active ownership and transparency in private equity funds

DESCRIPTION

Foundation for the guidelines for active ownership and transparancy in private equity fundsTRANSCRIPT

Danish Venture Capital and Private Equity Association

Active ownership and transparencyin private equity funds– Background report– Guidelines for responsible ownership and good corporate governance

DVCA’s secretariat is housed in the old stock exchangebuilding next to Christiansborg Palace. Christian IV had the Stock Exchange built between 1618 and 1624 with the intention that the building should promoteCopenhagen as a trading centre and metropolis.

01 Danish Venture Capital and Private Equity Association

Foreword: Greater understanding of active ownership . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 03

Executive summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 04

I. Background and purpose . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 06

II. Private equity – a new kind of active ownership . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

III. Private equity funds and their investors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

IV. DVCA’s analyses of private equity funds in Denmark . . . . . . . . . . . . . . . . . . . . . . . . . . 34

V. Review of ten investments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

VI. Private equity funds can make mistakes too . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

VII. Interviews . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76

VIII. Private equity funds in Denmark – an overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 98

IX. List of buyouts in Denmark . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 112

Foreword and introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 127

I. The guidelines’ outlines, target group and stakeholders . . . . . . . . . . . . . . . . . . . . . . 134

II. Guidelines at company level . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 138

III. Guidelines at fund level . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 142

IV. DVCA in the future . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 148

Appendices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 149

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 159

Executive summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 160

I. Capital structure of private equity portfolio companies . . . . . . . . . . . . . . . . . . . . . . . 162

II. Tax implications of private equity buyouts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 170

III. Literature . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 186

Glossary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .188

Most of the photographs in this report are taken from private equity portfolio companies’ own archives. Otherwise see page 192.

Contents

Guidelines

Report

Research report (CEBR)

Danish Venture Capital and Private Equity Association 02

Ole Steen Andersen Christian Frigast

Ole Steen Andersen became chairman of DVCA in March 2008.

Ole Steen Andersen has a long career with the central administration,NKT and Danfoss behind him. Most recently he was Executive Vice President and CFO of Danfoss A/S, where he retired in 2007 on the occasion of the annual meeting.

Ole Steen Andersen is a member of the board of SPEAS and Nordic Industrial Advisor for CVC Capital Partner as well as being a member of the Advisory Board of Dansk Merchant Capital.

Furthermore, Ole Steen Andersen is chairman of the board of theventure company HedgeCorp A/S and member of a large number of boards both in Denmark and abroad.

Christian Frigast is a managing partner in Axcel, which he co-foundedin 1994.

Previously Christian Frigast was Executive Vice President ofIncentive (1993–94) and director of the former Unibank, nowNordea (1973–92).

Christian Frigast is an M.Sc. (Political Science and Economics) andstudied, among other places, at Stanford University in the USA. As well as sitting on the boards of companies owned by Axcel, he isthe deputy chairman of Dampskibsselskabet Torm.

Christian Frigast is deputy chairman of DVCA and chairman ofDVCA’s Private Equity committee.

03 Danish Venture Capital and Private Equity Association

Since autumn 2007 DVCA has been working on developing a set of guidelines fortransparency in private equity funds; these guidelines form part of this report.DVCA also wishes to supplement and support these guidelines by providing adetailed description of what active ownership means in Denmark, which is whyDVCA has produced this background report.

The report includes a presentation of the players in the industry and the waythey work. This is supplemented with a review of ten investments, each of whichshows in its own way how private equity funds work on building strong andhealthy companies.

The report also contains a number of interesting innovations. For example,DVCA has performed for the very first time an analysis of the return on invest-ment in private equity portfolio companies. This gives us a good idea of why in-terest in private equity has been so strong in recent years. Read more about thisin the report.

One important part of the basis for this report is a major research project carriedout over the past year by researchers at the Centre for Economic and BusinessResearch (CEBR) at Copenhagen Business School. This work, funded by DVCA,has resulted in an independent report that will later be available for downloadfrom DVCA’s website: www.dvca.dk. Although DVCA funded the project, the re-searchers were given complete freedom in the production of their report, withDVCA making as much information available to them as possible. DVCA wouldlike to thank the research team for their hard work and dedication.

The report is supplemented with a number of interviews with members of thereference group who monitored work on the guidelines. We have also spoken toa number of others with views on how private equity funds operate. We wouldlike to take this opportunity to thank all those who have contributed to the pro-duction of this report.

Ole Steen AndersenChairman, DVCA

Christian FrigastChairman of DVCA’s working group and deputy chairman, DVCA

Greater understanding of active ownership

Foreword

Danish Venture Capital and Private Equity Association 04

This report looks at private equity funds operating in Denmark. It has been pro-duced by DVCA to promote an understanding of how private equity funds workand create value.

An introduction to the background to the report and the associated guidelinescan be found here. Both guidelines and report have been produced under theleadership of a working group made up of representatives of some of the mostimportant private equity funds in Denmark. The work has also been monitoredand commented on by an external reference group.

An introduction to private equity fundsThis section contains a general introduction to private equity funds. What termi-nology is used? Who are their investors? How are the funds organised into man-agement companies and investment vehicles? How do they exercise active own-ership? There is also a look at the tax aspects of private equity funds.

A historical overview of private equity fundsThis section provides an overview of private equity funds’ international originsand of their role in different economic climates from their beginnings in the ear-ly 1980s through to the present day. This is followed by a presentation of theDanish market. Private equity funds first took off in Denmark in the mid-1990sand peaked temporarily in 2005 when the likes of TDC, Falck and ISS werebought out by international private equity funds. There are also active Danishfunds, including Axcel, Polaris and LD Equity, which all have committed capitalin excess of DKK 5bn. The section concludes with a look at private equity funds’investors.

DVCA’s analyses of private equity fundsThis section presents three different analyses commissioned by DVCA in con-nection with this report.

First, Aalund Research conducted a questionnaire survey of employee-electedboard members at current and former private equity portfolio companies inDenmark. The results show that employee-elected board members are generallypleased with the way that private equity funds exercise their ownership. For ex-ample, 70% of those questioned believe that private equity funds show respectfor a company’s corporate culture and invest sufficiently in its fixed capital. Wellover half believe that private equity funds are good at communicating aboutchanges in the company. One point to note is that 28% of those questioned donot feel that sufficient resources are allocated to employee development.

Second, Aalund Research conducted a questionnaire survey of the largest in-vestors in private equity funds. These investors together account for the bulk ofDanish private equity funds’ committed capital. Most plan to increase their in-vestment in private equity funds, and none have plans to reduce their allocationto private equity. Most are also pleased with the information they receive fromthe funds. However, there are also areas where investors feel that private equityfunds need to improve. For example, investors would like private equity funds tobe more open about their investments vis-à-vis the public.

Third, ATP PEP examined the returns on 59 completed private equity fund in-vestments in the period from 1990 to 2006. The analysis reveals an average re-turn on investment of 37% per annum before management fees (administrativeexpenses) and incentive programmes (carried interest). Assuming that thesecosts are equivalent to 3.5 percentage points, this gives a net annual return of

Executive summary

Background and purpose

The report

05 Danish Venture Capital and Private Equity Association

33.5%. This means that private equity funds significantly outperformed the stockmarket during the period.

Review of ten investmentsThis section reviews ten private equity investments, which also formed the basisfor CEBR’s survey. Together with DVCA, CEBR conducted interviews with thecompanies’ management and the partners in the private equity funds involved.Access was also granted to data that is not normally publicly available.

Robert Spliid analyses investments that went wrongThis is followed by a look at a number of private equity transactions that wereless successful for one reason or another. DVCA asked Robert Spliid, author ofthe book Kapitalfonde – Rå pengemagt eller aktivt ejerskab [Private equity funds– asset strippers or active owners?] to investigate what the industry can learnfrom this. The transactions examined include Fona, ILVA and Partner Electrics.

