commercial market now and then petch gibbons january 26, 2011

TRANSCRIPT

Commercial MarketNow and Then

Petch GibbonsJanuary 26, 2011

Washington, DC Positive Absorption Hit Record Levels

- Occupancy Levels Increasing by 4.3 Million SF- Federal Government Activity and Spending

Sales Activity and Values Soared- The World Bank at 1225 Connecticut Ave NW for $216 Million ($900 psf)

Lots of tenants hunkering down

Northern Virginia The Tale of Two Markets; One Inside the Beltway; One Outside

Investors Lured by Financially Stable, Fully Leased, Quality Office Properties

Slow and Steady Recovery is Projected for Northern Virginia in 2011 with Tighter Markets Inside the Beltway

Suburban Maryland Bethesda Brings Suburban Maryland Office Market into Solid Recovery Mode

Government/Contractors Responsible for The Largest Transactions.

Southern Montgomery County Leads the Office Market Recovery in 2011

Tell ‘em what you’re going to tell ‘em!

A Record-Breaking Year for Absorption Downtown while the Suburbs turn Positive

Government Activity was Responsible for Most of the Demand in 2010 in all Markets

Private Sector Activity Led by:

Law firms (Core DC markets) Consulting, Technology (Northern VA) Consulting, Accounting (Suburban MD)

Absorption (msf)

3

Source: Cushman & Wakefield Research

* Overall absorption is defined as the change in occupied built space for a given period of time, including sublease space within five years.

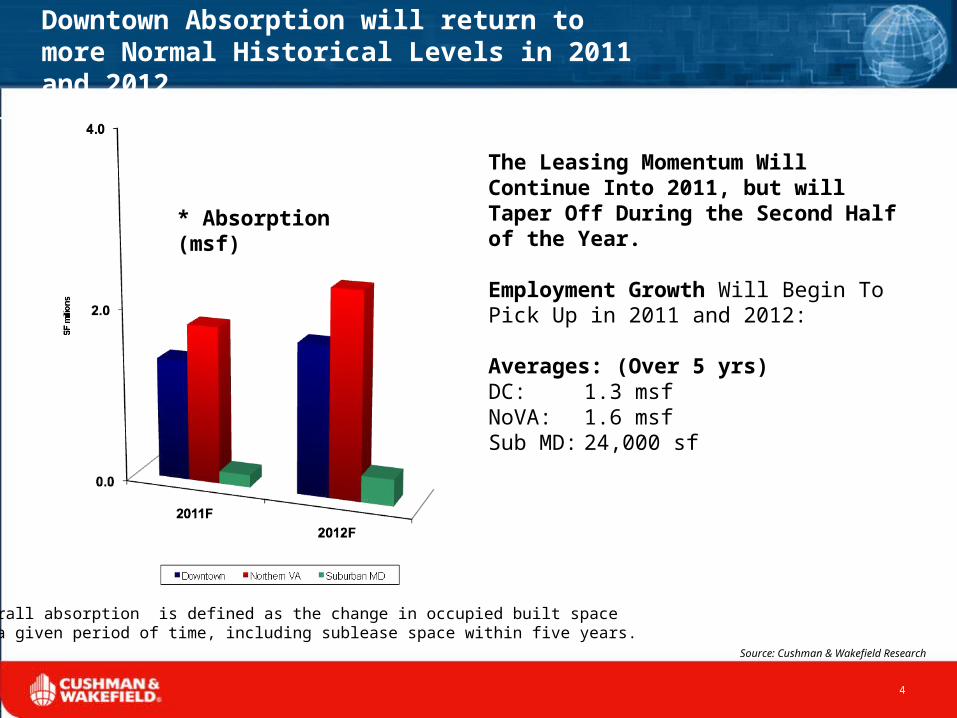

Downtown Absorption will return to more Normal Historical Levels in 2011 and 2012

The Leasing Momentum Will Continue Into 2011, but will Taper Off During the Second Half of the Year.

