current infra status

TRANSCRIPT

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 1/34

Highways:

The present condition:

Heres an interesting statistic. Ten

out of 28 states (barring Delhi,

which is not a full-fledged state)

account for 65 per cent of the

countrys national highways

totalling around 71,000 km.

Globally, while a goods vehicle

clocks anywhere up to 800 km a

day, in India, this used to be

around 300 km until recently. The

road network of India needs to be

coordinated at both Central and

state levels. One way is to expand

the scope of NHDP III that aims to

connect key national capitals,

towns and cities.

Ports

Shipping minister G.K. Vasan told the parliament recently,

major and non-major ports in India achieved a total cargo

throughput of 844.9 million tonnes, reflecting an increase of

13.6 per cent in 2009-10, compared to a marginal increaseof 2.5 per cent in 2008-09. Separately, growth in cargo

handled at major and non-major ports was 5.7 per cent and

33.2 per cent, respectively, compared to 2.2 per cent and

3.3 per cent, in 2008-09.

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 2/34

The National Maritime Development Programme (NMDP) is aimed at overhauling Indias ports. Of the

total 199 ports, upgradation of 47 has been completed and 71 projects are in progress. For the

remaining 81 ports, upgradation plans are awaiting clearances. In the 12 major ports, 276 sub-projects

have been identified for implementation up to 2011-12.

Airports

Way back in 2003, the Naresh Chandra committee,

which was appointed to look at Indias aviation

infrastructure, had noted that several airports

across India are an embarrassment for the country.

Today, the airports at Delhi, Mumbai, Hyderabad

and Bangalore have become truly world class,

thanks to private sector involvement. But still

travellers to smaller airports such as Ludhiana,

Pune, Ahmedabad, Ranchi, Goa and Bhopal wouldvouch for the fact that the state of these airports

have left a lasting impression on them, and we are

not talking positive here.

A carefully worked out plan to involve the private

sector in upgrading at least 35-odd non metro

airports (see map) has been languishing since 2008.

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 3/34

Senior ministry officials say the plan has primarily been stymied by AAI itself. They dont have the

money to modernise all the airports, says a senior ministry source. But fearing loss of power, AAI has

been opposing the private sector getting involved, too.

Considering the fact that the ministry has set itself a target of operationalising 500 airports by 2020, it

may be a good idea to take the modernisation and upgradation of existing airports out of the AAIshands so that it can concentrate on operationalising new ones.

Power

If all goes according to plan, in 2010-11, the country is expected to add 21,441 MW of fresh power

projects the highest ever in a single year. But heres the irony: the country will still face huge power

shortages over the medium term.

Barring states such as Delhi, Sikkim, Himachal Pradesh, Jharkhand and Orissa, which are expected to

meet peak power demand in 2010-11, all other states are expected to face shortages. As many as 16 of

the 28 states may face a shortage of over 10 per cent. Of these, four states can see a shortage of 30 per

cent.

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 4/34

In The Pipeline

West Bengal tops the list of states

with upcoming power capacity in the

next year

State

No. of

Projects

Capacity

(MW)

West Bengal 5 2882

UP 5 2390

Maharashtra 3 2200

Andhra

Pradesh 8 1680

Gujarat 4 1612

Delhi 2 1608

Karnataka 3 1485

Rajasthan 3 1310

Tamil Nadu 2 1250Orissa 1 1200

Harayana 2 1100

Jharkhand 2 1025

Chhattisgarh 1 500

HP 4 439

J&K 2 240

Uttarakhand 1 200

Kerala 1 100

Sikkim 1 99

Meghalaya 1 84Assam 1 37

Total 52 21441

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 5/34

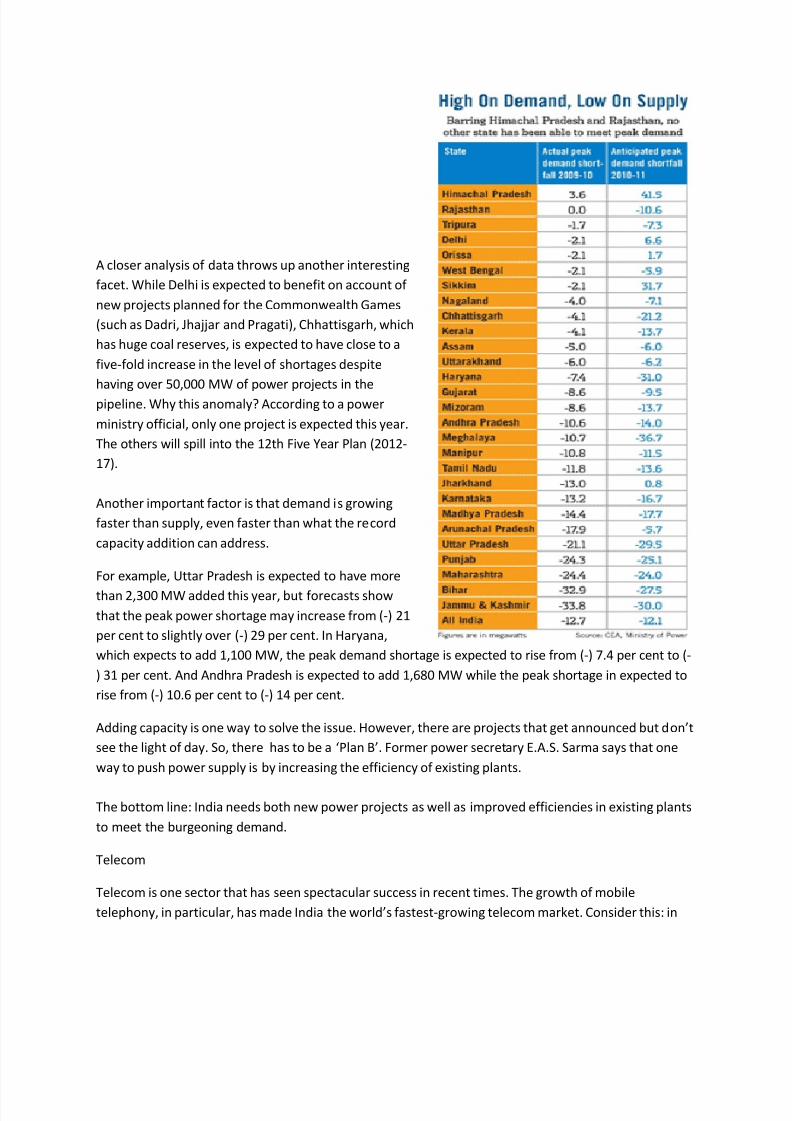

A closer analysis of data throws up another interesting

facet. While Delhi is expected to benefit on account of

new projects planned for the Commonwealth Games

(such as Dadri, Jhajjar and Pragati), Chhattisgarh, which

has huge coal reserves, is expected to have close to a

five-fold increase in the level of shortages despite

having over 50,000 MW of power projects in the

pipeline. Why this anomaly? According to a power

ministry official, only one project is expected this year.

The others will spill into the 12th Five Year Plan (2012-

17).

Another important factor is that demand is growing

faster than supply, even faster than what the record

capacity addition can address.

For example, Uttar Pradesh is expected to have more

than 2,300 MW added this year, but forecasts show

that the peak power shortage may increase from (-) 21

per cent to slightly over (-) 29 per cent. In Haryana,

which expects to add 1,100 MW, the peak demand shortage is expected to rise from (-) 7.4 per cent to (-

) 31 per cent. And Andhra Pradesh is expected to add 1,680 MW while the peak shortage in expected to

rise from (-) 10.6 per cent to (-) 14 per cent.

Adding capacity is one way to solve the issue. However, there are projects that get announced but dont

see the light of day. So, there has to be a Plan B. Former power secretary E.A.S. Sarma says that one

way to push power supply is by increasing the efficiency of existing plants.

The bottom line: India needs both new power projects as well as improved efficiencies in existing plants

to meet the burgeoning demand.

Telecom

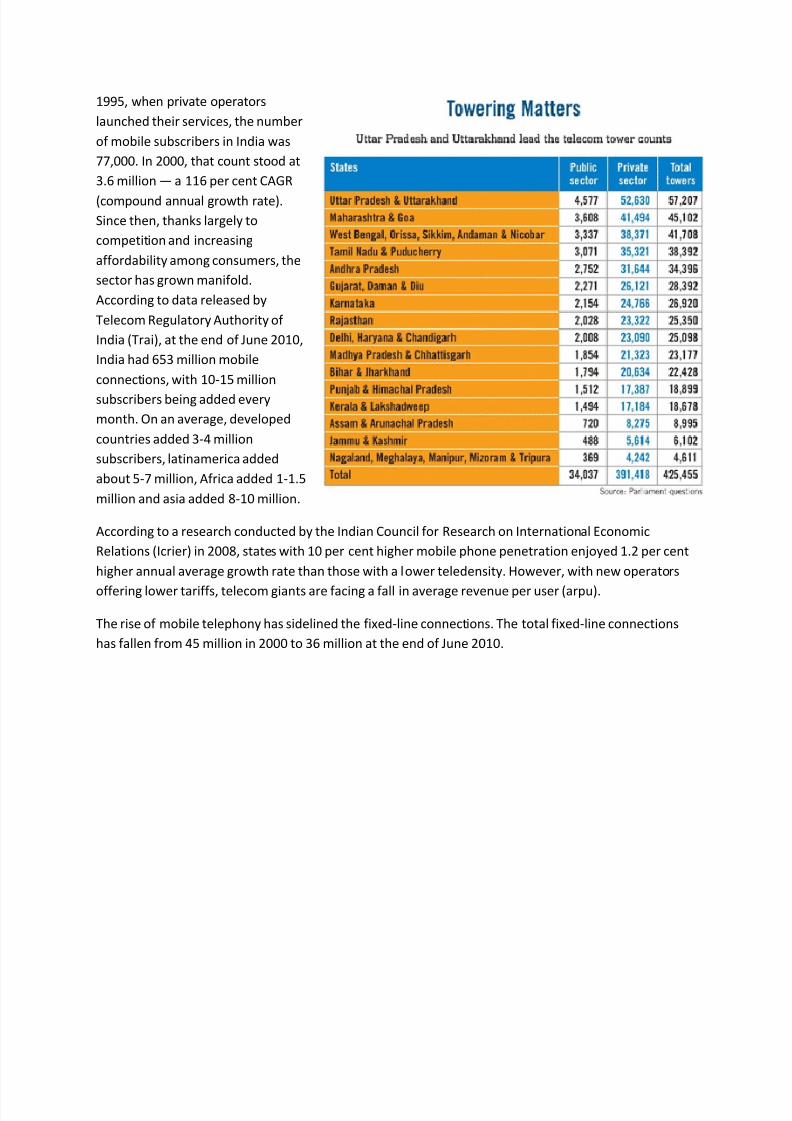

Telecom is one sector that has seen spectacular success in recent times. The growth of mobile

telephony, in particular, has made India the worlds fastest-growing telecom market. Consider this: in

