a research on amortization

TRANSCRIPT

8/4/2019 A Research on Amortization

http://slidepdf.com/reader/full/a-research-on-amortization 1/8

A

Research on Amortization

Submitted to:

Dr. Elvira Aniciete

Submitted by:

Abero, Ian Floro Y.Magnayon, Maria Erika Paulyn R.

Molinyawe, Angelou H.

Sulit, Julius Benedict I.

Villar, Kristine B.

8/4/2019 A Research on Amortization

http://slidepdf.com/reader/full/a-research-on-amortization 2/8

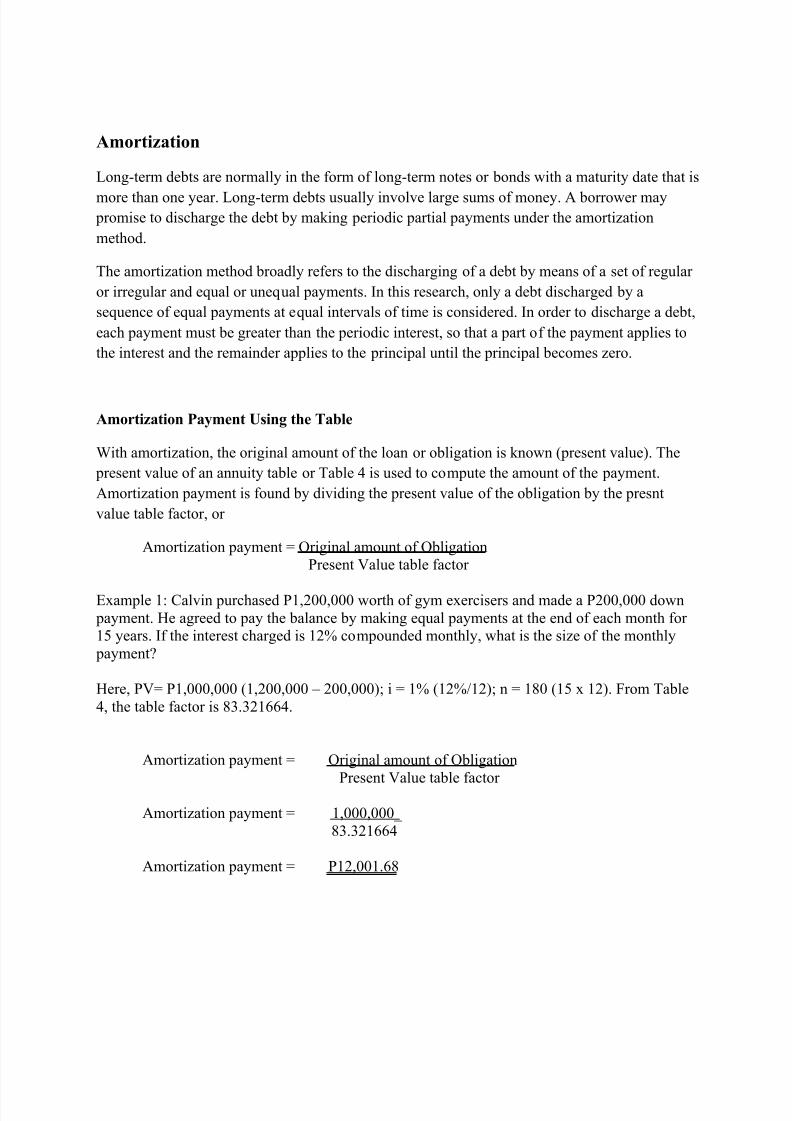

Amortization

Long-term debts are normally in the form of long-term notes or bonds with a maturity date that is

more than one year. Long-term debts usually involve large sums of money. A borrower may promise to discharge the debt by making periodic partial payments under the amortization

method.

The amortization method broadly refers to the discharging of a debt by means of a set of regular

or irregular and equal or unequal payments. In this research, only a debt discharged by a

sequence of equal payments at equal intervals of time is considered. In order to discharge a debt,

each payment must be greater than the periodic interest, so that a part of the payment applies to

the interest and the remainder applies to the principal until the principal becomes zero.

Amortization Payment Using the Table

With amortization, the original amount of the loan or obligation is known (present value). The

present value of an annuity table or Table 4 is used to compute the amount of the payment.

