1 - 1 powerpoint authors: susan coomer galbreath, ph.d., cpa charles w. caldwell, d.b.a., cma jon a....

TRANSCRIPT

1 - 1

PowerPoint Authors:Susan Coomer Galbreath, Ph.D., CPACharles W. Caldwell, D.B.A., CMAJon A. Booker, Ph.D., CPA, CIACynthia J. Rooney, Ph.D., CPA

Copyright © 2011 by The McGraw-Hill Companies, Inc. All rights reserved.1 - 1

Environment and Theoretical Structure of Financial Accounting

1

1 - 2

Financial Accounting Environment

Profit-orientedcompanies

Not-for-profitentities

Households

Providers ofFinancial

InformationExternal

User Groups

Investors

Creditors

Employees

Labor unions

Customers

Suppliers

Governmentagencies

Financialintermediaries

Relevant

FinancialInformation

1 - 3

Financial Accounting Environment

Relevant financial information is provided primarily through financial statements and related disclosure notes. Balance Sheet Income Statement Statement of Cash Flows Statement of Shareholders’ Equity

1 - 4

The Economic Environment and Financial Reporting

A sole proprietorshipis owned by a

single individual.

A sole proprietorshipis owned by a

single individual.

A partnership isowned by two ormore individuals.

A partnership isowned by two ormore individuals.

A corporation is ownedby shareholders.

A corporation is ownedby shareholders.

1 - 5

Investment-Credit Decisions ─ A Cash Flow Perspective

Shareholders Receive

Cash

1. Dividends2. Sale of Stock

Creditors Receive

Cash

1. Interest2. Loan Repayment

Accounting information should help investors and creditors evaluate the amount, timing, and uncertainty of the enterprise’s future

cash flows.

1 - 6

Cash versus Accrual Accounting

Cash Basis Accounting Revenue is recognized when cash is received. Expenses are recognized when cash is paid.

OROROR

OR

Accrual AccountingRevenue is recognized when earned.

Expenses are recognized when incurred.

1 - 7

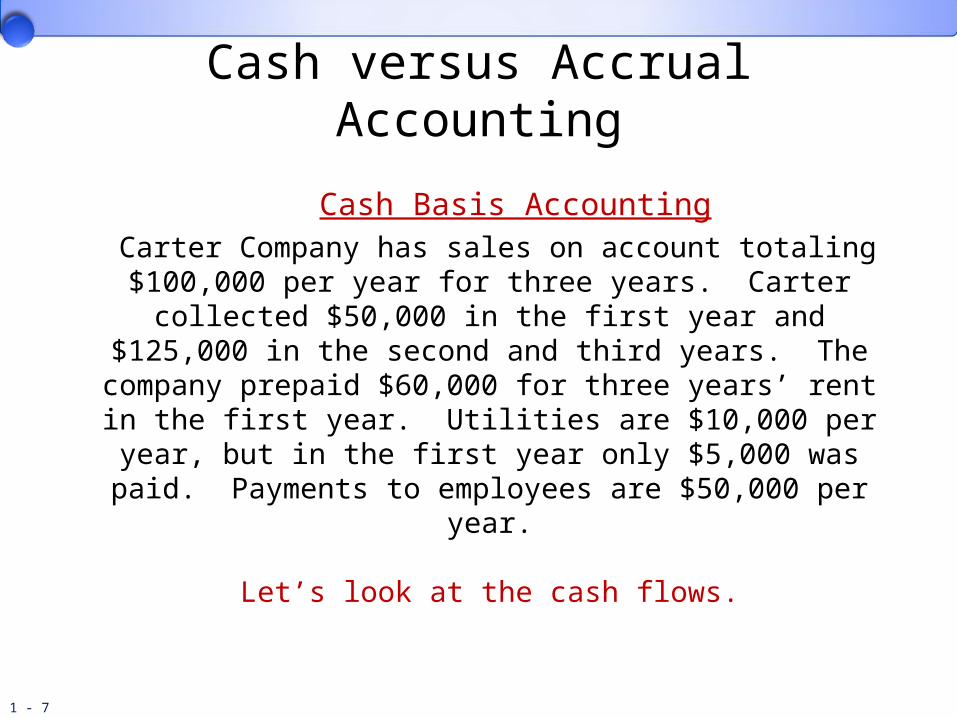

Cash versus Accrual Accounting

Cash Basis Accounting Carter Company has sales on account totaling

$100,000 per year for three years. Carter collected $50,000 in the first year and $125,000 in the second and third years. The company prepaid $60,000 for

three years’ rent in the first year. Utilities are $10,000 per year, but in the first year only $5,000 was paid.

