city of edgewater, florida rpts/2016 edgewater.pdf · the city of edgewater was incorporated in...

TRANSCRIPT

CITY OF EDGEWATER,

FLORIDA

COMPREHENSIVE ANNUAL FINANCIAL REPORT

For the fiscal year ended September 30, 2016

Prepared by: The Finance Department

This page intentionally left blank

I

TABLE OF CONTENTS

Page Introductory Section Letter of Transmittal III GFOA Certificate of Achievement VI List of Principal Officials VII Organizational Chart VIII Financial Section Independent Auditor’s Report 1 Management’s Discussion and Analysis 3 Basic Financial Statements Government-Wide Financial Statements: Statement of Net Position 15 Statement of Activities 16 Fund Financial Statements: Balance Sheet - Governmental Funds 18 Reconciliation of the Balance Sheet of Government Funds to the Statement of

Net Position

19 Statement of Revenues, Expenditures and Changes in Fund Balances - Governmental Funds 20 Reconciliation of the Statement of Revenues, Expenditures and Changes in Fund Balances of Governmental Funds to the Statement of

Activities 21 Statement of Revenues, Expenditures and Changes in Fund

Balances - Budget and Actual - General Fund 22 Statement of Revenues, Expenditures and Changes in Fund

Balances - Budget and Actual - CRA Fund 23 Statement of Net Position - Proprietary Funds 24 Statement of Revenues, Expenses and Changes in

Fund Net Position - Proprietary Funds 25 Statement of Cash Flows - Proprietary Funds 26 Statement of Fiduciary Net Position - Fiduciary Funds 27 Statement of Changes in Fiduciary Net Position – Pension Trust Funds 28 Notes to the Financial Statements 29 Required Supplementary Information (Unaudited) Schedules of changes in the City's Net Pension Liability and Related Ratios 58 Schedules of General Employees' Contributions 60 Schedules of Police Officers' Contributions 61 Schedules of Firefighters' Contributions 62 Other Post Employment Benefit Plan 63 Combining and Individual Fund Statements and Schedules Nonmajor Governmental Funds – Fund Descriptions 65 Combining Balance Sheet - Nonmajor Governmental Funds 66 Combining Statement of Revenues, Expenditures and Changes In Fund Balances - Nonmajor Governmental Funds 68 Schedule of Revenues, Expenditures and Changes in Fund

Balances - Budget and Actual – Nonmajor Special Revenue Funds 70 Schedule of Revenues, Expenditures and Changes in Fund

Balances - Budget and Actual – Nonmajor Debt Service Funds 74 Schedule of Revenues, Expenditures and Changes in Fund

Balances - Budget and Actual – Major Capital Projects Funds 75 Internal Service Funds – Fund Descriptions 77 Combining Statement of Net Position 78 Combining Statement of Revenues, Expenses, and Changes in Fund

Net Position – Internal Service Funds

79 Combining Statement of Cash Flows – Internal Service Funds 80

II

Page

Financial Section - Continued Other Supplemental Schedules – Fiduciary Funds – Fund Descriptions 81 Combining Statement of Fiduciary Net Position – Pension Trust Funds 82 Combining Statement of Changes in Fiduciary Net Position – Pension

Trust Funds

83 Statistical Section (Unaudited) Table of Contents 85 Financial Trends Net Position by Component 86 Changes in Net Position 87 Fund Balances of Governmental Funds 89 Changes in Fund Balances of Governmental Funds 90 Revenue Capacity: Tax Revenues by Source of Governmental Funds 91 Assessed Value and Actual Value of Taxable Property 92 Property Tax Rates - Direct and Overlapping Governments 93 Principal Taxpayers 94 Property Tax Levies and Collections 95 Debt Capacity: Ratios of Outstanding Debt by Type 96 Ratios of General Obligation Bonded Debt Outstanding 98 Direct and Overlapping Debt 99 Legal Debt Margin Information 100 Pledged-Revenue Coverage 101 Demographic and Economic Information: Demographic and Economic Statistics 102 Principal Employers 103 Operating Information Full-time Equivalent City Government Employees by Function/Program 104 Operating Indicator by Function/Program 105 Capital Asset Statistics by Function/Program 106 Other Reports: Independent Auditors’ Report on Internal Control over Financial Reporting and on

Compliance and Other Matters Based on an Audit of Financial Statements

Performed In Accordance with Government Auditing Standards 107 Independent Auditors’ Management Letter 109 Independent Accountants’ Examination Report 112 Reply to the Independent Auditor’s Report 113 Affidavit of Impact Fee Compliance 114

III

March 8, 2017 To the Honorable Mayor, and Members of the City Council, and Citizens of the City of Edgewater City Charter and State law requires that all general-purpose local governments publish a complete set of financial statements presented in conformity with the generally accepted accounting principles in the United States of America (GAAP) and that they be audited in accordance with generally accepted auditing standards in the United States of America by a firm of licensed certified public accountants. Pursuant to the requirement, it is with great pleasure that we present to the City of Edgewater, the Comprehensive Annual Financial Report (CAFR) for the fiscal year ended September 30th, 2016. This report consists of management’s representations concerning the finances of the City of Edgewater. Consequently, management assumes full responsibility for the completeness and reliability of all the information presented in this report. To provide a reasonable basis for making these representations, management of the City of Edgewater has established a comprehensive internal control framework that is designed both to protect the government’s assets from loss, theft, or misuse and to compile sufficient reliable information for the preparation of the City of Edgewater’s financial statements in conformity with GAAP. Because the cost of internal controls should not outweigh their benefits, the City of Edgewater’s comprehensive framework of internal controls has been designed to provide reasonable rather than absolute assurance that the financial statements will be free from material misstatements. As management, we assert that, to the best of our knowledge and belief, this financial report is complete and reliable in all material respects. James Moore & Co., P.L. a firm of licensed certified public accountants, has issued an unmodified (“clean”) opinion on the City of Edgewater’s financial statements for the fiscal year ended September 30, 2016. The independent auditor’s report is located at the front of the financial section of this report. Management’s discussion and analysis (MD&A) immediately follows the independent auditor’s report. GAAP requires that management provide a narrative introduction, overview, and analysis to accompany the basic financial statements in the form of Management’s Discussion and Analysis (MD&A). This letter of transmittal is designated to complement the MD&A and should be read in conjunction with it. Profile of the Government The City of Edgewater was incorporated in 1951 and has operated under the Council-Manager form of government since 1981. Primary responsibilities of the City Manager are to implement the policies of the elected officials. The City Manager assumes responsibilities of the day-to-day operations of the City, annual budget preparation, appointing/removing officers and employees. In addition to supervising the daily operations, the City Manager works with elected officials, committees and citizens to plan for the future of the community. The City of Edgewater is located in southeast Volusia County, primarily east of I-95 south of New Smyrna Beach, two miles west of the Atlantic Ocean and runs along 10.5 miles of the Indian River coastline. The City is within the economic zone of Central Florida, which roughly follows Interstate 4 from Tampa through Orlando to Daytona Beach and the communities along the Atlantic Coast in Volusia County. There are approximately 14,550 acres of land within the City with an estimated population of 21,280.

IV

The City of Edgewater offers a full range of services to its citizens through multiple funds. The City uses funds to separate resources and assure that the City adheres to restrictions placed upon it by legislators, grantors, donors, and other outside parties (e.g. GASB, GAAP). The following is a list of services provided by each fund:

• General Fund - provides planning and zoning, economic development, building (e.g. permits, inspections, etc), police, fire, fire rescue, animal control, parks, recreation, streets (new and maintained), code enforcement, and general administrative services.

• Water and Sewer Fund - provides water and sewer services. • Refuse Fund - uses a combination of City personnel and assets along with private contracted

companies to provide solid waste collection. • Stormwater Fund – provides and ensures proper water drainage from all properties. • Internal Service Funds – account for fleet management services, management information

systems, general liability insurance, health insurance, and workers compensation insurance. • CRA Fund - account for the ad valorem proceeds for the redevelopment of our US1 and Park

Avenue Corridor.

