changing what’s possible home improvement …

TRANSCRIPT

184-242-00 | REV. AUGUST 2021

CHANGING WHAT’S POSSIBLE

HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

Great Customers Aren’t Born, They’re Made

NOTE: This is for INTERNAL USE ONLY and is not to be shared with consumers for any reason.

Table Of Contents

Introduction ................................................................... 5

Payment Discussions ...................................................... 9

Applying And Transacting .............................................. 21

Resources And Tools ..................................................... 29

Pages with a symbol contain important compliance information.

Throughout this document we have included images of some Synchrony materials and web pages. These images are only used for representations, not content, therefore they are marked SAMPLE and the actual versions may be slightly different from what you see in the guide.

HOME IMPROVEMENT ORIENTATION GUIDE Credit extended by Synchrony • www.synchronybusiness.com

This page intentionally left blank.

INTRODUCTIONOverview and Benefits!

5HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

6

INTRODUCTION Synchrony’s financing options are designed for you and your customers.

HOME IMPROVEMENT ORIENTATION GUIDE Credit extended by Synchrony • www.synchronybusiness.com

This Is The First Step To Offering Financing Options For Your Customers.• Review “What you need to know” about offering financing fairly and compliantly.

• Show how to comply with the applicable Federal and State regulations.

• Get you set up and ready to introduce payment options to your team and customers as part of your sales process.

• Get you and your team ready to introduce payment options to your customers as part of your sales process.

• Demonstrate how to achieve your business goals by offering a Synchrony Private Label Credit Card.

• Show how payment options can help your customers get what they really want or need.

Overview

*Subject to credit approval.

**You must validate 2 forms of ID on the Credit Application for non-recourse. Subject to any chargeback rights in the Synchrony Merchant Agreement and compliance with Synchrony Operating Procedures.”

Customer Benefits

• Get more work done, with the products they really want, when they want it.*

• Purchase a better product than they can get with on-hand cash

• A simple application process and fast credit decision

Your Benefits

• Get more sales, from more customers, with more loyalty

• Plus…With your Synchrony program, you get payments in just 24-48 hours, and purchases are non-recourse.**

7HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

Your customers have access to special payment options promotions for initial purchase and repeat purchases

Predictable budgeting plans

Private Label Credit Card with your business name on it

Unsecured revolving credit limit*• Credit limits are based on consumer credit quality and estimated sale amount. There is no minimum or maximum credit limit.• Open credit limit for repeat purchases via a Private Label Credit Card• One of the lowest payment options in the industry

Simple application and funding process• Instant credit decisions• Funding generally occurs within 24-48 hours of job completion and submission for payment

Important Notes:• Primary applicant must own and reside at the property to be improved• Synchrony will finance the installation of approved products for mobile home owners (owner occupied), including those in mobile

home parks. Rental properties of any type are prohibited• A joint-applicant should sign the Credit Application only if he/she wishes to be obligated to repay the debt. It is the customer’s

choice whether or not to have a joint-applicant• One account per property (household) in a 60-day period• Synchrony does not allow split ticket financing - i.e., processing a single purchase between two new separate credit limits or

two separate lenders• Using existing credit cards, lines of credit or personal loans is acceptable. Dealers cannot set up separate financing with multiple

lenders for the same project• Always verify and document two forms of ID for all applicants. ID verification is not required if the application is completed on the

consumer’s personal device.• For purchases using an existing Synchrony Private Label Credit Card account, if processing by paper always call Synchrony for an

authorization to ensure the customer has enough available credit to complete the purchase• A one-time $29 Account Activation Fee will be charged at the time the first purchase posts to the cardholder’s account• At no cost to the Merchant or customer, cardholders may change their promotional option for up to 60 days post-funding

through Merchant request *Subject to credit approval. Proof of income may apply on loans over $35,000, depending on program. See page 24 for details.

Program Basics

8HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

Two Primary Methods To Apply and Process

Synchrony Transact is our preferred application process. An online digital platform that makes the financing process faster and easier for both the contractor and the consumer.

Synchrony Transact the following:

Payment Estimator Review estimated monthly payments with customers, and view promotional financing options.

Apply for Credit Help customers apply for a Private Label Credit Card on your tablet or smart phone.

Sales Slip Complete transaction details.

Transactions Go to Business Center for one click funding.

Our paper process can be used when an internet connection is not available or for those companies who do not use technology in the home.

Call in/Paper process the following:

Promotional Offers Paper Silent Sales document let’s you review promotional options with the customers.

Apply for Credit Customers complete a paper application and you call Synchrony for processing.

Sales Slip Complete a paper sales slip with the transaction details. You retain the copy the customer signs, and make sure the customer is provided with a copy as well.

Transactions Application and Sales Slip are returned to the office. The sales slip is faxed to Synchrony for funding.

