corporate social capital implementation draft guidance ... · zingales, 2008). moreover, social...

TRANSCRIPT

DGD 1 09-02-2018

Corporate Social Capital Implementation

Draft Guidance Document 1

Table of Contents Page No. 1 Introduction 1 1.1 Scope of the Guidance Document (GD) 4 1.2 Development Stages of the GD 4 1.3 What is Social Capital? 4 1.4 Corporate Social Capital 6 2 Development of Social Responsibility Practices and Social Capital in

Corporations 8

3 Management Approach for the Development of Corporate Social Capital while

Performing Corporate Social Responsibility 12

3.1 Stage 1: Forming Stage (PLAN) 14 3.2 Stage 2: Implementing Stage (DO) 15 3.3 Stage 3: Confirming Stage (CHECK) 16 3.4 Stage 4: Improving Stage (ACT) 16 Annex A

Linking Corporate Social Capital to HKQAA Sustainability Rating and

Research (HKQAA SRR) for Hang Seng Corporate Sustainability Index Series

(Index Series)

18

Annex B HKQAA SRR seven core subjects and subsequent practices

21

Annex C Implementation Templates for CSC projects to be supplemented in DGD 2 after completion of the pilot-run projects

23

Annex D Case studies

24

4 Bibliography 25 5 Acknowledgments 28

1

1 Introduction

Community Investment and Inclusion Fund (CIIF) was set up by the Government of the Hong

Kong Special Administrative Region in 2002 to implement diversified Social Capital development

projects in the community, promote reciprocity between the public and private sectors, and build

together a cross-sectoral collaborative platform and mutual help network. The Fund seeks to build

Social Capital – to garner mutual trust, social networks, spirit of cooperation and social cohesion,

and enhance mutual support among individuals, families and organizations, so that our community

can grow from strength to strength.

While addressing organization’s objectives and targets, the CIIF funded projects aim to achieve six

core Social Capital dimensions, namely, (1) social networks; (2) trust and solidarity; (3) mutual

help and reciprocity; (4) social cohesion and inclusion; (5) social participation; and (6) information

and communication.

Nowadays, corporations around the world and their stakeholders, including direct stakeholders such

as their employees, customers, end-users, investors, suppliers, and indirect stakeholders such as the

regulators, governmental agencies, non-governmental organizations, pressure groups,

neighbourhoods and media, etc., are becoming increasingly aware of the need for corporations to

exhibit and disclose their socially responsible behaviour. This may pose social risks to the

corporations but these, when being properly managed, will in turn bring about numerous

opportunities for corporations.

Corporations could enhance their transparency and accountability to their stakeholders by means of

Environmental, Social and Governance (ESG) or sustainability reporting, which would

communicate the risks and opportunities they face and how they manage them for achieving

sustainable development.

To promote the concept of social responsibility and to assist organizations in contributing to

sustainable development, the ISO 26000:2010 Guidance on social responsibility identifies norms of

seven core subjects of social responsibility, including organizational governance, human rights,

labour practices, the environment, fair operating practices, consumer issues, and community

involvement and development (International Organization for Standardization [ISO], 2010). By

addressing and acting on the core subjects, corporations are not only performing their social

responsibility, but also contributing to sustainable development and creating benefits for society.

In 2014, the Hong Kong Quality Assurance Agency (HKQAA) designed and developed its

proprietary management and assessment methodology, namely, the HKQAA Sustainability Rating

and Research (HKQAA SRR) methodology, for organizations to manage their social risks and

opportunities, and ultimately assess their social responsibility performance in contributing to

sustainable development (HKQAA, 2016). Since then, this methodology has been used for the

HKQAA Corporate Social Responsibility (CSR) Index Plus assessment and for supporting the

compilation of Hang Seng Corporate Sustainability Index Series (Index Series).

2

The HKQAA SRR was developed mainly based on ISO 26000:2010 Guidance on social

responsibility and the Plan-Do-Check-Act (PDCA) model (Moen & Norman, 2009). The PDCA

management model is widely adopted by various international management system standards, such

as ISO 9001 Quality Management Systems (ISO, 2015a) and ISO 14001 Environmental

Management Systems (ISO, 2015b).

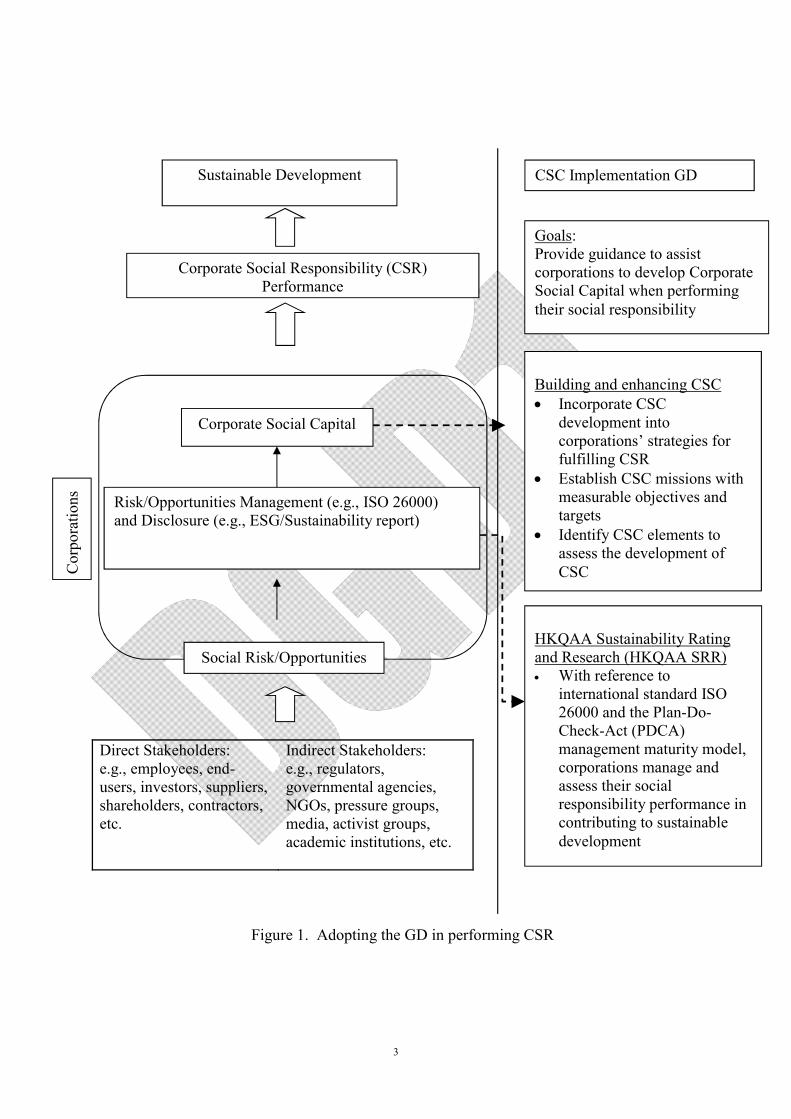

This Corporate Social Capital Implementation Guidance Document (GD) is intended to assist

corporations to develop their Corporate Social Capital (CSC) while performing their CSR. More

specifically, corporations will learn how to use the HKQAA SRR methodology and its elements as

a management tool in performing CSR with the six core Social Capital dimensions as the

underlying concepts. The linkage to the Index Series will also be demonstrated in this GD. Figure 1

illustrates how the adoption of GD can help corporations in performing CSR and to maximize their

contribution to sustainable development.