Employment Growth Will Begin To Pick Up in 2011 and 2012:

Averages: (Over 5 yrs)DC: 1.3 msfNoVA: 1.6 msfSub MD: 24,000 sf

* Absorption (msf)

4

Source: Cushman & Wakefield Research

* Overall absorption is defined as the change in occupied built space for a given period of time, including sublease space within five years.

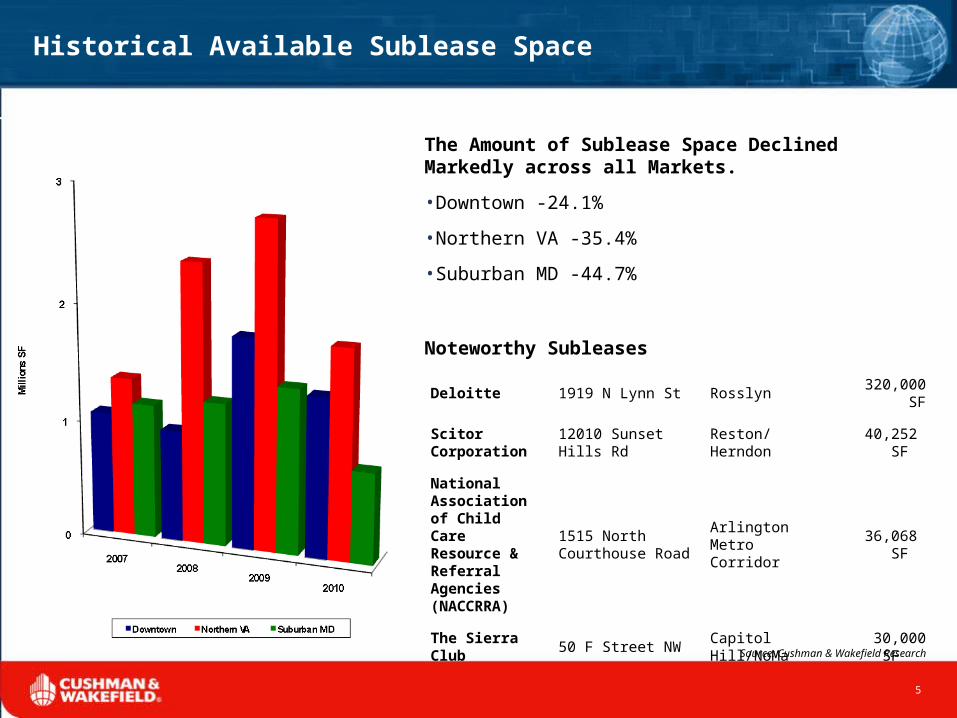

Historical Available Sublease Space

5

The Amount of Sublease Space Declined Markedly across all Markets.

•Downtown -24.1%

•Northern VA -35.4%

•Suburban MD -44.7%

Noteworthy Subleases

Source: Cushman & Wakefield Research

Deloitte 1919 N Lynn St Rosslyn 320,000 SF

Scitor Corporation 12010 Sunset Hills Rd Reston/Herndon 40,252 SF

National Association of Child Care Resource & Referral Agencies (NACCRRA)

1515 North Courthouse Road

Arlington Metro Corridor 36,068 SF

The Sierra Club 50 F Street NW Capitol Hill/NoMa 30,000 SF

Building Submarket Tenant SF

Shady Grove Life Sciences Center North Rockville National Cancer Institute 575,000