OR

Please refer to the “Synchrony Transact Overview and User Guide” for additional details or visit MyToolbox at https://toolbox.mysynchrony.com/transact.

or Call in Paper Process

PAYMENT DISCUSSIONSThey’re easy with Synchrony

9HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

10HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

5 Things to Know About Deferred Interest

These are the key concepts about deferred interest promotional financing. All employees should understand and be able to share these 5 things with customers:

Deferred interest promotional financing is just as it sounds: when a customer uses this type of financing on a purchase, interest accrues (adds up) from the purchase date but is deferred to the end of the promotion period (ex. 12 months).

Deferred interest promotional financing DOES NOT mean deferred payments.

With deferred interest promotional financing, a customer must make minimum monthly payments.

The required minimum payment, shown on a customer’s billing statement, will typically NOT pay off the full purchase within the promo period. A customer can choose to pay more every month to pay off the balance within the promo period (ex. 12 months) and avoid paying interest.

If the customer doesn’t pay off the purchase in full, by the end of the agreed-to promo period (ex. 12 months), then the interest that has accrued from the date of purchase WILL be added to the remaining balance.

1

2

3

4

5

11HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

What to Say VS What NOT to Say About Deferred Interest Promotional Financing

What deferred interest IS:

Deferred interest promotional financing is just as it sounds: when a patient/client uses this type of financing on their purchase, interest accrues (adds up) from the purchase date but is deferred to the end of the promotion.

This type of financing requires minimum monthly payments that start right away. The payments are not deferred.

The required minimum monthly payments typically will NOT pay off the full purchase, within the promo period. Although patient/client must make minimum monthly payments, they can choose to pay more every month to pay the promotional balance within the promo period (ex. 12 months) in order to avoid paying interest.

A type of promotional financing that allows a patient/client to pay no interest ONLY IF they pay off their full purchase, within the agreed-to promo period (ex. 12 months).

If the patient/client does not pay off the purchase in full, by the end of the agreed-to promo period (ex. 12 months), then the interest that has accrued from the date of purchase WILL be added to the remaining balance.

What deferred interest is NOT:

“Deferred payments” financing Why: A patient/client must make minimum monthly payments during the promo period (ex. 12 months).

“No interest” financing Why: Interest will be charged from the purchase date if the promo balance is not paid in full within the promo period (ex. 12 months).

“Buy now, pay later” financing Why: Buy now, pay later is a way to describe short-term fixed payment loans.

“No payments” financing Why: Minimum monthly payments are required and typically will NOT pay off the full purchase, within the promo period. A patient/client could choose to make suggested equal monthly payments, which are larger, to help pay off the balance during the promo period (ex. 12 months).

“Reduced APR/lower interest” financing Why: The patient/client pays NO interest IF they pay off their promotional purchase by the end of the promo period.

12HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

How to Direct a Customer to More Information About Deferred Interest

The Synchrony credit application and the terms and conditions have important details about the deferred interest promotional financing.

the store has a customer brochure that covers credit and financing:

“If you want to know more about how deferred interest promotional financing works, I have a brochure for you that explains it in detail…”

the store has a poster/sign with a QR code to access deferred interest promotional financing content:

“If you want to know more about how deferred interest promotional financing works, just bring your phone to this poster, and aim the camera at this QR code. You’ll get a link to more information.”

the store has signage or posters from Synchrony that shows the disclosures for deferred interest promotional financing:

“If you want to know more about how deferred interest promotional financing works, you can check out this sign for more details…”

the store doesn’t have any of these, employees can direct customers to MySynchrony.com (or another appropriate website):

“If you need more information about deferred interest promotional financing, here is a website with details.”

IF

IF

IF

IF

NOTE: It is important that customers have details on their deferred interest promotional financing before you complete the transaction, and they must agree to the terms. Provide the terms to them in writing (brochure or other material) or electronically (partner device/pin pad or customer device/phone.)

You may also direct customers to the Synchrony deferred interest online portal at https://www.mysynchrony.com/deferred-interest.html

13HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

Payment Estimators:

Details About Deferred InterestIf your store uses the digital MySynchrony payment estimator tool, the customer can get detailed information about deferred interest promotional financing.

https://www.mysynchrony.com/payment-calculator.html

Please note: Associates should only use payment estimators/tools provided by Synchrony.

The monthly payments shown on payment estimators assume there are no other balances on the account.

If customers have questions about their balance(s), they should contact Synchrony customer service.

14HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

Supervising Employees:

Offering Deferred Interest Promotional Financing to CustomersIf your employees share information about deferred interest financing with customers, it’s important they do it accurately. As a manager, you can help employees feel confident about the 5 things to know about deferred interest. Encourage them not to try to answer additional questions, but refer customers to other materials, like signage or brochures. This checklist can help you observe and track employee performance, and coach as needed.

If the employee shared information on deferred interest promotional financing, did they correctly mention any or all of these points:

You have deferred interest promotional financing available.

