copyright © 2013 by the mcgraw-hill companies, inc. all rights reserved. 14-1 powerpoint authors:...

TRANSCRIPT

Copyright © 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

14-1

PowerPoint Authors:Susan Coomer Galbreath, Ph.D., CPACharles W. Caldwell, D.B.A., CMAJon A. Booker, Ph.D., CPA, CIACynthia J. Rooney, Ph.D., CPA

Bonds and Long-Term Notes

Chapter 14

14-2

The Nature of Long-Term Debt

Liabilities signify creditors’ interest in a company’s assets.

Liabilities signify creditors’ interest in a company’s assets.

A note payable and note receivable are

two sides of the same coin.

A note payable and note receivable are

two sides of the same coin.

Periodic interest is the effective interest rate

times the amount of the debt outstanding during

the period. Debt is reported at its present

value

Periodic interest is the effective interest rate

times the amount of the debt outstanding during

the period. Debt is reported at its present

value

A bond payable divides a large

liability into many smaller liabilities.

A bond payable divides a large

liability into many smaller liabilities.

Corporations issuing bonds are obligated to repay a

stated amount at a specified maturity date and

period interest between the issue date.

Corporations issuing bonds are obligated to repay a

stated amount at a specified maturity date and

period interest between the issue date.

14-3

Bonds

Bond Selling PriceBond Selling Price

Bond CertificateBond Certificate

Interest PaymentsInterest Payments

Face Value Payment Face Value Payment at End of Bond Termat End of Bond Term

At Bond Issuance DateAt Bond Issuance Date

Company Company Issuing Issuing BondsBonds

Company Company Issuing Issuing BondsBonds

Subsequent PeriodsSubsequent Periods

Investor Investor Buying Buying BondsBonds

Investor Investor Buying Buying BondsBonds

Company Company Issuing Issuing BondsBonds

Company Company Issuing Issuing BondsBonds

Investor Investor Buying Buying BondsBonds

Investor Investor Buying Buying BondsBonds

14-4

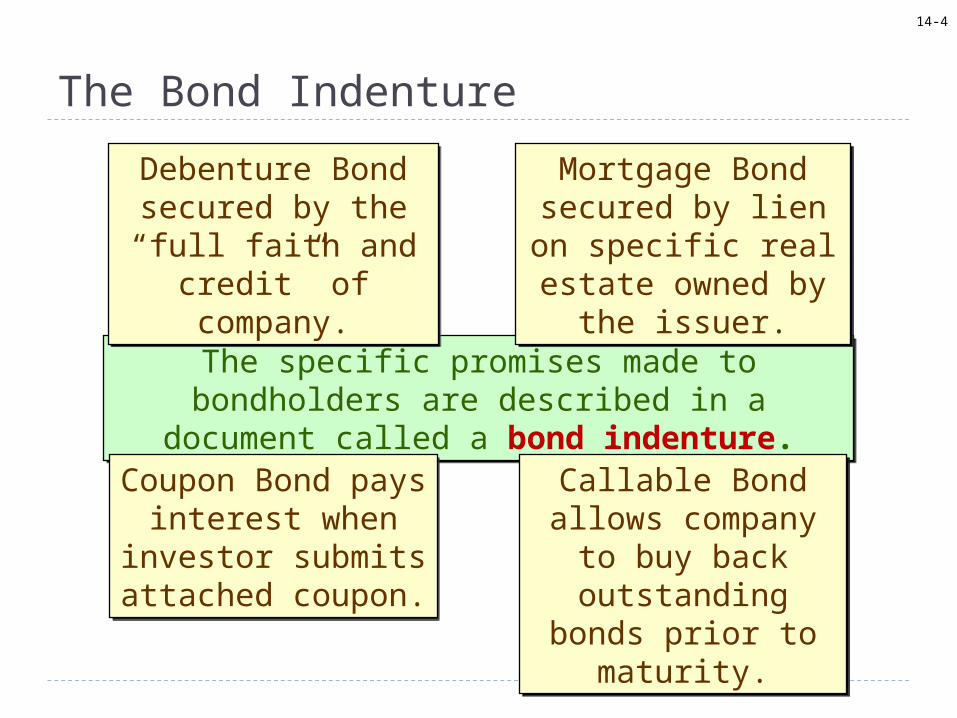

The Bond Indenture

The specific promises made to bondholders are described in a document called a bond

indenture.

The specific promises made to bondholders are described in a document called a bond

indenture.

Mortgage Bond secured by lien on specific real estate

owned by the issuer.

Mortgage Bond secured by lien on specific real estate

owned by the issuer.

Callable Bond allows company to

buy back outstanding bonds prior to maturity.

Callable Bond allows company to

buy back outstanding bonds prior to maturity.

Coupon Bond pays interest when

investor submits attached coupon.

Coupon Bond pays interest when

investor submits attached coupon.

Debenture Bondsecured by the “full faith and

credit” of company.

Debenture Bondsecured by the “full faith and

credit” of company.