7700-7720 Hubble Dr. Greenbelt TRAX International (on behalf of NASA) 120,000

45 W. Gude Dr. North Rockville Montgomery County Board of Education

113,845

7501 Wisconsin Ave. Bethesda/Chevy Chase The Reznick Group 105,000

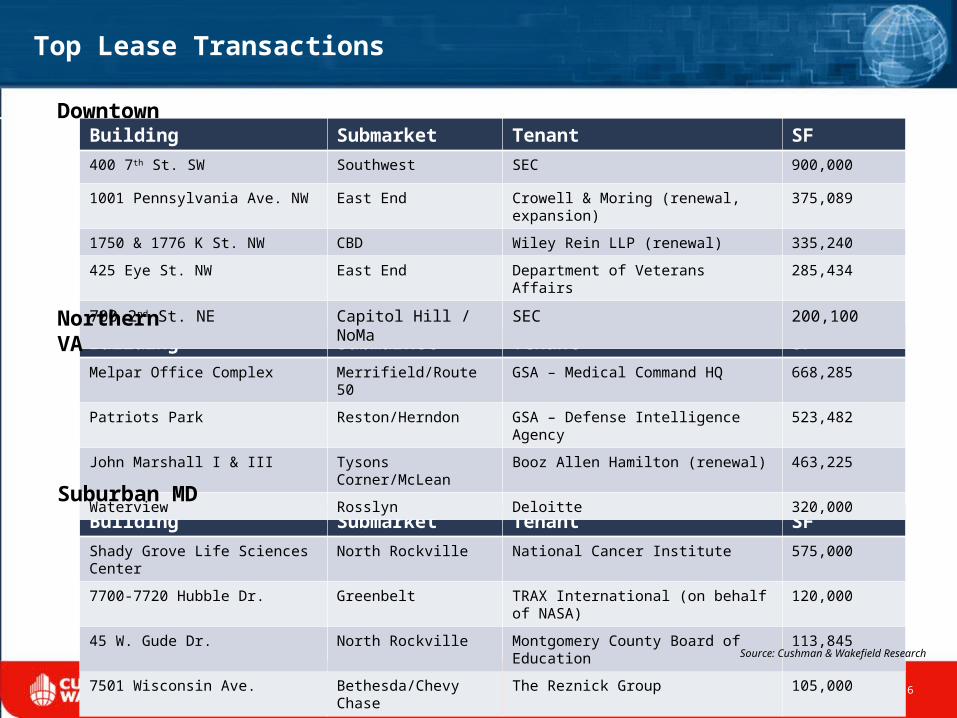

Top Lease Transactions

Downtown

Building Submarket Tenant SF

Melpar Office Complex Merrifield/Route 50 GSA – Medical Command HQ 668,285

Patriots Park Reston/Herndon GSA – Defense Intelligence Agency 523,482

John Marshall I & III Tysons Corner/McLean Booz Allen Hamilton (renewal) 463,225

Waterview Rosslyn Deloitte 320,000

Building Submarket Tenant SF

400 7th St. SW Southwest SEC 900,000

1001 Pennsylvania Ave. NW East End Crowell & Moring (renewal, expansion) 375,089

1750 & 1776 K St. NW CBD Wiley Rein LLP (renewal) 335,240

425 Eye St. NW East End Department of Veterans Affairs 285,434

700 2nd St. NE Capitol Hill / NoMa SEC 200,100

Northern VA

Suburban MD

6

Source: Cushman & Wakefield Research

Other Renewals

Building Submarket Tenant SF

John Marshall I & III Tysons Corner/McLeanBooz Allen Hamilton (renewal)

463,225

Washington Technology Park Route 28 South/ChantillyComputer Sciences Corporation (renewal)

257,485

Hunters BranchFairfax/Oakton/Vienna

ICF Consulting (renewal/expansion) 201,707

370 L'Enfant Plaza SWSouthwest Department of Health & Human Services 185,120

470-490 L'Enfant Plaza SWSouthwest National Transportation Safety Board 179,519

7

Source: Cushman & Wakefield Research

Vacancy Rates remained Elevated from their Pre-Recession Levels…

Submarkets with low 2010 vacancy rates:

East End 10.4%

Ballston 4.2%

Bethesda/Chevy Chase 10.5%

8

Source: Cushman & Wakefield Research

…but will Continue to Inch Down in 2011 and 2012

Very Few Construction Completions Help Vacancy Rates Tighten.