Amortization payment is found by dividing the present value of the obligation by the presnt

value table factor, or

Amortization payment = Original amount of ObligationPresent Value table factor

Example 1: Calvin purchased P1,200,000 worth of gym exercisers and made a P200,000 down

payment. He agreed to pay the balance by making equal payments at the end of each month for 15 years. If the interest charged is 12% compounded monthly, what is the size of the monthly

payment?

Here, PV= P1,000,000 (1,200,000 – 200,000); i = 1% (12%/12); n = 180 (15 x 12). From Table

4, the table factor is 83.321664.

Amortization payment = Original amount of Obligation

Present Value table factor

Amortization payment = 1,000,000_

83.321664

Amortization payment = P12,001.68

8/4/2019 A Research on Amortization

http://slidepdf.com/reader/full/a-research-on-amortization 3/8

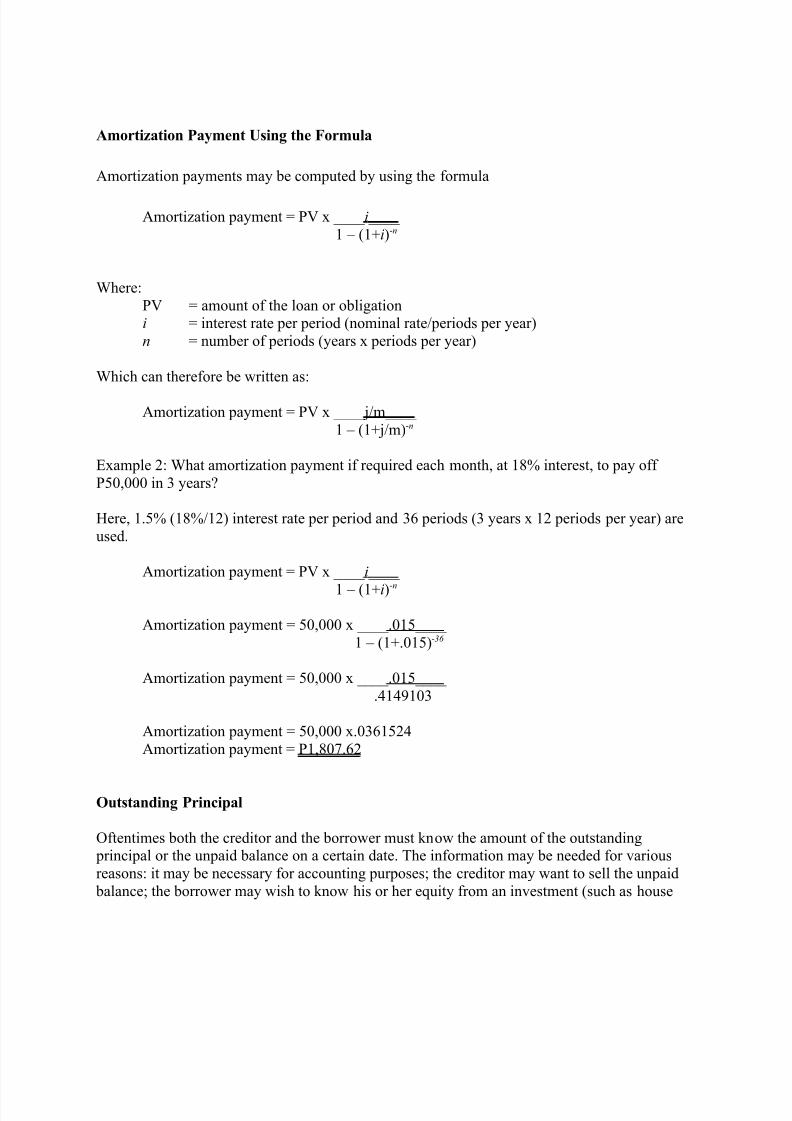

Amortization Payment Using the Formula

Amortization payments may be computed by using the formula

Amortization payment = PV x ____ i ____

1 – (1+i)-n

Where:

PV = amount of the loan or obligationi = interest rate per period (nominal rate/periods per year)

n = number of periods (years x periods per year)

Which can therefore be written as:

Amortization payment = PV x ____j/m____

1 – (1+j/m)-n

Example 2: What amortization payment if required each month, at 18% interest, to pay off

P50,000 in 3 years?

Here, 1.5% (18%/12) interest rate per period and 36 periods (3 years x 12 periods per year) are

used.