Whenever possible the City seeks alternative sources of revenue to provide services, enhance services, and supplement the existing expenses in the budget. The most prominent example of alternative revenue is grants through the federal, state, and local levels. Local Economy Long established businesses such as Boston Whaler, Everglades Boats, Edgewater Power Boats, R.J. Dougherty Associates, Inc, Publix and Winn Dixie Supermarkets, as well as new businesses provide employment opportunities within the City. NASA and related supporting enterprises at Cape Canaveral as well as the cruise industry located at Port Canaveral provide further employment opportunities. The City of Edgewater currently has a 5.1 percent unemployment rate (in line with the state average of 5.0 percent). During the last year, taxable assessment values of property in Edgewater increased 7.27 percent. The City continues exploring several options to increase economic growth within the City and improve economic development within southeast Volusia County. The Community Redevelopment Agency was created to encourage redevelopment along our US. 1 and Park Ave. corridor. The City continues to develop many partnerships between various economic development agencies and local businesses. The City of Edgewater’s outlook for fiscal year 2017 is for modest gains in economic growth as the recovery and expansion from the financial crisis and national and international recessions gain a small degree of traction in the local economy. With the modest gains, the City of Edgewater continues to apply for Federal and State grants to fund sidewalks, bicycle trails along our major corridors. Without these funds, this project would not have been completed within the foreseeable future. Financial Planning and Budgeting The City continued to stress expenditure control in preparing the FY2017 General Fund budget. The City ad valorem millage rate for FY2017 was 6.70, which was 5.79% more than the rolled-back rate. The millage rate of 6.70, resulted in property tax collections increase of 5.5% due to an increase in property assessments an annexations. The City adopts a five-year capital improvement plan that identifies future funding needs to maintain, repair and upgrade capital assets and infrastructure including road resurfacing, water line upgrades and vehicle and technology replacement programs within the funding constraints. It should be noted; however, that the CIP is not a fixed document but a flexible, evolutionary document that may change to reflect changing priorities, opportunities, costs, or different financing approaches.

V

Relevant Financial Policies The City Council recognizes the need to meet seasonal shortfalls in cash flows, its susceptibility to emergency or unanticipated expenditures or the possibility of revenue shortfalls during any fiscal year. To address these issues, the City Council included in its Charter a requirement to maintain reserves at a minimum of 15 percent to a maximum of 25 percent of the general fund appropriations (excluding operating transfers). The unassigned fund balance at September 30, 2016 was 17.37% which is within the range of 15-25% per the charter. For Fiscal Year 2017 operating expenditures budget show modest increases to allow for increasing operating cost while still maintaining our capital improvements. Budgeting Controls The annual budget serves as the foundation for the City of Edgewater’s financial planning and control. All departments of the City of Edgewater are required to submit requests for appropriation to the City Manager. The City Manager then uses these requests as the starting point for developing a proposed budget. The City Manager then presents this proposed budget to the City Council for review. The City Council is required to hold public hearings on the proposed budget and to adopt a final budget by no later than September 30, the close of the City of Edgewater’s fiscal year. The appropriated budget is prepared by fund (i.e., General Fund), department (i.e., Fire Department) and division (i.e., Fire Operations). The City Manager may make transfers of appropriations within and between divisions and departments; however, any revisions that alter the total appropriations of any funds must be approved by City Council. Original and final amended budget-to-actual comparisons are provided in this report for each individual governmental fund. Certificate of Achievement Award The Government Finance Officers Association of the United States and Canada (GFOA) awarded a Certificate of Achievement for Excellence in Financial Reporting to the City of Edgewater for its comprehensive annual financial report for the fiscal year ended September 30, 2015. This was the thirty-second consecutive year that the City of Edgewater has achieved this prestigious award. In order to be awarded a Certificate of Achievement, a government must publish an easily readable and efficiently organized comprehensive annual financial report. This report must satisfy both generally accepted accounting principles and applicable legal requirements. A Certificate of Achievement is valid for a period of one year only. We believe that our current comprehensive annual financial report continues to meet the Certificate of Achievement Program’s requirements and we are submitting it to the GFOA to determine its eligibility of another certificate. Acknowledgements The preparation of this report would not have been possible without the efficient and dedicated commitment of the entire Finance Department. The City departments, although not extensively involved in year-end audit activities, contributed significantly by ensuring the accuracy and integrity of the accounting information and statistics compiled throughout the year. Without their diligence, the work of the Finance Department would have been considerably more difficult. Appreciation must also be expressed to the City’s external auditor whose suggestions and attention to detail enhanced the quality of this report. In closing, special thanks to the Mayor and City Council for their support and commitment to maintaining the financial integrity and sustainability of the City. Respectfully submitted,

Tracey T. Barlow Jonathan C. McKinney City Manager Finance Director

VI

VII

CITY OF EDGEWATER FLORIDA

List of Elected and Appointed Officials

September 30, 2016

CITY COUNCIL

MAYOR

Michael Ignasiak

DISTRICT 1 Christine Power

DISTRICT 3

Dan Blazi

DISTRICT 2 Gigi Bennington

DISTRICT 4 Gary Conroy

ADMINISTRATION

CITY MANAGER

CITY ATTORNEY

Tracey T. Barlow

Aaron R. Wolfe

ASSISTANT CITY MANAGER / FINANCE DIRECTOR

CITY CLERK / PARALEGAL

Jonathan McKinney

Robin L. Matusick

FIRE CHIEF

POLICE CHIEF

Stephen Cousins

David J. Arcieri

HUMAN RESOURCES DIRECTOR

DEVELOPMENT SERVICES DIRECTOR

Julie A. Christine

Darren Lear

ENVIRONMENTAL SERVICES

PARKS & RECREATION

DIRECTOR

ACTING DIRECTOR Brenda Dewees

Jonathan McKinney

VIII

CITY OF EDGEWATER FLORIDA City Organization Chart

September 30, 2016

INDEPENDENT AUDITORS’ REPORT

To the Honorable Mayor, City Council, and City Manager City of Edgewater, Florida:

Report on the Financial Statements

We have audited the accompanying financial statements of the governmental activities, business-type activities, each major fund, and the aggregate remaining fund information of the City of Edgewater, Florida (the City), as of and for the year ended September 30, 2016, and the related notes to the financialstatements, which collectively comprise the City’s basic financial statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements

The City’s management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditors’ Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the City’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the City’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, the business-type activities, each major fund,and the aggregate remaining fund information of the City as of September 30, 2016, and the respective changes in financial position and, where applicable, cash flows thereof and the respective budgetary comparison for the general fund and CRA fund for the year then ended in accordance with accounting principles generally accepted in the United States of America.

1

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the management’s discussion and analysis and other required supplementary information, as listed in the table of contents,be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

Other Information

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the City’s basic financial statements. The introductory section, combining and individual nonmajor fund financial statements, budgetary comparison schedules, and statistical section and are presented for purposes of additional analysis and are not a required part of the basic financial statements.

The combining and individual nonmajor fund financial statements, and budgetary comparison schedulesare the responsibility of management and were derived from and relate directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the information is fairly stated, in all material respects in relation to the basic financial statements as a whole.

The introductory section and statistical section have not been subjected to the auditing procedures applied in the audit of the basic financial statements, and accordingly, we do not express an opinion or provide any assurance on them.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated March 4, 2017, on our consideration of the City’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the City’s internal control over financial reporting and compliance.

Daytona Beach, FloridaMarch 4, 2017

2

Management’s Discussion and Analysis

As management of the City of Edgewater, Florida we offer readers of the City of Edgewater’s financial statements this narrative overview and analysis of the financial activities of the City of Edgewater for the fiscal year ended September 30, 2016. We encourage readers to consider the information presented here in conjunction with additional information that we have furnished in our letter of transmittal. Financial Highlights

• Net Position - The assets of the City exceeded its liabilities at the close of FY 2015-16 by $74,331,779, which represents an increase in net position of $1,118,548 or 1.53% from the prior fiscal year.

• The City’s governmental funds reported combined ending fund balance of $4,283,009, a

decrease of $430,392 from the prior fiscal year.

• At the end of FY 2015-16, the General Fund unassigned fund balance was $2,376,555 or 17.37% of the budgeted FY 2017 General Fund expenditures, excluding transfers. This represents a decrease of $432,420 from the prior fiscal year.

• During the fiscal year, the City’s total debt decreased by $2,858,704. Governmental debt

decreased by $385,183 and business-type debt reflected a decrease of $2,473,521. Overview of the Financial Statements This discussion and analysis are intended to serve as an introduction to the City of Edgewater’s (the City) basic financial statements. The City’s basic financial statements comprise three components: 1) government-wide financial statements, 2) fund financial statements, and 3) notes to the financial statements. This report also contains other supplementary information in addition to the basic financial statements themselves. Government-Wide Financial Statements The government-wide financial statements are designed to provide readers with a broad overview of the City of Edgewater’s finances, in a manner similar to a private-sector business. The statement of net assets presents information on all of the City’s assets and liabilities, with the difference between the two reported as net position. Over time, increases or decreases in net position may serve as a useful indicator of whether the financial position of the City is improving or deteriorating. The statement of activities presents information showing how the government’s net position changed during the most recent fiscal year. All changes in net position are reported as soon as the underlying event giving rise to the change occurs, regardless of the timing of related cash flows. Thus, revenues and expenses are reported in this statement for some items that will only result in cash flows in future fiscal periods (e.g., uncollected taxes and earned but unused vacation leave).

