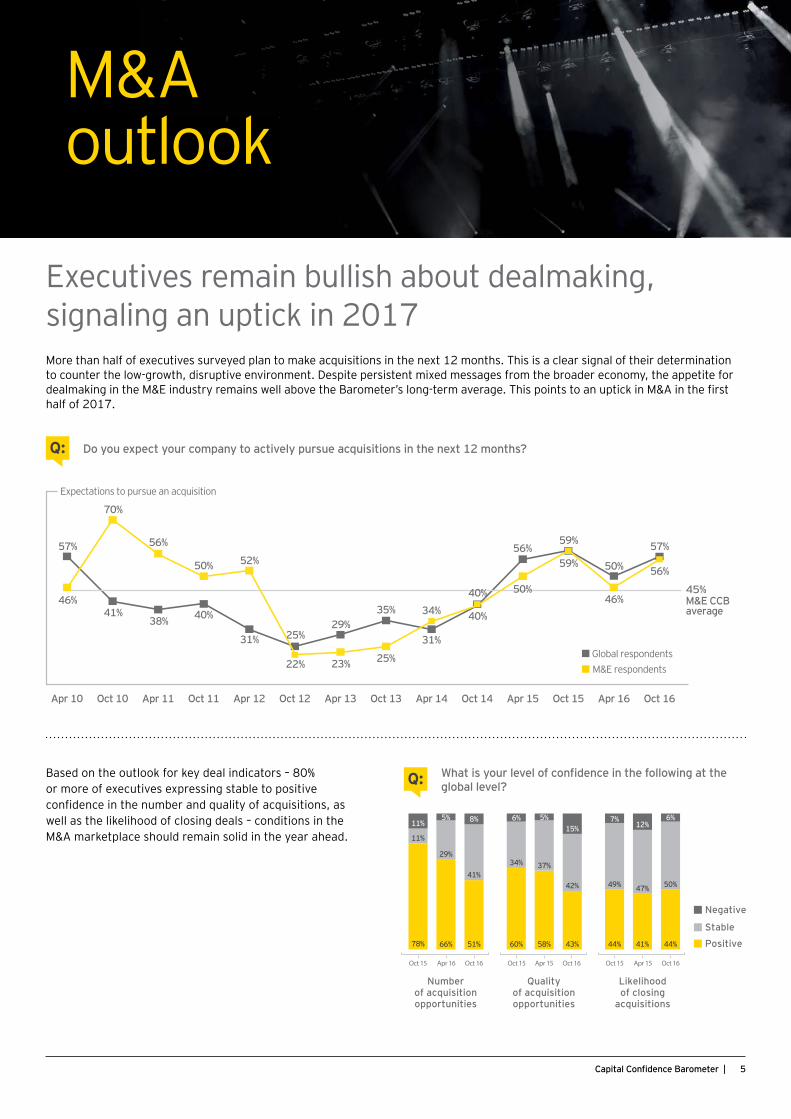

Executives remain bullish about dealmaking, signaling an uptick in 2017More than half of executives surveyed plan to make acquisitions in the next 12 months. This is a clear signal of their determination to counter the low-growth, disruptive environment. Despite persistent mixed messages from the broader economy, the appetite for dealmaking in the M&E industry remains well above the Barometer’s long-term average. This points to an uptick in M&A in the fi rst half of 2017.

Based on the outlook for key deal indicators – 80% or more of executives expressing stable to positive confi dence in the number and quality of acquisitions, as well as the likelihood of closing deals – conditions in the M&A marketplace should remain solid in the year ahead.

M&Aoutlook

Do you expect your company to actively pursue acquisitions in the next 12 months?Q:

What is your level of confi dence in the following at the global level?Q:

Expectations to pursue an acquisition

Apr 10 Oct 10 Apr 11 Oct 11 Apr 12 Oct 12 Apr 13 Oct 13 Apr 14 Oct 14 Apr 15 Oct 15 Apr 16 Oct 16

57%

46% 41%

70%

38%

56%

40%

50%

29%

23% 25%

35%

31%

40%

40%

56% 59%

59% 50%

46%

57%

56% 52%

31% 25%

22%

34%

45%M&E CCBaverage

M&E respondents

Global respondents

50%

Qualityof acquisitionopportunities

Oct 15 Apr 15 Oct 16

Likelihoodof closing

acquisitions

Numberof acquisitionopportunities

Oct 15 Apr 16 Oct 16 Oct 15 Apr 15 Oct 16

Positive

Stable

Negative

11%

78%

11%

29%

66%

5%

41%

51%

8%

34%

60%

6%

37%

58%

5%

42%

43%

15%

49%

44%

7%

47%

41%

12%

50%

44%

6%

5Capital Confi dence Barometer |

67 M 67 M65 M 65 M49 51 M 53 47 MThe hunt for growth is leading companies to seek out cross-sector and cross-border opportunitiesSector blurring — companies making increasing and deeper incursions into adjacent or unrelated industries — has become a prominent feature of the current M&A market. Executives looking for deals outside their own industries show determination to reimagine their market and support their growth plan.