Amortization payment = PV x ____ i ____

1 – (1+i)-n

Amortization payment = 50,000 x ____.015____

1 – (1+.015)-36

Amortization payment = 50,000 x ____.015____

.4149103

Amortization payment = 50,000 x.0361524

Amortization payment = P1,807.62

Outstanding Principal

Oftentimes both the creditor and the borrower must know the amount of the outstanding principal or the unpaid balance on a certain date. The information may be needed for various

reasons: it may be necessary for accounting purposes; the creditor may want to sell the unpaid

balance; the borrower may wish to know his or her equity from an investment (such as house

8/4/2019 A Research on Amortization

http://slidepdf.com/reader/full/a-research-on-amortization 4/8

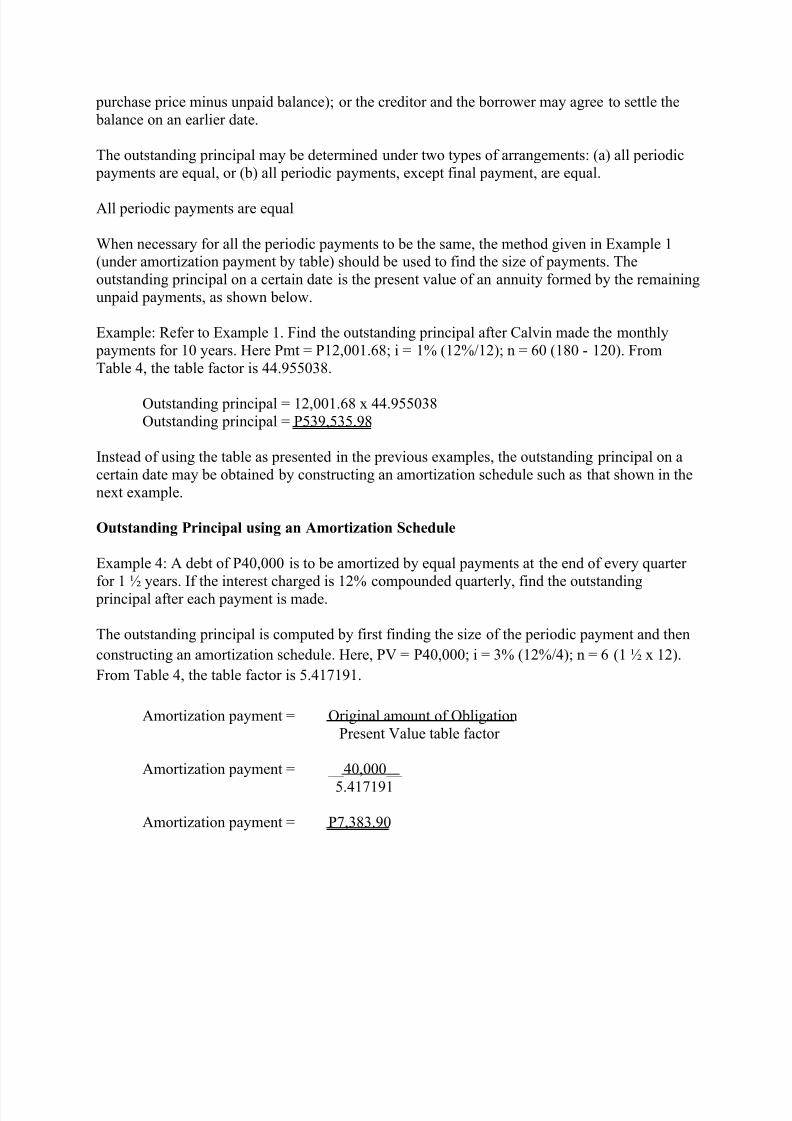

purchase price minus unpaid balance); or the creditor and the borrower may agree to settle the

balance on an earlier date.

The outstanding principal may be determined under two types of arrangements: (a) all periodic

payments are equal, or (b) all periodic payments, except final payment, are equal.

All periodic payments are equal

When necessary for all the periodic payments to be the same, the method given in Example 1(under amortization payment by table) should be used to find the size of payments. The

outstanding principal on a certain date is the present value of an annuity formed by the remaining

unpaid payments, as shown below.

Example: Refer to Example 1. Find the outstanding principal after Calvin made the monthly

payments for 10 years. Here Pmt = P12,001.68; i = 1% (12%/12); n = 60 (180 - 120). From

Table 4, the table factor is 44.955038.