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 6/34

1995, when private operators

launched their services, the number

of mobile subscribers in India was

77,000. In 2000, that count stood at

3.6 million a 116 per cent CAGR

(compound annual growth rate).

Since then, thanks largely to

competition and increasing

affordability among consumers, the

sector has grown manifold.

According to data released by

Telecom Regulatory Authority of

India (Trai), at the end of June 2010,

India had 653 million mobile

connections, with 10-15 million

subscribers being added every

month. On an average, developed

countries added 3-4 million

subscribers, latinamerica added

about 5-7 million, Africa added 1-1.5

million and asia added 8-10 million.

According to a research conducted by the Indian Council for Research on International Economic

Relations (Icrier) in 2008, states with 10 per cent higher mobile phone penetration enjoyed 1.2 per cent

higher annual average growth rate than those with a lower teledensity. However, with new operators

offering lower tariffs, telecom giants are facing a fall in average revenue per user (arpu).

The rise of mobile telephony has sidelined the fixed-line connections. The total fixed-line connections

has fallen from 45 million in 2000 to 36 million at the end of June 2010.

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 7/34

Investment Scenario: Statewise

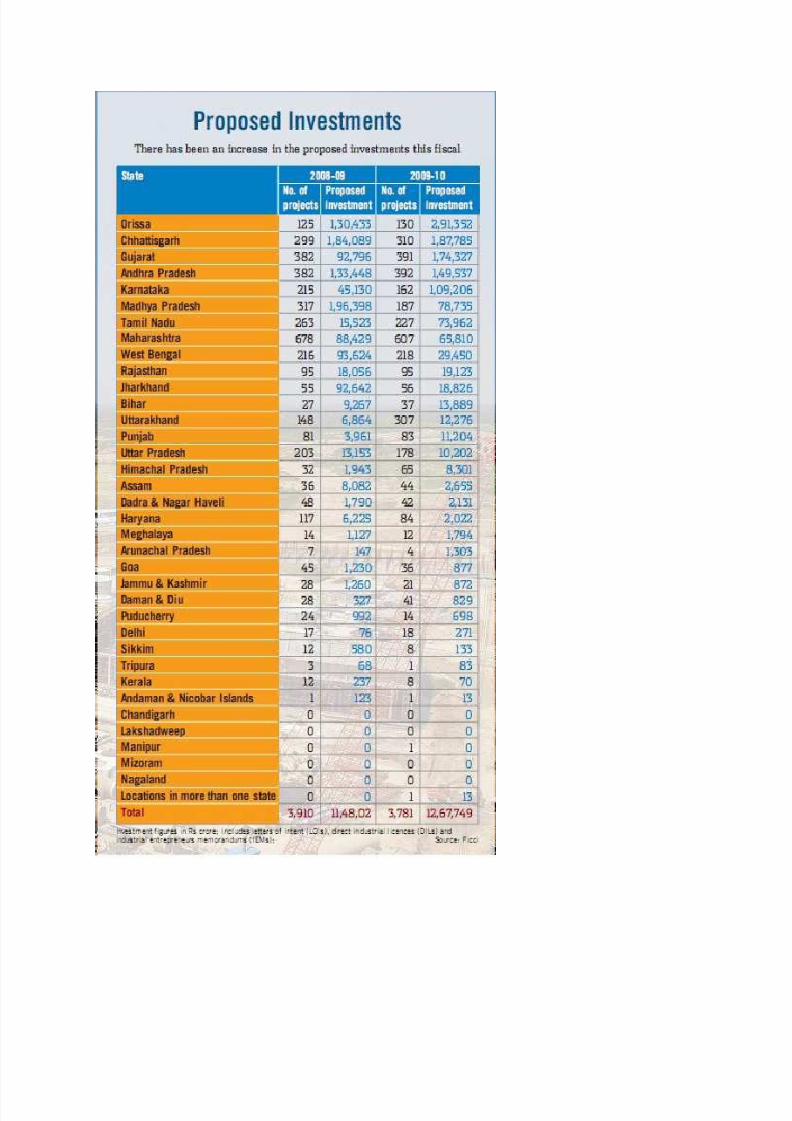

So, what attracts a business entity to a state? Obviously, availability of land and other resources, accessto markets, availability of skilled labour, etc., all matter. Orissa, Chhattisgarh and Andhra Pradesh, for

instance, offer immense natural resources.

What also matters is how the state approaches the idea of investment. Things like tax incentives, how

fast projects can start, how quickly and smoothly land allotment and labour employment clearances are

done, speed of water and electricity connections, etc., make a difference. Gujarat, for instance, is known

for its quick decision-making and good infrastructure. Most states are getting investments for their

investment-friendly approach, says Anjan Roy, adviser for economic affairs at Ficci. Adds Sunil R.

Chandiramani, partner and business leader for government services at Ernst & Young: There has to be

commitment from senior individuals within the government who reach out to the companies and makethose commitments.

Another important factor in attracting investments is political stability and security. Jharkhand, for

example, attracted investment proposals worth Rs 92,600 crore in 2008-09. But in 2009-10, the number

slumped to a mere Rs 18,800 crore, thanks to security issues.

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 8/34

In terms of attracting foreign direct investment (FDI), the northern and western financial centres top the

charts. Delhi and parts of Uttar Pradesh and Haryana attracted the most FDI in 2009-10 worth Rs 46,197

crore, pushing Mumbai (Maharashtra, Dadra & Nagar Haveli, and Daman & Diu) to second spot (Rs

39,404 crore). According to the World Investment Report 2010, India received $34.6 billion of FDI in

2009 to rank 9th globally. With domestic and foreign investments picking up, Indias economy can only

get stronger.

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 9/34

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 10/34

Major Power Hubs of Future

Going by these plans, on paper, just three states (MP,Orissa&Chattisgarh) will supply 125,000 MW

power in the next decade, and almost 34 per cent of Indias targeted capacity in the next three to four

years (taking into account the spillovers). The contemplated capacity addition during the 12th Five-year

Plan is only 100,000 MW.

More than a decade ago, Indias power map was drawn on different lines. Large projects were near the

consumer or coal mines. Development was solely by central or state governments. And what were

called super thermal power stations had capacities of only about 2,000 MW.

Now, not only is 2,000 MW small, the factors influencing the location of power stations have changed.

For instance, at Mundra (Gujarat), Tata Power and Adani Power have projects of over 8,000 MW

together; much bigger than the erstwhile super power station at Ramagundam in Andhra Pradesh,

whose increased potential is just over 3,000 MW.

Orissa, Chhattisgarh, Madhya Pradesh, Tamil Nadu and Andhra Pradesh also have power hubs.

Arunachal Pradesh has plans for hydel projects of 49,126 MW more than half of Indias estimated

80,000 MW hydel potential.

This concentration of power projects in a few regions is giving rise to power clusters and is happening

mainly due to changes in policy about who can build power plants, merchant sale and, of course, fuel

supply options.

One of the factors responsible for the spurt in mega power projects is delicensing. With generation

being delicensed, developers are free to set up projects anywhere as long as they have land and fuel

supply source, says D.V. Kapur, former chairman of NTPC. Other reforms included target-basedperformance for government power utilities; distribution in states was split into zones and converted

into companies; and power pricing was freed to an extent which made power an attractive sector.

A couple of years ago, the central government amended the hydel power policy allowing a promoter to

use 40 per cent of the output for merchant sales. Arunachal Pradesh emerged a hydel power major.

Upper Siang project on the Dibangriver alone can produce 11,000 MW similar to the coastal power

cluster at Krishnapatnam in Andhra Pradesh. Projects totalling 30,000 MW have already been awarded

to developers. Private bidders included big names such as Anil Ambanis Reliance Power, LancoInfratech,

KSK Energy, GMR and GVK, as well as smaller players such as Hyderabad-based Rithwik Projects.

A Win-Win Deal: How can a private player gain? States get investments as well as cheap power. In Madhya Pradesh, the power generator has to offer 10

per cent of the output at variable cost, which can even be below Re 1 per unit (the fixed or the capital

cost can be Re 1-Rs 2.5 per unit). Indiabulls has offered the Chhattisgarh government a long-term rate of

less than Re 1 per unit for a part of the output from its 1,320-MW Bhaiyathan project; it can sell the

balance in the merchant power market where rates are Rs 4-5 per unit. Its offer of Re 1 per unit is lower

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 11/34

than the Rs 1.19 per unit that Reliance ADAG offered for the Sasan mega project in Madhya Pradesh.