Deferred interest promotional financing is just as it sounds: when a customer uses this type of financing on a purchase, interest accrues (adds up) from the purchase date but is deferred to the end of the promotion period (ex. 12 months).

Deferred interest promotional financing DOES NOT mean deferred payments.

With deferred interest promotional financing, a customer must make minimum monthly payments

The required minimum monthly payments typically will NOT pay off the full purchase, within the promo period. Although customers must make minimum monthly payments, they can choose to pay more every month to pay the promotional balance within the promo period (ex. 12 months) in order to avoid paying interest.

If the customer doesn’t pay off the purchase in full, by the end of the agreed-to promo period (ex. 12 months), then the interest that has accrued from the date of purchase WILL be added to the remaining balance.

Did the employee provide information without errors, misleading information or going “off script?”

If the employee gave details about the deferred interest promotional financing, did they do so before they completed the transaction (ex. in writing or on a pin pad); and did the customer agree to the terms?

Managers: If you have signage in your store that mentions deferred interest, ensure it is correct and up-to-date.

15HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

Additional Tips

This helpful graphic explains the two paths a customer could take after making a purchase with deferred interest promotional financing. It can help explain how deferred interest works.

MORE TIPS:• If a store associate is asked a question they can’t

confidently and correctly answer about deferred interest promotional financing, have a process in place. For example, they should point to in-store signage, a brochure (if applicable), or details on the credit application.

• Encourage store associates to “stick to the script” around deferred interest promotional financing. Use the information in 5 things to know. Don’t introduce the possibility of giving a customer incorrect or confusing information by getting creative in the conversation.

• Ensure store managers and associates have had recent training on deferred interest promotional financing. Utilize your applicable learning sites and other training tools.

• If you need more information on deferred interest promotional financing, contact your Synchrony representative.

HOW DEFERRED INTEREST WORKS

After a customer makes a purchase using deferred interest promotional financing, they either:

MAKE PAYMENTS MAKE PAYMENTS

PAY OFF WITHIN PROMO PERIOD

DON’T PAY OFF WITHIN PROMO PERIOD

PAY ZERO INTEREST

$0 BALANCE

PAY PURCHASEBALANCE

+ALL ACCRUED

INTEREST

A B-OR-

+

=

+

=

16HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

Knowledge Check Questions

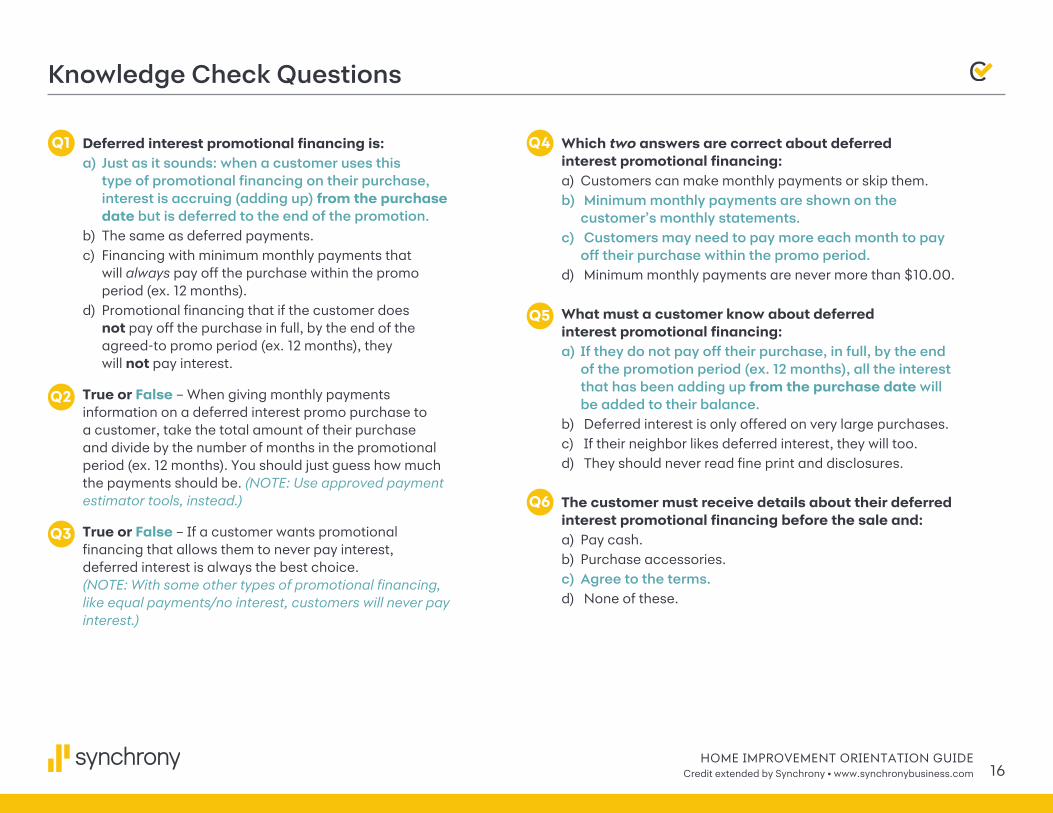

Deferred interest promotional financing is:a) Just as it sounds: when a customer uses this

type of promotional financing on their purchase, interest is accruing (adding up) from the purchase date but is deferred to the end of the promotion.

b) The same as deferred payments.c) Financing with minimum monthly payments that

will always pay off the purchase within the promo period (ex. 12 months).

d) Promotional financing that if the customer does not pay off the purchase in full, by the end of the agreed-to promo period (ex. 12 months), they will not pay interest.

