cmbc tourism report

DESCRIPTION

TRANSCRIPT

1

Tourism, Leisure, Investment and Jobs: Opportunities and Challenges for Calderdale – Draft Final Report

Professor Tom Cannon, University of Liverpool

Summary –

The Tourism Economy in Calderdale

1. The current Tourism economy is worth around £250 Million with almost double that in the closely related cultural, creative

and heritage sectors

2. Sufficient growth has been achieved in the past and

confidence in the area‟s potential exists to make the 5% growth target set by Yorkshire Forward achievable

3. The major assets of the Borough (around which there was considerable agreement) should be prioritized. These are the

natural environment, market towns, heritage and locational/connectivity assets

4. Equally important an array of ventures and facilities had been built up including Eureka!, the Piece Hall, The Minster,

Incredible Edible, Dean Clough, Bankfield Museum, Shibden Hall and Victoria Theatre.

5. Three major issues emerged from the analysis of existing or

developing ventures:

a. There was currently weak connectivity between these

ventures

b. None constituted an “attack brand” capable of

significantly enhancing other offerings

c. The Third Sector through organizations like Eureka!, the

Piece Hall, The Minster, Incredible Edible, Bankfield Museum was very important but vulnerable during a

time of economic restraint

6. The Tourism economy had, however, grown on average at

over 6% pa over the last three years, faster than the target set by Welcome to Yorkshire.

7. The changing structure of support for Tourism locally and across Yorkshire provides a major opportunity to reshape both

policies and strategies to enhance the tourism economy

2

The Potential for The Tourism Economy in Calderdale

8. The economic potential of Tourism in Calderdale is massive; this is well illustrated by the progress and achievements to

date and the identifiable opportunities for the future.

9. Sufficient growth has been achieved in the past and

confidence in the area‟s potential exists to make the 5%

growth target set by Yorkshire Forward achievable

10. The fragmented nature of the Authority‟s Visitor and

Tourist offering – by location and activity – is a major challenge in efforts to achieve their full potential

11. The profile of Tourism reflects and enhances the diversified nature of Calderdale providing the capacity to

enhance jobs, business development and innovation in all postcode areas

12. Shifting the balance of activity in the medium to long term to more focused and directed support could add a

further £100M to the tourism and related economies in the short to medium term

13. Growth of this order can generate upwards of 3,000 new jobs (depending on the profile of businesses, skills and

capabilities) and play a key role in the wider economic

development and regeneration strategies locally

14. Small, medium sized and growing firms can to play an

especially important role across Calderdale

15. The third sector or social economy already plays a key

role and is capable of expanding and developing its role(s)

16. Downstream developments in the creative and cultural

industries linked to tourism are important and should be prioritized in wider economic development and regeneration

programmes

17. Preliminary work identified relatively low morale and

concerns about the effective marketing and promotion of the Calderdale or more local destinations among tourism or visitor

focused venture. These issues and ways of addressing them require closer analysis

18. The greatest prospects for growth lie in:

a) The immediate catchment areas of Manchester, East Lancashire, (other) West Yorkshire and Greater Leeds

b) Broadening the local visitor base, learning the lessons of successes like Hebden Bridge or Incredible Edible and

3

transferring these to other locations such as

Mytholmroyd and new ventures

c) Gaining a higher profile in Pennine Yorkshire and

Welcome to Yorkshire promotions

Building the Action Plan – Key Issues

19. A Tourism Action plan drawing together short/medium

term and medium/long term priorities and developments is a priority

20. A “portfolio” approach to presenting the Tourism offer is recommended which highlights the importance of the major

locational, environmental and heritage assets, while recognizing the difficulty of building a sustainable Calderdale

tourism brand

21. Building the Calderdale brand Portfolio is crucial to this

Action Plan

22. There is, however, little support for building the Tourism

strategy around the Calderdale “brand.”

23. Establishing and developing a local Tourism Board with

strong private and third sector engagement is crucial

24. Engagement with the Tourism business and related

communities though the Tourism Board is vital

25. The work of the Board should be complemented by a more broadly based Tourism Partnership

26. Infrastructure development is key – from micro-signage and local information, through better links between key

facilities to capacity in hotels, guest houses and B&Bs

27. Investment in the people skills and competence is

necessary to deliver the quality offerings – especially in customer service - that are essential to success not only in

the tourism sector but in the key related culture, heritage and creative sectors

28. Small, medium sized and growing firms can play an especially important role across Calderdale, but delivering

their potential seems likely to need:

a. Greater attention to supply chain policies

b. More co-operation between SMEs

c. Support for investment in new technologies, notably IT

d. Effective people development

4

29. The priority is to develop and deliver initiatives that

meet the needs of the sector as defined by the sector and achievable within restricted resources

30. Building effective local partnerships with other stakeholders, notably the private sector is crucial to delivering

the Authority‟s goals in the Visitor and Tourist1 economy

31. Lifestyle analysis undertake by the Yorkshire Tourist

Board may provide important clues to valuable initiatives and target markets

32. Enhancing the links between the visitor, tourist economies with the related culture, heritage and creative

economies is crucial

33. The identification and development of appropriate

tourism “attack brands” especially those capable to reinforcing

the wider “destination marketing” strategy requires close study

34. The E-tourism potential and barriers to achieving this potential is an important element in this analysis

35. Effective implementation of the Action Plan is the key to short, medium and long term success.

36. In the Short to Medium Term the Action Plan should prioritise

a. Activity holidays

b. Better and lower cost promotion of the available

accommodation

c. A stronger and nationally focused events and festivals

programme

d. Building clearer links and better connectivity between

existing amenities like the Minster and ventures such as

Eureka

e. Better local information services for tourism and related

businesses

f. Gaining a higher profile in Pennine Yorkshire and

Welcome to Yorkshire promotions

g. Better integration between the Tourism, Creative,

Culture and Heritage offerings.

37. In the Medium to Long Term the Action Plan should

prioritise

1 Visitor and Tourist are often used interchangeably in this review

5

a. Addressing the accommodation issue

b. Shifting the Visitor profile from low spending, short stay visitors to higher spending, longer stay visitors

c. Improving the skills, competences and capabilities of the Tourism workforce is a priority

d. The creation of one or more “attack brands” in the form of facilities, events, festivals or events is crucial

e. This latter calls for a sustained programme of innovation and creativity to incorporate new ideas, new businesses

and related developments

f. The development of the Piece Hall

6

Introduction and Remit

This report is the result of a programme of research designed to address a series of specific questions centering around Calderdale

Council‟s wish to maximise the contribution tourism makes to the economic well being of district. The Council also wants to play its

part in the regional agenda helping the growth of the region‟s visitor economy by 5% year on year.

Within this overall remit the specific tasks were:

1. To review progress with the current Calderdale Tourism Action

Plan, „Setting the Scene, approved in 2006.

2. To assess the current and potential tourism offer within the

Calderdale District and where there is the greatest potential for growth.

3. To make recommendations for the development of an Action

Plan identifying which sectors or markets hold the best prospect for delivering growth in the local tourism economy.

4. To make recommendations concerning the marketing of the district‟s tourism offer within the Welcome to Yorkshire brand.

5. To consider and make recommendations for improved corporate working across Council Directorates which impact on the

tourism offer or tourism development of the district. (including governance of the tourism agenda)

6. To make recommendations for the development of a group or network to engage with local tourism providers and the private

sector in general.

7. To make recommendations concerning the engagement of the

Calderdale District with Welcome to Yorkshire and the alignment of local and regional priorities.

Core Findings

Progress against the current Calderdale Tourism Action Plan

Real progress was being made in achieving the objectives of the

Calderdale Tourism Action Plan, „Setting the Scene, approved in 2006 in each of the four areas identified. The Tourism economy had

grown on average at over 6% pa, faster than the target set by Welcome to Yorkshire.

There were, however, real problems in defining and implementing a “holist strategy” around the Calderdale “brand”. These were made

worse by relatively weak information systems at a local level, inadequate engagement with the private and third sector and

fragmentation of organization and delivery with the Council.

7

The current and potential tourism offer within the Calderdale District

and where there is the greatest potential for growth

There was widespread confidence in the quality of the current

tourism offer within the District and a belief that there was considerable potential for growth in a range of areas.

The quality of the offer was demonstrated on one level by the sustained growth of the sector. Equally important, major

assets existed at a local and an organizational level. There was a great deal agreement that the greatest locational

assets were:

o The Natural Environment

o The market towns with their individual identities and the cultural diversity across Calderdale

o The Heritage assets

o Its location and connectivity by canal, rail and road.

Equally important an array of ventures and facilities had been

built up including Eureka!, the Piece Hall, The Minster, Incredible Edible, Dean Clough, Bankfield Museum, Shibden

Hall and Victoria Theatre.

It was, however, equally clear that the greatest potential for

growth, or the strategies best designed to support growth locationally were either at a Yorkshire or Pennine Yorkshire level or

at a more local level i.e. in the market towns themselves, activities based on the natural environment.

Three major issues emerged from the analysis of existing or developing ventures:

There was currently weak connectivity between these ventures

None constituted an “attack brand” capable of significantly

enhancing other offerings

The Third Sector through organizations like Eureka!, the Piece

Hall, The Minster, Incredible Edible, Bankfield Museum was very important but vulnerable during a time of economic

restraint

Overall, however, there was little support for building the Tourism

strategy around the Calderdale “brand.”

8

Recommendations for the development of an Action Plan identifying

which sectors or markets hold the best prospect for delivering growth in the local tourism economy

At the heart of any efforts to develop an achievable action plan lie three core building blocks:

Greater engagement with the private and third sector through the Calderdale Tourism Board and the Tourism Partnership

A commitment to working with others regionally such as Pennine Yorkshire and Welcome to Yorkshire

A clear focus on a “portfolio” approach based the distinct identities, communities and capabilities within the Borough

not around a unitary Calderdale brand.

In identifying the sectors and/or markets with the greatest

prospects for growth, one must distinguish between the

short/medium term and the medium/long term.

In the short/medium term (especially given the lack of hotel

accommodation) the greatest prospects for growth lie in:

The immediate catchment areas of Manchester, East

Lancashire, (other) West Yorkshire and Greater Leeds

Broadening the local visitor base, learning the lessons of

successes like Hebden Bridge or Incredible Edible and transferring these to other locations such as Mytholmroyd and

new ventures

Gaining a higher profile in Pennine Yorkshire and Welcome to

Yorkshire promotions

Activity holidays

Better and lower cost promotion of the available accommodation

A stronger and nationally focused events and festivals

programme

Building clearer links and better connectivity between existing

amenities and ventures

Better local information services for tourism and related

businesses

Better integration between the Tourism, Creative, Culture and

Heritage offerings.

In the medium to long term

Addressing the accommodation issue is a priority

9

This, in turn, will facilitate a shift in the Visitor profile from low

spending, short stay visitors to higher spending, longer stay visitors

Improving the skills, competences and capabilities of the Tourism workforce is a priority

The creation of one or more “attack brands” in the form of facilities, events, festivals or events is crucial

This latter calls for a sustained programme of innovation and creativity to incorporate new ideas, new businesses and

related developments

The development of the Piece Hall was a recurrent theme in

discussions of the longer term. This appears to have special, but largely undefined (to date) potential as an “attack brand”,

“a world heritage site” and a “tourism hub”

The new rail link to London offers the scope to widen the areas catchment nationally and internationally.

