corporate equity ownership and the governance of product...

TRANSCRIPT

Corporate Equity Ownership and the Governance of Product Market Relationships*

C. Edward Fee

Michigan State University [email protected]

Charles J. Hadlock

University of Virginia [email protected]

Shawn Thomas

University of Pittsburgh [email protected]

*We thank Wei-Lin Liu and seminar participants at the University of Virginia and Washington University for helpful comments. Hoon-Taek Seo provided superb research assistance. All errors remain our own.

Corporate Equity Ownership and the Governance of Product Market Relationships

ABSTRACT We assemble a sample of over 10,000 customer-supplier relationships and determine whether the customer owns equity in the supplier. We find that factors related to both contractual incompleteness and financial market frictions are important in the decision of a customer firm to take an equity stake in a supplier. Evidence on the size of equity stakes suggests that there may be limits to equity ownership in some contexts. Finally, even after controlling for a number of other factors, we find that relationships accompanied by equity ownership last significantly longer than other relationships, suggesting that ownership aids in bonding trading parties together. Keywords: Contracting, Ownership, Vertical Integration JEL classifications: G32, L22, D23

1

I. Introduction

Firms face a menu of choices in obtaining inputs from their suppliers. At one extreme,

firms can simply purchase inputs in spot market transactions. At the other extreme, customers

and suppliers can vertically integrate. Intermediate possibilities include signing detailed long-

term contracts or forming partially integrated structures where one firm takes an equity stake in

the other. While previous research has devoted much attention to understanding both vertical

integration and long-term contracting, there is comparatively little evidence on the role of partial

equity stakes as a mechanism to aid in the governance of product market relationships.

In this paper, we study the decision to take an equity stake in a trading partner with a

unique sample of over 10,000 customer-supplier pairs from 1988-2001. We examine whether

variables that proxy for the theorized benefits of equity ownership are systematically related to

the presence or size of observed equity stakes. In addition, we investigate whether the presence

of an ownership position is related to the subsequent evolution of the trading relationship.

Our analysis reveals several interesting findings. First, we find that intense trading

relationships where a firm sells a significant fraction of its output to a single customer are quite

common. Second, we find that it is relatively rare for a customer to take an equity stake in their

supplier.1 Specifically, equity stakes are present in only 3.31% of all sample relationships,

although this frequency is higher in some subsamples. The low overall incidence of equity

ownership suggests that many trading relationships can be governed effectively by explicit or

implicit contracts, with no need for equity participation. There are still, however, a large number

of relationships where this is apparently not the case: these cases, where customers do take

equity stakes in their suppliers, provide us the opportunity to investigate the types of frictions

1 Suppliers in our sample are much smaller than customers. Thus, equity blocks by suppliers in their major customers are virtually non-existent.

2

that arise in customer-supplier relationships and also allow us to study the role of equity in

easing these frictions.

Our results suggest that factors related to contractual incompleteness, relationship-

specific investment, and financial market frictions contribute to the decision for a customer to

obtain an equity stake in its supplier. In particular, the likelihood of observing an equity stake is

related to whether the supplier is a research and development (R&D) intensive firm. Since we

expect relationships involving R&D activities to be particularly prone to contractual frictions

arising from poorly delineated property rights, this finding appears consistent with an incomplete

contracts motivation for the use of equity. The presence of an equity stake is also significantly

related to the fraction of a supplier's sales that are made to the customer. This suggests that

equity ownership may encourage efficient actions in settings where firms are concerned with

expropriation and hold-up problems arising from relationship-specific investments.

We also find that equity stakes are significantly more common in relationships with

formal alliance agreements. This indicates that explicit contracts and equity ownership are often

complements rather than substitutes in governing potential conflicts between trading parties.

Since relationships with explicit alliances are more likely to include substantial relationship-

specific investments and/or scope for incentive conflicts, our findings on alliances suggest that

equity ownership helps ease inefficiencies arising from incomplete contracting in these settings.

Turning to financial market frictions as a potential motivation for equity stakes, we find

that suppliers who are cash constrained (i.e., have negative free cash flow) are more likely to

have customers as blockholders than firms who are not cash constrained. This suggests that part

of the equity stake phenomenon reflects behavior in which customers serve as informed sources

of capital to ease financial constraints at the supplier level. Customer financial constraints also

3

appear important, as we find some evidence that customers with deeper pockets are more likely

to invest in their suppliers.

When we examine the variation in the size of observed equity blocks, we find that

variables that have a positive effect on the likelihood of observing the presence of a block often

have an insignificant or negative effect on the size of the blocks. This suggests that there are

limits to equity ownership, perhaps because suppliers are concerned about customers having too

much control over their operations at high ownership levels. Thus, in settings where incentives

must be delicately managed, notably relationships entailing high levels of R&D, a large fraction

of supplier sales to the customer, or explicit alliance agreements, it appears that an equity stake is

relatively more likely to be established, but that the size of the stake will be moderate.

Finally, we find that relationships accompanied by equity ownership last significantly

longer than other relationships. However, outright mergers between customers and suppliers are

rare, even when customers own equity in their suppliers. These findings suggest that ownership

may affect relationship governance and help bond trading parties. This evidence fits nicely with

our findings on the decisions to take equity stakes, which presumably are made in anticipation of

the potential future benefits.

The rest of the paper is organized as follows. In Section 2, we review the existing

theoretical and empirical literature concerning the governance of product market relationships

and the possible role for equity ownership. We use this discussion to motivate our empirical

strategy, which we outline at the end of Section 2. In Section 3, we discuss our data, sample

selection, and summary statistics. In Section 4, we present our main multivariate results on the

factors associated with equity stakes in product market relationships. In Section 5, we report our

findings on the duration of relationships. We conclude in Section 6.

4

2. Related Literature and Empirical Strategy

2.1 Theoretical Considerations

The vertical integration decision is a classic issue in the theory of the firm. Pioneering

work in transactions cost economics by Williamson (1975, 1985) and Klein, Crawford, and

Alchian (1978) emphasizes the role of asset specificity and relationship-specific investments in

the integration decision. Related work on incomplete contracts by Grossman and Hart (1986)

and Hart and Moore (1990) demonstrates how integration can change investment incentives by

changing property rights and the division of jointly created surplus. If we view a customer

taking an equity stake in its supplier as a form of partial vertical integration, we might expect that

the factors that the theory suggests will affect the vertical integration decision will also affect the

likelihood of partial integration. Thus, we might expect relationships characterized by a high

degree of asset specificity and/or the presence of important non-contractible decisions to be more

likely to exhibit equity stakes.2

This view of partial integration, while informative, may overlook some of the subtleties

that arise in this hybrid ownership structure. An alternative view of partial ownership is that it

provides the blockholder with an incentive to partially internalize the effects of its actions on its

trading partner. Thus, in cases when one party may underinvest in actions that help the other

party, a partial equity stake may be beneficial in improving total surplus.3 The size of such

stakes will be limited if high ownership by a blockholder begins to dilute the target's incentives.

2 Holmstrom and Roberts (1998) and Whinston (2003) note that the transactions cost approach and the property rights approach to integration are distinct and have different empirical implications. We do not formally test these theories, but rather use them as general motivation for the role of incomplete contracting in partial equity ownership. 3 The general idea that equity stakes help internalize the effect of one parties actions on a partner is used by, among others, Riordan (1990, 1991) and Mathews (2003).