True or False – When giving monthly payments information on a deferred interest promo purchase to a customer, take the total amount of their purchase and divide by the number of months in the promotional period (ex. 12 months). You should just guess how much the payments should be. (NOTE: Use approved payment estimator tools, instead.)

True or False – If a customer wants promotional financing that allows them to never pay interest, deferred interest is always the best choice. (NOTE: With some other types of promotional financing, like equal payments/no interest, customers will never pay interest.)

Which two answers are correct about deferred interest promotional financing:a) Customers can make monthly payments or skip them.b) Minimum monthly payments are shown on the

customer’s monthly statements.c) Customers may need to pay more each month to pay

off their purchase within the promo period.d) Minimum monthly payments are never more than $10.00.

What must a customer know about deferred interest promotional financing:a) If they do not pay off their purchase, in full, by the end

of the promotion period (ex. 12 months), all the interest that has been adding up from the purchase date will be added to their balance.

b) Deferred interest is only offered on very large purchases.c) If their neighbor likes deferred interest, they will too.d) They should never read fine print and disclosures.

The customer must receive details about their deferred interest promotional financing before the sale and:a) Pay cash.b) Purchase accessories.c) Agree to the terms.d) None of these.

Q1 Q4

Q2

Q5

Q3

Q6

17HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

Payment Options Explained*

No Interest:• Often referred to as “Equal Pay”

• No interest is charged on the promotional purchase, regardless of the length of promotion

• Monthly payments on promotional purchase are the same every month**

Reduced Interest:• Often referred to as “Fixed Pay”

• A reduced interest rate is charged on the promotional purchase, regardless of the length of promotion

• Monthly payments on promotional purchase are the same every month**

For each promotional type, minimum monthly payments are calculated by multiplying the loan amount by the Payment Factor and are rounded up to the next whole dollar.

For example: $5,000 x 1.25% Payment Factor = $62.50 rounded up to $63.00

*Cost should be incorporated into Merchant’s General & Administrative expenses and any additional credit related surcharges or fees charged by Merchant are prohibited. Cardholder may be charged fees for late payments.

** A one-time $29 Account Activation Fee will be charged at the time the first purchase posts to the cardholder’s account.