A Look into the Competitors Moves

Videocon in Oil & Gas, Telecom & Power: Picked up stakes in Brazilian offshore block which discovered

oil. Also, another field gave such good news. Videocon Group chairman VenugopalNandlalDhoot was

suddenly sitting on a goldmine.

Globally, oil and gas delivers a gross margin of 50-60 per cent, while durables offers 13-15 per cent. The

saviour will be the oil and gas find, which will keep its cash flow (going). Or, it will be tough for the

company operating in highly competitive verticals, says a senior official from a foreign rating agency.

The pivot of this makeover is oil and gas in which Dhoot will invest $500-600 million in the next 3-5

years. The second axis of this change is a thrust into the power sector where Videocon hasnt had the

most auspicious beginning. Its first attempt in 1998 with a 1,000-MW plant in Tamil Nadu did not go

through as the state government refused to sanction it. But it has planned two 2,400-MW thermal

plants in Gujarat and Chhattisgarh at an estimated investment of Rs 11,600 crore over four years.

Telecom, where Videocon has already invested an equity capital of Rs 540 crore in four circles, will see

fresh funds of Rs 14,000 crore over five years for an all-India rollout. Established businesses such as

consumer durables are not as capital intensive as the new ones, and DTH is a small business in

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 12/34

comparison. Before the makeover is complete, Dhoot expects to treble the groups topline to $10 billion

by 2012.

Dhoots first oil interest the ONGC-Cairn Energy-Videocon consortiums 15-year-old fields at Ravva in

Andhra Pradesh have seen production fall 44 per cent last year to 40,000 barrels a day as reserves

begin to deplete. At peak production, Videocons share of oil from the new fields would be around

10,000 barrels a day, and gas at 0.45 million metric standard cubic meter per day (mmscmd). It may be

small, but significant. In the private sector, for instance, RIL produces 50,000 barrels of oil and 62

mmscmd of gas and Cairn produces 69,095 barrels of oil equivalent per day.

Videocon is still a small player (in oil and gas), compared to a Reliance Industries and even Cairn Energy.

The business is not big, but it is profitable, and the company has got in at the right time, says

AvinashGorakshakar, head of research at Anagram Stock Broking. Oil contributes about Rs 1,100 crore to

the groups Rs 10,674 crore revenues.

Dhoot says his biggest advantage is that oil and gas investment will make money at global crude prices

of $40 per barrel and above. If oil prices go down to $30, we lose, he says. But with crude prices

hovering around $75 per barrel, the margins are good for now.

He now eyes his consortias eight other blocks in five countries (East Timor, Brazil, Mozambique,

Indonesia and Australia) and hopes to continue the dream run by entering Kenya, where the gas

opportunity is l ikely to be four times bigger than Mozambique.

To his credit, Dhoot knew his limitations in oil and gas. In spite of a decade and a half of experience of

investing in oil and gas at Ravva, he did not bid as an operator in any of the international assets. Bidding

as an operator-investor is not only the big boys multi-billion dollar game, but also risky for the low

success rates in discoveries. So, the group continues to be a minority investor in each of the oil and gas

assets.

But even that needs detailed assessment of oil fields. So, as far back as 1992, Videocon had hired S.

Padmanabhan, a retired IAS officer, as a director to advise on the oil and gas and power businesses. In

1996, it set up a research centre in Chennai with three geo-scientists and four geo-physicists all ex-

ONGC advising Dhoot in bidding for oil and gas assets.

Power Foray: While a Dhirubhai-like goal of a 5,000-MW plant is still some time away, Videocon is

starting out with two projects of 2,400 MW each in Gujarat and Chhattisgarh, and the company has

pumped in Rs 400-450 crore. This being a low-margin business, players have to be careful in assessing

risks such as execution, raw material availability and tariff,Today, we can sell power in the open

market. The peak demand price is as high as Rs 7 per unit, against the generation cost of Rs 2.5-3 per

unit.

Telecom Tussle: Videocon plans to invest Rs 14,000 crore in telecom over the next five years, and has

targeted a market share of 6-7 per cent with 100 million subscribers. But with Indias mobile subscriber

base touching 618 million and the average revenue per user falling to just Rs 260-270 per month, the

challenge is differentiation in a crowded market. Also, Videocon failed to win anything in the recent 3G

auctions.

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 13/34

But as it turns out, Dhoots may not have a long-term view on telecom, and may wish to monetise the

investment soon enough. Cellcos can bring in up to 74 per cent foreign partnerships. People are waiting

to enter India. One would realise a better value of our business if we cover a greater part of the country,

garnering more subscribers, says Saurabh.

RIL in shale gas: RIL has invested $3 billion in shale gas exploration in North US. What is really attractinghydrocarbon investors such as RIL to shale gas is the possibility of extracting shale gas at affordable rates

to make it viable for production and sale. Half a decade ago, shale gas finds were not viable. However,

technologies such as horizontal drilling and developments such as hydraulic fracturing has made gas

extraction from shale rocks more affordable.

It may still be a while before shale gas starts flowing freely through gas stations the world over. Or, even

in the US. Production of shale gas is viable at around $5 per million British thermal units (mmbtu) while

current spot price is around $6 per mmbtu (long-term contracts are being tied at over $7 per mmbtu).

However, the hope is that as soon as the US and the world economy recovers, demand should perk up,

raising prices to the level that makes shale gas affordable. Alternatively, new extraction techniques

could bring down costs, making it viable even before. The belief is that the gap between viability and

current costs is so low that a solution will emerge sooner rather than later.

As for RIL, the bet on shale gas is crucial to Ambanis dream of doubling RILs enterprise value from $80

billion to $160 billion in the next decade. We will enhance efficiencies across the chain by drawing on

our experience in drilling and project management. We will commit capital alongside proven low-cost

operators to accelerate the development of this resource, he said at the AGM. Reliance viewed

foreign ventures in a more sombre light because of high political risk. To compensate the risk, it wanted

10 per cent higher return compared to its average of 20 per cent return in India, says a Mumbai-based

analyst. But with shale gas, RIL may be seeing foreign investments in a different light.

GMR

As visible as airports are in the groups business they are impressive showcases the projects

portfolio is itself changing. In three years from now, energy and power projects will form the biggest

chunk, accounting for more than half of the groups revenues and capital expenditure.

Infrastructure projects have a few critical success factors: the height of the entry barriers, the ability to

get long-term debt financing, execution within budget and on time, backed by a well-designed overall

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 14/34

plan. On the face of it, most analysts seem to agree that GMR has demonstrated that it has all the

necessary tools, or is in the process of developing

them.

Powering Through

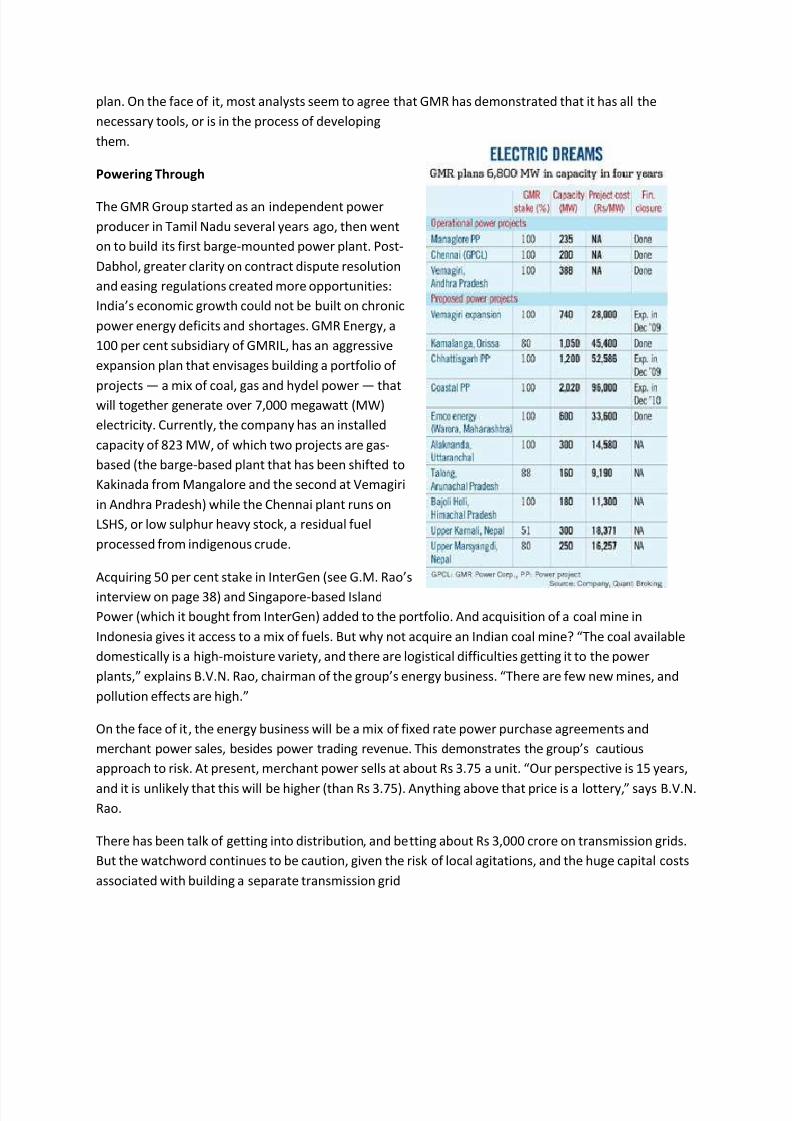

The GMR Group started as an independent power

producer in Tamil Nadu several years ago, then went

on to build its first barge-mounted power plant. Post-

Dabhol, greater clarity on contract dispute resolution

and easing regulations created more opportunities:

Indias economic growth could not be built on chronic

power energy deficits and shortages. GMR Energy, a

100 per cent subsidiary of GMRIL, has an aggressive

expansion plan that envisages building a portfolio of

projects a mix of coal, gas and hydel power that

will together generate over 7,000 megawatt (MW)

electricity. Currently, the company has an installed

capacity of 823 MW, of which two projects are gas-

based (the barge-based plant that has been shifted to

Kakinada from Mangalore and the second at Vemagiri

in Andhra Pradesh) while the Chennai plant runs on

LSHS, or low sulphur heavy stock, a residual fuel

processed from indigenous crude.