14-5

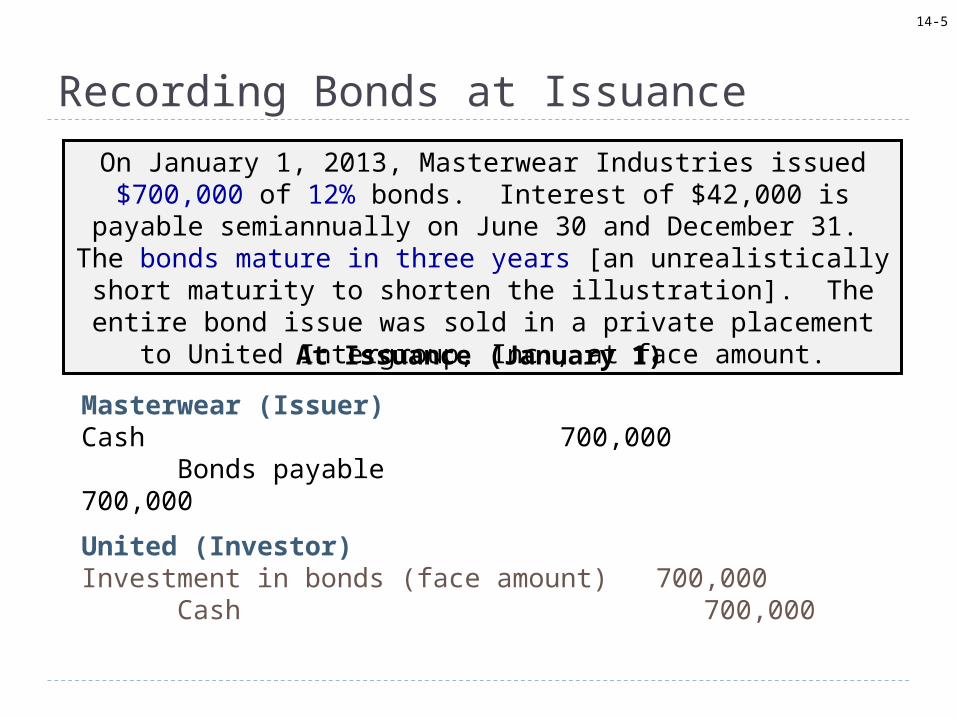

Recording Bonds at Issuance

On January 1, 2013, Masterwear Industries issued $700,000 of 12% bonds. Interest of $42,000 is payable semiannually on June 30 and December 31. The bonds mature in three years [an unrealistically

short maturity to shorten the illustration]. The entire bond issue was sold in a private placement to United Intergroup, Inc., at face amount.

At Issuance (January 1)

Masterwear (Issuer)Cash 700,000

Bonds payable 700,000

United (Investor)Investment in bonds (face amount) 700,000

Cash 700,000

14-6

Determining the Selling Price

Stated interest rate is: The bonds sells:

Below market rateAt a discount

(Cash received is less than face amount)

Equal to market rateAt face amount

(Cash received is equal to face amount)

Above market rateAt a premium

(Cash received is greater than face amount)

Stated interest rate is: The bonds sells:

Below market rateAt a discount

(Cash received is less than face amount)

Equal to market rateAt face amount

(Cash received is equal to face amount)

Above market rateAt a premium

(Cash received is greater than face amount)

14-7

Determining the Selling PriceOn January 1, 2013, Masterwear Industries issued

$700,000 of 12% bonds, dated January 1. Interest is payable semiannually on June 30 and December 31. The

bonds mature in three years. The market yield for bonds of similar risk and maturity is 14%. The entire

bond issue was purchased by United Intergroup.

Present ValuesInterest $ 42,000 × 4.76654 = 200,195$ Principal $700000 × 0.66634 = 466,438

Present value (price) of bonds 666,633$

Calculation of the Price of the BondsPresent Values

Interest $ 42,000 × 4.76654 = 200,195$ Principal $700000 × 0.66634 = 466,438

Present value (price) of bonds 666,633$

Calculation of the Price of the Bonds

Because interest is paid semiannually, the present value calculations use: (a) the semiannual stated rate (6%), (b) the semiannual market rate (7%), and (c) 6

(3 x 2) semi-annual periods.

Present value of an ordinary annuity of $1: n=6, i=7%

present value of $1: n=6, i=7%

14-8

Bonds Issued at a DiscountMasterwear (Issuer)Cash 666,633Discount on bonds payable 33,367

Bonds payable 700,000

United (Investor)Investment in bonds 700,000

Discount on bond investment 33,367Cash 666,633

Alternative Net MethodMasterwear (Issuer)Cash 666,633

Bonds payable 666,633United (Investor)Investment in bonds 666,633

Cash 666,633

14-9

Determining Interest – Effective Interest Method

Interest accrues on an outstanding debt at a constant percentage of the debt each period. Interest each period is recorded as the

effective market rate of interest multiplied by the outstanding balance of the debt (during the interest period).

The bond indenture calls for semiannual interest payments of only $42,000 – the stated rate (6%) times the face value of $700,000. The difference ($4,664) increases the liability and is reflected as a

reduction in the discount (a contra-liability account).

Interest is recorded as expense to the issuer and revenue to the investor. For the first six-month interest period the amount is

calculated as follows:

$666,633 × (14% ÷ 2) = $46,664Outstanding Balance Effective Rate Effective Interest

14-10

Recording Interest ExpenseThe effective interest is calculated each period as the market rate

times the amount of the debt outstanding during the interest period.

At the First Interest Date (June 30)

Masterwear (Issuer)Interest expense 46,664

Discount on bonds payable 4,664Cash 42,000

United (Investor)Cash 42,000Discount on bond investment 4,664

Investment revenue 46,664

$700,000 × (12% ÷ 2) = $42,000 $700,000 × (12% ÷ 2) = $42,000

$46,664 - $42,000 = $4,664 $46,664 - $42,000 = $4,664

$666,633 × (14% ÷ 2) = $46,664$666,633 × (14% ÷ 2) = $46,664

14-11

Bond Amortization Schedule

Effective Increase in OutstandingDate Cash Interest Balance Balance

1/1/13 666,633$ 6/30/13 42,000$ 46,664$ 4,664$ 671,297

12/31/13 42,000 46,991 4,991 676,288 6/30/14 42,000 47,340 5,340 681,628

12/31/14 42,000 47,714 5,714 687,342 6/30/15 42,000 48,114 6,114 693,456

12/31/15 42,000 48,544 * 6,544 700,000 252,000$ 285,367$ 33,367$

*Rounded.

Here is a bond amortization schedule showing the cash interest, effective interest, discount amortization, and the carrying value of the bonds.

$666,633 + $4,664 = $671,297$666,633 + $4,664 = $671,297

14-12

Zero-Coupon Bonds

These bonds do not pay interest. These bonds do not pay interest. Instead, they offer a return in Instead, they offer a return in the form of a deep discount the form of a deep discount

from the face amount. from the face amount.

These bonds do not pay interest. These bonds do not pay interest. Instead, they offer a return in Instead, they offer a return in the form of a deep discount the form of a deep discount

from the face amount. from the face amount.