5

This view of partial equity ownership as a solution, albeit imperfect, to a double moral hazard

problem, would suggest that equity stakes are more likely to be observed in relationships where

actions by one party have a significant positive spillover effect on their partner.

While partial equity ownership may at times alleviate incentive problems, Aghion and

Tirole (1994) show that it is possible for partial equity ownership to be irrelevant in relationships

when parties bargain ex post over any trading surplus. In their analysis, the price that product

market partners agree on in bargaining will adjust to reflect any equity stake in a way that leaves

both partners with the same surplus that they would realize without the ownership position.

However, recent papers by Dasgupta and Tao (2000), Harbaugh (2001), and Van den Steen

(2002) show that when one generalizes the Aghion and Tirole (1994) framework, there can be a

role for partial equity stakes to increase relationship efficiency by changing the threat points in

the bargaining game over joint surplus. For example, Dasgupta and Tao (2000) show that if a

customer has a stake in a supplier, the supplier will tilt its choices towards relationship-specific

investments and away from general investments, because part of the return from the general

investment will accrue to the customer via its equity position.

These models of partial equity ownership are quite specialized. Thus, it is hard to

interpret them as literal descriptions of typical multi-dimensional, long-lived product market

relationships. Nevertheless, this work suggests that equity may play a role in enhancing

efficiency in environments where contracting is incomplete. In addition, it seems possible that

equity stakes may serve a role in encouraging information sharing or cooperation between

trading parties over time in ways not captured by existing models. In our empirical analysis we

hope to both confirm some general possibilities suggested by existing theory and to inform

further work in this area.

6

2.2 Related Empirical Evidence

Following the work of Pisano (1989), several studies have examined equity stakes in

product market relationships.4 Motivated primarily by transactions cost economics, these papers

identify several factors that are related to equity participation and are plausibly related to

contracting problems and expropriation risks. A common result in several of these studies is that

R&D intensive relationships are more likely to include an equity tie between partners.

While these prior studies are informative, they do not provide a comprehensive picture of

equity holdings in a broad cross-section of publicly traded firms. Many of these studies focus on

specific industries (e.g., biotechnology), and almost all restrict attention to a special type of

product market relationship (e.g., strategic alliances or technology transfer agreements). In

addition, many of the firms studied are private and/or foreign. Given these sampling procedures,

which are usually dictated by data availability, it is not surprising that the existing literature

reports substantially higher rates of equity participation in relationships than we find, with a rate

of over 50% reported by Gulati (1995).

A recent working paper by Pablo and Subramaniam (2002) shares similar goals to our

study. These authors examine whether the presence of equity stakes in a sample of 759 product

market alliances can be predicted by variables related to contractual frictions and/or financial

constraints, and they find some evidence in the affirmative. Our sample is much larger, as

product market alliances comprise only a small fraction of intense trading relationships. Thus,

we are able to test whether relationships governed by alliance agreements are different than other

trading relationships, and it turns out they are. In addition, given the richness of our data, we are

4 A partial list of studies includes Gulati (1995), Gulati and Singh (1998), Oxley (1997, 1999), Robinson and Stuart (2001), and Pablo and Subramaniam (2002).

7

able to examine how the intensity of a trading relationship affects ownership stakes. Moreover,

we can exploit the unique panel nature of our data to examine relationship duration. Where our

analysis overlaps with Pablo and Subramaniam (2002), the results are similar in nature,

suggesting that the two studies are uncovering similar economic phenomena.

Our investigation is also related to the work of Allen and Phillips (2000). In a sample of

block purchases, they find that blocks established in connection with product market alliances

exhibit the most positive announcement returns and subsequent changes in operating

performance. These results certainly suggest that there is something special about equity

ownership coupled with a product market relationship. However, because Allen and Phillips

(2000) select their sample based on the purchase of an equity block, their study is unable to

contrast relationships accompanied by equity stakes with relationships not accompanied by such

stakes. As we show, close trading relationships without equity ownership are quite common.

The broader literature on large blockholders (e.g., Holderness and Sheehan (1988, 2000))

is also related to our analysis. This literature establishes that corporations do at times hold large

blocks in other firms, suggesting that this can be a viable organizational form. However, this

literature is silent on identifying when this organizational form is preferred to others, and it does

not identify any special role for equity in the context of product market relationships. Of related

interest is also the literature on corporate venture capital, although the focus there is on private

firms rather than public firms. Gompers and Lerner (2000) and Santhanakrishnan (2003) report

that equity ties in a venture capital setting are more successful when the investor and the venture

have some strategic overlap or an alliance. Similar to Allen and Phillips (2000), this suggests

that equity stakes coupled with product market relationships may ease contractual frictions or

financing constraints.

8

2.3 Empirical Strategy

Our approach is to identify several variables that theory suggests may be related to equity

stakes and then to examine whether these variables systematically predict the presence of a stake.

Our preceding discussion establishes that there may be several scenarios under which equity

plays a role in easing incentive conflicts and contracting frictions between trading parties in a

world where contracts are incomplete. We refer to this general role for partial equity stakes as

the contracting hypothesis.

One variable that we expect will be related to contracting problems is the R&D focus of

the relationship. As has been well recognized (e.g., Aghion and Tirole (1994)), property rights

are often quite blurry when it comes to R&D activities. In addition, when firms are sharing

knowledge, there may be significant potential for the activities of one party to indirectly benefit

the other party in ways outside the scope of any contractual agreement. If equity stakes alleviate

these frictions, then they should be more prevalent in R&D oriented relationships. Other studies

have found a relation between R&D and equity in certain special samples, and thus this variable

is not unique to our study. However, our study is unique in looking at the relation between R&D

and equity stakes in a broad set of relationships between publicly traded firms.

The second contracting factor we study is the fraction of a firm's sales that are made to

their product market partner. The idea here is that the more a supplier sells to a given customer,

the more likely the supplier is making a substantial relationship-specific investment, and,

consequently, the greater will be concerns about expropriation. If equity stakes serve to ease

concerns about expropriation or holdup, we would expect to observe greater equity stakes when

this sales dependence variable is elevated.

9

The final factor we identify to test the contracting hypothesis is a variable indicating

whether the two firms in a relationship have an explicit alliance agreement. Many prior studies

of corporate equity ownership either restrict attention to alliances (e.g., Pablo and Subramaniam

(2002)), or use the existence of an alliance to identify a product market relationship (e.g., Allen

and Phillips (2000)). As we show below, it is quite common for firms to have close product

market relationships without an alliance agreement. The existence of a formal alliance

agreement suggests that trading partners are concerned about conflicts that may evolve over time

and that they attempt to ameliorate these conflicts using a contractual mechanism. If these

contractual agreements only imperfectly alleviate the problems, we would expect to observe the

presence of an equity stake as an additional governance device. Additionally, the formal alliance

can itself be viewed as a form of relationship-specific investment. As such, the contracting

hypothesis might predict a greater need for equity in alliances compared to relationships with

less mutual investment.

Equity investments by product market partners may also arise because of financial market

imperfections.5 In particular, firms may have a difficult time securing external financing at

reasonable terms in arm's length transactions because of information problems (e.g., Myers and

Majluf (1984)). If a product market partner, by virtue of their relationship with the firm, has the

ability to more accurately assess a firm's value, they may be in a superior position to provide

financing.6 We will refer to this possibility as the financial frictions hypothesis.