3

Both of the government-wide financial statements distinguish functions of the City of Edgewater that are principally supported by taxes and intergovernmental revenues (governmental activities) from other functions that are intended to recover all or a significant portion of their costs through user fees and charges (business-type activities). The governmental activities of the City of Edgewater include general government, public safety, transportation/public works and leisure services. The business-type activities of the City of Edgewater include water and sewer, refuse collection and stormwater management. The government-wide financial statements include only the City of Edgewater itself (known as the primary government). The City of Edgewater has one component unit, the Edgewater Community Redevelopment Agency (CRA). The CRA is reported as if it were part of the primary government as a major special revenue fund. The government-wide financial statements can be found on pages 15-17 of this report. Fund Financial Statements A fund is a grouping of related accounts that is used to maintain control over resources that have been segregated for specific activities or objectives. The City of Edgewater, like other state and local governments, uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. All of the funds of the City of Edgewater can be divided into three categories: governmental funds, proprietary funds and fiduciary funds. Governmental Funds - Governmental funds are used to account for essentially the same functions reported as governmental activities in the government-wide financial statements. However, unlike the government-wide financial statements, governmental fund financial statements focus on near-term inflows and outflows of spendable resources, as well as on balances of spendable resources available at the end of the fiscal year. Such information may be useful in evaluating a government’s near-term financing requirements. Because the focus of governmental funds is narrower than that of the government-wide financial statements, it is useful to compare the information presented for governmental funds with similar information presented for governmental activities in the government-wide financial statements. By doing so, readers may better understand the long-term impact of the government’s near-term financing decisions. Both the governmental fund balance sheet and the governmental fund statement of revenues, expenditures, and changes in fund balances provide a reconciliation to facilitate this comparison between governmental funds and governmental activities. The City of Edgewater maintains ten individual governmental funds. Information is presented separately in the governmental fund balance sheet and in the governmental fund statement of revenues, expenditures, and changes in fund balances for the general fund, the community redevelopment agency (CRA) and the capital projects fund, all of which are considered to be major funds. Data from the other eight governmental funds are combined into a single, aggregated presentation. Individual fund data for each of these non-major governmental funds is provided in the form of combining statements elsewhere in this report. The City of Edgewater adopts an annual appropriated budget for all of its governmental funds. Budgetary comparison statements have been provided for the general fund and community redevelopment fund to demonstrate compliance with their budgets on pages 22 and 23 respectively. Budgetary comparison schedules have been provided for the non-major, debt service and capital projects funds at pages 70-75.

4

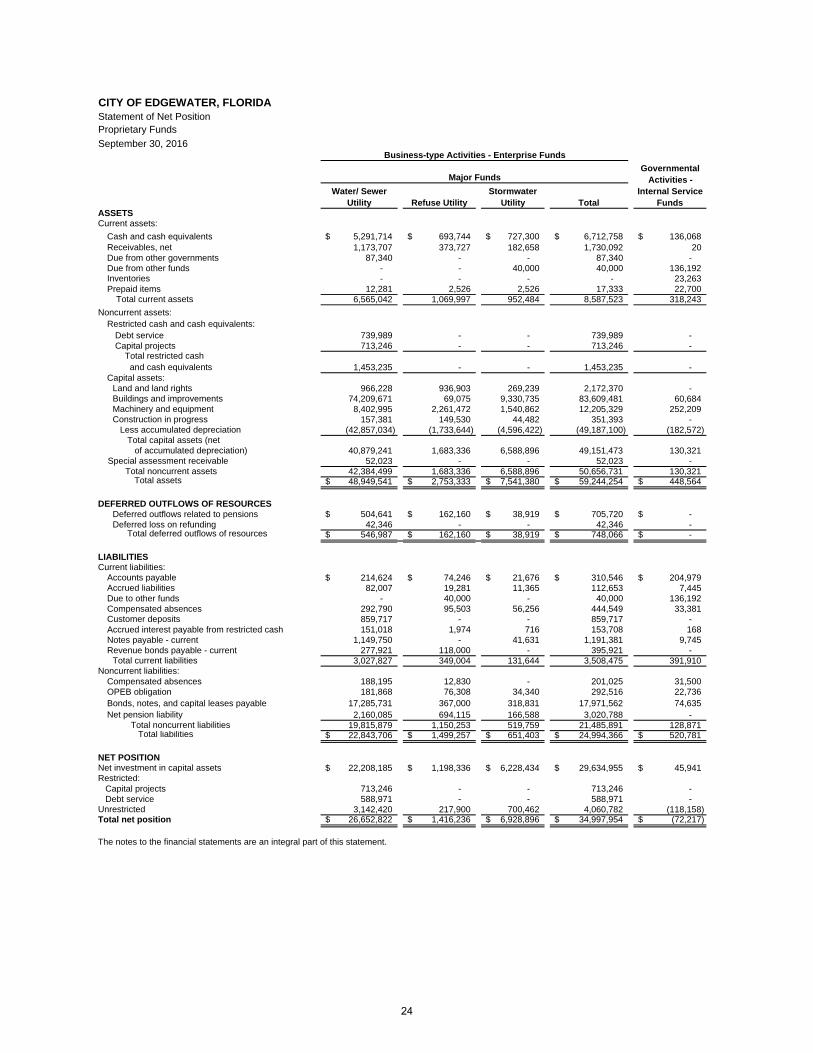

The basic governmental fund financial statements can be found on pages 18-23 of this report. Proprietary Funds - The City of Edgewater maintains two types of proprietary funds, enterprise funds and internal service funds. Both enterprise and internal service funds are used to report the same functions presented as business-type activities in the government-wide financial statements. The City of Edgewater uses enterprise funds to account for water and sewer, refuse collection and stormwater management. Internal service funds are used to account for management information systems, fleet servicing, and property and casualty, health, dental, life, and workers compensation insurances. Proprietary funds provide the same type of information as the government-wide financial statements, only in more detail. The proprietary fund financial statements provide separate information for water and sewer, refuse collection and stormwater management which are all considered to be major funds. The basic proprietary fund financial statements can be found on pages 24-26 of this report. Internal Services Funds – Internal Service funds are used to account for the financing of centralized services to the City departments on a cost-reimbursement basis. The basic internal services fund financial statements can be found on pages 77-80 of this report. Fiduciary Funds - Fiduciary funds are used to account for resources held for the benefit of parties outside the government. Fiduciary funds are not reflected in the government-wide financial statements because the resources of those funds are not available to support the City of Edgewater’s own programs. The accounting used for fiduciary funds is much like that used for the proprietary funds. The basic fiduciary fund financial statements can be found on pages 81-83 of this report. Notes to the Financial Statements The notes provide additional information that is essential to a full understanding of the data provided in the government-wide and fund financial statements. The notes to financial statements can be found on pages 29-57 of this report. Other Information In addition to the basic financial statements and accompanying notes, this report also presents certain required supplementary information concerning the City’s progress in its obligation to provide pension benefits to its employees which can be found on pages 58-63. The combining statements referred to earlier in connection with non-major governmental funds are presented immediately following the notes to financial statements and required supplementary information. Combining and individual fund statements and schedules can be found on pages 65-69 of this report. Government-Wide Financial Analysis As noted earlier, net position may serve over time as a useful indicator of a government’s financial position. In the case of the City of Edgewater, assets exceeded liabilities by $74,331,779 at the

5

close of the most recent fiscal year. The following table reflects the condensed statement of net position for the current and prior years. For more detail see the Statement of Net Position on page 15.

At the end of the current fiscal year, the government’s liabilities decreased by $1,911,493 which is mainly attributed to the reduction of Water & Sewer system debt by $2,473,521. The City’s net pension liability increased by $1,353,487 during the current year. Accounts payable decreased $297,751 mainly from major capital improvement projects being completed. Ninety-five percent (95%) of the City’s net position reflect its investment in capital assets (e.g., land, buildings, improvements, infrastructure and equipment) less any related debt used to acquire those assets that is still outstanding. The City uses these capital assets to provide services to citizens; consequently, these assets are not available for future spending. Although the City of Edgewater’s investment in its capital assets is reported net of related debt, it should be noted that the resources needed to repay this debt must be provided from other sources, since the capital assets themselves cannot be used to liquidate these liabilities. An additional portion of the City of Edgewater’s net position (3%) represents resources that are subject to external restrictions on how they may be used. The remaining balance of Net Position is unrestricted and may be used to meet the government’s ongoing obligations to citizens and creditors. At the end of the current fiscal year, the City of Edgewater is able to report positive balances in all categories of net position except for Governmental unrestricted which is due to the City’s net pension liability being reflected on the statements.