Outstanding principal = 12,001.68 x 44.955038

Outstanding principal = P539,535.98

Instead of using the table as presented in the previous examples, the outstanding principal on a

certain date may be obtained by constructing an amortization schedule such as that shown in the

next example.

Outstanding Principal using an Amortization Schedule

Example 4: A debt of P40,000 is to be amortized by equal payments at the end of every quarter

for 1 ½ years. If the interest charged is 12% compounded quarterly, find the outstanding

principal after each payment is made.

The outstanding principal is computed by first finding the size of the periodic payment and then

constructing an amortization schedule. Here, PV = P40,000; i = 3% (12%/4); n = 6 (1 ½ x 12).

From Table 4, the table factor is 5.417191.

Amortization payment = Original amount of Obligation

Present Value table factor

Amortization payment = __40,000__

5.417191

Amortization payment = P7,383.90

8/4/2019 A Research on Amortization

http://slidepdf.com/reader/full/a-research-on-amortization 5/8

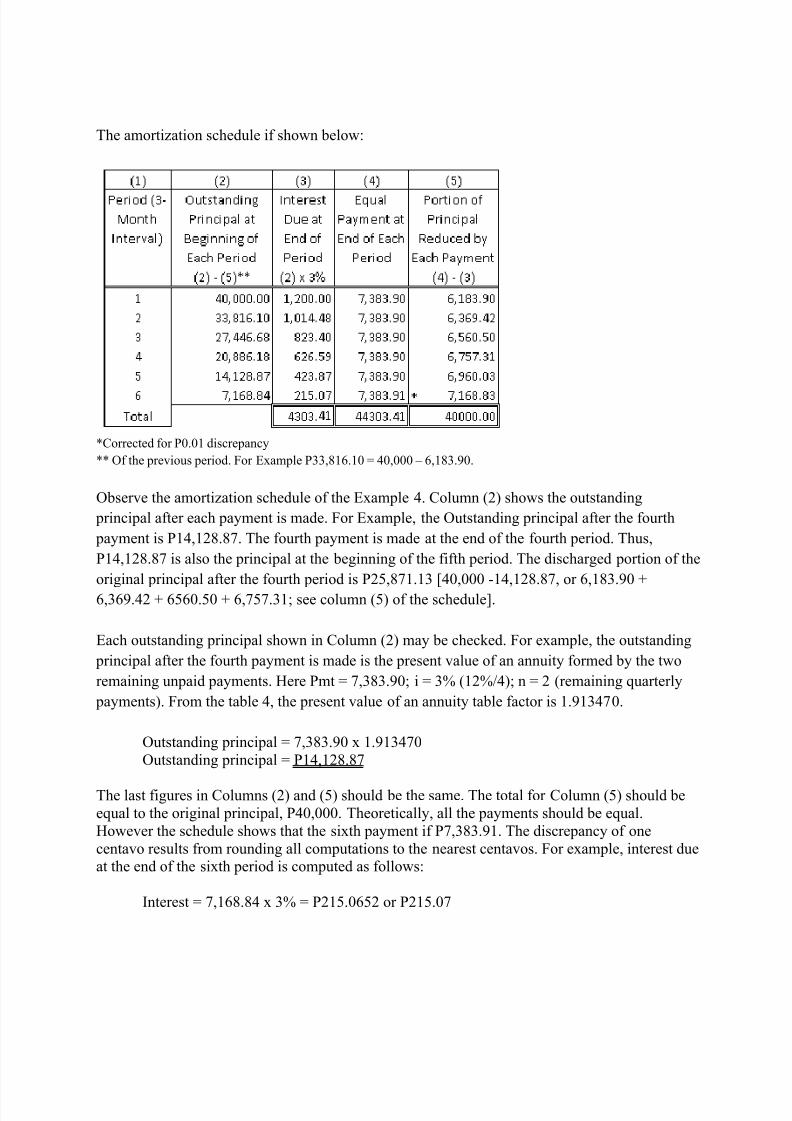

The amortization schedule if shown below:

*Corrected for P0.01 discrepancy

** Of the previous period. For Example P33,816.10 = 40,000 – 6,183.90.

Observe the amortization schedule of the Example 4. Column (2) shows the outstanding

principal after each payment is made. For Example, the Outstanding principal after the fourth

payment is P14,128.87. The fourth payment is made at the end of the fourth period. Thus,

P14,128.87 is also the principal at the beginning of the fifth period. The discharged portion of the

original principal after the fourth period is P25,871.13 [40,000 -14,128.87, or 6,183.90 +

6,369.42 + 6560.50 + 6,757.31; see column (5) of the schedule].

