cost improvement curves learning amortization and yield - covert

TRANSCRIPT

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 1/26

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 2/26

Cost Drivers Learning Event, 2nd November 2005

16 September 2005 2

Agenda Introduction

Cost Improvement Factors The Plant Model

Nonrecurring and recurring costs

Nonrecurring cost improvement Recurring cost improvement

Example hardware cost improvement model

Summary

Acronym List

References

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 3/26

Cost Drivers Learning Event, 2nd November 2005

16 September 2005 3

Introduction This presentation is intended for an audience with an

intermediate understanding of cost analysis methods

We will discuss the phenomenon of “costimprovement”, which is loosely defined as theobserved reduction of cost of successive units or projects

0

50

100

150

200

250

300

350

400

0 10 20 30

Unit Number

R e c u r r i n g

C o s t , $

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 4/26

Cost Drivers Learning Event, 2nd November 2005

16 September 2005 4

Cost Improvement Factors and Learning Cost Improvement is the observed reduction of costs between

successive units or projects

Factors affecting cost improvement: Nonrecurring and recurring accounting standards affect measurement

Reuse of existing designs, materials, equipment, effort, or products

Learning or gained experience in value added effort

Skill Mix changes

Process shortcuts that eliminate effort or expenses

Yield improvements that reduce cost

Production Rate increases allowing for amortization of pooled costsand greater efficiency

Technological advances allowing greater yield and efficiency Inflation which measures the time variable cost of a “basket of goods”

*True “learning” is a subset of cost improvement, so cost

improvement is more than learning

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 5/26

Cost Drivers Learning Event, 2nd November 2005

16 September 2005 5

The Plant Model Can use a plant economic model to show the effects

of different factors on cost improvements [Ref. 1, p. 183]

Skills Labor Rates

Engineering 1 2 3 4 5

Manufacturing

Quality and Reliability

Labor Hours $Tooling Fee

Testing Labor Overhead G&A

Labor Other + Overhead

Travel and Other Direct Costs $ $ Price

Material Prices Total Cost

Material Measures A B C D E Material

+ OverheadPounds G&A

Yards Fee

Material quantities $Gallons

Linear Feet Material Overhead

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 6/26

Cost Drivers Learning Event, 2nd November 2005

16 September 2005 6

The Plant Model The plant economic model contains the three classic

Elements of Cost: Labor, Materials and Expenses

These costs can be Project related or Pooled (period costs)

Direct or Allocable (overhead and fringe)

Nonrecurring or Recurring costsMaterials (M) Labor (L) Expenses (E) Total = M+L+E

Direct 105,000.00 2,500,000.00 80,000.00 2,685,000.00

Burden 26,250.00 3,000,000.00 64,000.00 3,090,250.00

Total 131,250.00 5,500,000.00 144,000.00 5,775,250.00

Administration 10,000.00 125,000.00 6,250.00 141,250.00 Distribution 5,000.00 25,000.00 1,250.00 31,250.00

Corporate Transfer 125.00 250,000.00 12,500.00 262,625.00

Marketing 30,000.00 200,000.00 10,000.00 240,000.00

Research 50,000.00 275,000.00 13,750.00 338,750.00

Development 20,000.00 125,000.00 6,250.00 151,250.00

Finance 20,000.00 195,000.00 9,750.00 224,750.00

Total 135,125.00 1,195,000.00 59,750.00 1,389,875.00

Total 266,375.00 6,695,000.00 203,750.00 7,165,125.00

Pooled Costs

(Period)

Project Costs

TOTAL

COSTS

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 7/26

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 8/26

Cost Drivers Learning Event, 2nd November 2005

16 September 2005 8

Nonrecurring and Recurring Costs Nonrecurring (NR) and recurring (REC) cost definitions

Nonrecurring costs - unique costs of effort, material and expenses

tied to a production run rather than a particular unit Recurring costs – costs of repeated effort, material and expenses

repeated for each subsequent unit

Hard to segregate NR and REC in small or single unit

production What was recurring work if we only build one unit?

What was the theoretical first unit cost (T1)?

What if we build a prototype unit and make it the first productionunit?

What was the fist prototype unit cost (P1) and T1 cost?

What will the theoretical second unit cost (T2) be?