Assets: 2016 2015 2016 2015 2016 2015

Current and other assets $4,976,732 $6,598,006 $10,052,781 $9,872,715 $15,029,513 $16,470,721

Capital Assets 42,877,980 43,323,485 49,151,473 50,681,937 92,029,453 94,005,422

Total Assets 47,854,712 49,921,491 59,204,254 60,554,652 107,058,966 110,476,143

2,769,798 1,574,814 748,066 448,151 3,517,864 448,151

Liabilities:

Long term liabilities 10,219,712 9,811,830 23,517,742 25,461,895 33,737,454 35,273,725

Other liabilities 740,986 1,079,457 1,436,624 1,473,375 2,177,610 2,552,832

Total Liabilities 10,960,698 10,891,287 24,954,366 26,935,270 35,915,064 37,826,557

329,987 1,138,286 - 321,034 329,987 321,034

Net Position:

Net investment in capital assets 41,225,542 41,696,833 29,634,955 29,142,964 70,860,497 70,839,797

Restricted 783,398 1,325,008 1,302,217 1,900,301 2,085,615 3,225,309

Unrestricted (2,675,115) (3,555,109) 4,060,782 2,703,234 1,385,667 (851,875)

Total Net Position $39,333,825 $39,466,732 $34,997,954 $33,746,499 $74,331,779 $73,213,231

City of Edgewater’s Statement of Net Position (in whole dollars)

Governmental Activities Business-Type Activities Total Primary Government

Total deferred outflows of resources

Total deferred intflows of resources

6

The government’s net position increased $1,118,548 in the current fiscal year. The government’s restricted net position decreased by $1,139,694 in the current fiscal year. This was mainly attributed to a decrease of $701,041 in net position being restricted for debt service as well as a decrease of $569,614 in net position being restricted for public safety related to the firefighter net pension asset. Further explanations of the decrease are detailed below. The following table reflects the condensed Statement of Activities for the current and prior years. For more detail see the Statement of Activities on page 16-17.

7

The remainder of this page intentionally left blank. Statement of Activities Governmental Activities - Governmental activities decreased the City of Edgewater’s net position by $132,907 which is a $1,382,054 decline from the previous year’s increase of $1,249,147. Key elements of this decrease are as follows:

• Capital grants decreased by $986,529 due to decreased sidewalk construction activity. • Expenses increased in total by $1,182,787, the majority of which relates to an increase in

Public Safety expenses of $797,027 due to increased staffing levels during the year.

• General Administrative expenses increased $498,652 from the prior year due to grant expenditures in the current year and increased internal service funds expenditures.

Business-Type Activities - Business-type activities increased the City of Edgewater’s net position by $1,251,455 as compared to a decrease of $253,452 in the prior year. Key elements of this increase are as follows:

• Charges for services reflect an overall 8.00% increase this year as compared to a 2.58% increase last year. Charge for services increased by $1,015,865 over the previous year. All of the rates are adjusted per continuing professional rate study analyses. Refuse and Stormwater rates were adjusted for the first time in several years in FY 2016.

• Miscellaneous revenues increased $279,025 primarily due to an insurance recovery for

damages to the wastewater treatment plant electricity feed line. The damage was done by a private utility contractor servicing a private utility line.

• Water and Sewer and Refuse operations expenses decreased by $280,553. This decrease

was due to savings throughout various operational lines.

The remainder of this page intentionally left blank.

8

9

10

Financial Analysis of the Government’s Funds As noted earlier, the City of Edgewater used fund accounting to ensure and demonstrate compliance with finance-related requirements. Governmental Funds - The focus of the City’s governmental funds is to provide information on near-term inflows, outflows, and balances of spendable resources. Such information is useful in assessing the City of Edgewater’s financing requirements. In particular, unassigned fund balance may serve as a useful measure of a government’s net resources available for spending at the end of the fiscal year. As of the end of the current fiscal year, the City of Edgewater’s governmental funds reported combined ending fund balances of $4,283,009, a decrease of $430,392 in comparison with the prior year. Approximately 55% of this amount or $2,376,555 constitutes unassigned fund balance, which is available for spending at the City’s discretion. The City has assigned fund balance for the replacement of City Hall in the amount of $707,749, and $376,235 for the subsequent year’s budget appropriation. Restricted fund balance of $792,429 is for scholarships, public safety, debt service, community redevelopment and capital projects. Nonspendable fund balance of $30,041 is held for inventories and prepaids. The General Fund is the chief operating fund of the City of Edgewater. At the end of the current fiscal year, unassigned fund balance of the General Fund was $2,376,555, while total fund balance was $3,536,118. As a measure of the General Fund’s liquidity, it may be useful to compare both unassigned fund balance and total fund balance to total fund expenditures. Unassigned fund balance represents 16% of the total General Fund expenditures, while total fund balance represents 24% of that same amount. During the current fiscal year, the fund balance of the General Fund decreased by $511,187. This decrease was attributed to increased staffing in Public Safety, increased debt service, and capital lease proceeds (in the previous year). During the current fiscal year, the Capital projects fund has continued to add or improve various sidewalks in the City, and to increase or improve recreational facilities. Fiscal Year 2016 is the first year of activity for the City’s recently established Community Redevelopment Agency Fund (CRA). This agency is established for the purpose of making improvements to core downtown properties to enhance economic activity in the City. During the year revenues were collected from the County and City. Expenditures are budgeted for the Northern Gateway Park and pond project. Proprietary Funds - The City of Edgewater’s proprietary funds provide the same type of information found in the government-wide financial statements, but in more detail. Unrestricted net position of the proprietary funds (including enterprise and internal service funds) at the year-end amounted to $3,942,624. The total increase in net position for these funds was $1,131,556. Other factors concerning the finances of the enterprise funds have already been addressed in the discussion of the City of Edgewater’s business-type activities.

11

General Fund Budgetary Highlights During the year, actual revenues were $375,812 less than budgeted revenues primarily due to a residential construction mitigation grant not commencing yet. Actual expenditures were $569,019 less than budgeted expenditures primarily due to expenditures related to residential construction mitigation grant not yet occurring and unfilled Culture and Recreation positions. The final revenue budget was increased from the original budget by $478,387 primarily due to a discontinued joint venture payout ($163K), increased intergovernmental revenues ($143K), retirement plan forfeitures ($18K), and increased utility and franchise taxes ($68). The expenditures budget was increased by $1,164,151 primarily for five new vehicles ($491K), a debt payoff of a 2010 rescue vehicle ($163K), and various other expenditures ($272K) that included two additional police officers, and necessary repairs to City Hall. Capital Asset and Debt Administration Capital Assets - The City of Edgewater’s investment in capital assets for its governmental and business-type activities as of September 30, 2016, amounts to $92,029,453 net of accumulated depreciation. This investment in capital assets includes land, buildings, improvements, machinery and equipment and infrastructure. The total decrease in the City’s investment in capital assets for the current fiscal year was 2.1%.

Additional information on the City of Edgewater’s capital assets can be found in Note IV E of the notes to the financial statements on pages 41-42 of this report. Long-Term Debt At the end of the current fiscal year, the City of Edgewater had total debt outstanding of $21,211,302. This debt includes notes payable, state revolving loan and capital leases. In FY 2016, the City refinanced the Water and Wastewater Refunding Revenue Bond, Series 2009 and Water and Wastewater System Refunding Revenue Bond, Series 2012 with a single Utility System Refunding Revenue Note, Series 2016. The City is current on all required debt service obligations.

2016 2015 2016 2015 2016 2015

Land $ 23,171,411 $ 23,164,264 $ 2,172,370 $ 2,455,915 $ 25,343,781 $ 25,620,179

Buildings 4,422,090 4,649,274 7,169,607 8,010,646 11,591,697 12,659,920

Improvements 7,079,491 7,652,314 35,605,954 36,189,338 42,685,445 43,841,652

Machinery and equipment 1,933,834 1,517,452 3,852,149 3,832,436 5,785,983 5,349,888

Infrastructure 5,827,415 3,422,467 - - 5,827,415 3,422,467

Construction in progress 443,739 2,917,714 351,393 193,602 795,132 3,111,316

Total $ 42,877,980 $ 43,323,485 $ 49,151,473 $ 50,681,937 $ 92,029,453 $ 94,005,422

Governmental Activities Business-Type Activities Total Primary Government

City of Edgewater’s Capital Assets(net of depreciation)(in whole dollars)

12

During the current fiscal year, the City’s total debt decreased by $2,858,704 (12%). Additional information on the City of Edgewater’s long-term debt can be found in Note IV G of the notes to the financial statements on pages 43-46 of this report. Reserve Policy The City Council has approved a Reserve Policy, which was adopted within the City Charter. The policy addresses that the City is required to maintain reserves at a minimum of 15 percent with a maximum of 25 percent of the general fund. The reserve range is established based on a percentage of current years’ budget. Reserve levels above the top of the range are deemed to be available for capital or other lawful purposes. The Reserve amount per Charter is currently set at $2,258,197 (15%) of the FY2016 – 2017 General Fund Budget. The City Council has designated $707,749 towards the future replacement of City Hall and $376,235 for subsequent year’s budget appropriation. The nonspendable balance is $30,041 with restricted balances of $45,538. The amount available for capital or other lawful purposes less any reserves or set asides is $2,376,555 at September 30, 2016. In November 2016, voter’s approved a charter amendment requiring the City to maintain reserves at a minimum of 15 percent of all operating funds (General, Water & Sewer, Refuse and Stormwater). This will affect future year’s reserves. Next Year’s Budget and Rates The City Council adopted a conservative budget for Fiscal Year 2017. The proposed budget contains many ambitious work plan objectives that are intended to address the highest priorities in the community and the goals of the City Council. This budget also sets the financial foundation to establish an accurate and understandable assessment and tracking of the uses and sources of all funds. The 2017 budget presents a number of opportunities and challenges to improve overall service to the community while dealing with the slow recovery as a result of the severe economic downturn. By any standard this is a very aggressive program of work that will challenge the capacity of staff and the City Council to accomplish under the slow recovery. The proposed General Fund budget for Fiscal Year 2017 includes the following assumptions:

• Realization of increased revenues as a result of the current economic conditions. • Modest increases in operating expenditures consistent with the revenue forecasts. • Maintenance of service levels and program to the extent possible and minimal

reductions in service levels where appropriate. • The Issuance of the March 15, 2016 voter approved GO Bond for parks improvements.