14-13

Bond Issued at PremiumOn January 1, 2013, Masterwear Industries issued $700,000 of

12% bonds, dated January 1. Interest is payable semiannually on June 30 and December 31. The bonds mature in three years. The market yield for bonds of similar risk and maturity is 10%10%.

The entire bond issue was purchased by United Intergroup.

Present ValuesInterest $ 42,000 × 5.07569 = 213,179$ Principal $700,000 × 0.74622 = 522,354

Present value (price) of bonds 735,533$

Calculation of the Price of the BondsPresent Values

Interest $ 42,000 × 5.07569 = 213,179$ Principal $700,000 × 0.74622 = 522,354

Present value (price) of bonds 735,533$

Calculation of the Price of the Bonds

Because interest is paid semiannually, the present value calculations use: (a) the semiannual stated rate (6%), (b) the semiannual market rate (5%), and (c) 6

(3 x 2) semi-annual periods.

Present value of an ordinary annuity of $1: n=6, i=5%

present value of $1: n=6, i=5%

14-14

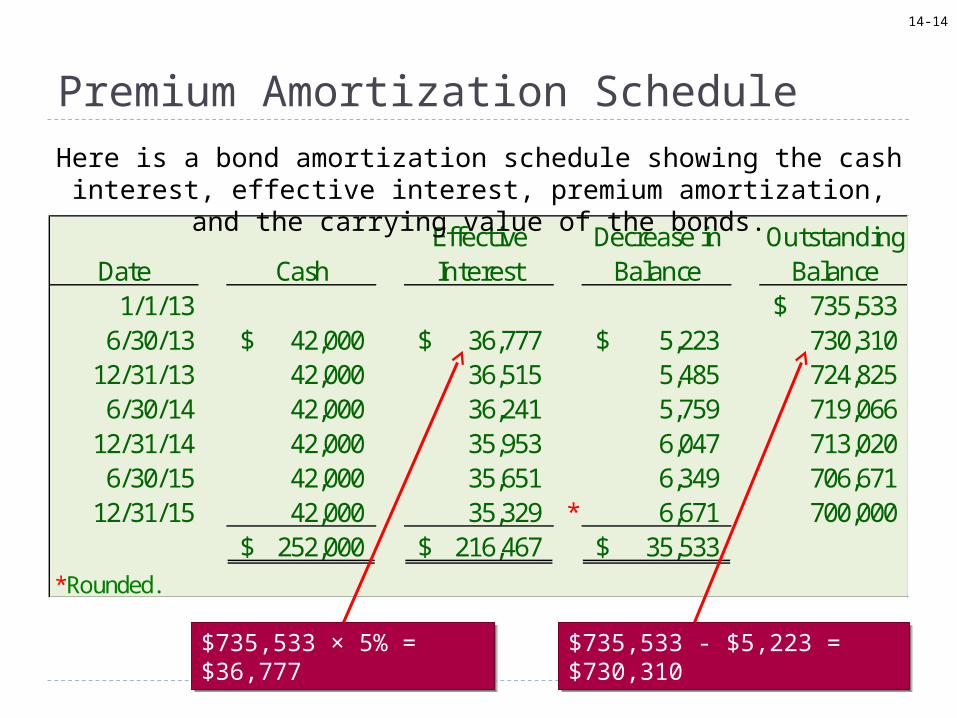

Premium Amortization Schedule

Effective Decrease in OutstandingDate Cash Interest Balance Balance

1/1/13 735,533$ 6/30/13 42,000$ 36,777$ 5,223$ 730,310

12/31/13 42,000 36,515 5,485 724,825 6/30/14 42,000 36,241 5,759 719,066

12/31/14 42,000 35,953 6,047 713,020 6/30/15 42,000 35,651 6,349 706,671

12/31/15 42,000 35,329 * 6,671 700,000 252,000$ 216,467$ 35,533$

*Rounded.

Here is a bond amortization schedule showing the cash interest, effective interest, premium amortization, and the carrying value of the bonds.

$735,533 - $5,223 = $730,310$735,533 - $5,223 = $730,310$735,533 × 5% = $36,777$735,533 × 5% = $36,777

14-15

Bonds Sold at a Premium

Masterwear (Issuer)Cash 735,533

Premium on bonds payable 35,533Bonds payable 700,000

United (Investor)Investment in bonds 700,000Premium on bond investment 35,533

Cash 735,533

Interest expense and interest revenue will be recognized in a manner consistent with bonds issued at a discount.