3

Corporate Social Capital

Risk/Opportunities Management (e.g., ISO 26000) and Disclosure (e.g., ESG/Sustainability report)

Cor

pora

tion

s

Direct Stakeholders: e.g., employees, end-users, investors, suppliers, shareholders, contractors, etc.

Indirect Stakeholders: e.g., regulators, governmental agencies, NGOs, pressure groups, media, activist groups, academic institutions, etc.

CSC Implementation GD

Goals: Provide guidance to assist corporations to develop Corporate Social Capital when performing their social responsibility

Building and enhancing CSC Incorporate CSC

development into corporations’ strategies for fulfilling CSR

Establish CSC missions with measurable objectives and targets

Identify CSC elements to assess the development of CSC

HKQAA Sustainability Rating and Research (HKQAA SRR) With reference to

international standard ISO 26000 and the Plan-Do-Check-Act (PDCA) management maturity model, corporations manage and assess their social responsibility performance in contributing to sustainable development

Social Risk/Opportunities

Sustainable Development

Corporate Social Responsibility (CSR) Performance

Figure 1. Adopting the GD in performing CSR

4

1.1 Scope of the Guidance Document

This Guidance Document (GD) provides guidance to corporations, independent of their activity or

size, on developing Social Capital in their organizations while performing their social responsibility.

The methodologies provided in this GD will serve as a management and assessment tool.

1.2 Development Stages of the GD

The development and publication of this GD will be accomplished in 3 stages, namely, the Draft

Guidance Document 1 (DGD1), Draft Guidance Document 2 (DGD2) and the final

Guidance Document (GD).

The DGD1 will be published based on the findings of the literature review and the advice gathered

from the Stakeholders Group (SG) which is composed of approximately 10 individual members

from various sectors including corporations, NGOs, academic institutions and the government.

The DGD1 contains the conceptual design of the Corporate Social Capital (CSC)

framework which will be subject to the trial implementation by the collaborating corporations.

The DGD2 will be published after the trial implementation by mid-2019. The DGD2 will contain a

detailed CSC framework and a list of plausible elements (see Table 3 on p.10) of CSC under the six

core dimensions of Social Capital. A solid process flow and measurement tool will also be

developed for more widespread adoption. The experience gained from various supporting activities

including an online platform, pilot community projects, personnel and project registration

schemes will contribute to the final version.

The final Guidance Document (GD) is expected to be published early 2020 alongside the wider

adoption of DGD2. The linkage between CSC management model developed and the HKQAA

SRR will also be supplemented in Annex A of the final GD.

1.3 What is Social Capital?

Social Capital is considered as one of the key drivers of social development in modern societies,

the other being economic capital, cultural capital and human capital. According to the World Bank,

Social Capital refers to “the institutions, relationships, attitudes, and values that govern interactions

among people and contribute to economic and social development” (Grootaert and van Bastelaer,

2001). Social Capital is seen as the “connections among individuals, social networks and norms of

reciprocity and trustworthiness that arise from them” (Putman, 2000). Meanwhile, the Organisation

for Economic Co-operation and Development (OECD) defines Social Capital as “networks

together with shared norms, values and understandings that facilitate cooperation within or among

groups” (OECD, 2001).

Social capital includes social norms (personal attitudes and social values), networks and institutions. The strategies deployed in social capital development include cognitive, relational and structural aspects, incorporating psychological and sociological concepts of role transformation, social trust

5

in horizontal bridging across heterogeneous groups and collaboration in vertical linking partnerships across sectors and power hierarchy. Increasing evidence has shown that social cohesion is essential for economic prosperity and long-term sustainable development of a society. Social capital holds people and institutions together to work for the common good. The multifaceted nature of Social Capital is shown in Table 1 below.

Table 1. Multifaceted nature of Social Capital

Aspects of Social Capital (Nahapiet and Ghoshal, 1998)

Cognitive Focus on the people’s feelings, values and perceptions. It represents resources

obtained from a shared vision and value, common set of goals and shared

representations and interpretations among groups.

Relational Kind of personal relationships people have developed with each other through

interactions, with focuses on the quality of the relationship or interactions and

the resources that are created or balanced. It attributes the relationship of trust,

trustworthiness, respect and friendship.

Structural Structure or pattern of connections between people – who you contact, how to

contact and frequency of shared resources and information. It accounts for what

people do (associational links, networks).

Forms of Social Capital (as cited in Ting, 2012)

Bonding Linkage between like-minded people (Putnam, 2000).

Bridging Links between people of heterogeneous groups or with different backgrounds.

Through these linkages, people would have access to external resources of

different groups (Putnam, 2000; Gittel and Vidal, 1998).

Linking Linkage in the vertical dimension of bridging Social Capital, in which people of

different groups could leverage resources, ideas and information from those who

have power to those who do not in the community (Woolcock, 2001).

From the economic perspective, various studies have shown that Social Capital is important for

economic growth and development (Fukuyama, 1995; Knack & Keefer, 1997; Guiso, Sapienza, &

Zingales, 2008). Moreover, Social Capital, together with Governance, Personal Freedom and Safety

& Security, are described as the four institutional pillars1 in measuring society’s wealth and well-

being in the Legatum Prosperity IndexTM (Legatum Institute Foundation, 2017). The report has

shown that Social Capital is an essential element in developing prosperity.

1 There are nine pillars in the Legatum Prosperity IndexTM measurement.

6

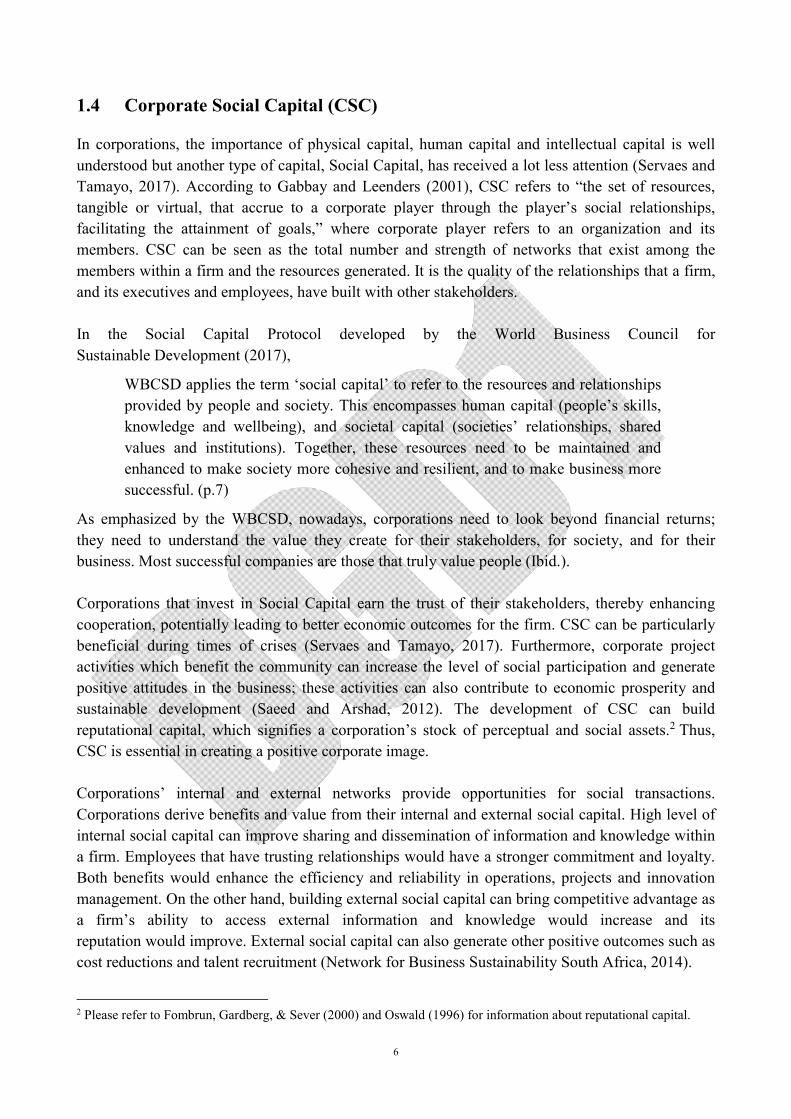

1.4 Corporate Social Capital (CSC)

In corporations, the importance of physical capital, human capital and intellectual capital is well

understood but another type of capital, Social Capital, has received a lot less attention (Servaes and