5 With the exception of Allen and Phillips (2000) and Pablo and Subramaniam (2002), prior studies of partial equity stakes largely ignore financial frictions as a motivation for these ownership positions. 6 Our argument here parallels similar arguments for choosing to issue private securities over public securities (e.g., Wruck (1989) and Hadlock and James (2002)). See Lerner, Shane, and Tsai (2003) for evidence on equity market conditions and partner financing.

10

To test this hypothesis, we consider two types of factors that may proxy for heightened

problems in accessing arm's length equity markets. First, we consider a firm's need for external

funding, since financing problems can be avoided if a firm has sufficient internal funding. We

measure external capital needs as the difference between a firm's capital spending and its internal

cash flow. Second, we consider variables that may proxy for the severity of information

problems when firms decide to access the external capital markets. We expect that the relative

preference for partner financing should be elevated when these variables are elevated. We

identify these variables from the existing literature (described below).

While both the contracting hypothesis and the financial frictions hypothesis suggest that

partial equity ownership may be an optimal arrangement under some circumstances, contracting

theories also suggest that there can be limits to partial equity ownership stakes. In particular,

majority stakes can allow one firm to control the other, and large minority stakes can lead to the

possibility of seizing control in the future. Concerns about control may impair incentives,

suggesting that there are limits to the optimal size of partial equity blocks. Thus, in situations

where equity ownership has the potential to ease contracting frictions by delicately managing

incentives, we may expect to observe moderate sized equity stakes rather than large blocks. We

will directly examine this possibility in the data.

To add to our understanding of the role of ownership in relationships, it would be helpful

to evaluate whether the presence of a partial equity stake actually has an effect on how a

relationship evolves over time. This is a challenge, since many possible effects concern

variables we do not observe (pricing, investment, etc.). To address this issue indirectly, we

propose to examine relationship durability. If relationships with equity stakes tend to last longer,

this would suggest that equity aids in fostering cooperation and in increasing the surplus from

11

trade. Of course the existence of an equity stake is endogenous, so the direction of causality is

unclear. However, whatever the direction of causality, such a finding would appear broadly

consistent with the contracting hypothesis.

3. Data and Sample Selection

3.1 Identifying Customer-Supplier Relationships

We begin by selecting the set of all firms listed on the merged Center for Research in

Security Prices (CRSP) and Compustat database with non-missing values reported for book

value of assets and fiscal-year-end stock price. Since our ownership data is only available

starting in 1988, we restrict attention to the 1988-2001 period. Disclosure rules require that

firms report the identities of all customers responsible for over 10% of their annual sales, and

some firms voluntarily report the names of other major customers when sales are below this

threshold. We consider all disclosed customers to be major customers of the firm, although

much of our later analysis conditions on the magnitude of trade between the customer and the

supplier. The identity of the firm's customers and sales to these customers are extracted from the

Compustat industry segment files.

For each identified customer, we attempt to determine whether the customer is another

CRSP/Compustat listed firm. This is not a straightforward task, as customer names are often

abbreviated. Thus, following Fee and Thomas (2004), we use a computer algorithm to generate

a list of the four names listed in the CRSP historical name field that are most likely to be a match

to the customer's name. We then use visual inspection and information on the industry of the

supplier to determine if the customer is in fact one of these CRSP listed firms. For customer

names where we find no match on CRSP, we search the Directory of Corporate Affiliations to

12

determine if the customer is a subsidiary of a publicly traded firm. If it is, we assign the

customer the CRSP identifier of the parent corporation. We are deliberately conservative in our

matching of customer names to firm identifiers, and thus we are confident that customers are

matched to the appropriate financial information.

3.2 Firms in Customer-Supplier Relationships

We retain in our sample all relationship-years from 1988-2001 in which a supplier is

listed in the CRSP/Compustat merged database and is matched in the observation year with a

customer that we can confirm appears in the CRSP and Compustat databases at some point

during the sample period. The resulting sample includes 10,493 distinct relationships

representing 27,037 relationship-years.

In Panel A of Table I we report summary statistics where each relationship is treated as a

single observation. Firm characteristics are measured as of the first sample-period year that the

relationship is observed. For comparison purposes, we also report statistics for the entire

Compustat universe.7 Given the skewness in many of the variables, we focus our discussion here

on medians rather than means. As we report in Panel A, suppliers are typically much smaller

than their major customers, with a median ratio of supplier assets to customer assets of less than

0.01. However, the median supplier is nearly half the size of the median Compustat firm,

indicating that suppliers are not extraordinarily small firms in general. Suppliers are typically

much younger than their major customers (median age of 6.00 versus 30.00) and slightly

younger than the median Compustat firm. The median level of R&D intensity for suppliers is

7 All figures are inflation adjusted. The Compustat universe figures in Panel A are for 1993, the year near the middle of our sample period with the greatest number of new relationships. Our summary statistics comparisons are very similar if we treat the relationship-year as our basic unit of observation rather than the relationship.

13

slightly larger than it is for customers, and both groups of firms appear to have fairly similar

market-to-book ratios.8

To gauge the overall frequency of trading relationships, we report in Panel B of Table I

the fraction of firm-year observations in the entire CRSP/Compustat universe where a firm is

involved in an identified relationship. We find that in 16.78% (7.17%) of all firm-years a firm is

identified as a supplier (customer) in a trading relationship. Smaller firms are relatively more

likely to be identified as suppliers, while larger firms are more likely to be major customers. The

fact that a sizeable fraction of public firms are involved in intense trading relationships suggests

that understanding the dynamics of these relationships is a fruitful area for inquiry. If anything,

our figures here are likely to be understated, since the conservative procedures we follow are

likely to miss some customer-supplier matches.

To understand how relationships vary by industry, we also report in Panel B of Table I

the industries in the Compustat universe with the highest proportion of firms involved in

relationships using the Fama and French (1997) industry classification scheme. Firms in the

automobile and aerospace industries are represented both in the supplier list and the customer

list, indicating that large within-industry sales relationships are common in these sectors. Other

industries in this panel reflect natural vertical supply relationships. For example, the fact that the

apparel industry is on the supplier industry list and retailers are on the customer industry list is

consistent with the common dependence of apparel manufacturers on sales to large retailers.9

8 Firm age is the number of years since the firm was first listed on Compustat. R&D intensity is a firm's annual R&D expenditures divided by total assets, where missing values for R&D are treated as zero. The Market-to-book ratio (MB) is calculated as (total assets - book value of equity + market value of equity) / total assets. Both R&D intensity and MB are winsorized at the 1% and 99% level. 9 The firm in our sample that is a major customer to the highest number of suppliers is Wal-Mart. Interestingly, Wal-Mart never takes a 5% equity block in any of the 292 suppliers who identify Wal-Mart as a major customer.

14

Lastly, in panel C of Table I we report statistics on multiple relationships. Our figures

here indicate that this phenomenon is quite common. In particular, more than one third of the

sample supplier-years (customer-years) are cases where the firm is a supplier (customer) in

another relationship in that same year.

3.3 Ownership and Alliances

Most of the variables we use in our analysis are collected directly from the Compustat or

CRSP files. However, these data sources do not contain information on ownership or alliances.