Acquiring 50 per cent stake in InterGen (see G.M. Raos

interview on page 38) and Singapore-based Island

Power (which it bought from InterGen) added to the portfolio. And acquisition of a coal mine in

Indonesia gives it access to a mix of fuels. But why not acquire an Indian coal mine? The coal available

domestically is a high-moisture variety, and there are logistical difficulties getting it to the power

plants, explains B.V.N. Rao, chairman of the groups energy business. There are few new mines, and

pollution effects are high.

On the face of it, the energy business will be a mix of fixed rate power purchase agreements and

merchant power sales, besides power trading revenue. This demonstrates the groups cautious

approach to risk. At present, merchant power sells at about Rs 3.75 a unit. Our perspective is 15 years,

and it is unlikely that this will be higher (than Rs 3.75). Anything above that price is a lottery, says B.V.N.Rao.

There has been talk of getting into distribution, and betting about Rs 3,000 crore on transmission grids.

But the watchword continues to be caution, given the risk of local agitations, and the huge capital costs

associated with building a separate transmission grid

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 15/34

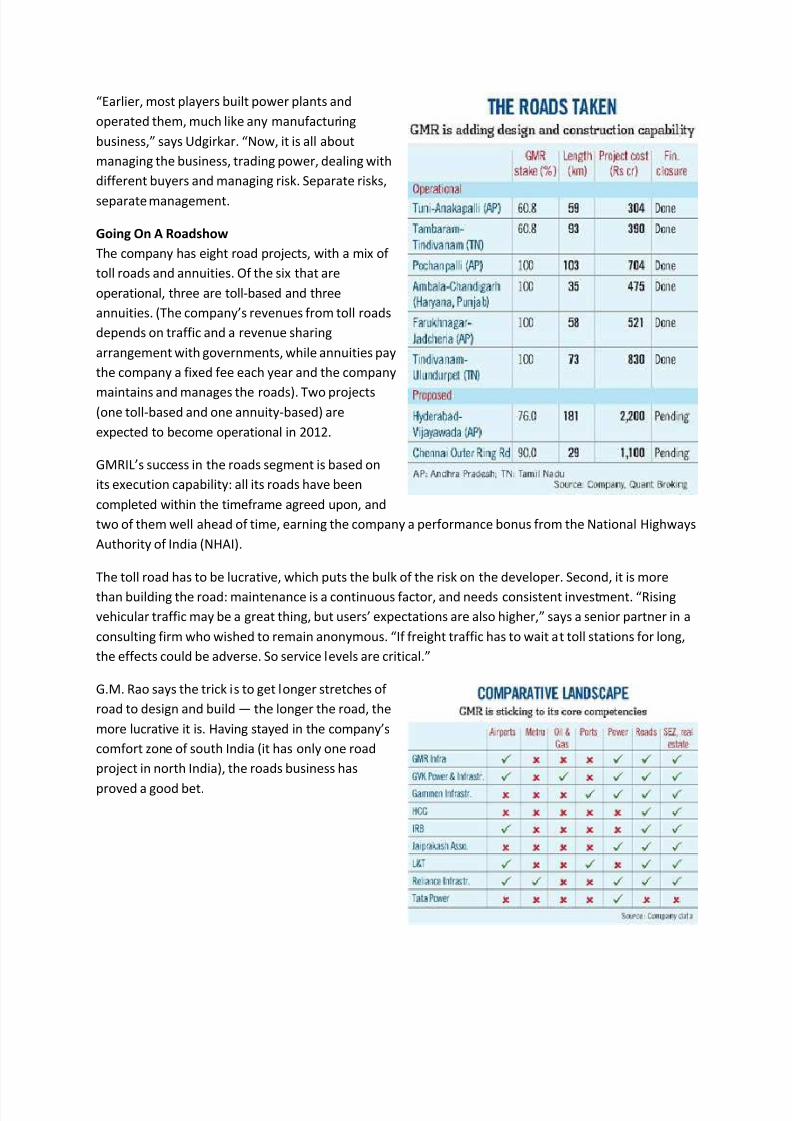

Earlier, most players built power plants and

operated them, much like any manufacturing

business, says Udgirkar. Now, it is all about

managing the business, trading power, dealing with

different buyers and managing risk. Separate risks,

separate management.

Going On A Roadshow

The company has eight road projects, with a mix of

toll roads and annuities. Of the six that are

operational, three are toll-based and three

annuities. (The companys revenues from toll roads

depends on traffic and a revenue sharing

arrangement with governments, while annuities pay

the company a fixed fee each year and the company

maintains and manages the roads). Two projects(one toll-based and one annuity-based) are

expected to become operational in 2012.

GMRILs success in the roads segment is based on

its execution capability: all its roads have been

completed within the timeframe agreed upon, and

two of them well ahead of time, earning the company a performance bonus from the National Highways

Authority of India (NHAI).

The toll road has to be lucrative, which puts the bulk of the risk on the developer. Second, it is more

than building the road: maintenance is a continuous factor, and needs consistent investment. Rising

vehicular traffic may be a great thing, but users expectations are also higher, says a senior partner in a

consulting firm who wished to remain anonymous. If freight traffic has to wait at toll stations for long,

the effects could be adverse. So service levels are critical.

G.M. Rao says the trick is to get longer stretches of

road to design and build the longer the road, the

more lucrative it is. Having stayed in the companys

comfort zone of south India (it has only one road

project in north India), the roads business has

proved a good bet.

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 16/34

OIL RETAIL BUSINESS: Has price deregulation helped?

The retail fuel pump owners and managers of three private

sector companies Essar, Reliance Industries and Shell

are hoping that this move will give them the edge to get

their business back on track, at least partially (diesel pricesare still regulated). At least Essar and Reliance fuel pumps

are hoping that their more efficient refineries and better

managed buying capacities, coupled with quicker decision

making, will help them undercut public-sector fuel pumps in

petrol prices and woo away customers.

At the moment, the three players have a mere 2,829 pumps

between themselves compared to around 37,331 pumps of the public-sector oil marketing companies

(OMCs). The market share of the private players in the fuel retail business is a minuscule 4 per cent of

the overall 53 million tonnes retail market. Of the trio, Essar has the biggest retail operation currently

it has 1,340 outlets and 2.5 per cent of the total market. It has sanction to set up 2,500 by the end of the

year. Reliance Industries has 600- odd pumps functioning.

Shell is the smallest, and perhaps the weakest of the lot. It has 74 pumps operating currently, and it is

handicapped by the fact that it does not have any refinery of its own. It buys petrol and diesel from the

Mangalore Refinery, and sells it

through its pumps. So its

flexibility in pricing is

limited.(M&M can also enter

this way.)

Analysts expect a price war to

break out soon at least in

petrol and in the areas the

private sector players have their

pumps because of a few

reasons. For one, given that the

private sector players

really have no other weapon

than pricing in their armoury totake away customers from

public-sector pumps, they could

play it to the hilt. More

importantly, the public sector

OMCs will be somewhat

handicapped initially at least.

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 17/34

Sources in the petroleum and natural gas ministry say that the public sector OMCs are expected to

maintain pricing parity with each other, and also revise petrol prices only once every three weeks. On

the other hand, Reliance and Essar will not have to deal with issues like this. Also, because they have

modern refineries capable of handling a wide range of crude oil varieties and very efficiently at that,

they have a cost advantage in terms of refining compared to public sector OMCs. Many of the old public-

sector refineries that supply oil are capable of producing only limited varieties of oil, which makes them

somewhat uncompetitive while buying crude from the global market.

Currently, Essar seems best poised to take advantage of the petrol decontrol move. It runs its retail

outlets in a Franchisee Model, wherein the franchisee brings in suitable land, which is taken on lease

by the company at the rate of 5 per cent of the government assessed value of the land. Then the

franchisee puts up the RO as per Essar design and he is compensated for the same by way of Return on

Investment at the rate of 5 per cent of the investments every year. He then gets commission for the

product bought and sold by him.

Reliance operates through two models Coco (company owned, company operated) and Dodo (dealerowned, dealer operated). The dealer-owned, dealer-operated outlets had the worst time during the

price hike, because they could not remain competitive. Most of the 815 outlets that closed were dealer-

owned outlets. Reliance compensated them by buying their land and helping them exit when the

businesses became unviable. Analysts say that Reliance will expand mostly through the company-owned

and -operated route.

Is power profitable?

Currently, around 100 power projects are being developed by the private sector in India.Most of these

plants have an installed capacity of over 1,000 megawatt (MW), and add up to over Rs 5,00,000 crore of

investment. But a similar enthusiasm in power projects was witnessed just over a decade back. Of that

list, totalling 74,000 MW, barely 2,000-3,000 MW actually got commissioned. Investors came and left,

and the projects remained only on paper. So what has changed over the past 10 years for this renewed

enthusiasm?

The biggest attraction is something that did not exist 10 years ago power trading. A rather obtuse

concept for a power-deficient nation, power trading on exchanges is a lucrative opportunity for power

producers with peak rates rising to as high as Rs 7-8 per unit especially during summer compared

to Rs 2.5-3 per unit for power sold to the state utilities. It is this high price that states are willing to

pay that encourages merchant power producers to bear the risks instead of opting for assured long-

term power supply contracts for the entire project.