Marketing of the districts tourism offer within the Welcome to Yorkshire brand

Key aspects of this are addressed above notably:

Gaining a higher profile in Pennine Yorkshire and Welcome to

Yorkshire promotions

Building on the successes like Hebden Bridge or Incredible

Edible and enhancing the profile of other locations such as Mytholmroyd and new ventures

Linking the Calderdale Tourism Board and the Tourism Partnership with complementary structures within the

Welcome to Yorkshire and Pennine Yorkshire brand

At the same time, serious consideration should be given – noting

the weakness of the Calderdale brand - to the Kirklees strategy of

subsuming the Calderdale identity – for promotional purposes – in the wider Pennine Yorkshire brand

Consider and make recommendations for improved corporate working across Council Directorates

There was little support and in some cases substantive criticism of the current division of responsibilities in the organization and

delivery of Council services.

The overall view was the delivery of services should:

Be better integrated

Be client focused

10

Enhance the profile and presence in the market of tourism

Target realizing the full, economic potential of the sector

Make recommendations for the development of a group or network

to engage with local tourism providers and the private sector in general

Creating, supporting and empowering the Calderdale Tourism Board was widely seen as a priority

It was viewed as important to ensure external (to Council) leadership of the Board

The importance of the Third Sector in the provision of tourism offering and services suggests that this group of stakeholders

is well represented of the Board

Alongside the Tourism Board, a larger a looser Tourism

Partnership can be developed

Make recommendations concerning the engagement of the Calderdale District with Welcome to Yorkshire and the alignment of

local and regional priorities

This is covered above

11

Methodology

To deliver these tasks a three part research process was created.

1. Initially a substantial secondary analysis of the research

undertaken into the Tourism economy nationally, regionally and locally and its implications for the future of Tourism in

Calderdale and gaining the maximum economic return and contributing to the growth of the region‟s visitor economy

2. This was followed by a series of in-depth interviews with key players from the public, private and third sectors locally and

key partners at a regional level. The interviewees were agreed between the University and the Borough Council.

3. Subsequently a series of Focus Groups were undertaken with key local stakeholders. These were designed largely to draw

out the views of key local stakeholders, while giving them

some insights into the outcomes emerging from the study.

Outcomes

In real sense, the finding of the research were summarized by one of the private sector participants in the focus groups who found it

“fascinating” to see the “similarities and differences” between the views expressed and perspectives adopted not only in her focus

group but in the other focus groups. These similarities and differences extended across each aspect of the analysis and the

responses to each of the tasks set for the study.

There was broad consensus that real progress was being made in

achieving the objectives of the Calderdale Tourism Action Plan, „Setting the Scene, approved in 2006 in each of the four areas

identified:

1. Business support and advice

2. Marketing and promotion

3. Product development and innovation

4. Representation and strategy

The tourism economy has grown from around £178M (2004-5) to around £250M (2008/9) or just over 6% pa - ahead of the current

Yorkshire Forward target of 5% per annum. At least as important, however, is the view that emerged that there was significant

additional scope for growth if specific strengths were realised and weaknesses addressed.

Assets

The overwhelming view from the in-depth interviews was that the

countryside was the key element in the Calderdale offer. The next

12

most popular choice were the twin assets of Halifax and the Lower

Calder Valley with its wide range of buildings, the Piece Hall and the Minster and the market towns along the Upper Calder Valley. The

latter were seen as providing a different but strong experience to the Halifax offering and giving a different offering to most other

places in Yorkshire and the wider North of England.

This conclusion was broadly reflected in the views expressed in the

Focus Groups where the greatest assets (in no particular order) were commonly described as the natural environment, the market

towns along the Upper Calder Valley and Halifax with the Lower Calder Valley. The key amenities notably Eureka, the Minster, The

Piece Hall, Shibden Hall, Dean Clough, Bankfield Museum and other local attractions

This broadly reflected the conclusion of the Action Plan that the

tourism product of Calderdale (accommodation, attractions, culture, events, countryside) lends itself to two main destination sells: Halifax and the Lower Calder Valley and the market towns along the Upper Calder Valley.

Further analysis of the views expressed raised deeper questions,

first about the nature of the “main destination sells” and then about the delivery of this proposition. This is, perhaps, best illustrated by

the questions raised about whether this twin strategy fully exploits the importance of the countryside offering. This was especially clear

in the Focus Groups. Each of these highlighted the natural

environment as perhaps the greatest asset, while distinguishing this offering from that of both Halifax and the Market Towns, especially

along the Upper Calder Valley.

Besides this, this research highlighted a range of additional,

substantial assets notably:

Heritage – from the Middle Ages (the Minster) through the

Industrial Revolution (confectionery, Mackintosh's; carpets, Crossley) to the modern cultural icons (Ted Hughes, Sylvia

Platt)

Lifestyle and related creative or cultural assets from

Incredible Edible to Guerrilla Gardening

Location was widely mentioned both in the context of good

transport links by both road and rail but also the large catchment area that was within easy reach of the offerings.

Eureka was consistently identified as a strength but only in

certain markets and within relatively narrow focus.

13

Challenges

The wide and diverse array of assets and strengths rapidly emerged as major challenges. These challenges are not only to the delivery

of the 2006 Action Pan, but to the creation of a coherent, relatively integrated strategy or “holistic marketing plan” of the type

described in the Action Plan with its search for the :

Who? - who are the target markets for Calderdale - short

breaks, day trips, young, old, families, couples?

What? - what type of marketing do they like - direct mail, web

based, pieces of print

Where? - where should marketing be targeted - locally,

regionally, nationally, in general press or specialist publications?

Why? - What is the positive message of visiting Calderdale

that we want to put across - why visit - general versus specific reasons

When? - plan should include dates for all types of activity to ensure as integrated and holistic as possible.

How? - what is the best way to attract visitors, what marketing methods will work best.

Calderdale – A Tourism Destination?

Serious questions must be asked about the extent to which

Calderdale as described above can presented as visitor destination in anything other than the technical sense. The strongest brands or

greatest assets appear to be either on a larger or a smaller scale.

Hence, Yorkshire is a powerful brand with high recognition and

substantial promotional investment. During both the in-depth interviews and the Focus Groups there were powerful and coherent

arguments for greater integration of activities and higher levels of

engagement at a cross Yorkshire level. The amount of resource being put behind "Yorkshire" meant that during the in-depth

interviews, people saw an opportunity to ride on those coat-tails.

Pennine Yorkshire was considered by some to have merit as a

"wrap-around" brand but this would require continuing collaborative development with the surrounding local authorities. It was noted on

several occasions that Kirklees have dropped their much of its local tourism identification to support the Pennine Yorkshire brand.

14

Branding and the Kirklees Visitor Guide

Some respondents saw an obsession with boundaries, particularly in relation to surrounding local authorities, which was counter-

productive to fully realizing the area‟s tourism potential.

This theme recurred throughout the Focus Groups with recurrent

calls for greater integration of the local, Calderdale offering(s) with

West Yorkshire / Pennine Yorkshire and Welcome to Yorkshire. It should, however, be noted that respondents were equally clear that

this needed to be a two way street, with the widespread view held that that Calderdale was not getting its fair share of the Welcome to

Yorkshire promotion.

Besides the strength of the Yorkshire brand, efforts at developing a

Calderdale destination brand must face up to the strength of more local offerings. The tourist target market for Hebden Bridge,

Mytholmroyd, and Todmorden may be significantly different from the target market for Halifax and its environs. Equally, those

seeking a canal boat holiday may want a very different Visitor message to those visiting Eureka.

So far, it is clear that the Action Plan aim of developing a holistic marketing plan has not been achieved. The one unifying comment

from the majority of those involved in the in-depth interviews was

that “Calderdale was not a brand that could or should be pushed.”

It was the widely held view that the greatest local successes in the

tourism or visitor economy were at the local or individual (venture or enterprise level). The view was expressed that more could and

should be learned from the successes of locations like Hebden Bridge or ventures like Incredible Edible, the Elsie Whiteley Centre,

Dean Clough and Eureka.

Learning from and disseminating their successes would have

multiple benefits. The most basic are, of course, the regeneration,

15

economic development and job creation returns as the base of the

Visitor economy widens, bringing economic returns to towns like Mytholmroyd, Todmorden, Brighouse and Sowerby Bridge. Equally

important, development of tourism market in these locations would reduce the pressure on locations like Hebden Bridge, where it was

reported that some residents object to the pressure on facilities generated by tourists.

Halifax and its environs were seen to offer specific opportunities and challenges. There was little doubt about the value of existing

offerings like Eureka and Dean Clough nor the potential of the Minster or the Piece Hall. There was, however, a sense that Halifax

currently epitomized the problems of the whole of Calderdale especially the fragmentation of the offering and the lack of obvious

connectivity between them. Some participants commented that “if

you solve the (tourism) problems of Halifax, you solve the (tourism) problems of the whole of Calderdale”.2

The success of ventures like Incredible Edible, the Elsie Whiteley Centre, Dean Clough and Eureka raised further questions which

relate to the importance of learning more from local successes. The most immediate were the calls for greater private and third sector

engagement in shaping and delivering policies and programmes to develop the Visitor economy.

Policies and Programmes

Two distinct proposals emerged from these comments. First, there

was almost universal support for the creation of a Calderdale Tourism Board which brought together the main public, private and

third sector stakeholders in the tourism economy. Just as the unmistakable, was the view that sustaining the commitment and

enthusiasm of the private and third sector members depended on

the Board “not merely being a talking shop” and having real authority.

There were memories that “the whole support structure was withdrawn in a very peremptory manner some years ago”. Equally

strong was the view that a Calderdale Tourism Board should not adopt a “little Calderdale” view of its roles and responsibilities but

look beyond the Borough, actively collaborate at a West Yorkshire / Pennine Yorkshire and Yorkshire level.