Tamayo, 2017). According to Gabbay and Leenders (2001), CSC refers to “the set of resources,

tangible or virtual, that accrue to a corporate player through the player’s social relationships,

facilitating the attainment of goals,” where corporate player refers to an organization and its

members. CSC can be seen as the total number and strength of networks that exist among the

members within a firm and the resources generated. It is the quality of the relationships that a firm,

and its executives and employees, have built with other stakeholders.

In the Social Capital Protocol developed by the World Business Council for

Sustainable Development (2017),

WBCSD applies the term ‘social capital’ to refer to the resources and relationships

provided by people and society. This encompasses human capital (people’s skills,

knowledge and wellbeing), and societal capital (societies’ relationships, shared

values and institutions). Together, these resources need to be maintained and

enhanced to make society more cohesive and resilient, and to make business more

successful. (p.7)

As emphasized by the WBCSD, nowadays, corporations need to look beyond financial returns;

they need to understand the value they create for their stakeholders, for society, and for their

business. Most successful companies are those that truly value people (Ibid.).

Corporations that invest in Social Capital earn the trust of their stakeholders, thereby enhancing

cooperation, potentially leading to better economic outcomes for the firm. CSC can be particularly

beneficial during times of crises (Servaes and Tamayo, 2017). Furthermore, corporate project

activities which benefit the community can increase the level of social participation and generate

positive attitudes in the business; these activities can also contribute to economic prosperity and

sustainable development (Saeed and Arshad, 2012). The development of CSC can build

reputational capital, which signifies a corporation’s stock of perceptual and social assets.2 Thus,

CSC is essential in creating a positive corporate image.

Corporations’ internal and external networks provide opportunities for social transactions.

Corporations derive benefits and value from their internal and external social capital. High level of

internal social capital can improve sharing and dissemination of information and knowledge within

a firm. Employees that have trusting relationships would have a stronger commitment and loyalty.

Both benefits would enhance the efficiency and reliability in operations, projects and innovation

management. On the other hand, building external social capital can bring competitive advantage as

a firm’s ability to access external information and knowledge would increase and its

reputation would improve. External social capital can also generate other positive outcomes such as

cost reductions and talent recruitment (Network for Business Sustainability South Africa, 2014).

2 Please refer to Fombrun, Gardberg, & Sever (2000) and Oswald (1996) for information about reputational capital.

7

In matching with the trend of disclosing ESG information by corporate organizations in Hong Kong,

Hong Kong corporations are more willing to develop their own Corporate Social Responsibility

(CSR) activities alongside their corporate policy and business development. Research has found

that the adoption of CSR practices would help to create reliable social

networks for organizations and social capacity. Social Capital is accumulated through such

networks and interactions which encourage cooperation and collective action. The creation of

Social Capital is embedded into many corporate activities in a way that helps knowledge transfer

and innovation. It also boosts efficiency in community development and CSR (Saeed & Arshad,

2012)

In fact, many corporations have incorporated Social Capital development into their strategies for

fulfilling CSR. This includes utilizing corporate expertise to actively participate in social services,

helping disadvantaged groups expand their social networks and increase opportunities to broaden

their horizons, thereby bringing longer-term benefits to society and the corporation. When

corporations fulfil corporate social responsibilities by leveraging Social Capital development

strategy, both corporations and society can reap ample returns. In addition, corporations which

participate in implementing social capital projects can improve corporate culture and inculcate

positive values in the community and society, thereby creating an environment favourable for

social and economic development (see Figures 2 & 3).

Figure 2. Positive returns to corporations and society. Adapted from the CIIF website.

Figure 3. CSC building as an alternative investment. Adapted from the CIIF website.

8

2 Development of Social Responsibility Practices and Social Capital in

Corporations

Recognizing the importance of social responsibility to their stakeholders, a vast majority of

corporations now focus on and practice a few broad categories of corporate social responsibility

(CSR). Corporations would integrate different CSR-generated policies, practices, initiatives,

programmes, and projects in their organization based on their business vision, mission and

strategies.

The development of CSR means can take reference from the general social responsibility reference

or international standards, such as SA8000, ISO 50001, ISO 14001, ISO 26000, and United Nations’

Sustainable Development Goals (2015), etc.

Corporations can select their CSR means in accordance with the business strength, financial budget,

internal and external resources, stakeholders’ needs and expectations, respect for rules of law,

service targets and social requirements, etc. Incorporating the concept of Corporate Social Capital

(CSC) while developing CSR practices has the advantage of fostering long-lasting impact through

self-sustaining activities of a relationship network bound by shared values.