Each outstanding principal shown in Column (2) may be checked. For example, the outstanding

principal after the fourth payment is made is the present value of an annuity formed by the two

remaining unpaid payments. Here Pmt = 7,383.90; i = 3% (12%/4); n = 2 (remaining quarterly

payments). From the table 4, the present value of an annuity table factor is 1.913470.

Outstanding principal = 7,383.90 x 1.913470

Outstanding principal = P14,128.87

The last figures in Columns (2) and (5) should be the same. The total for Column (5) should be

equal to the original principal, P40,000. Theoretically, all the payments should be equal.

However the schedule shows that the sixth payment if P7,383.91. The discrepancy of one

centavo results from rounding all computations to the nearest centavos. For example, interest dueat the end of the sixth period is computed as follows:

Interest = 7,168.84 x 3% = P215.0652 or P215.07

8/4/2019 A Research on Amortization

http://slidepdf.com/reader/full/a-research-on-amortization 6/8

The size of the sixth payment, therefore, is 7,168.84 + 215.07 = P7,383.91. The final payment

covers the outstanding principal at the beginning of the last payment interval and the interest duethereon.

Here, the interest for each period is computed by the simple interest method. It should beobserved that when a debtor makes each of the simple interest payments on the interest date, the

simple interest method is actually a compound interest method.

Also, note that as the principal gradually reduced, the periodic interest becomes smaller after

each payment is made. Thus, a greater portion of each equal payment is used in reducing the

principal.

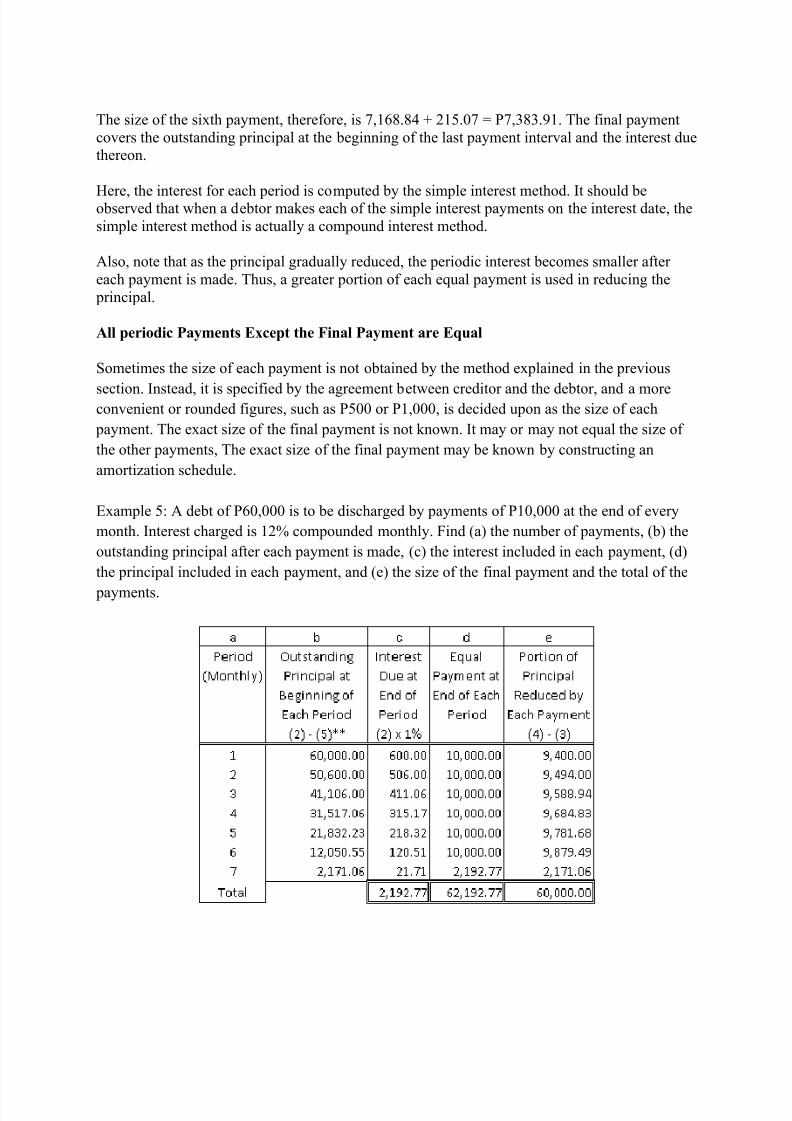

All periodic Payments Except the Final Payment are Equal

Sometimes the size of each payment is not obtained by the method explained in the previous

section. Instead, it is specified by the agreement between creditor and the debtor, and a moreconvenient or rounded figures, such as P500 or P1,000, is decided upon as the size of each

payment. The exact size of the final payment is not known. It may or may not equal the size of

the other payments, The exact size of the final payment may be known by constructing an

amortization schedule.