Two in three media and entertainment executives — more than the global average — cite new technology and digitalization as the strongest driver for cross-sector deals, while the second most cited factor is, unsurprisingly, reacting to competition. In both cases, deals are the strategic response to new market entrants upsetting the status quo, changing the competitive landscape with new operating models and new ways of creating demand, as well as hybridization of products and services.

At the same time, over 40% of media and entertainment executives say they are targeting a cross-border acquisition in the coming year. Companies are expanding geographic reach in order to gain exposure to high-growth regions and under-penetrated markets.

6 | Capital Confi dence Barometer

Larger deal pipelines support a forecast of an uptick in M&A activity. Executives report an increase in the number of potential targets they are reviewing; nearly two-thirds of respondents say they have three or more deals in their acquisition pipelines.

The need to acquire smaller, more innovative assets is refl ected in executives’ planned deal sizes over the next 12 months. Our survey refl ects an increase in planned deals in the US$250m to US$1b range. Previously, these deals may have been considered bolt-ons. However, due to their positioning at the heart of companies’ growth strategies, transactions of this size can now be considered “augmental” M&A deals, a status between a transformative-scale deal and a smaller add-on.

M&A outlook

Media & Entertainment sector Global

have three or more deals in the pipeline67% 67%

expect no change in the current pipeline over the next 12 months65% 65%

are targeting deal size in the US$250m to US$1b range in the next 12 months49% 53%

What is the main strategic driver for pursuing acquisitions in your current sector?Q:

Growing market share

Acquiring innovative start-ups

Acquiring technology or new production capabilities

Acquiring talent

Reacting to customer behavior

23%

22%

22%

14%

11%

Percent

Top five answers chosen

7Capital Confi dence Barometer |

67 M 12 88 M42 58 M 36 M

M&A outlook

Media & Entertainment sector Global

see access to new materials or technology / digitalization as the main strategic driver for pursuing an acquisition outside of their sector

expect to pursue cross-border deals in the next 12 months

67% 12%

42% 36%

Companies acquiring in their own sectors are looking for future growth potentialCompanies continue to actively pursue deals in their core sectors, with a primary focus on traditional market share growth. They are also seeking to acquire complementary assets with new technology and production capabilities to improve operating performance. Additonally, executives say they are reacting to changing customer behavior when considering such deals.

In an ongoing low-growth environment with margins and profi tability challenged, companies are looking to enhance their industry positioning and create cost effi ciencies to support future earnings growth.

8 | Capital Confi dence Barometer

M&A outlook

Top investment destinations

The key developed and largest emerging economies dominate executives’ investment plans. Based on the current outlook, the United States economy should remain robust through 2016. Many US corporates, operating in a low-growth, low-interest rate, low-infl ation environment, are viewing deals as a strategic means to grow faster. Consequently, the US M&A market is expected to maintain its upward momentum and its attractiveness to foreign investors. Due to concerns raised by Brexit, the UK slid to third place from fi rst in the last survey.

1. United States

2. France

3. UK

4. Germany

5. China

M&E executives are prepared to walk away rather than overpayAlmost half of M&E executives see the current M&A valuation gap as somewhat high, and half of them expect this gap to remain at the current levels for the next 12 months. The disagreement over valuation, which may be due to greater investor or board scrutiny, has resulted in executives acting with discretion and walking away rather than overpaying. Economic and political instability has also caused deals to be pulled during the past 12 months.

How do you use analytics and big data for executing your M&A process and strategy? (Select all that apply.)Q:

45 55 M 56 44 M50 50 M 45 55 M

9Capital Confi dence Barometer |

M&A outlook

Media & Entertainment sector Global

think the valuation gap between buyers and sellers is 10% to 25%

expect the valuation gap to remain at current levels in the next 12 months

45% 56%

50% 45%

94 6M 89 11 Mhave canceled/failed to complete a planned acquisition in the past 12 months94% 89%

Executives are using big data and analytics to identify growth and valueAs well as being a driver of today’s deal marketplace, big data and analytics are being adapted as an enabler of a more robust and sophisticated deal process for companies. Transaction analytics uses data, technology and advanced quantitative analysis to achieve more speed and precision than before. This enables better questions to be asked during the diligence process.