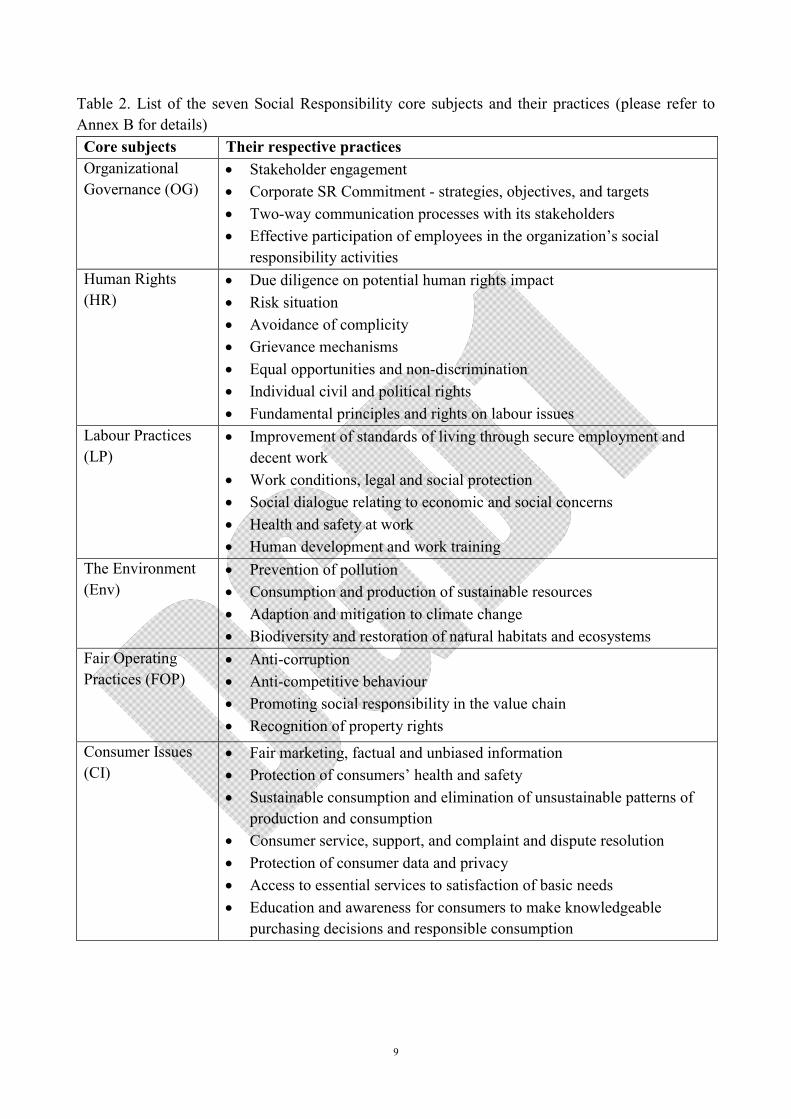

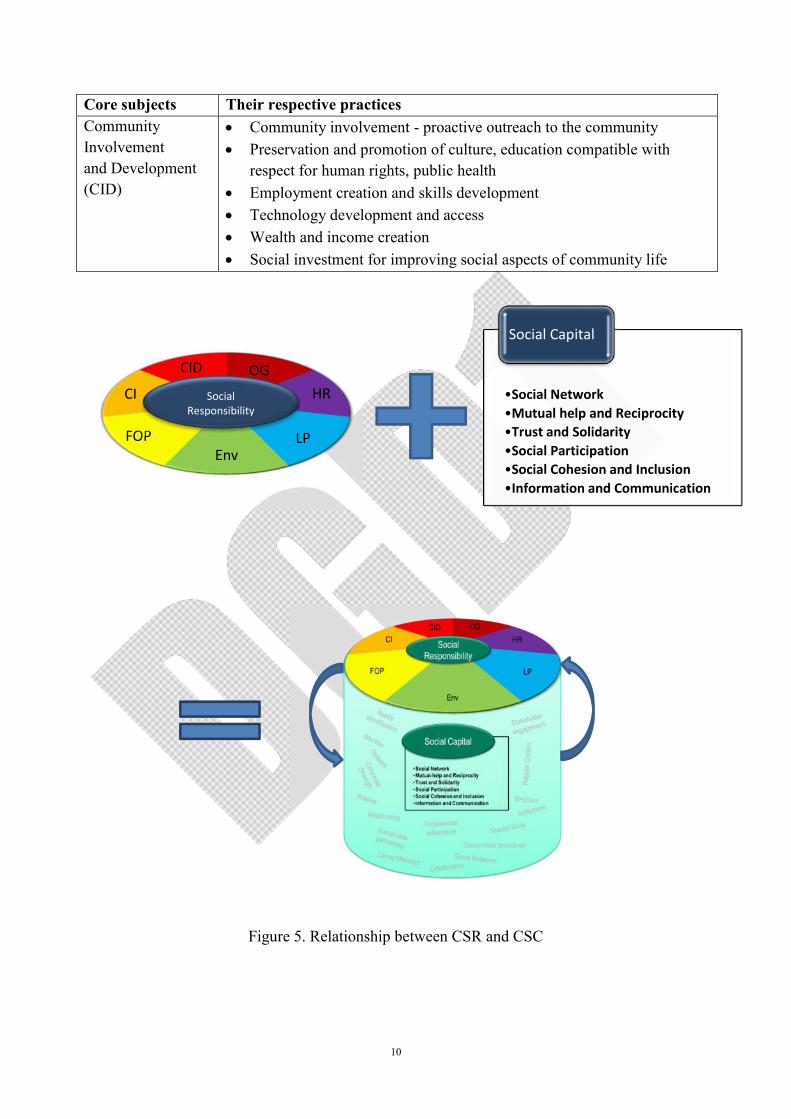

The seven social responsibility core subjects defined in ISO 26000 (Figure 4) can be applied for

corporations to build and enhance CSC. Table 2 listed the seven core subjects and a brief

description of the related social responsibility practices. Different issues of CSR may have different

CSC elements and dimensions. CSC can improve the quality of CSR implementation. By

performing CSR, organizations can build and enhance CSC. Figure 5 illustrates the relationship

between CSR and CSC. The six dimensions and elements of CSC are listed in Table 3.

Figure 4. Social Responsibility: seven core subjects. Adapted from ISO 26000

9

Table 2. List of the seven Social Responsibility core subjects and their practices (please refer to

Annex B for details)

Core subjects Their respective practices

Organizational

Governance (OG) Stakeholder engagement

Corporate SR Commitment - strategies, objectives, and targets

Two-way communication processes with its stakeholders

Effective participation of employees in the organization’s social

responsibility activities

Human Rights

(HR) Due diligence on potential human rights impact

Risk situation

Avoidance of complicity

Grievance mechanisms

Equal opportunities and non-discrimination

Individual civil and political rights

Fundamental principles and rights on labour issues

Labour Practices

(LP) Improvement of standards of living through secure employment and

decent work

Work conditions, legal and social protection

Social dialogue relating to economic and social concerns

Health and safety at work

Human development and work training

The Environment

(Env) Prevention of pollution

Consumption and production of sustainable resources

Adaption and mitigation to climate change

Biodiversity and restoration of natural habitats and ecosystems

Fair Operating

Practices (FOP) Anti-corruption

Anti-competitive behaviour

Promoting social responsibility in the value chain

Recognition of property rights

Consumer Issues

(CI) Fair marketing, factual and unbiased information

Protection of consumers’ health and safety

Sustainable consumption and elimination of unsustainable patterns of

production and consumption

Consumer service, support, and complaint and dispute resolution

Protection of consumer data and privacy

Access to essential services to satisfaction of basic needs

Education and awareness for consumers to make knowledgeable

purchasing decisions and responsible consumption

10

Core subjects Their respective practices

Community

Involvement

and Development

(CID)

Community involvement - proactive outreach to the community

Preservation and promotion of culture, education compatible with

respect for human rights, public health

Employment creation and skills development

Technology development and access

Wealth and income creation

Social investment for improving social aspects of community life

Figure 5. Relationship between CSR and CSC

OG

HR

LPEnv

FOP

CI

CID

Social Responsibility

•Social Network

•Mutual help and Reciprocity

•Trust and Solidarity

•Social Participation

•Social Cohesion and Inclusion

•Information and Communication

Social Capital

11

Table 3. List of Corporate Social Capital dimensions and elements

Six dimensions Elements

Social networks

Mutual-help and reciprocity

Trust and solidarity

Social participation

Social cohesion and inclusion

Information and communication

Stakeholders’ needs identification

Win-win situation demonstrated

Network established

Corporate strengths identification

SR and SC policies formulation

Relationship established

Conduct stakeholder engagement

Regular contact with relevant value chain

Provision of professional information

Social networks creation

Provision of caring message

Sustainable partnership established with the

collaborator

Shared value demonstrated

etc…

12

3 Management Approach for the Development of Corporate Social

Capital while Performing Corporate Social Responsibility

The 4-stage management method of Plan-Do-Check-Act (PDCA) for the control and continual

improvement of performance will be adopted.