In Downtown and Suburban Maryland Vacancy Rates Will Remain Well Above10-year Averages:

10 Year Average Vacancy Rate

Downtown 7.9%

Northern VA 12.9%

Suburban MD 12.3%

9

Source: Cushman & Wakefield Research

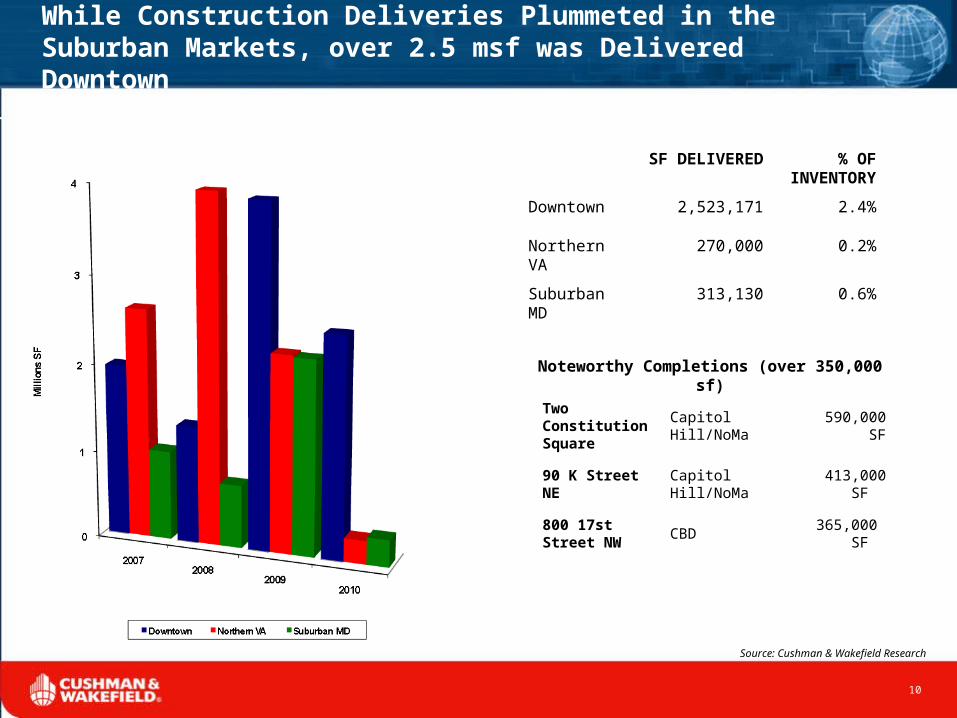

While Construction Deliveries Plummeted in the Suburban Markets, over 2.5 msf was Delivered Downtown

10

SF DELIVERED

% OF INVENTORY

Downtown 2,523,171 2.4%

Northern VA 270,000 0.2%

Suburban MD 313,130 0.6%

Source: Cushman & Wakefield Research

Two Constitution Square Capitol Hill/NoMa 590,000 SF

90 K Street NE Capitol Hill/NoMa 413,000 SF

800 17st Street NW CBD 365,000 SF

Noteworthy Completions (over 350,000 sf)