The second distinct proposal was for the creation of a Tourism Partnership modeled, in part, on the Creative Industries Partnership

that already exists but working with and through the Tourism Board on some issues that the Calderdale Cultural Partnership currently

2 It should be noted that this view was disputed by some participants

16

undertakes. Its membership would be much looser, while its

priorities would focus more narrowly on issues such as:

Maximising opportunities for joint working with all partners

within the tourism sector and beyond, including the private, voluntary and community sectors

Sharing and disseminating information within the tourism sector

Developing effective relationships across the tourism sector in Calderdale – private, public, voluntary and community and

other tourism stakeholders

Advising the Tourist Board on the tourism indicators and

associated indicators in the Calderdale Futures Plan 2006-2016

Acting as a representative voice of the private and third

sectors across the Borough

Promoting recognition for the significant contribution of

tourism in enhancing the economic, social, educational and environmental life of the Borough

Harnessing the views, skills and aspirations of all the stakeholders in the Visitor economy of the Borough

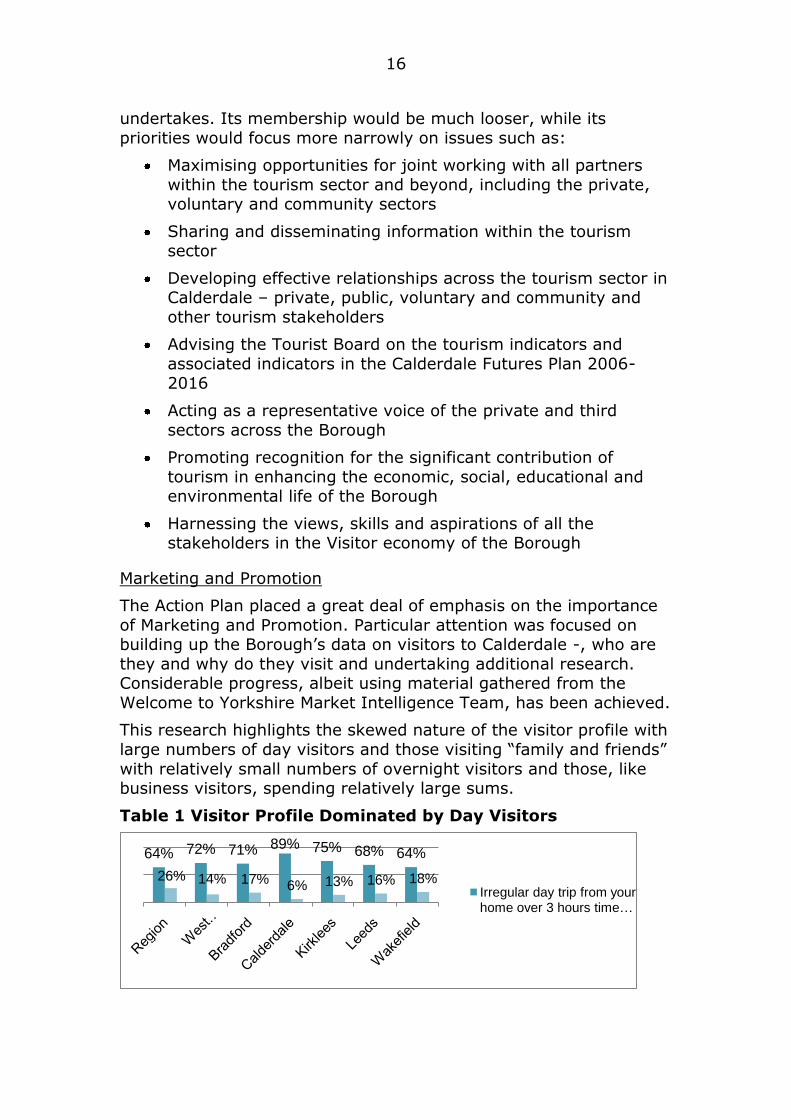

Marketing and Promotion

The Action Plan placed a great deal of emphasis on the importance

of Marketing and Promotion. Particular attention was focused on building up the Borough‟s data on visitors to Calderdale -, who are

they and why do they visit and undertaking additional research. Considerable progress, albeit using material gathered from the

Welcome to Yorkshire Market Intelligence Team, has been achieved.

This research highlights the skewed nature of the visitor profile with

large numbers of day visitors and those visiting “family and friends”

with relatively small numbers of overnight visitors and those, like business visitors, spending relatively large sums.

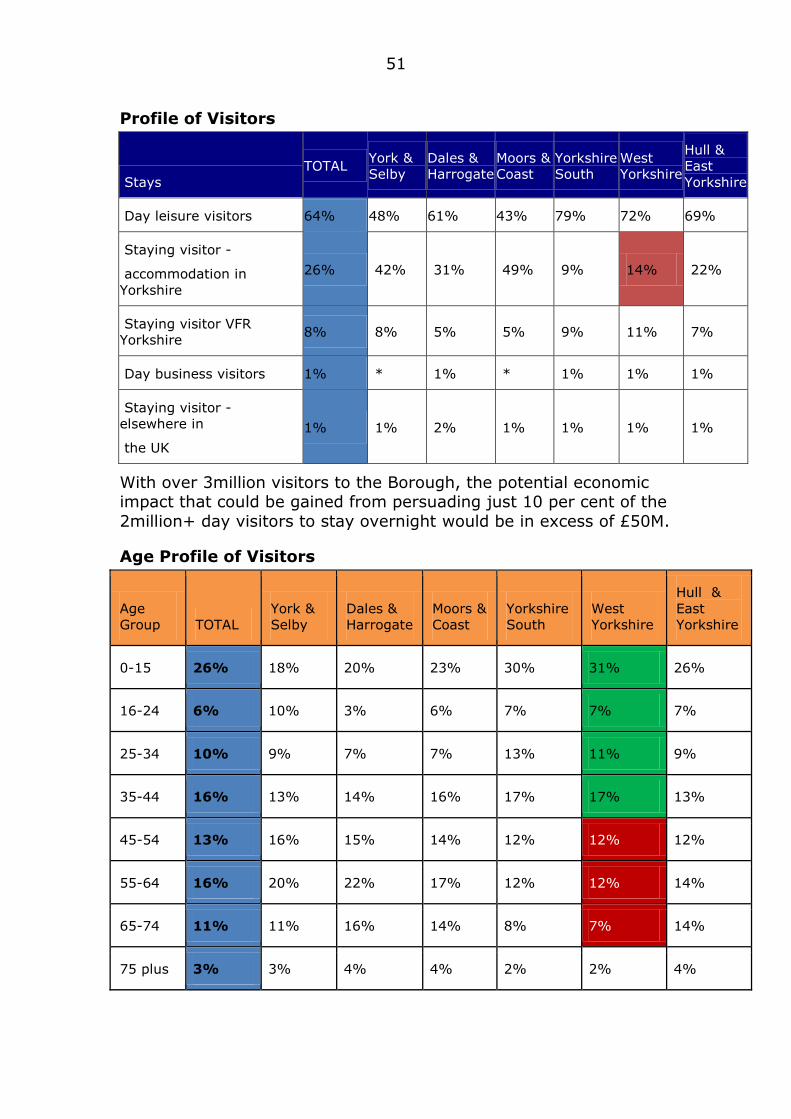

Table 1 Visitor Profile Dominated by Day Visitors

64% 72% 71% 89% 75% 68% 64%

26% 14% 17% 6% 13% 16% 18%Irregular day trip from your home over 3 hours time …

17

Perhaps the most striking feature of the Welcome to Yorkshire

Market Intelligence Team data was the lack of visitors from London and the high proportion of visitors from the North West (see table

2).

Table 2 Source of Day Visitors

Source: West Yorkshire Regional Visitor Survey 08/09 Results

There is, however, a continuing lack of substantive, time-series data

at the micro level on visitors to the key, target local communities at either the level indicated in the Action Plan - Halifax and the Lower

Calder Valley and the market towns along the Upper Calder Valley.

Some data is gathered locally or by specific enterprises but this is not collated at a Borough level. The distinctive nature of the

communities – from Brighouse and Elland, through Halifax to Hebden Bridge, Mytholmroyd and Todmorden – suggests that the

visitor profiles may differ significantly.

Aspects of these differences, priorities among target communities

and ways of reaching them were raised repeatedly in the in-depth interviews and the focus groups. The size of the potential, “local”

catchment area came up frequently. By road and rail, there are around 7.5M people within an hour‟s travel.

Such a large population is inevitably diverse, which ought to complement the diversity within the Calderdale tourism

communities. Without better data at this level, it is hard to answer the questions asked in the Action Plan on “how do we get

information out”, the balance between local, regional and national

advertising and promotion.

The broad consensus was that the authority should integrate much

more of its “borough” wide promotional effort within the Yorkshire or the Pennine Yorkshire brands, while enabling and facilitating local

18

efforts. This would deliver two further benefits to the Visitor

economy. First, it would capitalize on the “local pride” which was consistently highlighted as a major local asset. Second, it would tap

the commitment to local volunteering as seen in areas like Todmorden. Relatively small sums of money could be used to great

effect at this micro level such as Todmorden Pride.

Product Development and Innovation

The Action Plan placed considerable emphasis on the need for investment in product development and innovation. The plan

highlighted the need for

“A series of small-scale actions relating to immediate,

opportunities for Calderdale to make the most of, its natural, and already existing product

Long, term, over the next 5 years, decisions will have to, be

made as to where to enhance development,, either built (hotels or additional attractions) or, more natural (new

walking and cycling routes) for, the benefit of tourism.”

Some progress has been made especially in developing immediate

opportunities and in specific areas such as developing cycle routes. The integration of bridleways, walking and mountain bike routes

was seen as moving forward positively while the mountain bike and equine interest groups were working together positively.

No Room at the Inn

Few issues generated a greater level of agreement or sense of

concern than the lack of quality hotel, guest-house or related accommodation. During the in-depths, the conclusion was clear –

“the overwhelming weakness (of the tourism offer) was the lack of hotel rooms”. Similar sentiments recurred throughout the focus

groups with even “locals” saying how they had tried and failed to

get quality accommodation for a family holiday.

At every level the “absolute lack of accommodation” and “the

shortage of hotels” was seen as a major constraint on improving the quality of the tourism offer, changing the profile of the local tourism

Todmorden Pride

Taking a practical approach to the regeneration of Todmorden

19

market – from day visitors to overnight stays or from low spenders

to high spenders - and increasing the economic returns from tourism. This problem was seen as especially taxing in those

locations already seeing large numbers of visitors. “Large numbers of short stay/day visitors put more pressure on local amenities like

car parks for little economic gain, than smaller numbers of high value tourists who stay overnight.”

Some, limited changes appear to be occurring. There are reports of an increase in the number of B&Bs and more entrepreneurs opening

small guest houses. Although this is encouraging, disseminating information about them is limited by:

The rules imposed on local Tourism Information Centres

Poor IT skills

The existence of significant numbers of life-style business

Local Tourism Information Centres can only recommend accommodation that meets the England Quality Rose standard and

has been checked out by independent assessors. Similar constraints exist on the accommodation promoted through literature sponsored

by VisitEngland. This inspection can cost around £1,000, which many smaller or lifestyle B&Bs and small guest houses are reluctant

to pay.

The lack of IT skills reflects both a wider sectoral and regional

weakness. People 1st (the Sector Skills Council for the hospitality, leisure, travel and tourism) has identified a range of human

resource, behavioural and skills gaps as among the greatest challenges facing the tourism and related sectors3. The lack of IT

skills poses particular problems for smaller businesses offering accommodation as the number of visitors booking on-line grows.

The overall picture for Yorkshire is mixed with less tourism business

using a computer to assist them operate their business (58% in Yorkshire against 71% nationally).

There was, however, greater use of the web to promote their tourism business (74% within Yorkshire against 62% nationally). An

even greater gap exists between those who can via the Internet without having to contact a member of staff via the phone, fax or e-

mail (48% in Yorkshire only 36% nationally). There is limited disaggregated data for Calderdale or locations across Calderdale.

3 People 1st (2009) Skills priorities for the Hospitality, Leisure, Travel and Tourism

sector Uxbridge

20

Table 3 Booking Accomodation

Source: West Yorkshire Regional Visitor Survey 08/09 Results

It is hard to see how some of the more ambitious long term goals

for tourism in Calderdale can be met – especially those seeking to change the profile of Visitors or encouraging people to “stay longer

and spend more” can be met without addressing the accommodation and skill shortages.

Innovation

Hitherto much of the work in this area falls under the remit of the

WYTP. Calderdale is a very active partner and supports initiatives developing business tourism, group travel and a major rural

campaign. During this programme of research the combination of a growing sense of the distinctiveness of many local offerings and the

need for greater innovation in markets, products and services led to significant interest in locally focused innovations.