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 18/34

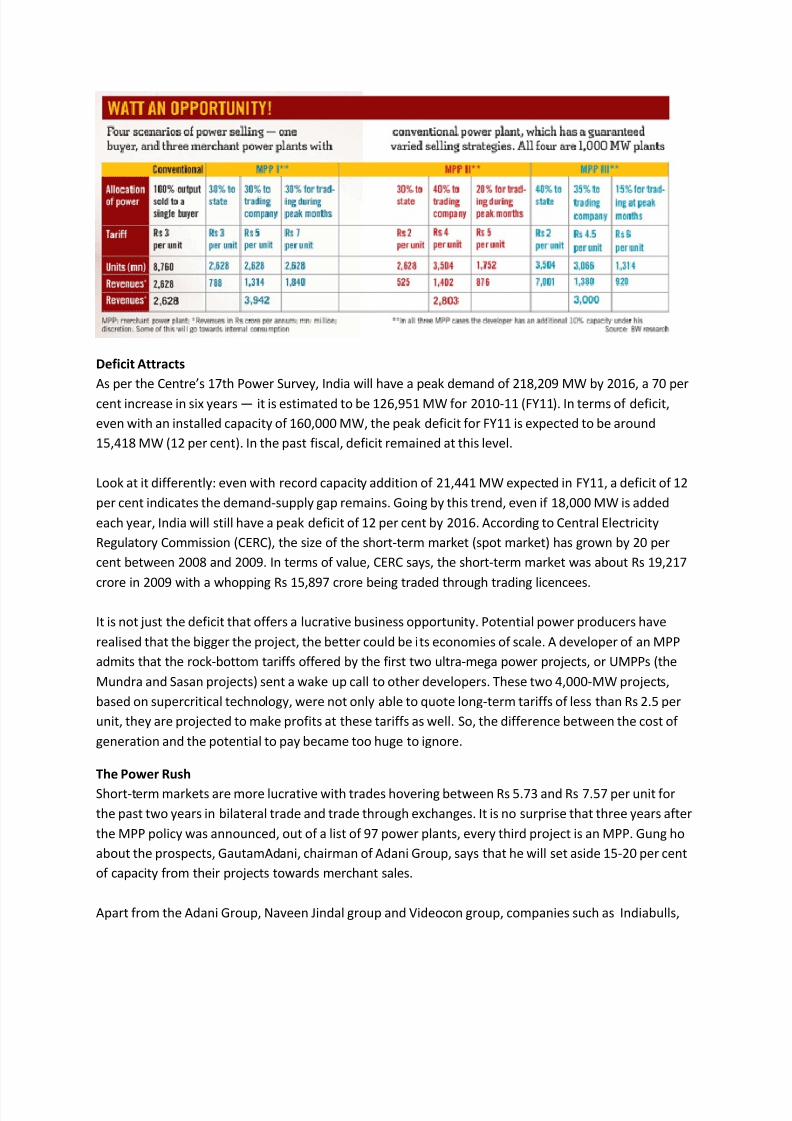

Deficit Attracts

As per the Centres 17th Power Survey, India will have a peak demand of 218,209 MW by 2016, a 70 per

cent increase in six years it is estimated to be 126,951 MW for 2010-11 (FY11). In terms of deficit,

even with an installed capacity of 160,000 MW, the peak deficit for FY11 is expected to be around

15,418 MW (12 per cent). In the past fiscal, deficit remained at this level.

Look at it differently: even with record capacity addition of 21,441 MW expected in FY11, a deficit of 12

per cent indicates the demand-supply gap remains. Going by this trend, even if 18,000 MW is added

each year, India will still have a peak deficit of 12 per cent by 2016. According to Central Electricity

Regulatory Commission (CERC), the size of the short-term market (spot market) has grown by 20 per

cent between 2008 and 2009. In terms of value, CERC says, the short-term market was about Rs 19,217

crore in 2009 with a whopping Rs 15,897 crore being traded through trading licencees.

It is not just the deficit that offers a lucrative business opportunity. Potential power producers have

realised that the bigger the project, the better could be its economies of scale. A developer of an MPP

admits that the rock-bottom tariffs offered by the first two ultra-mega power projects, or UMPPs (the

Mundra and Sasan projects) sent a wake up call to other developers. These two 4,000-MW projects,

based on supercritical technology, were not only able to quote long-term tariffs of less than Rs 2.5 per

unit, they are projected to make profits at these tariffs as well. So, the difference between the cost of

generation and the potential to pay became too huge to ignore.

The Power Rush

Short-term markets are more lucrative with trades hovering between Rs 5.73 and Rs 7.57 per unit for

the past two years in bilateral trade and trade through exchanges. It is no surprise that three years after

the MPP policy was announced, out of a list of 97 power plants, every third project is an MPP. Gung ho

about the prospects, GautamAdani, chairman of Adani Group, says that he will set aside 15-20 per cent

of capacity from their projects towards merchant sales.

Apart from the Adani Group, Naveen Jindal group and Videocon group, companies such as Indiabulls,

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 19/34

Moser Baer, Sona Group and Navbharat Ventures, all have also announced plans to set up MPPs. If I get

customers who are willing to pay tariffs of over Rs 5 per unit, there is a ready market for my project,

says KuldeepDrabu, advisor of Videocon Industries, which is executing an MPP in Gujarat.

However, S.S. Rao, who till recently was joint MD and CEO of JSW Energy, says that once the plant, its

buyers and the avenues of finances have been identified, it is very important to maintain the scheduleand execute the plant within 36-40 months.

Is MPP correct way to enter?

In 2006, the Union power ministry came out with the concept of merchant power plants (MPPs) with

generation capacity of less than 1,000 megawatt (MW) each. These private power plants which could

be standalone plants or part of the capacity of regular power plants could be set aside for merchant

power would not be tied to any power distribution firm or electricity board through power purchase

agreements (PPAs). Instead, they would supply power to either power distributors or open access

consumers through an open grid. They are confident that there are consumers who are willing to pay

in a shortage.

The response has been phenomenal. Several private players have invested significant amounts in setting

up MPPs. And banks have also been willing to live with the risks and finance their projects. The

Chhattisgarh government, which is sitting on huge coal reserves, has entered into memoranda of

understanding (MoUs) with companies for over 50 projects, each over 1,000-MW capacity. Of course,

not all will finally take off as MPPs or even as conventional power projects with firm buyers. In all, an

estimated 16 projects with a capacity of 14,000-15,000 MW of merchant power is now in the pipeline,

say power ministry sources.

The Enablers To run a power plant, you need fuel, and coal dominates in India. Coal has been in short supplyin recent times even for the existing power plants. So, to ensure merchant power projects do not

come a cropper right at the outset, the power ministry has reserved coal for them.

Fifteen coal blocks with estimated reserves of about 3.6 billion tonnes have been identified for

merchant and captive power plants. Of this, about 2.4 billion tonnes are expected to be reservedfor MPPs. There are some who plan to import coal.

The government has also allowed hydel power plant developers to set aside 40 per cent of

capacity for merchant sales, besides permitting developers of regular thermal plants to keep aside

up to 15 per cent of capacity for merchant sales.

But what has really got the sector buzzing is the Rs 1.19 tariff that Reliance Power, the developer

of the Sasan ultra mega power project (UMPPs, plants with capacity of 4,000 MW), has promised to charge. Normal prevailing tariffs in the country average Rs 2.63. Sasan¶s tariff has

made merchant power developers believe that they, too, can peg their costs really low. A lip-smacking possibility, given that state governments in distress have been willing to pay more than

Rs 10 per unit in recent times. That translates to amazingly high margins in the best case

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 20/34

scenario. ³If I get customers who are willing to pay tariffs of over Rs 5 per unit, then there is aready market for my project,´ says KuldeepDrabu, director of Videocon Industries.

BW Research (Pic ByTribhuwan Sharma)

According to ministry officials, Union Power Minister Sushil Kumar Shinde is planning tomove a proposal to extend the tax sops ² excise

and customs duty waivers ² given to UMPPs toMPPs. If implemented, these would help further

bring down the cost of generating power and,consequently, the tariffs.

T.N. Thakur, chairman and MD of PTC (Power Trading

Corporation), says, A plant will be called an MPP if

the developer has only short-term contracts and isstill to enter into long-term contracts. By that definition, MPPs should be high-risk projects because

they do not have life-long power-purchase pacts that Indian power plants have traditionally had with

state governments. In reality, however, these are not that risky.

For, if the yardstick for an MPP is that it should not have any long-term contracts, then practically none

of the current breed of projects would qualify as MPP most of the projects have a mix of both short

and long-term contracts. By government definition, a long-term contract is for seven years and above, a

medium-term contract is between one and seven years, and anything less than one year is a short-term

contract.

Consider these examples. The 1,000 MW Hinduja National Power project in Andhra Pradesh is classified

as MPP, but not all of its capacity is marked for merchant sales. Officials say around 60 per cent of the

output has been tied up with PTC. The promoter will be selling 25 per cent of the plants capacity to the

state, while the balance 15 per cent is left for the market.

Even JSW Energys 1,200-MW Ratnagiri project in Maharashtra is split into four units of 300 MW each.

Sources say, though the project is identified as MPP, it has a conventional power-purchase agreement to

sell 300 MW to the state at Rs 2.72 per unit. Another 300 MW is also under discussion with the state.

Only the balance is expected to be set aside for merchant sales.

According to government policy, there are typically three ways to procure power. First, the case 1

bidding for power, where the location, technology, or fuel is not specified by the buyer.Second, the case

2 projects where the buyer specifies the location, fuel and quantum of power, and offers the project to

the bidder with lowest tariff. The third mode is buying through exchanges and short-term bilateral

trade.

