creating an ever stronger weir - seeking alpha

TRANSCRIPT

Creating an ever stronger Weir

LSE ticker: WEIR.LN

US ADR ticker: WEGRY

Presented by Jon Stanton and John Heasley

Glasgow

31 July 2018

Jon Stanton Chief Executive Officer

Delivering significantly improved profitability

3

Execute

Strong orders1: Record Minerals AM; O&G +35%; FC +34%

Operating Profit1,2 +62%; Continuing margin 15.1%

Full year guidance unchanged

Current market conditions remain encouraging

Long term market fundamentals positive

Good progress on We are Weir strategic initiatives

ESCO acquisition completed in July

Flow Control sale process planned to launch in late Q3

Continued balance sheet deleveraging

Grow

Transform

Confident outlook underlined by return to dividend growth

1. Constant currency 2. Total Group

Execute:

Financial review

John Heasley

37.1 46.3

-4.8

3.1

-5

0

5

10

15

20

25

30

35

40

45

50

2017 H1 2018 H1

p EPS2

104 143

-11

9

-20

0

20

40

60

80

100

120

140

160

2017 H1 2018 H1

£m PBTA2

13.4%

15.1%

10%

12%

14%

16%

2017 H1 2018 H1

% Margin1

Delivering strong profit growth in line with expectations

5

976 1,166

0

200

400

600

800

1,000

1,200

2017 H1 2018 H1

£m Orders1

+20%

865 1,062

0

200

400

600

800

1,000

1,200

2017 H1 2018 H1

£m Revenue1

+170bps +23%

1 Continuing operations at constant currency before exceptional items and intangibles amortisation. 2 Continuing operations as reported before exceptional items and intangibles amortisation. 3 Total Group

+38%

78

139

0

25

50

75

100

125

150

2017 H1 2018 H1

£m Cash from operations3

+78% +25%

Discontinued Operations

Minerals: Early investment delivering strong growth

£m

H1 18 H1 171 YOY +/- H2 171

OE orders 222 205 9% 183

AM orders 506 445 14% 458

Total orders 728 650 12% 641

Mining markets continued positive momentum

Brownfield opportunities dominate

Q2 AM at record levels

Strong greenfield pipeline developing

1 2017 restated at H1 2018 average exchange rates. 6

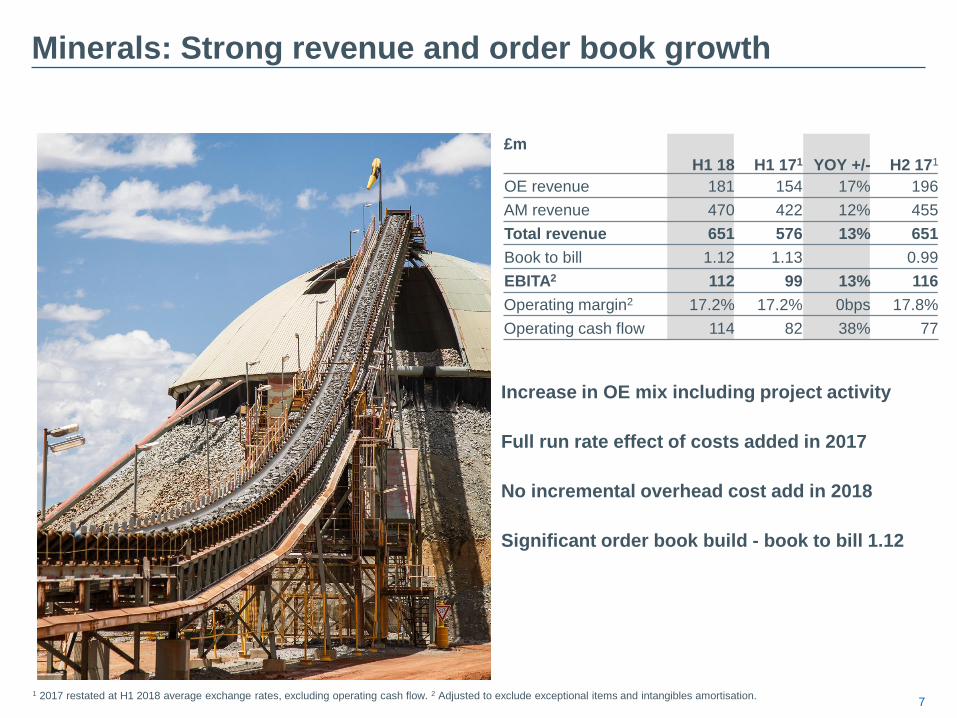

Minerals: Strong revenue and order book growth

1 2017 restated at H1 2018 average exchange rates, excluding operating cash flow. 2 Adjusted to exclude exceptional items and intangibles amortisation.