These clustered around three areas:

1. Targeting largely untapped, growing or new tourism markets.

1.1. The heritage visitor economy locally provides significant

opportunities for growth. These range from oldest “tourism” market – religious tourism illustrated by the designation of

21

Minster status on the former parish church dedicated to St

John the Baptist.

1.2. The growth of “activity” tourism means that almost

seventy per cent of UK holidays, now involve participation in an outdoor activity and for more than 10% of, holidays;

participation in a specific activity is the main motivation for, the trip. The fastest growth of Activity tourism has been in

Scotland and, Wales but many English destinations including the Lake District, Peak District and Yorkshire, are seeing

growth. Both the Lower and Upper Calder Valley with their bridleways, cycleways, towpaths and “ways” such as the

Calderdale and Pennine Ways.

1.3. “New” tourism areas such as events – the lessons of

Hay-on-Wye were flagged alongside local innovative Festivals

like Halifax Food and Drink Festival at The Piece Hall, Hebden Bridge Arts Festival and the annual Dock Pudding

Competition.

2. Rethinking ways of considering the Visitor or Tourist client

2.1. This has led to a wider move away from traditional socio-economic to more lifestyle type analysis. One approach

classifies tourism customers into four types – Mercenaries, Rebels, Apostles and Capitives - based on their satisfaction or

loyalty. Mercenaries have no loyalty and constantly seek the best deals. Rebels are fickle and unpredictable, apostles have

been converted and will evangelise while captives visit often but for personal reasons e.g. visiting family.

2.2. Other approaches focus on the travel and tourist track and routes followed by tourists. One suggestion was that

significant numbers of tourists travelled a route from Chester

to York through Calderdale. Another highlighted the importance of overseas tourists with an interest in literature

who could be tempted to link visits to the Bronte country of south Pennine with Ted Hughes and Sylvia Plath‟s association

with Hebden Bridge and Mytholmroyd on to Beatrix Potter‟s property in the Lake District.

3. The use of new technologies notably;

3.1. Information technologies to identify, reach and engage

with potential visitors

3.2. Presentational technologies to enhance the visitor

experience

3.3. Amenities such as those linked with extreme sports

Few aspects of the development of the Tourism economy rely more heavily on meaningful representation of the different stakeholder

22

interests and effective support and advice than innovation and the

underlying process of creativity.

Representation, Support and Advice

Representation

Some aspects of the representation of different interest groups have

already been addressed in comments about the creation of a local Tourism Board and the formation of a Tourism Partnership. These

were seen as important mechanisms for ensuring effective representation of the Private and Third Sector in internal (to

Calderdale) policies and programmes. It was felt both within and external to the council that outside bodies should play a major role

in whatever structure was put in place.

The view emerged that the Council (in the terms expressed in the

Action Plan) had played an important representational role up to

now in “influencing the Regional Economic Strategy, discussions over the City Region and Northern Way initiatives”. Complementary

views were expressed about the Council involvement with “the Yorkshire Tourist Board … as well as the West Yorkshire Tourism

Partnership.”

Some participants in the in-depth interviews expressed the view

that “bodies such as West Yorkshire Partnership, Welcome to Yorkshire, England‟s North Country and Visit Britain need more

information about what is happening on the ground in the area. This would help them do a better job but would also make it more likely

that Calderdale got more prominence in marketing materials and campaigns.” Two bodies mentioned in the Action Plan - British

Waterways, the National Trust – were specifically identified during the Focus Groups as requiring stronger engagement with local,

Calderdale interests.

Support and Advice

The Action Plan was quite specific in its proposals on support and

advice. It said that:

“We need to engage with businesses, understand their business and

skills needs, provide advice on business creation, growth and longevity as well as relevant legislation and national/regional,

developments.

We need to establish regular, timely and beneficial communications

with local, business, providing information and the, opportunity to network and learn from others,

23

(We need) the creation, of management information systems, the,

development of a newsletter and annual, networking event, and an audit of training needs.”

In both the In-depth interviews and the Focus Groups it became clear that a high level of engagement with the private and third

sector remains a priority.

At the same time there were concerns that there was too much

fragmentation in the organization and delivery of Council services. “The distribution of roles over different directorates with separate

responsibilities is unhelpful especially in delivering the economic development and regeneration potential of tourism.”

The divided responsibilities within the Council‟s support for tourism was seen to create a number of specific and identifiable problems

notably:

Blurred priorities

Poor connectivity within and beyond the Council. Criticism of

the recent Calderdale Tourism Guide centred on omissions that “could have been avoided” with greater internal cohesion

Weak integration with other parts of the Borough‟s activities

A failure to tackle a range of, seemingly minor, but together

significant problems including;

o Weaknesses in “micro-signage” for example Sylvia

Plath‟s grave St Thomas a Beckett and St Thomas the Apostle Church, Heptonstall, Calderdale or on a larger

scale the links between Eureka, the Piece Hall and the Minster in Halifax

o Lack of parking spaces in key locations and poor signposting to available parking nearby

o Problems of gathering specific local information of the

type identified by Susan Stevens of Shire Cruisers.

There was strong sense that a single or clearly “lead” arm of the

Council would make it easier to ensure the development of themes to make destinations “hang together.” This need for integration of

policy and delivery was expressed in several ways notably:

“We have the (tourism) packages but not the packaging”

“There is a need for a narrative at a local or borough level – telling me why I should come or stay”

In the same way, a more integrated structure would facilitate the identification and promotion of the “hidden gems” that proliferate

across the Borough.

24

The creation of the Calderdale Tourism Board was seen a crucial

element in efforts to integrate the Tourism offering(s) but greater cohesion with the Authority was facilitate this effort significantly.

25

The Wider Context

In England responsibility for tourism policy and resourcing tourism related activities is primarily the responsibility of the Department of

Culture, Media and Sport (DCMS), but the Departments of Communities and Local Government (DCLG) and Business,

Innovation and Skills (BIS) have important roles in the provision of

resources, policies and programmes.

The DCMS and DCLG generally view the leisure, visitor and tourism

economies and the opportunities deriving from them as closely linked. In defining these sectors they note that :

Tourism is generally perceived as holidays or breaks involving time away from home. Leisure is usually perceived to mean

entertainment (in and out-of-home) including most attractions, formal and informal sports and outdoor activities.

Cultural, heritage and hospitality facilities are perceived to overlap both sectors. Tourism is driven by many of the same

forces as leisure. However, it has important characteristics that must be considered:

o Travel is an integral part of tourism whereas in leisure it is generally a means of accessing a desired facility

o Tourism includes business as well as leisure travel

o Leisure (holiday) tourism is often motivated by attractions that are free goods e.g. historic towns,

spectacular scenery and/or assets that are not primarily developed or maintained as tourism businesses,

including most historic buildings. These attractions are not footloose, unlike most leisure activities (and)

o Tourism is not a coherent industry. Rather, it creates economic activity across a wide spectrum of other

industries e.g. transport, hospitality, retailing.

For planning purposes DCLG makes it clear that leisure and tourism

uses need to be considered as two separate sectors while appreciating the significant inter-relationships. The most important

distinction is regularity of use.

Leisure facilities are used on a regular, often spontaneous,

basis from home, as part of an individual‟s normal leisure

time.

Tourism facilities are used on special, generally pre-planned,

non-routine or longer trips including, but not limited to, overnight trips.

26

Although many leisure facilities are used by tourists, and vice-versa,

there are significant differences between the uses as defined here, in terms of their land-use planning effects.

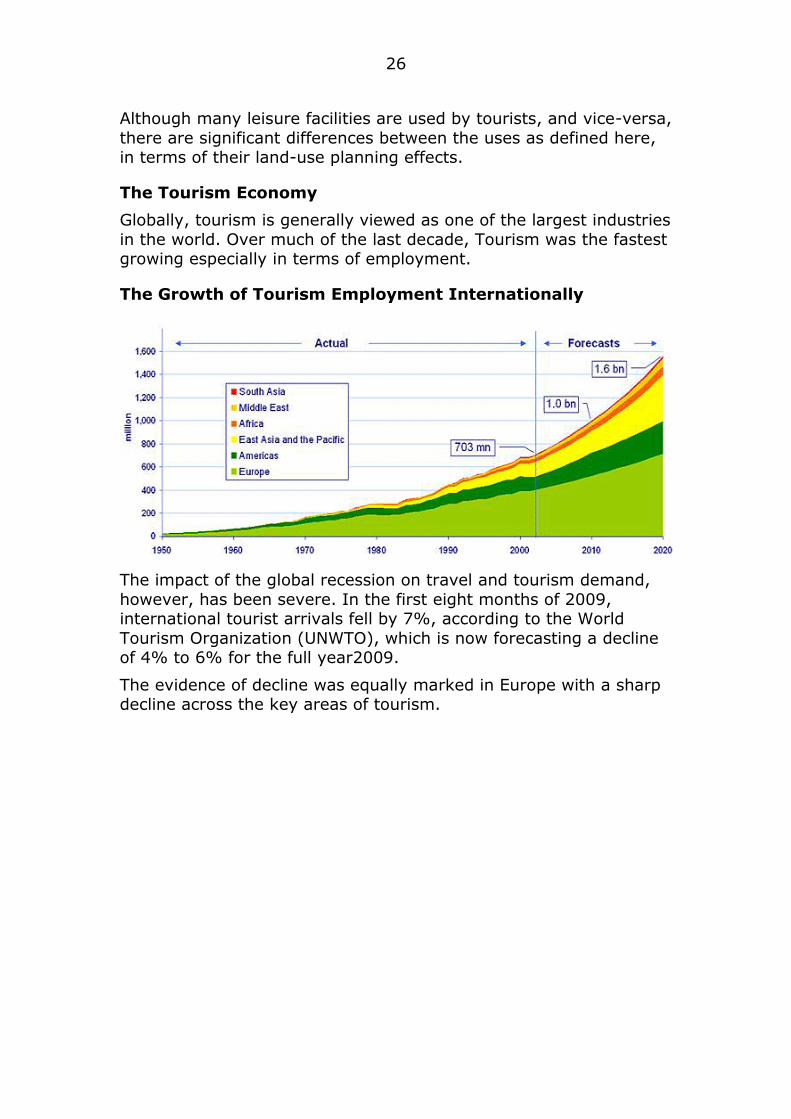

The Tourism Economy

Globally, tourism is generally viewed as one of the largest industries

in the world. Over much of the last decade, Tourism was the fastest growing especially in terms of employment.

The Growth of Tourism Employment Internationally

The impact of the global recession on travel and tourism demand,

however, has been severe. In the first eight months of 2009, international tourist arrivals fell by 7%, according to the World

Tourism Organization (UNWTO), which is now forecasting a decline of 4% to 6% for the full year2009.

The evidence of decline was equally marked in Europe with a sharp decline across the key areas of tourism.

27

Growth returned to international tourism in the last quarter of 2009 contributing to better than expected full-year results.

According to the latest edition of the UNWTO World Tourism Barometer, international tourist arrivals fell by an estimated 4% in

2009. Prospects have, however, improved with arrivals now forecast to grow between 3% and 4% in 2010. This outlook is confirmed by

the remarkable rise of the UNWTO Panel of Experts‟ Confidence Index – “2009 – Last quarter sees return to growth”.

International tourist arrivals for business, leisure and other purposes are estimated to have declined worldwide by 4% in 2009

to 880 million. This represents a slight improvement on the previous estimate as a result of the 2% upswing in the last quarter

of 2009.