14-16

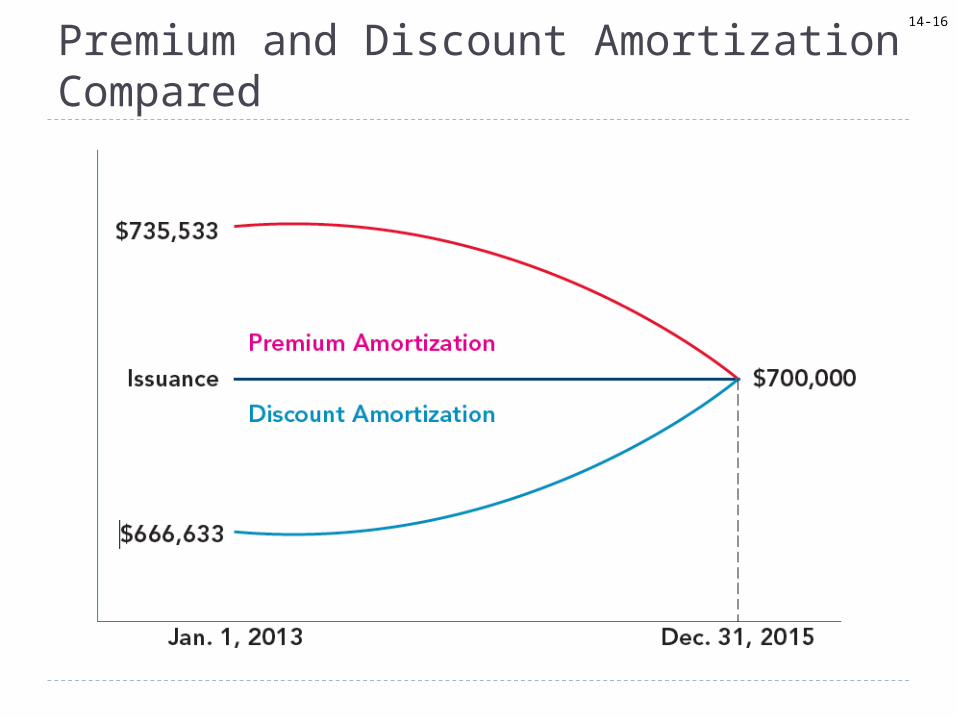

Premium and Discount Amortization Compared

14-17

When Financial Statements Are Prepared Between Interest Dates

Masterwear and United both have Masterwear and United both have October 31October 31stst year-ends. year-ends.

On January 1, 2013, Masterwear Industries issued $700,000 of 12% bonds, dated January 1. Interest is payable semiannually on

June 30 and December 31. The bonds mature in three years. The market yield for bonds of similar risk and maturity is 14%. The entire bond issue was purchased by United Intergroup at a

cost of $666,633.

$700,000 × (12% ÷ 2) = $42,000 $700,000 × (12% ÷ 2) = $42,000 $666,633 × (14% ÷ 2) = $46,664$666,633 × (14% ÷ 2) = $46,664Semi-annual Stated Interest June 30, 2013 Effective Interest

14-18

When Financial Statements Are Prepared Between Interest Dates

Year-end is on October 31, 2013, before the second Year-end is on October 31, 2013, before the second interest date of December 31, so we must accrue interest date of December 31, so we must accrue interest for 4 months from June 30 to October 31.interest for 4 months from June 30 to October 31.

Year-end accrual of interest expense and interest income.

Masterwear (Issuer)Interest expense 31,327

Discount on bonds payable 3,327Interest payable 28,000

United (Investor)Interest receivable 28,000Discount on bond investment 3,327

Investment revenue 31,327

$31,327 - $28,000 = $3,327$31,327 - $28,000 = $3,327

$671,297 × 7% × 4/6 = $31,327$671,297 × 7% × 4/6 = $31,327$42,000 × 4/6 = $28,000 $42,000 × 4/6 = $28,000

14-19

When Financial Statements Are Prepared Between Interest Dates

On December 31, the next interest payment date,On December 31, the next interest payment date,the following entries would be recorded.the following entries would be recorded.

Masterwear (Issuer)Interest expense 15,664Interest payable 28,000

Discount on bonds payable 1,664Cash 42,000

United (Investor)Cash 42,000Discount on bond investment 1,664

Interest receivable 28,000Investment revenue 15,664

14-20

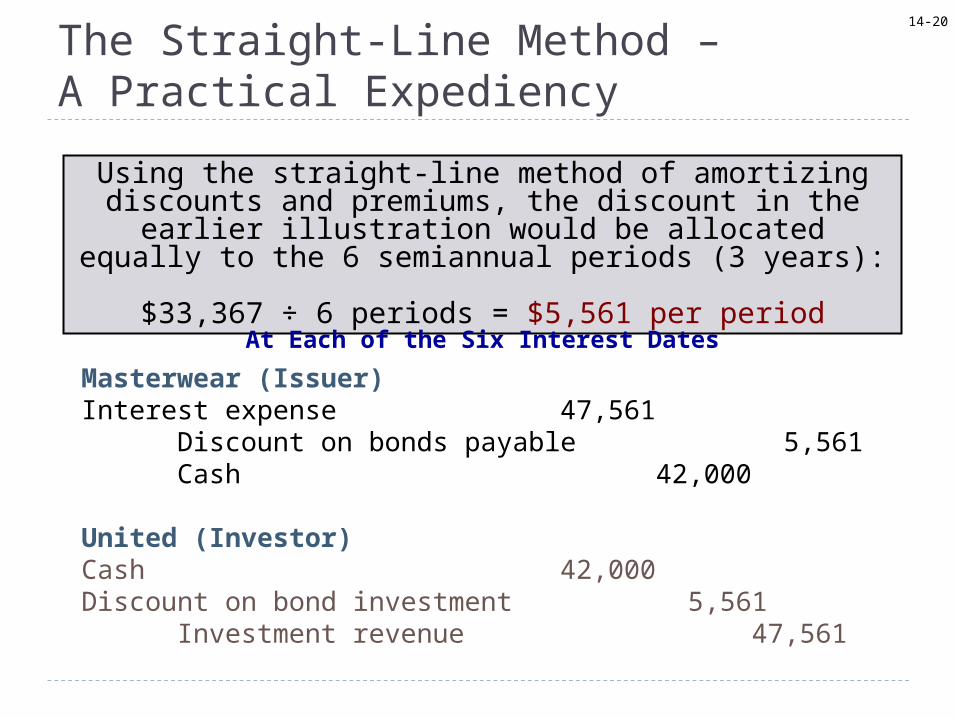

The Straight-Line Method – A Practical Expediency

Using the straight-line method of amortizing discounts and premiums, the discount in the earlier illustration would be allocated equally to the 6 semiannual periods (3 years):

$33,367 ÷ 6 periods = $5,561 per period

At Each of the Six Interest Dates

Masterwear (Issuer)Interest expense 47,561

Discount on bonds payable 5,561Cash 42,000

United (Investor)Cash 42,000Discount on bond investment 5,561

Investment revenue 47,561

14-21

Debt Issue Costs

LegalLegal AccountingAccounting UnderwritingUnderwriting CommissionCommission EngravingEngraving PrintingPrinting RegistrationRegistration Promotion Promotion

14-22

U. S. GAAP vs. IFRS

Unless the recorded amount of the debt is reduced by the transaction costs, the higher effective interest rate is not

reflected in a higher recorded interest expense.

Debt issue costs (called transaction costs under IFRS) are accounted for differently by U.S. GAAP and IFRS.