As companies need to look at more targets, often in unfamiliar industries, deal teams are using data and analytical tools to identify areas of growth and related potential targets, aligned with their strategy.

To enhance the post-closing monitoring and optimization of the investment assumptions

To identify growth options and potential targets

To review our current portfolio of assets

To enhance the due diligence process

We are not using, but we are considering it

We are not using at all

To better identify synergies and determine appropriate valuation of the targeted asset

55%

52%

41%

41%

33%

5%

2%

With the deal table permanently reset, these are the better questions all executives need to ask themselves to enhance their growth strategy in today’s market:

21Are you capitalizing on the breadth of deal structures to realize your strategic objectives?Amid unprecedented change, many companies have to reinvent themselves fast — organically and through inorganic investments. Beyond traditional M&A, JVs, alliances, partnerships and industrial mash-ups are emerging as alternatives to secure deal value effectively.

Will geopolitical challenges derail your growth strategies?Political uncertainty is increasingly affecting global trade and credit markets. Executives who do not proactively consider or effectively respond to this in their approach to dealmaking run the risk of poorly executed growth strategies.

10 | Capital Confi dence Barometer

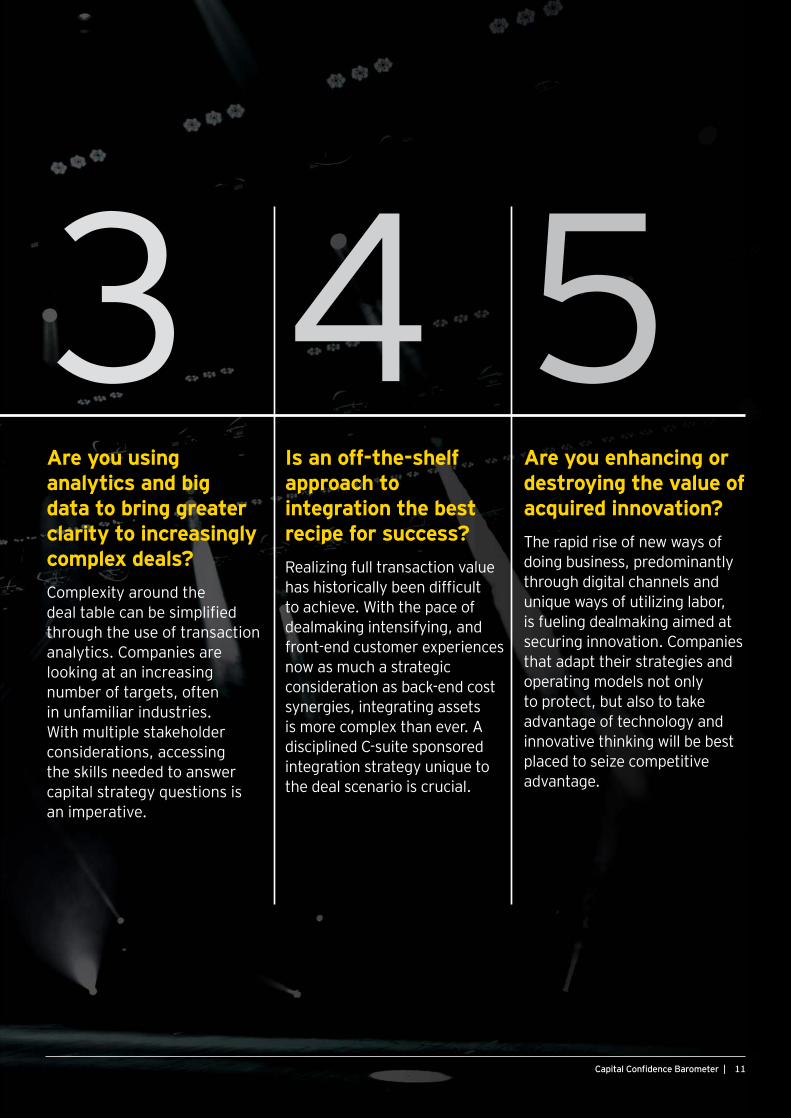

3Are you using analytics and big data to bring greater clarity to increasingly complex deals?Complexity around the deal table can be simplifi ed through the use of transaction analytics. Companies are looking at an increasing number of targets, often in unfamiliar industries. With multiple stakeholder considerations, accessing the skills needed to answer capital strategy questions is an imperative.