2016 2015 2016 2015 2016 2015

Bonds payable $ - $ - $ - $ 11,439,000 $ - $ 11,439,000 Notes payable 1,358,288 1,462,674 13,692,712 4,454,327 15,051,000 5,917,001 g loan - - 5,866,152 6,139,058 5,866,152 6,139,058 Capital leases 294,150 574,947 - - 294,150 574,947

$ 1,652,438 $ 2,037,621 $ 19,558,864 $ 22,032,385 $ 21,211,302 $ 24,070,006

Governmental Activities Business-Type Activities Total Primary Government

City of Edgewater’s Outstanding Debt(in whole dollars)

13

• Hurricane Matthew impacted our area on October 6, 2016 creating the need to makeamendments to our approved budget in the amount of $1,729,464 that effected ourCapital Outlay and held all open positions.

Requests for Information

This financial report is designed to provide a general overview of the City of Edgewater’s finances for those with an interest in the government’s finances. Questions concerning any of the information should be addressed to the office of the Finance Director, City of Edgewater, P.O. Box 100, Edgewater, Florida 32132-0100.

14

CITY OF EDGEWATER, FLORIDAStatement of Net PositionSeptember 30, 2016

Governmental -type Activities

Business-type Activities Total

ASSETS

Cash and cash equivalents 1,412,599$ 6,712,758$ 8,125,357$

Investments 2,333,531 - 2,333,531

Receivables, net 391,791 1,730,092 2,121,883

Special assessment receivable, net - 52,023 52,023

Due from other governments 762,807 87,340 850,147 Inventories and prepaids 76,004 17,333 93,337

Restricted assets:

Cash and cash equivalents - 1,453,235 1,453,235 Capital Assets

Nondepreciable assets 23,615,150 2,523,763 26,138,913 Depreciable assets, net 19,262,830 46,627,710 65,890,540

Total assets 47,854,712$ 59,204,254$ 107,058,966$

DEFERRED OUTFLOWS OF RESOURCESDeferred outflows related to pensions 2,769,798$ 705,720$ 3,475,518$ Deferred Loss on Refunding - 42,346 42,346

Total deferred outflows of resources 2,769,798$ 748,066$ 3,517,864$

LIABILITIES

Accounts payable and other current liabilities 660,112$ 423,199$ 1,083,311$

Accrued interest payable 16,890 153,708 170,598

Unearned revenue 62,270 - 62,270

Due to other governments 1,714 - 1,714

Customer deposits - 859,717 859,717

Noncurrent liabilities

Due within one year

Bonds, notes, and capital leases payable 202,249 1,587,302 1,789,551

Compensated absences 913,311 444,549 1,357,860

Due in more than one year

Bonds, notes, and capital leases payable 1,450,189 17,971,562 19,421,751

Compensated absences 678,230 201,025 879,255

OPEB obligation 585,316 292,516 877,832

Net pension liability 6,390,417 3,020,788 9,411,205

Total liabilities 10,960,698$ 24,954,366$ 35,915,064$

DEFERRED INFLOWS OF RESOURCESDeferred inflows related to pensions 329,987$ -$ 329,987$

NET POSITION

Net investment in capital assets 41,225,542$ 29,634,955$ 70,860,497$

Restricted for:

Debt service 38,781 588,971 627,752

Public safety 73,286 - 73,286

Capital projects 660,075 713,246 1,373,321

Community redevelopment 9,398 - 9,398

Scholarships 1,858 - 1,858

Unrestricted (2,675,115) 4,060,782 1,385,667

Total net position 39,333,825$ 34,997,954$ 74,331,779$

The notes to the financial statements are an integral part of this statement.

15

CITY OF EDGEWATER, FLORIDAStatement of ActivitiesFor the Fiscal Year Ended September 30, 2016

Functions / Programs ExpensesCharges for

Services

Operating Grants and

Contributions

Capital Grants and

Contributions Governmental activities:

General administrative 3,112,845$ 193,140$ -$ 346,749$ Public works 1,914,982 382,989 641,231 217,564 Public safety 7,164,944 773,067 191,145 30,822 Culture and recreation 1,534,765 51,991 - 107,509 Community Redevelopment 4,955 - - - Interest on long-term debt 56,794 - - -

Total governmental activities 13,789,285 1,401,187 832,376 702,644

Business-type activities: Water / Sewer 8,697,283 9,284,327 - 334,843 Refuse 2,427,299 2,962,543 - - Stormwater 1,336,821 1,466,495 - -

Total business-type activities 12,461,403 13,713,365 - 334,843

Total primary government 26,250,688$ 15,114,552$ 832,376$ 1,037,487$

General revenues: Property taxesUtility and franchise taxesIntergovernmental shared revenue - non-programInvestment earningsMiscellaneous revenue

TransfersTotal general revenues and transfers

Change in net position

Net position - beginningNet position - ending

The notes to the financial statements are an integral part of this statement.

Program Revenues

16

Governmental Activities

Business-type Activities Total

(2,572,956)$ -$ (2,572,956)$ (673,198) - (673,198)

(6,169,910) - (6,169,910) (1,375,265) - (1,375,265)

(4,955) - (4,955)(56,794) - (56,794)

(10,853,078) - (10,853,078)

- 921,887 921,887- 535,244 535,244- 129,674 129,674- 1,586,805 1,586,805

(10,853,078) 1,586,805 (9,266,273)

4,572,959 - 4,572,959 3,222,232 - 3,222,232 2,028,373 - 2,028,373

38,006 5,704 43,710106,099 411,448 517,547752,502 (752,502) -

10,720,171 (335,350) 10,384,821 (132,907) 1,251,455 1,118,548

39,466,732 33,746,499 73,213,231 39,333,825$ 34,997,954$ 74,331,779$

Changes in Net PositionNet (Expense) Revenue and

17

CITY OF EDGEWATER, FLORIDABalance Sheet

Governmental Funds

September 30, 2016

General FundCapital Projects

Fund CRA Fund

Other Governmental

Funds

Total Governmental

FundsASSETS Cash 562,367$ 378,709$ 9,398$ 326,057$ 1,276,531$ Investments 2,333,531 - - - 2,333,531

Receivables--net of allowance for uncollectibles 391,732 - - 39 391,771 Due from other governments 542,095 174,800 - 45,912 762,807 Inventories and prepaids 30,041 - - - 30,041

Total assets 3,859,766$ 553,509$ 9,398$ 372,008$ 4,794,681$

LIABILITIES Accounts payable 98,935$ 188,024$ -$ -$ 286,959$ Accrued liabilities 160,729 - - - 160,729 Due to other governments 1,714 - - - 1,714 Unearned revenues 62,270 - - - 62,270

Total liabilities 323,648 188,024 - - 511,672

FUND BALANCESNonspendable:

Inventories and prepaids 30,041 - - - 30,041 Restricted for:

Scholarships 1,858 - - - 1,858 Public safety - - - 73,286 73,286 Debt service 43,680 - - 4,132 47,812 Community redevelopment - - 9,398 - 9,398 Capital projects - 365,485 - 294,590 660,075

Assigned to:Subsequent year's budget appropriation of fund balance 376,235 - - - 376,235 City Hall 707,749 - - - 707,749

Unassigned 2,376,555 - - - 2,376,555

Total fund balances 3,536,118 365,485 9,398 372,008 4,283,009

Total liabilities and fund balances 3,859,766$ 553,509$ 9,398$ 372,008$ 4,794,681$

The notes to the financial statements are an integral part of this statement.

18

CITY OF EDGEWATER, FLORIDAReconciliation of the Balance Sheet of Governmental FundsTo the Statement of Net PositionSeptember 30, 2016

Total governmental funds fund balance 4,283,009$

Amounts reported for governmental activities in the statement of net position are different because:

in the funds - total less accumulated depreciation.