• Debt issue costs are recorded separately as an asset.

• Amortized over the term to maturity.

“Transaction costs” reduce the recorded amount of the debt.

The cost of these services reduces the net cash the issuing company receives and the amount recorded for the debt.

14-23

Long-Term Notes

BankBank

Promissory

Note(Note

Payable)

Promissory

Note(Note

Payable)

Company(Borrower)Company(Borrower)

Property, goods, or services.

Property, goods, or services.

The liability, note payable, is reported at its present value, similar to the accounting for bonds payable.

14-24

Long-Term Notes

On January 1, 2013, Skill Graphics, Inc., a product labelingand graphics firm, borrowed $700,000 cash from First BancCorp

and issued a 3-year, $700,000 promissory note. Interest of$42,000 was payable semiannually on June 30 and December 31.

January 1, At Issuance

Skill Graphics (Borrower)Cash 700,000

Note payable 700,000

First BancCorp (Lender)Note receivable 700,000

Cash 700,000

14-25

Long-Term NotesAt Each of the Six Interest Dates

At Maturity

Skill Graphics (Borrower)Interest expense 42,000

Cash 42,000

First BancCorp (Lender)Cash 42,000

Interest revenue 42,000

Skill Graphics (Borrower)Notes payable 700,000

Cash 700,000

First BancCorp (Lender)Cash 700,000

Notes receivable 700,000

14-26

Note Exchanged for Assets or Services

Present ValuesInterest $ 42,000 × 4.76654 = 200,195$ Principal $700000 × 0.66634 = 466,438

Present value (price) of note 666,633$

Present ValuesInterest $ 42,000 × 4.76654 = 200,195$ Principal $700000 × 0.66634 = 466,438

Present value (price) of note 666,633$

present value of $1: n=6, i=7%

Present value of an ordinary annuity of $1: n=6, i=7%

Skill Graphics purchased a package labeling machine from Hughes–Barker Corporation by issuing a 12%, $700,000, 3-year note that

requires interest to be paid semiannually. The machine could have been purchased at a cash price of $666,633. The cash price implies

an annual market rate of interest of 14%. That is, 7% is the semiannual discount rate that yields a present value of $666,633 for the note’s cash flows (interest plus principal) computed as follows:

The accounting treatment is the same whether the amount is determined directly from the market value of the machine or

indirectly as the present value of the note.

14-27

Note Exchanged for Assets or ServicesAt the Purchase Date (January 1)

At the First Interest Date (June 30)

Skill Graphics (Buyer/Issuer)Machinery 666,633Discount on note payable 33,367

Notes payable 700,000

Hughes-Barker (Seller/Lender)Notes receivable 700,000

Discount on notes payable 33,367Sales revenue 666,633

Skill Graphics (Buyer/Issuer)Interest expense 46,664

Discount on note payable 4,664Cash 42,000

Hughes-Barker (Seller/Lender)Cash 42,000Discount on notes payable 4,664

Investment revenue 46,664

14-28

Installment Notes

o To compute cash payment use present To compute cash payment use present value tables.value tables.

o Each payment includes both an interest Each payment includes both an interest amount and a principal amount.amount and a principal amount.

o Interest expense or revenue:Interest expense or revenue: Effective interest rate× Outstanding balance of debt Interest expense or revenue

o Principal reduction:Principal reduction: Cash amount– Interest component Principal reduction per period

14-29

Installment Notes

Decrease OutstandingDate Cash Effective Interest in Debt Balance

(7% × OutstandingBalance)

01/01/13 666,633 06/30/13 139,857 .07 × 666,633 = 46,664 93,193 573,440 12/31/13 139,857 .07 × 573,440 = 40,141 99,716 473,724 06/30/14 139,857 .07 × 473,724 = 33,161 106,696 367,028 12/31/14 139,857 .07 × 367,028 = 25,692 114,165 252,863 06/30/15 139,857 .07 × 252,863 = 17,700 122,157 130,706 12/31/15 139,857 .07 × 130,706 = 9,151 130,706 -

839,142 172,509 666,633

Decrease OutstandingDate Cash Effective Interest in Debt Balance

(7% × OutstandingBalance)

01/01/13 666,633 06/30/13 139,857 .07 × 666,633 = 46,664 93,193 573,440 12/31/13 139,857 .07 × 573,440 = 40,141 99,716 473,724 06/30/14 139,857 .07 × 473,724 = 33,161 106,696 367,028 12/31/14 139,857 .07 × 367,028 = 25,692 114,165 252,863 06/30/15 139,857 .07 × 252,863 = 17,700 122,157 130,706 12/31/15 139,857 .07 × 130,706 = 9,151 130,706 -

839,142 172,509 666,633

$666,633 ÷ 4.76654 = $139,857 amount of loan (from Table 4) installment

n=6, i=7.0% payment

Notes often are paid in installments, rather than a single amount at maturity.

Rounded

0

14-30

Installment NotesAt the Purchase Date (January 1)

At the First Interest Date (June 30)

Skill Graphics (Buyer/Issuer)Machinery 666,633

Notes payable 666,633

Hughes-Barker (Seller/Lender)Notes receivable 666,633

Sales revenue 666,633

Skill Graphics (Buyer/Issuer)Interest expense 46,664Note payable 93,193

Cash 139,857

Hughes-Barker (Seller/Lender)Cash 139,857

Notes receivable 93,193Interest revenue 46,664

14-31

Financial Statement Disclosures

Disclosures include fair value, the nature of the company’s liabilities, interest rates, maturity dates, call provisions, conversion options,

restrictions imposed by creditors, any assets pledged as collateral, and the aggregate

amounts payable for each of the next five years.

Long-term liabilities: Bonds payable, face amount 50,000,000$ Less: unamortized discount (244,875) Less: unamortized issue costs (127,500) Bonds payable, net 49,627,625$

Matrix Inc.Partial Balance SheetDecember 31, 2013

14-32

Times interest earned ratio

= Net income + interest + taxesInterest

Decision Makers’ Perspective

Debt toequity ratio

Total liabilitiesShareholders’ equity

=

Rate of return on shareholders’ equity

Net incomeShareholders’ equity==

Rate of return on assets

Net incomeTotal assets

=

14-33

Early Extinguishment of Debt

Debt retired at maturity results Debt retired at maturity results in no gains or losses. in no gains or losses.