Payments to employees are $50,000 per year.

Let’s look at the cash flows.

1 - 8

Cash versus Accrual Accounting

Cash Basis Accounting

Cash flows in any one year may notbe a predictor of future cash flows.

1 - 9

Cash versus Accrual Accounting

Accrual Basis Accounting

Net Income is considered a better indicator of future cash flows.

1 - 10

The Development of Financial Accounting and Reporting Standards

Concepts, principles, and

procedures weredeveloped to meet the

needs of external users (GAAP).

1 - 11

Historical Perspective and Standards

1 - 12

Current Standard Setting

• Supported by the Financial Accounting Foundation

• Five full-time, independent voting members• Answerable only to the Financial Accounting

Foundation• Members not required to be CPAs

Financial Accounting Standards Board

1 - 13

FASB Accounting Standards Codification

The objective of the codification project was to integrate and organize by topics all relevant accounting pronouncements

into a searchable, online database.

1 - 14

Establishment of Accounting StandardsA Political Process

GAAP

Internal RevenueServicewww.irs.gov

American Instituteof CPAswww.aicpa.org

Securities andExchangeCommissionwww.sec.gov

AmericanAccountingAssociation www.aaa-edu.org

GovernmentalAccountingStandards Boardwww.gasb.org

Financial ExecutivesInternationalwww.fei.org

International Accounting Standards Boardwww.iasb.org

1 - 15

FASB’s Standard-Setting Process Board receives recommendations for projects. Board votes to add the project to its agenda . Board deliberates the issues at a series of public

meetings. Board issues an Exposure Draft (ED). Board holds a public roundtable meeting on the ED. Staff analyzes feedback and the Board re-deliberates

the proposed revisions at public meetings . Board issues a Standards Update describing

amendments to the Codification.

1 - 16

Toward Global Accounting Standards

The main objective of the International Accounting Standards Board (IASB) is to

develop a single set of high quality, understandable and enforceable global

accounting standards to help participants in the world’s capital markets and other users

make economic decisions.

1 - 17

Role of the Auditor

Auditors serve as independent intermediaries to help insure that

management has appropriately applied GAAP in preparing the company’s

financial statements.

1 - 18

Financial Reporting Reform

As a result of numerous financial scandals, Congress passed the Public Company Public Company

Accounting Reform and Investor Protection Accounting Reform and Investor Protection Act of 2002Act of 2002, (Sarbanes-Oxley Act). The goal

was to restore credibility and investor confidence in the financial reporting process.

1 - 19

A Move Away from Rules-Based Standards?

• Rules based accounting standards vs. objectives-oriented approach

• Objectives oriented (principles-based) approach stressed professional judgment

1 - 20

Ethics in Accounting

• For financial information to be useful, it should possess the fundamental decision-specific qualities of relevance and faithful representation.

• Management may be under pressure to report desired results and ignore or bend existing rules.