Land and land rights 23,171,411Buildings and improvements 26,998,428Infrastructure 59,237,749Furniture and equipment 4,971,749Construction in progress 443,739Accumulated depreciation (72,075,417)

42,747,659

(72,217)

On the governmental fund statements, a net pension liability/asset is not recorded until an

amount is due and payable and the pension plan’s fiduciary net position is not sufficient

for payment of those benefits (no such liability exists at the end of the current fiscal

year). On the Statement of Net Position, the City's net pension liability/asset of the defined

benefit pension plans is reported as a noncurrent liability. Additionally, deferred

outflows and deferred inflows related to pensions are also reported.

Net pension liability (6,390,417)

Deferred outflows related to pensions 2,769,798

Deferred inflows related to pensions (329,987) (3,950,606)

Compensated absences 1,526,660 OPEB 562,580Long-term debt 1,568,058

(3,657,298)

(16,722)

Net position of governmental activities 39,333,825$

The notes to the financial statements are an integral part of this statement.

Capital assets used in governmental activities are not financial resources and, therefore, are not reported

Long-term liabilities are not due and payable in the current period and, therefore, are not reported in the funds.

Accrued interest payable on bonds that is not recognized on the fund statements.

Internal service funds are used by management to charge the costs of fleet, management information systems

and insurance activities to individual funds. The assets and liabilities of the internal service funds are included in governmental activities in the statement of net position.

19

CITY OF EDGEWATER, FLORIDAStatement of Revenues, Expenditures, and Changes in Fund BalancesGovernmental FundsFor the Fiscal Year Ended September 30, 2016

General FundCapital Projects

Fund CRA Fund

Other Governmental

Funds

Total Governmental

FundsREVENUES Taxes: Property 4,530,693$ -$ 9,394$ 32,872$ 4,572,959$ Utility and franchise taxes 3,222,232 - - - 3,222,232 Intergovernmental 3,013,844 489,957 - 2,731 3,506,532 Licenses and permits 398,346 - - - 398,346Charges for services 1,736,070 - - - 1,736,070 Fines and forfeitures 210,387 - - 56,477 266,864Investment earnings 37,652 - 4 177 37,833Impact fees - - - 160,103 160,103Miscellaneous revenue 265,625 - - - 265,625

Total revenues 13,414,849 489,957 9,398 252,360 14,166,564

EXPENDITURES Current: Legislative 99,820 - - - 99,820 Executive 619,910 - - - 619,910 Legal counsel 158,443 - - - 158,443 Community development 983,354 - - - 983,354 Public works 757,743 293,332 - - 1,051,075 Public safety: Law enforcement 3,521,013 - - 3,231 3,524,244 Fire and emergency services 3,460,655 - - - 3,460,655 Code enforcement 125,334 - - - 125,334 Animal services 109,865 - - - 109,865 Culture and recreation 1,265,641 - - - 1,265,641 General administrative services 2,234,076 - - - 2,234,076 Debt Service: Principal 355,675 - - 20,000 375,675 Interest 37,736 - - 12,112 49,848Capital outlay 761,027 488,911 - - 1,249,938

Total expenditures 14,490,292 782,243 - 35,343 15,307,878 Excess (deficiency) of revenues over (under) expenditures (1,075,443) (292,286) 9,398 217,017 (1,141,314)

OTHER FINANCING SOURCES (USES) Transfers in 764,611 254,385 - - 1,018,996 Transfers out (206,865) - - (107,719) (314,584) Sale of capital assets 6,510 - - - 6,510 Total other financing sources (uses) 564,256 254,385 - (107,719) 710,922

Net change in fund balances (511,187) (37,901) 9,398 109,298 (430,392)

Beginning fund balances 4,047,305 403,386 - 262,710 4,713,401

Ending fund balances 3,536,118$ 365,485$ 9,398$ 372,008$ 4,283,009$

The notes to the financial statements are an integral part of this statement.

20

CITY OF EDGEWATER, FLORIDAReconciliation of the Statement of Revenues,

Expenditures, and Changes in Fund Balances of Governmental Funds

To the Statement of Activities

For the Fiscal Year Ended September 30, 2016

Net change in fund balances - total governmental funds (430,392)$

Expenditure for capital assets 1,249,938

Current year depreciation (1,629,923)

(379,985)

(3,325)

(163,210)

Changes in compensated absences 116,756

Changes in OPEB obligation (71,828)

Changes in interest payable 548

45,476

(119,899)

However, in the Statement of Activities, the amount contributed to defined benefit pension plans

reduces future the net pension liability/asset. Also included in pension expense in the Statement of Activities

are deferred inflow and deferred outflow amounts required to be amortized.

Change in net pension liability/asset and deferred inflows/outflows related to pensions 542,753

The issuance of long-term debt (I.e., bonds and leases ) provides current financial resources to governmental

funds, while the repayment of the principal long-term debt consumes the current financial resources of

governmental funds. Neither transaction has any effect on net position. Also, governmental funds report the

effect of premiums, discounts, and deferred amount on refunding, when debt is first issued, whereas these

amounts are deferred and amortized in the Statement of Activities.

Principal payments 375,675

Change in net position of governmental activities (132,907)$

The notes to the financial statements are an integral part of this statement.

Amounts recorded for governmental activities in the statement of activities are different because:

Governmental funds report capital outlays as expenditures. However, in the statement of activities the cost of those assets is allocated over their estimated useful lives and reported as depreciation expense. This is the amount by which capital outlays exceeded depreciation in the current period.

The net revenue of certain activities of internal service funds is reported with governmental activities.

Governmental funds report contributions to defined benefit pension plans as expenditures.

Some expenses reported in the statement of activities do not require the use of current financial resources and, therefore, are not reported as expenditures in the governmental funds.

The net effect of various miscellaneous transactions involving capital assets (i.e. sales, trade-ins,

donations, CIP project abandoned) is to decrease net position.

Investment in joint venture was not a financial asset and therefore was not reported in the funds.

Because of this, the amount of gain recorded on the sale differs for the governmental funds.

21

CITY OF EDGEWATER, FLORIDAStatement of Revenues, Expenditures, and

Changes in Fund Balances--Budget and ActualGeneral Fund

For the Fiscal Year Ended September 30, 2016

Variance with Final Budget-

Original Final Actual

Amounts Positive

(Negative)

REVENUES

Taxes:

Property 4,520,903$ 4,530,693$ 4,530,693$ -$

Utility and franchise taxes 3,210,830 3,279,169 3,222,232 (56,937)

Intergovernmental 3,124,856 3,267,600 3,013,844 (253,756)

Licenses and permits 360,900 401,259 398,346 (2,913)

Charges for services 1,785,735 1,779,832 1,736,070 (43,762)

Fines and forfeitures 206,300 207,375 210,387 3,012

Investment earnings 42,750 42,750 37,652 (5,098)

Miscellaneous revenue 60,000 281,983 265,625 (16,358)

Total revenues 13,312,274 13,790,661 13,414,849 (375,812)

EXPENDITURES

Current:

Legislative 113,847 113,847 99,820 14,027

Executive 654,460 628,960 619,910 9,050

Legal counsel 90,000 158,443 158,443 -

Community development 1,194,973 1,181,753 983,354 198,399

Public works 792,132 832,132 757,743 74,389

Public safety:

Law enforcement 3,457,093 3,520,713 3,521,013 (300)

Fire and emergency services 3,346,942 3,485,483 3,460,655 24,828

Code enforcement 133,560 133,560 125,334 8,226

Animal services 118,369 118,369 109,865 8,504

Culture and recreation 1,361,735 1,361,811 1,265,641 96,170

General administrative services 2,142,880 2,286,316 2,234,076 52,240

Debt service:

Principal 196,625 357,423 355,675 1,748

Interest 35,303 37,736 37,736 -

Capital outlay 257,241 842,765 761,027 81,738

Total expenditures 13,895,160 15,059,311 14,490,292 569,019

Excess (deficiency) of revenues over

(under) expenditures (582,886) (1,268,650) (1,075,443) 193,207

OTHER FINANCING SOURCES (USES)

Transfers in 763,866 763,866 764,611 745

Transfers out (440,980) (206,865) (206,865) -

Sale of capital assets 10,000 10,000 6,510 (3,490)

Total other financing sources (uses) 332,886 567,001 564,256 (2,745)

Net change in fund balances (250,000) (701,649) (511,187) 190,462

Beginning fund balances 4,047,305 4,047,305 4,047,305 -

Ending fund balances 3,797,305$ 3,345,656$ 3,536,118$ 190,462$

The notes to the financial statements are an integral part of this statement.