Figure 6. Four-stage Plan-Do-Check-Act (PDCA) management model

Stage 1. Plan

Stage 2. Do

Stage 3. Check

Stage 4.Act

Figure 7. Flow of 4-stage Plan-Do-Check-Act (PDCA) management model

Stage 2: Do

B.1 Initiative design development and management

Stage 4: Act

D.1 Analysis of results

D.2 CSC and initiative review

meeting

Stage 1: Plan

A.1 Organization context

A.2 Stakeholders’ needs and

expectations

A.3 CSC mission establishment

A.4 Develop and provide adequate

resources

B.2 Initiative realization

B.3 Stakeholder communication

Inputs

Process

Outcome

Output

Initiative monitoring & measurement

Stage 3: Check

C.1 Monitoring and measurement

C.2 Evaluation

3.1 Stage 1: PLAN - Establish the objectives and programmes necessary to deliver results in accordance with the corporation’s targets or goals.

A.1. Organizational context

The corporation can determine its organizational context in terms of external and internal issues that are relevant to its business role and its strategic direction and that affects its ability to achieve the expected outcomes.

External issues include: legal, technological, competitive, market, cultural, social and economic environments, etc., whether international, national, regional or local.

Internal issues include: values, culture, knowledge and performance of the organization, etc.

A.2. Stakeholders’ needs and expectations

With reference to the seven core subjects and practices of CSR, the corporation identifies the needs and expectations of interested parties that are relevant to its business role and corresponding social contribution.

A diversity of relevant stakeholders may include customers, end-users, regulatory bodies, external providers, pressure groups, neighbourhoods, non-governmental organizations, governmental agencies and media, etc. Stakeholder engagement can be conducted in order to collect relevant information.

A.3. CSC mission establishment

Organizations can establish CSC missions with measurable objectives and targets with reference to external and internal issues, interested parties’ needs and expectations. Missions can be established in accordance with corporation’s goals and objectives. Organizations can also define which direct and indirect stakeholders to be served and what kinds of relationships and networks to be formed to suit the target stakeholder groups.

Periodical review of missions subject to organizations’ policy and business strategies would also provide directions for CSC development. The external and internal issues, interested parties’ needs and expectations can be monitored and reviewed regularly.

A.4. Develop and provide adequate resources

The organization should determine and provide the resources needed for the establishment, implementation, and continual improvement of the CSC development. The organization should consider:

Corporate strength, capabilities, and constraints on existing resources;

15

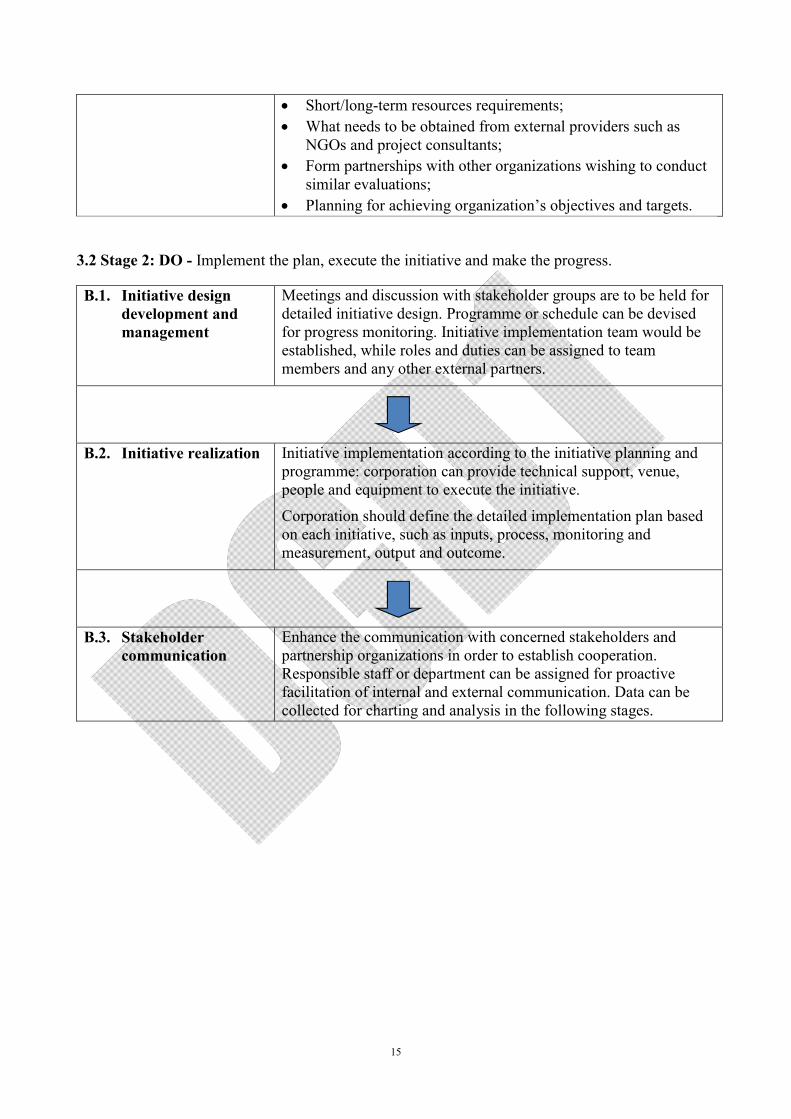

Short/long-term resources requirements;

What needs to be obtained from external providers such as NGOs and project consultants;

Form partnerships with other organizations wishing to conduct similar evaluations;

Planning for achieving organization’s objectives and targets.

3.2 Stage 2: DO - Implement the plan, execute the initiative and make the progress.

B.1. Initiative design development and management

Meetings and discussion with stakeholder groups are to be held for detailed initiative design. Programme or schedule can be devised for progress monitoring. Initiative implementation team would be established, while roles and duties can be assigned to team members and any other external partners.

B.2. Initiative realization Initiative implementation according to the initiative planning and programme: corporation can provide technical support, venue, people and equipment to execute the initiative.

Corporation should define the detailed implementation plan based on each initiative, such as inputs, process, monitoring and measurement, output and outcome.

B.3. Stakeholder communication

Enhance the communication with concerned stakeholders and partnership organizations in order to establish cooperation. Responsible staff or department can be assigned for proactive facilitation of internal and external communication. Data can be collected for charting and analysis in the following stages.

16

3.3 Stage 3: CHECK – Study the actual initiative results and compare against the expected results to ascertain any differences.

C.1. Monitoring and measurement

Initiative progress and outcomes should be monitored and measured for further evaluation. CSC evaluation tools (before-and-after evaluation) such as surveys, questionnaires, interviews, focus groups, etc. can be used.

Before-and-after survey is one of the commonly applied tools for evaluation. Depending on the resources allocation, interim evaluation can also be conducted in order to obtain the full programme progress and achievement along with the implementation.

The data collected can be presented with charts in order to oversee the trends of implementation cycles and convert the data into project information and experience. If deviation is identified in implementation from the plan, fine-tuning of project activity or the appropriateness and completeness of the plan would enable the project execution to be adjusted to the right track for desired outcomes.

C.2. Conducting the evaluation

The evaluation targets can be focused on participants and/or their families, staff, volunteers, and other stakeholders.

Corporations can conduct the actual evaluation with the efforts of stakeholders and partnership organizations in order to get closer cohesion and trust with the targeted stakeholders.

3.4 Stage 4: ACT – Improvement or adjustment can be induced from the initiative evaluation in order to establish a new standard (baseline) for potential future enactment.