Debt retired at maturity results Debt retired at maturity results in no gains or losses. in no gains or losses.

Debt retired Debt retired beforebefore maturity may result in an maturity may result in an gain or loss gain or loss on extinguishment.on extinguishment.

Cash Proceeds – Book Value = Gain or LossCash Proceeds – Book Value = Gain or Loss

Debt retired Debt retired beforebefore maturity may result in an maturity may result in an gain or loss gain or loss on extinguishment.on extinguishment.

Cash Proceeds – Book Value = Gain or LossCash Proceeds – Book Value = Gain or Loss

BUTBUT

14-34

Early Extinguishment of Debt

Illustration – On January 1, 2013, Masterwear Industries called its $700,000, 12% bonds when their carrying amount was

$676,290. The indenture specified a call price of $685,000. The bonds were issued previously at a price to yield 14%.

$685,000 – 676,290 $700,000 – 676,290

Masterwear (Issuer)Bonds payable 700,000Loss on early extinguishment 8,710

Discount on bonds payable 23,710Cash 685,000

14-35

Convertible Bonds

Some bonds may be converted into common Some bonds may be converted into common stock at the option of the holder. When stock at the option of the holder. When

bonds are converted the issuer (1) updates bonds are converted the issuer (1) updates interest expense and (2) amortization of interest expense and (2) amortization of

discount or premium to the date of discount or premium to the date of conversion. The bonds are reduced and conversion. The bonds are reduced and shares of common stock are increased.shares of common stock are increased.

Bonds into Stock

14-36

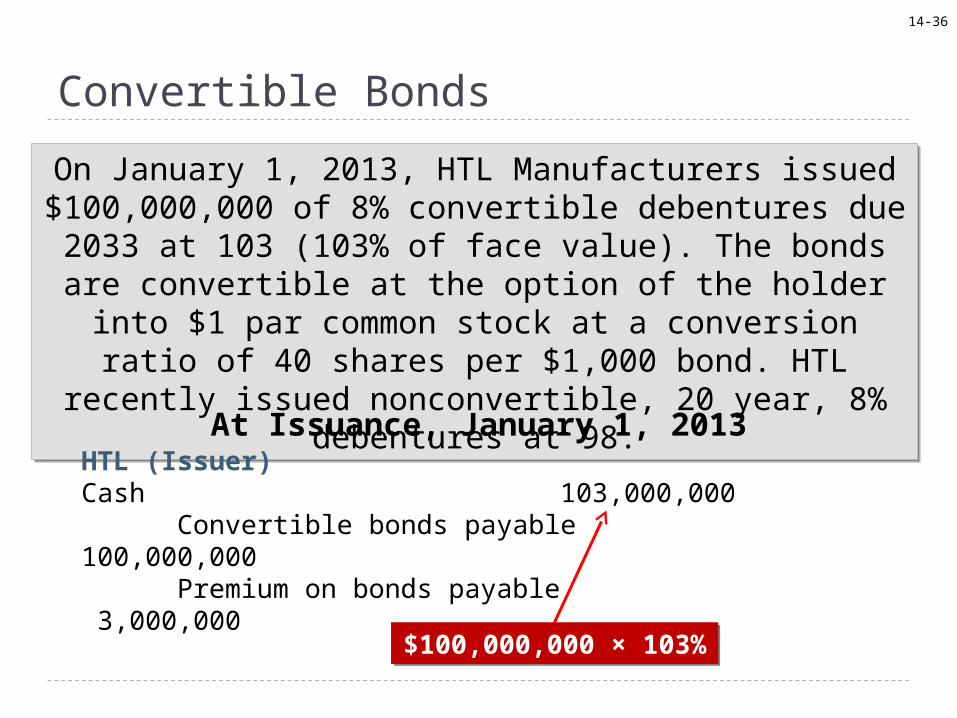

Convertible Bonds

On January 1, 2013, HTL Manufacturers issued $100,000,000 of 8% convertible debentures due 2033 at 103 (103% of face value). The bonds are convertible at the option of the holder into $1 par common stock at a conversion ratio

of 40 shares per $1,000 bond. HTL recently issued nonconvertible, 20 year, 8% debentures at 98.

On January 1, 2013, HTL Manufacturers issued $100,000,000 of 8% convertible debentures due 2033 at 103 (103% of face value). The bonds are convertible at the option of the holder into $1 par common stock at a conversion ratio

of 40 shares per $1,000 bond. HTL recently issued nonconvertible, 20 year, 8% debentures at 98.

At Issuance, January 1, 2013

$100,000,000 × 103%$100,000,000 × 103%

HTL (Issuer)Cash 103,000,000

Convertible bonds payable 100,000,000Premium on bonds payable 3,000,000

14-37

Convertible Bonds

Assume the bondholder exercises one-half of their option to convert the bonds into shares of stock when there is an

unamortized premium of $2,000,000 associated with these bonds. The bonds are removed from the accounting records and the new shares issued are recorded at the same amount

(in other words, at the book value of the bonds).

Assume the bondholder exercises one-half of their option to convert the bonds into shares of stock when there is an

unamortized premium of $2,000,000 associated with these bonds. The bonds are removed from the accounting records and the new shares issued are recorded at the same amount

(in other words, at the book value of the bonds).

HTL (Issuer)Convertible bonds payable 50,000,000Premium on bonds payable 1,000,000

Common stock 2,000,000Paid-in capital – excess of par 49,000,000

At Date of Exercise of One-half of the Bonds

50,000 bonds × 40 shares × $1 par = $2,000,000 par value50,000 bonds × 40 shares × $1 par = $2,000,000 par value

14-38

Induced Conversion

Companies sometimes try to induce conversion. The

motivation might be to reduce debt and become a better risk to potential lenders or achieve a lower debt-to-equity ratio.