7

Increase in OE mix including project activity

Full run rate effect of costs added in 2017

No incremental overhead cost add in 2018

Significant order book build - book to bill 1.12

£m

H1 18 H1 171

YOY +/- H2 171

OE revenue 181 154 17% 196

AM revenue 470 422 12% 455

Total revenue 651 576 13% 651

Book to bill 1.12 1.13 0.99

EBITA2 112 99 13% 116

Operating margin2 17.2% 17.2% 0bps 17.8%

Operating cash flow 114 82 38% 77

Oil & Gas: Strong recovery in North America continues

Positive NAM fundamentals

NAM orders ahead of rig count trends

OE includes strong growth in frack pumps

AM driven by completions activity and intensity

International markets remain competitive

£m

H1 18 H1 171 YOY +/- H2 171

OE orders 108 69 58% 81

AM orders 330 257 28% 281

Total orders 438 326 35% 362

8 1 2017 restated at H1 2018 average exchange rates.

Weir RFID tracking system for flow iron

Oil & Gas: Significantly higher profitability

› Strong operational performance

› Profits driven by NAM; flow through of 37%

› Margin in line with mid-teens expectations

› Working capital closely managed

£m

H1 18 H1 171 YOY +/- H2 171

OE revenue 96 57 67% 75

AM revenue 315 232 36% 297

Total revenue 411 289 42% 372

Book to bill 1.07 1.13 0.97

EBITA (incl. JVs)2 63 29 117% 56

Operating margin2 15.3% 10.1% 520bps 15.1%

Operating cash flow 39 -1 5701% 44

9 1 2017 restated at H1 2018 average exchange rates, excluding operating cash flow. 2 Adjusted to exclude exceptional items and intangibles amortisation.

Discontinued operations: Flow Control

Markets continue to recover

Good OE order momentum driven by increased nuclear demand

Fifth straight quarter of YOY AM growth

Significant order book build with book to bill of 1.28

Mid single digit margins in line with expectations

£m

H1 18 H1 171 YOY +/- H2 171

OE orders 105 67 53% 86

AM orders 101 86 19% 67

Total orders 206 153 34% 153

10 1 2017 restated at H1 2018 average exchange rates, excluding operating cash flow. 2 Adjusted to exclude exceptional items and intangibles amortisation.

OE revenue 84 91 -8% 115

AM revenue 77 70 10% 77

Total revenue 161 161 0% 192

Book to bill 1.28 0.95 0.80

EBITA2 9 (11) 176% 8

Operating margin2 5.4% -7.2% 1260bps 4.2%

Operating cash flow 8 7 5% 15

11

Exceptional items and other financial matters

Exceptional costs – H1

›Mainly ESCO acquisition costs

›Initial Flow Control disposal costs

Translational foreign exchange

›Full year operating profit headwind c. £16m based on current

exchange rates

Central costs

›H1 £2m higher than prior year – primarily digital investment

Interest

›H1 £4m lower than prior year reflecting £95m private

placement refinancing, equity placing proceeds and

favourable FX

Effective tax rate in line with expectations at 25.3%

£m

H1 18

ESCO acquisition related costs 24

Other exceptional costs 1

Continuing 25

Discontinued operations 1

Strong growth in operating cash flow

Cash flow statement £m Total operations - as reported

H1 18

H1 17

Operating cash flows – pre working capital 199 144

Working capital outflow (60) (66)

Operating cash flows 139 78

Net interest (18) (21)

Tax (36) (15)

Net capex (32) (37)

Settlement of derivative financial instruments (19) 1

Other cash flows (2) 1

Free cash flow pre dividends 32 7

Dividends paid (39) (57)

Free cash outflow (7) (50)

12

416 491 501

77 80 75

0

50

100

0

200

400

600

2017 H1 2017 H2 2018 H1

Debtor days

£m Debtors1

585 607 663

2.3 2.5 2.5

0

1

2

0

250

500

750

2017 H1 2017 H2 2018 H1

Inventory turns

£m Inventory1

Operating cash flows increased by £61m

Working capital metrics continue to improve

Tax cash flows reflect increase in profits

Derivatives outflow driven by USD:GBP rate movements

Dividends paid reflect £31m vs. £6m scrip take-up in H1 2017

546 601

656

27.6 26.8

26.9

0

10

20

30

0

250

500

750

2017 H1 2017 H2 2018 H1

Working capital as % sales

£m Working Capital1

1 At constant currency.

0

200

400

600

800

1,000

1,200

1,400 US$1,285m

Movement in net debt

13

£m

Net debt at 31 December 2017 843

Free cash outflow 7

Exceptional cash outflow 7

FX 25

ESCO placing (357)

