contractual considerations by kylie van heerden

TRANSCRIPT

Contractual Considerations:

Structuring Commercial

Relationships and Associated

Agreements to Suit your

Needs

Kylie van Heerden

CONTRACTUAL CONSIDERATIONS Key things to consider in any Product

Development / Research Agreement

• The Project

• Obligations of the Provider

• Fees and Payment

• Intellectual Property

• Confidentiality

• Insurance and Indemnity

• Termination

• Dispute Resolution

The Project

1. Scope:

• What are you wanting to achieve / what are you

asking of the Provider?

2. Term:

• How long is the Project likely to take?

• Is there a fixed or required timeframe?

• Are there milestones to be met?

3. Supervision:

• Who has general responsibility for the Project?

• What level of involvement do you want / how frequently do you want to be kept up

to date?

Key Obligations of the Provider

• Standard of care / compliance with applicable

laws and regulations.

• Recording of results.

• Reporting requirements.

• Responsibility for outgoings.

Fees and Payment

• Fixed fees / staged fees based on milestones /

success fees?

• Who is responsible for expenses such as travel

and other incidentals?

• Is any external funding being provided

(e.g. MBIE funding)?

Intellectual Property

• Ownership of Background IP (e.g. each party

retains ownership)

• Licence to use Background IP? If so, on what

terms?

• Who owns Project IP?

• Licence to use Project IP? If so, on what terms?

• Are there any rights of publication granted to the

Provider (e.g. if project forms part of a Thesis)?

Confidentiality

• Each party to observe obligations of

confidentiality.

• No unauthorised disclosure.

• No competition.

• Exceptions (e.g. where information is in the

public domain).

Insurance and Indemnity

• Public liability insurance / minimum

requirements?

• Indemnity for loss resulting from breach?

• Unlimited or limited liability?

Termination

• Grounds for termination?

• Consequences of termination?

• Reconciliation of fees paid?

Dispute Resolution

• Negotiation

• Mediation

• Arbitration

• Court proceedings

STRUCTURAL OPTIONS

Often a company will get to a point where they no

longer want to, or are able to, take their vision to

the next step alone.

There are various structural options, and the right

structure will depend on a number of factors,

including capital requirements, tax considerations,

number of interested parties, Government funding

requirements etc….

For the purpose of this presentation we will look at

three of the more popular structures:

• Incorporated Joint Venture

• Unincorporated Joint Venture

• Limited Partnership

Incorporated Joint Venture

Shareholder 1 Shareholder 2 Shareholder 3 Shareholder 4 Shareholder 5

Joint Venture Company

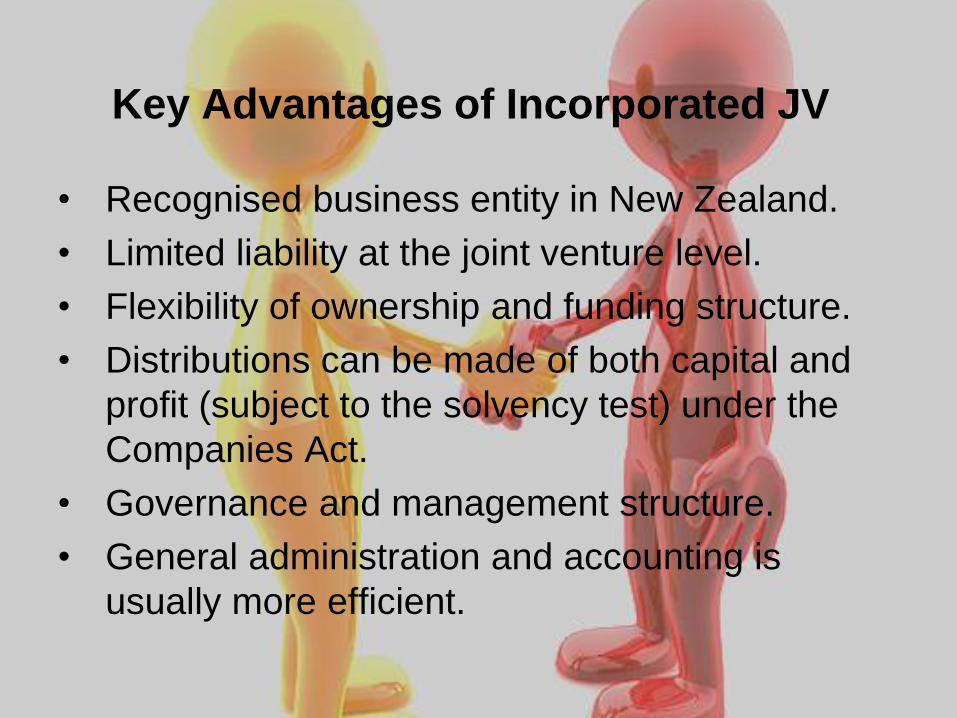

Key Advantages of Incorporated JV

• Recognised business entity in New Zealand.