InterviewsIn connection with the production of its guidelines, DVCA interviewed the exter-nal reference group that monitored work on the guidelines. The group sharetheir views on the guidelines and on private equity funds’ activities in general.These views are supplemented with those of former Novo Nordisk CEO MadsØvlisen and Bain & Company partner Niels Peder Nielsen.

Overview of private equity funds in DenmarkThis overview shows which private equity funds operate in Denmark, how muchcommitted capital they have, and which investments they have been involved in.

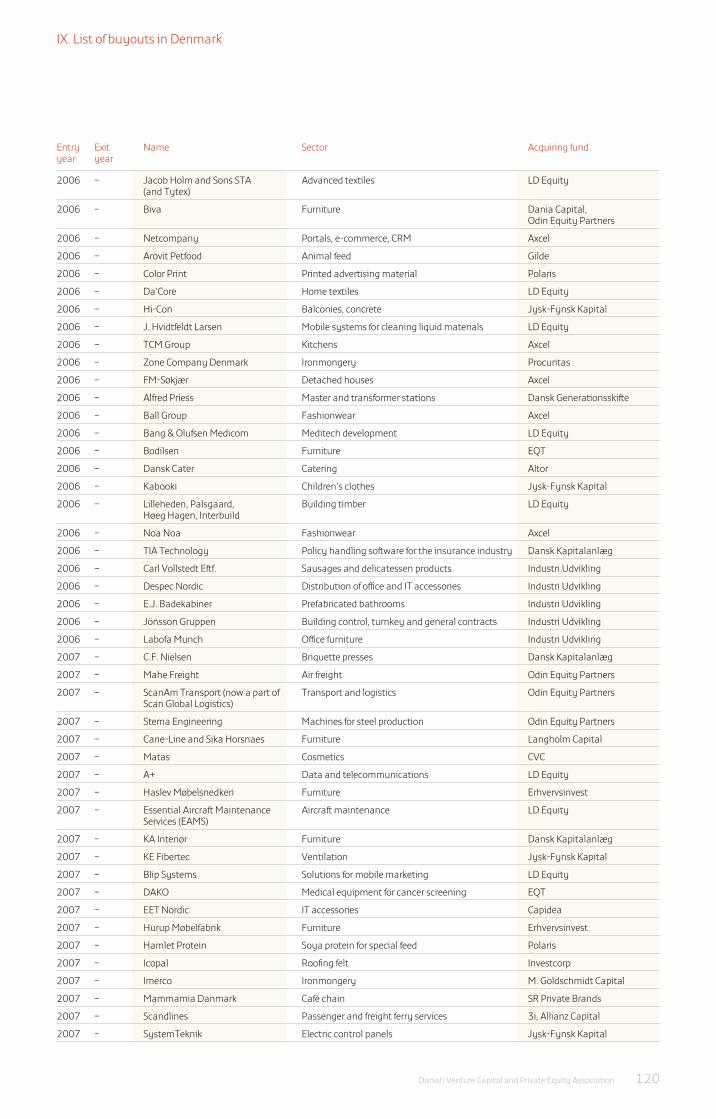

List of transactionsThis list provides for the first time a complete picture of all 307 private equityfund transactions carried out in Denmark since 1989. It includes information onexit year, revenue, sector, acquiring fund etc.

DVCA’s guidelines for responsible ownership and good corporate governanceare reproduced as part of this report.

DVCA asked the Centre for Economic and Business Research (CEBR) atCopenhagen Business School to look at a number of issues related to private equity fund ownership. The report reproduces the sections on capital structureand tax matters.

Guidelines

Research report (CEBR)

Danish Venture Capital and Private Equity Association 06

As private equity funds come to play an ever more important role in industry,they have a growing social responsibility, and this demands transparency.Private equity funds, investors and the rest of society have a mutual interest inthe companies owned by private equity funds being competitive on a sustain-able basis. Responsible ownership in private equity funds means that fundshave an opportunity to develop their companies in close collaboration with eachcompany’s board, management and employees. One important requirement inthis respect is for the wider society to be confident that private equity funds op-erate on a known and transparent basis.

The Danish Private Equity and Venture Capital Association (DVCA) has thereforedeveloped a set of guidelines for how private equity funds and their portfoliocompanies should operate and report. The aim of the guidelines is to create aconcrete and easily understood framework for private equity funds’ activitiesthat can help to build support for these activities among the general public.

DVCA thereby wishes to signal that it is preferable to avoid unnecessary regula-tion. DVCA is of the opinion that self-regulation is the best and most effectiveway of ensuring a healthy and productive business climate, and that legislationis appropriate only where other possibilities have been exhausted.

The guidelines are designed to be applied on a “comply or explain” basis. Thismeans that, in future, members of DVCA will be required either to comply withthe guidelines or to explain their reasons for not doing so if they wish to remainmembers.

Besides these guidelines, DVCA wishes to give the public a better insight intohow private equity funds work and add value to their portfolio companies. DVCAhas therefore commissioned a number of analyses in this area which are pre-sented in this report.

Transparency and guidelines for private equity funds are an international trendRequirements for greater transparency in private equity funds are an interna-tional phenomenon. In London, for example, guidelines for private equity fundsoperating in the UK were published by the Walker Working Group in November2007. These guidelines will impact on all private equity funds, as London is aglobal financial centre. Denmark is a small player by international standards,which would make it hard to produce Danish guidelines without reference to de-velopments on the international stage.

Guidelines for private equity funds are also being developed in Sweden.

A comparison of the content of the Walker guidelines and DVCA’s own can befound in appendix B to the guidelines.

Ten investments illustrating active ownership in private equity fundsDVCA wishes to show in this report how private equity funds work in practice.We have therefore selected ten investments believed by DVCA to paint a repre-sentative picture of private equity funds’ activities over the last six to eight years.

Each investment is described in terms of both the company’s key financial figures and qualitative descriptions based on interviews with key personnel involved.

The 10 investments

Danske TrælastFalckISSKompanLøgstør RørNovasolPost DanmarkRoyal CopenhagenTDCVest-Wood

Background and purpose

Background

I.

07 Danish Venture Capital and Private Equity Association

Research project looking at Danish private equity fundsTo get an independent take on issues identified when it comes to the wider eco-nomic implications of private equity funds’ activities, DVCA asked a team fromthe Centre for Economic and Business Research (CEBR) at Copenhagen BusinessSchool to carry out a research project based on the ten transactions mentionedabove.

The project fell into four parts:B The importance of active ownership (corporate governance) for portfolio

companiesB Portfolio companies’ capital structureB An economic analysis of changes in tax payments due to private equity

ownershipB The consequences of private equity ownership for the Danish capital market

The sections on tax and capital structure in the resulting report from CEBR are re-produced at the end of this report. The complete report from CEBR will be avail-able for download from DVCA’s website at a later date.

Analyses of returns, board-level involvement and investor attitudesDVCA has also commissioned a number of other analyses to promote under-standing of how private equity funds work:B An analysis of the returns on private equity funds relative to other investments

(conducted by ATP)B A study of employee-elected board members’ attitudes to private equity

ownership (conducted by Aalund Research)B A study of investors’ views of private equity funds (also conducted by Aalund

Research)

These three analyses are presented in detail in section IV of the report.

Private equity funds, investors and the rest of soci-ety have a mutual interest in the companies owned byprivate equity funds beingcompetitive on a sustainablebasis. Responsible ownershipin private equity fundsmeans that funds have anopportunity to develop theircompanies in close collabor -ation with each company’sboard, management andemployees.

Danish Venture Capital and Private Equity Association 08

A new DVCAOne important part of this project is for DVCA to play a more active role in the de-bate about private equity funds in Denmark.

To create a better understanding of private equity funds, it is important that thesector itself takes responsibility for collecting and consolidating data. Thesedata are to come from both portfolio companies and the funds themselves. DVCAwill ensure that the data are collected by an audit firm, while DVCA itself will beresponsible for the subsequent analysis of the data.