To gather ownership information, we use the Compact Disclosure database. This data source

reports information on 5% blockholders collected directly from proxy statements and other

federal filings for virtually all publicly traded U.S. firms from 1988 onwards.10 For each

relationship, we use the Compact Disclosure disks to determine whether the customer is ever

listed as a 5% blockholder in the supplier. If it is, we record the size of the blockholding each

year and supplement this with information collected directly from the supplier firm's proxy

statements. Our rules for combining and coding the ownership data from Compact Disclosure

and proxy statements are detailed in the Appendix. Our final data set includes information on

whether the customer owned equity in the supplier and, if so, the size of the equity stake around

the end of each fiscal year. By adding the requirement that a supplier is listed on Compact

Disclosure, our final sample size falls slightly to 10,211 relationships.

To gather information on alliances, we select the first year that a relationship appears

during our sample period and search for whether the firms were listed together in the Securities

10 For more details on Compact Disclosure, see Anderson and Lee (1997). We use two disks a year from January 1988 to January 2003. Consistent with very broad coverage, we lose very few observations (less than 3%) when we add the restriction that the supplier must be listed in Compact Disclosure.

15

Data Corporation (SDC) strategic alliance database at any point in time from 1980 up to 365

days after the end of this fiscal year. The SDC database begins listing alliances in 1980, and the

comprehensiveness of their coverage appears to increase starting in 1985. Thus, we believe that

we should detect most instances in where relationships are accompanied by alliance agreements.

3.4 Characteristics of Customer-Supplier Relationships

We present basic information on sample relationships in Panel A of Table II. The mean

(median) value for the fraction of the supplier's sales made to their customer is 19.23%

(13.73%). As one would expect given our data collection procedures, this confirms that we have

selected relationships where the supplier sells a substantial fraction of their output to a single

customer. A fairly small fraction (5.09%) of sample relationships entail an alliance agreement,

indicating that intense trading relationships often exist without formal alliance-type contracts.

The figures in the table indicate that a majority of relationships involve firms in different

industries, even when industries are categorized at the coarse 1-digit or 2-digit SIC code level.

Finally, we report in Panel A of Table II evidence that there is substantial heterogeneity in the

estimated duration of trading relationships. Many relationships are quite short lived (25 percent

last only one year), but a fair number last for many years (25 percent last 6 years or more).11

In Panel B of Table II we report figures on equity ownership. We define a relationship to

have had an equity stake if the customer owned a block in the supplier at some point in the

relationship during the sample period. In almost all cases where there is an equity stake, the

11 Relationships first observed in 1978 (the first year customers are reported) are excluded from the duration calculation since the starting year for the relationship cannot be observed. Relationship duration is calculated by estimating the distribution of survival times using the Kaplan-Meier product limit estimator.

16

ownership position appears early on in the relationship.12 As we report in the table, equity

ownership by customers in their suppliers is the exception rather than the rule. In fact, in only

3.31% of our trading relationships do we observe the customer holding a 5% block of the

supplier's equity. Thus, while we have a sample of suppliers who are either moderately or highly

dependent on certain large customers, it appears that many of these relationships flourish without

the need for the customer to purchase equity in the supplier.

The overall sample rate of equity participation of 3.31% is significantly lower than what

is reported in prior studies. This suggests, not surprisingly, that the sampling procedures in these

studies result in samples where equity ties are relatively more important than for the typical

public firm. However, our overall rate of equity ownership is also much lower than recent

figures reported by Barclay, Holderness and Sheehan (2003) and Field and Sheehan (2003) for

block ownership rates in public corporations. To reconcile these findings and confirm the

validity of our data collection procedures, we selected 100 random suppliers in our sample in

1995 and inspected all available machine-readable proxy statements. Similar to Barclay,

Holderness, and Sheehan (2003), we find that just over 30% of these suppliers have blocks held

by other corporations (32.6%), with approximately half of these blocks held by non-financial

firms. However, the proxy statements confirm that we correctly identified each customer's status

as a blockholder in the selected supplier. This evidence indicates that while many firms have

blocks of stock held by other corporations, a relatively small number of these blocks are between

firms with significant trading relationships.

Turning to ownership rates for selected subsamples, we report in Panel B of Table II

some initial evidence consistent with the hypotheses outlined in our introductory sections.

12 In 93% of all relationships we observe an equity stake in the first or second year of the relationship. Our results are qualitatively unchanged when we restrict attention to equity stakes that exist early in the relationship.

17

Consistent with the contracting hypothesis, we find that suppliers with high R&D intensity (i.e.,

R&D intensity above the sample median) are significantly more likely to have equity stakes held

by customers compared to low R&D intensity suppliers. In addition, relationships where the

customer is responsible for a large (greater than median) fraction of the supplier's sales are also

characterized by a higher frequency of equity stakes. Finally, there is a significant difference

between relationships with an alliance agreement and relationships without such an agreement.

The magnitudes here are particularly large. We find that 19.23% of all relationships that are

accompanied by an alliance have an equity stake, compared to 2.46% for all other relationships.

Other interesting comparisons are also reported in panel B of Table II. We find that

younger suppliers are more likely to have an equity stake held by the customer, while firm size

does not appear to be related to the likelihood of a stake. If younger firms have greater

information problems, the difference across age groups could be interpreted as broadly consistent

with the financing frictions hypothesis. More convincing evidence is provided when we divide

the sample into suppliers that have negative and positive free cash flow, where free cash flow is

defined as operating earnings plus depreciation minus capital expenditures. Here we find that

customers with negative free cash flow are more likely to have customers with equity stakes.

3.5 The Establishment of Equity Stakes

Before turning to modeling the equity stake decision, it is informative to investigate how

these stakes are typically established. To determine this, we performed news searches in the

Factiva.com news sources (newspapers, newswires, magazines, etc.) The results of this analysis

are described in Table III. Approximately two-thirds of the observed equity stakes appear to be

related to either a formal or informal business arrangement, e.g., anticipated cooperation on

18

activity of mutual interest, establishment of supply contract, signing of a licensing agreement,

etc.13 Less common ways these stakes arise are through carve-outs of formerly wholly-owned

divisions, as consideration in asset sales between parties, and as pre-emptive purchases to

prevent third-party takeovers. The anecdotal evidence here suggests that equity stakes are not

typically merely coincidental to trading relationships, but serve a role in maintaining them. In

Section 5, below, we investigate the link between equity stakes and relationship maintenance in a

more quantitative fashion.

4. Models of Equity Stakes

4.1 Determinants of Equity Stakes in Customer-Supplier Relationships

The univariate statistics we discuss above are broadly consistent with the contracting and

financial frictions hypotheses. However, since many of the variables are correlated, a

multivariate analysis is called for. Our approach here is to estimate logit models where the

dependent variable takes a value of one if a relationship is characterized by an equity stake and

zero otherwise. All of the explanatory variables are measured as of the first year during the

sample period that we observe the relationship. To account for possible changes in ownership

patterns over time, all models include a year trend.

In column 1 of Table IV we report results for a simple specification that includes the

supplier's R&D intensity and the fraction of the supplier's sales to the customer (sales

dependence) as explanatory variables. We do not have explicit data on the nature of each trading

relationship, so we assume that suppliers with high levels of R&D are more likely to be involved

13 In the majority of these cases (76%), news articles indicate that the stake was established in direct connection with the signing of some type of explicit agreement. In the remaining cases we find more limited evidence that the ownership position is related to a business relationship or explicit contract.

19

in R&D focused trade with the customer. The estimates on the R&D variable and the sales

dependence variable in column 1 are both positive and highly significant. Since we expect

contracting frictions to be elevated in R&D focused relationships and in arrangements where the

supplier is dependent on the customer, these findings provide initial support for the contracting

motivation for the use of partial equity stakes.