D.1. Analysis of results Conclusions can be drawn from the analysis of data collected in order to compare with the corporation’s measurable CSC objectives and targets.

D.2. CSC and initiative review meeting

The development of corporate level CSC and project level CSC activities can be regularly reviewed in order to determine the effectiveness of CSC development. Meetings can be conducted with stakeholder groups, service organizations, NGOs, service clients, social workers and expertise, etc. in order to evaluate:

delivery of activities;

responses and feedbacks from stakeholders and/or service

17

clients;

performance and effectiveness of the CSC initiatives/projects;

performance of external providers;

need for instant improvements to the project execution;

routine communication channels, etc. Corrective actions can be executed for initiative implementation or potential future enactment.

18

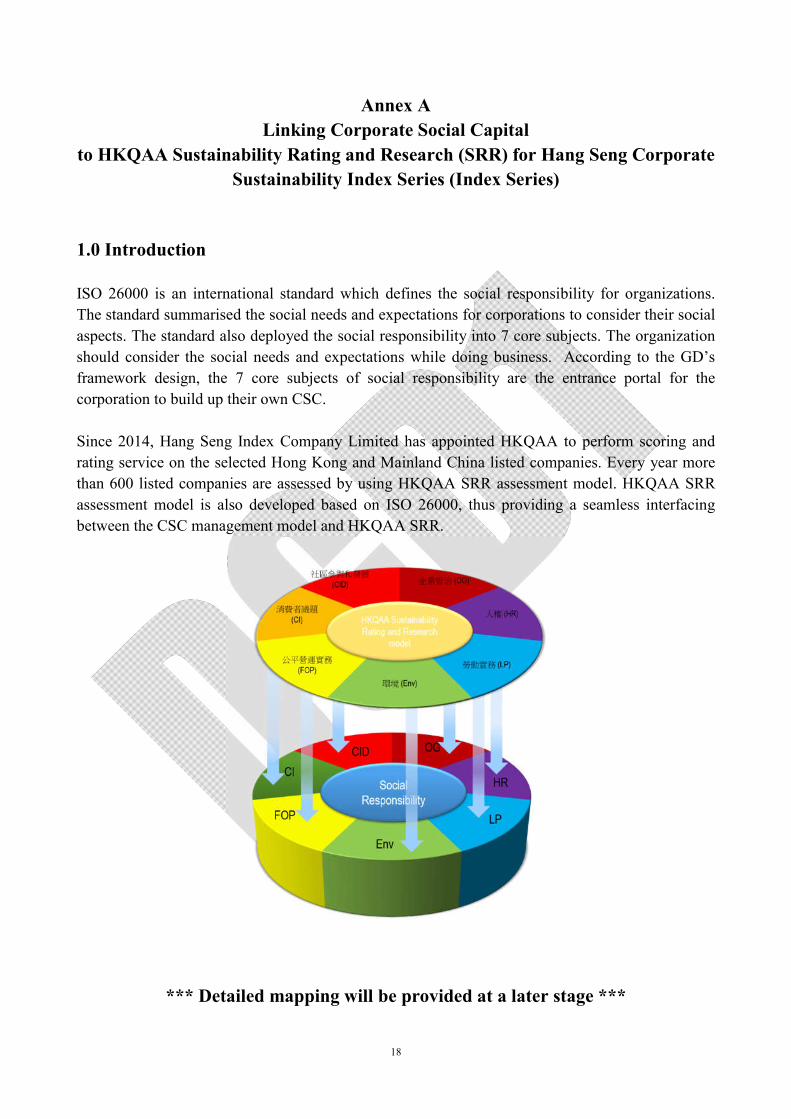

Annex A

Linking Corporate Social Capital

to HKQAA Sustainability Rating and Research (SRR) for Hang Seng Corporate

Sustainability Index Series (Index Series)

1.0 Introduction

ISO 26000 is an international standard which defines the social responsibility for organizations.

The standard summarised the social needs and expectations for corporations to consider their social

aspects. The standard also deployed the social responsibility into 7 core subjects. The organization

should consider the social needs and expectations while doing business. According to the GD’s

framework design, the 7 core subjects of social responsibility are the entrance portal for the

corporation to build up their own CSC.

Since 2014, Hang Seng Index Company Limited has appointed HKQAA to perform scoring and

rating service on the selected Hong Kong and Mainland China listed companies. Every year more

than 600 listed companies are assessed by using HKQAA SRR assessment model. HKQAA SRR

assessment model is also developed based on ISO 26000, thus providing a seamless interfacing

between the CSC management model and HKQAA SRR.

*** Detailed mapping will be provided at a later stage ***

19

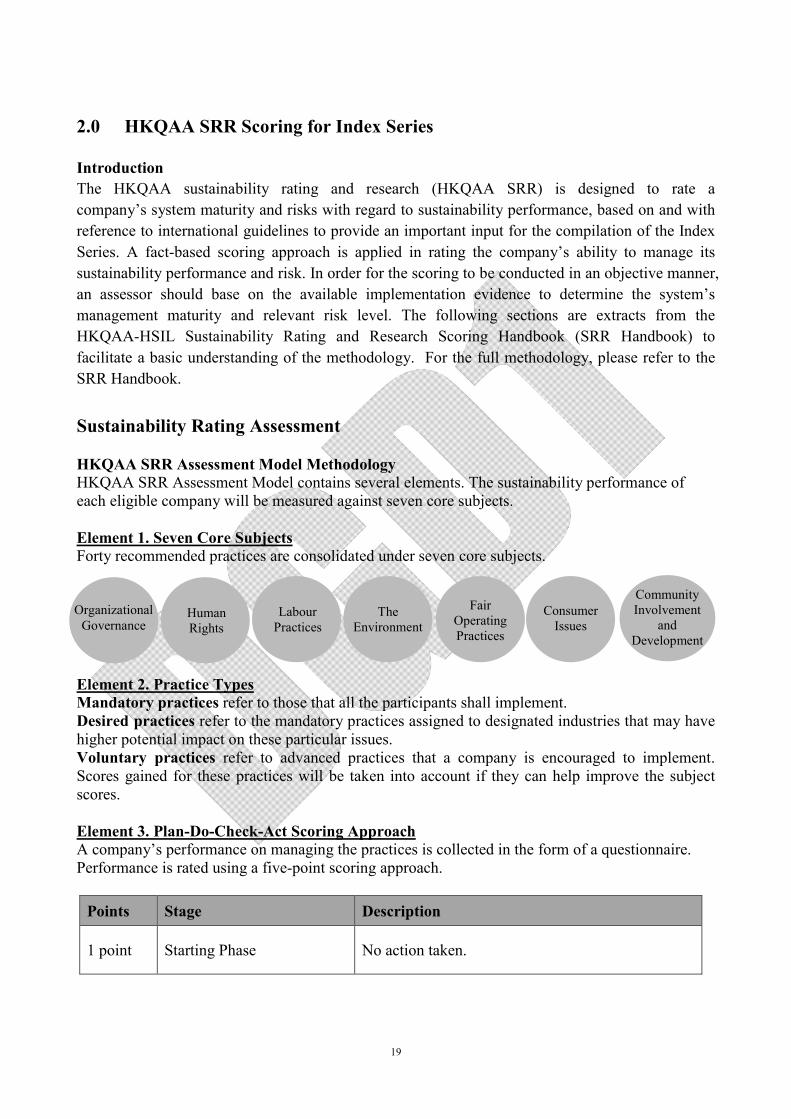

2.0 HKQAA SRR Scoring for Index Series

Introduction

The HKQAA sustainability rating and research (HKQAA SRR) is designed to rate a

company’s system maturity and risks with regard to sustainability performance, based on and with

reference to international guidelines to provide an important input for the compilation of the Index

Series. A fact-based scoring approach is applied in rating the company’s ability to manage its

sustainability performance and risk. In order for the scoring to be conducted in an objective manner,

an assessor should base on the available implementation evidence to determine the system’s

management maturity and relevant risk level. The following sections are extracts from the

HKQAA-HSIL Sustainability Rating and Research Scoring Handbook (SRR Handbook) to

facilitate a basic understanding of the methodology. For the full methodology, please refer to the

SRR Handbook.