Each year DVCA will publish a report on the basis of a variety of information sub-mitted by private equity funds and their portfolio companies. This report is to in-clude a general account of trends in the industry and a statement from DVCA’scorporate governance committee.

External reference group advising DVCATo ensure that the guidelines satisfy a broad cross-section of relevant stakehold-ers, DVCA has drawn widely on an external reference group comprising:

Ingerlise Buck, head of department, Danish Confederation of Trade Unions (LO)Jan Schans Christensen, professor of corporate law, University of CopenhagenJørgen Mads Clausen, chief executive officer, DanfossBjarne Graven Larsen, chief investment officer, ATPPeter Schütze, head of retail banking, NordeaBente Sorgenfrey, chairwoman, Confederation of Professionals in Denmark (FTF)

The members of the reference group have monitored the debate about trans-parency in private equity funds and gathered views and experience from theirrespective networks. DVCA has held individual meetings with all of the mem-bers, and the group held a final meeting where the guidelines were discussed intheir entirety. The group’s views on the guidelines are presented in interviews in-cluded in this report. It should be stressed, however, that responsibility for theguidelines rests solely with DVCA.

One important part of this project is for DVCA to play amore active role in the debateabout private equity funds inDenmark.

09 Danish Venture Capital and Private Equity Association

DVCA’s committee for good corporate governance in private equity fundsIn autumn 2008 DVCA will appoint a committee to monitor compliance with theguidelines and propose any necessary adjustments. The committee will com-prise DVCA’s chairman, a state-authorised public accountant and an independ-ent industry representative.

The committee will also submit an annual statement concerning members’ com-pliance with the guidelines in connection with DVCA’s yearly report.

DVCA’s working group on transparency and active ownership in private equity funds DVCA’s transparency and active ownership project has been led by a workinggroup comprising a number of representatives of private equity funds that oper-ate in Denmark:

Lars Berg-Nielsen, DeloitteAnders Bruun-Schmidt, Dania CapitalChristian Dyvig1, Nordic CapitalChristian Frigast, Axcel (chairman)Søren Møller, LD EquityViggo Nedergaard Jensen, Polaris Private EquityThomas Schleicher, EQTSøren Vestergaard-Poulsen, CVC Capital Partners

The working group has been assisted by communication consultant JoachimSperling (project manager), state-authorised public accountant Bill HaudalPedersen from Deloitte, senior consultant Gorm Boe Petersen from DVCA, andchief financial officer Lars Thomassen and communications manager Trine JuulWengel from Axcel.

1. Succeeded by Michael Haaning in January 2008.

In autumn 2008 DVCA will appoint a committee to monitor compliance with theguidelines and propose anynecessary adjustments. The committee will compriseDVCA’s chairman, a state-authorised public accountantand an independent industryrepresentative.

“I work on building solid, profitable growth year after year through operational improvements andstrategic investments at the companies in whichwe have invested. I enjoy the close collaborationwith management at the companies in which we have invested, but the process of finding suitable investment candidates is also incrediblyinteresting.”

Søren Vestergaard Poulsen, partner, CVC Capital Partners

Søren Vestergaard Poulsen is a partner in CVC Capital Partners, one ofEurope’s largest private equity funds. He is currently responsible for itsDanish operations and sits on the boards of Post Danmark and Matas.

Søren Vestergaard Poulsen has been with CVC for ten years and was previ-ously a consultant at McKinsey & Co. He holds a Master’s degree in eco-nomics and business administration from Copenhagen Business School.

Danish Venture Capital and Private Equity Association 12

II.

The term “private equity” ultimately refers to companies in private ownership asopposed to those in public ownership – listed and state-owned companies. At itspurest, private equity is the oldest form of ownership there is. Before the days ofthe stock exchange, companies’ managers and owners were often the same people.

The private equity industry has evolved over many years starting in the 1970s. Ithas its origins partly in pension funds’ growing need to spread the risk in theirinvestment portfolios, which could be achieved by also investing in unlistedshares. In the beginning, pension funds managed these investments them-selves, but it became clear as activity levels increased that a more structured in-vestment approach was needed.

The term “private equity” is now used for a type of investment where an investment vehicle (private equity fund) with capital committed by a number ofinvestors invests directly in portfolio companies, and a management companyhandles day-to-day investment activities. The aim is to generate a larger returnthan investors could have achieved by investing in listed shares. This type of investment is known as private equity ownership and is illustrated in figure II.1below.

Investors in private equity are mainly professional investors such as pensionfunds, funds of funds, banks, insurers and wealthy private individuals/families/foundations. The investors in Danish private equity funds come from bothDenmark and abroad.

These investors’ goal is to achieve the highest possible return for their owners (inmany cases pension savers), and so they are very critical and thorough when in-vesting in a private equity fund. They choose the funds in which they wish to in-vest on the basis of their investment strategy and an assessment of the manage-ment company’s/partners’ past performance.

Private equity – a new kind of active ownership

Background and terminology

Investors1

Pension funds, insurers, wealthy

families etc.Partners

Investors

Investment vehicle (private equity fund)

Portfolio companies Financial institutions

Management company

Advice

Management fee

SalaryReturn Committed capital Return (carried interest)

Sale proceeds/dividends

Equity

Interest and repayments

Debt capital (bank loans)

Partners

1. Investors in private equity funds are also known as limited partners (LPs).

Figure II.1. The structure of a private equity fund.

13 Danish Venture Capital and Private Equity Association

The investors make a binding commitment to invest a set amount of money inthe investment vehicle. This is not paid in all at once but gradually as the invest-ment vehicle makes investments and incurs costs.

Investors get their return when each individual investment (portfolio company)is sold or listed. Thus the main form of value creation is the development of port-folio companies under the fund’s ownership so that buyers are willing to pay ahigher price for them.

An investment in private equity is therefore a long-term and relatively illiquid in-vestment. This can be illustrated by the J-curve, which is the typical profile formovements in the value of a private equity fund (see figure II.2 below). It is seenprimarily because costs are incurred in establishing and operating the fund, andthe expected increases in the value of the investments made do not arrive untilafter a couple of years of ownership, once value-adding measures and/or invest-ments begin to impact on the portfolio companies.

The private equity fund’s overall return depends on the performance of the indi-vidual companies in which it has invested. The return to investors is typicallymeasured as an annual return – the internal rate of return (IRR) – and a multiplecomparing the total amount paid out once the fund has been wound up with thetotal amount drawn from the fund’s investors.

Danish investors pay standard tax on any capital gains they make. Pensionfunds and insurance companies pay PAL tax2 while other Danish investors typi-cally pay corporation or personal income tax on their returns. Foreign investorswill be taxed primarily in their home countries (just as Danish investors in for-eign private equity funds are typically taxed on their returns in Denmark).

Figure II.2. J-curve showing movements in the value of a private equity fund.

Value

Time

2. PAL tax is a special capital tax with a fixed rate of 15% that life insurers, pension funds and the like are required to pay on their investment returns.

Danish investors pay standard tax on any capital gains they make.

Danish Venture Capital and Private Equity Association 14

II. Private equity – a new kind of active ownership

The investment vehicle is the legal entity that constitutes the actual private eq-uity fund, in other words the entity in which investors’ money is deposited andfrom which returns are paid out when a given investment is sold.

In Denmark, the corporate form normally used is the limited partnership. This issuitable because it is a flexible corporate form (e.g. when it comes to increas-es/decreases in capital, as happens every time money is drawn from investors)and because it ensures that all investors are taxed in their home countries (seediscussion of tax transparency below). The Danish limited partnership is alsovery similar to the investment vehicles used abroad, with which investors are fa-miliar and therefore feel more comfortable.

Danish limited partnerships are tax-transparent, which means that it is the part-ners/investors who are taxed on the returns generated. This tax transparencymeans that double taxation is avoided, just as with the structures used abroad.

Danish limited partnerships are required to file an annual report in accordancewith the Danish Financial Statements Act and are therefore covered by the sameaudit requirements as limited companies.