In column 2 of Table IV, we add the strategic alliance dummy variable. As we report in

the table, the coefficient on this variable is positive and highly significant. This indicates that

extensive formal contracts (i.e., alliances) and partial equity ownership are complements rather

than substitutes. As was discussed earlier, this is consistent with equity ownership easing

contractual frictions in arrangements where firms make important relationship-specific

investments and/or where there is significant scope for incentive conflicts to arise over time.

Given the correlation between the variables, it is not surprising that inclusion of the alliance

variable lowers the estimated coefficients on the R&D variable and the sales dependence

variable. However, they remain positive and significant at the 1% level. Thus, while prior

studies typically restrict attention to firms with alliance agreements, our evidence suggests that

contracting frictions play a role in determining ownership structure even in relationships not

governed by such an agreement.

One may be concerned that our contracting frictions variables are correlated with other

characteristics, such as the supplier's size or age, that are not as clearly related to the theory. In

column 3 of Table IV, we add these variables to the specification. The coefficient on age is

negative and significant, indicating that younger firms are more likely to have equity stakes held

by their trading partners. Surprisingly, the coefficient on firm size is positive and significant.

This suggests that, holding all else equal, larger firms are more likely to have equity blocks held

20

by their product market partners.14 The coefficients on the variables related to contractual

frictions maintain their signs and significance levels with these added controls.

Turning to financial market frictions possibilities, we include in column 4 a dummy

variable that assumes a value of one when a firm has a cash flow that is insufficient to cover its

capital expenditures (negative free cash flow). These are firms who are likely to need external

funding and may turn to their partners for financing if other sources of capital are relatively

expensive. Consistent with this conjecture, the estimated coefficient on this variable in column 4

is in fact positive and significant. This finding lends substantial support to the financial-frictions

motivation for the presence of partial equity stakes.

To investigate the role of other variables that may represent capital market frictions, we

include variables related to the supplier's stock return volatility (a proxy for asymmetric

information), the supplier's leverage ratio (a proxy for financial constraints), and a dummy

variable indicating whether the supplier pays dividends (indicating a lack of financial

constraints). The estimates on the volatility measure and the dividend measure are small and

insignificant, while the estimate on the leverage ratio is significant and negative, opposite of the

expected sign. We are hesitant to infer much from the leverage coefficient, because leverage is

endogenous and borrowing may serve as a substitute for customer equity financing. Clearly

these additional variables add no additional support to the financial frictions hypothesis.

To summarize our evidence here, it appears that the existence of a financial deficit is

related to partner financing. However, further distinctions based on the severity of financial

constraints or information problems cannot be easily detected. We interpret this evidence as

14 We are hesitant to put too much weight on the size coefficient, as the univariate results in Table II reveal no significant difference in equity ownership between small and large firms. We experimented with using sales rather than assets as a measure of size (and as a normalizing variable), but this had no substantive effect on any of the coefficient estimates. Supplier size could proxy for mutual dependence between the supplier and the customer.

21

broadly consistent with the financial frictions hypothesis, with the caveat that the types of

frictions and the mechanism by which they lead to partner financing are quite murky.

To gauge the economic magnitude of our estimates, we select the specification in column

4 of Table IV as our baseline model and calculate the effect of changing the explanatory

variables on the implied probability of observing an equity stake. In these calculations, we vary

the explanatory variables, one at a time, from the 10th percentile level to the 90th percentile level

for scalar variables, and from zero to one for dummy variables. All other variables are held

constant at their sample mean. For the R&D variable, the estimated likelihood of observing an

equity stake increases from 1.8% to 2.9%. The corresponding figures for the sales dependence

variable are 1.6% and 3.0%. Relationships without alliances have a 1.9% estimated likelihood of

observing an equity stake, increasing to 8.2% when there is an alliance. These figures indicate

that the likelihood of observing an equity stake seems to rise sharply (in a relative sense) as our

measures of contracting frictions and the likelihood of relationship-specific investment increase.

The other estimates in specification 4 of Table IV also seem to have reasonably large

economic magnitudes. As firm age moves from the 10th percentile to the 90th percentile, the

estimated probability of observing an equity stake declines sharply from 3.9% to 0.6%. When

we turn to firm size, the figures are 1.1% and 4.6%. Finally, when suppliers move from positive

free cash flow to negative free cash flow status, the estimated likelihood of observing an equity

stake jumps from 1.6% up to 2.6%. This increase suggests that financial constraints play an

economically significant role in the decision to obtain partner financing.

4.2 Robustness and extensions

22

The results above support both the contracting and financial frictions motivations for the

use of partial equity ownership stakes in product market relationships. In this subsection we

experiment with some alternative empirical specifications in order to assess the robustness of

these findings and to further add to our understanding of the partial equity stake phenomenon.

We select specification 4 of Table IV as our baseline model and experiment with alterations to

this model.

One concern with the findings above is that they may be driven by a certain industry or a

small set of industries. For example, much of the related empirical literature focuses on the

pharmaceutical sector, and it is possible that what we are finding is being driven by that industry.

To investigate, we experiment with (a) dropping all pharmaceutical firms, and (b) including

industry dummy variables (using Fama and French (1997) industry definitions). These

alterations to our baseline model have no effect on the signs or significance levels of any of the

explanatory variables included in Table IV.

In some cases we first detect a relationship when the supplier initially appears on

Compustat, while other relationships appear later in a supplier's life. In the former case the

parties are likely to have had a significant level of trade before the supplier's initial public

offering (IPO), and one may suspect that equity ties are more common in these cases. To

investigate, we create an IPO dummy variable indicating whether a relationship exists in the first

year a supplier appears on Compustat. When we add this variable to our baseline model, the

estimate is small, positive, and insignificant, and the other estimates are qualitatively unchanged.

This suggests that there is nothing unique about equity ties that are established before the IPO.

We also experiment with excluding all relationships that existed in our first sample year, 1988,

23

as our variables for these relationships typically are measured at a later stage in the relationship's

existence. This exclusion has no substantive effect on any of our coefficient estimates.

As an extension to our analysis, we also consider the role of customer characteristics.

Our approach here is to replace the age, size, R&D, and free cash flow variables in our baseline

model (column 4, table IV) with the corresponding variables based on customer characteristics

(estimates not reported).15 The estimated coefficients from this model for the customer's age and

size variables are small and insignificant. The coefficient on the customer's R&D intensity is

positive and significant at the 5% level. Since supplier R&D intensity and customer R&D

intensity are both likely to proxy for R&D focus, this finding adds additional support to the

hypothesis that R&D focused relationships are more frequently accompanied by equity

ownership. Finally, the coefficient on a dummy variable indicating whether the customer has

positive free cash flow is positive and significant at the 10% level (p-value = .073). Consistent

with a generalized version of the financial frictions hypothesis, this provides some suggestive

evidence that deep pockets are necessary for informed sources of capital to be the optimal

financiers of financially constrained partners.

4.3 Multiple Relationships

A striking feature in the data that we noted above is that firms are often involved in

multiple trading relationships. It seems quite possible that the presence of other partners may

change the bargaining dynamics in any given relationship, which in turn may change the need for

15 We also experiment with including both the supplier and customer characteristics together in one regression. The results were quite similar to what we report above. If we add a variable indicating the customer's dependence on the supplier (amount purchased/cost of goods sold), the estimate is small and insignificant. We suspect that customers are too large for this variable to be meaningful.