There is considerable evidence that UK domestic tourism also saw

significant declines in 2009 but these were partly compensated for a

small growth in international tourism, largely attributed to the weakness of the £ against the Euro. Premium domestic tourism has,

also, been assisted by the reduction in mortgage interest rates.

UNWTO Secretary-General, Taleb Rifai said recently that “the

results of recent months suggest that recovery is underway, and even somewhat earlier and at a stronger pace than initially

expected”. Experience shows that tourism earnings generally follow

28

the trend in arrivals quite closely, even if they suffer somewhat

more in difficult times.

In 2008, the UK tourism industry was estimated to have generated

£85 billion (directly and indirectly) for the UK economy, with 80% coming from the domestic tourism market. This suggests that

tourism contributes just over 3% to national gross value added. In 2008, overseas residents made an estimated 34 million visits to the

UK, generating expenditure of approximately £18 billion.

Employment

In 2008, there were just over 1.5 million people directly employed in tourism (44% in restaurants, bars and canteens and 16% in

tourist accommodation) with more employed indirectly, equal to 5% of all employment in the UK. Although this is believed to have

dropped in 2009, it is expected to recover in 2010.

Employment in tourism

Units 2006 2007 2008 2009

4 2010

Employment in tourism (000s) 1466 1489 1513 1484 1496

of which: Hotels and other tourist accommodation (000s) 237 241 245 245 247

Restaurants, bars, canteens (000s) 638 648 659 642 647

Transport (000s) 136 138 141 140 141

Travel agents/tour operators (000s) 152 154 157 155 157

Recreation services (000s) 86 87 88 85 86

Rest of the economy (000s) 218 221 225 216 217

According to DCLG, tourism (alone) in Britain has a turnover of £53

billion a year (directly). In 2008, there were an estimated 180 000 businesses in tourism industries. International tourist arrivals in the

UK grew by 34% between 2001 and the 2008 total of 33.0 million, while expenditure by tourists in the UK reached £18 billion in 2008,

28% higher than in 2001. The largest origin markets for the UK are the USA which contributed 11.5% of total arrivals in 2005, Germany

(11.1%) and France (11.0%).

Tourism accounts for 1 in 6 of all new jobs created in the last ten years. In certain regions, there is a high dependency on tourism

income (e.g. in Cumbria it accounts for 17% of jobs and 18% of local GDP).

4 2009 and 2010 estimated

29

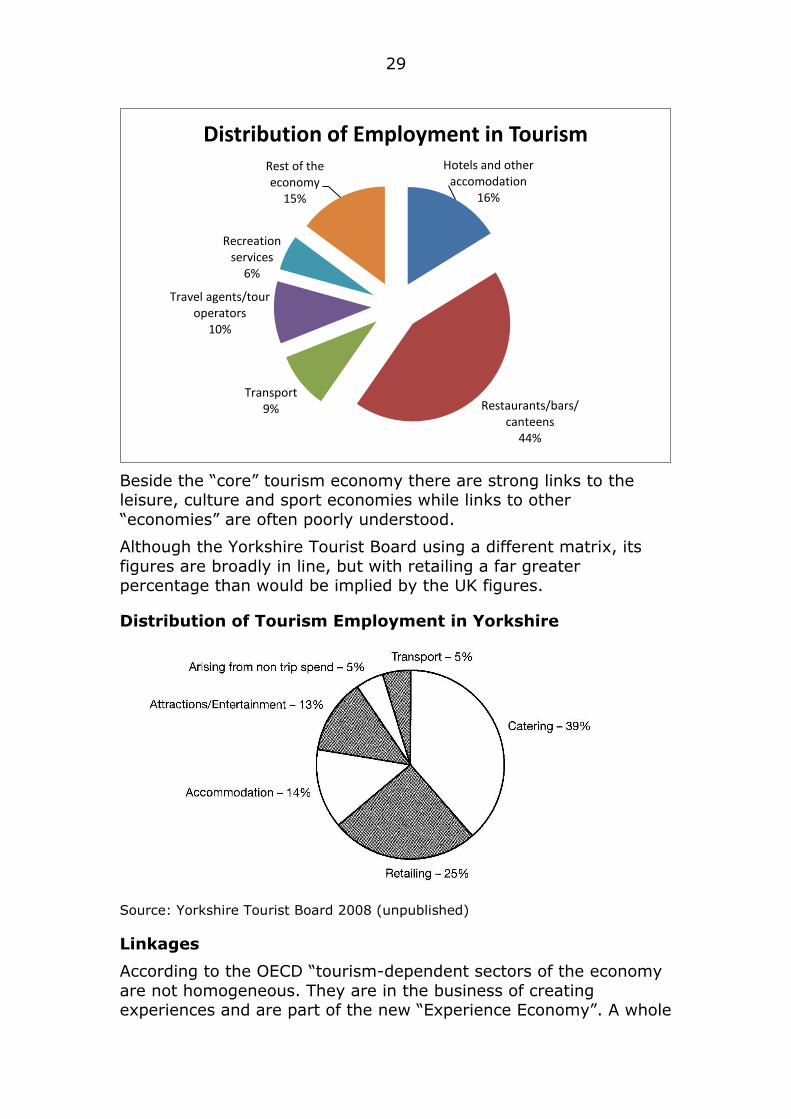

Beside the “core” tourism economy there are strong links to the leisure, culture and sport economies while links to other

“economies” are often poorly understood.

Although the Yorkshire Tourist Board using a different matrix, its

figures are broadly in line, but with retailing a far greater percentage than would be implied by the UK figures.

Distribution of Tourism Employment in Yorkshire

Source: Yorkshire Tourist Board 2008 (unpublished)

Linkages

According to the OECD “tourism-dependent sectors of the economy

are not homogeneous. They are in the business of creating experiences and are part of the new “Experience Economy”. A whole

Hotels and other accomodation

16%

Restaurants/bars/canteens

44%

Transport9%

Travel agents/tour operators

10%

Recreation services

6%

Rest of the economy

15%

Distribution of Employment in Tourism

30

package of services is designed, developed and commercialised for

visitors to enjoy as experiences.

The tourism industry is a kind of “dream factory”, with the

manufacture of unforgettable experiences requiring high quality levels. Indeed, productivity in tourism depends on the quality of the

experience, reflected in the perceived satisfaction of the visitor which is a subjective judgment. Anything that contributes to the

efficient production and marketing of quality experiences helps to promote productivity in tourism.”5

This latter point was vividly illustrated at the meeting with the Scrutiny Committee, where the importance of “religious” tourism

was discussed.

Halifax Gains a Minster

Religious tourism accounts, for example, for some of the largest “tourism” events in the world, for example, pilgrimages to Mecca

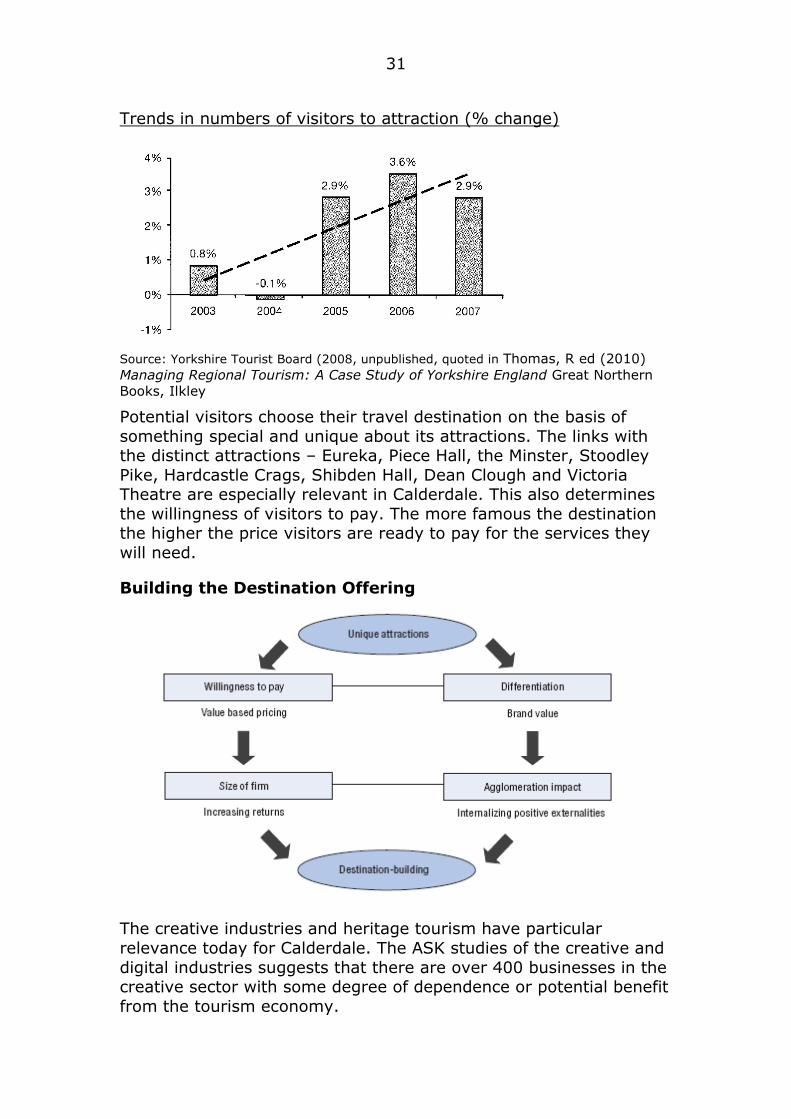

and many of the oldest tourism events viz Chaucer‟s Canterbury Tales. Across Yorkshire, however, although the number of visitors to

attractions grew significantly during the 2000s, there was a drop in growth rates as the recession bit.

5 OECD (2009) TOURISM IN OECD COUNTRIES 2008: TRENDS AND POLICIES – ISBN

978-92-64-03967-4

31

Trends in numbers of visitors to attraction (% change)

Source: Yorkshire Tourist Board (2008, unpublished, quoted in Thomas, R ed (2010)

Managing Regional Tourism: A Case Study of Yorkshire England Great Northern

Books, Ilkley

Potential visitors choose their travel destination on the basis of

something special and unique about its attractions. The links with the distinct attractions – Eureka, Piece Hall, the Minster, Stoodley

Pike, Hardcastle Crags, Shibden Hall, Dean Clough and Victoria Theatre are especially relevant in Calderdale. This also determines

the willingness of visitors to pay. The more famous the destination the higher the price visitors are ready to pay for the services they

will need.

Building the Destination Offering

The creative industries and heritage tourism have particular

relevance today for Calderdale. The ASK studies of the creative and

digital industries suggests that there are over 400 businesses in the creative sector with some degree of dependence or potential benefit

from the tourism economy.

32

These include Training & Development, Crafts, Design, Fashion

Design, Heritage, Museums & Conservation, Multiple Arts Practice, Music, Performing Arts and Other. Currently, these businesses

employ around 4,000 people (full and part-time, but not temporary staff) across Calderdale, but with potential to grow rapidly

generating several times that number of net additional jobs.

This growth potential is vividly illustrated in the preliminary results

of the parallel study of the fastest growing companies in Calderdale. This indicates that upwards of 15% of the fastest growing 130

businesses identified to date operate either within the Tourism sector or in sectors linked to tourism.