The management company, which is normally owned by a group of people withextensive experience of private equity investing, has an agreement with the fundto advise on the investment and management of the fund’s assets. The employ-ees of the management company invest personally in the investment vehicle,which is normally a condition made by many of the general partners in order toensure a sufficient financial incentive and ensure that everyone is acting in thesame financial interests (see box on page 16 on carried interest).

The individuals employed by the management company and the historical re-turns generated by the management company will be the main reasons why in-vestors choose to invest in a particular private equity fund. It is the managementcompany that is the true creator of value in the process, while the fund itself ismerely a vehicle through which capital flows.

Once an investment has been made, the management company will be closelyinvolved in the general management of the portfolio company, typically for a period of 3–7 years, with a view to developing the company and so increasing itsvalue ahead of its subsequent sale or listing. This involvement is known as activeownership and is described in more detail below.

Portfolio companies are the companies in which a private equity fund invests.The fund’s active ownership depends on control of the company so that thestrategic measures needed to ensure value creation can be implemented. Thefund will also ideally have control of the company so that it is not reliant on other shareholders when it comes to an exit (or have concluded agreements withthem on a joint sale).

Investments are financed with a mixture of investors’ money (mainly in the formof equity) and debt finance (bank loans). The level of bank debt varies and de-pends primarily on the company’s cash-flow-generating capacity. A more de-tailed discussion of optimal capital structure can be found later in this section.

The management company

Portfolio companies

The investment vehicle (the private equity fund)

15 Danish Venture Capital and Private Equity Association

A private equity fund exercises focused and active ownership in order to add val-ue to the company and so generate a return for its investors. This is characterisedin part by the following, which differ from other forms of investment:B A simple governance structure with a well-defined ownerB Inclusion of management as co-owners and incentive programmes reflecting

value addedB Limited period of ownership of each company (sense of urgency)B Optimisation of financing structureB Capital available as and when the company needs it

Private equity funds are fundamentally different to both hedge funds, whichmake speculative short-term investments in market trends, and venture cap-ital funds, which invest in start-up companies in hi-tech industries. In manycontexts – even in academic studies – private equity funds are lumped together with both hedge funds and venture capital, which is probably because the fund structure is fairly similar. When it comes to the investmentmodel and underlying assets, however, there are few points of similarity.

CEBR, Private Equity i Danmark [Private Equity in Denmark], June 2008

Active and focused ownership is crucial to private equity funds’ investment strat-egy. As a rule, therefore, these funds will acquire a majority stake in the compa-nies in which they invest, so gaining absolute control over strategic decisions atthe company. Another feature of these funds’ investment strategy is that the com-pany’s senior managers are co-investors in the company. This partnership withmanagement helps to ensure that management always works from a strategy oflong-term value creation in the company.

The private equity fund exercises active ownership on behalf of its investors anddevelops companies with a view to improving their earnings. Active ownershipmeans that the fund not only makes capital available but also actively collabor -ates with the company’s board and management on its development. The typicalinvestment horizon for investors investing in private equity funds is 10–12 years.During this period, known as the investor commitment period, the fund will ac-quire portfolio companies, develop them and sell them on to new owners.

Active ownership

Danish Venture Capital and Private Equity Association 16

II. Private equity – a new kind of active ownership

The investors in a private equity fund are keen for the management of port- folio companies, the employees of the management company and the in-vestors in the fund to have common financial interests. This alignment of interests is ensured by bringing the management of the companies and theemployees of the management company on board as co-investors, and byhaving incentive programmes reflect value added and so the returns gener-ated for investors.

Many listed and other privately held companies also have incentive pro-grammes for their management. However, these are often linked to moreshort-term performance or fluctuations in the stock markets and so not di-rectly to the return to investors.

What is carried interest (carry)?Private equity funds’ investment and incentive programmes are known ascarried interest, or carry.

Carry is a share of the return that the successful private equity fund gener-ates on its investments over and above a basic annual rate of return (hurdlerate), typically 8% of total capital invested after all costs (including manage-ment fees etc.). It is normally 20% of this additional return.

If investments perform well for investors, those covered by the carried inter-est programme will also benefit, but they also run the risk of personally los-ing money.

Carried interest and catch-upCarried interest is normally calculated on the basis of the return on the entirefund, while some funds pay out carried interest from investment to invest-ment, although this is now very unusual in Europe.

Once investors have received an agreed level of return, the managementcompany will often temporarily take an increased share of profits until theagreed level of carried interest is reached. This is known as catch-up.

Carried interest

17 Danish Venture Capital and Private Equity Association

When a private equity fund takes over a company, often more than half of thepurchase price is financed with loans. This means that the portfolio company of-ten finds itself with more debt than under its previous owners.

The reason why private equity funds normally increase a company’s debt is notto get money out of the company but to optimise its capital structure in terms ofrisk and required rates of return. This debt is therefore very different to the debtthat results from negative operating results.

It may seem a good idea to a company manager to have as much equity as pos- sible to hand (at least if he has not invested his own money in the business), be-cause this provides scope for mistakes without the company’s existence beingjeopardised.

However, it is rare for the company to own this equity. It is not without good rea-son that equity is included as a liability (alongside the company’s debt) in thecompany’s balance sheet, but as an asset in the individual shareholder’s bal-ance sheet. Both debt and equity need to be serviced from the company’s cashflow. The creditors who make debt capital available must be serviced first and sorequire a lower rate of return than shareholders. Shareholders, on the otherhand, only receive their share of the profits when all of the other bills have beenpaid, including interest on the company’s debt, and so require a significantlyhigher return on their investment.

Shareholders naturally also have an interest in the company’s survival, but theyinvest primarily to obtain a higher rate of return than they can get on other in-vestments with a similar risk profile. In other words, shareholders have an inter-est in equity levels being high enough for the company to be able to ride out un-expected fluctuations in earnings. On the other hand, equity levels should notbe so high that dividends are eroded, because this will reduce the expected re-turn (see figure II.3).

Optimal capital structure

0%

Market value

Debt 100%

Optimal structure

Value with 100% equity

Risk premium

Figure II.3. Optimal capital structure.

II. Private equity – a new kind of active ownership

Danish Venture Capital and Private Equity Association 18

When a private equity fund acquires a company, it considers how much equity ordebt is most appropriate for that particular company. The ratio of debt to equitygenerally hangs on two factors:1. The volatility of the company’s earnings.2. The likelihood of its owners’ quickly providing additional capital where

necessary.

The latter factor is very relevant to private equity portfolio companies, because,in principle, the fund always has additional capital to hand thanks to the com-mitments from its investors to invest more capital in the fund where necessary –whether to fund large investments or to counter unforeseen negative fluctua-tions in earnings.

Other things being equal, private equity portfolio companies will need less equi-ty than listed companies because it is rather more difficult and expensive to raisecapital on the stock market. Furthermore it is not always possible to raise capitalin the capital markets, especially in cases where a company’s results have notlived up to expectations for a while. This is also one of the key considerations forfinancial institutions when they assess the risk of investing in a listed companyas opposed to a private equity portfolio company.

Debt-financing the activities of a company or private equity fund is not ne -cessarily a problem, rather a natural part of economic reality in modern soci-ety. The debt taken on by companies under private equity ownership hasnevertheless given rise to public debate, and this debate is justified, becauseaggressive leverage makes companies and the economy more vulnerable inthe event of a downturn. However, private equity funds’ debt appears to ac-count for only a tiny share of overall borrowing, and is therefore of only pe-ripheral significance in the ongoing credit crunch, which can be attributedprimarily to mortgage finance and, in the second instance, banks’ generalcredit practices.

CEBR, Private Equity i Danmark, June 2008

As mentioned above, Danish private equity funds are normally organised as alimited partnership, which provides the legal framework for the fund. There areseveral points in favour of this corporate form. The most important from a taxviewpoint is that a limited partnership is tax-transparent. In other words, thepartners/investors are considered to be the owners of the underlying assets.