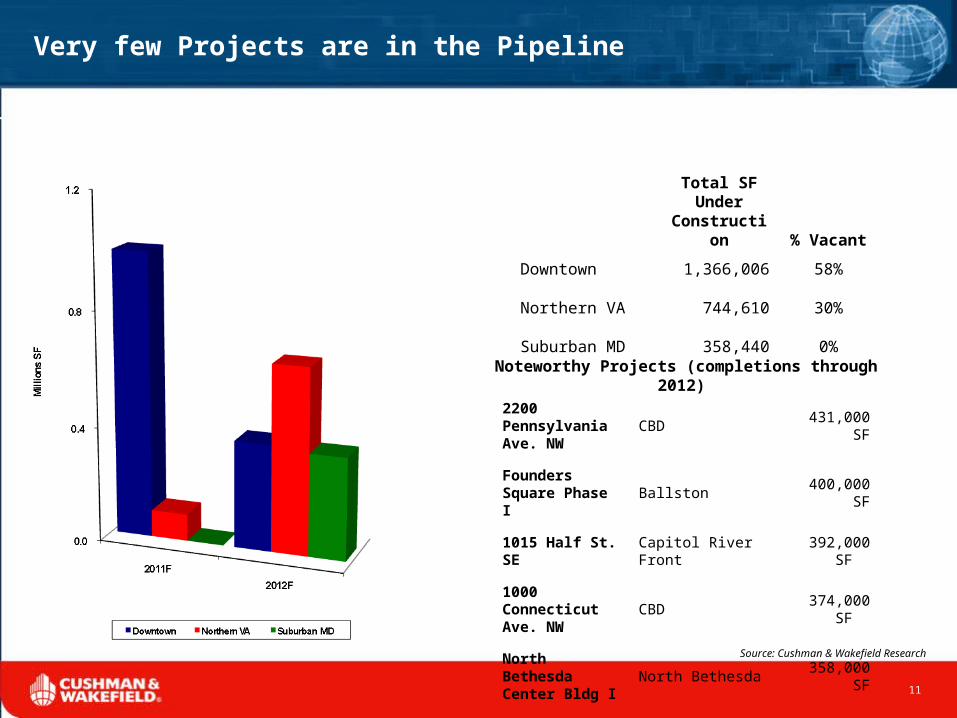

Very few Projects are in the Pipeline

11

Total SF Under

Construction % Vacant

Downtown 1,366,006 58%

Northern VA 744,610 30%

Suburban MD 358,440 0%

Source: Cushman & Wakefield Research

2200 Pennsylvania Ave. NW CBD 431,000 SF

Founders Square Phase I Ballston 400,000 SF

1015 Half St. SE Capitol River Front 392,000 SF

1000 Connecticut Ave. NW CBD 374,000 SF

North Bethesda Center Bldg I North Bethesda 358,000 SF

Noteworthy Projects (completions through 2012)

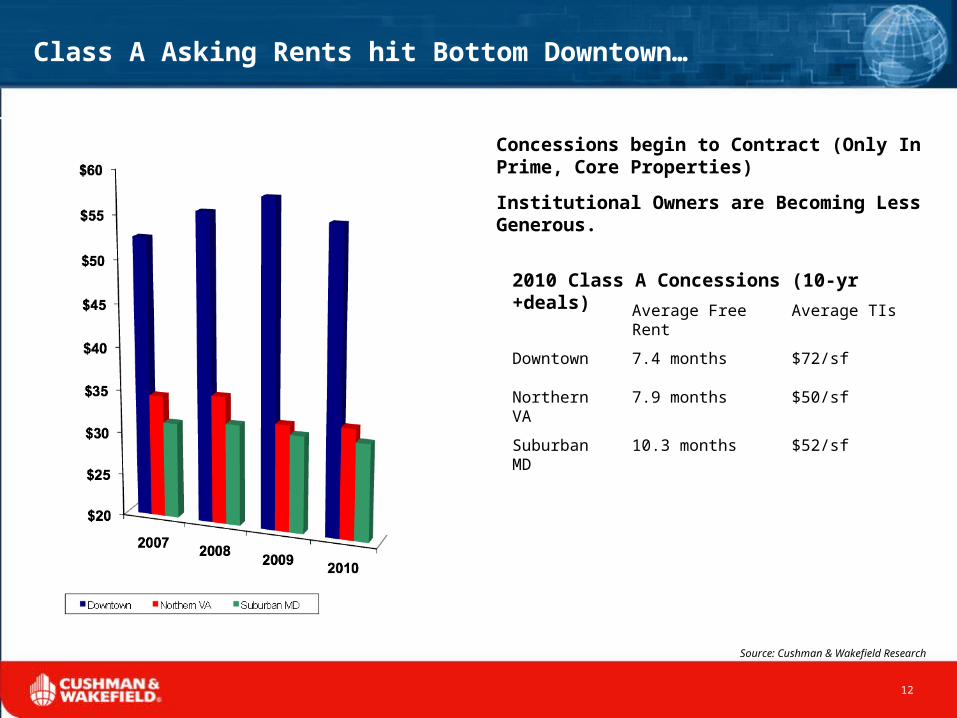

Class A Asking Rents hit Bottom Downtown…

Concessions begin to Contract (Only In Prime, Core Properties)

Institutional Owners are Becoming Less Generous.