• Limited liability at the joint venture level.

• Flexibility of ownership and funding structure.

• Distributions can be made of both capital and

profit (subject to the solvency test) under the

Companies Act.

• Governance and management structure.

• General administration and accounting is

usually more efficient.

Key Disadvantages of Incorporated JV

• Inability to pass losses through to the

shareholders.

• Compliance with continuity of ownership

requirements before a company can carry

forward losses and imputation credits (this

makes a company vulnerable to ownership

changes).

• Capital gains cannot be distributed to resident

shareholders without a further tax impost, other

than on the winding up of the company/through

a company share buy-back.

Unincorporated Joint Venture

Participant 1 Participant 2 Participant 3

Key Advantages of Unincorporated JV

• Typically, each party is only liable for its

proportionate share of the joint venture’s

liabilities.

• Tax losses incurred are received by the parties,

and depreciation and interest costs can be

claimed directly by the parties.

• Imputation credits are generated in the correct

entity.

• Capital gains are received by the parties without

any tax on dividends.

• The joint venture has no separate legal

personality and therefore is not required to file a

tax return.

• Each party is effectively obliged to return its

proportionate share of joint venture income and

is assessed on an individual basis.

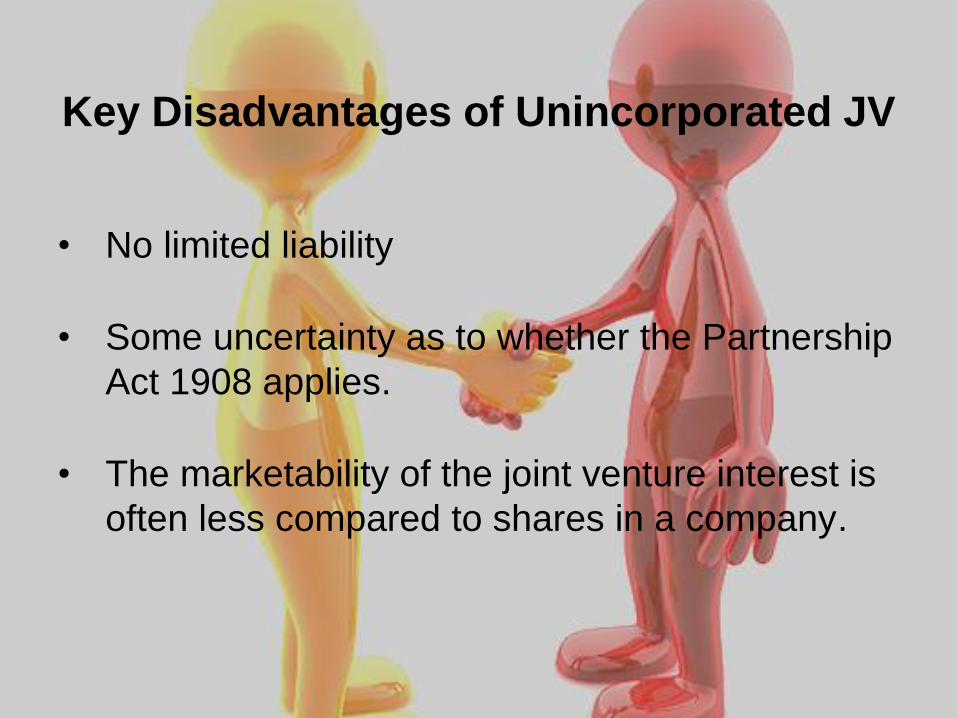

Key Disadvantages of Unincorporated JV

• No limited liability

• Some uncertainty as to whether the Partnership

Act 1908 applies.

• The marketability of the joint venture interest is

often less compared to shares in a company.

• The ability to finance the joint venture

itself or a joint venture interest through

lending institutions is often more difficult.

• Capital gains cannot be distributed to

resident shareholders without a further tax

impost, other than on the winding up of

the company/through a company share

buy-back.