Budgeted Amounts

22

CITY OF EDGEWATER, FLORIDAStatement of Revenues, Expenditures, andChanges in Fund Balances--Budget and ActualCRA FundFor the Fiscal Year Ended September 30, 2016

Variance with Final Budget-

Original Final Actual

Amounts Positive

(Negative) REVENUES Property tax 11,387$ 11,387$ 9,394$ (1,993)$ Investment earnings - - 4 4 Total revenues 11,387 11,387 9,398 (1,989)

EXPENDITURES

Other Services & Charges 11,387 11,387 - 11,387 Total expenditures 11,387 11,387 - 11,387 Excess (deficiency) of revenues over (under) expenditures - - 9,398 9,398

Beginning fund balances - - - -

Ending fund balances -$ -$ 9,398$ 9,398$

Budgeted Amounts

23

CITY OF EDGEWATER, FLORIDAStatement of Net PositionProprietary Funds

September 30, 2016

Water/ Sewer Utility Refuse Utility

Stormwater Utility Total

ASSETS Current assets:

Cash and cash equivalents 5,291,714$ 693,744$ 727,300$ 6,712,758$ 136,068$ Receivables, net 1,173,707 373,727 182,658 1,730,092 20Due from other governments 87,340 - - 87,340 -Due from other funds - - 40,000 40,000 136,192 Inventories - - - - 23,263Prepaid items 12,281 2,526 2,526 17,333 22,700

Total current assets 6,565,042 1,069,997 952,484 8,587,523 318,243

Noncurrent assets:Restricted cash and cash equivalents:

Debt service 739,989 - - 739,989 - Capital projects 713,246 - - 713,246 - Total restricted cash and cash equivalents 1,453,235 - - 1,453,235 -

Capital assets: Land and land rights 966,228 936,903 269,239 2,172,370 - Buildings and improvements 74,209,671 69,075 9,330,735 83,609,481 60,684 Machinery and equipment 8,402,995 2,261,472 1,540,862 12,205,329 252,209 Construction in progress 157,381 149,530 44,482 351,393 - Less accumulated depreciation (42,857,034) (1,733,644) (4,596,422) (49,187,100) (182,572) Total capital assets (net

of accumulated depreciation) 40,879,241 1,683,336 6,588,896 49,151,473 130,321 Special assessment receivable 52,023 - - 52,023 -

Total noncurrent assets 42,384,499 1,683,336 6,588,896 50,656,731 130,321Total assets 48,949,541$ 2,753,333$ 7,541,380$ 59,244,254$ 448,564$

DEFERRED OUTFLOWS OF RESOURCES Deferred outflows related to pensions 504,641$ 162,160$ 38,919$ 705,720$ -$ Deferred loss on refunding 42,346 - - 42,346 - Total deferred outflows of resources 546,987$ 162,160$ 38,919$ 748,066$ -$

LIABILITIES Current liabilities:

Accounts payable 214,624$ 74,246$ 21,676$ 310,546$ 204,979$ Accrued liabilities 82,007 19,281 11,365 112,653 7,445Due to other funds - 40,000 - 40,000 136,192 Compensated absences 292,790 95,503 56,256 444,549 33,381Customer deposits 859,717 - - 859,717 -Accrued interest payable from restricted cash 151,018 1,974 716 153,708 168Notes payable - current 1,149,750 - 41,631 1,191,381 9,745Revenue bonds payable - current 277,921 118,000 - 395,921 -

Total current liabilities 3,027,827 349,004 131,644 3,508,475 391,910 Noncurrent liabilities:

Compensated absences 188,195 12,830 - 201,025 31,500OPEB obligation 181,868 76,308 34,340 292,516 22,736Bonds, notes, and capital leases payable 17,285,731 367,000 318,831 17,971,562 74,635 Net pension liability 2,160,085 694,115 166,588 3,020,788 -

Total noncurrent liabilities 19,815,879 1,150,253 519,759 21,485,891 128,871 Total liabilities 22,843,706$ 1,499,257$ 651,403$ 24,994,366$ 520,781$

NET POSITIONNet investment in capital assets 22,208,185$ 1,198,336$ 6,228,434$ 29,634,955$ 45,941$ Restricted: Capital projects 713,246 - - 713,246 - Debt service 588,971 - - 588,971 -Unrestricted 3,142,420 217,900 700,462 4,060,782 (118,158) Total net position 26,652,822$ 1,416,236$ 6,928,896$ 34,997,954$ (72,217)$

The notes to the financial statements are an integral part of this statement.

Business-type Activities - Enterprise Funds

Major FundsGovernmental

Activities - Internal Service

Funds

24

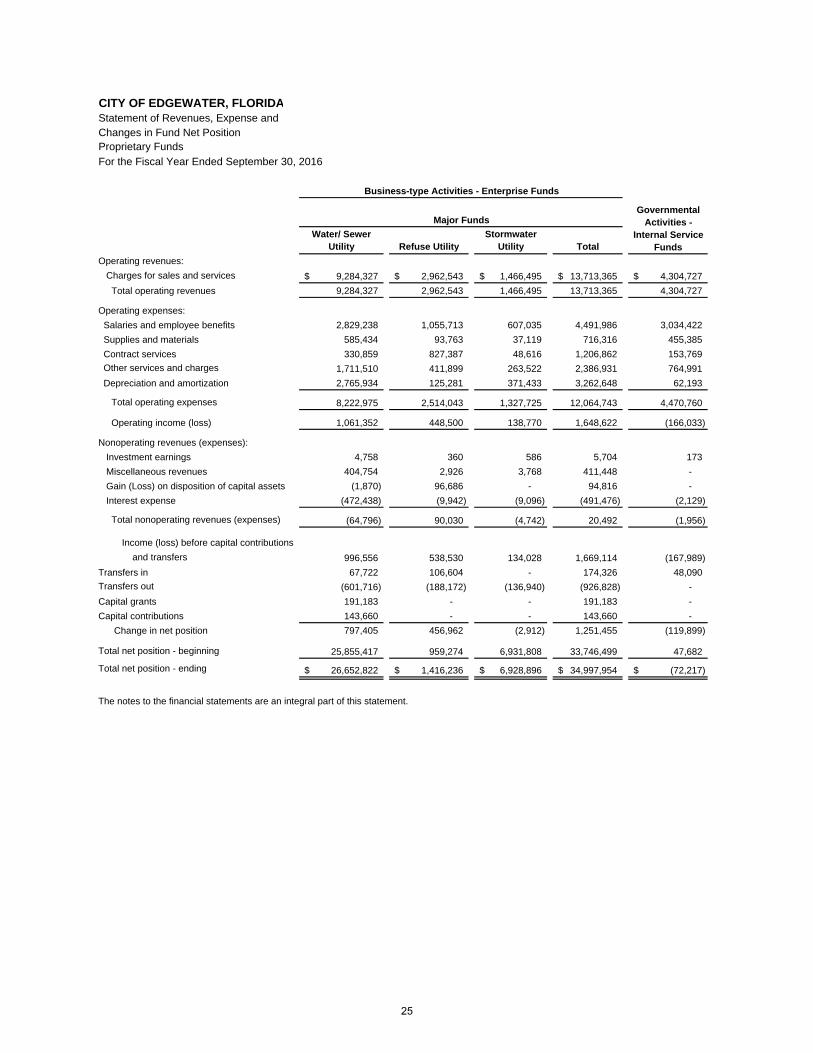

CITY OF EDGEWATER, FLORIDAStatement of Revenues, Expense andChanges in Fund Net PositionProprietary Funds

For the Fiscal Year Ended September 30, 2016

Water/ Sewer Utility Refuse Utility

Stormwater Utility Total

Operating revenues:

Charges for sales and services 9,284,327$ 2,962,543$ 1,466,495$ 13,713,365$ 4,304,727$

Total operating revenues 9,284,327 2,962,543 1,466,495 13,713,365 4,304,727

Operating expenses:

Salaries and employee benefits 2,829,238 1,055,713 607,035 4,491,986 3,034,422

Supplies and materials 585,434 93,763 37,119 716,316 455,385

Contract services 330,859 827,387 48,616 1,206,862 153,769

Other services and charges 1,711,510 411,899 263,522 2,386,931 764,991

Depreciation and amortization 2,765,934 125,281 371,433 3,262,648 62,193

Total operating expenses 8,222,975 2,514,043 1,327,725 12,064,743 4,470,760

Operating income (loss) 1,061,352 448,500 138,770 1,648,622 (166,033)

Nonoperating revenues (expenses):

Investment earnings 4,758 360 586 5,704 173

Miscellaneous revenues 404,754 2,926 3,768 411,448 -

Gain (Loss) on disposition of capital assets (1,870) 96,686 - 94,816 -

Interest expense (472,438) (9,942) (9,096) (491,476) (2,129)

Total nonoperating revenues (expenses) (64,796) 90,030 (4,742) 20,492 (1,956)

Income (loss) before capital contributions

and transfers 996,556 538,530 134,028 1,669,114 (167,989)

Transfers in 67,722 106,604 - 174,326 48,090

Transfers out (601,716) (188,172) (136,940) (926,828) -

Capital grants 191,183 - - 191,183 -

Capital contributions 143,660 - - 143,660 -

Change in net position 797,405 456,962 (2,912) 1,251,455 (119,899)

Total net position - beginning 25,855,417 959,274 6,931,808 33,746,499 47,682

Total net position - ending 26,652,822$ 1,416,236$ 6,928,896$ 34,997,954$ (72,217)$

The notes to the financial statements are an integral part of this statement.