MPPs can fit into any of the three cases depending on the policies of the state where the project is

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 21/34

located as well as the

riders attached with a

project when it is offered

to a developer

especially in hydel

projects. For instance, for

case 1 projects located in

Gujarat, after having

acquired land, the state

policy only requires the

developer to set aside 10

per cent of capacity for

sale to the state. In case the government gives the fuel, the developer gets 30 per cent capacity to sell in

any manner he likes. In Maharashtra, this amount is 50 per cent.

Take Uttar Pradesh. On 16 June the state called for long-term bids for 2,000 MW to cater to a portion of

base load (minimum power requirement during the entire day through the year) requirements of the

state. Such bids show there will be a steady demand for power from projects located anywhere in the

country.

In fact, developers are innovating ways to sell power in the merchant market. Power traders are

entering power-tolling agreements with power companies. In these agreements, fuel for the plant is

arranged by the trading company. PTC has entered into one such agreement with Meenakshi Group that

plans a 540-MW plant in the Nellore district of Andhra Pradesh. Under the arrangement, PTC will buy 70

per cent of the power and the balance is left for merchant sales.

The Risks

One of the important aspects that needs attention is ensuring states implement the provisions of open

access, says Razdan. This will allow a consumer to choose his source of supply.

To spread the risk, some promoters would like to apportion some capacity for merchant sale and tie up

the balance with assured buyers through PPAs. The key for attracting debt financing for an MPP,

according to Singh of PFC, is that the tariff should be around the national average of Rs.2.63 per unit.

The Housing Sector: How Lucrative It Is?

There is a slight difference between the current construction activity and the one during the boom of 2006-08. During that period, while many residential projects had been announced and built, the big

focus area for many of the big builders was commercial space. Currently, there is relatively little activity

on the commercial property area, which is still struggling to offload the huge inventory built up during

the boom.

But interest in buying homes has picked up sharply once again. Reserve Bank (RBI) data shows there has

been a robust growth in the disbursement of home loans in the past few months. Fresh home loans

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 22/34

disbursed for 12 months

ending 26 February 2010 (the

latest data available)

amounted to Rs 22,880 crore,

compared to the Rs 16,431

crore disbursed over the same

period in the previous year.

Mixed Trends In Low-Cost

Housing

At the trough of the slowdown

from July 2008 to end 2009,

desperate builders abandoned

premium projects as demand

had plunged. They turned to

mass, budget homes to keepthe market ticking. Some

cautious builders are still

sticking to affordable housing

houses costing less than Rs

20 lakh in the metros. In April,

some big Mumbai builders

signed anMoU with the

Maharashtra government to

build 500,000 affordable

homes in the Mumbai Metropolitan Region (MMR) over five years. The government has promised torelax density norms. In the National Capital Region Gurgaon, Faridabad, Noida, Ghaziabad and

Indirapuram dozens of low-priced projects have been announced. But a number of builders who had

embraced low-priced housing projects are slowly upgrading many of these to target middle- and higher-

income groups. These segments, after all, offer far better returns.

Of course, there are still those who swear by mass housing. This is the only way out in the long run.

Builders must learn to work with small margins and large volumes, says Sunil Mantri, president of the

Maharashtra Chamber of Housing Industry.

Interestingly, builders in NCR are also creating projects targeting buyers who prefer independent floors

on low-rise flats buildings that do not exceed ground +4 floors. Low-rise flats, long adopted in Delhi

Development Authority colonies, are 25 per cent cheaper to build, though it also means less utilisation

of land. In suburbs where land is cheap, this allows builders to peg competitive prices for mid-sized

homes. Nearly 25-30 per cent of new launches in Gurgaon and Noida are in this category.

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 23/34

PPP scene in India:

PPPs: Do they Make it Easier?

Given the central and state governments financial position, its fairly clear that private publicpartnerships (PPPs) will hog a huge chunk of infrastructure projects in the country. Thus far, Rs 1,36,000

lakh crore in 300-odd projects has been the envisaged investment through PPPs across sectors. Contrary

to popular expectations, domestic players have accounted for roughly Rs 1,34,000 lakh crore in 278

projects, the rest going to foreign players.

But the success record for PPPs is a little mixed; in ports, which account for 32 per cent of the total

investment (but where GMRIL has no presence) things are going well, while in airports (15 per cent)

regulatory hurdles are an issue. There is always the risk of future regulation, says VishwasUdgirkar,

executive director at PricewaterhouseCoopers, the global consultancy. We will have to wait and see

how the new regulator, the Airports Economic Regulatory Authority (AERA), views its role.

This might explain why just five airport projects have been awarded (a sixth is for a cargo terminal in

New Delhi), of which two Kolkata and Chennai are being handled by the Airports Authority of India

(AAI). Roads account for another 35 per cent of the total investment, urban infrastructure about 4 per

cent and energy about 13 per cent.

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 24/34

Opportunity in Power Equipment Manufacturing

For five decades, India had only

one power equipment

manufacturer government-

owned Bharat Heavy Electricals(BHEL). Over the next two years,

BHEL will have at least three

companions, all private sector

joint ventures (JVs): L&T-MHI, a

JV between Larsen & Toubro

(L&T) and Japans Mitsubishi

Heavy Industries (MHI); Bharat

Forge-Alstom, a JV between

Baba Kalyanis Bharat Forge and

Frances Alstom; and JSW-Toshiba, between Sajjan Jindals

JSW and Japans Toshiba.

Why the rush? Indias power

generation capacity is projected

to explode by 2030, making the

country the worlds third biggest

power producer. Current

demand is so high that BHEL,

even with an annual capacity of 15,000 MW, already has an

order book of this size. Besides

BHEL, there are Chinese

companies, whose equipments

reliability is doubtful, and

manufacturers from developed

countries, who are expensive.

This presents a golden opportunity for Indian companies to participate in a market that, as per estimates

of World Energy Outlook towards capacity addition, amounts to Rs 60,000 crore annually. Profit margins

of 18-20 per cent have only added to the lure.

Domestic production of power equipment gives immense advantage to Indias power sector. The three

JVs, for instance, can manufacture equipment for 10,000-12,000 MW within 3-4 years, effectively

doubling domestic capacity.These companies plan to compete with not only BHEL, but also the rapidly

advancing Chinese companies, whose progress played a big role in the government encouraging private

sector production of power equipment.

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 25/34

The Chinese Invasion

Chinese manufacturers, who have been gaining ground, supply equipment that is 20 per cent cheaper,

and have garnered 20 per cent of the market. Ravi Uppal, managing director and CEO of L&T Power, says

orders worth 50,000 MW has been placed with Chinese companies.

According to industry observers, the problem with Chinese equipment is, nobody knows whether they

will perform as per their rated output, say, in 10 years. But that has not stopped private sector power

companies from placing huge orders with Chinese equipment suppliers, creating a sense of unease

about the future.

The government caught on to this early and, in 2007, decided to encourage domestic production of

power equipment from companies other than BHEL. At the initiative of Prime Minister Manmohan

Singh, veteran technocrat V. Krishnamurthy, the then finance minister P. Chidambaram and others, the

government decided to give preference for government power projects to JVs of Indian private sector

companies and foreign power equipment manufacturers. But there was a caveat: the foreign companyhad to transfer its technology to the Indian partner over the years.

The strategy worked. Foreign companies saw good reason to come into India in a JV due to the sheer

size of the opportunity. In fact, the L&T-MHI (51:49 per cent equity distribution) combine has already

bagged orders more than its initial capacity.

Reason to Invest In HealthCare

The Finance Bill extended a five-year tax holiday granted to new hospitals with 100-plus beds in semi-

urban and rural areas in 2008 to such projects in large cities such as Mumbai, Pune, Chennai, Kolkata

and the national capital region. The fact that the incentive is no longer limited by geography should

help unlock future investments in the sector, says Vishal Bali, CEO, Fortis Hospitals

How events can present infrastructure opportunities to a state: Case Study of Delhi

Thanks in part to the massive infrastructure build-up for the Commonwealth Games, Delhi now tops the

list as the most competitive state to do business in, relegating Maharashtra to second place. The fact

that Delhi, being Indias capital, is the centre of political power, does tend to sway businessmen as well

as workers its way. But to its credit, the state has also taken several steps to ensure heightened

commercial activity. In fact, out of the four major parameters of the BW-Institute for Competitiveness

study, Delhi tops on three.

In the past two years, Delhis government stepped up revenue expenditure massively by Rs 3,971

crore between 2008 and 2010 leading to visible improvements on the ground. While spending on

transport and communication went up by 60 per cent, education, sports and culture spend rose by 66

per cent. Expenditure on energy rose by a huge 117 per cent. With the Commonwealth Games in mind,

the Centre has also pumped in money to raise the states infrastructure to world class standards.

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 26/34

Therefore, Delhi now has new metro lines,

a new airport metro express, new flyovers

and bridges changes that cannot be

missed.

Delhis Public Works Department (PWD)alone has more than doubled its spending

from Rs.533 crore in 2008 to over

Rs.1,230crore in 2009. For the Games, the

Delhi PWD is building 26 flyovers and 31

foot over-bridges. Nineteen flyovers have

been completed. Also, according to chief

minister Sheila Dikshit, over the next three

to four years, Delhi should have 10,000

new buses currently, it has 3,000. As

many as 1,475 buses will be procuredbefore August for which the Delhi

government allotted Rs.2,019crore in the

2010-11 Budget.