The partnership itself is not treated as an independent entity for tax purposes,and so it is the investors who are taxed. This ensures at a very fundamental levelthat a portfolio company’s taxed earnings are not taxed further on their way upthrough the legal structure when they come to be transferred to investors.

Investors pay tax in their home countries on the basis of local tax rules.

The use of a limited partnership structure therefore ensures that taxation takesplace at portfolio company level and investor level. Were the partnership also tobe taxed, this would result in double taxation and increase the effective rate oftax on investments. This would distort the effective tax rate relative to investingdirectly in a listed company, for example.

II. Private equity – a new kind of active ownership

The tax structure of a private equity investment

Optimal capital structure(continued)

19 Danish Venture Capital and Private Equity Association

As stated above, private equity funds are often organised as a tax-transparententity. Where this entity is physically located varies and typically depends onthe fund’s desired investors. Both Danish and foreign investors want to invest ina familiar environment where there is some degree of assurance that the legisla-tive regime will not change during the ten or so years for which a fund normallyexists.

The Channel Islands and similar jurisdictions have become a kind of marketstandard for funds looking mainly to attract international investors, and aretherefore widely used for the formation of the investment vehicle. The limitedpartnerships available for this purpose correspond closely to the Danish limitedpartnership.

Debt at private equity portfolio companies is, if at all, a problem first andforemost for the banks that have lent the money. So one might ask whetherany debt problems (cf. the current credit crunch) should be put down to thefunds or the banks. Everything suggests that the credit crunch is due to abubble in the housing market and the associated poor-quality (sub-prime)mortgages, whereas private equity funds are only a very small part of theproblem.

CEBR, Private Equity i Danmark, June 2008

Corporate buyouts are a complex discipline and require extensive preparationand thorough consideration of their commercial, financial, legal and fiscal as-pects. Private equity funds therefore invest considerable resources in ensuringthat their investments will generate an attractive return.

Tax aspects are not normally crucial to an investment, but tax must naturally beviewed as a cost like any other. Tax aspects play a role in several parts of theprocess. The first arise in connection with the due diligence process, when thefund investigates the target company to identify any risks that may have finan-cial consequences once it has gained control of the company. The second comewhen choosing the legal structure for the company, which depends on both theprivate equity fund’s structure and the financing structure implemented at thecompany after the buyout.

When a private equity fund structures a buyout, the chosen approach will beclosely linked to the fund’s structure, purpose and required rate of return (IRR).A private equity fund’s job is to acquire companies with its investors’ money andgive them an annual return ideally in excess of 20–25%. This high required re-turn on investment means that private equity funds are careful not to investmore equity than necessary in the companies they acquire.

It is important to strike the right balance between equity and debt when acquir-ing a company, as discussed on the previous pages.

Figure II.4 shows a standardised example of a buyout model.

Private equity fund A, which is organised legally as a tax-transparent limitedpartnership, wishes to acquire target company C, which is a Danish limited com-pany. As mentioned above, private equity funds can also be registered in anoth-er jurisdiction if this is more appropriate for attracting investors.

II. Private equity – a new kind of active ownership

The tax implications of corporate buyouts

Danish Venture Capital and Private Equity Association 20

What happens in practice is that fund A forms company B, whose sole purpose isto be a holding company for company C. Company B is capitalised with equityfrom fund A and debt finance. Company B then acquires the shares of company C.

Careful analysis is made of how much equity the investment requires for thebusiness plan to be realised and for the company to function in terms of itseveryday operations. There is also careful analysis of what other credit facilitiesmay be needed (such as special facilities to cover investments, acquisitions andfluctuations in working capital).

The ratio of debt to equity will also depend on local tax rules. In Denmark, localtax rules on thin capitalisation and restrictions on interest deductions play arole. A Danish company can forfeit the right to deduct interest from taxable income if it exceeds a debt-to-equity ratio of 4:1. There is also a ceiling on theamount of interest that can be deducted from taxable income. Thus, if debt levels rise too high, it may not be possible to make tax deductions for all interestcosts.

On 1 June 2007 Denmark introduced new rules limiting interest deductions, withan asset test and an EBIT test to supplement the existing rule on thin capitalisa-tion.

The existing rule on thin capitalisation means that there is no tax deduction for“excess interest” if the ratio of debt to equity at the end of the year exceeds 4:1based on market values (i.e. including goodwill). This is, however, conditionalon “controlled” (related party) debt exceeding DKK 10m.

The asset test means the introduction of an interest ceiling determined by a stan-dard rate of return (7.0% for 2008) on the tax value of certain assets. However,net financing costs up to DKK 20.6m per year will always be allowable. Interestcosts that cannot be deducted as a result of this rule cannot be carried forward.

The EBIT test means that interest deductions may not exceed 80% of EBIT, de-fined as taxable income plus net financing costs, which is different from EBIT foraccounting purposes. As with the asset test, net financing costs up to DKK 20.6m

II. Private equity – a new kind of active ownership

The new Danish restrictionson interest deductions

Private equity fund(A)

Equity

Bank debtDanish acquisition vehicle

(B)

Danish target company(C)

Danish subsidiary

Management company

Foreign subsidiaryForeign subsidiary

Joint taxation

Figure II.4. Standardised example of a buyout model.

21 Danish Venture Capital and Private Equity Association

per year will always be allowable. Interest costs that cannot be deducted as a result of this rule can, however, be carried forward and deducted from taxableincome in subsequent years.

Denmark is not the only country to have brought in rules restricting interest de-ductibility. In Germany, a rule has been introduced that limits deductions of netinterest costs in excess of an amount corresponding to 30% of EBITDA for taxpurposes. However, this rule applies only to companies that are part of a groupand incur annual net interest costs in excess of EUR 1m. Nor does the rule applyif the company’s equity/liabilities ratio is the same as, or higher than, that of therest of the group.

Despite these elements of uncertainty, a private equity fund is nothing spe-cial from a tax viewpoint. It is a particular type of financial institution that“makes its living” from buying and selling companies, but the investmentsmade by the funds and the cash flows resulting from these buyouts are cap-tured by the tax system. However, it is also a fact that funds actively testweaknesses in the tax system. For as long as interest on debt is treated differ-ently to returns on equity, for as long as the taxation of international incomeremains inconsistent, for as long as there are problems differentiating be-tween the fruits of labour and the returns on savings in the tax system, andfor as long as different types of capital income are taxed in very differentways, taxpayers will be able to think tax and maximise their income by min-imising their tax liabilities. Where this happens in connection with the activ-ities of private equity funds, it seems to be an expression of a more generalphenomenon.

CEBR, Private Equity i Danmark, June 2008

“The most exciting thing about my work is buildingbetter companies in the long term by strength-ening them both strategically and operationally.And you can see this from the companies we’veowned – they’ve grown very substantially underour ownership.”

Peter Korsholm, partner, EQT Partners

Peter Korsholm was recruited by EQT Partners in 1999 and assumed responsibility for EQT’s Danish operations in 2008.

He worked previously for Morgan Stanley in London in 1996–98.

Peter Korsholm holds an MBA from INSEAD, an MSc in econometrics andmathematical economics from the London School of Economics, and a BScin economics from the University of Copenhagen. He sits on the boards ofISS A/S, BTX Group A/S and Gambro BCT.

Danish Venture Capital and Private Equity Association 24

Private equity funds are by no means a new phenomenon. The first leveragedbuyout of a listed company took place in the USA back in 1955, when McLeanIndustries took over Waterman Steamship Corporation using mostly debt finance.But it was not until 1964 that the first example of the private equity fund modelsaw the light of day, when investment bank Bear Stearns, led by Jerome Kohlbergand Henry Kravis,2 acquired and subsequently delisted Orkin ExterminatingCompany.