Multipliers

It is not hard to see a Tourism sector capable of having a

“Multiplier” effect on the wider Calderdale economy significantly

greater than size of the “core” tourism economy.

This potential multiplier effect can be seen across a number of

indicators. Although the number of businesses in the core tourism sector appears to be less than 200, around 600 businesses seem to

be directly or indirectly linked to the sector.

Number of Businesses in the Core and Related Sectors

The research referred to earlier by ASK suggests that the potential for growth and new firm formation is relatively high with over 50%

of the businesses operating in the sector started in the last ten years.

Core Tourism

Economy, 147

Closely Related e.g.

Culture & Heritage,

313

Indirectly related e.g. transport,

123

33

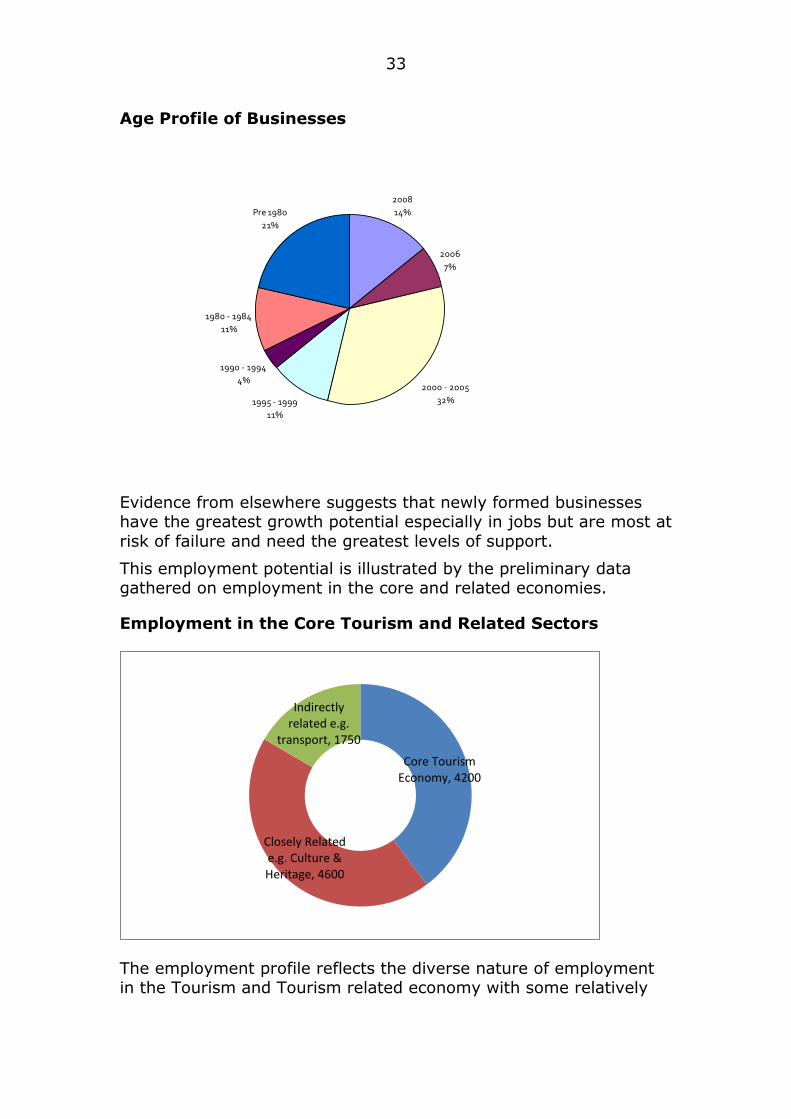

Age Profile of Businesses

Evidence from elsewhere suggests that newly formed businesses have the greatest growth potential especially in jobs but are most at

risk of failure and need the greatest levels of support.

This employment potential is illustrated by the preliminary data gathered on employment in the core and related economies.

Employment in the Core Tourism and Related Sectors

The employment profile reflects the diverse nature of employment in the Tourism and Tourism related economy with some relatively

2008

14%

2006

7%

2000 - 2005

32%1995 - 1999

11%

1990 - 1994

4%

1980 - 1984

11%

Pre 1980

21%

Core Tourism Economy, 4200

Closely Related e.g. Culture & Heritage, 4600

Indirectly related e.g.

transport, 1750

34

large organisations but a preponderance of small and micro-

enterprises.

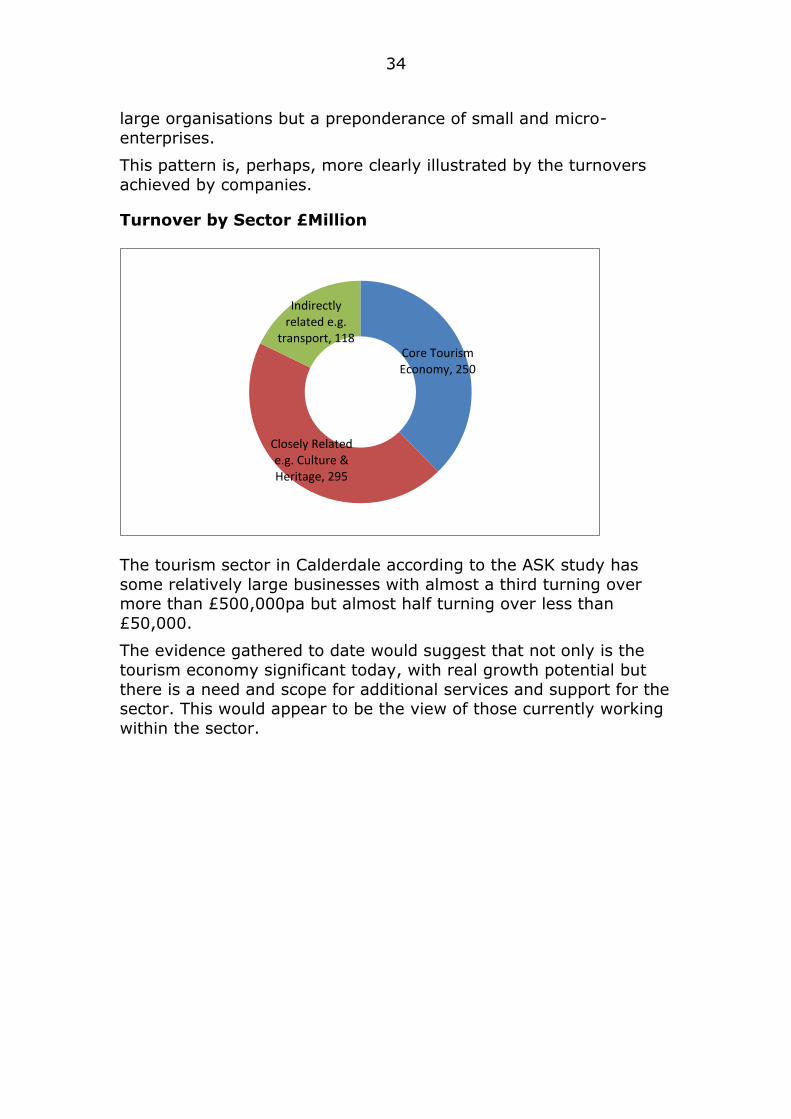

This pattern is, perhaps, more clearly illustrated by the turnovers

achieved by companies.

Turnover by Sector £Million

The tourism sector in Calderdale according to the ASK study has

some relatively large businesses with almost a third turning over more than £500,000pa but almost half turning over less than

£50,000.

The evidence gathered to date would suggest that not only is the

tourism economy significant today, with real growth potential but

there is a need and scope for additional services and support for the sector. This would appear to be the view of those currently working

within the sector.

Core Tourism Economy, 250

Closely Related e.g. Culture & Heritage, 295

Indirectly related e.g.

transport, 118

35

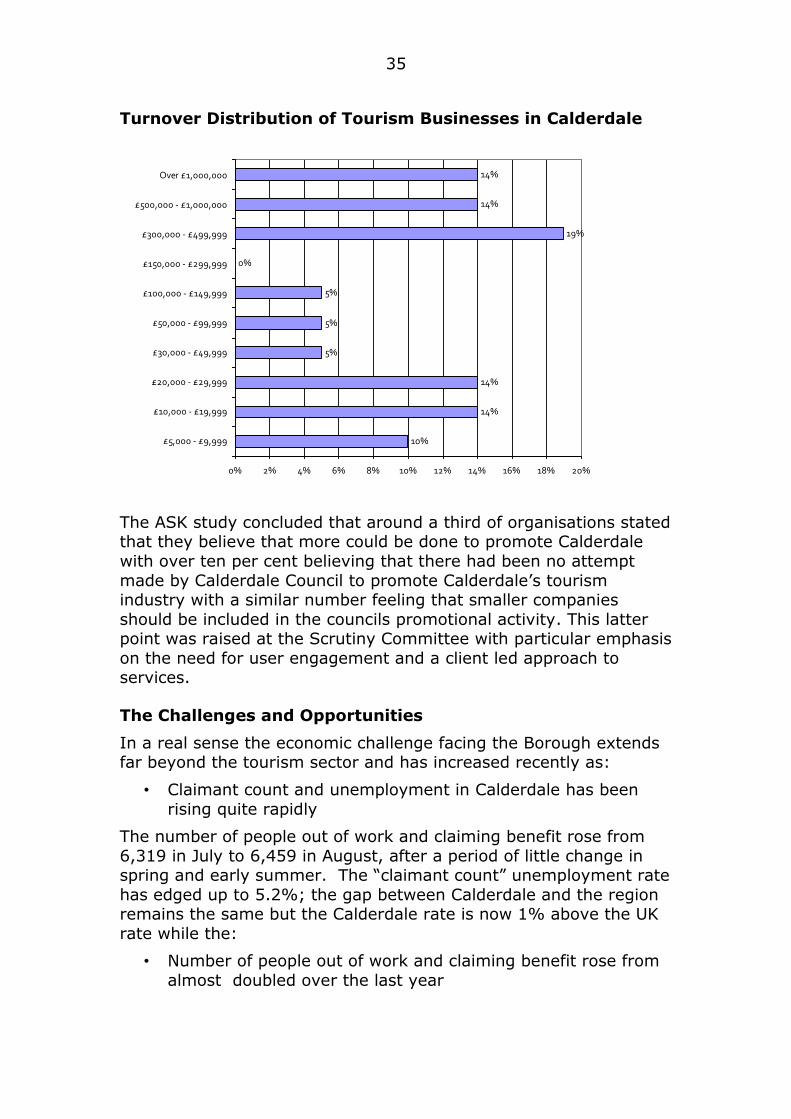

Turnover Distribution of Tourism Businesses in Calderdale

The ASK study concluded that around a third of organisations stated that they believe that more could be done to promote Calderdale

with over ten per cent believing that there had been no attempt

made by Calderdale Council to promote Calderdale‟s tourism industry with a similar number feeling that smaller companies

should be included in the councils promotional activity. This latter point was raised at the Scrutiny Committee with particular emphasis

on the need for user engagement and a client led approach to services.