Sustainability Rating Assessment HKQAA SRR Assessment Model Methodology HKQAA SRR Assessment Model contains several elements. The sustainability performance of each eligible company will be measured against seven core subjects. Element 1. Seven Core Subjects Forty recommended practices are consolidated under seven core subjects. Element 2. Practice Types Mandatory practices refer to those that all the participants shall implement. Desired practices refer to the mandatory practices assigned to designated industries that may have higher potential impact on these particular issues. Voluntary practices refer to advanced practices that a company is encouraged to implement. Scores gained for these practices will be taken into account if they can help improve the subject scores. Element 3. Plan-Do-Check-Act Scoring Approach A company’s performance on managing the practices is collected in the form of a questionnaire. Performance is rated using a five-point scoring approach.

Points Stage Description

1 point Starting Phase No action taken.

Organizational

Governance Human Rights

Labour Practices

The Environment

Fair Operating Practices

Consumer Issues

Community Involvement

and Development

20

2 points Forming Phase (Plan) Actions are under development/established without full implementation/implemented on an ad-hoc basis.

3 points Implementing Phase (Do) Actions have been fully implemented with advance planning to realise the recommended practice.

4 points Confirming Phase (Check)

Data collection and analysis on the actions are conducted to gather relevant information to evaluate the effectiveness of the implemented practice.

5 points Improving Phase (Act) There is a review of the implemented actions for identifying improvement areas.

21

Annex B HKQAA SRR seven core subjects and subsequent practices

Core Subject 1: Organizational Governance (OG) OG1 Organization should set its direction by making sustainability/social responsibility an

integral part of its policies, strategies and operations. OG2 Organization should establish programme or mechanism for raising awareness and

building competency for sustainability/social responsibility in the company (e.g., new staff training, on-going training, seminars, etc.).

OG3 Organization should be aware of applicable social responsibility laws and regulations, inform those within the company responsible for observing these laws and regulations and see that they are observed (e.g., initial and regular review, applicability evaluation, control and monitoring mechanism, internal and/or external compliance audit, report verification, etc.).

OG4 Organization should disclose how the highest governance body is established and structured in support of the organization’s purpose, and how this purpose related to economic, environmental and social aspects are evaluated and managed.

OG5 Organization should establish sustainability risk and crisis management mechanism or means.

OG6 Organization should establish a two-way communication process between the organization and its stakeholders so as to identify areas of agreement and disagreement and resolve possible conflicts.

Core Subject 2: Human Rights (HR) HR1 Organization should establish a programme or means to resolve grievances. HR2 Organization should ensure that it does not discriminate against employees, partners,

customers, stakeholders, members and anyone else with whom the organization has any contact or on whom it can have any impact.

HR3 Organization should ensure the fundamental principles and rights at work. HR4 Organization should ensure every person, as a member of society, has economic, social

and cultural rights necessary for his or her dignity and personal development (For companies involved in utilities sector with industry code: 40 Utilities).

HR5 Organization should establish a programme or means to face challenges and dilemmas relating to human rights and in which the risk of human rights abuse may be exacerbated.

HR6 Organization should respect all individual civil and political rights. HR7 Organization should respect human rights and have a responsibility to exercise due

diligence to identify, prevent and address actual or potential human rights impacts resulting from their activities or the activities of those with which they have relationships.

HR8 Organization should ensure avoidance of complicity. Core Subject 3: Labour Practices (LP) LP1 Organization should encourage lawful and proper employment that signifies human

development and contribute to the improvement of standards of living through full and secure employment and decent work.

LP2 Organization should ensure decent conditions of work and provide social protection.

LP3 Organization should ensure health and safety at work. LP4 Organization should encourage human development and training in the workplace. LP5 Organization should encourage social dialogue.

22

Core Subject 4: The Environment (Env) Env1 Organization should implement measures or means to prevent pollution and minimize

waste. Env2 Organization should promote the sustainable use of resources. Env3 Organization should implement measures to adapt to climate change and mitigate its

impacts. Env4 Organization should be socially responsible by acting to protect the environment and

restore natural habitats and the various functions and services that ecosystems provide. Core Subject 5: Fair Operating Practices (FOP) FOP1 Organization should develop and implement mechanisms or means to prevent

corruption. FOP2 Organization should promote social responsibility in the value chain. FOP3 Organization should develop and implement programmes or means to protect property

rights. FOP4 Organization should prevent engaging in anti-competitive behaviour. Core Subject 6: Consumer Issues (CI) CI1 Organization should ensure that no unfair marketing or misleading information about

products and services is delivered to consumers. CI2 Organization should reduce and eliminate unsustainable patterns of production and

consumption. Organization’s role in sustainable consumption arises from the products and services it offers, their life cycles and value chains, and the nature of the information it provides to consumers.

CI3 Organization should develop and implement systems on delivery of consumer service and support, complaints handling, and dispute resolution.

CI4 Organization should implement measures to protect consumer data and privacy. CI5 Organization should educate consumers to make knowledgeable purchasing decisions

and consume responsibly. Skills should be developed for consumers to assess products and services and for making comparisons.

CI6 Organization should ensure that its products and services will not be inherently harmful to consumers’ health and safety.

CI7 Organization should contribute to the right of the community to satisfy basic needs. Core Subject 7: Community Involvement and Development (CID) CID1 Organization should proactively outreach the community. It is aimed at preventing and

solving problems, fostering partnerships with local organizations and stakeholders and aspiring to be a good organizational citizen of the community.

CID2 Organization should preserve and promote the culture and promote the education compatible with respect for human rights.

CID3 Organization should create employment in the community, and develop their skills for employment promotion and securing decent and productive jobs.

CID4 Organization should create wealth and income, and promote a balanced distribution of the economic benefits among community members. It should invest their resources in initiatives and programmes aimed at improving social aspects of community life.

CID5 Organization should contribute to the promotion of public health, prevention of health threats and diseases, and mitigation of any damage to the community.

CID6 Organization should promote technology development and access.

Annex C

*Implementation Templates for CSC projects to be supplemented

in DGD2 after completion of the pilot-run projects.