Other 4

Net debt at 30 June 2018 529

ESCO placing 357

Underlying net debt at 30 June 2018 886

£357m proceeds from placing held at 30 June before

being used to fund the ESCO acquisition on 12 July

Underlying net debt increase mainly driven by FX

translation of US$ debt

Weighted average no of shares in H1 230.9m

›Shares in issue now 259.4m after completion of ESCO

acquisition

869 843 886

3.1

2.5 2.1

0

1

2

3

4

0

500

1,000

2017 H1 2017 H2 2018 H1

Net debt / EBITDA

£m

Placing 16.7m shares

Vendor equity 16.8m shares

Equity Value US$1,048m

Debt / pensions US$237m1

Debt

US$m

ESCO transaction funding

Net debt & covenant

1 ESCO debt/pensions estimated.

Grow:

We are Weir

Jon Stanton

Grow: Strategic Progress - H1 2018 Highlights

15

› Safety: TIR of 0.53; significant reduction in severity

› Progressed engagement strategy

› Defined organisational effectiveness KPIs

People Improved sustainable

engagement score and

organisational effectiveness

Customers Increased market share

Technology Increased revenues from new

solutions

Performance Sustainably higher margins through

the cycle

› c. £50m in revenues for Minerals integrated solutions

› ‘Weir Edge’ O&G field services launched

› Major nuclear contract successes for Flow Control

› Revenues from new products +16%

› Synertrex® pilots successful; Q3 commercialisation

› Strong initial uptake of O&G Simplified Frac System

› 80 Value Chain Excellence projects underway

› Sustainability pilots to improve energy efficiency

› Drive towards long term margin improvements

16

Grow: Mining and Infrastructure markets

Current market conditions

›Miners focused on maximising productivity

›Strong brownfield and AM demand

›Significant growth in greenfield quotations pipeline

Long term fundamentals

›Supply shortages anticipated in key commodities

Power infrastructure demand for copper/lithium/cobalt

›Ore grade declines continue despite new developments

›Mining long wavelength upcycle underway

›Infrastructure benefiting from global GDP growth

Why Weir benefits

›Biased to most attractive commodities

›Premium productivity-enhancing technology

›AM based business model; High barriers to entry

1 Deutsche Bank July 2018. 2 CRU February 2018.

10

15

20

25

2017 2018E 2019E

£b

Top 4 miners total capex1

95

100

105

110

115

2017 2018 2019 2020 2021

2016 b

aselin

e =

100

Copper Gold Iron Ore (excl. Oceania)

Mined ore production projections2

Grow: Differentiating through Integrated Solutions

Close customer proximity crucial

Detailed site audit

›Digital analysis of plant flows

›Ability to see solutions before installation

Very quick customer payback

›10% increase in plant capacity

›Initial investment recouped in 3 days

Supports long term relationships

›Additional order for cyclones, pumps and

screens

Cavex® Hydrocyclone Warman® slurry pump Linatex® screen media

17

Digital mapping allows the customer to see the solution before the installation takes

place.

18

Grow: Oil and gas markets

Current market conditions

›US rig count levelled off; Canada still growing

›Increased intensity of operations supporting AM demand

›No impact from Permian issues to date

›International still challenging but improvement expected

Long term fundamentals

›Global oil demand +1.2 mb/d p.a. through to 20231

›Supply side challenges in Iran, Libya and Venezuela

›Underinvestment and depletions costs 3 mb/d p.a.

›IEA: US to provide majority of global supply growth1

Why Weir benefits

›~80% of revenues from attractive NAM markets

›Strong and growing technology leadership

›Unrivalled service coverage includes all major basins

1 IEA, Oil 2018, 2 IHs Markit 3 EIA Annual Energy Outlook 2018

0

5

10

15

15Q1 15Q3 16Q1 16Q3 17Q1 17Q3 18Q1 18Q3F

Completions continue to recover strongly2

Frack demand

0

50

100

150

200

250

1990 2000 2010 2020 2030 2040

petroleum

coal

natural gas

renewables

nuclear

Global energy consumption by fuel type3

(quadrillion BTU)

19

Grow: Differentiating through Technology leadership

First Simplified Frac System

Solution from pump to wellhead

›Integrated Pressure Pumping and Pressure

Control system

›Large bore iron and valves simplify the frac

job

Safer and faster

›88% reduction in leak paths

›Significant improvement in safety

›Reduced rig up and de-rig times

US$10m in orders in H1

A traditional frack site has 100s of connections

The Simplified Frac System is safer and more efficient

20

2018 Outlook

Minerals

›Expectations for strong constant currency profit growth unchanged

›Strong revenue growth and broadly stable margins YoY

Oil & Gas

›Continue to anticipate strong increase in constant currency revenues and profits