12

Average Free Rent Average TIs

Downtown 7.4 months $72/sf

Northern VA 7.9 months $50/sf

Suburban MD 10.3 months $52/sf

2010 Class A Concessions (10-yr +deals)

Source: Cushman & Wakefield Research

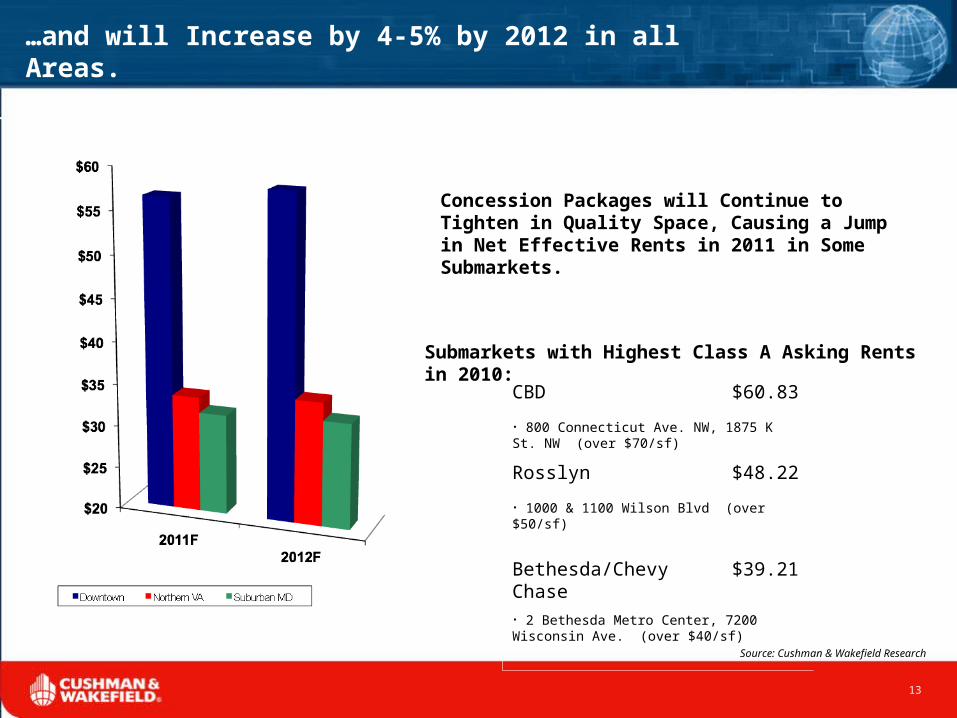

…and will Increase by 4-5% by 2012 in all Areas.

Concession Packages will Continue to Tighten in Quality Space, Causing a Jump in Net Effective Rents in 2011 in Some Submarkets.

13

Submarkets with Highest Class A Asking Rents in 2010: CBD $60.83

• 800 Connecticut Ave. NW, 1875 K St. NW (over $70/sf)

Rosslyn $48.22

• 1000 & 1100 Wilson Blvd (over $50/sf)

Bethesda/Chevy Chase $39.21

• 2 Bethesda Metro Center, 7200 Wisconsin Ave. (over $40/sf)