The Challenges and Opportunities

In a real sense the economic challenge facing the Borough extends far beyond the tourism sector and has increased recently as:

• Claimant count and unemployment in Calderdale has been

rising quite rapidly

The number of people out of work and claiming benefit rose from

6,319 in July to 6,459 in August, after a period of little change in spring and early summer. The “claimant count” unemployment rate

has edged up to 5.2%; the gap between Calderdale and the region remains the same but the Calderdale rate is now 1% above the UK

rate while the:

• Number of people out of work and claiming benefit rose from

almost doubled over the last year

10%

14%

14%

5%

5%

5%

0%

19%

14%

14%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20%

£5,000 - £9,999

£10,000 - £19,999

£20,000 - £29,999

£30,000 - £49,999

£50,000 - £99,999

£100,000 - £149,999

£150,000 - £299,999

£300,000 - £499,999

£500,000 - £1,000,000

Over £1,000,000

36

• Published total of vacancies over the last six months is 23%

lower than the previous six months

• Substantial rise in numbers receiving Council Tax and/or

Housing Benefit is a major cause for concern

• Over the 12 months from July 2008 to July 2009 there has

been a 14% rise in the numbers in receipt of Council Tax and/or Housing Benefit, and a 7.5% rise in pupils receiving

Free School Meals.

• Average house prices in Calderdale fell by 14% in the year up

to mid 2009

These challenges contrast sharply with the opportunities provided

by tourism and related sectors.

There assets within the Borough are significant and include:

• Attractions like Eureka! The National Children‟s Museum, the

Piece Hall, Dean Clough, Stoodley Pike, Hardcastle Crags, Shibden Hall and Victoria Theatre

• Powerful industrial and cultural legacy

• Dramatic landscapes

• Diverse and distinctive local communities

• Eight million people within a 2 hour drive.

The successes achieved over the last few years allied to the new priority given across Yorkshire to the Tourism economy suggest that

the potential exists within Tourism to – at the very least – alleviate the economic challenges facing the people of Calderdale. This will,

however, depend on a combination of factors notably:

Delivery of the right sort of support to businesses and others

working in the tourism and related sectors

Active engagement of these sectors

Investment of resources in those sectors offering the greatest

returns

Some key aspects of the Tourism “community” in Calderdale will

help to shape the opportunities that will emerge and the challenges faced.

Central to this is the extent to which local tourism businesses are deeply rooted in the local economy and community. Over ninety per

cent of the tourism businesses identified in the ASK study have always been based in Calderdale. This illustrates the extent to which

these firms are committed not only to the Borough but its success.

37

Distribution of Tourism Businesses by Postcode

Equally important to a diverse community such as Calderdale, tourism businesses are spread across the Borough with a significant

number of tourism businesses in each Post Code area.

Unfortunately, however, evidence to date suggests that there is a

general air of pessimism about prospects. The ASKE research

reported that forty percent of Tourism businesses interviewed expected their turnover to decrease for the next financial year

whilst only thirteen per cent of businesses expected turnover to increase. Part of the challenge facing Authority is to develop and

deliver policies that: change this thinking, focus on the drivers of growth against a background of resource constraints and limited

control of aspects of tourism support.

Tourism: Economic Development and Regeneration

The relationship between tourism, economic development and regeneration. Twenty years ago Christopher Law6 pointed out that:

“Investment for tourism involves the development of facilities, physical environments and infrastructure which will have many

benefits for the local community. It also involves marketing and the selling of an image, which will assist in the attraction of industrial

and commercial activities. With the transformation of districts (see

below) and the new image, it will be easier to bring middle-class residents back to the inner city. The money which tourists spend at

facilities, such as concerts and theatres, may make these activities

6 Christopher M . Law (1992) Urban Tourism and its Contribution to Economic

Regeneration Urban Studies, Vol. 29, Nos . 3/4, 599-618

13%

17%

10%

7%

7%

17%

10%

7%

13%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

HX1

HX2

HX3

HX4

HX5

HX6

HX7

OL14

HD6

38

more economically viable and this in turn will be of benefit to the

local community. Finally, the development of these facilities, the physical regeneration of areas and the arrival of visitors may

increase civic pride, which is usually deemed a good thing. It is suggested that local residents who have civic pride will take much

greater care of the environment.”

Source: Saxena, G and Watts, M (2010) Regeneration Projects and Tourism in Yorkshire in

Thomas, R ed (2010) Managing Regional Tourism: A Case Study of Yorkshire

England Great Northern Books, Ilkley

Saxena and Watts (2010) provide a neat model of how the positive and negative aspects of tourism related regeneration can be

analysed.

More recently a series of articles in Regeneration & Renewal have

flagged this relationship in a range of environments. There is evidence, however, that these regeneration effects are especially

important for communities like Calderdale because of their influence on the development of:

• Small and medium sized firms (SMEs)

• Technologies, skills

• Other parts of the local economy.

39

The potential for generating positive impacts is, in turn, affected by

the willingness of policy makers locally to rethink the way they view the visitor economy and they way they approach other

stakeholders.

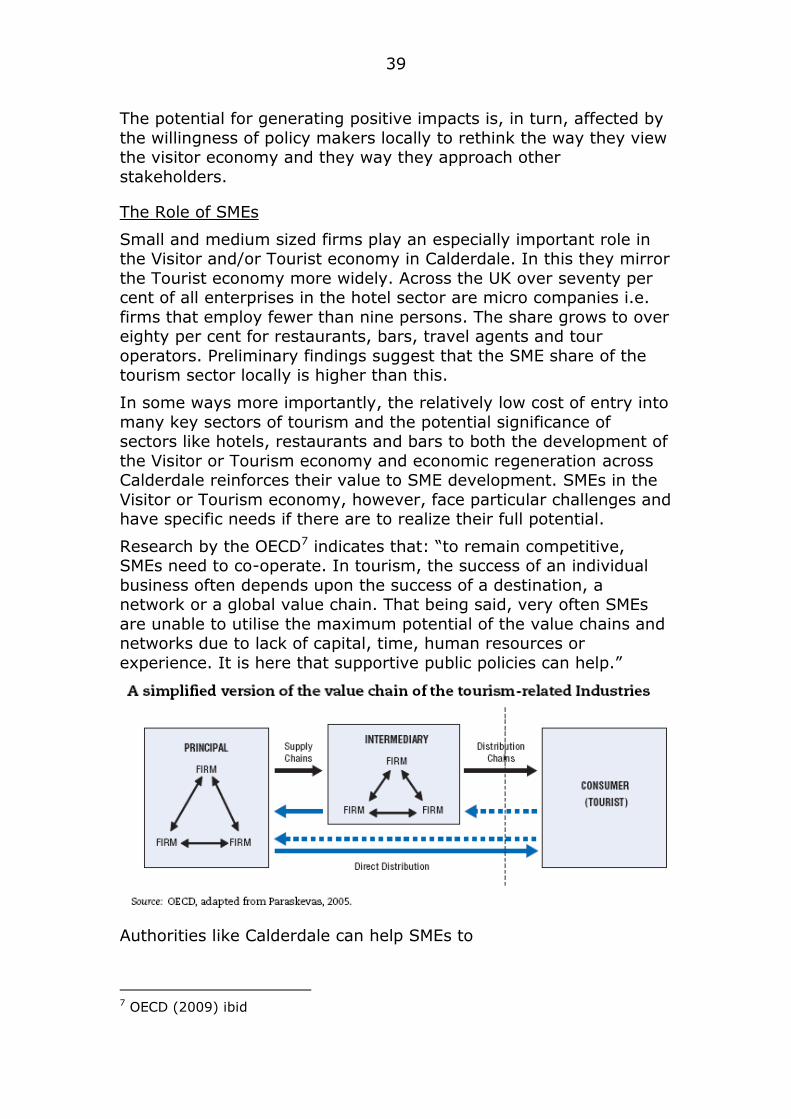

The Role of SMEs

Small and medium sized firms play an especially important role in the Visitor and/or Tourist economy in Calderdale. In this they mirror

the Tourist economy more widely. Across the UK over seventy per cent of all enterprises in the hotel sector are micro companies i.e.

firms that employ fewer than nine persons. The share grows to over eighty per cent for restaurants, bars, travel agents and tour

operators. Preliminary findings suggest that the SME share of the tourism sector locally is higher than this.

In some ways more importantly, the relatively low cost of entry into

many key sectors of tourism and the potential significance of sectors like hotels, restaurants and bars to both the development of

the Visitor or Tourism economy and economic regeneration across Calderdale reinforces their value to SME development. SMEs in the

Visitor or Tourism economy, however, face particular challenges and have specific needs if there are to realize their full potential.

Research by the OECD7 indicates that: “to remain competitive, SMEs need to co-operate. In tourism, the success of an individual

business often depends upon the success of a destination, a network or a global value chain. That being said, very often SMEs

are unable to utilise the maximum potential of the value chains and networks due to lack of capital, time, human resources or

experience. It is here that supportive public policies can help.”

Authorities like Calderdale can help SMEs to

7 OECD (2009) ibid

40

● Enhance productivity and the rate of technological

innovation

● Help to build a common view to influence policies

● Overcome some of the disadvantages of small size by undertaking co-operative actions (e.g. in marketing)

● Pool resources for human resource development

● Enhance growth and the competitive performance of firms.

Facilitating the creation of partnerships, clusters and networks can enable SMEs across the authority to combine the advantages of

small scale with the benefits of large scale.

SMEs Key Assets, Challenges and Scope for Intervention

Assets

Focus

Personal commitment

Differentiation

Personal service

Local knowledge

Challenges

Lack of finances

Skills

Resources such as IT

Weak alliances and partnerships

Change management

Marketing and branding

Scope for Intervention

Building capabilities and competences

Technical support

Creating alliances and partnerships

Accessing resources

Adding value

Skills development

Targeting resources

Events

41

E-Tourism

The last decade has seen dramatic growth in e-tourism. Across Europe, online travel sales increased by at an annual rate of over

30% between 2003 and 2008 to reach almost €20 billion (just under 8% of the total market).

Growth in the wider European online travel market is expected to

slow, but its value was predicted to increase to more than €25 billion by 2008 – an expected 10% of the total travel market. There

are notable differences in the levels of e-commerce and e-business activity among European countries and within individual countries.

The UK is generally well placed for both access to the internet and other aspects of e-tourism but there are significant local gaps and

specific weaknesses in SMEs.

The internet, in particular, is transforming the distribution of

tourism information and sales. An increasing proportion of internet users are buying on–line and tourism will gain a larger and larger

share of the online commerce market. SMEs, however, are facing more challenging demands from customers and commercial clients

who expect them to adopt new information technologies, in particular, e-business. Part of the problem relates to the scale and

affordability of information technology, as well as the facility of

implementation within rapidly growing and changing organisations. In addition, new solutions configured for large, stable, and

internationally-oriented firms do not fit well for small, dynamic, and locally-based tourism firms.

Despite these challenges, SMEs with well-developed and innovative web sites can now have “equal Internet access” to international

tourism markets. This implies equal access to telecom

42

infrastructure, as well as to marketing management and education.

According to a UN report8, “it is not the cost of being there, on the on-line market place, which must be reckoned with, but the cost of

not being there.”

The main benefits of e-commerce for tourism enterprises are

typically reported as „providing easy access to information on tourism services,‟ „providing better information on tourism services,‟

and „providing convenience for customers‟. This result implies that respondents are less aware of many other benefits of e-commerce,

such as „creating new markets,‟ „improving customer services,‟ „establishing interactive relationships with customers‟, „reducing

operating cost‟, „interacting with other business partners‟, and „founding new business partners‟

The main constraints range from „limited knowledge of available

technology,‟ „lack of awareness,‟ „cost of initial investment,‟ „lack of confidence in the benefits of e-commerce,‟ and „cost of system

maintenance, ‟ to „shortage of skilled human resources,‟ and „resistance to adoption of e-commerce.‟ In terms of market

situation, one might also mention „insufficient e-commerce infrastructure,‟ and „small e-commerce market size‟.