Companies sometimes try to induce conversion. The

motivation might be to reduce debt and become a better risk to potential lenders or achieve a lower debt-to-equity ratio.

When the specified call price is less than the conversion value of the bonds (the market value

of the shares), calling the convertible bonds provides bondholders with incentive to convert.

When the specified call price is less than the conversion value of the bonds (the market value

of the shares), calling the convertible bonds provides bondholders with incentive to convert.

14-39

U.S. GAAP vs. IFRSConvertible Bonds

Under IFRS, unlike U.S. GAAP, convertible debt is divided into its liability and equity elements.

($ in millions)

Cash (103% $100 million) 103

Convertible bonds payable (value of the debt only) 98*

Equity–conversion option (difference) 5

*The discount is combined with the face amount of the bonds. This is the “net method” – the preferred method under IFRS.

Compound instruments such as this one are separated into their liability and equity components in accordance with IAS No. 32.

If the bonds have a separate fair value of $98 million, we record that amount as the liability and the remaining $5 million as equity.

14-40

Bonds With Detachable Warrants

Stock warrants provide the option to purchase a specified number of shares of common stock at a specified option price per share within a stated period.

A portion of the selling price of the bonds is allocated to the detachable stock warrants.

Stock warrants provide the option to purchase a specified number of shares of common stock at a specified option price per share within a stated period.

A portion of the selling price of the bonds is allocated to the detachable stock warrants.

14-41

Bonds With Detachable Warrants

On January 1, 2013, HTL issued $100,000,000 of 8% bonds On January 1, 2013, HTL issued $100,000,000 of 8% bonds due in 2020 at 103 (103% of face value). Accompanying each due in 2020 at 103 (103% of face value). Accompanying each

$1,000 bond were 20 warrants. Each warrant permitted the $1,000 bond were 20 warrants. Each warrant permitted the holder to buy one share of $1 par common stock at $25 per holder to buy one share of $1 par common stock at $25 per

share. Shortly after issuance, the warrants were listed on the share. Shortly after issuance, the warrants were listed on the stock exchange at $3 per warrant. stock exchange at $3 per warrant.

On January 1, 2013, HTL issued $100,000,000 of 8% bonds On January 1, 2013, HTL issued $100,000,000 of 8% bonds due in 2020 at 103 (103% of face value). Accompanying each due in 2020 at 103 (103% of face value). Accompanying each

$1,000 bond were 20 warrants. Each warrant permitted the $1,000 bond were 20 warrants. Each warrant permitted the holder to buy one share of $1 par common stock at $25 per holder to buy one share of $1 par common stock at $25 per

share. Shortly after issuance, the warrants were listed on the share. Shortly after issuance, the warrants were listed on the stock exchange at $3 per warrant. stock exchange at $3 per warrant.

HTL (Issuer)Cash 103,000,000Discount on bonds payable 3,000,000

Bonds payable 100,000,000Equity – stock warrants 6,000,000

100,000 bonds × 20 warrants × $3 100,000 bonds × 20 warrants × $3

14-42

Bonds With Detachable Warrants

Assume one-half of the warrants (1,000,000) are exercised when the market value of HTL’s common stock is $30 per

share. The exercise price is $25 per common share.

Assume one-half of the warrants (1,000,000) are exercised when the market value of HTL’s common stock is $30 per

share. The exercise price is $25 per common share.

HTL (Issuer)Cash 25,000,000Equity – stock warrants 3,000,000

Common stock 1,000,000Paid-in capital – common stock 27,000,000

1,000,000 warrants × $25 1,000,000 warrants × $25

$6,000,000 ÷ 2 $6,000,000 ÷ 2

14-43

Option to Report Liabilities at Fair Value

Companies have the option to value some or all of their financial assets and liabilities at fair value.

Companies have the option to value some or all of their financial assets and liabilities at fair value.

The same market forces that influence the fair

value of an investment in debt securities

(interest rates, economic conditions,

risk, etc.) influence the fair value of liabilities.

The same market forces that influence the fair

value of an investment in debt securities

(interest rates, economic conditions,

risk, etc.) influence the fair value of liabilities.

14-44

U. S. GAAP vs. IFRS

The fair value option may be elected by the firm.

Although U.S. GAAP guidance indicates that the intent of the fair value option under U.S. GAAP is to address these sorts of circumstances, it does not require that those circumstances exist.

International accounting standards are more restrictive than U.S. standards for determining when firms are

allowed to elect the fair value option.

Companies may only elect the fair value option when

1. When a group of financial assets or liabilities is managed and its performance is evaluated on a fair value basis, or

2. If the fair value option reduces “accounting mismatch.”

14-45

Where We’re HeadedUnder a proposed change in the way we account for financial assets and liabilities, financial assets would be measured at (a) fair value with changes reported in net income (FV-NI), (b) at fair value through Other Comprehensive Income (FV-OCI), or (c) at amortized cost, the classification depending on the assets’ characteristics and the company’s business strategy for holding the assets.

Most liabilities would be accounted for at amortized cost as described in this chapter. The fair value option, though, would no longer be permitted except in unique circumstances. The proposed change is a result of a joint project on financial instruments by the International Accounting Standards Board (IASB) and the FASB as part of a broader goal of achieving a single set of high quality global accounting standards. At the time this text is being written, a final standard is expected to be issued in 2012.

Under a proposed change in the way we account for financial assets and liabilities, financial assets would be measured at (a) fair value with changes reported in net income (FV-NI), (b) at fair value through Other Comprehensive Income (FV-OCI), or (c) at amortized cost, the classification depending on the assets’ characteristics and the company’s business strategy for holding the assets.

Most liabilities would be accounted for at amortized cost as described in this chapter. The fair value option, though, would no longer be permitted except in unique circumstances. The proposed change is a result of a joint project on financial instruments by the International Accounting Standards Board (IASB) and the FASB as part of a broader goal of achieving a single set of high quality global accounting standards. At the time this text is being written, a final standard is expected to be issued in 2012.