Source: Cushman & Wakefield Research

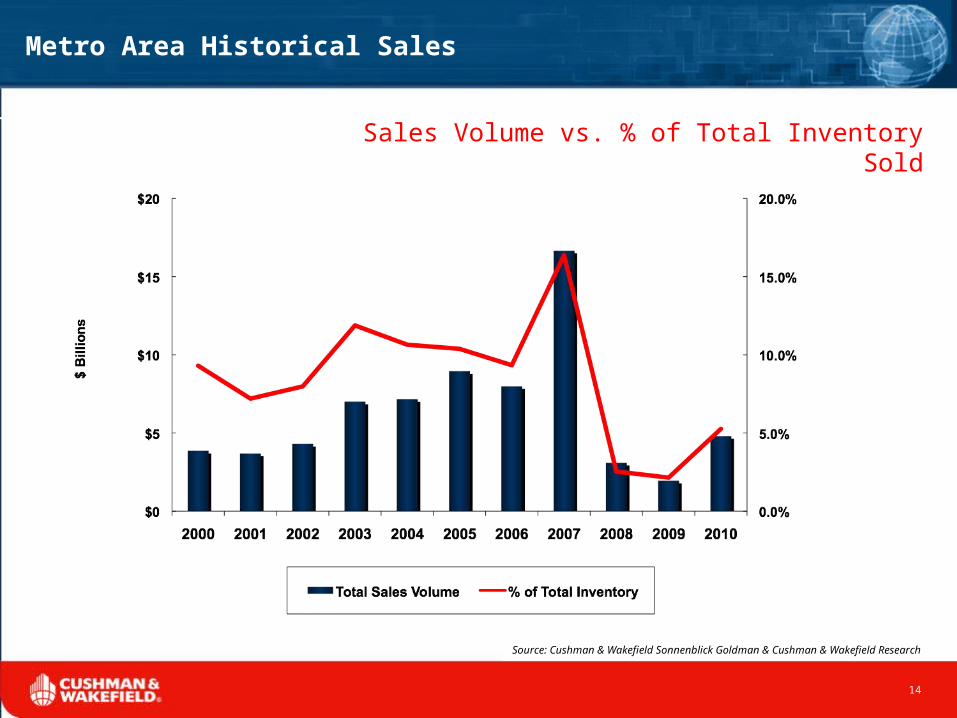

Metro Area Historical Sales

Sales Volume vs. % of Total Inventory Sold

Source: Cushman & Wakefield Sonnenblick Goldman & Cushman & Wakefield Research

14

Historical Sales Activity

Source: Cushman & Wakefield Sonnenblick Goldman & Cushman & Wakefield Research

Historical Sales (Washington, DC Metro 2000 - 2010)

Year Total Sales Volume $/psf Total SF % of Inventory # of Bldgs

2000 $3,862,477,644 $184.48 20,937,241 9.3% 124

2001 $3,689,443,116 $215.74 17,101,617 7.2% 105

2002 $4,301,725,504 $218.12 19,721,592 8.0% 106

2003 $7,004,205,648 $232.03 30,187,153 11.9% 170

2004 $7,165,640,289 $259.75 27,586,452 10.6% 179

2005 $8,952,360,458 $332.70 26,908,083 10.4% 127

2006 $7,983,818,446 $318.59 25,059,900 9.3% 193

2007 $16,657,538,696 $371.04 44,894,497 16.4% 265

2008 $3,094,278,879 $438.73 7,052,858 2.5% 47

2009 $1,948,496,982 $318.23 6,122,950 2.1% 36

2010 $4,789,200,959 $311.35 15,381,962 5.3% 89

Total / Avg $69,449,186,621 $288.23 240,954,305 131

15

2010 Significant Office Building Sales

ADDRESS SALES PRICE

DATE BUILT/RENOV

% LEASED SALE DATE NRSFCAP

RATE PRICE PSFSELLER/BUYER COMMENTS

Downtown

World Bank

1225 Connecticut Ave. NWWashington, DC $216,000,000

1967/2008100% November-10 240,000 5.70% $900

Brookfield Office

Properties/The World Bank

World Bank exercised 2008 lease

option; highest psf price Downtown

The Evening Star Building

1101 Pennsylvania Avenue NWWashington, DC $180,000,000

1898/198988% June-10 219,627 5.80% $820 KanAm/TIAA

1899 Pennsylvania Avenue NW

Washington, DC $151,100,000

1915/2002

100% September-10 186,462 5.60% $810

KanAm/Paramount

Group

Northern Virginia

The Hartford Building3101 Wilson Blvd.