24

Annex D

Case Studies

Core Subject 1: Organizational Governance (OG) Core Subject 2: Human Rights (HR)

Core Subject 3: Labour Practices (LP)

Core Subject 4: The Environment (Env)

Core Subject 5: Fair Operating Practices (FOP)

Core Subject 6: Consumer Issues (CI)

Core Subject 7: Community Involvement and Development (CID)

*** To be provided in DGD2 after completion of the pilot-run projects ***

25

4 Bibliography

CIIF Consortium (2004-2006). An Evaluation Study on the Impacts of CIIF Intergenerational Programmes on the Development of Social Capital in Hong Kong. Hong Kong: CIIF Consortium. Asia-Pacific Institute of Aging Studies (APIAS), Lingnan University. Retrieved from http://www.ciif.gov.hk/download/tc/resources-centre/ciif-evaluation-study/ln_full.pdf

CIIF Evaluation Consortium (2005). An Evaluation Study on the Effectiveness of Implementation of

Community Investment and Inclusion Fund (CIIF). Quality Evaluation Centre and Department of Applied Social Studies, the City of University. Retrieved from http://www.ciif.gov.hk/download/tc/resources-centre/ciif-evaluation-study/cityuqec_full.pdf

CIIF Research Team (2006). Building Social Capital: A Formative Program Review of CIIF Projects. Department of Social Work & Social & Administration, The University of Hong Kong. Retrieved from http://www.ciif.gov.hk/download/en/resources-centre/ciif-evaluation-study/hku_full.pdf

Fombrun, C., Gardberg, N. and Sever, J. (2000). The reputation quotient: A multi-stakeholder

measure of corporate reputation. Journal of Brand Management, 7(4): 241–256. Fukuyama, F. (1995). Trust. New York: Free Press. Knack, S., & Keefer, P. (1997). Does Social Capital Have an Economic Payoff? A Cross-country

Investigation. Quarterly Journal of Economics, 112, 1252–88. Gabbay, S. M., & Leenders, R. T. A. (2001). Social capital of organizations: From social structure

to the management of corporate social capital. In Social capital of organizations (pp. 1-20). Emerald Group Publishing Limited.

Gittell, R., & Vidal, A. (1998). Community organizing: Building Social Capital as a Development

Strategy. Thousand Oaks, CA: Sage Books. Global Reporting Initiative, GRI (2016). Consolidated set of GRI Sustainability Reporting Standards. Global Reporting Initiative, GRI (2000). Sustainability Reporting Guidelines on Economic,

Environmental, and Social Performance. GRI: Boston. Grootaert, C., Narayan, D., Nyhan Jones, V., & Woolcock, M. (2004). Measuring Social Capital,

An Integrated Questionnaire. World Bank Working Paper No. 18. Washington, D.C.: World Bank. https://openknowledge.worldbank.org/handle/10986/15033 License: CC BY 3.0 IGO

Grootaert, C., & van Bastelaer, T. (2001). Understanding and Measuring Social Capital: A

Synthesis and Findings from the Social Capital Initiative. Social Capital Initiative Working Paper 24. Washington, D.C.: World Bank, Social Development Department.

Guiso, L., Sapienza, P., & Zingales, L. (2008). Social Capital as Good Culture. Journal of

the European Economic Association, 6, 295–320.

26

Hong Kong Quality Assurance Agency. (2016). HKQAA-HSIL Sustainability Rating and Research Scoring Handbook. Revision 2.1. Hong Kong: Author.

International Organization for Standardization. (2015a). Quality management systems —Requirements. (ISO 9001:2015). Retrieved from https://www.iso.org/obp/ui/#iso:std:iso:9001:ed-5:v1:en International Organization for Standardization. (2015b). Environmental management systems — Requirements with guidance for use. (ISO 14001:2015). Retrieved from https://www.iso.org/obp/ui/#iso:std:iso:14001:ed-3:v1:en International Organization for Standardization. (2011). Energy management systems —

Requirements with guidance for use. (ISO 50001:2011). Retrieved from

https://www.iso.org/standard/51297.html

International Organization for Standardization. (2010). Guidance on social responsibility. (ISO

26000:2010). Retrieved from https://www.iso.org/obp/ui/#iso:std:iso:26000:ed-1:v1:en

Johnson, D., Headey, B., & Jensen, B. (2005). Communities, Social Capital and public policy: literature review. The Melbourne Institute of Applied Economic and Social Research, Policy Research Paper No. 26.

Legatum Institute Foundation. (2017). The Legatum Prosperity IndexTM 2017, Eleventh Edition.

London, UK: Legatum Institute. Moen, Ronald & Norman, Clifford. (2009) Evolution of the PDCA cycle. Paper delivered to the

Asian Network for Quality Conference in Tokyo on September 17, 2009. Nahapiet, J., & Ghoshal, S. (1998). Social Capital, intellectual capital and the

organizational advantage. Academy of Management Review, 23 (2), 242-266.

Network for Business Sustainability South Africa. (2014). Measuring and Valuing Social Capital: A guide for executives. Network for Business Sustainability South Africa. Retrieved from www.nbs.net/knowledge

OECD. (2001). The well-being of nations: The role of human and social capital. Paris: Author. Oswald, J. (1996) Human resources, scientists, and internal reputation: The role of climate and job

satisfaction. Human Relations, 49(3): 269–293. Putman, R. D. (2000). Bowling alone: The collapse and revival of American community. New York:

Touchstone. Saeed, M. M., & Arshad, F. (2012). Corporate social responsibility as a source of competitive

advantage: The mediating role of Social Capital and reputational capital. Journal of Database Marketing & Customer Strategy Management, 19(4), 219-232.

Servaes, H., & Tamayo, A. (2017). The Role of Social Capital in Corporations: A Review. Oxford

Review of Economic Policy, Forthcoming. Retrieved from https://ssrn.com/abstract=2933393

27

Siegler, V. (2014). Measuring Social Capital. Office for National Statistics. Retrieved from http://webarchive.nationalarchives.gov.uk/20160107115718/http://www.ons.gov.uk/ons/dcp171766_371693.pdf

Social Accountability International. (2014). Social Accountability 8000 (SA8000: 2014). Retrieved

from http://www.sa-intl.org/_data/global/files/SA8000Standard2014(3).pdf Ting, W. F. (2012). Final report on the effectiveness of CIIF projects in Social Capital

development in Tin Shui Wai. Hong Kong: Department of Applied Social Sciences, Hong Kong Polytechnic University.

Ting, W. F. (2006). Final report for evaluating the outcomes and impact of the Community

Investment and Inclusion Fund (CIIF). Hong Kong: Department of Applied Social Sciences, Hong Kong Polytechnic University.

United Nations (2015). Sustainable Development Goals. UN Sustainable Development Summit.

World Bank (2000), World Development report 2000/2001: Attacking poverty. Oxford: Oxford University Press.

World Business Council for Sustainable Development. (2017). Social Capital Protocol, Making

companies that truly value people more successful. Retrieved from http://social-capital.org/download-social-capital-protocol

28

5 Acknowledgements HKQAA would like to extend sincere thanks to the experts and companies who contributed their insight, experience and expertise on this Guidance Document development, including:

The Stakeholders Group Members:

• Mr. Daniel Wong • Ms. Dorothy Chan • Mr. Jimmy Chiu • Prof. Joe Leung, M.H., JP • Dr. Kee Chi-hing, JP • Ms. Lilian Law, JP • Mrs. May Lam-Kobayashi • Ms. Maria Cheung • Ms. Mimi Yeung • Ms. Yan Chan

Pilot Project Collaborators (Participating companies):

• Alliance Construction Materials Ltd. • Hong Kong Airlines Limited • Hong Kong Broadband Network Limited • Hysan Development Company Limited • MTR Corporation Limited • New World Development Company Limited

*Individuals and collaborators are listed in alphabetical order. We would also like to warmly acknowledge the support of the CIIF Secretariat in the development of this document.