Typical Customer Conversation Steps

Mention your financing promotions

and offerings when setting the appointment and early in the initial

sales consultation

1 2 3

Break purchases down into

monthly payments when the customer is

considering the scope of the project

Present your selected financing

options, allowing the customer to choose the promotion that

works best for them

18HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

Guiding Principles

Be Clear and Transparent

• Use Synchrony training materials

• Utilize compliant program materials

• Let the customer choose the promotion that works best for them

Present financing…

• To every customer

• Every time

• Early in the sales process

19HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

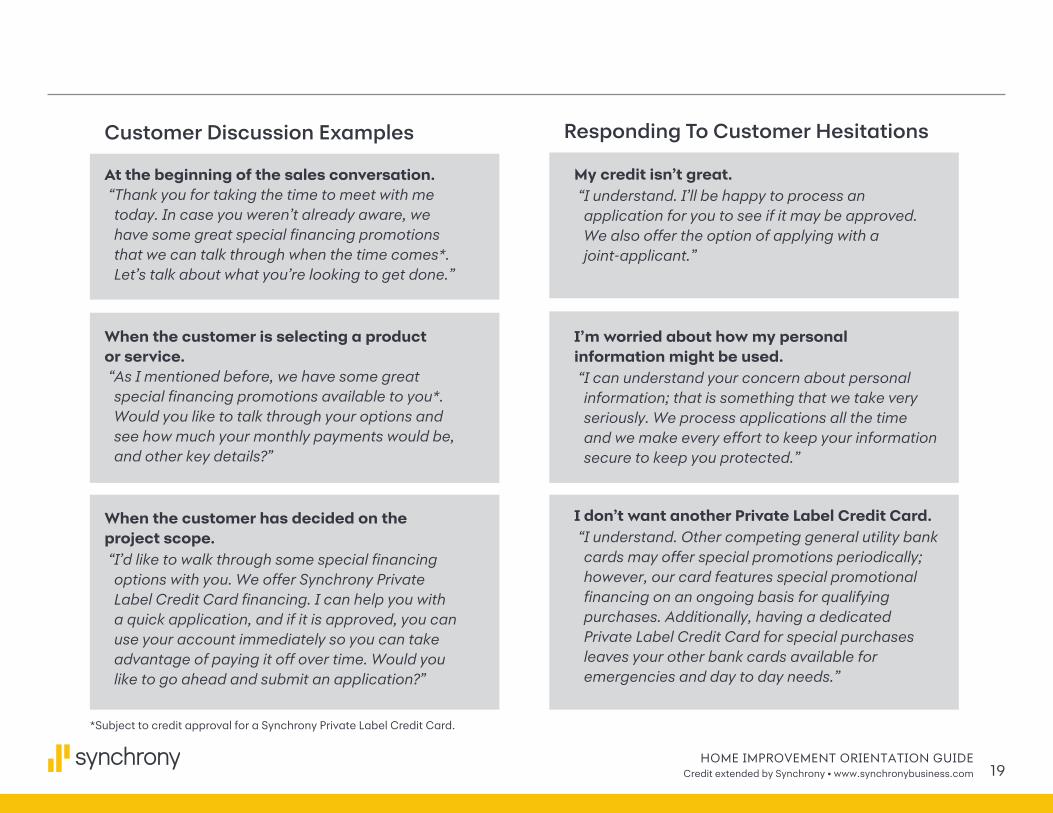

Customer Discussion Examples

At the beginning of the sales conversation.“Thank you for taking the time to meet with me today. In case you weren’t already aware, we have some great special financing promotions that we can talk through when the time comes*. Let’s talk about what you’re looking to get done.”

When the customer is selecting a product or service.“As I mentioned before, we have some great special financing promotions available to you*. Would you like to talk through your options and see how much your monthly payments would be, and other key details?”

When the customer has decided on the project scope.“I’d like to walk through some special financing options with you. We offer Synchrony Private Label Credit Card financing. I can help you with a quick application, and if it is approved, you can use your account immediately so you can take advantage of paying it off over time. Would you like to go ahead and submit an application?”

Responding To Customer Hesitations

My credit isn’t great.“I understand. I’ll be happy to process an application for you to see if it may be approved. We also offer the option of applying with a joint-applicant.”

I’m worried about how my personal information might be used.“I can understand your concern about personal information; that is something that we take very seriously. We process applications all the time and we make every effort to keep your information secure to keep you protected.”

I don’t want another Private Label Credit Card.“I understand. Other competing general utility bank cards may offer special promotions periodically; however, our card features special promotional financing on an ongoing basis for qualifying purchases. Additionally, having a dedicated Private Label Credit Card for special purchases leaves your other bank cards available for emergencies and day to day needs.”

*Subject to credit approval for a Synchrony Private Label Credit Card.

This page intentionally left blank.

APPLYING AND TRANSACTINGHere are the Nuts and Bolts

21HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

1. On the Synchrony Transact homepage, select the “Apply for Credit” button.

2. In the window that opens, select the relevant program from the dropdown menu (if applicable).

3. Ask the consumer if this will be an Individual or Joint application, and select the appropriate button.

Be sure to hand the consumer the paper version of the Terms & Conditions (T&C).

You must give theconsumer a paperversion of the T&C.

Many contractors only have one

program/ merchant number. For those

with multiple programs, choosing

the correct one is important to ensure relevant promotions are displayed and

available to offer theconsumer.

Start The Application

22HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

Synchrony Transact-Apply For Credit

12

3

23HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

The next step is to verify the consumer’s identity by reviewing two pieces of identification.

1. Verify primary and secondary ID with all applicants. Common primary and secondary ID types are

pre-selected as default options. Other options are also available.

2. If necessary, use the dropdown menu to change the primary or secondary ID type.

3. Enter the expiration date (month and year)and issue for the ID.

4. Click the “Continue· button to proceed.

• If necessary, reassure the consumer that you will be noting the type of ID and issuer/ expiration details, but NOT capturing personally identifiable information, such as a Private Label Credit Card or license numbers.

• Ensure Primary Identification is a valid, non-expired government-issued ID.

Enter ID Information

Synchrony Transact-Apply For Credit

1

3

4

2

Application Outcomes

24HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

Approved

“I’m happy to tell you that your application has been approved.”

Pending

“The application came back ‘Pending,’ which simply means the bank needs to clarify some information. Let’s give them a call to see what they need.”

Note: You must call 888-222-2176 on a pending application within 24 hours or it will be automatically denied.

Declined

“Unfortunately, Synchrony wasn’t able to extend credit to you at this time. You will receive a letter within 7-10 business days’. indicating the specific reasons for the decision.”

• If approved the cardholder can immediately use (in most cases) the account and can expect to receive a Private Label Credit Card in the mail in 7-10 business days for future purchases.