14-46

Appendix 14A: Bonds Issued Between Interest Dates

Suppose a weak market caused a delay in selling the bonds until two months after the bond date of January 1(four months before semiannual interest was to be

paid). In that case, the buyer would be asked to pay the seller accrued interest for two months in addition to the

price of the bonds.

Masterwear was unable to sell $700,000 face amount of bonds, dated January 1, and paying interest semiannually at an annual rate of 12%. The bonds were eventually sold on March 1. Let’s calculate the accrued interest.

14-47

Appendix 14A: Bonds Issued Between Interest Dates

The journal entry at the date of issuance (March 1) on the books of the issuer and investor are shown below:

14-48

Appendix 14A: Bonds Issued Between Interest Dates

On June 30, the first interest payment date, the following journal entries will be made for the issuer and investor.

14-49

Appendix 14BTroubled Debt Restructuring

When changing the original terms of a debt agreement is motivated by financial difficulties experienced by the debtor (borrower), the new arrangement is referred to as a troubled debt restructuring.

A troubled debt restructuring may be achieved in either of two ways:1.The debt may be settled at the time of the restructuring.2.The debt may be continued, but with modified terms.

14-50

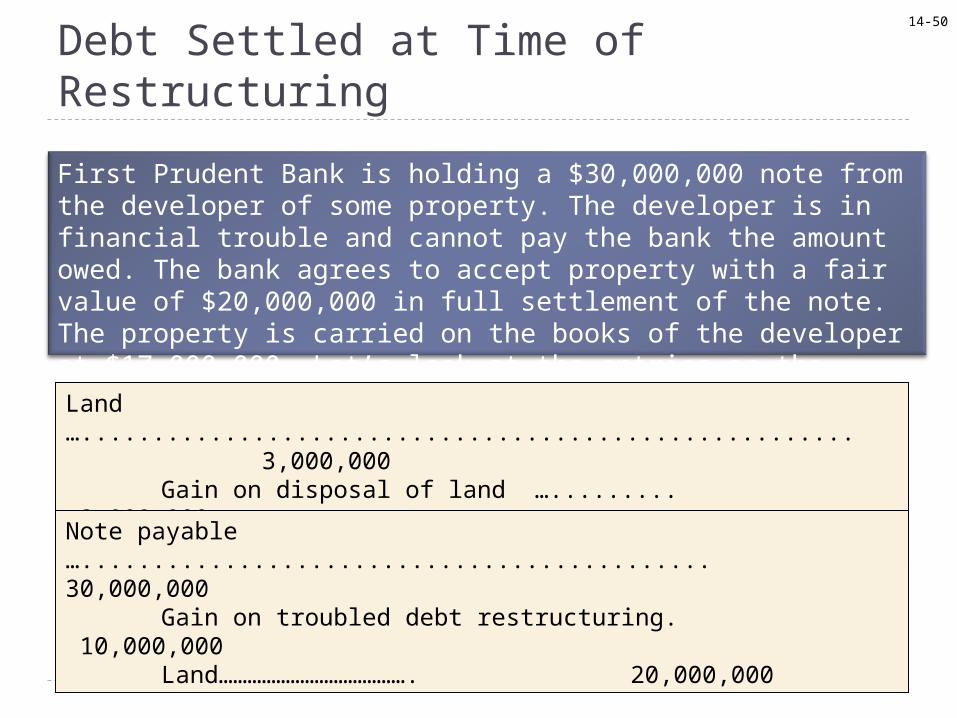

Debt Settled at Time of Restructuring

First Prudent Bank is holding a $30,000,000 note from the developer of some property. The developer is in financial trouble and cannot pay the bank the amount owed. The bank agrees to accept property with a fair value of $20,000,000 in full settlement of the note. The property is carried on the books of the developer at $17,000,000. Let’s look at the entries on the books of the developer to record the settlement.Land …...................................................... 3,000,000

Gain on disposal of land …......... 3,000,000($20,000,000 less carrying value of $17,000,000)

Note payable …............................................ 30,000,000Gain on troubled debt restructuring. 10,000,000Land…………………………………. 20,000,000

14-51

Debt is Continued, but with Modified Terms

Let’s look at an example where the total cash payments are less than the carrying amount of the debt. First Prudent Bank holds a $30,000,000 note from a property developer. The note bears interest at 10%, and matures in two years. The developer is in financial difficulty and the bank agrees to modify the terms of the agreement as follows:1.Forgive the interest accrued from last year of $3,000,000.2.Reduce the remaining two interest payments to $2,000,000 each.3.Reduce the principal amount to $25,000,000.

Let’s look at an example where the total cash payments are less than the carrying amount of the debt. First Prudent Bank holds a $30,000,000 note from a property developer. The note bears interest at 10%, and matures in two years. The developer is in financial difficulty and the bank agrees to modify the terms of the agreement as follows:1.Forgive the interest accrued from last year of $3,000,000.2.Reduce the remaining two interest payments to $2,000,000 each.3.Reduce the principal amount to $25,000,000.Principal Interest TotalCarrying amount 30,000,000$ 3,000,000$ 33,000,000$ Future payments 25,000,000 4,000,000 29,000,000 Gain to developer 4,000,000$

14-52

Debt is Continued, but with Modified Terms

Accrued interest payable ............................. 3,000,000Note payable …........................................... 1,000,000

Gain on debt restructuring ………. 4,000,000

Note payable …......................................... 2,000,000Cash ……………………………… 2,000,000

At the date of the new agreement, the following journal entry is required:

The debit to notes payable is for the difference between the old face amount of $30,000,000 and the total future cash payments of $29,000,000

At each of the next two interest payments, we will make the following entry:

14-53

Debt is Continued, but with Modified Terms

AmountFace amount of old note 30,000,000$ Entry at date of restructuring (1,000,000) First interest payment (2,000,000) Second interest payment (2,000,000) Maturity value of note 25,000,000$

At maturity, the developer will make the following entry:

Note payable …......................................... 25,000,000Cash ……………………………… 25,000,000

14-54

End of Chapter 14