4Is an off-the-shelf approach to integration the best recipe for success?Realizing full transaction value has historically been diffi cult to achieve. With the pace of dealmaking intensifying, and front-end customer experiences now as much a strategic consideration as back-end cost synergies, integrating assets is more complex than ever. A disciplined C-suite sponsored integration strategy unique to the deal scenario is crucial.

5Are you enhancing or destroying the value of acquired innovation?The rapid rise of new ways of doing business, predominantly through digital channels and unique ways of utilizing labor, is fueling dealmaking aimed at securing innovation. Companies that adapt their strategies and operating models not only to protect, but also to take advantage of technology and innovative thinking will be best placed to seize competitive advantage.

11Capital Confi dence Barometer |

12 | Capital Confi dence Barometer

Contacts

EY GlobalJohn HarrisonEY Global Media & Entertainment Leader Transaction Advisory [email protected] +1 212 773 6122

EY AmericasKarl ChengBostonMedia & Entertainment Corporate Finance Strategy [email protected]+1 617 478 6372

Dorian SwerdlowNortheastMedia & Entertainment Transaction Integration [email protected]+1 212 773 6179

Paul SheahenNortheastMedia & Entertainment TransactionTax [email protected]+1 212 773 5578

Todd NovakMidwestTMT Transaction AdvisoryServices [email protected]+1 312 879 2889

Dan BuchlerWestMedia & EntertainmentTransaction Advisory Services [email protected]+1 213 977 7654

Luis MerliniSouth America, Sao PauloTelecommunication, Media & TechnologyTransactions Advisory Services [email protected]+55 11 2573 3166

EY Europe, Middle East, Indiaand Africa (EMEIA)Eric SanschagrinEMEIATelecommunication, Media & TechnologyTransactions Advisory Services [email protected]+44 20 7951 9650

William FisherUnited Kingdom and IrelandMedia & EntertainmentTransaction AdvisoryServices [email protected]+44 20 7951 0432

Olivier WolfLondonTelecommunication, Media & Technology Transactions Advisory Services and Corporate Finance [email protected]+44 20 7980 9169

Dietmar KoeslingGermany, Switzerland and AustriaTelecommunication, Media & TechnologyTransactions Advisory Services [email protected]+49 89 14331 17709

Ajay ShahIndiaMedia & EntertainmentTransaction AdvisoryServices [email protected]+91 22 6192 0640

EY Asia-PacificBen KwanChinaMedia & EntertainmentOperational TransactionServices [email protected]+852 2849 9223

Ishwar MadhyasthaOceaniaMedia & EntertainmentTransaction AdvisorySupport [email protected]+61 2 9248 5865

For a conversation about your capital strategy, please contact:

13Capital Confi dence Barometer |

About this surveyThe Global Capital Confi dence Barometer gauges corporate confi dence in the economic outlook and identifi es boardroom trends and practices in the way companies manage their Capital Agendas — EY member fi rm's framework for strategically managing capital.It is a regular survey of senior executives from large companies around the world, conducted by the Economist Intelligence Unit (EIU). Our panel comprises selected global EY clients and contacts, and regular EIU contributors.

• In August and September 2016, we surveyed a panel of more than 1,700 executives in 45 countries.

• In this survey, we had 66 respondents from media and entertainment companies, of which 41% were CEOs, CFOs and other C-level executives.

• Media and entertainment companies’ annual global revenues range from: less than US$500m (23%); US$500m—US$1b (18%); US$1b—US$3b (20%); US$3b—US$5b (15%); and greater than US$5b (24%).

• Global media and entertainment companies’ ownership was as follows: publicly listed (76%), privately owned (18%) and family-owned (6%).

Mergers, acquisitions and alliances are in the spotlight as companies seek innovation to redefi ne their strategyOur latest Global Capital Confi dence Barometer continues to fi nd a strong acquisition appetite together with a growing inclination to forge new alliances.

Prolonged economic challenges are driving investment decisions and leading companies to ally and cooperate for growth, as well as compete for and acquire market share.

Connect with us at ey.com/ccb.

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

About EY’s Transaction Advisory ServicesHow you manage your capital agenda today will define your competitive position tomorrow. We work with clients to create social and economic value by helping them make better, more informed decisions about strategically managing capital and transactions in fast-changing markets. Whether you’re preserving, optimizing, raising or investing capital, EY’s Transaction Advisory Services combine a set of skills, insight and experience to deliver focused advice. We can help you drive competitive advantage and increased returns through improved decisions across all aspects of your capital agenda.

© 2016 EYGM Limited. All Rights Reserved.

EYG no. 04098-164GBL

ED NoneThis material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax or other professional advice. Please refer to your advisors for specific advice.

ey.com/ccb