Business-type Activities - Enterprise Funds

Major FundsGovernmental

Activities - Internal Service

Funds

25

CITY OF EDGEWATER, FLORIDAStatement of Cash FlowsProprietary Funds

For the Fiscal Year Ended September 30, 2016

Water/ Sewer Utility Refuse Utility

Stormwater Utility Total

Cash flows from operating activities: Receipts-customers and users 9,232,472$ 2,945,167$ 1,453,800$ 13,631,439$ 4,310,505$ Payments-suppliers (2,508,712) (1,335,917) (463,527) (4,308,156) (4,029,698) Payments-employees (2,866,430) (1,087,850) (629,287) (4,583,567) (398,787)

Net cash provided (used) by operating activities 3,857,330 521,400 360,986 4,739,716 (117,980)

Cash flows from noncapital financing activities: Cash paid to other funds (601,716) (188,172) (136,940) (926,828) - Cash received from other funds (net) 174,218 108 - 174,326 48,090

Net cash provided (used) by noncapital financing activities (427,498) (188,064) (136,940) (752,502) 48,090

Cash flows from capital and related financing activities: Acquisition and construction of capital assets (1,057,263) (29,040) (929,426) (2,015,729) - Proceeds from sale of capital assets - 380,231 - 380,231 - Grant revenue 108,166 - - 108,166 - Interest payments on debt (515,252) (10,410) (9,177) (534,839) (2,147) Capital contributions and fees 546,544 2,926 3,768 553,238 - Proceeds from issuance of debt 10,000,000 - - 10,000,000 - Principal paid on debt (12,317,906) (115,000) (40,615) (12,473,521) (9,509)

Net cash provided (used) by capital and related financing activities (3,235,711) 228,707 (975,450) (3,982,454) (11,656)

Cash flows from investing activities: Interest on investments 4,758 360 586 5,704 173 Sale of investment securities 1,649 - - 1,649 -

Net cash provided by investing activities 6,407 360 586 7,353 173

Net increase (decrease) in cash and cash equivalents 200,528 562,403 (750,818) 12,113 (81,373) Beginning cash and cash equivalents 6,544,421 131,341 1,478,118 8,153,880 217,441 Ending cash and cash equivalents 6,744,949$ 693,744$ 727,300$ 8,165,993$ 136,068$

Reconciliation of operating income (loss) to net cash provided by(used) by operating activities:

Operating income 1,061,352$ 448,500$ 138,770$ 1,648,622$ (166,033)$

Adjustments to reconcile operating income (loss) to net cash provided (used) by operating activities:

Depreciation and amortization 2,765,934 125,281 371,433 3,262,648 62,194 (Increase) decrease in assets:

Accounts receivable (51,855) (17,376) (12,695) (81,926) 5,778 Inventories - - - - 4,195 Prepaid items (4,607) (26) (26) (4,659) 514

Increase (decrease) in liabilities:Accounts payable and accrued expenses 156,500 (2,842) (114,244) 39,414 (27,698) Compensated absences 8,306 (11,974) (20,119) (23,787) (355) Net pension liability (67,526) (28,112) (6,747) (102,385) - OPEB obligation 22,028 7,949 4,614 34,591 3,425 Customer deposits (32,802) - - (32,802) -

Total adjustments 2,795,978 72,900 222,216 3,091,094 48,053

Net cash provided (used) by operating activities 3,857,330$ 521,400$ 360,986$ 4,739,716$ (117,980)$

Classified As:Cash and cash equivalents 5,291,714$ 693,744$ 727,300$ 6,712,758$ 136,068$ Restricted cash and cash equivalents 1,453,235 - - 1,453,235 -

Total 6,744,949$ 693,744$ 727,300$ 8,165,993$ 136,068$

The notes to the financial statements are an integral part of this statement.

Business-type Activities - Enterprise Funds

Major FundsGovernmental

Activities - Internal Service

Funds

26

CITY OF EDGEWATER, FLORIDAStatement of Fiduciary Net PositionFiduciary FundsSeptember 30, 2016

Pension

Trust Funds

ASSETS

Accrued interest 96,338$

Money market funds 1,237,453

Bonds

US Treasury notes 982,059

GNMA/FMNA 2,300,813

Municipal bonds 317,534

Corporate bonds 7,824,533

Equities 8,073,264

Mutual fund - equities 11,143,695

Total assets 31,975,689

LIABILITIES

Accounts payable 27,471

Unearned contributions 33,575

Total liabilities 61,046

NET POSITION

Held in trust for pension benefits 31,914,643$

The notes to the financial statements are an integral part of this statement.

27

CITY OF EDGEWATER, FLORIDAStatement of Changes in Fiduciary Net PositionPension Trust FundsFor the Fiscal Year Ended September 30, 2016

Pension Trust

Funds

ADDITIONS

Contributions:

Employer 1,896,397$ Employee 247,526

State of Florida 277,771

Total contributions 2,421,694

Investment earnings: Interest and dividends 1,020,252 Net increase in the fair value of investments 1,797,081

Total investment earnings 2,817,333

Less investment expenses (157,945) Net investment earnings 2,659,388

Total Additions 5,081,082

DEDUCTIONS

Pension benefits 2,650,643

Administrative expenses 168,311 Total deductions 2,818,954 Change in net position 2,262,128

Net position - beginning of year 29,652,515

Net position - end of year 31,914,643$

The notes to the financial statements are an integral part of this statement.

28

City of Edgewater, Florida Notes to the Financial Statements September 30, 2016

I. Summary of Significant Accounting Policies The accompanying financial statements present the financial position, changes in financial position and cash flows of the applicable fund types governed by the City Council of the City of Edgewater, Florida ("the City") and have been prepared in conformity with accounting principles generally accepted in the United States of America (GAAP) as applied to governmental units. The Governmental Accounting Standards Board (GASB) is the accepted standard-setting body for establishing governmental accounting and financial reporting principles. The most significant of the City's accounting policies are described below.

A. Reporting Entity: The City of Edgewater was originally incorporated under general law on October 20, 1924. The City became the City of Edgewater and incorporated in 1951 as a political subdivision of the State of Florida and a municipal corporation with a five-member Council, including a Mayor and Vice-Mayor. The registered voters of the City of Edgewater elect the Mayor and Council. The Council appoints the City Manager, who in turn performs as the administrator of the everyday operations of the City. The City provides a full range of municipal services as directed by the City Charter including general government, public safety, public improvements, planning and zoning, water and sewer service, refuse collection, a recycling program, a stormwater management utility program, and related general and administrative services to 21,280 residents. In evaluating how to define the government, for financial reporting purposes, the City has considered all potential component units. The definition of the reporting entity is based primarily on the notion of financial accountability. A primary government is financially accountable for the organizations that make up its legal entity. It is also financially accountable for legally separate organizations if its officials appoint a voting majority of an organization’s governing body, and either it is able to impose its will on that organization or there is a potential for the organization to provide specific financial benefits to, or to impose specific financial burdens on, the primary government. A primary government may also be financially accountable for governmental organizations that are fiscally dependent on it. A primary government has the ability to impose its will on an organization if it can significantly influence the programs, projects or activities of, or the level of services performed or provided by, the organization. A financial benefit or burden relationship exists if the primary government (a) is entitled to the organizations’ resources; (b) is legally obligated or has otherwise assumed the obligation to finance the deficits of, or provide financial support to, the organization; or (c) is obligated in some manner for the debt of the organization. In applying the above criteria, management has determined there is one component unit to be included within the reporting entity. The City of Edgewater, Florida, Edgewater Community Redevelopment Agency (CRA) was created by Ordinance No. 2015-O-04 to account for the receipt and expenditure of property tax revenues from the tax increment financing district to support City redevelopment in the designated community redevelopment area. The CRA's focus is mitigation or correction of infrastructure and utilities deficiencies, revitalization of the Ridgewood Avenue (US-1) corridor, various transportation and urban design improvements, and pedestrian safety issues. Although legally separate the City Council declared itself to be the CRA Board, and provided for the appointment of two additional members. Since the City is financially accountable for the activities of the CRA, its governing board is the same, and its relationship to the City is significant, its financial activities are reported on a blended basis as if it were part of the primary government as a major special revenue fund. Activity began in the CRA Fund during the fiscal year ended September 30, 2016.

29

City of Edgewater, Florida Notes to the Financial Statements September 30, 2016