24

equity ownership.16 For example, a supplier with multiple relationships may be less dependent

on any single customer, and thus an equity tie may be less important. To investigate, we

experiment with including in our baseline model a dummy variable indicating whether a supplier

is involved in more than one relationship during the observation year (estimates not reported).

Given the time-varying nature of this variable, all regressions concerning multiple relationships

are run at the relationship-year level rather than the relationship level.

When we estimate this model, the estimated coefficient on the multiple-relationship

variable is negative and significant at the 1% level. Holding other variables at their means, the

implied probability of a given customer holding a stake in the supplier drops from 2.55% to

1.56% as a supplier moves from single to multiple relationships. These figures suggests that the

likelihood a supplier gets financing from at least one customer is relatively independent of the

number of customers they have, but the probability of getting financing from any given customer

decreases once they have more than one major customer.17

This effect of multiple relationships on equity stakes could reflect a variety of

phenomenon. It could be that once a single customer has taken an equity stake, the other

customers can free-ride off of this customer's financing or monitoring capabilities. Alternatively,

it may be when there are multiple customers, there is some strategic interaction between

customers resulting in an outcome where either all customers have equity stakes or else none do.

To examine these possibilities, we estimate our baseline model restricted to cases where

suppliers are in multiple relationships. We include in this model a dummy variable indicating

16 It may be that potential for other trading opportunities affects the dynamics of a given relationship and the likelihood of observing an equity tie. However, when we include in the baseline model sales-based 4-digit SIC Herfindahl indices, they are insignificant and do not materially change the other coefficient estimates. 17 Confirming this intuition, when we run our baseline model treating each supplier (rather than each relationship) as the unit of observation, the estimate on the multiple relationship dummy variable is insignificant.

25

whether or not any other customer has an equity stake. The coefficient (estimates not reported)

on this variable is positive and significant (1% level), implying that the likelihood of taking an

equity stake increases from 1.10% to 8.12% when another customer holds equity. This suggests

that customers do pay close strategic attention to other customer's equity purchase decision.

Alternatively, we may be picking up unobserved supplier-specific characteristics. Either of these

possibilities is consistent with a generalized version of our contracting hypothesis. In any event,

the data here do not support a simple free-riding type story with regard to multiple relationships.

The presence of a large number of multiple relationships provides us with an opportunity

to revisit our earlier tests predicting equity stakes. In particular, it allows us to hold supplier

characteristics constant and then to predict which of the supplier's multiple partners takes equity.

To conduct this analysis, we use Chamberlain’s (1980) fixed effects (conditional) logit approach.

Specifically, we restrict attention to the subset of cases where the supplier has multiple

relationships in which at least one customer has a stake and at least one does not, and then we

estimate models predicting which customer has the ownership position (estimates not reported).

We include in these models the year each relationship started, the sales dependence of the

supplier on the customer, and a dummy variable for formal alliances. We then add the following

customer characteristics: R&D intensity, age, size (log assets), and a negative free cash flow

dummy variable. The coefficients on supplier sales dependence, customer R&D intensity, and

alliance variable are all positive and significant (1%, 5%, and 10% level respectively). The

customer cash flow dummy, while negative, is insignificant. These estimates are consistent with

our earlier findings that R&D intensity, sales dependence, and alliances are all positively related

to the equity stake decision, lending further support to the contracting hypothesis.

26

4.4 Equity Stakes and Formal Alliances

Our preceding results are consistent with equity ownership easing contractual frictions in

certain types of relationships. As we report above, the connection between alliances and equity

stakes is particularly strong. Since alliances themselves can be viewed as form of relationship

governance, it is informative to further investigate the link between these two governance

devices.

First we investigate whether alliances can be predicted based on relationship

characteristics. To accomplish this, we estimate our baseline model with an alliance dummy

rather than a partial equity stake dummy as the dependent variable. Interestingly, as we report in

column 1 of Table V, many of the factors that increase the likelihood of observing an equity tie

also increase the likelihood of an alliance. In particular, the estimated coefficients on R&D

intensity, sales dependence, and the negative cash flow dummy variable are all positive and

highly significant.18 This suggests that alliances and partial equity stakes are both chosen to

solve similar types of contracting and financing problems.

In column 2 of Table V we return to predicting equity stakes, but we restrict attention to

relationships that are not formalized by an alliance. The results here are informative. The

coefficients in column 2 are very similar to our earlier baseline model estimates. In particular, in

the absence of alliances, there is a strong relationship between equity stakes and R&D intensity,

sales dependence, and the negative cash flow dummy. This confirms that our earlier results on

equity stakes hold independent of the alliance effect.

18 Our results on the connection between R&D and the likelihood of an alliance complement the evidence of Chan, Kensinger, Keown, and Martin (1997) who report that abnormal returns in R&D/technology related alliances are particularly large in their sample of alliance agreement announcements.

27

Turning now to relationship with alliances, the estimates for this subsample are reported

in column 3 of Table V. Note that the subsample here is similar to those in prior studies that

choose samples based on the existence of an alliance or similar agreement (e.g., Pablo and

Subramaniam (2002)). The coefficient estimate on the supplier dependence variable in column 3

is positive and highly significant. This adds further to our evidence that equity ties are closely

related to the dependence of the supplier on the customer. However, the estimated coefficients

on R&D intensity and the cash flow variable in this column become insignificant. This is

perhaps not too surprising, as the sample of alliances is small and there is little variation in these

two explanatory variables once we restrict attention to alliances.

Taken as a whole, our evidence here suggests that alliances and equity stakes are

frequently observed together, and thus they can be viewed as complements at solving underlying

contractual issues. However, since it is also common to observe alliances without equity and

equity without alliances, there is clearly an independent dimension to each governance

mechanism. Even without the presence of an alliance, the variation in equity stakes appears

highly consistent with the notion that these positions help alleviate underlying contractual and

financing difficulties.

4.5 The Size of Equity Stakes

Our preceding analysis of the presence of equity blocks appears highly consistent with

idea that contracting problems and financing frictions lead to equity investments by product

market partners. We now turn to examining the size of observed equity blocks. As we discuss

earlier, the relationship between contracting problems and the size of blocks is less clear. In

28

particular, in delicate contracting environments there may be a dark side to high levels of equity

ownership arising from fears about excessive control or diluted incentives.19

To investigate this issue, we first we divide the entire sample into three groups: the no

ownership group (no disclosed block), the moderate ownership group (ownership in the 5%-25%

range), and the high ownership group (ownership > 25%).20 Summary statistics for each group

are reported in Panel A of the Table VI. The differences between the no ownership group and

the moderate ownership group are large and similar to our earlier comparisons between

relationships with and without equity ties. In particular, the moderate ownership group has

significantly higher average values for the variables measuring R&D intensity, sales dependence,

alliances, and financing needs. In contrast, the high ownership group actually looks more similar

to the no ownership group than to the moderate ownership group on these dimensions. These

simple comparisons suggest that contracting problems and financial frictions are more related to

moderate equity stakes than to large equity stakes, which in turn suggests that the mechanism

governing the size of equity stakes is different from that which governs the presence of a stake.