›Mid teens H2 operating margins consistent with H1 and prior guidance

ESCO

›Unchanged expectations for 2018; pro forma revenue of $675m and $80m EBITA

›Even phasing of revenue and profit pre and post acquisition

Flow Control

›Broadly stable constant currency revenues

›Mid single-digit operating margins

Group

›Outlook assumes market conditions remain supportive

›Strong constant currency revenue and profit growth

›Further balance sheet deleveraging and strong cash generation

Transform:

Long-term growth

Jon Stanton

2.5x ~2.0x

Weir2017A

Pro forma2018E

2019+

Transform: Creating an ever stronger Weir

22

A portfolio of global leading brands

Focusing on highly abrasive upstream

Exposure to resilient aftermarket

Financial strength to invest in growth1

SPM® Pressure Pumping solutions

Ground Engaging Tools

77%

69%

23%

31%

Pro-FormaIncl. ESCOExcl. Flow

Control

Weir2017A

AM OE

51%

39%

32%

38%

9%

17%

8% Pro-FormaIncl. ESCOExcl. Flow…

Weir2017A

Minerals Oil Industry Industrial & Power Sand & Aggregates Other

Cash generation

Flow Control proceeds

Revenue split

Revenue split

WARMAN® Centrifugal Slurry pumps

1 Pro forma net debt / adjusted EBITDA

23

Transform: A unique mining provider

24

Transform: Strong start to the integration process

Excellent first impressions

Experienced integration team

Revenue synergy work progressing well

US$30m cost synergy targets validated

Operating model to maximise upturn

Welcome to Weir event for the ESCO team

Key takeaways

25

Execute Delivering strong growth in line with expectations

Strategic progress in attractive markets

Grow

Transform

Building a platform for long term growth

Questions

Appendices

Appendix 1: Quarterly order trends Reported growth1 Like for like growth1, 2

Division 2017

Q3

2017

Q4

2018

Q1

2018

Q2

2017

Q3

2017

Q4

2018

Q1

2018

Q2

OE 19% 10% 19% - 19% 10% 19% -

AM 9% 8% 11% 16% 9% 8% 11% 16%

Minerals Total 12% 9% 13% 11% 12% 9% 13% 11%

OE 92% 130% 91% 33% 82% 97% 84% 22%

AM 52% 46% 40% 19% 50% 43% 38% 17%

Oil & Gas Total 59% 60% 50% 22% 56% 52% 47% 18%

OE 34% 32% 36% 9% 32% 26% 34% 6%

AM 23% 20% 21% 17% 22% 19% 20% 17%

Continuing Ops Total 25% 23% 25% 15% 24% 21% 24% 13%

Book to bill 0.99 0.96 1.15 1.05 1.00 0.96 1.15 1.05

OE -8% -1% -3% 110% -8% -1% -3% 110%

AM 7% 17% 6% 28% 7% 17% 6% 28%

Discontinued Ops Total -2% 6% 2% 61% -2% 6% 2% 61%

1 Continuing operations excludes the Flow Control Division which is being reported as discontinued operations after the announcement of the Group’s intention to sell on 19 April 2018. 2 Like for like excludes the impact of acquisitions (KOP Surface Products excluded for 2017).

28

Appendix 2: Orders by end market and geography

Orders by end market Minerals Oil & Gas

H1

Continuing

operations

2018

Total

H1

Continuing

operations

20171

Total

Discontinued

operations

2018

Total

Minerals 75% 0% 47% 48% 1%

Oil & Gas 6% 98% 41% 37% 19%

Power 5% 1% 3% 4% 45%

Sand & Aggregates 3% 0% 2% 4% 0%

General Industrial 10% 1% 7% 7% 13%

Other 1% 0% 0% 0% 22%

Total 100% 100% 100% 100% 100%

1 2017 restated at H1 2018 average exchange rates.