The Skills Challenge

People 1st (the Sector Skills Council for the hospitality, leisure,

travel and tourism) has highlighted these human resource, behavioural and skills challenges as among the greatest challenges

facing the tourism and related sectors9.

The Sector Skills Council estimates of the size of the sector are

broadly in line with those elsewhere with the sector itself accounting for approximately 4.8 percent of the UK‟s economic output. Their

2009 estimates of the indirect contribution of the „visitor economy‟

to the UK‟s Gross Domestic Product are slightly larger i.e. 8.2 percent (over £100 billion) that estimates elsewhere.

People 1st suggests that the sector has grown substantially over the last 20 years and, despite the current recession, is predicted to

continue to grow in the medium to long term. The sector is a significant employer across the UK, particularly in areas highly

dependent on tourism. In total, People 1st believes that the sector provides employment for approximately two million people.

8 World Tourism Organization (WTO) (2001). E-business For Tourism, Practical

Guideline For Tourism Destination and Business

9 People 1st (2009) Skills priorities for the Hospitality, Leisure, Travel and Tourism

sector Uxbridge

43

The sector has traditionally suffered from perceptions of low wages,

unsociable hours and poor conditions, which can make it difficult for employers to attract talent. Recruitment difficulties can lead to

inexperienced staff being recruited which then impacts on workforce skill levels and productivity10.

Whilst many employers in the sector do pay the minimum wage and require people to work „unsociable‟ hours, this does not necessarily

deter people from working in the sector if the work and working environment are constructed in an attractive way. In addition,

within many businesses there are opportunities for good staff to be promoted quickly and increase their pay accordingly.

The sector suffers from the highest rate of labour turnover of all sectors of the economy11.This is partly due to a reliance on a

transient workforce of students and overseas workers. The constant

need to replace leavers leads to high levels of skills gaps as it means there are always a large number of new recruits developing

into their roles.

Constant recruitment and retraining can be costly. Employers in the

sector (the hospitality element in particular) have, however, traditionally operated with high labour turnover and many do not

see it as a problem12. Public sector bodies including local authorities like Calderdale can play an important role in embedding strategies

and support systems to address these issues.

In a series of studies People 1st identified three main long term skill

problems across the sector:

1. A shortage of skilled chefs

2. Poor standards of management and leadership

3. Poor customer service skills

The economic downturn has, however, increased the importance of:

Good customer service skills

Good financial management as businesses struggle to survive,

People management skills as managers need to maintain staff morale in uncertain times in order to provide good customer

service.

10 According to the 2007 National Employer Skills Survey, 13 percent of sector

employers with skills gaps attribute the gap to recruitment problems 11 Recruitment and Retention Survey, CIPD, 2008 and Sector Skills Agreement,

People1st, 2006

12 People1st, (2009) Recruitment, Retention and Training Survey

44

Multi-skilling (as businesses make job cuts or decide not to

replace staff who leave, there is likely to be a need for remaining staff to undertake tasks for which they were

previously not responsible)

Entrepreneurialism (as the need to reduce costs and

maximise profit becomes paramount),

as businesses strive to win competitive advantage during the

recession. The main tactics being followed in the sector include:

Reducing costs such as staff costs (in some cases reducing

hours, wages or laying staff off), marketing costs, training costs and energy costs.

Offering more promotions such as two-for-one offers (promotions are often a more effective strategy than simply

lowering prices as they do not devalue the product and it is

easier to revert to the original prices when appropriate)

Diversification (particularly in the pub, bar and nightclub

industry where licensees are increasingly looking for innovative ways to attract customers)

Increasing training and development to upskill staff and retain customers

Increasing marketing to attract and retain customers

While these are, in many ways, appropriate tactics nationally and

locally to overcome immediate challenges, the available research suggests that more fundamental shifts in policies and thinking are

needed for longer term advantage.

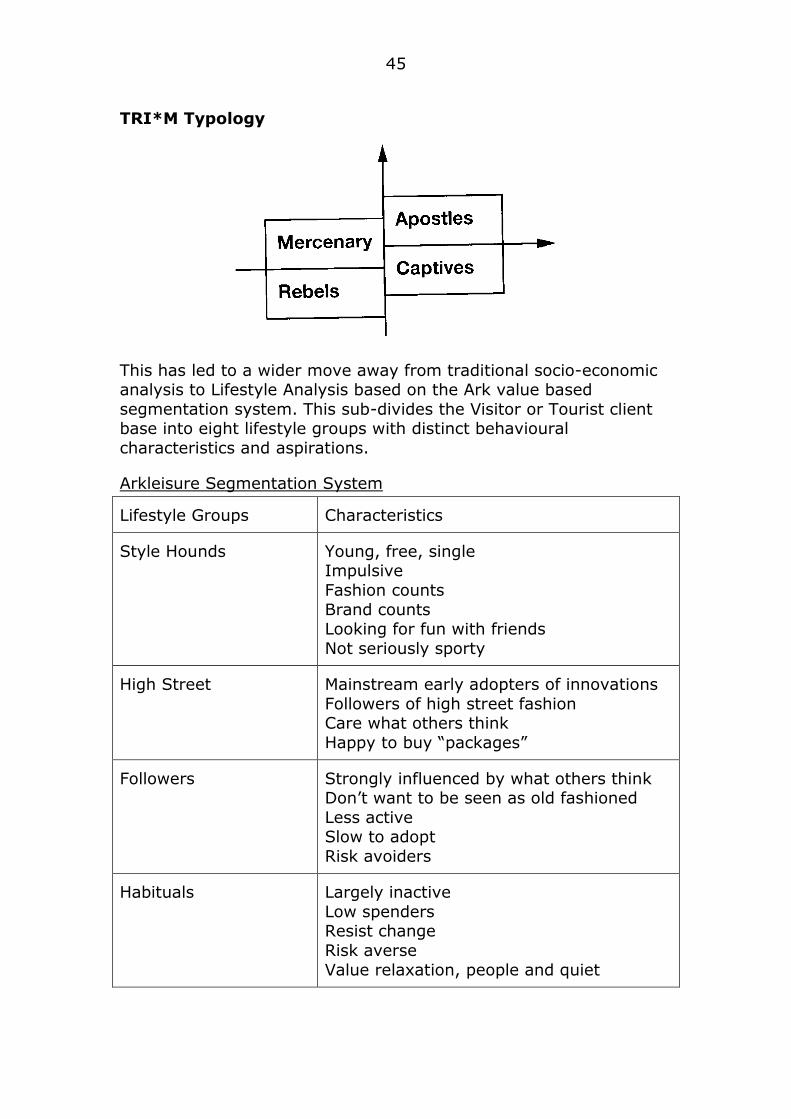

Lifestyles

A key shift in the thinking of the Yorkshire Tourist Board has been to rethink ways of considering the Visitor or Tourist client. One

approach classifies tourism customers into four types – Mercenaries,

Rebels, Apostles and Capitives - based on their satisfaction or loyalty.

Mercenaries have no loyalty and constantly seek the best deals. Rebels are fickle and unpredictable, apostles have been converted

and will evangelise while captives visit often but for personal reasons e.g. visiting family. Promotional activity seeks to move

Visitor in direction of arrows.

45

TRI*M Typology

This has led to a wider move away from traditional socio-economic analysis to Lifestyle Analysis based on the Ark value based

segmentation system. This sub-divides the Visitor or Tourist client base into eight lifestyle groups with distinct behavioural

characteristics and aspirations.

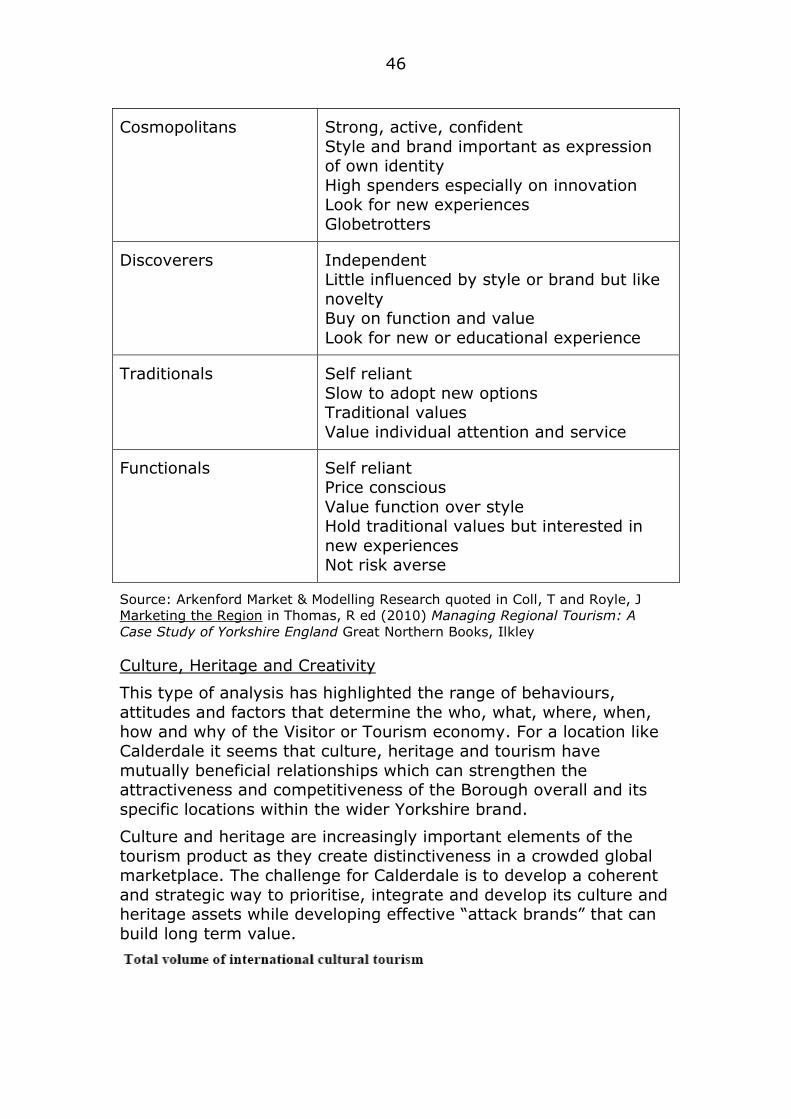

Arkleisure Segmentation System

Lifestyle Groups Characteristics

Style Hounds Young, free, single Impulsive

Fashion counts

Brand counts Looking for fun with friends

Not seriously sporty

High Street Mainstream early adopters of innovations

Followers of high street fashion Care what others think

Happy to buy “packages”

Followers Strongly influenced by what others think Don‟t want to be seen as old fashioned

Less active Slow to adopt

Risk avoiders

Habituals Largely inactive

Low spenders Resist change

Risk averse

Value relaxation, people and quiet

46

Cosmopolitans Strong, active, confident

Style and brand important as expression of own identity

High spenders especially on innovation Look for new experiences

Globetrotters

Discoverers Independent Little influenced by style or brand but like