Limited Partnership

Limited Partner Limited Partner Limited Partner Limited Partner Limited Partner

Limited Partnership General Partner

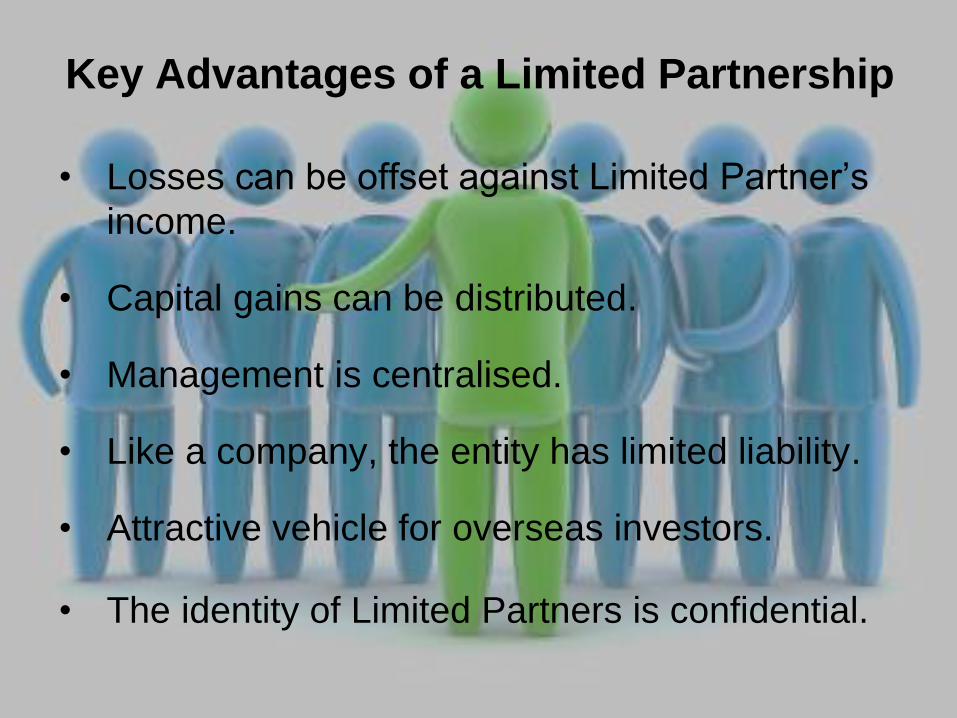

Key Advantages of a Limited Partnership

• Losses can be offset against Limited Partner’s

income.

• Capital gains can be distributed.

• Management is centralised.

• Like a company, the entity has limited liability.

• Attractive vehicle for overseas investors.

• The identity of Limited Partners is confidential.

Key Disadvantages of a Limited

Partnership

• Structure is slightly more complex than a

company.

• Limited Partners can not participate in the

management of the entity (although they can by

wearing a different hat).

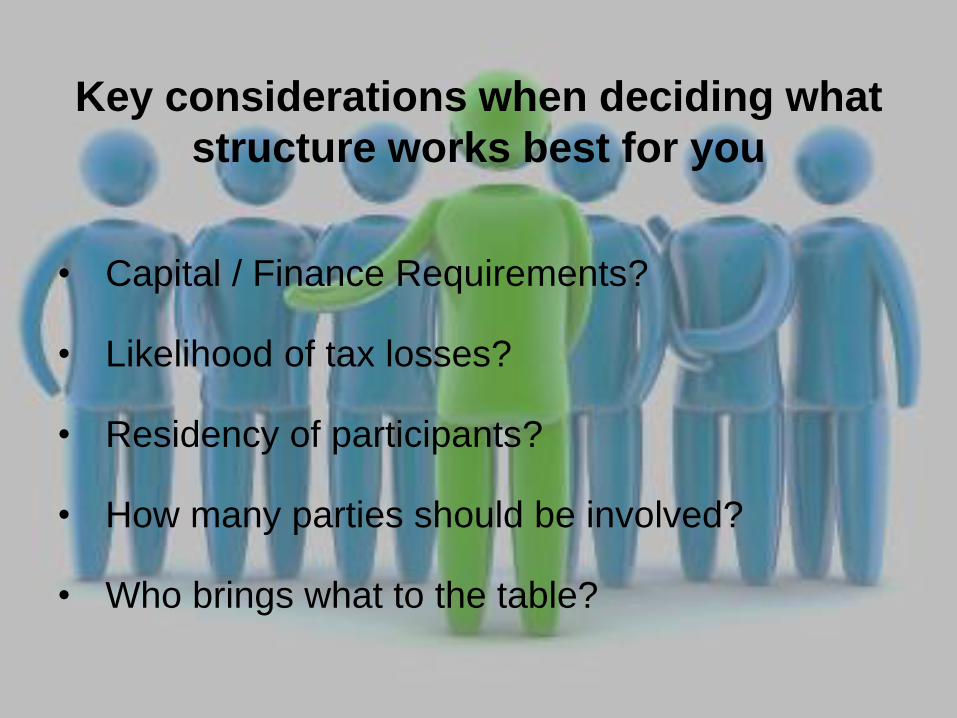

Key considerations when deciding what

structure works best for you

• Capital / Finance Requirements?

• Likelihood of tax losses?

• Residency of participants?

• How many parties should be involved?

• Who brings what to the table?

• The value of each party’s contribution (be it

financial or otherwise)?

• Is the venture a one off project or an on-going

business relationship?

• What sort of management structure is favoured

(i.e. a formal board or an informal management

committee)?

FURTHER ASSISTANCE

For further advice on the legal aspects associated

with taking your product / business to the next

level, please contact:

Kylie van Heerden

Partner

Sharp Tudhope

DDI: (07) 928 0777

Email: [email protected]