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 9/26

Cost Drivers Learning Event, 2nd November 2005

16 September 2005 9

NR/T1 Factors for Space Programs NR/T1 is the ratio of NR costs to T1 costs

Analysis of NR/T1 Ratios of 100 programs from theNAFCOM database* provide the following results:

TYPE

RocketEngine

EarthOrbiting

LaunchVehicle Manned Planetary

NUMBER 4 61 10 8 17

MIN 27.65 0.00 2.61 1.29 2.38MAX 202.24 7.59 39.78 11.56 18.35MEDIAN 128.83 2.02 16.00 3.48 6.18MEAN 121.89 2.35 16.93 4.44 6.52

min ML mean (average) max

ML = most likely= 3 * mean - (min + max)

* NASA / Air Force Cost Model (NAFCOM) Includes subsystem hardware, systems engineering, program management,integration, assembly and test, ground test equipment, launch and orbital operations support

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 10/26

Cost Drivers Learning Event, 2nd November 2005

16 September 2005 10

New Design and Reuse* The amount of new design on a program and reuse

from previous programs is a key factor in determiningNR/T1 Reuse = 1 – New Design

Assumes all have some prototype development

Almost never have 0% redesign or 100% redesign

Use table to estimate NR/T1 cost ratio from % new design% NewDesign Description NR/T1

0.0 Off the Shelf 0.1

0.1 0.20.2 0.30.3 0.50.4 0.80.5 1.30.6 1.70.7 2.10.8 2.50.9 2.81.0 3.0New Design

Tech Maturity

Min Mods

Moderate Mods

Major Mods

NR/T1 vs. % New Design

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

0.0 0.2 0.4 0.6 0.8 1.0

% New Design

N R / T 1

* For earth orbiting spacecraft

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 11/26

Cost Drivers Learning Event, 2nd November 2005

16 September 2005 11

Modeling NR Costs Using Reuse Use our plant economic model to build-up the T1

costs

Use T1 costs and reuse (or percent new design) todetermine NR costs

Look at effect of reuse on NR cost

How does this affect total cost improvement? Total acquisition costs = NR+ REC costs

Not really interesting until we look at other costimprovement factors like learning and amortization