1 - 21

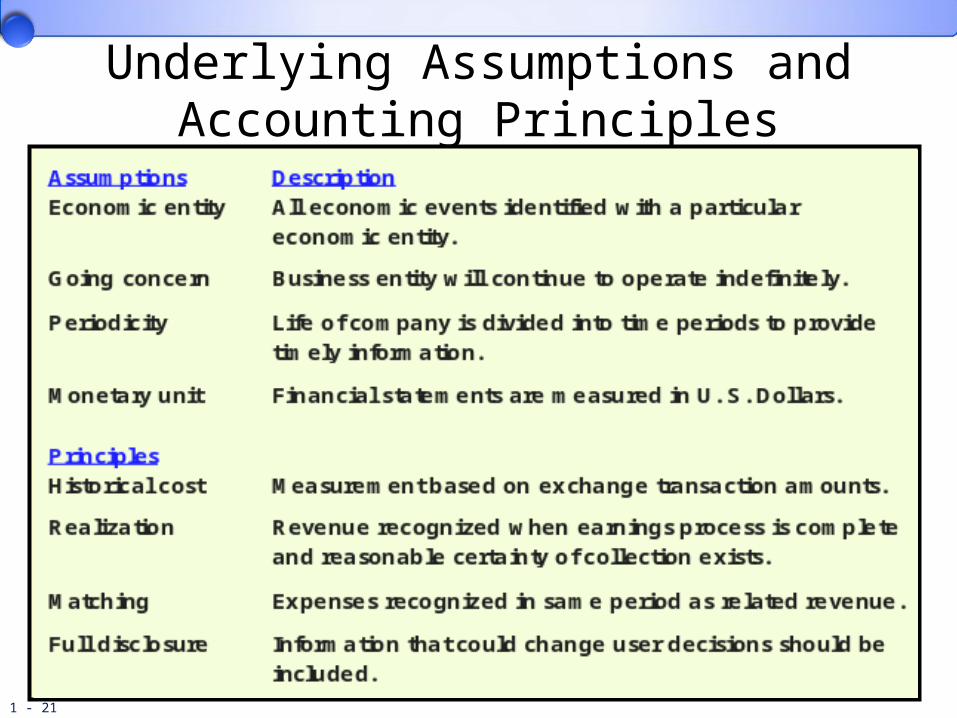

Underlying Assumptions and Accounting Principles

1 - 22

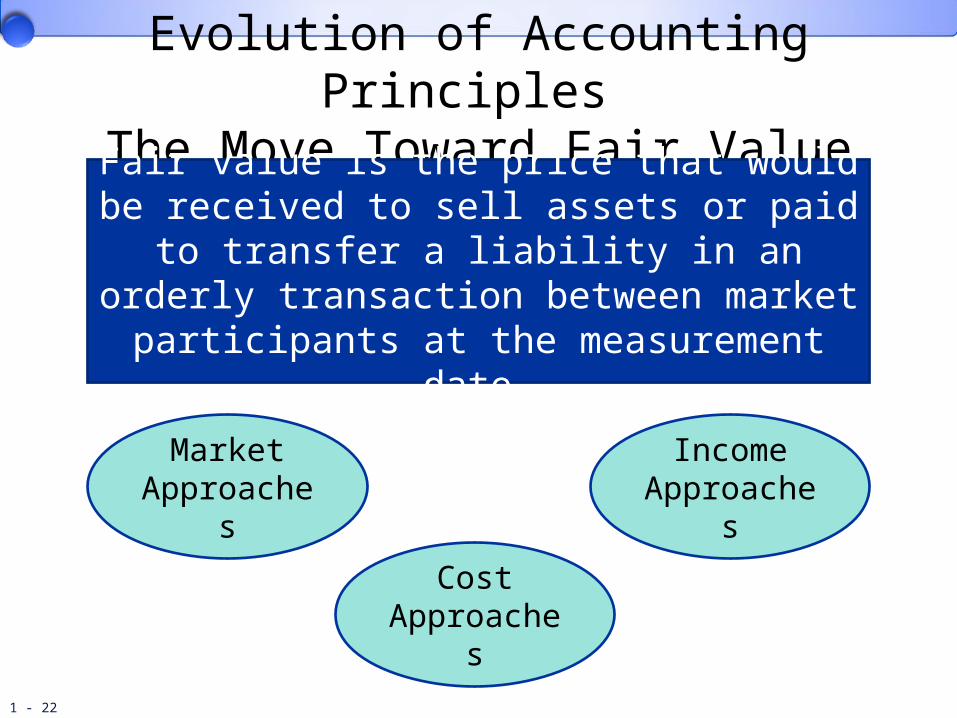

Evolution of Accounting Principles The Move Toward Fair Value

Fair value is the price that would be received to sell assets or paid to transfer a liability in

an orderly transaction between market participants at the measurement date.

Market Approaches

Income Approaches

CostApproaches

1 - 23

Fair Value Hierarchy

GAAP gives companies the option to report some or all of their financial assets and liabilities at fair value.