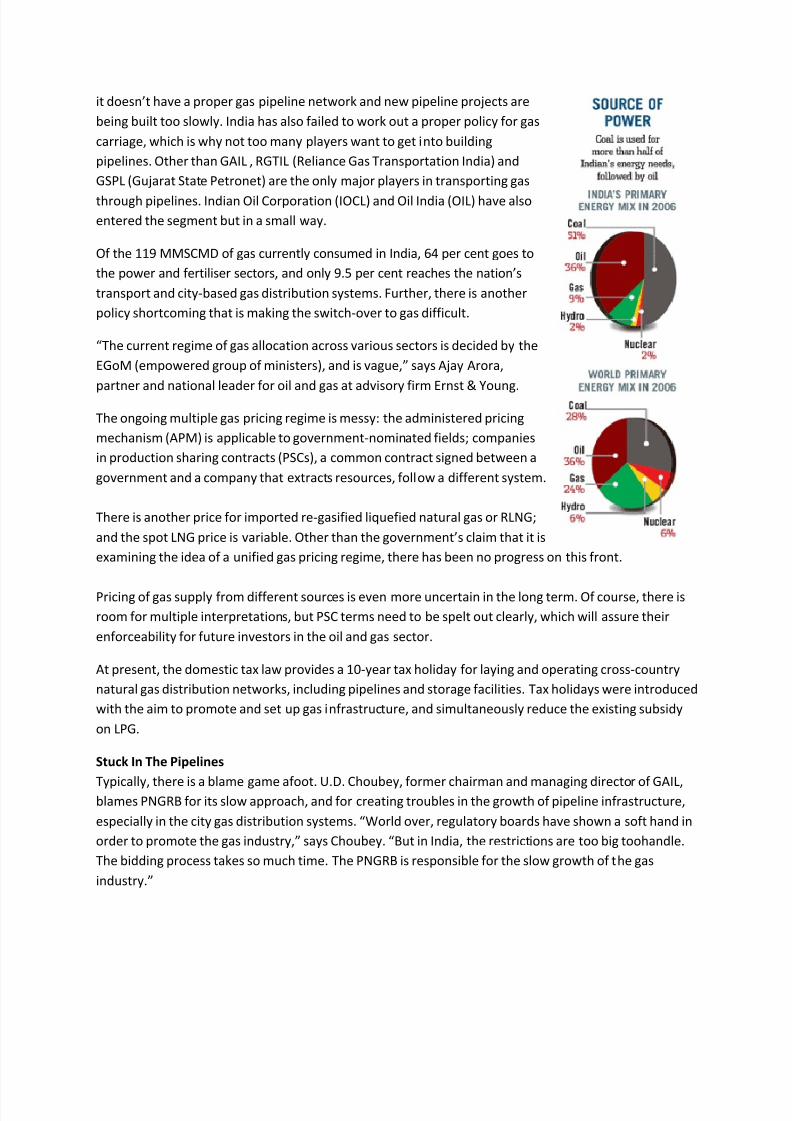

The Gas Distribution Status

Worldwide, gas discoveries and production are taking centre-stage even while oil production is slowing

down somewhat. For most of the world, gas is turning out to be a great source of energy because it is

relatively clean, can be substituted for oil in many cases (not all), and is also cheaper than oil as an

energy source.

Not only Pakistan, in the past 25 years, natural gas has grown to account for 24 per cent of total energy

consumption globally. Even Brazil (20.1 per cent) and China (25.8 per cent) are far ahead of India, which

only meets 9 per cent of its energy needs from gas.

The only issue with gas is that it is not as easy to transport as oil is. The situation is just like the chicken

and egg story, says B.S. Negi, member of the PNGRB. Which comes first? Gas or infrastructure? My

answer in this case would be the chicken, which is the infrastructure that is, pipelines. Talking to BW,

Negi says that in the past two decades, the countrys largest gas transmission company, GAIL, had failed

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 27/34

to capitalise on opportunities and slowed down the process. If we see what they have added in terms

of gas exploration and pipelines, it is minuscule.

In India too, there seems to be a huge amount of gas waiting to be discovered. Indias gas inventory will

be doubled by the end of fiscal 2010-11 as Reliance Industries D6 block reaches production of 90 million

metric standard cubic metres per day (MMSCMD) more than twice its present 44 MMSCMD.

Yet, even while the world is embracing gas wholeheartedly, India is in danger of missing the bus because

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 28/34

it doesnt have a proper gas pipeline network and new pipeline projects are

being built too slowly. India has also failed to work out a proper policy for gas

carriage, which is why not too many players want to get into building

pipelines. Other than GAIL , RGTIL (Reliance Gas Transportation India) and

GSPL (Gujarat State Petronet) are the only major players in transporting gas

through pipelines. Indian Oil Corporation (IOCL) and Oil India (OIL) have also

entered the segment but in a small way.

Of the 119 MMSCMD of gas currently consumed in India, 64 per cent goes to

the power and fertiliser sectors, and only 9.5 per cent reaches the nations

transport and city-based gas distribution systems. Further, there is another

policy shortcoming that is making the switch-over to gas difficult.

The current regime of gas allocation across various sectors is decided by the

EGoM (empowered group of ministers), and is vague, says Ajay Arora,

partner and national leader for oil and gas at advisory firm Ernst & Young.

The ongoing multiple gas pricing regime is messy: the administered pricing

mechanism (APM) is applicable to government-nominated fields; companies

in production sharing contracts (PSCs), a common contract signed between a

government and a company that extracts resources, follow a different system.

There is another price for imported re-gasified liquefied natural gas or RLNG;

and the spot LNG price is variable. Other than the governments claim that it is

examining the idea of a unified gas pricing regime, there has been no progress on this front.

Pricing of gas supply from different sources is even more uncertain in the long term. Of course, there is

room for multiple interpretations, but PSC terms need to be spelt out clearly, which will assure their

enforceability for future investors in the oil and gas sector.

At present, the domestic tax law provides a 10-year tax holiday for laying and operating cross-country

natural gas distribution networks, including pipelines and storage facilities. Tax holidays were introduced

with the aim to promote and set up gas infrastructure, and simultaneously reduce the existing subsidy

on LPG.

Stuck In The Pipelines

Typically, there is a blame game afoot. U.D. Choubey, former chairman and managing director of GAIL,blames PNGRB for its slow approach, and for creating troubles in the growth of pipeline infrastructure,

especially in the city gas distribution systems. World over, regulatory boards have shown a soft hand in

order to promote the gas industry, says Choubey. But in India, the restrictions are too big toohandle.

The bidding process takes so much time. The PNGRB is responsible for the slow growth of the gas

industry.

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 29/34

GAILs major focus is to

maintain its dominant

position in the gas

business, especially in the

transmission segment,

says the companys

official spokesperson.

Therefore, during the

11th Five-Year Plan, GAIL

will build 5,000 km of

pipeline with an estimated

investment of Rs 28,000

crore. When these

pipelines are

commissioned by 2012-

13, GAILs gas-carrying capacity will double to about 300 MMSCMD. However, in the larger picture, this

will be far from enough.

Future Gas Supplies

The worlds natural gas production is expected to grow to 106 trillion cubic feet by 2030 from 65 trillion

cubic feet in 2006. According to a report by US statistical and analytical agency Energy Information

Administration (EIA), non-OECD countries will account for 84 per cent of this hike. OECDs gas

production, on the other hand, grows by only 0.8 per cent per year from 40 trillion cubic feet to 47

trillion cubic feet.

With more than 40 per cent of the worlds proven natural gas reserves, West Asia will account for the

largest increase in regional natural gas production by 2030, thus accounting for more than one-fifth of the total increment in world production.

Currently, there are four major natural gas producers in West Asia: Iran, Saudi Arabia, Qatar, and the

United Arab Emirates, which together accounted for 83 per cent of the natural gas produced in West

Asia in 2006. Each of the four countries has announced plans to expand natural gas production in order

to meet the expected increase in regional demand and (or) to supply markets outside the region, says

EIA in a report published at the end of last year.

Education Sector as business proposal

For much of the next five decades(post Independence), higher education became almost entirely the

preserve of the government. Private citizens and corporate houses studiously stayed away, deterred

perhaps by the unfriendly government policies. The past decade saw private interest rekindle. However,

the activity was largely confined to a few states that were flexible with rules. More states have followed

suit in the past couple of years and, in the recent months, there has been an even greater spurt in

businesses talking of setting up institutes.

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 30/34

Philanthropy Or Business?

Why the sudden rush? No new incentives have yet been announced by the government to woo private

money into higher education, and nor have any of the curbs been lifted to make it easier for

businessmen to set up higher-education institutes.

Experts and analysts tracking the area differ on the reasons behind the sudden rush. Some say that

despite its public pronouncements, the governments attitude has changed towards private capital in

higher education. One of the reasons, they point out, is that barely 22 per cent of the total outlay for

education for 2008-09 is earmarked for higher education. While Rs 26,800 crore was kept for primary

and secondary education in last years annual Plan, only Rs 7,600 crore was earmarked for higher

education. Given the enormous demand for skilled workers, and the realisation that economic growth

cannot be sustained without enough people with college degrees, the government is perhaps becoming

more flexible. More importantly, many states, too, are making it easy for the private sector to set up

institutes.

Others feel that businessmen who have built big empires are now in a philanthropic mood and want to

set up institutes that will stand as a testimony to their l ives. Amitabh Jhingan, partner and education

leader at Ernst & Young, says, The big players are venturing into education these days as this is a great

brand building exercise. They want to leave a legacy behind.

The Mechanics Of Starting

Setting up an educational institute costs a lot. Even without factoring in the cost of land, it takes Rs 12-

15 crore to set up the infrastructure for a single-subject institution. Add other sundry costs and you are

looking at an initial investment of Rs 25 crore for a very small institute. And then there is the cost of

land. If you had to pay for land at current market prices in, say, Noida or Gurgaon, the costs could

balloon to Rs 500 crore. It takes several hundreds of crores to set up a full-fledged university, even when

the cost of acquiring land is excluded.