Arlington, VA $112,600,000

2003

100% December-10 212,443 6.00% $530

MRP JV Angelo

Gordon/Heitman, LLC

Prior sale June 2009

for $71.5 million

One & Two Potomac Yard2733 & 2777 Crystal Drive

Arlington, VA $241,900,000

2006

97% October-10 621,824 6.30% $389 JPMorgan/USAA

Three Ballston Plaza1100 N Glebe Road

Arlington, VA $120,000,000

1990

92% March-10 308,998 7.30% $388

Massachusetts

Mutual/AEW

Ridges at Quince Orchard

200 Orchard Ridge Dr.Gaithersburg, MD $27,500,000

1989100% December-10 104,025 NA $264

WRIT/MedImmune, LLC

Purchased for occupancy

Redland Corporate Center

520 and 530 Gaither Rd.Rockville, MD $85,000,000

2009

520, 100%; 530, 11% November-10 347,462 8.50% $245

Perseus Realty/ First Potomac Realty Trust 90% stake

Shady Grove Executive Center

9201-9231 Corporate BlvdRockville, MD $60,000,000

1984, 1985 &

198980% March-10 350,388 NA $171

BlackRock / PS Business Parks

Suburban Maryland

Source: Cushman & Wakefield Sonnenblick Goldman & Cushman & Wakefield Research

16

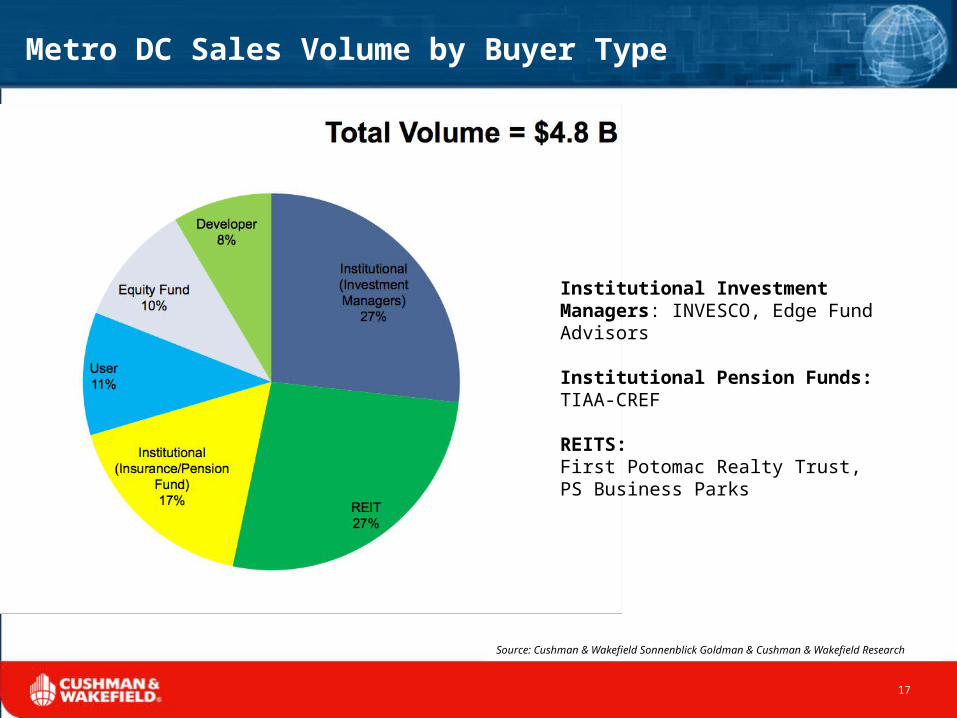

Metro DC Sales Volume by Buyer Type

Source: Cushman & Wakefield Sonnenblick Goldman & Cushman & Wakefield Research

17

Institutional Investment Managers: INVESCO, Edge Fund Advisors Institutional Pension Funds: TIAA-CREF REITS:First Potomac Realty Trust, PS Business Parks

Trends to Watch in 2011

Tenants will continue to hold occupancy costs down.

18

Investors widen their nets outside Downtown, but remain focused on well-located, class A product with good financials.

Slow and steady recovery in Northern Virginia and Suburban Maryland. Downtown returns to normal.

Source: Cushman & Wakefield Research