• Proof of income may apply on loans over $35,000. Contact Synchrony for additional instructions.

Declined ApplicationsHow you handle a declined Credit Application makes a difference.

Be positive. Say, “Let’s see what we can do.”

1. Double-check the Credit Application detail for accuracy.

2. Present the option of reapplying with a joint applicant.

3. Suggest other payment options, such as cash, check, or Private Label Credit Card.

4. Remind them that they will receive a letter within 7-10 business days’ indicating the specific reasons for the decision.

Transparency Principles: Compliance Requirements

25HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

1. You will ensure that training on how to offer, process and transact with the Synchrony Financing Program is integrated into your existing associate training program. Helpful training materials including videos, self-paced courses and pre-recorded webinars can be found online at Synchrony’s Learning Center: learn.synchronybusiness.com

2. Your customers must receive the Credit Card Agreement in writing and have the opportunity to review it and other disclosures in the application brochure before signing an application.

3. You must retain each applicant’s signature page for no less than 25 months from the date of the application. Failure to keep and, upon request, produce the signature page to Synchrony may expose your business to an automatic chargeback upon consumer dispute.

4. Fees may not be charged to consumers for applying for credit or for using their Synchrony account to finance purchases.

These fees have been called Administration Fees, Documentation Fees or other generic terms. All are prohibited by your Card Acceptance Agreement with Synchrony and you will be responsible for refunding customers accordingly.

5. You or your staff must inform all Synchrony Financing Program applicants of the following:

• The Synchrony Financing Program is a credit card and is NOT an in-house credit program. The Synchrony Financing Program is NOT an interest-free credit card.

• Cardholders should be provided with information about the different special financing options available to them and how they work before requested to choose which one to use for

Synchrony Bank promotes full transparency and disclosure to all applicants for its credit card program (the “Synchrony Financing Program”). To assure that applicants are aware of several key attributes of the Synchrony Financing Program, you hereby agree as follows:

their specific purchase. It is especially important that cardholders understand the basic features of No Interest, Reduced Interest and Deferred Interest/No Interest if Paid in Full options, if all these types of promotions are being offered. The key concepts include:

• The length of the promotion

• Whether the promotion expires and if so what happens upon expiration

• Required payments during the promotional term• For Deferred Interest promotions, deferred interest accrues on

the outstanding balance during the promotional period from the date of the transaction. Interest charges can be avoided ONLY IF the promotional balance is paid off prior to the end of the promotional period.

6. You must complete the document that provides the promotional terms to the customer. These may be referred to as sales slips, sales receipts or Optional Financing Plan (OFP) forms (not required for online sale transactions – these will auto print through Business Center).

7. You will advise customers of any policy regarding returns/refunds.

8. These program guidelines are designed to provide transparency for cardholders. Synchrony reserves the right to monitor your adherence to these and other Synchrony Financing Program policies subject to the consequences defined in your Card Acceptance Agreement.

Transparency Principles: Compliance Requirements (Cont’d)

26HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

Fair Lending Principles to Know Credit must be offered to all applicants fairly and consistently. Failure to do so may result in allegations of discrimination, potential violations of federal or state fair lending laws, litigation or reputational risk. All customers should be encouraged to apply for credit without regard to race, color, religion, national origin, sex, marital status, familial status, age, disability, receipt of income (in whole or in part) from public assistance programs, or an applicant’s good faith exercise of a right under the Consumer Credit Protection Act. In addition, credit-related activities must be conducted in a way that is not considered unfair, deceptive, or abusive from the customer’s perspective. Unfair activities are those that may cause unavoidable “substantial injury” (typically financial harm) to customers. Deceptive activities could include statements or omissions that mislead customers or influence their decision to buy or use a product or service. Abusive practices interfere with the customers’ ability to understand the terms and conditions of a product or service; or which take advantage of the customers’ lack of understanding or inability to protect their interests.

Clear and Accurate Communications Your advertising, signage, and conversations with customers should help them understand and make informed choices regarding your products and available financing options. Disclosures should clearly and accurately describe the terms, conditions, and any limitations associated with the purchase and the Synchrony relationship the customer is establishing.

Taking and Processing Applications All customers should be encouraged to complete and submit applications for credit. Do not discourage anyone from submitting an application, either through oral statements, body language, delays or discourtesy. Also, make certain that employees provide a consistent level of service in responding to questions from customers about the availability of credit and/or completing the application.

Completing the Credit Application The credit application and Credit Card Agreement must be provided to customers before they apply. It is the customer’s choice to have a joint applicant , but it is not required that a joint applicant be a spouse. Alimony, child support or separate maintenance payments do not need to be disclosed unless the customer wants this income to be considered.

Pricing and Fees No fees related to the application process or Synchrony financing are allowed, and the pricing of credit approved for customers cannot be changed from what Synchrony approved and communicated. The availability of promotions must be consistently shared with customers when they apply for credit.