Until 1980 buyout activity remained in its infancy, and players were limited to afew venture capital funds that began to show an interest in buyouts, and groupsorganised around investment banks like Bear Stearns. The first private equityfunds specialising in buyouts were created in the USA in the late 1970s and early1980s. These used the same structure as the venture capital funds had developedin the years before that, partly to allow the use of performance incentives at port-folio companies.

The first phase, 1980–1990: Private equity funds expand in the USAPrivate equity funds really began to take off in the USA in 1980 and the followingyears. A change in the regulation of pension fund investments opened up abrand new market for capital, the taxation of capital income was reduced sub-stantially, and in August 1982 the Federal Reserve decided to ease monetary pol-icy, causing long-term bond yields to fall. All of these factors made it easier forprivate equity funds to attract risk capital.

Things moved fast in the following years. Investors committed capital of USD160m to private equity funds in 1980, but USD 1.6bn in 1983. Four years later, in1987, investors committed USD 14.6bn, of which the fund raised that year bydominant US player Kohlberg, Kravis and Roberts accounted for USD 5.6bn on itsown.

The increase in the amount of money available to the funds led to growing buy-out activity, and it also became possible to increase the degree of leverage, insome cases to as high as 95%. At that rate, the committed capital figure for 1987of USD 14.6bn translates into acquisitions of almost USD 300bn. The impact onbuyout activity was therefore marked (see figure III.1).

Things culminated in 1988 when the total value of private equity transactions hitUSD 185bn. Activity in Europe was still relatively limited at this point, but spe-cialist European private equity funds began to be created towards the end of the1980s. Activity was, however, limited to the UK and a few other countries.

The second phase, 1990–2000: Buyout activity slowsAs can be seen from figure III.1, buyout activity collapsed around 1990 and re-mained in the doldrums for most of the next decade.

Private equity funds and their investors1

III.

The origins of private equity funds

1. This chapter is based largely on the report Private Equity i Danmark [Private Equity in Denmark] published by CEBR in 2008 and Robert Spliid’s book Kapitalfonde: Rå pengemagt eller aktivt ejerskab [Private equity funds: asset strippers or active owners?], Børsens Forlag, 2007.

2. Kohlberg and Kravis would come to play one of the lead roles in the growth of private equity investing. In 1976, together with George Roberts, they set up the firm Kohlberg, Kravis and Roberts (KKR), which was the dominant private equity fund in the USA throughout the 1980s. KKR made waves in Denmark in 2005 when, together with four other private equity funds, it bought out the country’s leading telecommunications company, TDC.

25 Danish Venture Capital and Private Equity Association

The dramatic decrease in activity had a number of causes, all of which made itharder to raise risk capital. There were two general economic factors that playeda role. First, the market for high-risk corporate bonds in the USA collapsed aftera series of bankruptcies. The market for the riskiest bonds, known as junkbonds, was hit hard by the bankruptcy of the leading investment bank in thismarket, Drexel Burnham Lambert.

Second, the US economy entered recession, which limited investors’ appetite forrisk, and there was a general increase in uncertainty in the financial marketswhen the Gulf War broke out. The result was soaring interest rates and a drasticdecrease in buyout activity that would persist in subsequent years.

Buyout activity began to pick up gradually from the mid-1990s, but it was not un-til after the millennium that private equity fund investments returned to the lev-els seen at their peak in the 1980s.

The third phase, 2000–?: Global expansionPrivate equity fund activity levels increased again after the millennium. The ex-planation for this can be found in changes in the general economic climate. Theglobal economy found itself in what has been called the longest economic up-swing in history, and interest rates were at a record low. Once again there wereopportunities to raise risk capital, and this led to a fresh wave of private equityfund activity. It is worth noting that this third phase in the history of private eq-uity has seen a significant spread of activity to Europe (and Asia).

Private equity investments in Europe have been higher than those in the USAevery year since 2001. By way of comparison, US listed companies account for40–50% of global market capitalisation, and EU listed companies for just 25–30%. One of the reasons for the surge in activity in Europe is probably that the in-tegration of the region’s economies has removed some of the previous obstaclesto the consolidation of industries across national borders. The introduction ofthe euro has also reduced the risk associated with fluctuating exchange rates.

200

180

160

144

120

100

80

60

40

20

0

Figure III.1. Market value of buyout investments in the USA and Europe 1980–2006.

USDbn

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

20

00

20

01

20

02

20

03

20

04

20

05

USA

Europe

Source: Gaughan (2007) and Thomson Financials.

Danish Venture Capital and Private Equity Association 26

Although it is still too early to conclude that private equity fund activity has stag-nated again, a number of economic indicators are suggesting a new market situ-ation. The economic outlook is uncertain, European interest rates are rising, andthe sub-prime crisis in the USA has increased the general level of uncertainty inthe financial markets. These factors all point towards reduced activity in thecoming years.

The first Danish private equity fund, Nordic Private Equity Partners (NPEP), wasset up in 1990 with committed capital of DKK 165m. The fund itself was regis-tered in the Channel Islands, though, so strictly speaking only its managementand part of its capital were Danish. NPEP’s first transaction was the takeover ofBroen Armatur in 1991. In 1994 NPEP raised a second fund with committed cap -ital of DKK 150m. Compared with later funds, NPEP was relatively small.

This was followed by a series of buyouts by Finnish fund CapMan and Sweden’sIndustri Kapital, as well as a few by other foreign funds. Until 1995, DanskKapitalanlæg’s acquisition of Reson in 1991 and Danfysik in 1993 and NPEP’s ac-tivities were the only Danish buyouts.

It was only with the formation of Axcel IndustriInvestor in 1994 that the localplayers in the Danish private equity market seriously began to approach the in-vestment model, organisation and size developed abroad during the previousdecade. That said, Axcel did differ from the norm by not having a limit on the lifeof the fund, and there was no separation of investment vehicle and managementcompany.3 Axcel managed to attract funding of DKK 200m from four investors,including pension fund manager PKA and bank Nordea (Unibank). Further in-vestors came in later.

One of Axcel’s first investments was Tvilum, a family-owned company produc-ing flat-pack furniture, which was subsequently merged with Scanbirk and soldto US group Masco Corporation. During Axcel IndustriInvestor’s life, its capitalwas extended to DKK 1.1bn. Axcel II was raised in 2000 with committed capital ofDKK 2.5bn, and Axcel III followed in 2005 with capital of DKK 3bn.

Polaris Private Equity was started up in 1998 with capital of DKK 1.6bn from in-vestors such as Danske Bank and pension funds Danica Pension, PFA and ATP.Since the millennium, a number of mainly relatively small private equity fundshave been established, including Dania Capital (2004), Erhvervsinvest Nord(2004), Odin Equity Partners (2004), Nordic Growth and SR Private Brands. Thelisted ITH Industri Invest (now Renewagy) and investment bank FIH also invest-ed in private equity for a long period, although both initiatives have recentlybeen closed.

In 2005 pension fund LD started up LD Equity by transferring its holdings in 23unlisted companies into the first fund. Two further funds have been raised to-gether with other institutional investors, and LD Equity has a total of DKK 7.5bnunder management. However, it should be noted that LD Equity invests in ven-ture capital as well as private equity. The last couple of years have also seen theformation of the private equity funds Capidea, Deltaq, EVO and Executive.

Besides these Danish players, many foreign private equity funds have offices inDenmark. These include some of the biggest players in the European market:

III. Private equity funds and their investors

3. When Axcel II was started up in 2000, a limit was introduced for the duration of investments, and the investment vehicle and management company were separated out.

Private equity funds in Denmark

The origins of private equity funds(continued)

27 Danish Venture Capital and Private Equity Association

3i (UK), Altor (Sweden), CapMan (Finland), CVC Capital Partners (UK), EQT Partners (Sweden), Industri Kapital (Sweden), Nordic Capital (Sweden) andProcuritas Partners (Sweden).