Example 5: A debt of P60,000 is to be discharged by payments of P10,000 at the end of every

month. Interest charged is 12% compounded monthly. Find (a) the number of payments, (b) the

outstanding principal after each payment is made, (c) the interest included in each payment, (d)

the principal included in each payment, and (e) the size of the final payment and the total of the

payments.

8/4/2019 A Research on Amortization

http://slidepdf.com/reader/full/a-research-on-amortization 7/8

8/4/2019 A Research on Amortization

http://slidepdf.com/reader/full/a-research-on-amortization 8/8

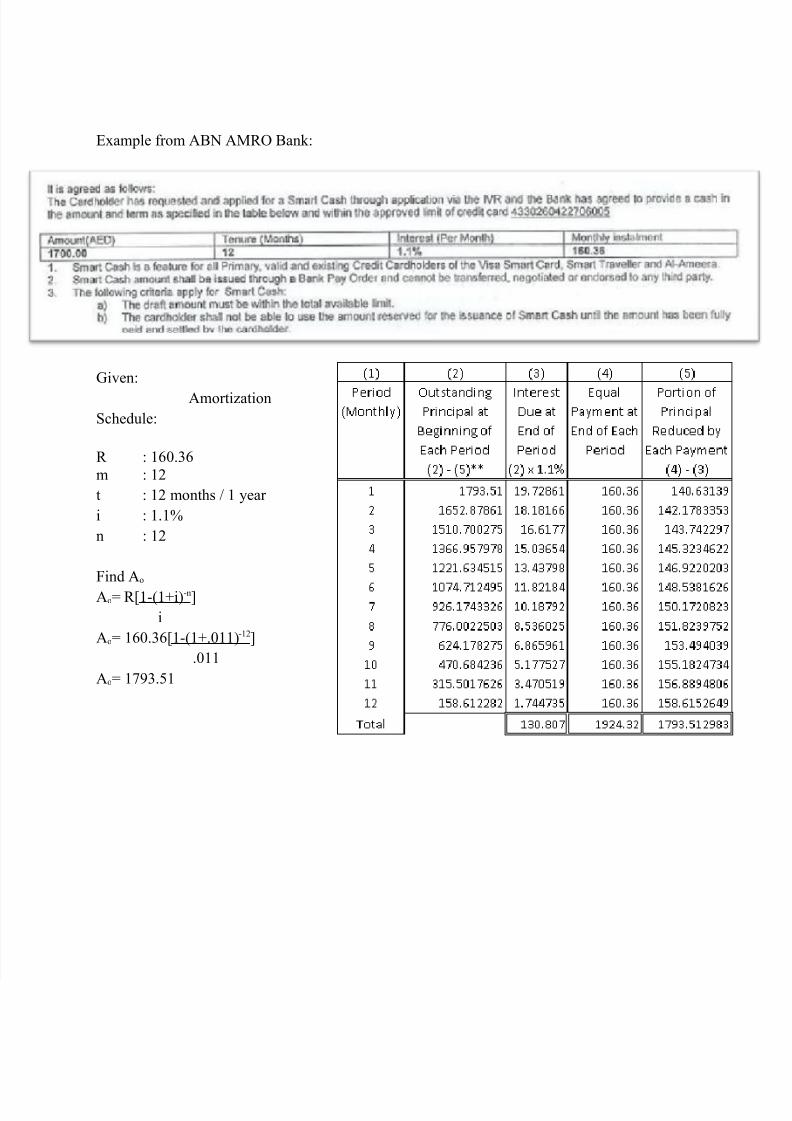

Example from ABN AMRO Bank:

Given:

Amortization

Schedule:

R : 160.36

m : 12

t : 12 months / 1 year

i : 1.1%

n : 12

Find Ao

Ao= R[1-(1+i)-n]

i

Ao= 160.36[1-(1+.011)-12]

.011

Ao= 1793.51