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 12/26

Cost Drivers Learning Event, 2nd November 2005

16 September 2005 12

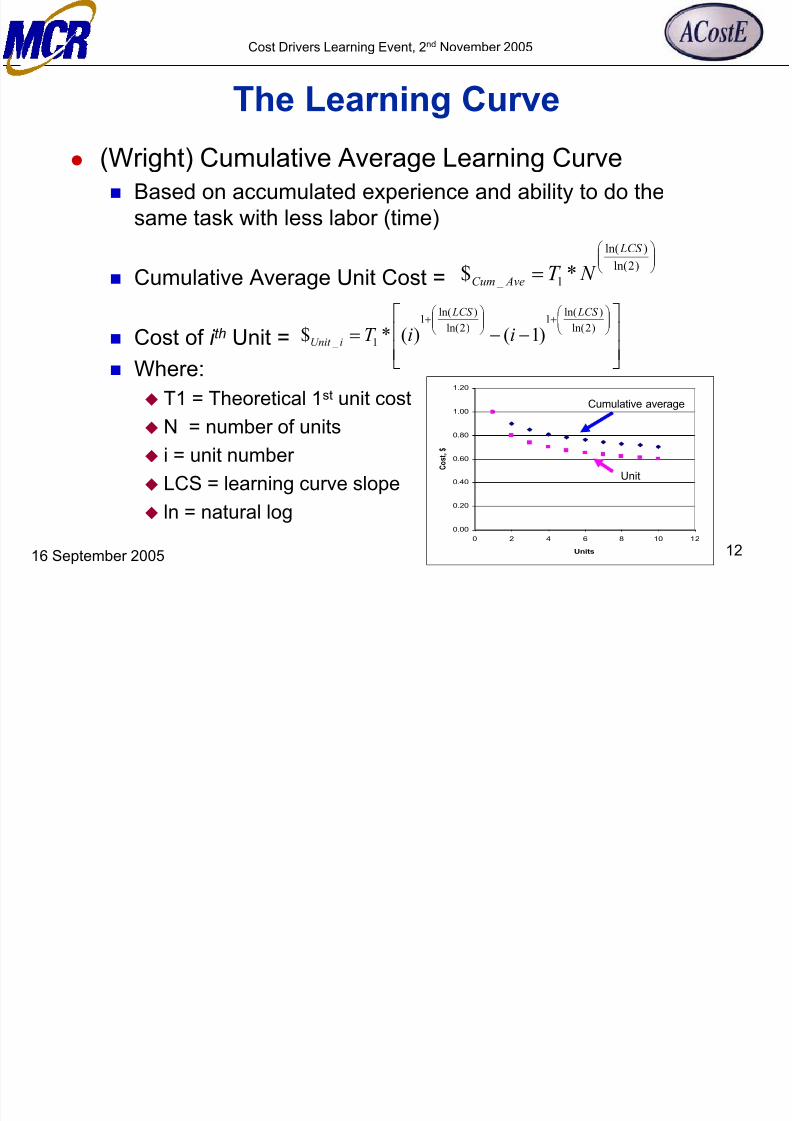

The Learning Curve (Wright) Cumulative Average Learning Curve

Based on accumulated experience and ability to do thesame task with less labor (time)

Cumulative Average Unit Cost =

Cost of i th Unit =

Where:

T1 = Theoretical 1st unit cost

N = number of units

i = unit number

LCS = learning curve slope

ln = natural log

= )2ln(

)ln(

1 _ *$

LCS

AveCum N T

−−=

+

+

)2ln()ln(1

)2ln()ln(1

1 _ )1()(*$ LCS LCS

iUnit iiT

0.00

0.20

0.40

0.60

0.80

1.00

1.20

0 2 4 6 8 10 12

Units

C o s t ,

$

Cumulative average

Unit

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 13/26

Cost Drivers Learning Event, 2nd November 2005

16 September 2005 13

Observations on Learning Can be measured in hours and dollars (Euros and Pounds are

OK as well!)

This implies that it covers the same work content Accounting standards need to include NR and REC cost definitions

True learning should be independent of other factors such as: Reuse of existing designs, materials, equipment, effort, or products

Skill Mix changes Process shortcuts that eliminate effort or expenses

Yield improvements that reduce cost

Production Rate increases allowing for amortization of pooled

costs and greater efficiency Technological advances allowing greater yield and efficiency

Inflation which measures the time variable cost of a “basket of goods”

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 14/26

Cost Drivers Learning Event, 2nd November 2005

16 September 2005 14

0.0

0.2

0.4

0.6

0.8

1.0

1.2

0 2 4 6 8 10 12

Units

C o s t , $

Unit Cost

The Production Rate Curve Production Rate Curve

Division of labor and overheads with number (N) of units

produced over a period of time Strongly influenced by amortization of period and fixed costs

Unit cost =

“Bath tub” shape due to added capital equipment and labor whenproduction capacity is exceeded

N

iable fixed

Unit

var $$$

+=

Max capacity

Increase

fixed costs

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 15/26

Cost Drivers Learning Event, 2nd November 2005

16 September 2005 15

Yield "Yield" is the fraction of units that meet specifications

Unit cost =

Process Screening

Fail = Does Not MeetSpecifications

Pass = MeetsSpecifications

N UnitsStarted

yield N

iable fixed

unit *

$$

$

var +

=

MeetsSpecifications

Does Not MeetSpecifications

0.0

0.2

0.4

0.6

0.8

1.0

1.2

0.0 0.2 0.4 0.6 0.8 1.0

Yield

U n i t C o s t ,

$

Unit Cost

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 16/26

Cost Drivers Learning Event, 2nd November 2005

16 September 2005 16

Sensitivity Analysis What affects cost improvement the most?

Reuse?

Amortization (production rate)? Yield?

Depends on the scenario (looked at 5 scenarios)

Small quantity satellite production Medium quantity satellite production

Large quantity satellite production

Electronic box production

Integrated circuit production

Use plant model with uniform distributions of quantity,reuse, amortization and yield to show sensitivity

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 17/26

Cost Drivers Learning Event, 2nd November 2005

16 September 2005 17

The Plant Model Equations Start with parameters we wish to vary: Total number of projects over which non-pooled costs will be amortized

Learning curve slope (LCS)

Yield parameters (start quantity, yield, final quantity)

Percent reuse for nonrecurring costs Pooled rate factor (factor for adjusting pooled / period costs)

Determine Direct costs T1 costs are constants

T1(labor) = 100, T1(material) = 20, T1(expenses) = 12

NR costs = f(T1, Reuse) from reuse table Recurring Costs from learning curve

Total direct costs = NR + Rec costs

Add indirect costs to direct costs using these factors

Materials (5%), Labor (150%), Expenses (70%) Add period costs (constants adjusted by pooled rate factor)