Finally, a number of funds of funds have been started up. Danske Bank’s initia-tive Danske Private Equity Partners was formed in 1999 and recently opened itsfourth fund. Together the four funds have committed capital of EUR 1.7bn.However, PEP invests in both private equity and venture capital, and its invest-ments are geographically diverse, mainly in Europe and the USA. In 2001 Nordeaembarked on a similar initiative called Nordea Private Equity, whose more re-cent funds focus exclusively on private equity. ATP also established ATP PrivateEquity Partners in 2001, which works like a fund of funds. To date ATP PEP hasraised four funds with a total of EUR 6bn under management. The latest fund of funds, Scandinavian Private Equity Partners, raised capital through an IPO in 2007.

The growing level of activity in Denmark can be seen from figure III.2. Between1998 and 2007, assets under management climbed from DKK 5bn to DKK 39bn.Total committed capital is higher than this, though, as Vækstfonden’s figures donot include all funds. In 2007 its figures were based on 13 funds, whereas DVCA’smembers included 14 private equity funds, seven investors in minority stakes,and five funds of funds.4

On top of this come Denmark’s EVO and Odin Equity Partners, and ProcuritasPartners and other foreign funds focusing on the Nordic countries. The totalnumber of private equity funds in Denmark engaged in buyouts is therefore atleast 17.

Figure III.3 shows the funds’ size and investment focus in terms of the enterprisevalue of prospective portfolio companies. As the size of the funds (in terms of

4. DVCA’s membership includes 14 private equity funds (3i, Altor, Axcel, Capidea, CapMan, CVC, Dania Capital, Deltaq, EQT, Executive, LD Private Equity, Industri Kapital, Nordic Capital and Polaris), nine investors in minority stakes (C.W. Obel, Dansk Kapitalanlæg, Danske Bank – Danske Markets, Erhvervsinvest, Industri Udvikling, Jysk-Fynsk Kapital, Kirkbi, Nordic Growth and SR Private Brands), three funds of funds (ATP Private Equity Partners, Danske Private Equity and Scandinavian Private Equity Partners), and Icelandic bank Glitnir, which also provides debt finance.

50

40

30

20

10

0

Figure III.2. Capital committed to Danish private equity funds 1998–2007.

DKKbn

Source: Vækstfonden (2007).Note: Vækstfonden does not include funds of funds in its figures.

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

III. Private equity funds and their investors

Danish Venture Capital and Private Equity Association 28

committed capital) grows, so does the size of prospective portfolio companies.Smaller funds such as Executive and Deltaq concentrate on companies with anenterprise value of DKK 25–250m, while the larger Danish funds like PolarisPrivate Equity and Axcel concentrate on medium-sized businesses typicallywith an enterprise value between DKK 500m and DKK 3bn. Finally, the large for-eign funds like EQT Partners, Nordic Capital and CVC Capital Partners targetcompanies with an enterprise value of at least DKK 2bn.

Activity in the Danish marketAs mentioned above, Nordic Private Equity Partners’ acquisition of BroenArmatur in 1991 was the first investment in a Danish portfolio company. After aquiet start-up period, activity has grown rapidly since the mid-1990s. Figure III.4shows total activity in the Danish market as measured by the number of buyoutsby private equity funds. The chart is based on a list of Danish private equity in-vestments between January 1991 and April 2008 drawn up by DVCA, which con-tains a total of 307 investments in portfolio companies by private equity fundsand includes both minority and majority investments. As the focus here is on ac-tive ownership, figure III.4 does not include investments in minority stakes byDansk Kapitalanlæg, Erhvervsinvest, Industri Udvikling, Jysk-Fynsk Kapital andSR Private Brands,5 but it does include all investments by LD Equity even thougharound half of its investments are in minority stakes.6 Thus a total of 192 portfo-lio companies are included in figure III.4.

III. Private equity funds and their investors

Figure III.3. Private equity funds’ size and investment focus.

Size of Investment focus as measured by enterprise value (debt-free basis)fund

DKK 0–500m DKK 0.5–1bn DKK 1–2.5bn DKK 2.5–5bn DKK 5–10bn >DKK 10bn

<DKK 1bn

DKK 1–5bn

DKK 5–10bn

>DKK 10bn

Source: Own illustration based on information from Vækstfonden (2007) and the funds’ websites.

Dania Capital

Capidea

Jysk-FynskKapital

Industriudvikling

Deltaq

Erhvervsinvest Nord

SR Private Brands

Executive Capital

Dansk Kapitalanlæg

Polaris Private Equity

Axcel

LD Equity

Nordic Capital

Industri Kapital

EQT

3i

Altor Equity Partners

CVC Capital Partners

CapMan

29 Danish Venture Capital and Private Equity Association

From modest beginnings at the start of the period, activity has grown substan-tially. Of the 192 investments made between 1991 and May 2008, 146 (76%) havecome since the millennium. Private equity funds acquired 39 Danish companiesin 2007 alone.

The most active players account for the majority of the 192 investments to date.Thus Axcel’s three funds have been involved in 31 buyouts in Denmark, which is16% of the total. Foreign private equity funds account for just over half of all buy-outs during the period (100 out of 192), and Nordic private equity funds for 41 ofthese. Table III.1 shows the number of buyouts by the nine most active privateequity funds in Denmark.

Table III.1. Number of buyouts by the nine most active private equity funds in Denmark 1991–2008.

Name Founded Country Buyouts

Axcel 1994 Denmark 31

LD Equity 2005 Denmark 23

Polaris 1998 Denmark 17

CapMan 1989 Finland 13

EQT 1994 Sweden 10

Nordic Capital 1990 Sweden 8

CVC 1981 UK 6

3i 1983 UK 6

Industri Kapital 1989 Sweden 6

Source: Based on figures from DVCA. Note that Nordic Private Equity Partners was taken over by CapMan in 2001.Note: Where two (or more) funds worked together on a buyout, both funds are credited with the transaction. See section IX for a more detailed presentation. Figures cover the period until April 2008.

5. Dansk Kapitalanlæg has made a number of investments in minority stakes that have subsequently been supple-mented with further share purchases to obtain a majority stake (e.g. mailbox producer ME-FA and manufacturingcompany M&J Industries). As the focus here is on buyouts, these investments are not included in this overview.

6. Of LD Equity’s 23 investments, 11 are majority stakes and the remainder are minority stakes. However, most of LD Equity’s minority stakes are acquired in close collaboration with the company’s management or another private equity fund, and so they have been included in the list of buyouts.

III. Private equity funds and their investors

50

40

30

20

10

0

Figure III.4. Number of buyouts by private equity funds in Denmark 1991–2008.

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

Source: Based on figures from DVCA. Note: These figures do not include investments in minority stakes by Dansk Kapitalanlæg, Erhvervsinvest Nord,Industri Udvikling, Jysk-Fynsk Kapital and SR Private Brands, but all investments by LD Equity are included asthe fund is focusing on both buyouts and minority investments going forward. The figure for 2008 covers the period from January to April.

Danish Venture Capital and Private Equity Association 30

As can be seen from table III.1, besides Axcel, activity in the Danish market isdominated by Denmark’s LD Equity and Polaris, Finland’s CapMan (which tookover NPEP in 2001 and has therefore been behind a total of 13 buyouts) andSweden’s EQT. The three most active funds account for around a third of all buy-outs, while the ten most active account for more than half of total activity. TableIII.2 breaks down the 192 buyouts by industry.

Table III.2. Number of buyouts in Denmark by industry 1991–2008.

Industry Number Percentage

Manufacturing 122 63.4

Service 22 11.5

Wholesale 19 9.9

Retail 12 6.3

IT development 8 4.2

Construction 4 2.1

Transport 4 2.1

Research 1 0.5

Total 192 100

Source: DVCA.

Unsurprisingly, manufacturing companies account for more than half of all buy-outs (122 out of 192), as they generally have stable earnings, enabling relativelyhigh levels of debt finance. Private equity funds have also invested in 22 servicecompanies and 19 wholesalers. The other sectors together account for around 15%of the total number of buyouts.