The big advantage that private institutes have, of course, is that they are free to charge for the courses

whatever they think the market can bear and thanks to the shortage of higher education facilities, themarket has shown it can bear a lot. Thus, a private technical institute can charge students over Rs 6 lakh

per annum, against the fraction that is charged by government institutes for a similar course.

Consultants who do project reports for private companies setting up educational institutes say that

purely from a point of view of quick returns, building a technical institute is far easier. One, the initial

investment required is low. More importantly, there is a huge demand for degrees and diplomas in

technical and business management fields. The demand for courses in liberal arts is relatively low.

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 31/34

Hence, institutes that offer technical or management courses can set the fees very high, as they can be

confident of getting students.

Consultants say that most technical institutes can hope to cover their initial costs within six to eight

years, and after that they can enjoy earnings before interest, taxes, depreciation and amortisation, or

EBIDTA, of 25-30 per cent. Of course, according to current laws the surplus generated cannot be taken

out by the promoter as profits, nor can it be used for setting up new colleges. Banks fund colleges and

institutes as businesses, and it is possible for well-run projects to start generating enough cash to pay

back the bank loans from year one of operations itself, says E&Ys Jhingan.

Apart from quick returns, what is equally important is that setting up technical institutes is often a way

of ensuring a ready pool of talent. Taken together, these factors explain why technical institutes are

mushrooming everywhere. Even big corporates such as Nirma, ArcelorMittal, NIIT, Reliance ADAG and

the Modis and Amity have set up technical universities rather than multi-disciplinary institutions

catering to arts and commerce streams too.

Of course, when it comes to sheer prestige, a technical institute does not compare with a university.AtulChauhan, chancellor of Noida-based Amity University, says, There is no comparison in power and

status between an institute and a university. Moreover, setting up ones own university gives one the

freedom to devise and run courses and decide how many students one wants to take.

However, opening a university needs enormous resources and commitment. The Vedanta institute in

Orissa, when it comes up, will be the biggest private multi-disciplinary university in recent times. Anil

Agarwal, chairman of Vedanta Resources, is reportedly giving the biggest-ever endowment $1 billion

(about Rs 4,800 crore). The largest private university, as of now, is perhaps the Lovely Professional

University (LPU) in Jalandhar promoted by Ashok Mittal, who made a fortune from his sweet shop in the

city. Spread over 600 acres, LPU offers over 150 courses to 24,000 students. It has 1,500 facultymembers.

Despite the huge demand and ready students available for almost any higher education-institute, there

are significant hurdles that promoters need to negotiate. The AICTE has stringent norms for accredition.

Apart from an annual fee of around Rs 50,000, there are strict norms for per student requirement of

space in laboratories, classrooms, etc. According to LPUs Mittal, to set up a decent engineering

institute, one needs at least 10 acres, and five acres are needed for a management institute. A medical

college requires at least 25 acres. The University Grants Commission (UGC) norms for setting up a

university are even more stringent.

Such norms ensure that only people with deep pockets can get into the game. C.S. VenkataRatnam,

director of Delhi-based International Management Institute (IMI), says, True academicians or scholars

cannot set up an institute today because of the land norms laid down by AICTE.

To keep costs low, businessmen often flock to states that give land at cheap or concessional rates, such

as Punjab, Andhra Pradesh, Rajasthan and Gujarat. The Punjab government, for instance, had given 70

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 32/34

acres in Mohali for the campus of International School of Business (ISB) at a token price of Re 1 per acre

in 2007, while industrialists with roots in that region had pledged Rs 200 crore for infrastructure.

Similarly, Hyderabad had given land at concessional rates for ISBs flagship institute.

The running cost of an institute depends on the kind of services and facilities provided and the level of

faculty hired. The 100-acre L.N. Mittal Institute of Information Technology (LNMIIT) with 600 students

and 35 faculty members has a running expenses bill of Rs 7.5 crore per annum, says the institutes

director, DheerajSanghi. Of this, more than two-thirds goes towards faculty salary, he says.

Public-Private Partnerships

From only 91 institutes in 2001, the number of technical institutes increased to 8,568 by 2008, accordingto the HRD ministrys latest annual report. The increase in access was important but the deterioration in

the quality of the students graduating from most of these institutes led to concerns over mismatch in

employability and skill shortage.

The Bihar government has given 25 acres to Birla Institute of Technology, Mesra, to set up a campus in

Patna. It has also given a one-time seed capital of Rs 23 crore for the project. P.K. Barhai, the institutes

vice-chancellor, says, MoUs such as these help institutes build up their reputation and also assist in

R&D work. On a bigger scale, the Rajasthan government which is doing fast work in this sector and

has seen a number of universities come up recently, the latest being the 100-acre campus of the NIIT

university offering B.Tech and M.Tech courses, and that of the Apeejay group being in the pipeline

has given 100 acres of land to LNMIIT free of cost. Sanghi says, The state government also gave Rs 15

crore as initial money and has representation on the board.

In Sikkim, the state government did something similar for the Manipal group, which set up the Sikkim

Manipal University in the state in 1995, the first PPP in the region. AnandSudarshan, CEO and managing

director of Manipal Education, says, While the governments thrust has been on conveying to the world

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 33/34

that India is ready for change, things will really change only after there is clarity on the Foreign

Education Providers Bill.

FINANCING EDUCATIONEasy availability of bank finance for higher education has led to more students

opting for private institutes. Public sector banks lend up to Rs 10 lakh for a course in India and up to Rs

20 lakh for studies abroad. Nationalised banks disbursed loans worth Rs 20,000 crore to 1.25 millionstudents in 2007-08 while private banks lent Rs 500 crore. Last year, the portfolio of education loans of

banks grew 40 per cent. The ministry of human resource development has recently notified a scheme of

interest-free education loans for children from poor families.

ACUTE SHORTAGE

India has a poor score in higher educationThe gross enrolment ratio in higher education in India is a low 12 per cent, compared to nearly

70 per cent in developed nations and 33 per cent in BRIC countries

y Public sector expenditure on higher education has been declining in real terms

y Average student-faculty ratio in India is 26:1, against a global average of 15:1

y Over 57 per cent faculty members do not have PhDs or M.Phil degrees

y Roughly 300,000 students compete every year for the 1,800 seats in IIMs

Developed countries such as the US allow educational institutes to make profits, but there are strict

controls. There are for-profit universities such as Apollo University of Phoenix, Laureate Education and

Corinthian Colleges in California, but none of them are top-notch institutes or centres of excellence.

Premier-league institutes such as Yale have been not-for-profit PPPs with the state providing land and

corporates pooling in resources for services and endowment, much like the ISB and IMI model here.

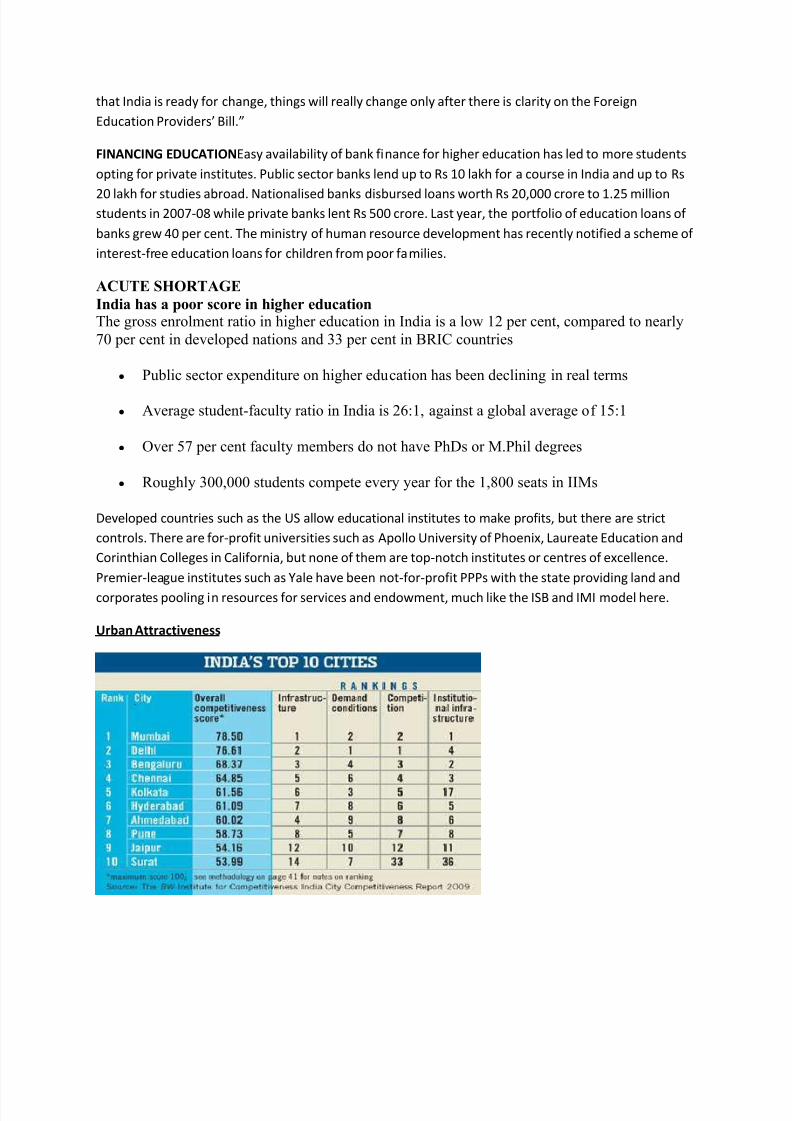

Urban Attractiveness

8/8/2019 Current Infra Status

http://slidepdf.com/reader/full/current-infra-status 34/34