MIN MAX BASE

1 2 Total Projects 1

0.999 1 LCS 1800 1200 FinalQuantity 1000

Start Quantity 2000

0.2 0.7 Yield 0.50.2 0.8 Reuse 0.8

1 3 Pooled Rate Factor 2

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 18/26

Cost Drivers Learning Event, 2nd November 2005

16 September 2005 18

Small Quantity Satellite Production Most sensitive to new design

MIN MAX BASE

1 2 Total Projects 1

0.9 1 LCS 11 3 FinalQuantity 2

Start Quantity 2

0.99 1 Yield 10.2 0.7 Reuse 0.5

250 400 Pooled Rate Factor 300

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 19/26

Cost Drivers Learning Event, 2nd November 2005

16 September 2005 19

Medium Quantity Satellite Production Most sensitive to:

New Design

Learning curve slope

MIN MAX BASE

1 2 Total Projects 1

0.9 1 LCS 14 10 FinalQuantity 5

Start Quantity 5

0.99 1 Yield 10.2 0.7 Reuse 0.5

250 400 Pooled Rate Factor 300

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 20/26

Cost Drivers Learning Event, 2nd November 2005

16 September 2005 20

Large Quantity Satellite Production Most sensitive to:

Learning curve slope

MIN MAX BASE

1 2 Total Projects 1

0.98 1 LCS 120 40 FinalQuantity 30

Start Quantity 30

0.99 1 Yield 10.2 0.7 Reuse 0.5

250 400 Pooled Rate Factor 300

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 21/26

Cost Drivers Learning Event, 2nd November 2005

16 September 2005 21

Electronic Box Production Most sensitive to:

Period costs (amortization)

MIN MAX BASE

1 2 Total Projects 1

0.98 1 LCS 120 80 FinalQuantity 50

Start Quantity 63

0.5 0.8 Yield 0.80.2 0.8 Reuse 0.810 30 Pooled Rate Factor 20

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 22/26

Cost Drivers Learning Event, 2nd November 2005

16 September 2005 22

Integrated Circuit Production Most sensitive to yield

MIN MAX BASE

1 2 Total Projects 1

0.999 1 LCS 1800 1200 FinalQuantity 1000

Start Quantity 2000

0.2 0.7 Yield 0.50.2 0.8 Reuse 0.8

1 3 Pooled Rate Factor 2

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 23/26

Cost Drivers Learning Event, 2nd November 2005

16 September 2005 23

Results of Scenarios Model results tell us what we probably already know

In small quantity production, reuse is the most important costimprovement factor

In large quantity, labor intensive production, learning is the mostimportant factor

In large quantity electronic box production, production rate is themost important factor

In very large quantity, automated processes, yield is the most

important factor

Scenario Quantities Primary Cost Improvement Factor:

Small quantity satellite production 1-3 Reuse (New design)

Medium quantity satellite production 4-10 Reuse & Learing curve slopeLarge quantity satellite production 20-40 Learning curve slope

Electronic box production 20-80 Amortization (production rate)

Integrated circuit production 800-1200 Yield

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 24/26

Cost Drivers Learning Event, 2nd November 2005

16 September 2005 24

Summary Many factors affect cost improvement

Cost improvement can be obtained betweensubsequent programs or subsequent production units

Use plant model to show sensitivities of these factors

We chose reuse, learning, amortization (productionrate) and yield

Effects are scenario dependent

Depends on quantity of production and production volumes Also depends on amount of process automation and external

factors such as plant amortization

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 25/26

Cost Drivers Learning Event, 2nd November 2005

16 September 2005 25

Acronym List NR = Nonrecurring cost

T1 = Theoretical first unit recurring cost

T2 = Theoretical second unit [recurring] cost

P1 = Theoretical first prototype unit cost

REC = Recurring cost

LCS = Learning curve slope

ML = Most likely

NR/T1 = Ratio of NR to T1 costs

N = number of units

i = unit number

ln = natural log

8/8/2019 Cost Improvement Curves Learning Amortization and Yield - Covert

http://slidepdf.com/reader/full/cost-improvement-curves-learning-amortization-and-yield-covert 26/26

Cost Drivers Learning Event, 2nd November 2005

16 September 2005 26

References1. Stewart, R. and Wyskida, R., “Cost Estimator’s Reference Manual”, 1997, John Wiley and

Sons, New York.

2. “Pricing Handbook: Cost Accounting Standards”, Federal Aviation Administration,

http://fast.faa.gov/archive/v1198/pguide/98-30C14.htm