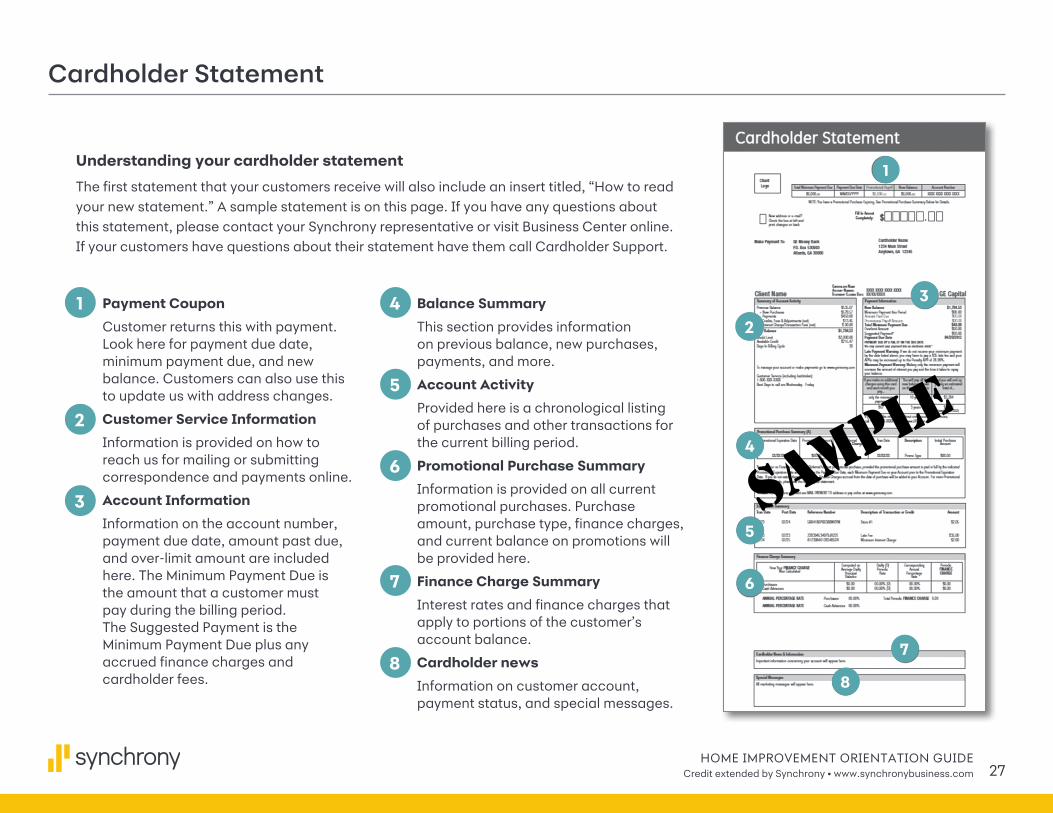

Cardholder Statement

27HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

Understanding your cardholder statement

The first statement that your customers receive will also include an insert titled, “How to read your new statement.” A sample statement is on this page. If you have any questions about this statement, please contact your Synchrony representative or visit Business Center online. If your customers have questions about their statement have them call Cardholder Support.

Payment Coupon

Customer returns this with payment. Look here for payment due date, minimum payment due, and new balance. Customers can also use this to update us with address changes.

Customer Service Information

Information is provided on how to reach us for mailing or submitting correspondence and payments online.

Account Information

Information on the account number, payment due date, amount past due, and over-limit amount are included here. The Minimum Payment Due is the amount that a customer must pay during the billing period. The Suggested Payment is the Minimum Payment Due plus any accrued finance charges and cardholder fees.

4. Balance Summary

This section provides information on previous balance, new purchases, payments, and more.

5. Account Activity

Provided here is a chronological listing of purchases and other transactions for the current billing period.

6. Promotional Purchase Summary

Information is provided on all current promotional purchases. Purchase amount, purchase type, finance charges, and current balance on promotions will be provided here.

7. Finance Charge Summary

Interest rates and finance charges that apply to portions of the customer’s account balance.

8. Cardholder news

Information on customer account, payment status, and special messages.

1

1 4

5

6

7

8

2

3

2

3

4

5

6

7

8

This page intentionally left blank.