To further explore this issue, we present in Panel B of Table VI figures on the average

size of ownership stakes grouped by firm and relationship characteristics. The figures in the first

column are calculated over only those relationships where there is at least some disclosed

ownership. Here we see that our variables related to R&D intensity, sales dependence, alliances,

and external financial needs are negatively related to the size of ownership stakes. However, if

we look at all relationships, most of which have no disclosed ownership, the figures in the

second column suggest that these same variables are positively related to ownership levels. The

19 See Fee (2002) for an examination of this issue in the context of motion picture financing. 20 Our choice of 25% to define high ownership is somewhat arbitrary but follows the convention first developed by Morck, Shleifer, and Vishny (1988). Control issues are likely to become important at around this ownership level.

29

natural explanation for these findings is that these variables are positively related to the presence

of a stake, as we document in our earlier analysis, but negatively related to the size of a stake

conditional on observing one. In the overall sample the first effect dominates the second.

Turning to a multivariate analysis, we present estimates from several different empirical

models in Table VII. In column 1, we estimate a Tobit model where the ownership level is the

dependent variable and relationships with no ownership are treated as censored at the 5%

ownership level. The results here are similar to our earlier analysis predicting the presence of an

equity stake. This indicates that the factors associated with the presence of an equity stake also

are associated with the size of the stake in an unconditional sense. In column 2, we run an

ordinary least squares regression explaining the size ownership positions restricted to

observations where there is some ownership (a conditional analysis). Here, the picture is quite

different. With the exception of the size and year variables, all of the explanatory variables have

opposite signs to what we observe in column 1, and in some cases they are significant. Thus,

conditional on the existence of an equity tie, the mechanism governing the size of the stake is

almost the opposite of that which governs the stakes presence.21

To present a reasonable unconditional picture of ownership positions, we consider a

multinomial logit model predicting which of the three ownership groups (no, moderate, and

high) a relationship will fall into using our usual set of explanatory variables. The estimates in

column 3 of Table VII, which indicate the relative likelihood of observing moderate ownership

rather than low ownership, are again similar to what we found earlier when we predicting equity

21 As discussed by Greene (1993, p. 700) and Wooldridge (2002, p.536), there are many economic contexts where a significant difference in the mechanism governing closely related variables arises, in this case the presence and size of equity stakes. The Tobit model implicitly assumes that this difference is not substantial.

30

stakes using logit models. Thus, the evidence is quite strong that our contracting and financial

frictions variables are significantly related to the decision to take on a moderate equity stake.

When we turn to column 4, which indicates the relative likelihood of observing moderate

ownership rather than high ownership, the results have a different character. The estimated

coefficients on R&D intensity, sales dependence, alliance, and negative cash flow variables are

all positive, and the latter three significantly so (10%, 1%, and 1% levels respectively). This

indicates that when contracting and financing frictions are elevated, it more likely that we will

observe moderate ownership rather than high ownership.

Taken as a whole, our evidence on the size of ownership stakes presents a picture where

factors that we associate with high levels of contractual difficulties and financial frictions lead to

relationships where a customer takes a moderate stake in its supplier. The presence of high

ownership in relationships appears to be much less driven by these factors, if at all. This

evidence is consistent with moderate ownership stakes being chosen in order to delicately

balance incentives between trading parties and to provide financing to financially constrained

suppliers without ceding control. The data are less informative on the factors driving the

presence of larger ownership blocks where control is likely an important issue.

5. Equity Ownership and the Dynamics of Relationships

5.1 Equity Ownership and the Duration of Trading Relationships

Our preceding analysis assumes that equity investments are the outcome of an optimizing

process where firms choose this organizational form when the expected benefits are particularly

high. The systematic variation we uncover certainly does suggest that trading partners anticipate

that block ownership will have a real effect on the dynamics of their relationship. To

31

complement this analysis, it is informative to consider whether any of the anticipated effects of

block ownership manifest themselves after the formation of the block. However, measuring

these effects is difficult, as they are likely to appear in variables that are inherently difficult to

observe (pricing decisions, investment in relationship-specific assets, information sharing, etc.).

As a more modest goal, we consider whether block equity ownership has an effect on

relationship durability. If ownership has the effect of easing contractual frictions and

encouraging cooperation, we would expect relationships with partial ownership, all else equal, to

last longer on average.

To examine this issue, we use duration analysis techniques (see Kiefer (1988)). These

techniques estimate a hazard function describing the length of a typical relationship.

Importantly, the estimation procedures can adjust for the fact that for some relationships we

know exactly how long the relationship lasts, while for others our information is more limited

(but still useful) because of censoring. To accomplish the estimation, we define the start year

(end year) of each relationship to be the first year (last year) the two firms are linked together in

the Compustat files.22 In cases where we can confirm that both firms are still listed on

Compustat immediately after the end year, we assume that the relationship's completed length is

equal to end year minus start year. In the remaining cases, we lose the ability to detect a

relationship's status after some year because one of the two firms disappears from Compustat. In

these cases, we record the relationship's censored length as end year minus start year. Here we

know that the relationship lasted at least as long as the censored length.

22 Our sample includes all relationships in existence between 1988 and 2001. Because of this, relationships in existence as of the start of the sample period will be biased towards longer length relationships. To account for this, when an observation enters the sample with a tenure of n, our estimation adjusts for this delayed entry by using this observation only to make inferences about the hazard function in the region pertaining to a tenure of n or more.

32

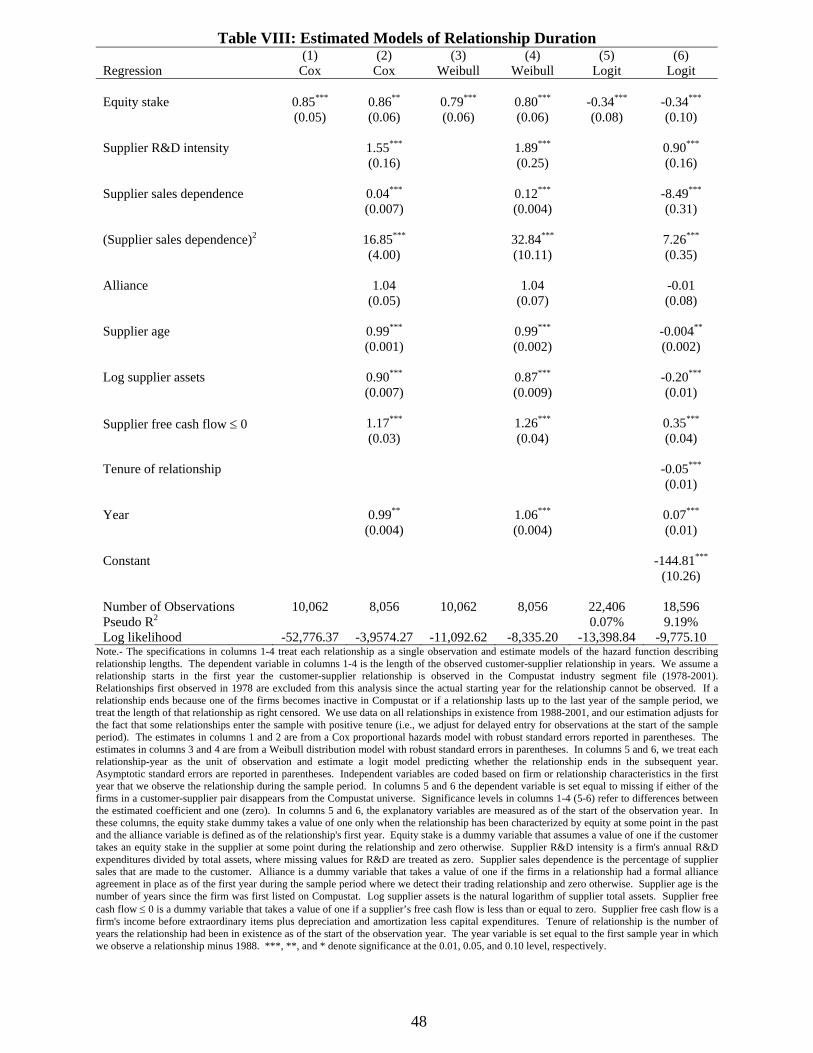

In columns 1-4 of Table VIII we present estimates from proportional hazards type

models. These models jointly estimate an underlying hazard function and the role of selected

explanatory variables in proportionally shifting the hazard function. A coefficient above one