Investors in private equity funds can be divided into five main groups:1. Institutional investors (banks, insurers and pension funds)2. Companies3. Public bodies4. Funds of funds5. Private investors

Figure III.5 breaks down the sources of capital for private equity funds raised inEurope and Denmark in 2006. The charts include funds of funds, even though, inprinciple, these funds have also raised capital from investors. Funds of funds ac-count for 18% of total committed capital in Europe but just 3% in Denmark. Thisgap shows that funds of funds are a relatively new financial instrument that hasemerged to help investors to invest in private equity.

Both nationally and internationally, institutional investors are the dominantclass of investor in buyouts. Taken together, institutional investors account forabout two thirds of committed capital in Europe. Within this group, pensionfunds are the biggest players, contributing more than half of total capital frominstitutional investors, followed by banks and insurers.

III. Private equity funds and their investors

Who invests in private equity funds?

Private equity funds in Denmark(continued)

31 Danish Venture Capital and Private Equity Association

In Denmark, pension funds account for more than half of capital from institu-tional investors and so more than a third of total committed capital. Banks ac-count for slightly more than half of the remaining institutional capital, and in-surers for the rest.

In Europe, companies account for 4% of total committed capital, while publicbodies and others (individuals) each account for 9%. Companies’ share is muchhigher in Denmark at 10%, while public and other sources account for 21%, di-viding into 9% from public bodies and 12% from other sources.

Overall, institutional investors, led by pension funds, are behind the bulk of thecapital invested in private equity funds. Thus the investors in buyouts do not dif-fer greatly from those that dominate the stock market. In the USA and the UK, do-mestic institutional investors hold more than half of listed companies’ capital,while in Denmark the level is around 30%. If foreign institutional investors areincluded, these figures are much higher. In other words, the investors in privateequity funds are largely the same as the investors in listed companies.

III. Private equity funds and their investors

Pension funds 27%

Insurers 10%

Banks 14%

Others 9%

Public bodies 9%

Private investors 9%

Companies 4%

Europe

Pension funds 38%

Insurers 11% Banks 17%

Others 12%

Public bodies 9%

Companies 10%

Funds of funds 3%

Denmark

Figure III.5. Capital committed to private equity funds in Europe and Denmark in 2006 by source.

Source: EVCA Yearbook 2007.

Funds of funds 18%

“Private equity funds are now so good at the finan-cial side that they compete more on industrial insight and an ability to develop companies operationally and strategically. The private equity industry has become more mature, and developingcompanies in close and committed collaborationwith management will be increasingly importantin the future. I find this very exciting.”

Lars Terney, partner, Nordic Capital

Lars Terney has headed Nordic Capital’s Danish activities since spring 2008.

He worked previously for Boston Consulting Group (BCG), first in Chicago in1994–97 and then helping to establish BCG’s office in Copenhagen in 1998.He became a member of BCG’s Nordic management team, and was made a senior partner in 2007.

Lars Terney holds an MBA from the Kellogg School of Management atNorthwestern University in the USA.

Danish Venture Capital and Private Equity Association 34

This section presents the results of three analyses commissioned by DVCA in con-nection with the preparation of this report. There is a survey of how employee-elected board members view private equity funds, a survey of investors’ views ofprivate equity funds and their communication, and finally a study of returns onprivate equity funds performed by ATP PEP. The section is rounded off with acomparison of returns on private equity funds with returns on the stock market.

The analyses show that private equity funds are viewed positively by employee-elected board members, that investors are happy with both the information andthe returns they get from private equity funds, and that returns on private equityfunds are well above those on the stock market. However, there are also areaswhere private equity funds need to improve, such as communication with theoutside world.

A telephone-based questionnaire survey of employee-elected board members atcurrent and former private equity portfolio companies in Denmark was carriedout for DVCA by Aalund Research in spring 2008.

The survey covers a number of aspects of private equity funds’ day-to-day workwith the companies they own.1 Much of this work is channelled through the com-pany’s board of directors.

Almost 70% of the employee-elected board members surveyed believe that pri-vate equity funds show respect for the corporate culture of the companies theyown (see figure IV.1). At companies previously but no longer owned by a privateequity fund, the picture is even more positive, with 91% believing that the fundshowed respect for the company’s corporate culture.

The employee-elected board members surveyed also believe that private equityfunds are good at providing information on the changes they want to see at aportfolio company. 61% agree or partially agree that private equity funds aregood at providing information on the changes they wish to make, or have made,at the company. At companies previously but no longer owned by a private equi-ty fund, 73% believe that the fund was good at providing this information.2

Figure IV.1. Do the new owners show respect for the company’s corporate culture?

DVCA’s analyses of private equity funds in Denmark

IV.

How do employee-electedboard members view private equity funds?

Background

1. Employee-elected board members were chosen for the survey because they have close daily contact with private equity funds through their board work. The analysis covers a total of 39 respondents, of whom 28 are on the boards of companies currently owned by a private equity fund and 11 are on the boards of companies previously owned by a private equity fund.

2. Chart not shown. All charts are based on underlying data available from DVCA’s website: www.dvca.dk

Plenty 31%

Some 38%

Definitely not 3%

Neither yes nor no 23%

Don’t know 3%

No 3%

On balance, we can concludefrom this analysis that privateequity funds have made a positive impression on employee-elected board members, but also that there is room for improvement in anumber of areas, such as employee development.

35 Danish Venture Capital and Private Equity Association

Employee-elected board members are also positive about private equity owner-ship when asked whether the funds do much to make the company an attractiveplace to work (see figure IV.2). 41% believe this to be the case, while only 26%disagree. The remaining 33% are either unsure or see no difference. Again thefigure is even more positive if we look only at companies that have experiencedprivate equity ownership but are now under a different form of ownership. Here, 64% agree that the private equity fund did a lot to make their company anattractive place to work.

Figure IV.2. Do the new owners do much to make the company an attractive place to work?

The survey also shows that private equity funds are considered to be good at de-veloping their companies. More than half of the respondents believe that thefunds bring new expertise to the companies and that sufficient funds are ear-marked for investment in production equipment (see figure IV.3).

Thus the picture that emerges is that employee-elected board members are gen-erally positive about private equity ownership. The funds respect the companiesin which they invest, their management style is open, and they do a great deal tomake the company an attractive place to work.

Figure IV.3. Do the new owners put sufficient money into long-term investments in production equipment?

However, one point to note is that employee-elected board members do not believe that sufficient resources are invested in employee development (see figure IV.4). 29% feel that sufficient resources are earmarked, while 28% feel theopposite. Around 43% responded “Don’t know” or “Neither yes nor no” to thisquestion.

Plenty 13%

Some 28%

Neither yes nor no 31%

No 15%

Definitely not 10%

Don’t know 3%

Plenty 54%

Some 0%

Neither yes nor no 15%

No 28%

Definitely not 0%

Don’t know 3%

The picture that emerges isthat employee-elected boardmembers are generally positive about private equityownership.

Danish Venture Capital and Private Equity Association 36

Figure IV.4. Do the new owners ensure that sufficient funds continue to be invested in employee development?

However, it should be stressed that DVCA has not looked into how this questionabout employee development would be answered at other companies. It is there-fore difficult to gauge whether private equity portfolio companies differ from other companies in this respect.

Having active and well-prepared board members normally ensures that manage-ment receives useful feedback and guidance from the board, and this is verymuch the case at private equity portfolio companies (see figure IV.5). 75% of thosesurveyed believe that the board is a better sounding board for management underprivate equity ownership.

Figure IV.5. Is the board a better sounding board for management than before the companywas in private equity ownership?

On balance, we can conclude from this analysis that private equity funds havemade a positive impression on employee-elected board members, but also thatthere is room for improvement in a number of areas, such as employee develop-ment.

The results of the analysis above paint a different picture to the only previousDanish survey of the impact of private equity ownership on companies, pub-lished by the Danish Confederation of Trade Unions (LO) in its newsletterUgebrevet A4 in late 2007 and early 2008.