29

Orders by geography Minerals Oil & Gas

H1

Continuing

operations

2018

Total

H1

Continuing

operations

20171

Total

Discontinued

operations

2018

Total

North America 21% 80% 43% 43% 34%

Europe & FSU 12% 5% 9% 9% 33%

Australasia 16% 1% 10% 11% 1%

Middle East & Africa 14% 8% 12% 12% 9%

South America 22% 0% 14% 14% 1%

Asia Pacific 15% 6% 12% 11% 22%

Total 100% 100% 100% 100% 100%

Appendix 3: Foreign exchange by currency

H1 2017 Revenue £m H1 2017 Operating profit1 £m

Currency At 2017

rates FX

At 2018

rates

At 2017

rates FX

At 2018

rates

US Dollar 426 (37) 389 63 (5) 58

Australian Dollar 124 (8) 116 13 (1) 12

Canadian Dollar 78 (4) 74 12 - 12

Euro 29 1 30 8 - 8

Chilean Peso 65 (1) 64 18 (1) 17

United Arab Emirates Dirham 29 (2) 27 3 - 3

South African Rand 56 (1) 55 5 - 5

Brazilian Real 23 (3) 20 2 - 2

Russian Rouble 12 (1) 11 2 - 2

Other 80 (1) 79 (2) (1) (3)

Continuing operations 922 (57) 865 124 (8) 116

Variance (6%) (8%)

Interest (20) 1 (19)

PBTA 104 (7) 97

Variance (7%)

1 Adjusted to exclude exceptional items and intangibles amortisation.

30

Appendix 4: Foreign exchange by division

H1 2017 Revenue £m H1 2017 Operating profit1 £m

Division At 2017

rates FX FX %

At 2018

rates

At 2017

rates FX FX %

At 2018

rates

Minerals 608 (32) (5%) 576 105 (5) (5%) 100

Oil & Gas 314 (25) (8%) 289 32 (3) (8%) 29

Central costs - - - - (13) - (1%) (13)

Continuing operations 922 (57) (6%) 865 124 (8) 7% 116

Discontinued operations 165 (4) (3%) 161 (11) 0 5% (11)

1 Adjusted to exclude exceptional items and intangibles amortisation.

31

Appendix 5:Foreign exchange headwind expected in 2018

FY 2017 Revenue £m FY 2017 Operating profit1 £m

Currency At 2017

rates FX

At 20182

rates

At 2017

rates FX

At 20182

rates

US Dollar 923 (60) 863 168 (11) 157

Australian Dollar 264 (16) 248 29 (2) 27

Euro 60 - 60 16 - 16

Canadian Dollar 161 (8) 153 28 (1) 27

Chilean Peso 141 (1) 140 38 (1) 37

South African Rand 112 1 113 9 - 9

United Arab Emirates Dirham 58 (4) 54 4 - 4

Brazilian Real 45 (5) 40 5 (1) 4

Russian Rouble 32 (2) 30 5 - 5

Other 187 - 187 (10) - (10)

Continuing operations 1,983 (95) 1,888 292 (16) 276

Variance (5%) (5%)

Interest (42) 1 (41)

PBTA 250

(15) 235

Variance (6%)

1 Adjusted to exclude exceptional items and intangibles amortisation.

2 2018 FX rates reflect June 2018 average

32

33

Appendix 6: Exchange rates

H1 2018

Average

H1 2018

Closing

H1 2017

Average

H1 2017

Closing

US Dollar 1.38 1.32 1.26 1.30

Australian Dollar 1.78 1.78 1.67 1.69

Euro 1.14 1.13 1.16 1.14

Canadian Dollar 1.76 1.73 1.68 1.69

United Arab Emirates Dirham 5.06 4.85 4.62 4.78

Chilean Peso 842.00 861.70 830.80 863.50

South African Rand 16.92 18.15 16.63 16.98

Brazilian Real 4.71 5.10 4.00 4.30

Russian Rouble 81.73 82.78 73.00 76.92

Disclaimer

This information includes ‘forward-looking statements’. All statements other than statements of

historical fact included in this presentation, including, without limitation, those regarding The Weir

Group’s (“the Company”) financial position, business strategy, plans (including development plans

and objectives relating to the Company’s products and services) and objectives of management for

future operations, are forward-looking statements. These statements contain the words “anticipate”,

“believe”, “intend”, “estimate”, “expect” and words of similar meaning. Such forward-looking

statements involve known and unknown risks, uncertainties and other important factors that could

cause the actual results, performance or achievements of the Company to be materially different

from future results, performance or achievements expressed or implied by such forward-looking

statements. Such forward-looking statements are based on numerous assumptions regarding the

Company’s present and future business strategies and the environment in which the Company will

operate in the future. These forward-looking statements speak only as at the date of this document.

The Company expressly disclaims any obligation or undertaking to disseminate any updates or

revisions to any forward-looking statements contained herein to reflect any change in the

Company’s expectations with regard thereto or any change in events, conditions or circumstances

on which any such statement is based. Past business and financial performance cannot be relied

on as an indication of future performance.