(below one) implies that the indicated variable shifts the hazard function upwards (downwards),

thus indicating that the variable decreases (increases) average relationship length. In column 1

we present estimates from the Cox proportional hazard model with ownership as the only

explanatory variable. This model places no parametric structure on the hazard function, but it

allows the explanatory variables to shift the function up or down in a parametric way. The

estimated coefficient on the ownership dummy variable in this model is significantly less than

one at the 1% level. This provides strong initial evidence that relationships accompanied by

equity ownership tend to have lower hazard functions and, consequently, longer average

durations.

In column 2 of Table VIII we estimate the same model but add our usual set of

explanatory variables. We also add a quadratic term for sales dependence, since the requirement

that firms report customers who are responsible for 10% of sales is likely to generate some

nonlinearities with respect to this variable.23 The estimated coefficient on ownership in this

model remains significantly below one at the 5% level, again indicating that ownership is

associated with more durable relationships. Many of the other explanatory variables are also

significantly different from one. This suggests that there is substantial systematic variation in

how long relationships last. For example, the estimated coefficient on R&D, which significantly

23 Results are substantively unchanged if we use sales dependence quartiles rather than a quadratic. Many relationships that we deem to have "ended" are likely to be situations where sales fall below the 10% threshold. Our duration results are still informative, as the length of an intense trading partnership is an important quantity in its own right, and, we suspect, highly correlated with the length of time the two parties have any significant trade.

33

exceeds one, indicates that relationships with an R&D focus are typically shorter lived than

others.

To confirm these results in a more parametric framework, we also estimate models that

assume the hazard function follows the (fairly flexible) Weibull distribution. These results,

which we report in columns 3 and 4 of Table VIII, are even stronger than our prior results based

on the Cox model. The coefficient on ownership in both specifications is significantly below one

at the 1% level. All of the other control variables, with the exception of the year variable, have

similar interpretations and significance levels to the earlier Cox model estimates.

Finally, we consider a more traditional model that treats the relationship-year as the unit

of observation rather than the relationship. Our approach here is to estimate logit models

predicting whether a relationship breaks up in a given year as a function of whether the firms had

an equity tie at some point in the past. All other explanatory variables are measured as of the

start of the year. We include in these models the tenure of the relationship as of the start of the

year, as relationships with longer past tenures may be more durable in the future. We report

estimates from this type of model, with and without the full set of control variables, in columns 5

and 6, respectively, of Table VIII. In both specifications, the coefficient on the ownership

variable is negative and highly significant. This indicates that a relationship where there has

been an equity tie at some point in the past is significantly less likely to break up in the

subsequent year than relationships without equity. If we hold all control variables at their sample

means, the estimates in column 6 imply that the annual probability of a breakup for a relationship

without equity is 24.11%, falling to 18.41% when there has been an equity tie.

Taken as whole, the evidence here appears fairly convincing that the presence of equity

ownership is associated with longer-lived relationships, even when we control for factors that

34

govern the ownership choice. A natural interpretation of this finding is that an ownership tie

helps ease contracting frictions and disagreements, thus nurturing the relationship and allowing it

to last for a longer period of time. If one wants to be more cautious with regard to causality, at

the very least we can view this as another piece of evidence indicating that ownership is elevated

in situations where contracting frictions are expected to be magnified (i.e., in longer

relationships).

5.2 Equity Ownership and Mergers

An alternative way for an independent trading relationship to end is for the trading parties

to merge. Our preceding analysis implicitly assumes that partial equity ownership is a unique

form of relationship governance that is at times preferable to full vertical integration. Certainly

much of the variation in the data appears consistent with this view. However, it is possible that

equity stakes are typically just a step in a dynamic process of full integration.

To explore the connection between ownership and integration, we use the SDC mergers

and acquisitions database to determine whether the two parties in each of our 10,211 customer-

supplier relationships eventually merge together. Interestingly, we find that only 55 of these

relationships (.54%) end in a merger. Thus, it appears that intense trading relationships only

rarely result in mergers. In the subsample of relationships with an equity tie, the propensity to

eventually merge climbs to a still modest 7.10% (24 out of 338).24 Thus, while equity

investments are occasionally preludes to outright integration, in the vast majority of cases they

24 Many of these mergers (almost half) are reverse carveouts. These are usually high-ownership relationships where our models above (see Table VII) offer only weak evidence on the role of contracting and financial frictions in the equity investment.

35

are not. This helps confirm our assumption that we are studying a unique form of relationship

governance that is quite different from full vertical integration.

6. Conclusion

We study the causes and consequences of the decision to take an equity stake in a trading

partner by examining blockholdings by customers in their suppliers. We find that in most

relationships, there is no such equity investment, indicating that it is often the case that intense

trading partnerships can be effectively governed without equity participation. However, the

presence of an equity stake does systematically vary with several explanatory variables,

suggesting that equity can at times play a role in relationship governance.

Our results indicate that factors related both to contractual incompleteness and financial

market frictions are related to the equity stake phenomenon. With regard to contracting related

problems, we find that the likelihood of an equity stake is strongly positively related to whether

the supplier is an R&D intensive firm, whether a large fraction of the supplier's sales are made to

the customer, and whether there is a formal alliance agreement between the trading partners. We

argue that these findings are consistent with equity ownership easing contractual frictions that

arise in a world of incomplete contracts where trading parties are concerned about possible

expropriation problems and incentive conflicts arising over time.

With regard to financial frictions, we find that suppliers who are cash constrained in the

sense that they exhibit negative free cash flow are more likely than other firms to have equity

blocks held by their major customers. This suggests that part of the equity stake phenomenon

reflects behavior where customers serve as informed sources of capital to ease financial

constraints at the supplier level. However, other variables that may be related to supplier

36

financial constraints, for example stock return volatility and the payment of a cash dividend, do

not appear to be related to the presence of equity holdings.

When we examine the size of customers' equity holdings in their suppliers, we find that

many of the factors that affect the likelihood of observing the presence of a block do not affect

the size of a block if it is observed, and several factors even have opposite signs. This suggests

that there are limits to equity ownership, perhaps because suppliers are concerned about

customers having too much control over their operations if the customer's stake grows beyond a

certain level. Thus, in settings where incentives must be delicately managed, notably

relationships entailing high levels of R&D, a large fraction of supplier sales to the customer, or

explicit alliance agreements, it appears that an equity stake is more likely to be established, but

the size of the stake will be moderate.

Finally, we find that partial equity stakes are associated with longer-lived relationships.

However, outright mergers between customers and suppliers are rare, even when there is an

equity tie. These findings suggest that ownership has a real effect on the dynamics of trading