RESOURCES AND TOOLS Important Websites

29HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

Business Center

bc.syf.com

• Manage your Synchrony account

• Pull business and funding reports

• Order signage and forms

• Print current program documents

Toolbox

toolbox.mysynchrony.com

• Watch webinars about selling with financing

• Access printable sales tools to use during financing conversations

• Synchrony Transact Overview and User Guide and other support tools

Learning Center

learn.synchronybusiness.com

• Take short online courses showing how to use financing

• Watch videos of best practices by other businesses

• View on-demand business-building webinars

Your Online Resources

30HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

31HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

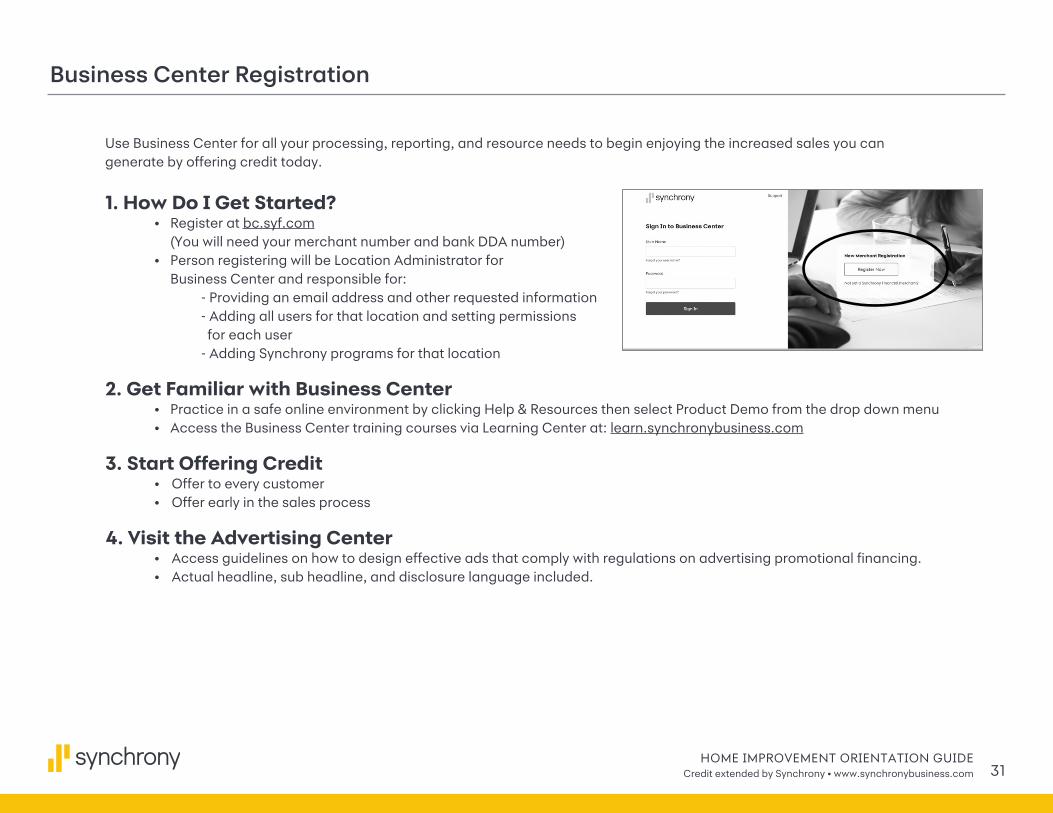

Business Center Registration

Use Business Center for all your processing, reporting, and resource needs to begin enjoying the increased sales you can generate by offering credit today.

1. How Do I Get Started? • Register at bc.syf.com (You will need your merchant number and bank DDA number) • Person registering will be Location Administrator for Business Center and responsible for: - Providing an email address and other requested information - Adding all users for that location and setting permissions for each user - Adding Synchrony programs for that location

2. Get Familiar with Business Center • Practice in a safe online environment by clicking Help & Resources then select Product Demo from the drop down menu • Access the Business Center training courses via Learning Center at: learn.synchronybusiness.com

3. Start Offering Credit • Offer to every customer • Offer early in the sales process

4. Visit the Advertising Center • Access guidelines on how to design effective ads that comply with regulations on advertising promotional financing. • Actual headline, sub headline, and disclosure language included.

Merchant Support1-800-222-2176

• Assistance with submitting applications

• Obtain names on an account

• Check available credit amount

• Request a credit limit increase

• Technical assistance with Business Center

• Obtain Authorization Code

Cardholder Support 800-250-5411

• Account questions

• Credit Limit Increases

• Address updates

On-Demand Training

• Learning Center: learn.synchronybusiness.com

• Call 866-885-2637

Mon-Fri 8:00am EST to 8:00pm EST

Please Note: Cardholder inquiry representatives are authorized to speak only with cardholders about their account.

Help & Support

32HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com

• How financing can help you achieve your business’s priorities, while helping your customers get what they really want or need.

• How to complete Applications and Sales Slips.

• How promotional financing works, including Deferred Interest, No Interest and Reduced Interest promotions.

• How and when to discuss financing with every customer clearly.

• How to get additional training for new and existing team members.

• Important rules for fair and compliant business practices when offering financing.

This page intentionally left blank.

This page intentionally left blank.

CHANGING WHAT’S POSSIBLE

184-242-00 | REV. AUGUST 2021HOME IMPROVEMENT ORIENTATION GUIDE

Credit extended by Synchrony • www.synchronybusiness.com